Pike Robert, Neal Bill. Corporate finance and investment: decisions and strategy

Подождите немного. Документ загружается.

.

Chapter 2 The financial environment 55

The share price, of course, is based on investors’ expectations of future profits. A

high P:E ratio indicates that investors expect future profits to grow – the higher the

P:E, the greater the profit growth expectation.

Dividend yield

In the UK, income tax at 10% is deducted at source, so the calculation should

therefore be based on the gross dividend.

■ Interpretation of the accounts and ratios

The financial manager or investor needs to put together all the clues suggested by ratio

analysis and reading the accounts to gain insights into the financial position, perform-

ance and prospects of the company. This will probably involve looking at the trend of

financial indicators, not simply comparison with the previous year, together with com-

parison with industry and competitor data. It certainly requires a reasonable grasp of

the business, its objectives and strategies. Table 2.4 offers a brief report to senior man-

agement of Foto-U by the finance manager on the company’s published accounts.

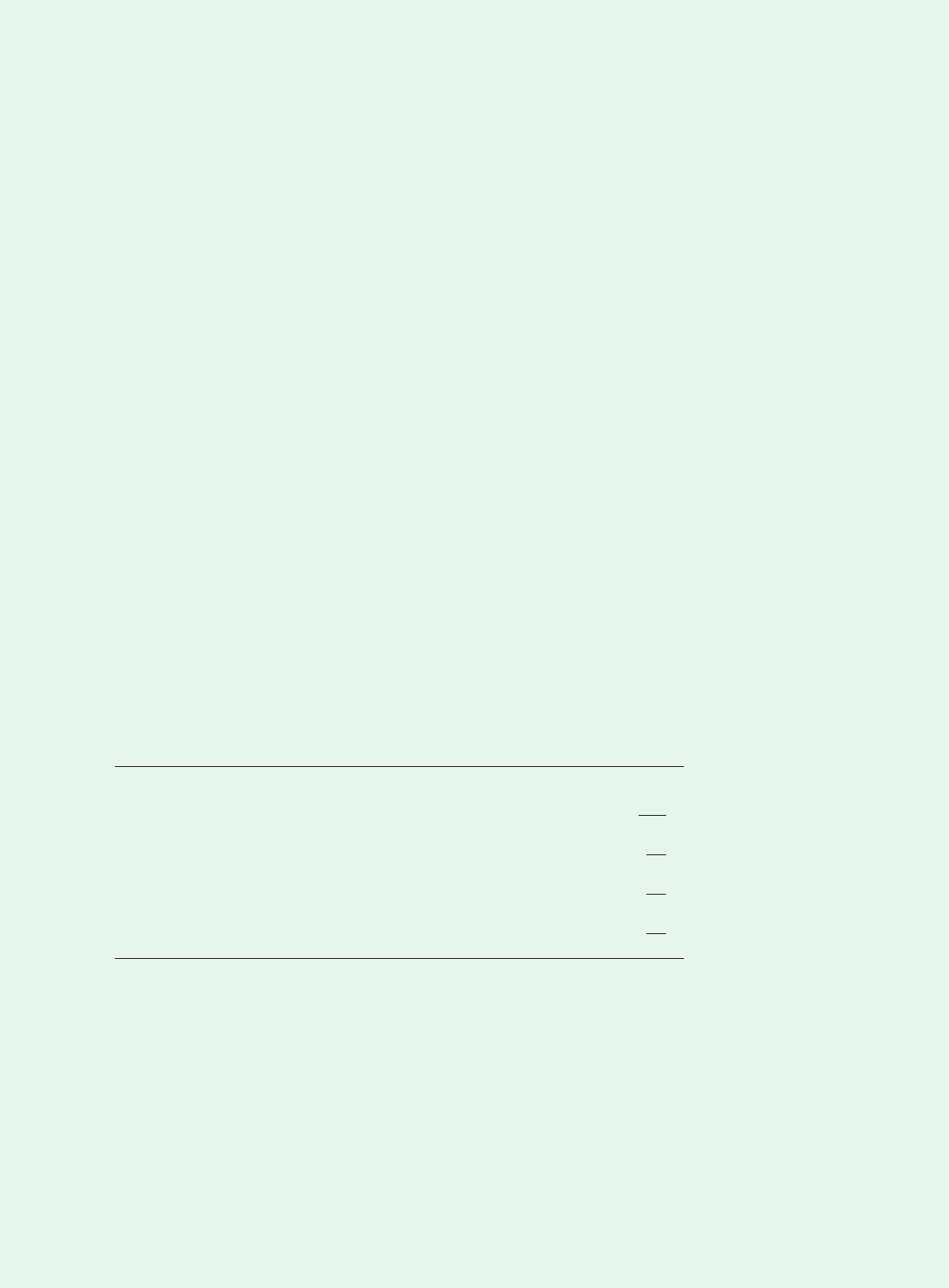

2.9%

13% last year2

Dividend per share 1p2

Share price 1p2

100

3.5

120

100

Table 2.4

Foto-U annual

corporate performance

report

To: Senior Management of Foto-U

From: Finance Manager

Subject: Annual corporate performance

30 April 2006

I have reviewed the published accounts for the past year to establish how successful

Foto-U was in financial terms.

Profitability. The Return on Capital Employed has improved over the year from 10.6%

to 16%. This is a significant improvement and well above the risk-free return we

would expect from investing in say building society deposits, but we need also to

compare the return against that achieved by our competitors. ROCE is a combination

of two subsidiary ratios – net profit margin and asset turnover:

ROCE Net profit margin Asset turnover

2005 10.6% 5.3% 2 times

2006 15.9% 11% 1.45 times

Both the gross and net profit margins have improved significantly as a result of the

£10 million growth in sales over the year without any increase in costs. However, this

growth has come at the expense of a poorer utilisation of our assets, as reflected in

the significant decline in asset turnover. This is mainly attributable to a major capital

expenditure programme during the year, the benefits of which will not be fully expe-

rienced for at least another year. A further factor is the increase in working capital.

Last year, we actually managed to have negative working capital (i.e. our trade credi-

tors and overdraft financed more than our current assets). This year, there has been a

slight deterioration in all elements of working capital:

• We take five more days to collect cash from customers

•

Stockholding period has increased by four days

• We pay suppliers a little quicker.

Liquidity. Our current and quick asset ratios are both well below the typical level for

the industry of 1.8 and 1.0 respectively. However, this is largely due to the fact that

CFAI_C02.QXD 10/28/05 2:19 PM Page 55

.

