Pike Robert, Neal Bill. Corporate finance and investment: decisions and strategy

Подождите немного. Документ загружается.

.

Chapter 2 The financial environment 25

The corporate financial manager has the important task of ensuring that there are

sufficient funds available to meet all the likely needs of the business. To do this prop-

erly, he or she requires a clear grasp both of the future financial requirements of the

business and of the workings of the financial markets. This chapter provides an

overview of these markets, and the major institutions within them, paying particular

attention to the Stock Exchange.

2.1 INTRODUCTION

2.2 FINANCIAL MARKETS

A financial market is any mechanism for trading financial assets or securities.

Frequently, there is no physical market-place, transactions being conducted via tele-

phone or computer. London is widely regarded as the pre-eminent European financial

centre and certainly is the largest by volume of dealing. Its main financial markets are

as follows:

1 The money market channels wholesale funds, usually for less than one year, from

lenders to borrowers. The market is largely dominated by the major banks and

other financial institutions, but local government and large companies also use it for

short-term lending and borrowing purposes.

2 The securities or capital market deals with long-dated securities such as shares and

loan stock. The London Stock Exchange is the best-known institution in the capital

market, but there are other important markets, such as the bond market (for long-

dated government and corporate borrowing) and the Eurobond market.

3 The foreign exchange market is a market for buying and selling one currency

against another. Deals are either on a spot basis (for immediate delivery) or on a

forward basis (for future delivery).

4 The London International Financial Futures and Options Exchange (LIFFE)

www.liffe.com provides various means of hedging (i.e. protecting) or speculating

against movements in currencies and interest rates. These are called derivatives

because they are derived from the underlying security. A future is an agreement to

buy or sell an asset (e.g. foreign currency, shares etc.) at an agreed price at some

future date. An option is the right, but not the obligation, to buy or sell such assets

at an agreed price at, or within, an agreed time period. LIFFE is now part of

Euronext.liffe after it was taken over in 2001 by Euronext, the operator of the linked

Amsterdam, Brussels and Paris stock exchanges. As a result, their derivatives trad-

ing, along with that of the Lisbon exchange, have been brought together into one

integrated market, another reflection of the ever-increasing globalisation of finan-

cial markets.

The financial markets provide mechanisms through which the corporate financial

manager has access to a wide range of sources of finance and instruments.

Capital markets function in two important ways:

1 Primary market – providing new capital for business and other activities, usually in

the form of share issues to new or existing shareholders (equity), or loans.

2 Secondary market – trading existing securities, thus enabling share or bond holders

to dispose of their holdings when they wish. An active secondary market is a nec-

essary condition for an effective primary market, as no investor wants to feel

‘locked in’ to an investment that cannot be realised when desired.

Imagine what business life would be like if these capital markets were not available

to companies. New businesses could start up only if the owners had sufficient per-

sonal wealth to fund the initial capital investment; existing businesses could develop

financial market

Any market in which financial

assets and liabilities are traded

money market

The market for short-term

money, broadly speaking for

repayment within about a year

securities/capital market

The market for long-term

finance

spot

The spot, or cash market, is

where transactions are settled

immediately

forward

The forward market is where

contracts are made for future

settlement at a price specified

now

derivatives

Securities that are traded sepa-

rately from the assets from

which they are derived

future

A tradable contract to buy or

sell a specified amount of an

asset at a specified price at a

specified future date

option

The right but not the obligation

to buy or sell a particular asset

CFAI_C02.QXD 10/28/05 2:19 PM Page 25

.

26 Part I A framework for financial decisions

only through re-investing profits generated; and investors could not easily dispose of

their shareholdings. In many parts of the world where financial markets are embry-

onic or even non-existent, this is exactly what does happen. The development of a strong

and healthy economy rests very largely on efficient, well-developed financial markets.

