Pike Robert, Neal Bill. Corporate finance and investment: decisions and strategy

Подождите немного. Документ загружается.

.

Chapter 2 The financial environment 35

any risk. In an efficient market, arbitrage activity will continue until the price dif-

ferential is eliminated.

■ The Efficient Market Hypothesis (EMH)

Information can be classified as historical, current or forecast. Only current or histori-

cal information is certain in its effect on price. The more information that is available

the better the situation. Informed decisions are more likely to be correct, although the

use of inside information to benefit from investment decisions (insider dealing) is ille-

gal in the UK.

Company information is available both within and without the organisation.

Those within the organisation will obviously be better informed about the state of the

business. They have access to sensitive information about future investment projects,

contracts under negotiation, forthcoming managerial changes, etc. The additional

knowledge will vary according to a person’s level of responsibility and place in the

organisational hierarchy.

Outsider investors fall into two categories: individual investors and the institutions.

Of these two groups, the institutions are the better informed, as they have greater

access to senior management, and may be represented on the board of directors.

Different amounts of financial information are available to different groups of peo-

ple. There is unequal access to the information, called ‘information asymmetry’, which

may affect a company’s share price. If you are one of the well-informed, this gives you

the opportunity to keep one step ahead of the market. Otherwise, you may lose out.

The share price reflects who knows what about the company. You should note, how-

ever, that in the UK, share dealings by company directors are tightly circumscribed; for

example, they can only buy and sell at specific times, and details of all such trades

must be publicly disclosed.

Market efficiency evolved from the notion of perfect competition, which assumes

free and instantly available information, rational investors and no taxes or transaction

costs. Of course, such conditions do not exist in capital markets, so just how do we

assess their level of efficiency? Market efficiency, as reflected by the Efficient Markets

Hypothesis (EMH), may exist at three levels:

1 The weak form of the EMH states that current share prices fully reflect all informa-

tion contained in past price movements. If this level of efficiency holds, there is no value

in trying to predict future price movements by analysing trends in past price move-

ments. Efficient stock market prices will fluctuate more or less randomly, any

departure from randomness being too expensive to determine. Share prices are said

to follow a random walk.

2 The semi-strong form of the EMH states that current market prices reflect not only

all past price movements, but all publicly available information. In other words, there

is no benefit in analysing existing information, such as that given in published

accounts, dividend and profits announcements, appointment of a new chief execu-

tive or product breakthroughs, after the information has been released. The stock

market has already captured this information in the current share price.

3 The strong form of the EMH states that current market prices reflect all relevant

information – even if privately held. The market price reflects the ‘true’ or intrinsic

value of the share based on the underlying future cash flows. The implications of

such a level of market efficiency are clear: no one can consistently beat the market

and earn abnormal returns. Few would go so far as to argue that stock markets are

efficient at this level.

You will have noticed that as the EMH strengthens, the opportunities for profitable

speculation reduce. Competition between well-informed investors drives share prices

to reflect their intrinsic values.

weak form

A weak-form efficient share

market does not allow investors

to look back at past share price

movements and identify clear,

repetitive patterns

semi-strong form

A semi-strong efficient share

market incorporates newly

released information accurately

and quickly into the structure

of share prices

strong form

In a strong-form efficient share

market, all information includ-

ing inside information is built

into share prices

CFAI_C02.QXD 10/28/05 2:19 PM Page 35

.

36 Part I A framework for financial decisions

■ The EMH and fundamental and technical analysis

Investment analysts who seek to determine the intrinsic worth of a share based on

underlying information undertake fundamental analysis. The EMH implies that funda-

mental analysis will not identify under-priced shares unless the analyst can respond

more quickly to new information than other investors, or has inside information.

Chapter 4 adopts a fundamental analysis approach in its examination of share valuation.

