Pike Robert, Neal Bill. Corporate finance and investment: decisions and strategy

Подождите немного. Документ загружается.

.

Chapter 3 Present values and financial arithmetic 65

3.5 PRESENT VALUE

An alternative way of assessing the worth of an investment is to invert the compound-

ing process to give the present value of the future cash flows. This process is called

discounting.

The time-value of money principle argues that, given the choice of £100 now or the

same amount in one year’s time, it is always preferable to take the £100 now because

it could be invested over the next year at, say, a 10 per cent interest rate to produce £110

at the end of one year. If 10 per cent is the best available annual rate of interest, then

one would be indifferent to (i.e. attach equal value to) receiving £100 now or £110 in

one year’s time. Expressed another way, the present value of £110 received one year

hence is £100.

We obtained the present value (PV) simply by dividing the future cash flow by 1

plus the rate of interest, i, i.e.

Discounting is the process of adjusting future cash flows to their present values. It is,

in effect, compounding in reverse.

Recall that earlier we specified the future value as:

Dividing both sides by we find the present value:

which can be read as the present value of future cash flow FV receivable in n years’ time

given a rate of interest i. This is the process of discounting future sums to their present

values.

Let us apply the present value formula to compute the present value of £133 receiv-

able three years hence, discounted at 10 per cent:

The message is: do not pay more than £100 today for an investment offering a cer-

tain return of £133 after three years, assuming a 10 per cent market rate of interest.

PV

110%, 3 yrs2

£133

11 0.102

3

£133

1.33

£100

V

o

FV

n

11 i2

n

11 i2

n

FV

n

V

o

11 i2

n

PV

£110

11 0.102

£110

11.12

£100

Calculator tip

Your calculator should have a power function key, usually Try the following steps for

the previous example.

Input 1.1

Press function key

Input 3

Press

Display 1.331

Press 1/x

Multiply 133

Press

Answer 99.9

x

y

x

y

.

present value

The current worth of future

cash flows

discounting

The process of reducing cash

flows to present values

CFAI_C03.QXD 10/26/05 11:11 AM Page 65

.

66 Part I A framework for financial decisions

■ Discount tables

Much of the tedium of using formulae and power functions can be eased by using dis-

count tables or computer-based spreadsheet packages. In the previous example, the

discount factor for £1 for a 10 per cent discount rate in three years’ time is:

This can be found in Appendix C by locating the 10 per cent column and the 3 year

row. We call this the present value interest factor (PVIF) and express it as

or

Multiplying the cash flow of £133 by the discount factor yields the same result as

before:

With a constant annual cash flow, termed an annuity, we can shorten the discount-

ing operation. Appendix D provides the present value interest factor for an annuity

(PVIFA). Thus, if £133 is to be received in each of the next three years, the present value

is:

It is standard practice to write interest factors as: Interest factor(rate, period).

Examples:

is the present-value interest factor at 8 per cent for ten years.

is the present-value interest factor for an annuity at 10 per cent for four

years.

PVIFA

110,42

PVIF

18,102

£133 2.4868 £331

PV £133 PVIFA

110%, 3 yrs2

PV £133 0.751 £100 1subject to rounding2

PVIF

110,32

.

PVIF

110%, 3 yrs2

1

11.102

3

1

1.33

0.751

Self-assessment activity 3.2

Calculate the present value of £623 receivable in eight years’ time plus £1,092 receivable

eight years after that, assuming an interest rate of 7 per cent.

(Answer in Appendix A at the back of the book)

Example of present values: Soldem Pathetic plc

Soldem Pathetic Football Club has recently been bought up by a wealthy business-

man who intends to return the club to its former glory days. He also wants to pay a

good dividend to the shareholders of the newly-formed quoted company by making

sound investments in quality players. One such player the manager would dearly

like in his squad is Bryan Riggs, currently on the market for around £9 million. The

chairman reckons that, quite apart from the extra income at the turnstiles from buy-

ing him, he could be sold for £11 million by the end of the year, given the way trans-

fer prices are moving. Should he bid for Riggs?