Financial markets promote savings and investment by providing mechanisms

whereby the financial requirements of lenders (suppliers of funds) and borrowers

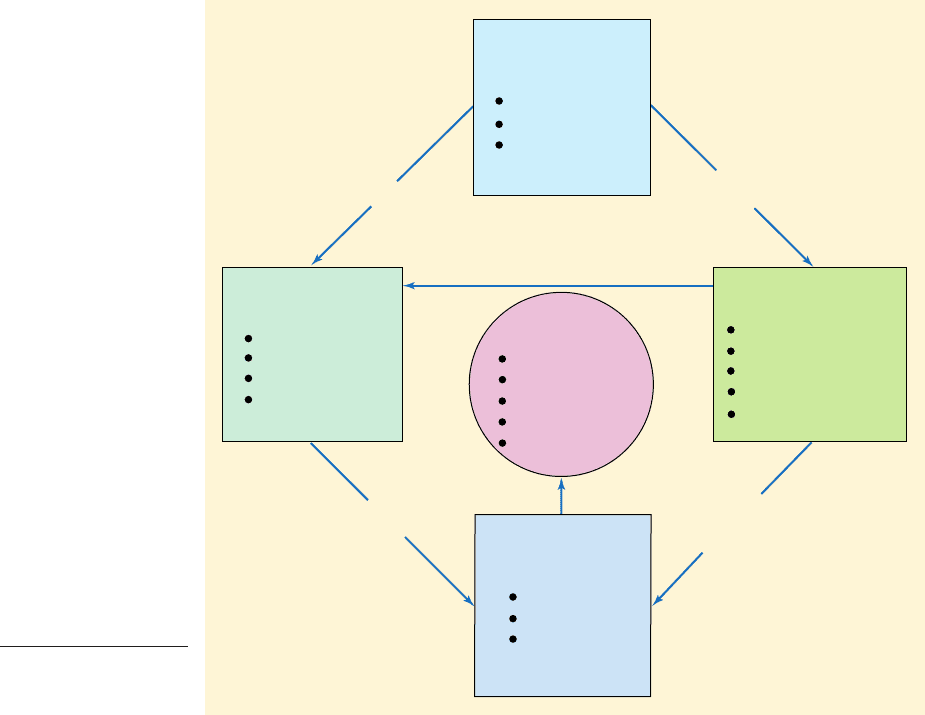

(users of funds) can be met. Figure 2.1 shows in simple terms how businesses finance

their operations.

Financial institutions (e.g. pension funds, insurance companies, banks, building

societies, unit trusts and specialist investment institutions) act as financial intermedi-

aries, collecting funds from savers to lend to their corporate and other customers

through the money and capital markets, or directly through loans, leasing and other

forms of financing.

Businesses are major users of these funds. The financial manager raises cash by sell-

ing claims to the company’s existing or future assets in financial markets (e.g. by issu-

ing shares, debentures or Bills of Exchange) or borrowing from financial institutions.

The cash is then used to acquire fixed and current assets. If those investments are suc-

cessful, they will generate positive cash flows from business operations. This cash sur-

plus is used to service existing financial obligations in the form of dividends, interest

etc., and to make repayments. Any residue is re-invested in the business to replace

existing assets or to expand operations.

We focus in this chapter on the financial institutions and financial markets shown

in Figure 2.1.

Financial institutions

Banks

Pension funds

Insurance companies

Building societies

Finance companies

Real investments

Land

Buildings

Plant

Stock

Debtors

Users of funds

Businesses

Individuals

Government

Financial markets

Money market

Capital market

Exchanges

Over-the-counter

Suppliers of funds

Businesses

Individuals

Government

Deposits and

investment

Investment

Direct

investment

New issues,

bills and acceptances

Loans, overdrafts,

mortgages, venture capital,

leasing etc.

Figure 2.1

Financial markets,

institutions, suppliers

and users

financial intermediaries

Institutions that channel funds

from savers and depositors

with cash surpluses to people

and organisations with cash

shortages

CFAI_C02.QXD 10/28/05 2:19 PM Page 26

.

Chapter 2 The financial environment 27

■

Financial institutions provide essential services

The needs of lenders and borrowers rarely match. Hence, there is an important role for

financial intermediaries, such as banks, if the financial markets are to operate efficient-

ly. Financial intermediaries perform the following functions:

1 Re-packaging, or pooling, finance: gathering small amounts of savings from a large num-

ber of individuals and re-packaging them into larger bundles for lending to busi-

nesses. The banks have an important role here.

2 Risk reduction: placing small sums from numerous individuals in large, well-diversified

investment portfolios, such as unit trusts.

