Pike Robert, Neal Bill. Corporate finance and investment: decisions and strategy

Подождите немного. Документ загружается.

.

Chapter 3 Present values and financial arithmetic 75

1 Formula approach

This approach is particularly useful with few cash flows or where discount factors

are not available in tables.

2 Present value tables (using Appendix C)

Year Cash flow £ Discount factor at 10% Present value £

1 6,000 0.90909 5,454

2 6,000 0.82645

4,959

1.73554 10,413

Less initial cost (10,000

)

NPV 413

3 Present value annuity tables (using Appendix D)

This approach is appropriate only when annual cash flows are constant. Notice that

the present-value interest factor for an annuity at 10 per cent for two years (taken

from Appendix D) is simply the cumulative total of the individual factors in the pre-

vious approach.

How would the net present value differ if the perceived project risk were greater?

The risk-averse management of Gazza would probably require a higher return from

the project, reflected in a higher discount rate. Let us repeat the exercise using 13 per

cent (average risk) and 16 per cent (high risk).

Using 13 per cent:

Using 16 per cent:

Looking at the net present values, what interpretation can be made? With a 10 per

cent discount rate, the project offers a positive NPV of £413. If the projected cash flows

are generally expected to be achieved, the market value of the firm should rise by £413.

Hence, the project should be accepted. On the other hand, if the project is classified as

high risk, the cash inflows are discounted at a rate of 16 per cent and the NPV is esti-

mated at Its acceptance would reduce the firm’s market value by £369. Hence,

the project should not be accepted. Clearly, it would not be wise to exchange £10,000

today for future cash flows having a present value of less than this amount.

If the project is classified as having average risk, the discount rate used is 13 per

cent, yielding an NPV of £8. The project is just acceptable; it yields 13 per cent, which

is the required rate of return. We can draw two important conclusions:

£369.

13692

NPV 1£6,000 1.60522 £10,000

£8 1i.e. approximately zero2

1£6,000 1.66812 £10,000

NPV 1£6,000 PVIFA

113,22

2 £10,000

£413

1£6,000 1.73552 £10,000

NPV 1£6,000 PVIFA

110,22

2 £10,000

£413

£5,454 £4,959 £10,000

NPV

£6,000

1.1

£6,000

11.12

2

£10,000

CFAI_C03.QXD 10/26/05 11:11 AM Page 75

.

76 Part I A framework for financial decisions

Self-assessment activity 3.7

Why should managers seek to maximise net present value? Is business not about maximis-

ing profit?

(Answer in Appendix A at the back of the book)

1 Project acceptability depends upon cash flows and risk.

2 The higher the risk of a given set of expected cash flows (and the higher the dis-

count rate), the lower will be its present value. In other words, the value of a given

expected cash flow decreases as its risk increases.

■ Why NPV makes sense

In Appendix II to this chapter, we examine more rigorously the rationale for the NPV

approach and how the net present value concept permits efficient separation of owner-

ship and corporate management.

The main rationale for the net present value approach may be summarised as follows:

1 Managers are assumed to act in the best interests of the owners or shareholders,

even if agency costs – in the form of incentives or controls – have to be incurred.

They seek to increase shareholders’ wealth by maximising cash flows through time.

The market rate of exchange between current and future wealth is reflected in the

current rate of interest.

2 Managers should undertake all projects up to the point at which the marginal

return on the investment is equal to the rate of interest on equivalent financial

investments in the capital market. This is exactly the same as the net present value

rule: accept all investments offering positive net present values when discounted at

the equivalent market rate of interest. The result is an increase in the market value

of the firm and thus in the market value of the shareholders’ stake in the firm.

3 Management need not concern itself with shareholders’ particular time patterns of

consumption or risk preferences. In well-functioning capital markets, shareholders

can borrow or lend funds to achieve their personal requirements. Furthermore, by

carefully combining risky and safe investments, they can achieve the desired risk

characteristics for those consumption requirements. This argument is discussed

more fully in Appendix II.