Assuming a 10 per cent rate of interest as the reward that the other shareholders

demand for accepting the delayed payoff, the present value (PV) of £11 million receiv-

able one year hence is:

£10 million

PV discount factor future cash flow

1

1.10

£11 million

annuity

A constant annual cash flow

for a prescribed period of time

CFAI_C03.QXD 10/26/05 11:11 AM Page 66

.

Chapter 3 Present values and financial arithmetic 67

In the highly simplified example above, we assumed that the future value was cer-

tain and the interest rate known. Of course, a spectrum of interest rates is listed in the

financial press.

This variety of rates arises predominantly because of uncertainty surrounding the

future and imperfections in the capital market. To simplify our understanding of the

time-value of money concept, let us ‘assume away’ these realities. The lender knows

with certainty the future returns arising from the proposal for which finance is sought,

and can borrow or lend on a perfect capital market. The latter assumes the following:

1 Relevant information is freely available to all participants in the market.

2 No transaction costs or taxes are involved in using the capital market.

3 No participant (borrower or lender) can influence the market price for funds by the

scale of its activities.

4 All participants can lend and borrow at the same rate of interest.

Under such conditions, the corporate treasurer of a major company like Shell can

raise funds no more cheaply than the chairman of Soldem Pathetic. A single market

rate of interest prevails. Borrowers and lenders will base time-related decisions on this

unique market rate of interest. The impact of uncertainty will be discussed in later

chapters; for now, these simplistic assumptions will help us to grasp the basics of

financial arithmetic.

