Pike Robert, Neal Bill. Corporate finance and investment: decisions and strategy

Подождите немного. Документ загружается.

.

Chapter 19 Does capital structure really matter? 525

There is a useful expression available to show how the various Betas are linked together.

It is important to recall the MM message that underlying business or activity risk is unaf-

fected by the method of financing. If a firm chooses to borrow, thus introducing financial

risk, the shareholders will respond by looking for a higher return as they perceive greater

financial risk affecting their future income, but the risk attaching to the firm’s actual oper-

ating activities is untouched – it is the same firm operating in the same business environ-

ment and operated by the same managers. All that has happened is a repackaging of the

firm’s flow of operating income resulting in lenders now having a prior claim. The size

of the operating income itself is unaffected, only its distribution changes.

Given that the activity risk is unaffected by gearing, we can use the accounting equa-

tion to show the linkages. The accounting equation tells us that the assets are equal to the

methods of financing. Translating this into CAPM terms, the asset Beta (i.e. the activity

Beta) equals the Beta of the methods of finance used to acquire those assets. In other

words, the asset Beta equates to a weighted average of the Betas of the various methods

of financing, according to the importance of each source of finance in the capital structure.

Algebraically, this is given by:

Notice that the tax shield is reflected in applying the term to the debt compo-

nent. Notice also that, as the debt proportion increases, the equity Beta must increase to

preserve the constant asset Beta. It is usual to assume that the debt Beta is zero, although

there is some evidence that corporate debt has a very low Beta, around 0.1 to 0.2.

However, if we do assume a debt Beta of zero, this becomes a very versatile expres-

sion, e.g. when moving into a new activity we can take a firm’s equity Beta and ungear

it to reveal the underlying activity Beta. This is particularly useful when diversifying

into a new activity – we might borrow a Beta from another firm, whose gearing may

differ from our own. In this case, we might ungear the borrowed Beta to strip out that

firm’s financial risk, and then re-gear to incorporate our own firm’s gearing ratio.

To illustrate this, assume we have the following data:

Ungearing the other firm’s equity Beta, assuming the debt Beta is zero, we have:

1.35 60>88 0.92

Beta

A

Beta

E

a

V

S

V

S

V

B

11 T2

b 1.35 a

60

60 4011 T2

b

Own gearing ratio 10% 1debt>equity2

Tax rate

30%

1i.e. debt proportion 40 : 1002

Gearing ratio 1debt>equity2 of this firm 40%

Equity Beta of firm operating in new activity 1.35

11 T2

Beta

A

aBeta

E

V

S

V

S

V

B

11 T2

b aBeta

D

V

B

11 T2

V

S

V

B

11 T2

b

1Equity Beta proportion of equity2 1Debt Beta proportion of debt2

Beta of assets

19.7 LINKING THE BETAS

This corresponds to the result obtained more directly with the CAPM formula. The

two separate components of the geared Beta are shown in Figure 19.3. The increase in

the geared Beta as the debt/equity ratio increases drives up the additional required

premium pro rata.

CFAI_C19.QXD 10/26/05 5:22 PM Page 525

.

526 Part V Strategic financial decisions

Re-gearing to incorporate our own gearing, the equity Beta is given by:

Whence, equity Beta 0.92 107>100 0.98

0.92 Beta

E

100

100 1011 T2

Beta

E

100>107

19.8 MM WITH FINANCIAL DISTRESS

In Section 19.5, we saw how including corporate taxation in the MM model implied

that companies should rely on debt for nearly 100 per cent of their financing. This

implication is clearly at odds with observed practice – few companies gear up to

extreme levels, through fear of insolvency and its associated costs. MM’s omission of

liquidation costs from their analysis was a logical consequence of their perfect capital

market assumptions. In such a market, where investors are numerous and rational, and

have homogeneous expectations and plentiful access to information, the resale value of

assets, even those being sold in a liquidation, will reflect their true economic values.

Investors will recognise the worth of such assets as measured by the present values of

their future income flows, and be prepared to bid up to this value, so that the price

realised by a liquidator should not involve any discount.