How NPV is used in debt relief to the poorest nations

The International Monetary Fund (IMF) and World Bank

have designed a framework to provide special assistance

for heavily indebted poor countries. It entails coordinated

action by the international financial community, including

banks and multinational companies, to reduce and

reschedule the debt burden to levels that countries can

service through exports and aid.

Net present value is central to the calculation of the sus-

tainable debt level. The face value of debt stock is not a

good measure of a country’s debt burden if a significant

part of it is contracted on concessional terms, for example

with an interest rate below the prevailing market rate. The

net present value of debt is used to find the sum of all

future debt-service obligations (interest and principal) on

existing debt, discounted at the market interest rate.

Whenever the interest rate on the loan is lower than the

market rate, the resulting NPV of debt is smaller than its

face value, with the difference reflecting the grant element.

Question

Explain to a government official from one of the

world’s poorest countries why the NPV approach is an

appropriate method for calculating the sustainable

debt level.

MINI CASE

CFAI_C03.QXD 10/26/05 11:11 AM Page 76

.

Chapter 3 Present values and financial arithmetic 77

We have examined the meaning of wealth and its fundamental importance in financial

management. Given that, for most capital projects, there is a time-lag between the ini-

tial investment outlay and the receipt of benefits, consideration must be given to both

the timing and size of the costs and benefits. Whenever there is an alternative oppor-

tunity to use funds committed to a project (e.g. to invest in the capital market or in

other capital projects), cash today is worth more than cash received tomorrow.

Key points

■ Money, like any other scarce resource, has a cost. We allow for the time-value of

money by discounting. The higher the interest cost for a future cash flow, the lower

its present value.

■ Discount tables take away much of the tedium of discounting – but computer

spreadsheets eliminate it altogether.

■ Standard discount factors are:

present value interest factor,

present value interest factor for an annuity.

Conventional shorthand is:

Interest factor (rate of interest, number of years)

e.g. reads ‘the present value interest factor for an annuity at 10 per cent

for three years’.

■ The term structure of interest rates shows how yields on bonds vary as the dura-

tions of loans increase.

■ The net present value (NPV) of a project is found by first discounting a project’s

future net cash flows at the minimum required rate of return for the project; and

then deducting the initial investment outlay from the total present values over the

project’s life.

■ Where the corporate goal is to maximise the wealth of its shareholders, the simple

decision rule is:

When the NPV is positive, accept the investment.

When the NPV is negative, reject the investment.

PVIFA

110,32

PVIFA the

PVIF the

SUMMARY

Further reading

The work of Hirshleifer (1958) and Tobin (1958) provides the background to the approach

adopted in Appendix II. Early writers on discounted cash flow include Fisher (1930) and Dean

(1951).

Useful websites

Discounted cash flow: www.investopedia.com

Annual percentage rate: www.moneyextra.com

www.investinginbonds.com

CFAI_C03.QXD 10/26/05 11:11 AM Page 77

.

78 Part I A framework for financial decisions

Yield

(%)

‘Normal’ yield

curve

‘Inverted’ yield

curve

‘LONGS’‘SHORTS’ ‘MEDIUMS’

Years to maturity

05

10

15

Figure 3.3

The term structure of

interest rates

APPENDIX I

THE TERM STRUCTURE OF INTEREST RATES AND THE YIELD CURVE

We saw in Section 3.7 that the interest rate depends on a number of factors, one of

which is duration of the investment or loan. This is called the term structure of inter-

est rates. It shows how the yields offered for loans of different maturities vary as the

term of the loan increases.

Relating this to bonds issued by the state, or government stock, the term structure

shows the rate of return expected, or yield, by today’s purchaser of stock who plans to

hold to maturity, or redemption, i.e. when the stock will be repaid, or redeemed, by

the government. It also shows how the yield varies for different lengths of time to

maturity. In graphical terms, it is shown by a relationship called the Yield Curve.