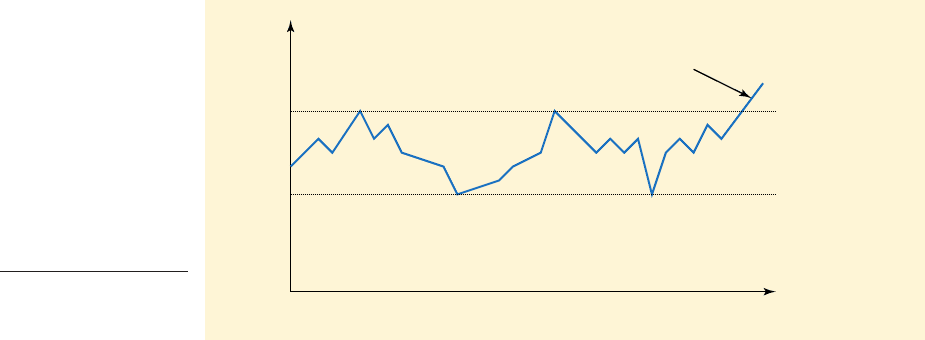

Another approach is technical analysis, its advocates being labelled chartists

because of their reliance upon graphs and charts of price movements. Chartists are not

interested in estimating the intrinsic value of shares, preferring to develop trading

rules based on patterns in share price movement over time, or ‘breakout’ points of

change. Charts are used to predict ‘floors’ and ‘ceilings’, marking the end of a share

price trend. Figure 2.2 shows how charts are used to detect patterns of ‘resistance’ (for

shares on the way up) and ‘support’ (for shares on the way down). This approach can

often prove to be a ‘self-fulfilling prophecy’. In the short term, if analysts predict that

share prices will rise, investors will start to buy, thus creating a bull market and result-

ing in upward pressure on prices.

Even in its weak form, the EMH questions the value of technical analysis; future price

changes cannot be predicted from past price changes. However, the fact that many ana-

lysts, using fundamental or technical analysis, make a comfortable living from their

investment advice, suggests that many investors find comfort in the advice given.

Considerable empirical tests on market efficiency have been conducted over

many years. In the USA and the UK, until the 1987 stock market crash, the evidence

broadly supported the semi-strong form of efficiency. More specifically, it suggests

the following:

1 There is little benefit in attempting to forecast future share price movements by analysing

past price movements. As the EMH seems to hold in its weak form, the value of charts

must be questioned.

2 For quoted companies that are regularly traded on the stock market, analysts are

unlikely to find significantly over- or under-valued shares through studying publicly held

information. Studies indicate (e.g. Ball and Brown 1968) that most of the information

content contained in annual reports and profit announcements is reflected in share

prices anything up to a year before release of the information, as investors make

judgements based on press releases and other information during the year. However,

analysts with specialist knowledge, paying careful attention to smaller, less well-

traded shares, may be more successful. Equally, analysts able to respond to new

information slightly ahead of the market may make further gains. The semi-strong

form of the EMH seems to hold fairly well for most quoted shares.

time

Share

price

Resistance line

Support line

Breakout

Figure 2.2

Chart showing break-

out beyond resistance

line

intrinsic worth

The inherent or fundamental

value of a company and its

shares

fundamental analysis

Analysis of the fundamental

determinants of company

financial health and future per-

formance prospects, such as

endowment of resources, quali-

ty of management, product

innovation record, etc.

technical analysis

The detailed scrutiny of past

time series of share price move-

ments attempting to identify

repetitive patterns

chartists

Analysts who use technical

analysis

CFAI_C02.QXD 10/28/05 2:19 PM Page 36

.

Chapter 2 The financial environment 37

3 The strong form of the EMH does not hold, so superior returns can be achieved by

those with ‘inside knowledge’. However, it is the duty of directors to act in the share-

holders’ best interests, and it is a criminal offence to engage in insider trading for

personal gain. The fact that cases of insider trading have led to the conviction of sen-

ior executives shows that market prices do not fully reflect unpublished information.

Recent governments have encouraged greater market efficiency in several ways:

■ Stock market deregulation and computerised dealing have enabled speedier adjust-

ment of share prices in response to global information.

■ Mergers and takeovers have been encouraged as ways of improving managerial

efficiency. Poorly performing companies experience depressed share prices and

become candidates for acquisition.

■ Governments have seen privatisation of public utilities as a means of subjecting

previously publicly-owned organisations to market pressures.

How people trade in London

The Big Bang in 1986 gave the London Stock Exchange a huge advantage over most of

its competitors. The result was strong growth in trading activity and international par-

ticipation. But Big Bang was only a partial revolution – automating the distribution of

price information, but stopping short of automating the trading function itself.

Since 1986, global equity markets have become increasingly complex, with investors

constantly looking for greater choice and lower costs. The London Stock Exchange

made various attempts to retain its reputation as one of the most efficient stock mar-

kets. In 1997, it took a major step by moving from a quote-based trading system, under

which share dealing is conducted by telephone, to order-driven trading, termed SETS –

the Stock Exchange Electronic Trading Service. The aim was to improve efficiency and

reduce costs by automating trading and narrowing the spread between buying and sell-

ing prices. This it achieves by the automatic matching of orders placed electronically by

prospective buyers and sellers.