In effect, liquidation costs and the other costs of financial distress introduce a new

imperfection into the analysis of capital structure decisions: namely the actual or

expected inability to realise ‘full value’ for assets in a distress sale and the costs of

actions taken to forestall this contingency.

Incorporating financial distress

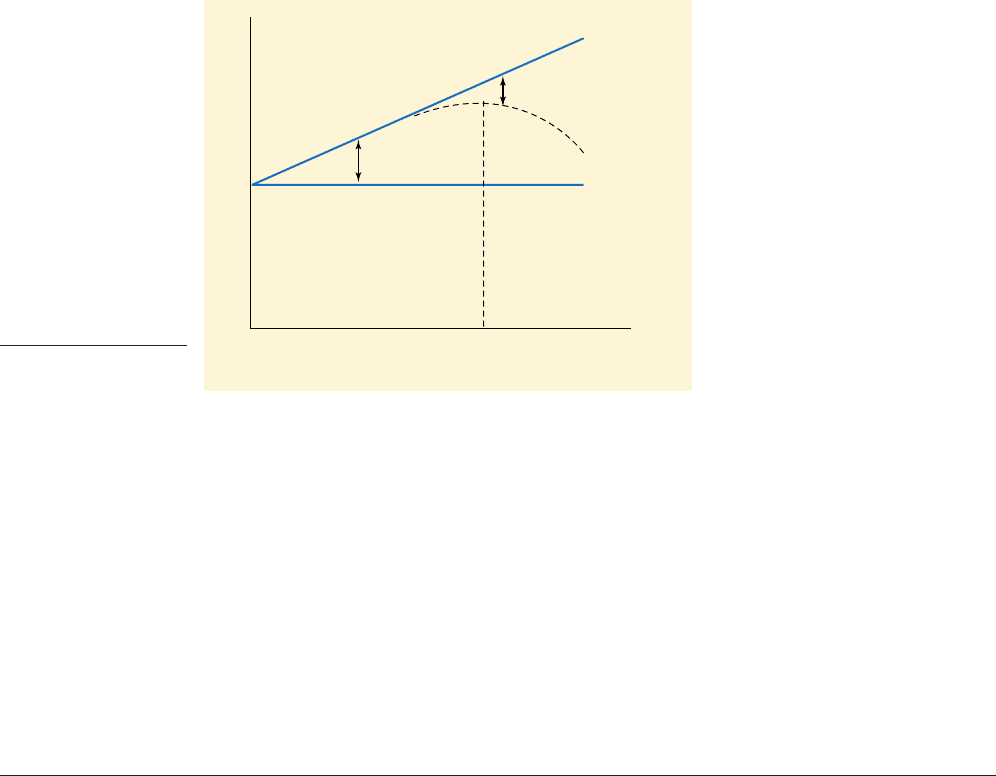

Denoting the ‘costs of financial distress’ by FD, the value of a geared company becomes:

From this, we may conclude that the financial manager should attempt to maximise the

gap between tax benefits and financial distress costs, i.e. and that there exists an

optimal capital structure where company value is maximised. This occurs where the mar-

ginal benefit of further tax savings equals the marginal cost of anticipated financial

distress. This occurs with debt of in Figure 19.4.

The costs of financial distress rise with gearing once the market starts to perceive a

substantially increased risk of financial failure. The likelihood of FD being non-zero

depends on the probability distribution of the firm’s earnings profile. For example, in

the Lindley example in Chapter 18, for gearing ratios up to 50 per cent the probability

of inability to meet interest payments is zero, but it would be 0.25 for any higher gear-

ing ratio. For most companies, the probability, p, of financial distress will increase with

the book values of debt, B, so that the FD function increases with gearing. If d denotes

the expected percentage discount on the pre-liquidation value in the event of a forced

sale, the expected costs of financial distress are:

FD 1p d V

g

2

X

*

1TB FD2,

V

g

V

u

3TB FD4

costs of financial distress

The costs incurred as a firm

approaches, and ultimately

reaches, the point of insolvency

Self-assessment Activity 19.5

Ungear a Beta of 1.45 if:

■ Tax

rate 30%

■ The debt–equity ratio

1:2

(Answer in Appendix A at the back of the book)

CFAI_C19.QXD 10/26/05 5:22 PM Page 526

.