56 Part I A framework for financial decisions

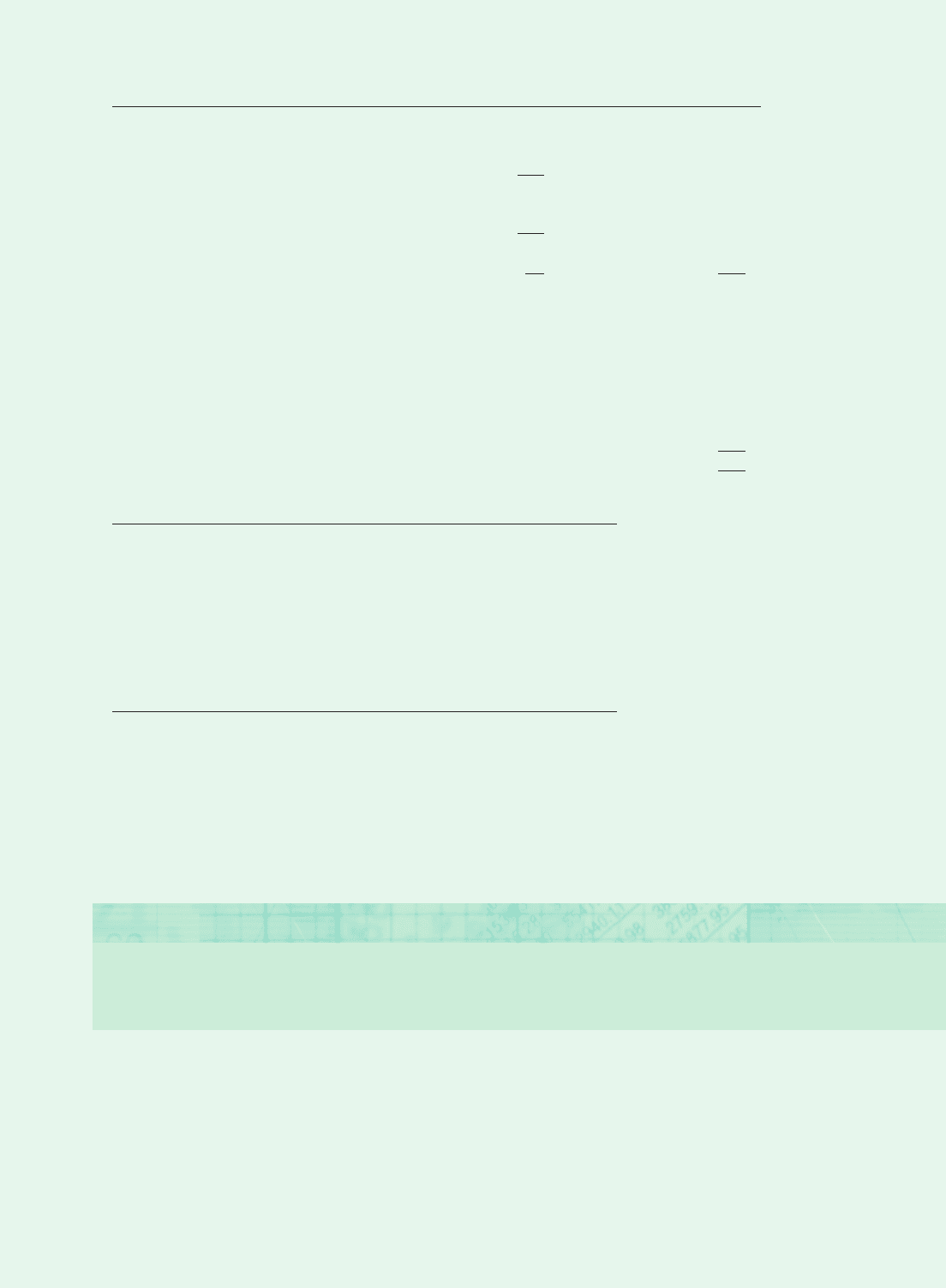

Table 2.4

Continued

our suppliers have been willing to grant us extended credit periods of about three

months. Realistically, we cannot expect this to continue. Were they to demand pay-

ment within say, 45 days, it is difficult to see where we would be able to find the

cash. It is not good financial management for us to rely on the generous credit of sup-

pliers over whom we have no control, and we need to address this issue urgently.

Linked to this, we have just raised a large medium-term loan in order to fund our

capital expenditure in the coming year. Our gearing ratio has now nearly doubled

and we will have to find cash both for additional interest payments and, eventually,

the loan repayments. Unless the new investment very rapidly produces higher profits

and cashflow, I am concerned that we could be in serious financial difficulty, despite

the strong level of profits. Perhaps it is time to consider asking shareholders to invest

more capital in the business, or to reduce dividend payments.

Investment attractiveness. The company’s share price has progressed from 50 pence to

120 pence over the year. No doubt this is due to the growth in sales, profits and divi-

dends in the year. Many of the investment performance indicators have improved,

particularly earnings per share and return on shareholders’ funds, the latter looking

much healthier at nearly 18%. However, the price:earnings ratio has slipped a little,

suggesting that investors do not expect the company’s profits and share price to con-

tinue to grow at quite the same rate as this year.

In summary, Foto-U has improved its performance over the past year, but there