Normally, we find that yields to maturity increase as the term increases. In other

words, rates of interest on ‘longs’ are higher than on ‘shorts’, as Figure 3.3 shows.

Notice that the relevant yield is the Gross Redemption Yield, which includes both

interest payments and any capital gain or loss at redemption.

By tradition, short-dated stocks, with up to further five years to maturity are called

shorts, mediums have between five and 15 years before repayment and longs will be

paid beyond 15 years. Notice that longs include a number of irredeemables or perpe-

tuities which quite literally will never be repaid but will attract interest forever. These

are also called undated stocks.

■ Explaining the shape of the Yield Curve

Three theories have been proposed to explain the shape of the Yield Curve – the

Expectations Theory, the Liquidity Preference Theory and the Market Segmentation

Theory. These are not mutually exclusive explanations – the influences incorporated in

each theory all tend to operate at any one time but with different degrees of pressure.

Sometimes, investors’ expectations (e.g. about future inflation) are predominant,

while, at other times, investors’ desire for liquidity may govern the shape of the curve.

Expectations theory

This theory asserts that investors’ expectations about future interest rates exert the

dominant influence. When the curve rises with years to maturity, this suggests that

Yield Curve

A graph depicting the relation-

ship between interest rates

and length of time to maturity

CFAI_C03.QXD 10/26/05 11:11 AM Page 78

.

Chapter 3 Present values and financial arithmetic 79

people expect interest rates to rise in the future. This is reflected in the relative

demand for short-dated and long-dated securities – investors expect to be able to earn

higher rates in the future so they defer buying long-dated stocks, preferring to invest

in shorts. This pushes up the price on shorts, and thus lowers the yields on them, and

conversely, for longer-dated stock.

Liquidity preference theory

Most investors, being risk-averse, prefer to hold cash rather than securities – cash

is effectively free of risk (although banks do go bust!), while even the shortest-

dated government stocks carry a degree of risk. Here, by risk, we mean not the risk

of default, but the risk of not being able to find a willing buyer of the stock at an

acceptable price, i.e. liquidity risk. Consequently, investors need to be compensat-

ed for having to wait for the return of their money. Preference for liquidity now,

and risk avoidance, thus explains the shape of the yield curve. The longer the time

to maturity, the greater the risk of illiquidity and the higher the compensation

required.

Market segmentation theory

In developed markets, there is a wide range of investors with different needs and time

horizons who, therefore, focus on different segments of the yield curve. For example,

some financial institutions, such as banks, are anxious to protect their ability to allow

investors to withdraw their deposits freely – for them, shorts are very attractive as they

need liquidity. Conversely, pension funds have far longer-term liabilities and wish to

match the maturity stream of their assets to these quite predictable liabilities. For

them, longs are more suitable.

According to this view, the ‘short’ market is quite distinct from the ‘long’ market

and the two ends could behave quite differently under similar conditions. For

example, if the government is expected to be a net repayer of its debt in the future,

this suggests a shortage of longs. This is likely to increase the demand for those

stocks presently available and thus reduce their yields. This would explain the case

of the ‘inverted’ i.e. downward-sloping, yield curve, shown by the red line in Figure

3.3.

In Chapter 16, we will examine how firms can use the information contained in the

yield curve for their financial planning.

APPENDIX II

THE INVESTMENT–CONSUMPTION DECISION

■ Theoretical case for NPV

We have suggested that managers should base investment decisions on the net pres-

ent value criterion: accept all projects that offer a positive net present value. We will

now justify this claim by presenting the theoretical case for the NPV rule.

There are three fundamental financial decisions facing individuals and shareholders:

1 Consumption decisions: how much of my available resources should I spend on imme-

diate consumption?

2 Investment decisions: how much of the resources available should I forgo now in the

expectation of increased resources at some time in the future? How should such

decisions be made?

CFAI_C03.QXD 10/26/05 11:11 AM Page 79

.

80 Part I A framework for financial decisions

3 Financing decisions: how much cash should I borrow or lend to enable me to carry

out these investment and consumption decisions?