Chapter 19 Does capital structure really matter? 527

and the value of the geared firm is:

This suggests that market imperfections can be exploited to raise company value so

long as TB exceeds Notice that the inverted ‘U’-shaped value profile

now appears remarkably similar to the traditional version and, of course, is associated

with a mirror-image WACC schedule.

You may recall our earlier comment that, after introducing market imperfections such

as tax, the MM model begins to look more like the traditional version. With the inclusion

of financial distress costs, this resemblance is closer still. However, the discussion of the

impact of personal taxation in Appendix III shows that the debate is not yet dead.

1p d V

g

2.

V

g

V

u

1TB p d V

g

2

19.9 CALCULATING THE WACC

Before progressing, you may find it useful to reread Chapter 11, where we discussed the

hierarchy of discount rates and required rates of return, but deferred consideration of the

problems posed by mixed capital structures until Chapter 18.

The WACC is the overall required return needed to satisfy all stakeholders. It is also

the required return on the assumption that new projects are financed in exactly the

same way as existing ones. If the company is all-equity financed, then the WACC is

simply the return required by shareholders.

Gearing does not affect the underlying risk of the company’s business activities. If

a company uses debt capital, it is merely repackaging its operating income into differ-

ent proportions of debt interest and equity income, but not influencing the size or the

riskiness of this income before appropriation. What does change is the riskiness of the

stream of residual equity income, which is why the equity Beta rises, pulling up with

it the return required by shareholders.

We can explore this preposition with the case of Higear. The relevant figures for

Higear were:

Value of debt V

B

£1 m

Value of equity V

S

£2.80 m

Shareholders’ required return k

eg

22.5%

Interest cost of debt i 10%

Rate of corporate tax T 30%

FD

TB

X

*

0

V

u

Company value

V

g

=

V

u

+

[

TB

–

FD

]

V

g

=

V

u

+

TB

Book value of debt

Figure 19.4

Optimal gearing with

liquidation costs

CFAI_C19.QXD 10/26/05 5:22 PM Page 527

.

528 Part V Strategic financial decisions

The expression for the WACC in the MM case with corporate tax is:

Using the data for Higear, this expression yields:

Alternatively, we can obtain the same result by using the expression:

■ Relaxing critical assumptions

Two important questions now arise. First, what happens to the discount rate if a com-

pany diversifies into an activity with a risk profile different from existing operations?

Second, what happens if the gearing ratio is altered? The first issue is easier to handle.

Allowing for different risks

Imagine Higear proposes to diversify into a higher risk business. Because the discount

rate applicable to evaluating this project should reflect the systematic risk involved, the

required return previously calculated is no longer appropriate. To cope with this prob-

lem, the following procedure is suggested:

1 Select a company already operating in the target activity, ideally, one with operat-

ing characteristics very similar to those exhibited by the project, and identify its

Beta coefficient, e.g by using the RMS.

2 If the surrogate company’s gearing differs from that of Higear, the Beta must be

adjusted by removing the effect of the surrogate’s own gearing, and then super-

imposing Higear’s gearing on the resulting ungeared Beta.

3 Calculate the WACC incorporating the surrogate activity Beta, adjusted for

Higear’s own gearing.

Assume Higear plans to enter an activity already served by Semigear, whose equity

Beta is 1.8, and which has a debt/equity ratio of 1:2. Semigear’s Beta is ungeared as

follows:

The geared Beta applicable to Higear’s capital structure (i.e. million debt and

million equity) is:

1.33

31.254 1.663

1.33 c1

£1 m

£2.80 m

11 30% 2d

b

g

b

u

c1

V

B

V

S

11 T2d

£2.80£1

b

u

b

g

1

V

B

V

S

11 T2

1.8

1

1

2

11 30% 2

1.8

1.35

1.33

18.4%

20% 0.92

20% c1 30%

£1 m

£3.80 m

d

k

o

k

eu

c1 T

V

B

V

S

V

B

d

16.6% 1.8% 18.4%

122.5% 0.742 17% 0.262

k

o

a22.5%

£2.80 m

£2.80 m £1 m

b c10%11 30%2

£1 m

£2.80 m £1 m

d

k

o

ak

eg

V

S

V

S

V

B

b ci11 T2

V

B

V

S

V

B

d

CFAI_C19.QXD 10/26/05 5:22 PM Page 528

.