3 Liquidity transformation: bringing together short-term savers and long-term borrow-

ers (e.g. building societies and banks). Borrowing ‘short’ and lending ‘long’ is

acceptable only where relatively few savers will want to withdraw funds at any

given time. The history of banking failures in the USA shows that this is not always

the case.

4 Cost reduction: minimising transaction costs by providing convenient and relatively

inexpensive services for linking small savers to larger borrowers.

5 Financial advice: providing advisory and other services for both lender and borrower.

2.3 THE FINANCIAL SERVICES SECTOR

The financial services sector can be divided into three groups: institutions engaged in

(1) deposit-taking, (2) contractual savings and (3) other investment funds.

■ Deposit-taking institutions

Clearing banks have three important roles: they manage nationwide networks of High

Street branches and on-line facilities; they operate a national payments system by clear-

ing cheques and by receiving and paying out notes and coins; and they accept deposits

in varying amounts from a wide range of customers. Hence, these operations are often

called retail banking. As well as being the dominant force in retail banking, the clearing

banks have diversified into wholesale banking and are continuing, to expand their

international activities. (Useful websites: www.bba.org.uk, www.bcsb.co.uk)

The Balance Sheet of any clearing bank reveals that the main sterling assets are

advances to the private sector, other banks, the public sector in the form of Treasury

Bills and government stock, local authorities and private households. Nowadays, the

main instruments of lending by retail banks are overdrafts, term loans and mortgages.

Wholesale banks

Wholesale banking (or merchant banking) developed out of the need to finance the

enormous growth in world trade in the 19th century. Accepting houses were formed

whose main business was to accept Bills of Exchange (promising to pay a sum of money

at some future date) from less well-known traders, and from discount houses which

provided cash by discounting such bills. Merchant banks nowadays concentrate on

dealing with institutional investors, large corporations and governments. They have

three major activities, frequently organised into separate divisions: corporate finance,

mergers and acquisitions, and fund management.

Merchant banks’ activities include giving financial advice to companies and arranging

finance through syndicated loans and new security issues. Merchant banks are also mem-

bers of the Issuing Houses Association, an organisation responsible for the flotation of

shares on the Stock Exchange. This involves advising a company on the correct mix of

financial instruments to be issued and on drawing up a prospectus and underwriting

clearing banks

Banks (mainly the High Street

banks) that are members of the

Central Clearing House that

arranges the mutual offsetting of

cheques drawn on different banks

retail banking

Retail banks accept deposits

from the general public who

can draw on these accounts by

cheque (or ATM), and lend to

other people and organisations

seeking funds

accepting houses

Accepting Houses are specialist

institutions that discount or

‘’accept’’ Bills of Exchange, espe-

cially short-term government

securities (see Chapter 15)

discount houses

Discount Houses bid for issues

of short-term government secu-

rities at a discount and either

hold them to maturity, or sell

them on in the money market

merchant banks

Merchant banks are wholesale

banks that arrange specialist

financial services like mergers

and acquisition funding, finance

of international trade fund

management

CFAI_C02.QXD 10/28/05 2:19 PM Page 27

.

28 Part I A framework for financial decisions

the issue. They also play a leading role in the development of new financial products, such

as swaps, options and other derivative products, that have become very widely traded

in recent years.

Another area of activity for wholesale banks is advising companies on corporate

mergers, acquisitions and restructuring. This involves both assisting in the negotiation of

a ‘friendly’ merger of two independent companies and also developing strategies for

‘unfriendly’ takeovers, or acting as an adviser for a company defending against an

unwanted bidder.

Finally, merchant banks fulfil a major role as managers of the investment portfolios of

some pension funds, insurance companies, investment and unit trusts, and various

charities. Whether in arranging finance, advising on takeover bids or managing the

funds of institutional investors, merchant banks exert considerable influence on both

corporate finance and the capital market.

The growth of overseas banking has been closely linked to the development of Euro-

currency markets and to the growth of multinational companies. Over 300 foreign

banks operate in London. A substantial amount of their business consists of providing

finance to branches or subsidiaries of foreign companies.