Clearly, these decisions are interrelated and should not be viewed in isolation.

Individuals are faced with the choice of how much of their wealth should be con-

sumed immediately, and how much should be invested for consumption at a later

date. This applies equally to young children with their pocket money, undergraduates

with their grants, professionals with their capital, and shareholders with their invest-

ment portfolios. All these cases involve a trade-off between immediate and delayed

consumption.

We are primarily concerned with how managers should reach investment decisions.

Cash generated from business operations can be utilised in two ways: it can be dis-

tributed to the shareholders in the form of a dividend, or reinvested within the busi-

ness. Periodically, the directors decide how much of the shareholders’ wealth to

distribute in the form of dividends and how much to withhold for investment pur-

poses, such as building up stock levels or purchasing new equipment. The sharehold-

ers will only be willing to forgo a higher present level of consumption (in the form of

dividends) if they expect an even greater future level of consumption. This willingness

to give up consumption now in order to increase future consumption characterises

investment decisions.

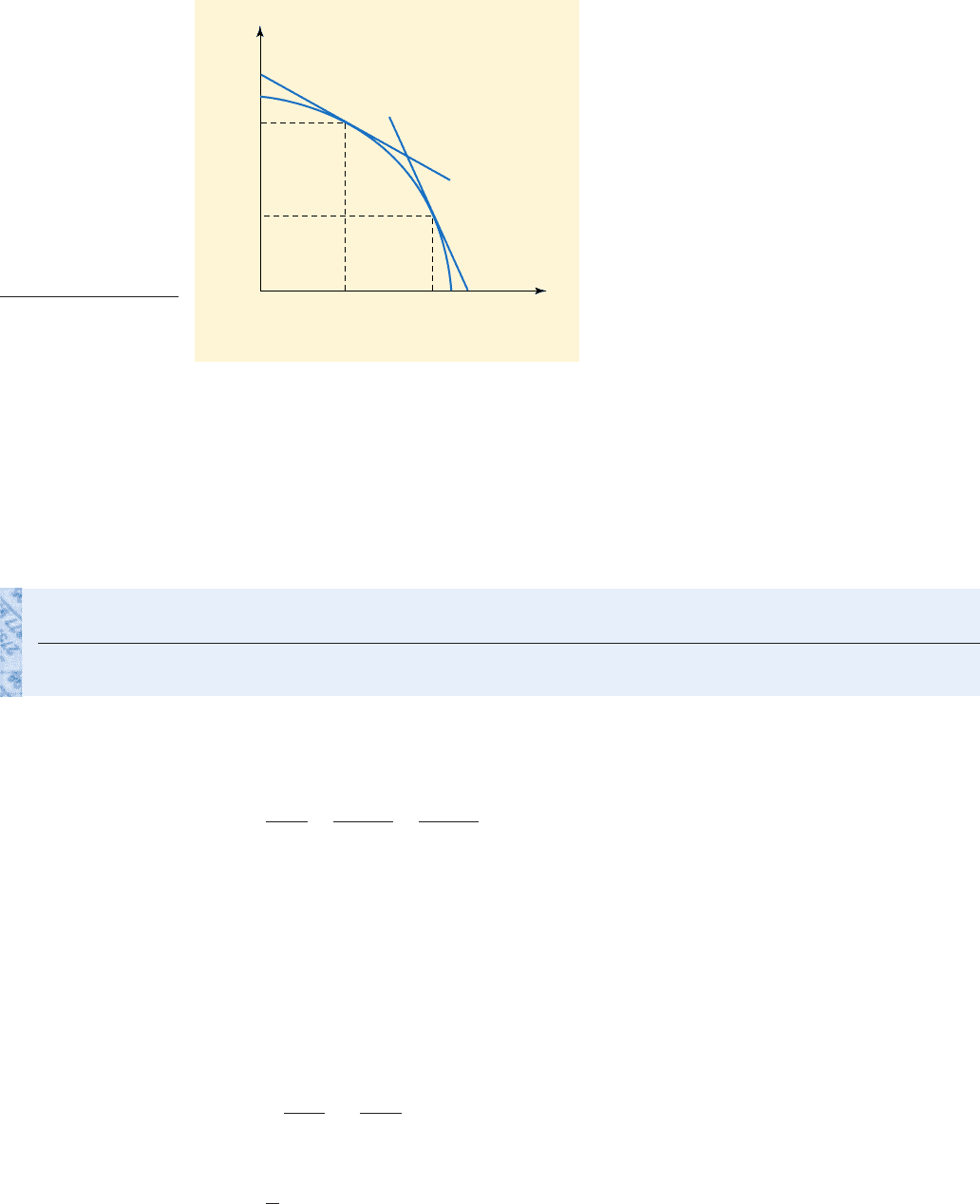

■ Graphical example

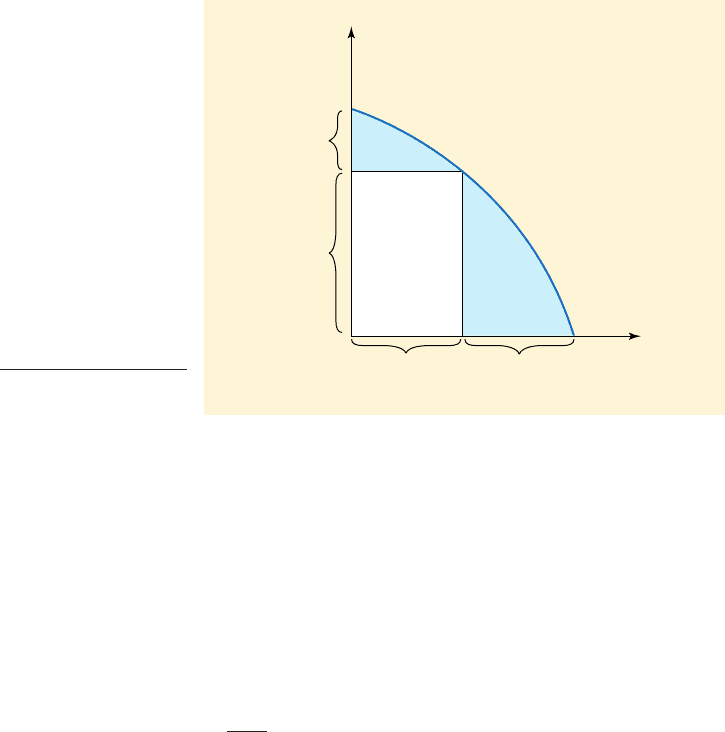

Derek Platt is the sole proprietor of Platt Enterprises, a new business with just one

asset of £4 million in cash. He has a number of interesting investment ideas (all lasting

just a year), but before investing his capital within the business, he asks the following

key questions:

1 What return could I earn by investing my capital (or some part of it) in the capital

market?

2 How much should I invest within the business?

3 What is the net present value of the business?

Before addressing these issues and in order to present a conceptual framework for

the NPV rule, it is first necessary to make certain simplifying assumptions that allow

us to portray in two-dimensional form the essential features of the investment–

consumption decision model. The basic assumptions are as follows:

1 Investors are wealth-maximisers.

2 Only two periods are considered – the present period and the next period

This two-period model implies that investments involve an immediate cash outlay

in in return for a cash benefit in the following period,

3 All information for decision-making is known with certainty.

4 Investment projects are entirely independent of each other and are divisible.

These assumptions are clearly unrealistic in the setting within which investment

decisions are taken in practice. Nonetheless, they serve as a useful guide to the rele-

vance and limitations of the net value approach.

Let us assume that Platt Enterprises has £4 million available for investment but

there are only two possible projects, each costing £2 million and having a one-year life.