Chapter 19 Does capital structure really matter? 529

For this risk, and with a 9 per cent market risk premium, Higear’s shareholders require

a return of:

Finally, the WACC applicable to this activity risk and Higear’s own gearing is:

The second issue, the effect of a change in gearing, poses more of a conundrum.

Allowing for a change of gearing

In the Higear example, no change in gearing was envisaged when financing new projects.

However, as we have repeatedly warned, a significant change in gearing affects the

market values of both debt and equity capital: for example, shareholders may respond

adversely to higher gearing and the higher financial risk. Also, the value of debt may

be marked down in the market. To compute the WACC, we would have to assess the

new return required by shareholders, given by:

where

To value the equity, i.e. to derive a measure for we would need to apply the (per-

petuity) expression for valuing a stream of post-tax geared equity income:

We now encounter a circular problem, since the market value depends on and

to find we need to know the market value!

A possible solution is to work in terms of a ‘tailor-made’ WACC based on the pro-

ject’s characteristics (i.e. its systematic risk, allowing for any divergence from existing

operations) and on the project’s own financing. For example, imagine the project in the

previous example were to be financed 20 per cent by debt and 80 per cent by equity.

You should verify that with that shareholders would seek a

return of 24 per cent, and that the WACC is:

As it happens, use of the WACC in this situation may be inappropriate anyway,

since unless the firm is at, and adheres to, the target ratio, the WACC and the marginal

cost of capital (MCC) will diverge. If the firm is below the optimal capital structure,

the MCC is less than WACC, and the MCC exceeds the WACC when it overshoots the

optimal gearing ratio. We found, in Chapter 18, that when the firm departs from the

optimal gearing ratio, the appropriate required return is the MCC:

However, to calculate the MCC we again need to know the market values of both

equity and debt at the higher level of gearing, i.e. we encounter the circular problem

described earlier. It is clear that the WACC is suitable only for small-scale projects that

do not materially disturb the gearing ratio, and that the theoretically more correct

MCC is also problematic.

MCC

Change in total returns required by shareholders and lenders

Amount available to invest

124% 4>52 110% 31 T4 1>52 119.2% 1.4%2 20.6%

b

g

1.56,b

u

1.33,

k

eg

,

k

eg

,

V

S

1E iB211 T2

k

eg

V

S

,

b

u

the ungeared Beta coefficient

k

eu

R

f

b

u

1ER

m

R

f

2

k

eg

k

eu

1k

eu

i211 T2

V

B

V

S

R

f

b

g

1ER

m

R

f

2

k

eg

,

125.0% 0.742 110% 31 30% 4 0.262 18.5% 1.8% 20.3%

ER

j

R

f

b

g

3ER

m

R

f

4 10% 1.66339% 4 25%

CFAI_C19.QXD 10/26/05 5:22 PM Page 529

.

530 Part V Strategic financial decisions

An ‘off-the-cuff’ solution is to work in terms of book values. This pragmatic

approach has the merit of simplicity, as book values do not vary with gearing, and it

might be appropriate for unlisted firms, which by definition have no market values.

Nevertheless, it is desirable to work, whenever possible, in terms of market values,

given that most investors are more concerned with the current values of their invest-

ments, and the returns thereon, than with historic Balance Sheet values.

Fortunately, as we shall see in the next section, help is at hand.