Building societies (www.buildingsociety.html, www.bsa.org.uk) are a form of savings

bank specialising in the provision of finance for house purchase in the private sector.

As a result of deregulation of the financial services industry, building societies now

offer an almost complete set of private banking services, and the distinction between

them and the traditional banks is increasingly blurred. Indeed, many societies have

given up their mutual status to become public limited companies, e.g. Northern Rock.

Self-assessment activity 2.1

What are financial intermediaries and what economic services do they perform?

(Answer in Appendix A at the back of the book)

■ Institutions engaged in contractual savings

Pension funds accumulate funds to meet the future pension liabilities of a particular

organisation to its employees. Funds are normally built up from contributions paid by

the employer and employees. They can be divided into self-administered schemes,

where the funds are invested directly in the financial markets; and insured schemes,

where the funds are invested by, and the risk is covered by, a life assurance company.

Pension schemes have enormous and rapidly growing funds available for investment

in the securities markets. Pension funds enjoy major tax advantages. Subject to certain

restrictions, individuals enjoy tax relief on their subscriptions to a fund. In turn, the

fund’s income and capital gains are tax-free. Together with insurance companies, pen-

sion funds comprise the major purchasers of company securities.

Insurance companies’ activities (www.abi.org.uk) can be divided into long-term and

general insurance. Long-term insurance business consists mainly of life assurance and

pension provision. Policyholders pay premiums to the companies and are guaranteed

either a lump sum in the event of death, or a regular annual income for some defined

period. With a guaranteed premium inflow and predictable aggregate future pay-

ments, there is no great need for liquidity, so life assurance funds are able to invest

heavily in long-term assets, such as ordinary shares.

General insurance business (e.g. fire, accident, motor, marine and other insurance) con-

sists of contracts to cover losses within a specified period, normally 12 months. As liq-

uidity is important here, a greater proportion of funds is invested in short-term assets,

although a considerable proportion of such funds is invested in securities and property.

building societies

Financial institutions whose

main function is to accept

deposits from customers and

lend for house purchase

pension funds

Financial institutions that man-

age the pension schemes of large

firms and other organisations

self-administered schemes

A pension fund that invests

client’s contributions directly

into the stock market and other

investments

insured schemes

A pension fund that uses an

insurance company to invest

contributions and to insure

against actuarial risks (e.g.

members living longer than

expected)

insurance companies

Financial institutions that guar-

antee to protect clients against

specified risks, including death,

and general risks in return for the

payment of an annual premium

CFAI_C02.QXD 10/28/05 2:19 PM Page 28

.

Chapter 2 The financial environment 29

The investment strategy of both pension fund managers and insurance companies

tends to be long-term. They invest in portfolios of company shares and government

stocks, direct loans and mortgages.

■ Other investment funds: unit and investment trusts

As we shall see in Section 2.4, private investors, independently managing their own

investment portfolios, are a dying breed. Increasingly, they are being replaced by finan-

cial institutions that manage widely diversified portfolios of securities, such as unit trusts

and investment trusts (www.investmentfunds.org.uk). These pool the funds of large num-

bers of investors, enabling them to achieve a degree of diversification not otherwise

attainable owing to the prohibitive transactions costs and time required for active portfo-

lio management. However, there are important differences between these institutions.

Investment trusts

Investment trusts are limited companies, whose shares are usually quoted on the Stock

Exchange, and set up specifically to invest in securities. The company’s share price

depends on the value of the securities held in the trust, but also on supply and demand.

As a result, these shares often sell at values different from their net asset values, usually

at a discount.

They are traditionally ‘closed-ended’ in the sense that the company’s articles restrict

the number of shares, and hence the amount of share capital, that can be issued.

However, several open-ended investment trust companies (OEICS) have now been

launched. To realise their holdings, shareholders can sell their shares on the stock market.

Unit trusts

Unit trusts are investment syndicates, established by trust deed and regulated by trust

law. Investors’ funds are pooled into a portfolio of investments, each investor being

allocated tranches or ‘units’ according to the amount of the funds they subscribe. They

are mainly operated by banks and insurance companies, which appoint managers

whose conduct is supervised by a set of trustees.