■ The effect of discounting

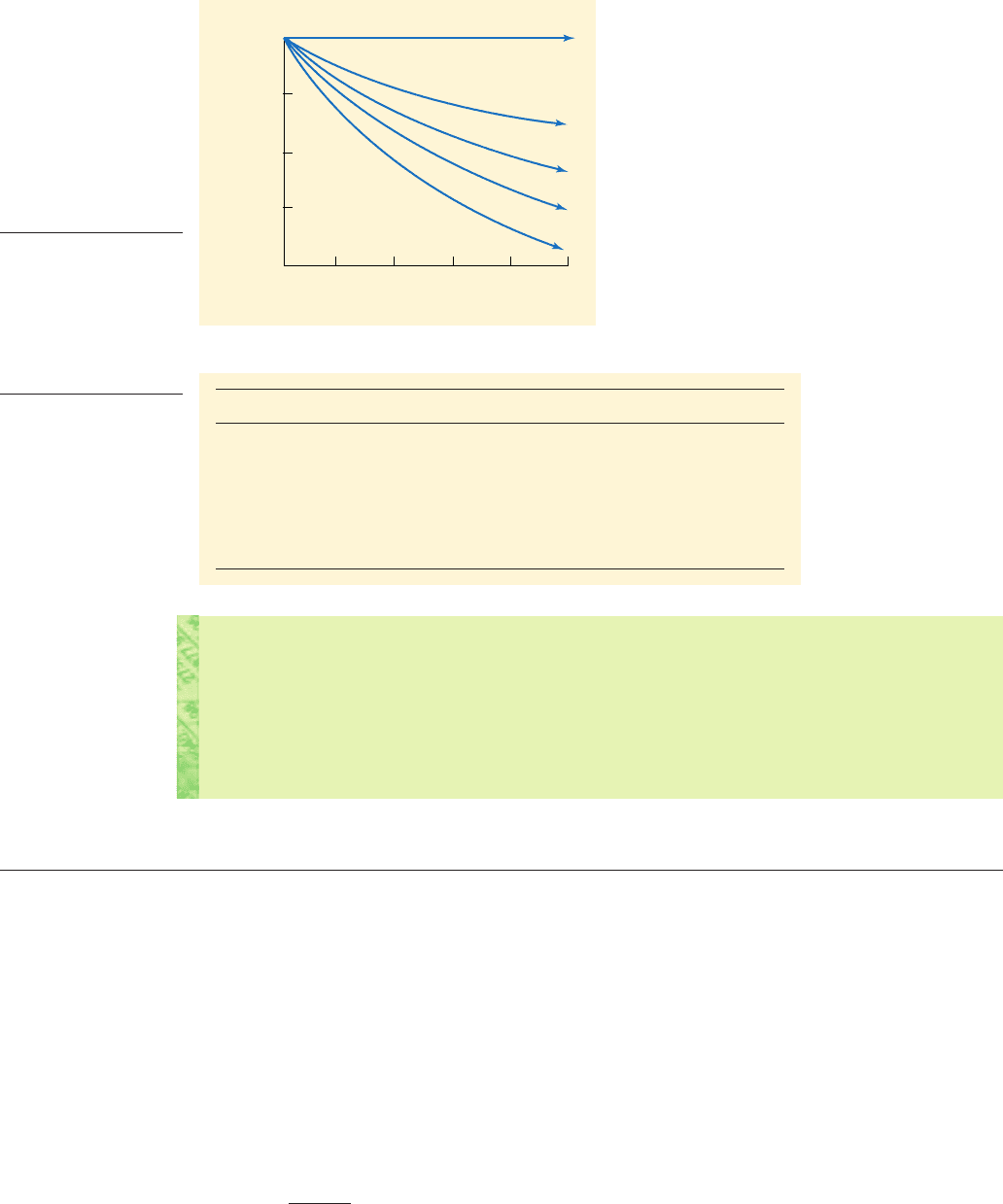

Figure 3.1 shows how the discounting process affects present values at different rates

of interest between 0 and 20 per cent. The value of £1 decreases very significantly as the

rate and period increase. Indeed, after 10 years, for an interest rate of 20 per cent, the

present value of a cash flow is only a small fraction of its nominal value.

Table 3.3 summarises the discount factors for three rates of interest. It is useful to

develop a ‘feel’ for how money changes with time for these rates of interest. The 15 per

cent discount rate is particularly useful, because investment surveys (e.g. Pike 1988)

suggest that this is a popular discount rate for evaluating capital projects. It also hap-

pens to be easy to remember: every five years the discounted value halves. Thus, with

a 15 per cent discount rate, after five years the value of £1 is 50p, after 10 years 25p, etc.

How much better off will the club be if it buys Riggs? The answer is, in present value

terms:

We call this the

net present value (NPV). The decision to buy the player makes eco-

nomic sense; it promises to create wealth for the club and its shareholders, even

excluding the likely additional gate receipts. Of course, Riggs could break a leg in the

very first game for his new club and never play again. In such an unfortunate situa-

tion, the club would achieve a negative NPV of £9 million, the initial cost.

Alternatively, he could be insured against such injury, in which case there would be

premiums to pay, resulting in a lower net present value.

Another way of looking at this issue is to ask whether the investment offers a return

greater than could have been achieved by investing in financial, rather than human,

assets. The return over one year from acquiring Riggs’ services is:

If the available rate of interest is 10 per cent, the investment in Riggs is a considerably

more rewarding prospect.

Return

Profit

investment

£11 m £9 m

£9 m

100 22.2%.

£10 million £9 million £1 million

net present value

The present value of

the future net benefits

less the initial cost

CFAI_C03.QXD 10/26/05 11:11 AM Page 67

.

68 Part I A framework for financial decisions

Present value of £1

1.00

0%

5%

10%

15%

20%

0246810

Periods

0.75

0.50

0.25

Figure 3.1

The relationship

between present value

of £1 and interest over

time

Table 3.3

Present value of a single

future sum

Year 10% 15% 20%

0 £1.00 £1.00 £1.00

5 0.60 0.50 0.40

10 0.40 0.25 0.16

15 0.24 0.12 0.06

20 0.15 0.06 0.03

25 0.09 0.03 0.01

Self-assessment activity 3.3

Your company is just about to sign a deal to purchase a fleet of lorries for £1 million. The

payment terms are £500,000 down payment and £500,000 at the end of five years. No

one present has a calculator or discount tables to hand. If the cost of capital for the com-

pany is 15 per cent, what is the present value cost of the purchase?

(Answer in Appendix A at the back of the book)

3.6 PRESENT VALUE ARITHMETIC

We have seen that the present value of a future cash flow is found by multiplying the

cash flow by the present value interest factor. The present value concept is not difficult

to apply in practice. This section explains the various present value formulae, and illus-

trates how they can be applied to investment and financing problems. Throughout, we

shall use the symbol X to denote annual cash flow in pounds and i to denote the inter-

est, or discount, rate (expressed as a percentage). Recall that PVIF is the present value

interest factor and PVIFA is the PVIF for an annuity.

