Pike Robert, Neal Bill. Corporate finance and investment: decisions and strategy

Подождите немного. Документ загружается.

.

Chapter 20 Acquisitions and restructuring 555

Fewston’s shareholders are thus left with only million of the net gains from the

takeover, 20 per cent lower than in the cash offer case, which is the same proportion as

the share of the expanded company handed to Dacre’s shareholders.

A share exchange of equivalent value to a cash bid generally leaves the bidder’s

shareholders worse off compared to a cash deal because their share of both the com-

pany and the gains from the takeover are diluted among the larger number of shares.

The post-bid share prices in these two cases are as follows:

Against this, given that takeovers carry risks, for example, the risk of inability to

capture the anticipated synergies, a share-based deal has the merit of transferring a

portion of these risks to the targets’ former owners.

However, if Fewston has to borrow in order to make the cash bid, the increase in

gearing may result in shareholders seeking a higher return, thus lowering the market

price. In addition, the analysis hinges on the existence of an efficient capital market

whose assessment of the gains from takeover corresponds with that of the two parties.

Share exchange:

1£260 m>125 m2 £2.08

Cash bid:

1£260 m>100 m2 £2.60

£8

20.6 WORKED EXAMPLE: ML PLC AND CO PLC

The following question appeared on the CIMA Strategic Financial Management exam-

ination paper, May 1999. (It carried 15 of the total 20 marks available.)

■ Question

ML plc is an expanding clothing retailer. It is all-equity financed by ordinary share cap-

ital of million in shares of 50p nominal. The company’s results to the end of March

1999 have just been announced. Pre-tax profits were million. The Chairman’s state-

ment included a forecast that earnings might be expected to rise by 5 per cent per

annum in the coming year and for the foreseeable future.

CO plc, a children’s clothing group, has an issued share capital of million in

shares. Pre-tax profits for the year to March 31 were million. Because of a recent

programme of reorganisation and rationalisation, no growth is forecast for the current

year but, subsequently, constant growth in earnings of approximately 6 per cent per

annum is predicted. CO plc has had an erratic growth and earnings record in the past

and has not always achieved its often ambitious forecasts.

ML plc has approached the shareholders of CO plc with a bid of two new shares in

ML plc for every three CO plc shares. There is a cash alternative of 135 pence per share.

Following the announcement of the bid, the market price of ML plc shares fell while

the price of shares in CO plc rose. Statistics for ML plc and two other listed companies

in the same industry immediately prior to the bid announcement are shown below. All

share prices are in pence.

£5.2

£1£33

£4.6

£10

Self-assessment activity 20.4

Predator is valued on the market at £1,000 million, and Prey at £200 million. Predator val-

ues the expected post-merger synergies at £50 million. If it bids £230 for Prey what is the

NPV of the bid? What is the share of the gains for each firm?

(Answer in Appendix A at the back of the book)

CFAI_C20.QXD 10/28/05 5:25 PM Page 555

.

556 Part V Strategic financial decisions

Both ML plc and CO plc pay tax at 33 per cent.

ML plc’s cost of capital is 12 per cent per annum and CO plc’s is 11 per cent per

annum.

Required

Assume you are a financial analyst with a major fund manager. You have funds invest-

ed in both ML plc and CO plc.

■ Assess whether the proposed share-for-share offer is likely to be beneficial to the

shareholders in ML plc and CO plc, and recommend an investment strategy based

on your calculations.

■ Comment on other information that would be useful in your assessment of the bid.

Assume that the estimates of growth given above are achieved and that the new

company plans no further issues of equity.

State any assumptions that you make.

■ Answer

First of all, some introductory calculations are needed, before we can analyse the

impact of the bid.

Basic information

ML CO Combined

Profit after tax (PAT) for each firm is

ML: CO:

Given respective P:Es, market values are:

ML: CO:

Given the number of shares, share price is:

ML: CO:

EPS:

ML: CO: 15.41p 10.56p

Analysis

Assessment

Assuming no changes in the level of market prices, and no re-rating of the sector,

ML’s share price would fall post-acquisition to At this price, the value of the£2.18.