19.10 THE ADJUSTED PRESENT VALUE METHOD (APV)

The adjusted present value (APV) of a project is simply the ‘essential’ worth of the proj-

ect, adjusted for any financing benefits (or costs) attributable to the particular method

of financing it. The rationale for the APV method was provided by Myers (1974), using

MM’s gearing model with corporate tax, but is valid only so long as the WACC profile

is declining due to the value of the tax shield. In Section 19.5, we saw that the value of

a geared firm, is the value of an equivalent all-equity-financed company, plus a

tax shield, TB, which is the discounted tax savings resulting from the tax-deductibility

of debt interest:

This can be translated from the value of a firm to the value of an individual project.

However, different projects can probably support different levels of debt. For example,

they may involve different inputs of easily resaleable fixed assets and may also have

different levels of operational gearing. As a result, it may be more appropriate to eval-

uate the effects of the financing of each project separately.

The APV is calculated in three steps:

Step 1 Evaluate the ‘base case’ NPV, discounting at the rate of return that sharehold-

ers would require if the project were financed wholly by equity. This rate is

derived by ungearing the company’s equity Beta.

Step 2 Evaluate separately the cash flows attributable to the financing decision,

discounting at the appropriate risk-adjusted rate.

Step 3 Add the present values derived from the two previous stages to obtain the

APV. The project is acceptable if the APV is greater than zero.

A simple example will illustrate the use of the APV.

■ Using the APV: Rigton plc

Rigton plc has a gearing ratio, measured by debt/equity at market values, of 20 per

cent. The equity Beta is 1.30. The risk-free rate is 10 per cent and a return of 16 per

cent is expected from the market portfolio. The rate of corporate tax is 30 per cent.

Rigton proposes to undertake a project requiring an outlay of million, financed

partly by equity and partly by debt. The project, a perpetuity, is thought to be able to

support borrowings of million at an interest rate of 12 per cent, thus imposing

interest charges of £0.36 million. It is expected to generate pre-tax cash flows of £2.3

million p.a.

Using the formula developed earlier for the ungeared Beta:

b

u

b

g

c1

V

B

V

S

11 T2d

1.30

1 0.2011 0.302

1.30

1.14

1.14

£3

£10

V

g

V

u

TB

V

g

,V

g

,

adjusted present value

The inherent value of a project

adjusted for any financial ben-

efits and costs stemming from

the particular method(s) of

financing

CFAI_C19.QXD 10/26/05 5:22 PM Page 530

.

Chapter 19 Does capital structure really matter? 531

This yields a required return on ungeared equity of:

The base case NPV is:

The present value of the tax savings, i.e. the tax shield, TB, is given by:

The adjusted present value is thus:

and the project appears worthwhile. The significance of this result is that, although the

base case NPV is negative, the project is rescued by the tax shield of million. An

essentially unattractive project is rendered worthwhile by the taxation system.

In the Rigton example, the project creates wealth only for Rigton’s shareholders.

From the perspective of the overall economy, it is wealth-reducing and, unless there

are compelling ‘social’ reasons to justify it, should not be undertaken. This sort of rea-

soning led the UK government in 1984 to reduce the rate of Corporation Tax in order

to lower the tax advantage of debt financing, and hence reduce the extent to which

investment decisions were likely to be distorted by the system of tax breaks.

£0.90

APV £0.42 m £0.90 m £0.48 m

TiB

i

10.30210.1221£3 m2

0.12

10.3021£0.36 m2

0.12

£0.108 m

0.12

£0.9 m

£0.42 m

£10 m £9.58 m

NPV £10 m

£2.3 m11 0.302

0.168

£10 m

£1.61 m

0.168

0.168,

i.e. 16.8%

ER

j

R

f

b

u

1ER

m

R

f

2 0.10 1.14 10.16 0.102 10.10 0.0682

Self-assessment activity 19.6

What is the APV and how is it calculated?

(Answer in Appendix A at the back of the book)

■ Further aspects

Before leaving the APV, several related issues are worth examining.

1 The APV in practice is affected by the terms and conditions of a pre-arranged sched-

ule for debt interest and capital repayment. Sometimes, the calculations can be

exceptionally tedious. Rather than using the convenient assumption of perpetual

debt financing, let us assume that the debt plus interest must be repaid over

two years, with interest and two equal capital payments occurring at end-year.