The system, which initially only applies to heavily traded shares, works as follows.

Instead of agreeing to trade at a price set by a market maker, prospective buyers and

sellers can:

(a) advertise through their broker the price at which they would like to deal, and wait

for the market to move, or

(b) execute immediately at the best price available.

An investor wishing to buy or sell will contact his or her broker and agree a price

at which the investor is willing to trade. The broker enters the order in the order book,

which is then displayed to the entire market along with other orders. Once the order

is executed, the trade is automatically reported to the Exchange. Time will tell whether

it does lead to greater efficiency, but it is hoped that it will offer users more attractive,

transparent and flexible trading opportunities.

Heads, shoulders and broadening bottoms

The popularity of business television channels such as CNBC has done wonders for the careers

of Wall Street’s technical analysts, who claim to be able to predict future share prices by spot-

ting trends in past prices. Their market charts, showing descriptively named patterns such as

‘head and shoulders’ – a big peak surrounded by two smaller peaks – or ‘broadening bottoms’ –

a series of troughs, each lower than the preceding one – make ideal graphics for television

Continued

CFAI_C02.QXD 10/28/05 2:19 PM Page 37

.

38 Part I A framework for financial decisions

■ Implications of market efficiency for corporate managers

In quoted companies, managers and investors are directly linked through stock mar-

ket prices, corporate actions being rapidly reflected in share prices. This indicates the

following:

1 Investors are not easily fooled by glossy financial reports or ‘creative accounting’

techniques, which boost corporate reported earnings but not underlying cash flows.

2 Corporate management should endeavour to make decisions that maximise share-

holder wealth.

3 The timing of new issues of securities is not critical. Market prices are a ‘fair’ reflec-

tion of the information available and accurately reflect the degree of risk in shares.

4 Where corporate managers possess information not yet released to the market,

there is an opportunity for influencing prices. For example, a company may retain

information so that, in the event of an unwelcome takeover bid, it can offer positive

signals.

producers in need of something pretty for viewers to watch while the glamorous reporters are

busy off-camera, catching up on the latest market gossip. The simple trading advice conveyed

by charts is, for CNBC’s stock-tip-hungry viewers, manna from heaven.

But technical analysis is not merely for gullible CNBC-watchers. It has been around a long

time, dating back a century to Charles Dow, the founder of Dow Jones, who invented the ‘Dow

theory’ for identifying trends in share prices. Charts are used by some of the world’s most suc-

cessful investors.

Nevertheless, economists who study financial markets have long regarded technical analysis

as mumbo jumbo, bearing much the same relationship to rigorous economic ‘fundamental

analysis’ that astrology does to astronomy. Since the 1960s, economists have believed, more

or less, in ‘efficient-market theory’. In an efficient market, prices reflect all available informa-

tion, and so scouring past prices for patterns can tell you nothing useful about whether in

future prices will go up or down. Instead, prices will move unpredictably, in a ‘random walk’.

In the past decade some economists have challenged efficient-market theory, by finding

numerous examples of apparently predictable movements in share prices. But there is still a

fierce debate about whether these movements are predictable enough for investors to make

money trading on the basis of expected price changes. The evidence was described at length in

A Non-Random Walk Down Wall Street (Princeton University Press, 1999), a book by Craig

MacKinlay, of the Wharton School, and Andrew Lo, of the Massachusetts Institute of

Technology.

Mr Lo and two new co-authors have now come to the defence of technical analysis.* Using

American share prices during 1962–96, they investigated the predictive ability of five pairs of

widely-used technical patterns. The results showed that the various technical patterns mostly

occurred far more frequently than they would have done if they were truly random events. The

most common patterns were double tops and bottoms – two peaks (or two troughs) at similar

prices to each other – followed by head and shoulders and inverted head and shoulders. In

general, the charts contained useful information about future share prices. The study does not

test whether this information was useful enough to allow investors to make sufficient profit

trading on it to justify the extra risk.

Since investors have been using charts for 100 years or so and they still seem to work, the

patterns may be so deeply ingrained that their predictive powers will persist come what may.

*‘Foundations of technical analysis’ by Lo, Mamaysky and Wang, Journal of Finance, August 2000.