remain concerns regarding its liquidity. Management is urged to give urgent atten-

tion to this matter.

CFAI_C02.QXD 10/28/05 2:19 PM Page 56

.

Chapter 2 The financial environment 57

Questions with a coloured number

have solutions in Appendix B on page 691.

1 When a company seeks a listing for its shares on a stock exchange, it usually recruits the assistance of a mer-

chant bank.

(a) Explain the role of a merchant bank in a listing operation with respect to the various matters on which its

advice will be sought by a company.

(b) Identify the conflicts which might arise if the merchant bank were part of a group providing a wide range

of financial services.

(CIMA)

2 (a) Briefly outline the major functions performed by the capital market and explain the importance of each

function for corporate financial management. How does the existence of a well-functioning capital mar-

ket assist the financial management function?

(b) Describe the Efficient Markets Hypothesis and explain the differences between the three forms of the

hypothesis which have been distinguished.

(c) Company A has 2 million shares in issue and company B 6 million. On day 1 the market value per share

is £2 for A and £3 for B. On day 2, the management of B decides, at a private meeting, to make a cash

takeover bid for A at a price of £3.00 per share. The takeover will produce large operating savings with a

value of £3.2 million. On day 4, B publicly announces an unconditional offer to purchase all shares of A

at a price of £3.00 per share with settlement on day 15. Details of the large savings are not announced and

are not public knowledge. On day 10, B announces details of the savings which will be derived from the

takeover.