■ Present value

We know that the present value of X receivable in n years is calculated from the

expression:

X times PVIF

1i,n2

PV

1i,n2

X

n

11 i2

n

CFAI_C03.QXD 10/26/05 11:11 AM Page 68

.

Chapter 3 Present values and financial arithmetic 69

Example

Calculate the present value of £1,000 receivable in 10 years’ time, assuming a discount

rate of 14 per cent:

Alternatively, the table in Appendix C provides PVIF of 0.26974 for and

per cent:

The present value of £1,000 receivable ten years hence, discounted at 14 per cent, is

thus £269.74.

PV £1,000 0.26974 £269.74

i 14

n 10

PVIF

114%, 10 yrs2

1

11.142

10

0.26974

Self-assessment activity 3.4

Calculate the present value of £1,000 receivable 12 years hence, assuming the discount

rate is 12 per cent.

(Answer in Appendix A at the back of the book)

■ Valuing perpetuities

Frequently, an investment pays a fixed sum each year for a specified number of years.

A series of annual receipts or payments is termed an annuity. The simplest form of

annuity is the infinite series or perpetuity. For example, certain government stocks offer

a fixed annual income, but there is no obligation to repay the capital. The present value

of such stocks (called irredeemables) is found by dividing the annual sum received by

the annual rate of interest:

Example

Uncle George wishes to leave you in his will an annual sum of £10,000 a year, starting

next year. Assuming an interest rate of 10 per cent, how much of his estate must be set

aside for this purpose? The answer is:

Suppose that your benevolent uncle now wishes to compensate for inflation, esti-

mated to be at 5 per cent per annum. The formula can be adjusted to allow for growth

at the rate of g per cent p.a. in the annual amount. (The derivation of the present value

of a growing perpetuity is found in Appendix II at the end of the chapter.)

As long as the growth rate is less than the interest rate, we can compute the present

value required:

This formula plays a key part in analysing financial decisions and will be developed

further in Chapter 4, when we consider the valuation of assets, shares and companies.

PV

£10,000

0.10 0.05

£200,000

PV

X

i g

PV perpetuity

£10,000

0.10

£100,000

PV perpetuity

X

i

perpetuity

A constant annual cash flow

for an infinite period of time

CFAI_C03.QXD 10/26/05 11:11 AM Page 69

.

70 Part I A framework for financial decisions

■ Valuing annuities

An annuity is an investment paying a fixed sum each year for a specified period of

time. Examples of annuities are many credit agreements and house mortgages.

The life of an annuity is less than that of a perpetuity, so its value will also be some-

what less. In fact, the formula for calculating the present value of an annuity of £A is

found by calculating the present value of a perpetuity and deducting the present value

of that element falling beyond the end of the annuity period. This gives the somewhat

complicated formula (see Appendix II at the end of chapter for the derivation) for the

present value of an annuity (PVA):

In words, the present value of an annuity for n years at i per cent is the annual sum

multiplied by the appropriate present value interest factor for an annuity.

Suppose an annuity of £1,000 is issued for 20 years at 10 per cent. Using the table in

Appendix D, we find the present value as follows:

£1,000 8.5136 £8,513.60

PVA

110%, 20 yrs2

£1,000 PVIFA

110,202

A PVIFA

1i,n2

PVA

1i,n2

A¢

1

i

1

i11 i2

n

≤

Self-assessment activity 3.5

Calculate the present value of £250 receivable annually for 21 years plus £1,200 receiv-

able after 22 years, assuming an interest rate of 11 per cent.

(Answer in Appendix A at the back of the book)

■ Calculating interest rates

Sometimes, the present values and future cash flows are known, but the rate of interest

is not given. A credit company may offer to lend you £1,000 today on condition that you

repay £1,643 at the end of three years. To find the compound rate of interest on the loan,

we solve the present value formula for i:

Rearranging the formula,

Turning to the tables in Appendix C and looking for 0.6086 under the year 3 col-

umn, we find the rate of interest is 18 per cent. As we shall see in Chapter 5, this cal-

culation is fundamental to investment and finance decisions and is termed the internal

rate of return.