Source: Based on The Economist, 19 August 2000.

CFAI_C02.QXD 10/28/05 2:19 PM Page 38

.

Chapter 2 The financial environment 39

Self-assessment activity 2.4

Consider why a dealing rule like ‘Always buy in early December’ should be doomed to fail-

ure. This rule is designed to exploit the so-called ‘end-of-year-effect’ claiming that share

prices ‘always’ rise at the end of the year.

(Answer in Appendix A at the back of the book)

■ Surfing towards greater stock market efficiency

One of the essential requirements of stock market efficiency is that all participants have

roughly equal access to price-sensitive information. In the past, the big players – with

online databases – were able to obtain information, and thereby enjoy a competitive

advantage, well before the small investors who may have had to rely on the daily news-

paper to keep abreast of recent events and price movements.

The Internet offers enormous scope for narrowing the information gap between big

and small market participants. This arises in various ways.

1 Company information. Electronic reporting of company information will result in a

significant enfranchisement of shareholders and enable greater accountability and

corporate governance. The electronic information revolution should also give rise

to a movement away from conventional accounting-based information to more

user-friendly shareholder information which focuses on the key determinants of

value. For example, customer satisfaction and market penetration may be regular

information as part of a ‘balanced scorecard’ performance measurement system.

Videos of AGMs, analysts’ presentations and information on ethical/environmen-

tal investment will become standard, enabling all investors to be kept up-to-date on

corporate progress.

2 Market information. There are already thousands of Web pages devoted to invest-

ment and personal finance information, much of which was hitherto only available

to professional users. Although a charge is made for real-time information, those

with share prices on a 20-minute delay are often free.

The following websites may be of interest:

Yahoo! (finance.yahoo.co.uk) focuses on providing share information for London,

Frankfurt and Paris, with links to the US exchanges.

Moneyworld (www.moneyworld.co.uk) covers a much wider range of financial serv-

ices as well as share prices.

The website of the Motley Fool (www.fool.co.uk) also ‘exists to educate, amuse and

enrich the individual investor’.

However much information efficiency may improve through surfing the Web’s

financial pages, remember that the market is renowned for its occasional catastrophic

share price waves, which few can predict and even fewer ride.

Self-assessment activity 2.5

Share prices of takeover targets invariably rise before the formal announcement of a

takeover bid. What does this suggest for the EMH?

(Answer in Appendix A at the back of the book)

CFAI_C02.QXD 10/28/05 2:19 PM Page 39

.

40 Part I A framework for financial decisions

■ Criticisms of the EMH

Michael Jensen, a leading financial economist, argued in 1978 that ‘the efficient markets

hypothesis is the best-established fact in all of social science’. Why then is the EMH

debate still hotly disputed? The main issue is whether investors react correctly to new

information or whether they make systematic errors by over- or under-reacting. The

overreaction hypothesis argues that share prices tend to overshoot the true value due

to excessive optimism or pessimism by investors in their initial reactions to new infor-

mation. There is some evidence for this in UK financial markets (Dissanaike 1997).

Much criticism of the EMH is misplaced because it is based on a misconception

of what the hypothesis actually says. For example, it does not mean that financial

expertise is of no value in stock markets and that a share portfolio might as well be

selected by sticking a pin in the financial pages. This is clearly not the case. It does

suggest, however, that in an efficient market, after adjusting for portfolio risk, fund

managers will not, on average, achieve returns higher than that of a randomly

selected portfolio. Roll (see Ross et al. 1991, p. 324) makes the point that publicly-

available information need not be reflected in share prices. Instead, the link

‘between unreflected information and prices is too subtle and tenuous to be easily

or costlessly detected’.

Market efficiency also suggests that share prices are ‘fair’ in the sense that they

reflect the value of that stock given the available information. So shareholders need not

be unduly concerned with whether they are paying too much for a particular share.

The fact that many investors have done very well through investing on the stock

market should not surprise us. For much of the last century, the market generated pos-

itive returns. Most investment advice, if followed over a long period of time, is likely

to have done well; the point is that, in efficient markets, investors cannot consistently

achieve above-average returns except by chance.

■ A few apparent anomalies in the EMH

There appear to be three main anomalies in the EMH; the effects of size and timing, and

the periodic emergence of ‘bubbles’.