Required

Ignoring tax and the time-value of money between days 1 and 15, and assuming the details given are the

only factors having an impact on the share prices of A and B, determine the day 2, day 4 and day 10 share

prices of A and B if the market is:

1 semi-strong form efficient, and

2 strong form efficient

in each of the following separate circumstances:

(i) the purchase consideration is cash as specified above, and

(ii) the purchase consideration, decided upon on day 2 and publicly announced on day 4, is one newly

issued share of B for each share of A.

(ACCA)

3 You are an accountant with a practice that includes a large proportion of individual clients, who often ask for

information about traded investments. You have extracted the following data from a leading financial news-

paper.

(i)

QUESTIONS

Stock Price P:E ratio Dividend yield (% gross)

Buntam plc 160p 20 5

Zellus plc 270p 15 3.33

(ii) Earnings and dividend data for Crazy Games plc are given below:

1993 1994 1995 1996 1997

EPS 5p 6p 7p 10p 12p

Div. per share (gross) 3p 3p 3.5p 5p 5.5p

The estimated before tax return on equity required by investors in Crazy Games plc is 20%.

Continued

CFAI_C02.QXD 10/28/05 2:19 PM Page 57

.

58 Part I A framework for financial decisions

Required

Draft a report for circulation to your private clients which explains:

(a) the factors to be taken into account (including risks and returns) when considering the purchase of

different types of traded investments.

(b) the role of financial intermediaries, and their usefulness to the private investor.

(c) the meaning and the relevance to the investor of each of the following:

(i) Gross dividend (pence per share)

(ii) EPS

(iii) Dividend cover

Your answer should include calculation of, and comment upon, the gross dividends, EPS and dividend

cover for Buntam plc and Zellus plc, based on the information given above.

(ACCA)

4 Beta plc has been trading for twelve years and during this period has achieved a good profit record. To date,

the company has not been listed on a recognised stock exchange. However, Beta plc has recently appointed a

new chairman and managing director who are considering whether or not the company should obtain a full

Stock Exchange listing.

Required

(a) What are the advantages and disadvantages which may accrue to the company and its shareholders, of

obtaining a full stock exchange listing?

(b) What factors should be taken into account when attempting to set an issue price for new equity shares in

the company, assuming it is to be floated on a stock exchange?

(Certified Diploma)

5 Collingham plc produces electronic measuring instruments for medical research. It has recorded strong and

consistent growth during the past 10 years since its present team of managers bought it out from a large multi-

national corporation. They are now contemplating obtaining a stock market listing.

Collingham’s accounting statements for the last financial year are summarised below. Fixed assets, includ-

ing freehold land and premises, are shown at historic cost net of depreciation. The debenture is redeemable

in two years although early redemption without penalty is permissible.

Profit and Loss Account for the year ended 31 December 1994 (£m)

Turnover 80.0

Cost of sales (70.0

)

Operating profit 10.0

Interest charges (3.0

)

Pre-tax profit 7.0

Corporation tax (after capital allowances) (1.0

)

Profits attributable to ordinary shareholders 6.0

Dividends (0.5

)

Retained earnings 5.5

CFAI_C02.QXD 10/28/05 2:19 PM Page 58

.

Chapter 2 The financial environment 59

Required

(a) Briefly explain why companies like Collingham seek stock market listings.

(b) Discuss the performance and financial health of Collingham in relation to that of the industry as a whole.

(c) In what ways would you advise Collingham:

(i) to restructure its balance sheet prior to flotation?

(ii) to change its financial policy following flotation?

Balance Sheet as at 31 December 1994 (£m)

Assets employed

Fixed: Land and premises 10.0

Machinery 20.0

30.0

Current: Stocks 10.0

Debtors 10.0

Cash 3.0 23.0

Current liabilities: Trade creditors (15.0)

Bank overdraft (5.0

) (20.0)

Net current assets 3.0

Total assets less current liabilities 33.0

14% Debentures (5.0)

Net assets 28.0

Financed by:

Issued share capital (par value 50p):

Voting shares 2.0

Non-voting ‘A’ shares 2.0

Profit and Loss Account 24.0

Shareholders’ funds 28.0

Select two companies from one sector in the Financial Times share information service. Analyse the share price

and other data provided and compare this with the FT All-Share Index data for the sector. Suggest why the P:E

ratios for the companies differ.