Figure 3.4 illustrates the investment opportunities line for the two projects, showing

the cost of investing this year and the payoffs arising next year. Platt could invest

£4 million, in both projects, producing a £4 million payoff next year. But he would

probably prefer to invest only in project A, costing £2 million, but giving a payoff of

£3 million. Project B is unprofitable, offering only £1 million from £2 million invest-

ment. If there are no opportunities to invest surplus cash externally, say by putting it

t

1

.t

0

1t

1

2.1t

0

2

CFAI_C03.QXD 10/26/05 11:11 AM Page 80

.

Chapter 3 Present values and financial arithmetic 81

on deposit with a bank or investing in short-term securities, Platt would have to pay

a dividend to shareholders of the £2 million unused cash.

In this example, the choice was fairly straightforward. But if Platt had hundreds of

potential projects, it would be far harder to know where the cut-off point for investment

should be drawn. He requires a criterion for judging between cash today and cash

receivable next year. In effect, he requires a rate of exchange for the transfer of wealth

across time. Suppose he requires a minimum of £115 receivable next year to induce him

to give up £100 now, the rate of exchange would be This rep-

resents a premium for delayed consumption of one year of

This exchange rate between today’s money and tomorrow’s money varies with the

level of present consumption sacrificed. Platt may be willing to forgo the first £100 of

potential dividend in return for an additional 15 per cent next year, but to persuade

him to delay the consumption of a further £100 will probably require something in

excess of 15 per cent. This variable exchange rate for the transfer of wealth across time

at various levels of investment is termed the marginal rate of time preference, and dif-

fers from individual to individual.

The investment opportunities line is concave to the origin rather than a straight

line. This indicates the decreasing returns to scale of each subsequent investment

opportunity. As a wealth-maximiser, Platt will first select those investment projects

offering the greatest return and work down towards those offering the least return.

Point C represents the marginal project beyond which it ceases to be worthwhile to

invest – the marginal return from the next £1 in investment would not be sufficient to

compensate for the sacrifice involved in giving up a further £1 in dividends. For Platt,

C represents the point where the marginal return on investment equals his marginal

rate of time preference.

■ Borrowing and lending opportunities

So far, under our highly simplistic assumptions, our owner-manager, Platt, is given

only two decisions – consumption and investment. The more he invests, the less he can

consume now, and vice versa. This ignores the third choice open to him, namely the

£115

£100

1 0.15,

or

15%

£115

t

0

: £100

t

1

or £1.15 : £1.

Period 0 (£m)

4

A

2

B

0

A

3

B

4

Investment outlay

Investment opportunities

line

Investment

payoff

Period 1 (£m)

C

Figure 3.4

Investment opportuni-

ties for Platt Enterprises

CFAI_C03.QXD 10/26/05 11:11 AM Page 81

.

82 Part I A framework for financial decisions

financing decision. Where capital markets exist, individuals and firms can buy and sell not

only real assets (i.e. fixed and current), but also financial assets. As we saw earlier in this

chapter, when perfect capital markets are introduced (i.e. no borrower can influence the

interest rate, all traders have equal and costless access to information, no transaction costs

or taxes), there will be a single market rate of interest for both borrowing and lending.