Unit prices are fixed by the managers, but reflect the value of the underlying secu-

rities. Prices reflect the costs of buying and selling, via an initial charge. Managers also

apply annual charges, usually about 1 per cent of the value of the fund. Unit-holders

can realise their holdings only by selling units back to the trust managers.

They are ‘open-ended’ in the sense that the size of the fund is not restricted and the

managers can advertise for funds.

Disintermediation and securitisation

While financial intermediaries play a vital role in the financial markets, disintermedia-

tion is an important new development. This is the process whereby companies borrow

and lend funds directly between themselves without recourse to banks and other insti-

tutions. Allied to this is the process of securitisation, the development of new financial

instruments to meet ever-changing corporate needs (i.e. financial engineering). Some

assets generate predictable cash returns and offer security. Debt can be issued to the mar-

ket on the basis of the returns and suitable security. Securitisation usually also involves

a credit rating agency assessing the issue and giving it a credit rating. Securitisation can

also be used to create value through ‘unbundling’ traditional financial processes. For

example, a conventional loan has many elements, such as loan origination, credit status

evaluation, financing and collection of interest and principal. Rather than arranging the

whole process through a single intermediary, such as a bank, the process can be ‘unbun-

dled’ and handled by separate institutions, which may lower the cost of the loan.

Securitisation and disintermediation have permitted larger companies to create

alternative, more flexible forms of finance. This, in turn, has forced banks to become

portfolios

Combinations of securities of

various kinds invested in a

diversified fund

disintermediation

Business-to-business lending

that eliminates the banking

intermediary

securitisation

The capitalisation of a future

steam of income into a single

capital value that is sold on the

capital market for immediate

cash

CFAI_C02.QXD 10/28/05 2:19 PM Page 29

.

30 Part I A framework for financial decisions

more competitive in the services offered to larger companies. Recent more exotic forms

of securitisation include pubs, gate receipts from a football club, future income from a

pop star’s recordings, and even the football World Cup competitions for 2002 and 2006.

Securitising the Beatles

Chrysalis, the media group, has completed a complex cross-border securitisation deal to unlock

£60 million over 15 years against the future value of its music publishing catalogue which

includes artists ranging from Blondie, the Beatles, Jethro Tull to David Gray and Moloko.

Music publishing is a separate business from recorded music, comprising the rights to the

written composition of a song, performance rights such as radio airplay, a share of CD sales

and synchronisation rights from use in advertisements or films. Chrysalis’s revenues from its

catalogue were £8 million in 2000.

The Chrysalis securitisation deal took 18 months to structure because of the complexity in

bringing together publishing rights in the UK, US, Germany, Sweden and Holland under their

different tax regimes.

Chrysalis follows in the footsteps of the singer-songwriter, David Bowie, who recently raised

$55 million via a bond issue against his share of the publishing rights to his compositions.

Source: Based on Financial Times, 2 March 2001.

2.4 THE LONDON STOCK EXCHANGE (LSE)

The capital market is the market where long-term securities are issued and traded. The

London Stock Exchange is the principal trading market for long-dated securities in the

UK (www.londonstockexchange.com).

A stock exchange has two principal economic functions: to enable companies to

raise new capital (the primary market), and to facilitate the trading of existing shares (the

secondary market) through the negotiation of a price at which title to ownership of a

company is transferred between investors. Secondary trading dwarfs the issue of new

ordinary shares. In 2004, secondary turnover in UK companies was £2,316 billion by

value, involving 2.15 million ‘bargains’ (deals). By contrast, new money raised by UK

firms in the same year was only £16 billion.

■ A brief history of the London Stock Exchange

The world’s first joint-stock company – the Muscovy Company – was founded in

London in 1553. With the growth in such companies, there arose the need for share-

holders to be able to sell their holdings, leading to a growth in brokers acting as inter-

mediaries for investors. In 1760, after being ejected from the Royal Exchange for

rowdiness, a group of 150 brokers formed a club at Jonathan’s Coffee House to buy and

sell shares. By 1773, the club was renamed the Stock Exchange.

The Exchange developed rapidly, playing a major role in financing UK companies

during the Industrial Revolution. New technology began to have an impact in 1872,

when the Exchange Telegraph tickertape service was introduced.