Practical assignment

The following information is also available regarding key financial indicators for Collingham’s industry.

Return on (long-term) capital employed 22% (pre-tax)

Return on equity 14% (post-tax)

Operating profit margin 10%

Current ratio 1.8:1

Acid test 1.1:1

Gearing (total debt/equity) 18%

Interest cover 5.2

Dividend cover 2.6

P:E ratio 13:1

CFAI_C02.QXD 10/28/05 2:19 PM Page 59

.

60 Part I A framework for financial decisions

Present values and financial arithmetic

3

Learning objectives

Having completed this chapter, you should have a sound grasp of the time-value of money and dis-

counted cash flow concepts. In particular, you should understand the following:

■ The time-value of money.

■ The financial arithmetic underlying compound interest and discounting.

■ Present value formulae for single amounts, annuities, perpetuities and bonds.

■ The net present value approach and why it is consistent with shareholder goals.

Skills developed in discounted cash flow analysis, using both formulae and tables, will help enormously

in subsequent chapters.

An investment parable

A man, going off to another country, called together his

servants and loaned them money to invest for him

while he was gone. He gave £500 to one, £200 to

another and £100 to the last – dividing it in proportion

to their abilities – and then left on his trip. The man

who received the £500 began immediately to buy and

sell with it and soon earned another £500. The man

with £200 went right to work, too, and earned another

£200. But the man who received the £100 dug a hole

in the ground and hid the money for safe keeping.

After a long time their master returned from his

trip and called them to him to account for his

money. The man to whom he had entrusted the £500

brought him £1,000. His master praised him for good

work. ‘You have been faithful in handling this small

amount,’ he told him, ‘so now I will give you many

more responsibilities.’ Next came the man who had

received £200, with the report, ‘Sir, you gave me

£200 to use, and I have doubled it.’ ‘Good work’, his

master said. ‘You have been faithful over this small

amount, so now I will give you much more.’

Then the man with the £100 came and said, ‘Sir,

I knew you were a hard man, and I was afraid you

would rob me of what I earned, so I hid your money

in the earth and here it is!’

But his master replied, ‘You lazy rogue! Since you

knew I would demand your profit, you should at least

have put my money into the bank so I could have

some interest.’

Source: Matthew, Chapter 25, Living Bible.

CFAI_C03.QXD 10/26/05 11:11 AM Page 60

.

Chapter 3 Present values and financial arithmetic 61

3.2 MEASURING WEALTH

‘Cash flow is King’ seems to be the message for businesses today. Spectacular business

collapses in recent years demonstrate that reliance on profits or earnings per share as

measures of performance can be dangerous.

The chairman of a fast-growing company that went out of business stated in the

annual report: ‘Last year, we delivered a 425% increase in turnover from £19.9 million

to £109.8 million.’ But when the firm was placed into the hands of the receiver the fol-

lowing year, it was not the lack of sales or even profits that put it there. It was the lack

of cash. Businesses go ‘bust’ because they run out of the cash required to fulfil their

financial obligations. Of course, there are always reasons why this happens – recession,

an over-ambitious investment programme, rapid growth without adequate long-term

finance – but basically corporate survival and success come down to cash flow and

value creation.

Boo.com, the internet fashion retailer, thought it had a promising future at the start

of 2000. It had raised $135 million to set up the new business and invest in marketing

to break into the competitive fashion retail sector. But less than six months later, it had

virtually run out of cash and was forced into liquidation.

Recall from Chapter 1 that the assumed objective of the firm is to create as much

wealth as possible for its shareholders. A successful business is one that creates value

for its owners. Wealth is created when the market value of the outputs exceeds the

market value of the inputs, i.e. the benefits are greater than the costs. Expressed

mathematically:

V

j

B

j

C

j

The value (V

j

) created by decision j is the difference between the benefits (B

j

) and

the costs (C

j

) attributable to the decision. This leads to an obvious decision rule: accept

only those investment or financing proposals that enhance the wealth of shareholders,

i.e. accept if B

j

C

j

0.

Nothing could be simpler in concept – the problems emerge only when we probe

more deeply into how the benefits and costs are measured and evaluated. One obvi-

ous problem is that benefits and costs usually occur at different times and over a num-

ber of years. This leads us to consider the time-value of money.