Size effects

Market efficiency seems to be less in evidence among smaller firms. Shares of smaller

companies tend to yield higher average returns than those of larger companies of com-

parable risk. Dimson and Marsh (1986) found that in the UK, on average, smaller firms

outperformed larger firms by around 6 per cent per annum. Some of the difference can

be accounted for by the higher risk and trading costs involved in dealing with smaller

companies. Another explanation is institutional neglect. Financial institutions domi-

nating the stock market often neglect small firms offering what appear to be high

returns because the maximum investment is relatively small (if they are not to exceed

their normal 5 per cent maximum stake). The costs of monitoring and trading may not

warrant the sums involved.

Timing effects

In the longer term, disparities in share returns seem to correct themselves. A share per-

forming poorly in one year is likely to do well the following year. Seasonal effects have

also been observed. At the other extreme, it has been observed that share performance

is related to the day of the week or time of the day. Prices tend to rise during the last

fifteen minutes of the day’s trading, but the first hour of Monday trading is generally

characterised by heavy selling. Investors may evaluate their portfolios over the week-

end and decide what to sell first thing on Monday, but are more cautious in their buy-

ing decisions, preferring to take their broker’s advice.

overreaction hypothesis

The notion that although stock

markets are essentially efficient

in reacting to new information,

they initially over-react, perhaps

in anticipation of further

good/bad news

CFAI_C02.QXD 10/28/05 2:19 PM Page 40

.

Chapter 2 The financial environment 41

Stock market surges and bubbles

An investor holding a wide portfolio of shares (e.g. the FTA All-Share Index) for, say, 25

years, would have been rewarded handsomely. But the capital growth was not a steady

monthly appreciation; the bulk of it came in just a fraction of the investment period

through stock market surges. In an efficient market, few – if any – are clever enough to

be able to predict short-term stock market surges.

The famous South Sea Bubble of 1722 was one of the early speculative stock market

‘bubbles’ where investors adopt the ‘herd’ instinct and drive up prices well above any

rational valuation based on economic fundamentals. The economist J.M. Keynes

described this in terms of a ‘beauty contest’ where investors are not following their

own judgments but trying to guess how other investors are going to behave. The

Internet Bubble of 1999 shows that speculative bubbles are still with us and the cost of

following the trend can be considerable.

Black Monday

In October 1987, on ‘Black Monday’, share prices fell by 30 per cent or more on most of the

world’s stock markets. Had this collapse been triggered by some cataclysmic event, shareholders’

reactions could be easily explained as the efficient market reacting to new information. However,

Black Monday was not a reaction to external events, but rather a recognition that the prolonged

bull market had ended and that the speculative share price bubble had burst. This brings into

question the validity of the simple EMH, which implies that share prices cannot rise to the artifi-

cially high levels observed prior to the 1987 crash. The newly-introduced computer trading meth-

ods, which automatically sell shares when they fall below a predetermined level, were unable to

cope with such an adverse situation. It is now generally accepted that the EMH failed to explain

why the Dow Jones Industrials index plummeted 23 per cent in just a few hours.

This enigma has led to a re-evaluation of the simple EMH and the assumption that there is a

single ‘true’ value for shares; there may be a very wide range of plausible values. The EMH, if it

operates at all, does so in the weakest of forms and is most efficient when conditions are stable.

Black Monday’s crash adds credence to the Speculative Bubble theory. Stock market behav-

iour is based on inflating and bursting speculative bubbles, rather than fundamental analysis

based on new information. Investors buy shares because they believe that others will pay yet

more for them later, thus creating a bull market. Eventually, the bubble bursts and the market

corrects itself or crashes, depending on the size of the bubble.

Self-assessment activity 2.6

If the stock market is efficient, can no one beat the market average return?

(Answer in Appendix A at the back of the book)

2.6 A MODERN PERSPECTIVE – CHAOS THEORY

The EMH is based on the assertion that rational investors rapidly absorb new informa-

tion about a company’s prospects, which is then impounded into the share price. Any

other price variations are attributable to random ‘noise’. This implies that the market

has no memory – it simply reacts to the advent of each new information snippet, regis-

ters it accordingly and settles back into equilibrium; in other words, all price-sensitive

events occur randomly and independently of each other.

CFAI_C02.QXD 10/28/05 2:19 PM Page 41

.

42 Part I A framework for financial decisions

The crash of 1987, possibly attributed to the market’s realisation that shares were

over-valued and triggered by the collapse of a relatively minor management buy-out

deal, has provoked more detailed scrutiny of the pattern of past share prices. This

has uncovered evidence that share price movements do not always conform to a

‘random walk’. For example, significant downturns happen more frequently than

significant upturns.