For over a century, the Exchange continued to expand and become more efficient,

but fundamental changes did not occur until 27 October 1986 – ‘Big Bang’ – the most

important of which were:

1 All firms became brokers/dealers able to operate in a dual capacity – either buy-

ing securities from, or selling them to, clients without the need to deal through a

CFAI_C02.QXD 10/28/05 2:19 PM Page 30

.

Chapter 2 The financial environment 31

third party. Firms could also register as market makers committed to making firm

bid (buying) and offer (selling) prices at all times.

2 Ownership of member firms by an outside corporation was permitted, enabling

member firms to build a large capital base to compete with competition from

overseas.

3 Minimum scales of commission were abolished to improve competitiveness.

4 Trading moved from being conducted face-to-face on a single market floor to being

performed via computer and telephone from separate dealing rooms. Computer-

based systems were introduced to display share price information, such as SEAQ

(Stock Exchange Automated Quotations).

The Alternative Investment Market (AIM) was introduced in 1995, to provide a mar-

ket that is accessible to both investors and companies from a wide range of backgrounds,

including start-ups and established firms. In 2004, AIM celebrated its 1,000th listing. By

the end of that year, 1,020 UK and international companies were listed on AIM with total

capitalisation of £31.75 billion. The total value of secondary deals on AIM in 2004 was

£18.2 billion, while AIM firms raised £4.6 billion in new issues.

In 1997, the settlement service for exchanging shares and associated payment

moved to the CREST electronic settlement system. In the same year, the Stock

Exchange Electronic Trading Service (SETS) was launched to bring greater speed and

efficiency to the market. Today, the London Stock Exchange is viewed as one of the

leading and most competitive places to do business in the world, second only to New

York in total market value terms.

The LSE has two tiers. The bigger market is the Main List, providing a quotation for

2,753 companies (as at August 2004). To obtain a full listing, companies have to satis-

fy rigorous criteria laid down in the Stock Exchange’s ‘Listing Rules’ (or ‘Yellow

Book’). These relate to size of issued capital, financial record, trading history and

acceptability of board members. These details are set out in a document called the

company’s ‘listing particulars’.

The second tier is the Alternative Investment Market (AIM). It attempts to min-

imise the cost of entry and membership by keeping the rules and application process

as simple as possible. A nominated adviser firm (typically a stock broker or bank)

both introduces the new company to the market and acts as a mentor, ensuring that

it complies with market rules. Although the majority of companies are capitalised at

between £2 million and £20 million, it also includes start-up operations at one end

and companies capitalised at over £200 million at the other. However, the require-

ment to observe existing obligations in relation to publication of price-sensitive

information and annual and interim accounts remains. The AIM is unlikely to

appeal to private investors unless they are prepared to invest in relatively high-risk

businesses.

While the vast majority of share trading takes place through the Stock Exchange, it

is not the only trading arena. For some years, there has been a small, but active Over-

The-Counter (OTC) Market, where organisations trade their shares, usually on a

‘matched bargain’ basis, via an intermediary.

Self-assessment activity 2.2

What type of company would be most likely to trade on:

(a) the Main Securities Market?

(b) the Alternative Investment Market?

(c) The Over-The-Counter Market?

(Answer in Appendix A at the back of the book)

CFAI_C02.QXD 10/28/05 2:19 PM Page 31

.

32 Part I A framework for financial decisions

■ Regulation of the market

Investor confidence in the workings of the stock market is paramount if it is to operate

effectively. Even in deregulated markets, there is still a requirement to provide strong

safeguards against unfair or incompetent trading and to ensure that the market oper-

ates as intended. The mechanism for regulating the whole UK financial system was

established by the Financial Services Act 1986 (FSA86), which provided a structure

based on ‘self-regulation within a statutory framework’.

In 1997, statutory powers were vested in a supervisory body, the Financial Services

Authority (FSA), responsible to the Treasury. Its objectives are to sustain confidence in

the UK’s financial services industry and monitor, detect and prevent financial crime

(www.fsa.gov.uk). This involves the regulation of the financial markets, investment

managers and investment advisors.

The FSA also takes on additional responsibilities for monitoring the Bank of England

and money markets, building societies and the insurance market. The hope is that, by

having a single regulator covering all financial markets, there will be greater efficiency,

lower costs, clearer accountability and a single point of service for customer enquiries

and complaints.