It is also possible to solve the present value formula for i:

i 1FV>PV2

1>n

1

11 i2

n

FV>PV

PV

FV

11 i2

n

PVIF

1i,32

PV

FV

£1,000

£1,643

0.60864

PV

1i,n2

PVIF

1i,n2

FV

internal rate of return

The rate of return that equates

the present value of future cash

flows with initial investment

outlay

CFAI_C03.QXD 10/26/05 11:11 AM Page 70

.

Chapter 3 Present values and financial arithmetic 71

In the above example:

i 11,643>1,0002

1>3

1 0.18 or 18%

3.7 VALUING BONDS

DCF has long been used to help value financial securities. We consider share valuation

in the next chapter, but deal here with the valuation of bonds. A bond is a long-term

loan which promises to pay interest and repay the loan in accordance with the agreed

terms. Governments, local authorities, companies and other organisations frequently

seek to raise funds by issuing bonds, sometimes termed loan stock.

Once issued, bonds are traded in the secondary bond markets. Although a bond has

a par, or nominal, value – typically £100 – its actual value will vary according to the

cash flows it pays (interest and repayments) and the prevailing rate of interest for this

type of bond. The fair price is the present value of the future interest and repayments.

Bondo Ltd issues a two-year bond with a 10 per cent coupon rate and interest

payable annually. The bond is priced at its face value of £100:

The bond value above includes the present value of the first year’s interest plus the

present value of the two elements of the Year 2 cash flow (i.e. interest and redemption

value).

Assume that the interest rate unexpectedly rises to 12 per cent. The bond is now

priced in the secondary market at a discount at the lower value of £96.62, reflecting the

fact that the 10 per cent interest rate is now less attractive to investors:

Assume now that the interest rates fall to 8 per cent. The bond would now be

viewed as more attractive and lead it to be priced at a premium:

From the above we may conclude that bonds will sell:

■ at a discount where the coupon rate is below the market interest rate, and

■ at a premium where the coupon rate is above the market interest rate.

£103.57

£10

1.08

£10 £100

11.082

2

£96.62

£10

1.12

£10 £100

11.122

2

£100

£10

1.10

£10 £100

11.102

2

V

o

PV 1interest payments2 PV 1redemption value2

Who wants to be a millionaire?

An advertisement in the financial press read: ‘How to become a millionaire? Invest £9,138

in the M&G Recovery unit trust in 1969 and wait for 25 years.’ So, for those of us who

missed out on this investment, let us grudgingly calculate its annual return:

By investing in a unit trust earning an annual rate of return of around 21 per cent,

£9,138 turns you into a millionaire in 25 years’ time. All you have to do is find an

investment giving 21 per cent for 25 years!

20.66%

1£1 million>£9,1382

1>25

1

i 1FV>PV2

1>n

1

discount

The amount below the face

value of a financial instrument

at which it sells

Coupon rate

The nominal annual rate of

interest expressed as a per-

centage of the principal value

premium

The amount above the face

value of a financial instrument

at which it sells

CFAI_C03.QXD 10/26/05 11:11 AM Page 71

.

72 Part I A framework for financial decisions

In the above example, the market interest was known. It may be that we know the bond

prices and wish to calculate the yield to maturity. Here we use the same formula but

the unknown is the interest rate. Thus, in the above where the market price is £103.57

we solve the equation (using a computer or trial and error) to find that 8 per cent is the

yield to maturity. The bond has a 10 per cent coupon and is priced at £103.57 to yield 8

per cent.

■ Valuing a bond in Millie Meter plc

Some time ago you purchased an 8 per cent bond in the fashion chain, Millie Meter.

Today, it has a par value of £100 and two years to maturity. Interest is payable half-

yearly. What is it worth?

Assuming the current comparable rate of interest is 8 per cent, the value should

equal the par value of £100.

Notice that because payments are made half-yearly, both the interest and discount

rate are half the annual figures.

In reality, the required rate of return demanded by investors may be different from

the original coupon rate. Let us say it is 10 per cent. As this is higher than the coupon

rate, the bond value for Millie Meter will fall below its par value:

This example shows that an investor would have to pay £96.45 for a bond offering

a 4 per cent coupon rate (i.e. based on the par value of £100) plus the redemption

value in two years’ time, assuming that the market rate of interest for this security is

10 per cent.