Table 19.2 shows the repayment schedule and the resulting tax savings.

With no tax delay assumed, the present value of the tax savings is:

£0.108 m

11.122

£0.054 m

11.122

2

1£0.096 m £0.043 m2 £0.139 m

Table 19.2

The tax shield with

finite-life debt

Balance of Balance of

loan at start Interest loan at end

of year at 12% Tax saving 30%) Repayment of year

0

£1.5 m

130% £0.18 m2 £0.054 m

£0.18 m£1.5 m

£1.5 m£1.5 m

130% £0.36 m2 £0.108 m

£0.36 m£3.0 m

1T

CFAI_C19.QXD 10/26/05 5:22 PM Page 531

.

532 Part V Strategic financial decisions

Obviously, the value of the tax shield is much lower with the shorter payment profile.

2 Although our example focused on the side-effects of debt financing, the APV rou-

tine can be easily applied to any other financing costs and benefits, many of which

are awkward to handle with the simple WACC. For example, if equity capital is

externally raised, normally there are various issuing and underwriting costs to bear.

Including these would alter the APV formula as follows:

A similar treatment would be applied to subsidised borrowing costs, investment

grants and tax savings from exploiting investment allowances.

3 Tax savings are not certain because they depend on the inherent profitability of the

company. As this is a random variable, the company’s ability to set off interest pay-

ments (and other tax reliefs) against income is also random. Our examples assume

continuous profitability, but if there are periods during which the company is

expected to be tax-exhausted, this should be allowed for in the computation of the

APV. If the future pattern of liability to tax is uncertain, then it is not appropriate to

use a risk-free rate to discount the tax savings.

4 Finally, we have glossed over the issues that impact on the debt-supporting capac-

ity of particular projects. In principle, the debt capacity of a project is given by the

present value of future expected earnings from the firm as a whole, taking into

account any existing borrowings. It might seem obvious that more profitable com-

panies are able to borrow relatively more than unprofitable companies. However,

this assumes that there are no costs of financial distress. Enhanced borrowing abil-

ity for more profitable companies is not universal, since a would-be lender would

still look at the break-up value of the enterprise. In the final analysis, the crucial fac-

tor which governs debt capacity is how much can be raised by a distress sale of

assets.

APV Base case NPV Tax shield PV of issue costs

Self-assessment activity 19.7

How would you identify the point beyond which a firm would be unable to borrow?

(Answer in Appendix A at the back of the book)

19.11 WHICH DISCOUNT RATE SHOULD WE USE?

Specifying the correct discount rate to use when a new project involves financing and

other differences from parent company activities is something of a puzzle. Now that we

have examined the main variations on the discount rate theme, this check-list should help.

If the new project has a:

Case 1 Similar business risk and capital structure as the parent company.

Use the parent’s WACC.

Case 2 Higher/lower business risk than the parent but similar financing mix.

Adjust the Beta, using a surrogate firm’s Beta as a basis but adjust for relative

gearing, i.e. ungear the surrogate Beta and gear up the residual equity Beta.

Then use the parent’s capital structure weights to calculate the WACC.

Case 3 Similar business risk, but capital structure different from that of the parent.

Use the parent’s equity Beta, gear it for the project financing mix and then

use the project’s financing mix to find the project WACC.

CFAI_C19.QXD 10/26/05 5:22 PM Page 532

.

Chapter 19 Does capital structure really matter? 533

SUMMARY

Chapters 18 and 19 have covered extensive ground, attempting to isolate the critical

variables relating company value to capital structure. In this process, we have moved

from the somewhat crude ‘traditional’ version to the pure and less pure MM analyses,

before arriving at the model displayed in Figure 19.4. This closely resembles the tradi-

tional theory itself, with its U-shaped cost of capital schedule and optimal capital

structure. We have established that the benefits of debt stem mainly from market imperfec-

tions, especially the tax relief on debt interest, but that a different type of imperfection, distress

costs, can offset these tax breaks at higher levels of gearing. In addition, even the tax bene-

fits of gearing may be overstated as they depend on the particular mix of personal and

corporate tax rates faced by the company and its stakeholders (see Appendix III).