3.1 INTRODUCTION

The introductory investment parable, taken from business life in 1st century Palestine,

is equally appropriate to present times. Managers are expected to make sound long-

term decisions and to manage resources in the best interests of the owners. To do oth-

erwise is to risk the wrath of an unmerciful stock market! Rather like the lazy servant

in the parable, Eurotunnel put the £10 billion entrusted to it by shareholders and

bankers into a ‘hole in the ground’ stretching from Dover to Calais. From an investment

perspective they would have done better letting it earn interest in a bank.

To assess whether investment ideas are wealth-creating, we need to have a clear

understanding of cash flow and the time-value of money. Capital investment deci-

sions, security and bond value analyses, financial structure decisions, lease vs. buy

decisions and the tricky question of the required rate of return can be addressed only

when you understand exactly what the old expression ‘time is money’ really means.

In this chapter we will consider the measurement of wealth and the fundamental

role it plays in the decision-making process; the time-value of money, which underlies

the discounted cash flow concept; and the net present value approach for analysing

investment decisions.

time-value of money

Money received in the future is

usually worth less than today

because it could be invested to

earn interest over this period

CFAI_C03.QXD 10/26/05 11:11 AM Page 61

.

62 Part I A framework for financial decisions

Self-assessment activity 3.1

Imagine you went to your bank manager asking for a £50,000 loan, for five years, to start

up a burger bar under a McDonald’s franchise. Which of the considerations in the previous

paragraph would the bank manager consider?

(Answer in Appendix A at the back of the book)

Boo.com collapses as investors refuse funds

Boo.com, the online sportswear retailer, last night became Europe’s first big internet casualty when the

refusal of its backers to continue funding its heavy losses forced it into liquidation. The company – one of

the highest profile internet retailers in Europe – appointed KPMG as liquidator, having spent all but

$500,000 of the $135 million it had raised since early last year.

Boo’s founders, including former model Kajsa Leander and Ernst Malmsten, chief executive, own about

40 per cent of the equity. Ernst Malmsten said last night: ‘It could be a big blow for the internet in

Europe and frighten investors from investing in start-ups because they could lose their reputation as well

as their funding. We have been too visionary. We wanted everything to be perfect, and we have not had

control of costs. My mistake has been not to have a counterpart who was a strong financial controller’.

After a high-profile launch, the company was dogged by technical problems that delayed the site going

live by five months. Boo needed $430 million to implement an emergency restructuring plan that would

have seen redundancies among the 300-strong workforce and closure of some overseas offices. But

investors were not prepared to back the plan with more money.

Source:Based on Financial Times, 18 May 2000.

3.3 TIME-VALUE OF MONEY

An important principle in financial management is that the value of money depends on

when the cash flow occurs – £100 now is worth more than £100 at some future time. There

are a number of reasons for this:

1 Risk. One hundred pounds now is certain, whereas £100 receivable next year is less cer-

tain. This ‘bird-in-the-hand’ principle affects many aspects of financial management.

2 Inflation. Under inflationary conditions, the value of money, in terms of its purchas-

ing power over goods and services, declines.

3 Personal consumption preference. Most of us have a strong preference for immediate

rather than delayed consumption.

More fundamental than any of the above, however, is the time-value of money.

Money – like any other desirable commodity – has a price. If you own money, you can

‘rent’ it to someone else, say a banker, and earn interest. A business which carries

unnecessarily high cash balances incurs an opportunity cost – the lost opportunity to

earn money by investing it to earn a higher return. The overall investor’s return, which

reflects the time-value of money, therefore comprises:

(a) the risk-free rate of return rewarding investors for forgoing immediate consump-

tion, plus

(b) compensation for risk and loss of purchasing power.

Before proceeding further, we need to understand the essential financial arithmetic

for the time-value of money. This will stand readers in good stead not only in

CFAI_C03.QXD 10/26/05 11:11 AM Page 62

.

Chapter 3 Present values and financial arithmetic 63

analysing capital and financial investments in the remainder of this book, but also in

handling their personal finances. For example, it will provide a better understanding

of how interest is calculated for credit cards, bank loans, repayment mortgages and

hire purchase arrangements.