In an attempt to enhance London’s reputation for clean and fair markets, the FSA

has introduced new powers, effective from 2000, to deal with insider dealing and

attempts to distort prices. It is a criminal offence to undertake ‘investment business’

without due authorisation. A Recognised Investment Exchange (RIE), of which the

London Stock Exchange is one, may also receive authorisation. Recognition exempts

an exchange (but not its members) from needing authorisation for any activity consti-

tuting investment business.

The Stock Exchange discharges its responsibilities by:

■ vetting new applicants for membership

■ monitoring members’ compliance with its rules

■ providing services to aid trading and settlement of members’ business

■ supervising settlement activity and management of settlement risk

■ investigating suspected abuse of its markets.

Market abuse includes three strands:

(a) Market distortion – acting in such a manner as to force up a company’s share price.

(b) Misuse of information – e.g. buying or selling shares on the basis of privileged

information.

(c) Creating false information – e.g. putting false information on to a website.

FSA86 also gave the Exchange responsibility for regulating both the admission of

companies to the Official List and their ongoing compliance with the listing require-

ments. Companies violating the Exchange’s rules of conduct can have their listings

removed.

Other bodies also keep a watchful eye on the workings of capital markets. These

include the Bank of England (www.bankofengland.co.uk), the Competition Commission

(CC), the Panel on Takeovers and Mergers, the Office of Fair Trading, the press and

various government departments.

Self-assessment activity 2.3

To what extent does an effective primary capital market depend on a healthy secondary

market?

(Answer in Appendix A at the back of the book)

CFAI_C02.QXD 10/28/05 2:19 PM Page 32

.

Chapter 2 The financial environment 33

■

Share ownership in the UK

Back in 1963, over half (54 per cent) of all UK equities were held by private individu-

als. This proportion had dropped to 14.9 per cent by the end of 2003 (www.statistics.

gov.uk). Today, share ownership is dominated by financial institutions (the pension

funds, insurance groups and investment and unit trusts). Together, including both UK

and foreign institutions, they own around 80 per cent of the value of UK traded com-

panies. These impersonal bodies, acting for millions of pensioners and employees, pol-

icyholders and small investors, have vast power to influence the market and the

companies they invest in. Institutional investors employ a variety of investment strate-

gies, from passive index-tracking funds, which seek to reflect movements in the stock

market, to actively managed funds.

Institutional investors have important responsibilities, and this can create a dilem-

ma: on the one hand, they are expected to speak out against corporate management

policies and decisions that are deemed unacceptable environmentally, ethically or

economically. But public opposition to the management could well adversely affect

share price. Institutions therefore have a conflict between their responsibilities as

major shareholders and their investment role as managers seeking to outperform the

markets.

A further indication of changing patterns of share ownership is the proportion of

the adult population that holds shares. Successive governments have promoted a

‘share-owning democracy’, particularly through privatisation programmes. However,

individuals tend to hold small, undiversified portfolios – over half of private investors

hold just one security – which exposes them to a greater degree of risk than from

investing in a diversified investment portfolio.

■ Towards a European stock market

The European Union is meant to be about removing barriers and providing easier

access to capital markets. Until recently, this was still a pipe dream, with some 30 stock

exchanges within the EU, most of which had different regulations. With the introduc-

tion of a single currency, there will undoubtedly be strong pressure towards a single

capital market. But does this mean a single European stock exchange, with one set of

rules for share listing and trading?

Euronext was formed in 2000 as a result of the merger of the Amsterdam, Brussels and

Paris stock exchanges. As the first pan-European stock exchange, it has already under-

taken further mergers with other smaller exchanges in Europe (e.g. LIFFE, Lisbon),

which is exerting more pressure on the London and Frankfurt exchanges. These two

exchanges attempted, but failed, to merge in 2000. The New York Stock Exchange is eas-

ily the largest in terms of market value, while Nasdaq, the US exchange for young

growth companies, has the most companies listed.

However, the London market lists the greatest number of foreign companies. At

year-end 2004, there were some 450 foreign firms listed on the main market, the major-

ity from the USA, Western Europe and the Commonwealth countries, but including

representation from Russia, Hungary and China.