A new branch of mathematics, chaos theory, has been harnessed to help explain

such features. Observations of natural systems such as weather patterns and river sys-

tems often give a chaotic appearance – they seem to lurch wildly from one extreme to

another. However, chaos theorists suggest that apparently random, unpredictable pat-

terns are governed by sets of complex sub-systems that react interdependently. These

systems can be modelled, and their behaviour forecast, but predictions of the behav-

iour of chaotic systems are very sensitive to the precise conditions specified at the start

of the estimation period. An apparently small error in the specification of the model

can lead to major errors in the forecast.

Edgar Peters (1991) has suggested that stock markets are chaotic in this sense.

Markets have memories, are prone to major price swings and do not behave entirely

randomly. For example, in the UK, he found that today’s price movement is affected

by price changes that occurred several years previously. The most recent changes,

however, have the biggest impact. In addition, he found that price moves were per-

sistent, i.e. if previous moves in price were upwards, the subsequent price move was

more likely to be up than down. Yet chaos theory also suggests that persistent

uptrends are also more likely ultimately to result in major reversals!

Peters’ work suggests that world stock markets exhibit patterns that are overlaid

with substantial random noise. The more noise, the less efficient the market. In this

respect, the US markets appear to be more efficient than those in the UK and Japan.

Other observers suggest that markets are essentially rational and efficient, but suc-

cumb to chaos on occasions, with bursts of chaotic frenzy being attributed to specula-

tive activity. This suggests some scope for informed insiders to outperform the market

during such periods.

Which view is right? Are stock markets efficient, chaotic or somewhere in between?

Pending the results of further research, it seems that corporate financial managers can-

not necessarily regard today’s market price as a fair assessment of company value, but

that the market may well correctly value a company over a period of years. Examination

of long-term trends gives more insight than consideration of short-term oscillations. For

example, if a company’s share price persistently underperforms the market, then per-

haps its profitability really is low, or its management poor, or it has failed to release the

right amount of information.

To conclude, it seems that the Efficient Markets Hypothesis does not hold, except

perhaps in its very weakest form, in today’s capital markets. Evolving from both the

EMH and chaos theory is a promising successor termed the Coherent Market

Hypothesis (CMH) based on a combination of fundamental factors and market senti-

ment or technical factors (see Vaga 1991). The CMH argues that capital markets are, at

any point in time, in one of the following states, depending on a combination of eco-

nomic fundamentals and ‘crowd behaviour’ in the market:

■ Random walks – market efficiency with neutral fundamentals

■ Unstable transition – market inefficiency with neutral fundamentals

■ Coherence – crowd behaviour with bullish fundamentals

■ Chaos – crowd behaviour with bearish fundamentals.

We will have to wait to see how well it helps explain stock market behaviour.

CFAI_C02.QXD 10/28/05 2:19 PM Page 42

.

Chapter 2 The financial environment 43

Self-assessment activity 2.7

List three important changes to the London Stock Exchange brought about by the ‘Big

Bang’ in 1986 and discuss their impact on market efficiency.

(Answer in Appendix A at the back of the book)

2.7 SHORT-TERMISM IN THE CITY

Pressure to perform well has not only led fund managers to increase their activity lev-

els in managing funds, but may also have led to a more short-term perspective regard-

ing capital investment. The argument is that fund managers focus on the short-term

performance of companies in arriving at a valuation of their worth, placing excessive

emphasis on current profit performance and dividend payments. Such apparent behav-

iour is said to have two consequences. First, management, in order to keep up the price

of its stock, will tend to focus on producing the short-term results that it thinks the mar-

ket wants to see. This results in management failing to undertake important long-term

investment in resources and research and development. Second, the volatility of short-

term corporate results will be exaggerated in securities markets, producing undesirable

fluctuations in stock prices.

This chain of argument gained support from a survey carried out by the

Department of Trade and Industry’s Innovation Advisory Board (1990), which sug-

gested the City placed too high a priority on short-term profits and dividends at the

expense of R&D and other innovative investment.

The argument was supported by a Confederation of British Industry (CBI) survey

of major companies in 1987, in which 35 per cent doubted that financial institutions

take a long-term and strategic evaluation of their companies. As a result, the CBI set

up a task force to investigate the whole issue. Its report concluded that many UK com-

panies have given insufficient weight to long-term development, but that this does not

arise primarily from City pressure. It arises mainly from underlying economic and

political factors, including inadequate profitability (Ferguson 1989).