For actively traded bonds there is little need to value them in this way because, if

the bond market is efficient, it has already done it for you. All you need do is to look

at the latest quoted price. However, the required rate of return is less easy to obtain.

Who says, in the above example, that 10 per cent is the return expected by the market

for this type of bond? The answer is simple. If we know the current bond price, we put

this in the above equation to find that discount rate which equates price with the dis-

counted future cash flows – 10 per cent in the previous example.

V

o

4

11.052

4

11.052

2

4

11.052

3

4

11.052

4

100

11.052

4

£96.45

V

o

4

11.042

4

11.042

2

4

11.042

3

4

11.042

4

100

11.042

4

£100

Back to the future

FT

‘Tis the season to be jolly but there’s

always someone to cry ‘Humbug’.

According to Guy Monson from Saracen

Investment Fund in London, things are

pretty much as they were back in 1843

when Charles Dickens gave the world

Ebenezer Scrooge, miser extraordinaire,

in his novel A Christmas Carol.

Interest rates, government bond yields

and inflation are all within a whisker of

where they stood 141 years ago. There’s

also much living beyond one’s means:

that exercised Scrooge then and worries

analysts now.

If that wasn’t enough, some things have

actually got worse since the days of poverty

that Dickens so savagely chronicled. Back

then, income tax stood at just 5 per cent.

As old Ebenezer so charmingly put it:

‘Every idiot who goes around with Merry

Christmas on his lips should be buried

with his own pudding.

’

Source: Financial Times, 23 December 2004, p. 12

yield to maturity

The interest rate at which the

present value of the future

cash flows equals the current

market price

CFAI_C03.QXD 10/26/05 11:11 AM Page 72

.

Chapter 3 Present values and financial arithmetic 73

■

Factors affecting interest rates

It is common in financial management to talk about the interest rate ruling in the

money market. However, it is important to realise that there is never a single prevail-

ing rate. At any time, there is a spectrum of interest rates on offer – along this spectrum

the rates depend on the identity of the borrower e.g. firm or government, and hence,

the degree of risk faced by the lender, the amount lent or borrowed and the period over

which the loan is made available. The last of these aspects is referred to as the term

structure of interest rates. This shows how the yields offered for loans of different

maturities vary as the term of the loan increases. We discuss this, together with the

Yield Curve, in Appendix I to this chapter.