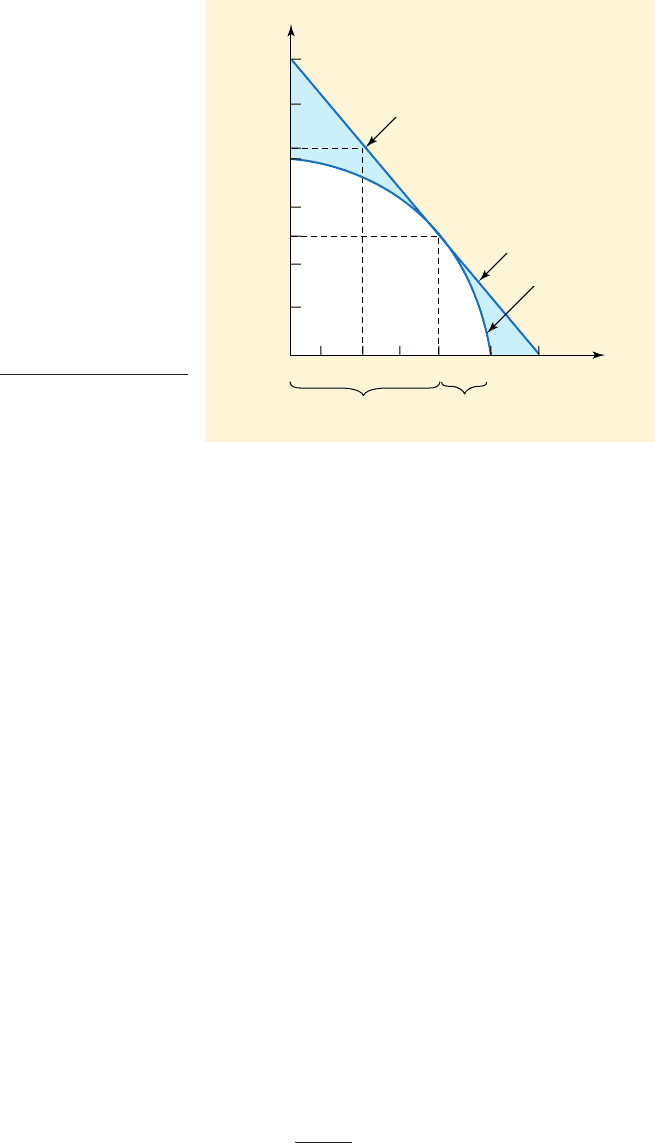

The existence of a capital market permits owners to transfer wealth across time in a

manner different from the investment–consumption pattern of the firm. This is shown

by the interest rate line in Figure 3.5, which represents the exchange rate between cur-

rent and future cash flows under perfect capital market conditions. Its slope is

where i denotes the single period rate of interest.

In our example, the interest rate is found by relating present wealth to next year’s

wealth at any point on the graph. At the extremes, this is

The interest rate is therefore 20 per cent.

With the introduction of financing opportunities afforded by the capital market,

Platt can now identify the appropriate level of corporate investment. He should con-

tinue to invest until project M – where the interest rate line is tangential to the invest-

ment opportunities line. At this point, all investments offering a return at least as

high as the market rate of interest are accepted, since they all offer positive net pres-

ent values. Reading off the graph in Figure 3.5, we find that investment as far as M

would mean a dividend of £3 million today and an investment of £1 million (i.e.

). It is not worth investing further as the projects offer negative

NPVs. It would be more beneficial for Platt to withdraw the £3 million from the busi-

ness and to invest it in the capital market at 20 per cent p.a.

What then is the net present value of the £1 million investment programme envisaged

by Platt? Reading off the investment opportunities curve, we find that the capital outlay

will produce cash flows of £2.4 million next year. The NPV is therefore £1 million:

The new value of the business becomes £5 million (starting capital of £4 million plus

NPV of investment programme).

We suggested earlier that the £3 million not invested by the firm would be paid

out as a dividend. An alternative would be for the firm to invest all or part of it on

behalf of the owners in the capital market until such time as investment opportunities

NPV

£2.4 m

1.2

£1 m £2 m £1 m £1 m

£4 million £3 million

£6 million>£5 million 1.20.

11 i2,

Owner’s consumption

requirement

Interest rate

Investment

opportunities

Today (£ million)

InvestDividend

0 1.0

1.5

2.0 3.0 4.0 5.0

6.0

Next year (£ million)

M

5.0

4.2

4.0

3.0

2.4

2.0

1.0

Figure 3.5

Investment and financ-

ing opportunities for

Platt Enterprises

CFAI_C03.QXD 10/26/05 11:11 AM Page 82

.