3.4 FINANCIAL ARITHMETIC FOR CAPITAL GROWTH

■ Simple and compound interest

The future value (FV) of a sum of money invested at a given annual rate of interest

will depend on whether the interest is paid only on the original investment (simple

interest), or whether it is calculated on the original investment plus accrued interest

(compound interest). Suppose you win £1,000 on the National Lottery and decide to

invest it at 10 per cent for five years, simple interest. The future value will be the orig-

inal £1,000 capital plus five years’ interest of £100 a year, giving a total future value

of £1,500.

With compound interest, the interest is paid on the original capital plus accrued

interest, as shown in Table 3.1. The process of compounding provides a convenient

way of adjusting for the time-value of money. An investment made now in the capital

market of V

o

gives rise to a cash flow of V

o

(1 i)

2

after two years, and so on. In gen-

eral, the future value of V

o

invested today at a compound rate of interest of i per cent

for n years will be:

FV

(i,n)

= V

o

(1 + i)

n

where FV

(i,n)

is the future value at time n, V

o

is the original sum invested, sometimes

termed the principal (note that the o subscript refers to the time period, i.e. today), and

i is the annual rate of interest.

Using this formula in the above example we obtain the same future value as in

Table 3.1.

FV

5

£1,000(1 0.10)

5

£1,610

Note that the effect of compound interest yields a higher value than simple interest,

which yielded only £1,500.

■ More frequent compounding and annual percentage rates

Unless otherwise stated, it is assumed that compounding or discounting is an annual

process; cash payments of benefits arise either at the start or the end of the year.

Frequently, however, the contractual payment period is less than one year. Building

societies and government bonds pay interest semi-annually or quarterly. Interest

charged on credit cards is applied monthly. To compare the true costs or benefits of such

financial contracts, it is necessary to determine the annual percentage rate (APR), or

effective annual interest rate.

Table 3.1

Compound interest on

£1,000 over five years

(at 10%)

Starting Closing

Year balance £ Interest £ Balance £

1 1000 100 1100

2 1100 110 1210

3 1210 121 1331

4 1331 133 1464

5 1464 146 1610

CFAI_C03.QXD 10/26/05 11:11 AM Page 63

.

64 Part I A framework for financial decisions

Returning to our earlier example of £1,000 invested for five years at 10 per cent com-

pound interest, we now assume 5 per cent payable every six months.

After the first six months, the interest is £50, which is reinvested to give interest for

the second half year of (£1,050 5%) £52. The end-of-year value is therefore (£1,050

£52) £1,102. We can still use the compound interest formula, but with i as the six-

monthly interest rate and n the six-monthly, rather than annual, interval:

Note that this value is higher than the £1,610 value based on the earlier annual inter-

val calculation. In converting the annual compounding formula to another interest

payment frequency, the trick is simply to divide the annual rate of interest (i) and mul-

tiply the time (n) by the number of payments each year.

If, in the above example, interest is calculated at weekly intervals over five years,

the future value will be:

Taking compounding to its limits, we can adopt a continuous discounting

approach.*

Table 3.2 calculates the APRs based on a range of interest payment frequencies for

a 22 per cent per annum loan. By charging compound interest on a daily basis, the

effective annual rate is 24.6 per cent, some 2.6 per cent higher than on an annual basis.

It is now a legal requirement for many financial contracts that the lender clearly states

the APR.

FV

5

£1,000 ¢1

0.10

52

≤

52152

£1,648

£1,629

After 5 years, FV

5

£1,00011 0.052

10

£1,102

After 1 year, FV

1

£1,00011 0.052

2

*When the number of compounding periods each year approaches infinity, the future value is found by:

where i is the annual interest rate, n is the number of years and e is the value of the exponential

function. Using a scientific calculator, this is shown as 2.71828 (to five decimal places).

Using the same example as before:

£1,648.72 1slightly more than compounding on a weekly basis2

FV

4

V

o

e

in

£1,000 e

10.125

FV

n

V

o

e

in

Table 3.2

Annual percentage

rates for a loan with

interest payable at 22

per cent per annum

Annually

Semi-annually

Quarterly

Monthly

Daily

0.246 or 24.6% 1¢1

0.22

365

≤

365

0.244 or 24.4% 1¢1

0.22

12

≤

12

0.239 or 23.9% 1¢1

0.22

4

≤

4

0.232 or 23.2% 1¢1

0.22

2

≤

2

0.22 or 22% 111 0.222

CFAI_C03.QXD 10/26/05 11:11 AM Page 64