So in response to the question posed at the start of the chapter, ‘Does capital struc-

ture matter?’ the answer seems to be ‘yes’, but in a number of complex ways. Debt, or

rather, excessive debt, certainly matters to the owners but it may not destroy value.

Distressed, but operationally viable, companies can still survive. For non-distressed

companies, debt can offer significant tax advantages.

Key points

■ MM argue that, as the method of financing a company does not affect its funda-

mental wealth-creating capacity, the use of debt capital, under perfect market con-

ditions, has no effect on company value.

■ Shareholders respond to an increase in the likely variability of earnings, i.e. finan-

cial risk, by seeking higher returns to offset exactly the apparent benefits of ‘cheap’

debt.

■ The appropriate cut-off rate for new investment is the rate of return required by

shareholders in an equivalent ungeared company.

■ When corporate taxation is introduced, the tax deductibility of debt interest creates

value for shareholders via the tax shield, but this is a wealth transfer from

taxpayers.

■ The value of a geared company equals the value of an equivalent ungeared com-

pany plus the tax shield:

■ With corporate taxation, the rate of return required by the geared company’s share-

holders is less than that in the all-equity company, reflecting the tax benefits.

■ A further effect of corporation taxation is to lower the overall cost of capital, which

appears to fall continuously as gearing increases.

■ However, this result relies on the absence of default risk and the consequent costs of

financial distress incurred as a company reaches or approaches the point of insolvency.

■ For geared companies, the required return can be derived by combining with the

after-tax debt cost to obtain the WACC.

Continued

k

e

V

g

V

u

TB

Case 4 Higher/lower business risk, and a different capital structure.

Use the project Beta, and, as in Case 2, gear it for the project financing, and

calculate the WACC using the project financing mix.

Case 5 Complex mixture of risk, financial structure, and side effects. Use the APV method.

CFAI_C19.QXD 10/26/05 5:22 PM Page 533

.

534 Part V Strategic financial decisions

■ However, the WACC is acceptable only under restrictive conditions: in particular,

when project financing replicates existing gearing, and when project risk is identi-

cal to that of existing activities.

■ To resolve the problems of the WACC, the adjusted present value can be used. This

is the ‘basic’ worth of the project, i.e. the NPV assuming all-equity financing,

adjusted for any financing benefits such as tax savings on debt interest, or costs

such as issue expenses.

■ Eventually, the costs of financial distress may begin to outweigh the benefits of the

tax shield. A major cost of financial distress is the inability to achieve ‘full market

value’ in a ‘distress sale’.

■ There is, in theory, an optimal capital structure where the marginal benefit of tax

savings equals the marginal cost of financial distress.

■ In reality, while companies should balance the benefits of the tax shield against the

likelihood of financial stress costs, most finance directors will restrain gearing lev-

els, especially as tax savings are uncertain, depending on fluctuations in corporate

earnings.

Further reading

Look at the original articles by Modigliani and Miller (1958, 1963). Other important articles are

those by Myers (1974, 1984), which analyse the interactions between financing and investment

decisions, and Miller’s attempt to resurrect the capital structure irrelevance thesis (1977) and his

subsequent Nobel lecture (1991). As ever, Copeland and Weston (2004) offer a more rigorous,

mathematical development. A resumé of current thinking on capital structure theory can be

found in Barclay et al. (1995). Luehrman (1997a,b) offers two articles on the present state of val-

uation theory and analysis, with strong emphasis on APV, and also on strategic options.

APPENDIX I

DERIVATION OF MM’S PROPOSITION II

Given that:

and

we may write

Substituting for E,

k

e

k

o

1V

S

V

B

2 iB

V

S

k

o

V

S

k

o

V

B

iB

V

S

k

o

1k

o

i2

V

B

V

S

E k

o

V

o

k

o

1V

S

V

B

2

k

e

1E iB2

V

S

E

V

S

V

B

E

V

o

k

o

CFAI_C19.QXD 10/26/05 5:22 PM Page 534