Chapter 3 Present values and financial arithmetic 83

offering positive NPVs arise. Suppose Platt is only looking for a dividend of £1.5 mil-

lion. The extra £1.5 million can be invested in the capital market to earn £1.8 million

next year (i.e. or ). Platt’s cash flow next year will then

be the £2.4 million from capital investments plus the £1.8 million from financial

investments.

■ Separating ownership from management

Most firms are characterised by a large number of shareholders (owners), few of

whom are actively involved in the management of the firm. It is obviously impossi-

ble for managers to evaluate investment decisions on the basis of the personal

investment–consumption preferences of all the shareholders. Happily, the existence of

capital markets renders any such attempt unnecessary. Managers do not need to select

an investment programme whose cash flows exactly match shareholders’ preferred

time patterns of consumption. The task of the manager is to maximise present value

by accepting all investment proposals offering a return at least as good as the market

rate of interest.

This criterion maximises the current wealth of the shareholders, who can then

transform that wealth into whatever time pattern of consumption they require. They

can do this by lending or borrowing on the capital market until their marginal rate of

time preference equals the capital market rate of interest. This Separation Theorem, as it

is usually termed, leads to the following decision rules:

1 Corporate management should invest in projects offering positive net present val-

ues when discounted at the capital market rate.

2 Shareholders should borrow or lend on the capital market to produce the wealth dis-

tribution which best meets their personal time pattern of consumption requirements.

■ Capital market imperfections

Based on the assumptions laid down at the start of the chapter, managers should

undertake investments up to the point at which the marginal return on investment is

equal to the rate of return in the capital market. You will recall that two important

assumptions were the existence of perfect capital markets and the absence of risk.

When these assumptions are relaxed, the argument in favour of the net present value

rule becomes weaker. For one thing, there is no longer a unique rate of interest in the

capital market, but a range of interest rates varying with the status of the borrower, the

amount required and the perceived riskiness of the investment. A detailed analysis of

investment under risk is the subject of subsequent chapters, but at this stage we can

say that a project’s return should be compared with the rate of return on investments

in the capital market of equivalent risk – the greater the investment risk, the higher the

required rate of return.

A major concern involves the particular capital market imperfections where the

borrowing rate is substantially higher than the lending rate. In this case, the two-period

investment model will resemble Figure 3.6. The steeper line represents the interest

rate for the borrower and the flatter line represents the lending rate. The existence

of two different interest rates gives rise to two different points on the investment

opportunities line CD. Prospective borrowers, having to pay a higher rate of interest

for funds, would prefer the company to invest only BD this year (i.e. up to project Y).

However, prospective lenders will require the company to discount at the lower lend-

ing rate, leading to a much greater investment of AD, with investment X being the

marginal project.

£1.5 m 1.20£4.2 m £2.4 m,

CFAI_C03.QXD 10/26/05 11:11 AM Page 83

.

84 Part I A framework for financial decisions

There is no simple solution to the investment–consumption decision when capital

market imperfections prevail. Fortunately, in the UK, USA, Japan and much of Western

Europe, capital markets are highly competitive and function fairly well, so that differ-

ences between lending and borrowing rates are minimised, but significant differentials

can be found in emerging capital markets such as that in Turkey.

■ Formula for the present value of a perpetuity

This formula derives from the present value formula:

Let and We now have:

(i)

Multiplying both sides by b gives us:

(ii)

Subtracting (ii) from (i) we have:

Substituting for a and b,

Multiplying both sides by and rearranging, we have:

PV

X

i

11 i2

PV¢1

1

1 i

≤

X

1 i

PV11 b2 a

PVb a1b b

2

b

3

p

2

PV a11 b b

2

p

2

1>11 i2 b.X>11 i2 a

PV

X

1 i

X

11 i2

2

X

11 i2

3

p

Lending

rate

Borrowing rate

Period 0 (£)

Period 1 (£)

C

X

Y

0

ABD

Figure 3.6

Investment decisions

in imperfect capital

markets

APPENDIX III

PRESENT VALUE FORMULAE

CFAI_C03.QXD 10/26/05 11:11 AM Page 84