The problem of short-termism has also been addressed by US researchers (e.g. Graves

1988), who argue that the increasing shareholder power of institutional investors has

had a damaging effect on R&D expenditure among US firms.

The EMH argues that rational investors will approve of any long-term investments

that make sound economic sense. They will not sell the stock of a fundamentally

sound firm undertaking long-term investments that promise remarkably high future

cash flows just because that firm has reported one bad trading period. Such short-term

stock shuttling is viewed as irrational behaviour.

The City rejects most allegations of short-termism, arguing that much of the respon-

sibility for the lack of long-term innovative investment is attributable to managers’

preference for growth by acquisition, their poor record of commercial development

and their reward systems based on short-term targets. This view is advocated by

Marsh (1990), who claims that:

There is no evidence that shares are priced in a way which emphasises their short- rather

than long-run prospects. Nor is there any evidence that the market penalises long-term

investments or expenditure on R&D by awarding the shares of the company in question

a lower rating – indeed, quite the contrary.

He identifies ‘managerial short-termism’ as a key force behind poor investment in

the UK. When it comes to making plans for the future, managers’ perceptions are

CFAI_C02.QXD 10/28/05 2:19 PM Page 43

.

44 Part I A framework for financial decisions

influenced by their organisational systems and contexts, including the way they are

remunerated and rewarded; their time-horizons within the jobs; the role played by the

internal performance measurement and management accounting systems; and the

internal capital budgeting and project appraisal systems.

There is broad consensus among all parties to the debate that action is required to

improve communication between the City and industry. Emerging very clearly from the

debate on short-termism is that UK companies need to improve the information they

provide to the capital markets on their R&D activity and other strategic investments if

they are to achieve a market rating appropriate to their future expected profitability.

2.8 READING THE FINANCIAL PAGES

Corporate finance is changing so quickly that it is essential for students of finance to

read the financial pages in newspapers on a regular basis. In this section, we explain the

main information contained in the Share Service pages of the Financial Times, and other

newspapers.

■ The FT-SE Index

Every day, shares move up or down with the release of information from within the

firm, such as a revised profits forecast, or from an external source, such as the latest

government statistics on inflation or unemployment. To indicate how the whole share

market has performed, a share index is used, the most common being the FT-SE 100 –

familiarly known as ‘Footsie’. This index is based on the share prices of the 100 most

valuable UK quoted companies, (sometimes termed ‘blue chips’) mostly those with

capitalisations above £3 billion, with each company weighted in proportion to its total

market value. All the world’s major stock markets have similar indices (for example,

the Nikkei index in Japan, the Dow Jones index in the USA and the CAC-40 in France).

Every share index is constructed on a base date and base value. The FT-SE 100 start-

ed with a base value of 1000 at the end of 1983. By January 2005, the index stood at

around 4,800. Despite the collapse in world markets in 2000, and the subsequent slow

recovery in confidence (punctuated by a fresh collapse at the time of the Iraq war), this

still represented an annual compound growth rate of about 8 per cent, well above both

the rate of inflation and the yield on low-risk investments over the same period.

Moreover, it includes only capital appreciation – inclusion of dividend income would

raise this percentage to about a 12 per cent return.

The FT-SE Actuaries Share Indices reveal share movements by sector. Their total

gives the All-Share Index, representing the more frequently traded quoted companies,

and between 98 and 99 per cent of market capitalisation.

Other FT indices

In recent years, the Stock Exchange has introduced several new indices.

■ FT-SE 250 covers medium-sized companies too small to enter the FT-SE 100, with

capitalisations in the range £350 million to £3 billion, and accounting for some 14

per cent of UK market capitalisation. It is calculated both including and excluding

investment trusts.

■ FT-SE Actuaries 350 provides the benchmark for investors who wish to focus on the

more actively traded large and medium-sized UK companies, and covers 95 per

cent of trading by value. It thus combines the FT-SE 100 and the FT-SE 250.

■ FT-SE Small Cap offers investors a daily measure of the performance of about 500

smaller companies, accounting for about 2 per cent of market capitalisation.

Whereas the previous indices are calculated continuously, this is computed only at

the close of trading.

CFAI_C02.QXD 10/28/05 2:19 PM Page 44