The box below gives the examples of Inion, a Finnish Company, maker of biodegrad-

able plates for mending broken bones. Inion announced plans to list in London in 2004,

Its market value at floatation was £72 million.

CFAI_C02.QXD 10/28/05 2:19 PM Page 33

.

34 Part I A framework for financial decisions

Inion plans £30m public offering

Inion, a Finnish medical devices company,

is planning to raise £30m in an initial pub-

lic offering on the London Stock Exchange.

The indicative price range for the flota-

tion has been set at between 113p and

136p a share, giving a market capitalisa-

tion of between £80m and £90m.

The company, which makes biodegrad-

able polymer implants, was set up in 1999

by senior researchers from Bionics, a

Nasdaq-listed Finnish implants company.

Auvo Kaikkonen, chief executive, said

listing alongside other medical technology

companies in London would ensure better

liquidity than floating on the Helsinki Stock

Exchange, which is dominated by Nokia.

‘We wanted a market where there was an

experienced analyst and investor commu-

nity,’ he said.

Inion’s products include biodegradable

screws, plates and meshes to stabilise bro-

ken and damaged bones while they heal.

Inion incurred a pre-tax loss of approxi-

mately ;3m (£2.1m) on revenues of ;2.4m

in the first half of 2004. Mr Kaikkonen

said it would break even when revenues

reached ;20m.

Source: Financial Times, 10 November 2004.

2.5 ARE FINANCIAL MARKETS EFFICIENT?

If financial managers are to achieve corporate goals, they require well-developed finan-

cial markets where transfers of wealth from savers to borrowers are efficient in both

pricing and operational cost.

Efficiency can mean many things. The economist talks about allocative efficiency –

the extent to which resources are allocated to the most productive uses, thus satisfying

society’s needs to the maximum. The engineer talks about operating or technical effi-

ciency – the extent to which a mechanism performs to maximum capability. The soci-

ologist and the political scientist talk about social efficiency – the extent to which a

mechanism conforms to accepted social and political values. The most important con-

cept of efficiency for our purposes is pricing or information efficiency. This refers to the

extent to which available information is built into the structure of share prices. If infor-

mation relevant for assessing a company’s future earnings prospects (including both

past information and relevant information relating to future expected events) is wide-

ly and cheaply available, then this will be impounded into share prices by an efficient

market. As a result, the market should allow all participants to compete on an equal

basis in a so-called fair game.

We often hear of the shares of a particular company being ‘under-valued’ or ‘over-val-

ued’, the implication being that the stock market pricing mechanism has got it wrong and

that analysts know better. In an efficient stock market, current market prices fully reflect avail-

able information and it is impossible to outperform the market consistently, except by luck.

Consider any major European stock market. On any given trading day, there are

hundreds of analysts – representing the powerful financial institutions which domi-

nate the market – closely tracking the daily performance of the share price of, say,

Wimpey, the construction company. They each receive at the same time new informa-

tion from the company – a major order, a labour dispute or a revised profits forecast.

This information is rapidly evaluated and reflected in the share price by their decisions

to buy or sell Wimpey shares. The measure of efficiency is seen in the extent and speed with

which the market reflects new information in the share price.

The Law of One Price suggests that equivalent securities must be traded at the

same price (excluding differences in transaction costs). If this is not the case, arbi-

trage opportunities arise whereby a trader can buy a security at a lower price and

simultaneously sell it at a higher price, thereby making a profit without incurring

allocative efficiency

The most efficient way that a

society can allocate its overall

stock of resources

operating/technical

efficiency

The most cost-effective way of

producing an item, or organis-

ing a process

social efficiency

The extent to which a socio-

economic system accords with

prevailing social and ethical

standards

pricing/information

efficiency

The extent to which available

information is impounded into

the current set of share prices

fair game

A competitive process in which

all participants have equal

access to information and

therefore similar chances of

success

arbitrage

The process whereby astute

entrepreneurs identify and

exploit opportunities to make

profits by trading on differen-

tials in price of the same item

as between two locations or

markets

FT

CFAI_C02.QXD 10/28/05 2:19 PM Page 34