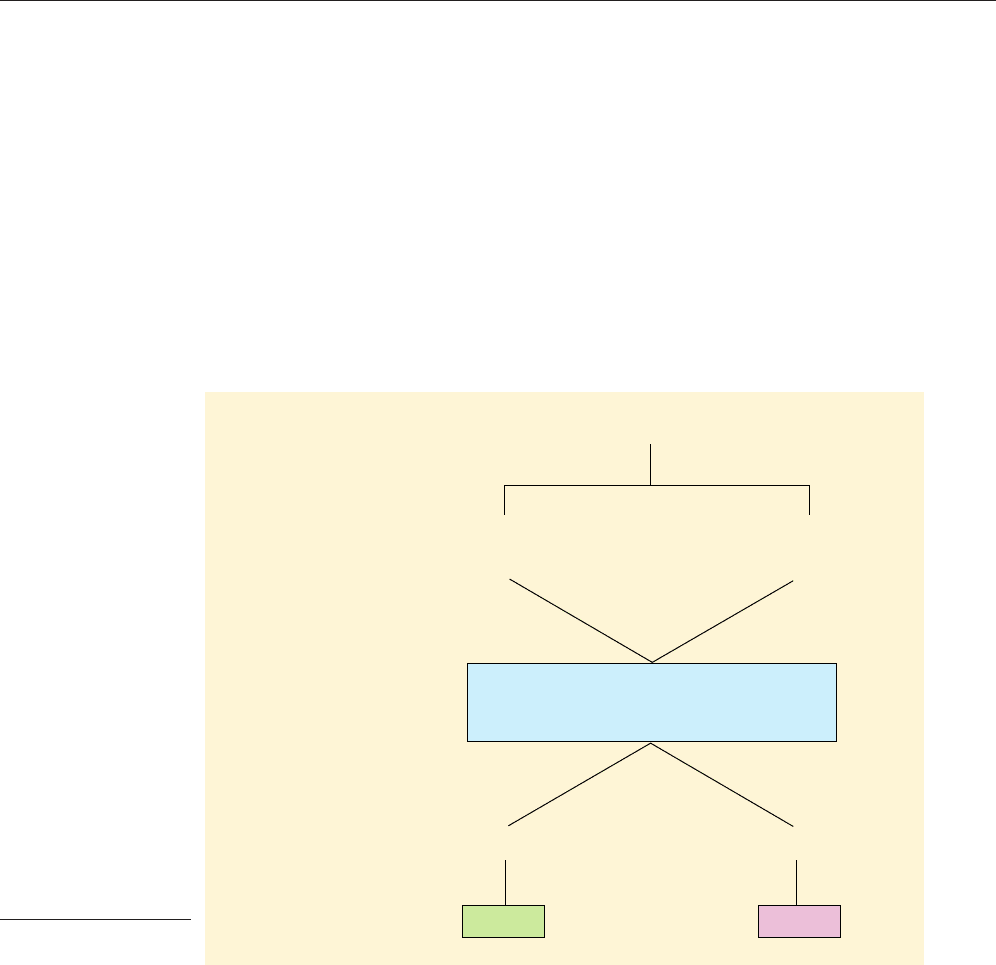

3.8 NET PRESENT VALUE

We have assumed that the paramount objective of the firm is to create as much wealth as

possible for its owners through the efficient use of existing and future resources. To cre-

ate wealth, the present value of all future cash inflows must exceed the present value of

all anticipated cash outflows. Quite simply, an investment with a positive net present value

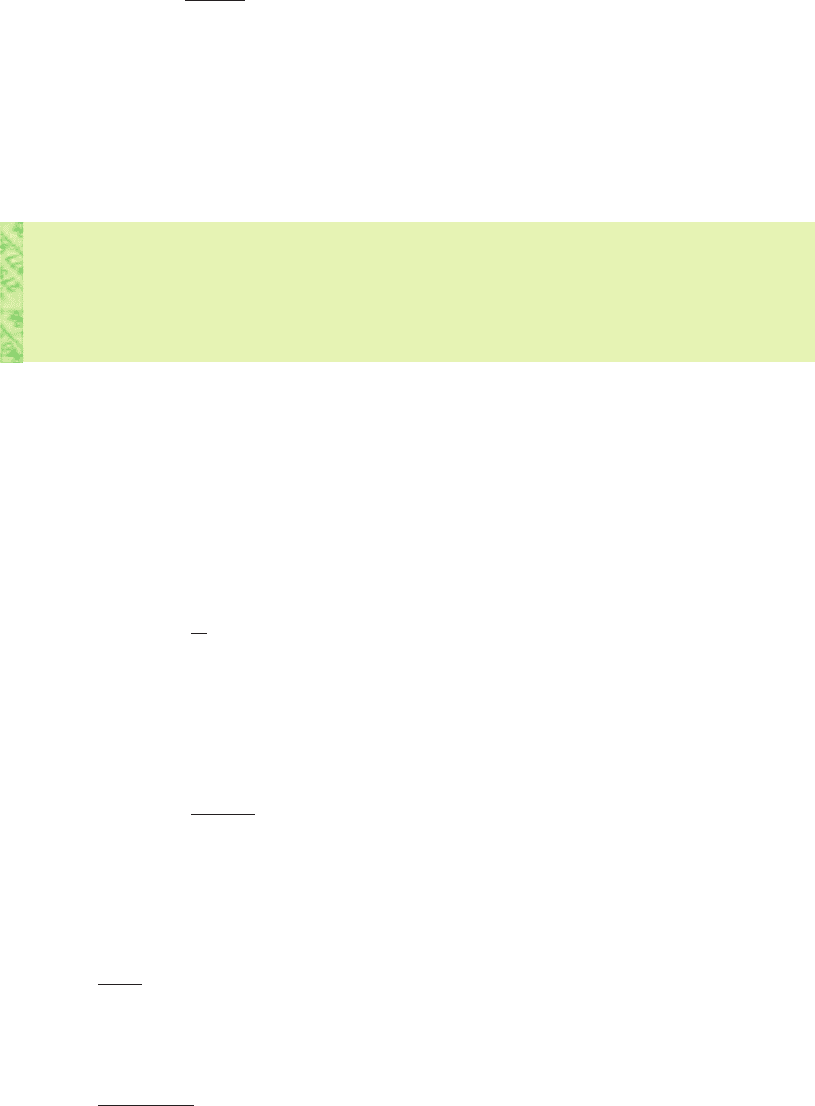

increases the owners’ wealth. The elements of investment appraisal are shown in Figure 3.2.

Most decisions involve both costs and benefits. Usually, the initial expenditure

incurred on an investment undertaken is clear-cut: it is what we pay for it. This

includes the cash paid to the supplier of the asset plus any other costs involved in

making the project operational. The problems start in measuring the worth of the

investment project. What an asset is worth may have little to do with what it cost or

what value is placed on it in the firm’s Balance Sheet. A machine standing in the firm’s

books at £20,000 may be worth far more if it is essential to the manufacture of a high-

ly profitable product, or far less than this if rendered obsolete through the advent of

new technology. To measure its worth, we need to consider the value of the current and

term structure of interest

rates

Pattern of interest rates on

bonds of the same risk with

different lengths of time to

maturity

Increase shareholder value

Annual cash flow

(

X

t

)

Cost of capital

(

K

)

Discount cash flows at the cost of capital

to find net present value

ACCEPT REJECT

–+

Goal

Inputs

Financial analysis

NPV signal

Decision outcome

Figure 3.2

Investment appraisal

elements

CFAI_C03.QXD 10/26/05 11:11 AM Page 73

.

74 Part I A framework for financial decisions

The net present value rule

Wealth is maximised by accepting all projects that offer positive net present values

when discounted at the required rate of return for each investment.

Most of the main elements in the NPV formula are largely externally determined.

For example, in the case of investment in a new piece of manufacturing equipment,

management has relatively little influence over the price paid, the life expectancy or

the discount rate. These elements are determined, respectively, by the price of capital

goods, the rate of new technological development and the returns required by the cap-

ital market. Management’s main opportunity for wealth creation lies in its ability to

implement and manage the project so as to generate positive net cash flows over the

project’s economic life.

■ An NPV example: Gazza Ltd

The management of Gazza Ltd is currently evaluating an investment in hair dye prod-

ucts costing £10,000. Anticipated net cash inflows are £6,000 received at the end of year

1 and a further £6,000 at the end of year 2. Assuming a discount rate of 10 per cent, cal-

culate the project’s net present value.

We can compute the NPV for Gazza using three different approaches, all of which

will be employed in later chapters.

Self-assessment activity 3.6

Define the main elements in the capital investement decision.

(Answer in Appendix A at the back of the book)

future benefits less costs arising from the investment. Wherever possible, these benefits

should be expressed in terms of cash flows. Sometimes (as will be discussed later) it is

impossible to quantify benefits so conveniently. Typically, investment decisions

involve an initial capital expenditure followed by a stream of cash receipts and dis-

bursements in subsequent periods. The net present value (NPV) method is applied to

evaluate the desirability of investment opportunities. NPV is defined as:

which may be summarised as:

where is the net cash flow arising at the end of year t, I is the initial cost of the invest-

ment, n is the project’s life, and k the minimum required rate of return on the invest-

ment (or discount rate). (The Greek letter or sigma, denotes the sum of all values in

a particular series.)

Note that we have introduced a subtle change in notation, replacing i, which denot-

ed the general market rate of interest, by k, which refers to the rate of return that must

be achieved by the firm in question. As we shall see, k may vary significantly from firm

to firm.

A project’s net present value (NPV) is determined by summing the net annual cash

flows, discounted at a rate that reflects the cost of an investment of equivalent risk on

the capital market, and deducting the initial outlay.

©,

X

t

NPV

a

n

t 1

X

t

11 k2

t

I

NPV

X

1

11 k2

X

2

11 k2

2

X

3

11 k2

3

p

X

n

11 k2

n

I

CFAI_C03.QXD 10/26/05 11:11 AM Page 74