Cash value of bid per 3 shares offered: 1£1.35 32

£4.05

Value of bid at post-issue price

12 shares £2.182 £4.36

1£91.520 m>42,0002 £2.18

Expected market prices post-bid Total market value>No of shares

No. of shares post-bid: 20,000 12>3 33,0002 42,000

1£3.484 m>33,00021£3.082 m>20,0002

£1.37£2.311£45.290 m>33,00021£46.230 m>20,0002

£91.520 m£45.290 m£46.230 m113 1£3.4842115 £3.0822

£6.566 m£3.484 m£3.082 m10.67 £5.2 m210.67 £4.6 m2

1998

High Low Company Dividend % Yield PER

225 185 ML plc 3.4 15

145 115 CO plc 3.6 13

187 122 HR plc 6.0 12

230 159 SZ plc 2.4 17

CFAI_C20.QXD 10/28/05 5:25 PM Page 556

.

Chapter 20 Acquisitions and restructuring 557

2-for-3 share offer should attract CO shareholders. They would get shares worth

in exchange for shares currently worth

The share-for-share offer is also worth more than the cash alternative: vs.

This is a ‘reverse takeover’, where the shareholders of the target end up holding a

majority stake in the expanded company – but who gains from this?

Former CO shareholders would hold (22,000/42,000) of the

value of the expanded firm, a gain of value of CO)

£2.649 m.

ML shareholders would lose making the share-financed deal distinctly

unattractive to them.

Conversely, the cash offer would create wealth for ML shareholders, i.e. they give

for something worth post-bid.

The advice to the fund manager is: ‘accept the bid in respect of CO shares and sell

ML shares in the market if you can achieve a price above ’.

Commentary on other information required

The advice given above hinges on the behaviour of ML’s share price – it has already

fallen on the announcement, but by how much? It may already be too late if the mar-

ket is efficient, as it would already have digested the information contained in the

announcement.

Also:

■ What benefits are expected from the merger, i.e. cost savings and synergies? To

make sense of the bid, ML must be setting the PV of these benefits above

to yield a positive NPV for the acquisition.

■ How quickly are these benefits likely to show through? Any delay in exploiting

these lowers the NPV.

■ It is feasible that the market might apply a higher PER to the expanded company –

maybe not as high as ML’s but possibly at the market average, currently 14.25, com-

pared to the weighted average PER for ML/CO of 14.

■ Is ML likely to sell part of CO’s operations? And to whom? If ML has already lined

up a buyer, it must expect to turn a profit on the deal.

■ Is the bid likely to be defended by the target’s managers, fearful for their jobs? If so,

a higher bid might be expected.

■ Is a White Knight likely to appear with a higher bid on more favourable terms?

■ Are there competition implications likely to attract the interest of the authorities?

£2.649 m

£2.18

£4.11£4.05

£2.649 m,

1£47.939 m £45.290 m pre-bid

£91.520 m £47.939 m

£4.05.

£4.36

13 £1.372 £4.11.12 £2.182 £4.36

20.7 THE IMPORTANCE OF STRATEGY

Considerable evidence has emerged that acquisitions have less than an even chance of

success. Although definitions of ‘success’ may vary, any activity that fails to enhance

shareholder interests is unlikely to be regarded favourably by the stock market. While

it is often difficult to assess what would have happened had a company not embarked

on the takeover trail, it is difficult to argue that the acquisition has not been a failure if

post-acquisition performance is inferior to pre-acquisition performance, or if the acqui-

sition actually leads to a fall in shareholder wealth.

The McKinsey firm of management consultants studied the ‘value-creation per-

formance’ of the acquisition programmes of 116 large US and UK companies, using

financial measures of performance. The criterion of success used was whether the

company earned at least its cost of capital on funds invested in the acquisition process.

On this basis, a remarkable 60 per cent of all acquisitions failed, with large unrelated

takeovers achieving a failure rate of 86 per cent.

CFAI_C20.QXD 10/28/05 5:25 PM Page 557

.

558 Part V Strategic financial decisions

Acquisitions fail for numerous reasons:

1 Acquirers often pay too much for their targets, either as a result of a flawed evalu-

ation process that overestimates the likely benefits or as a result of getting caught

up in a competitive bidding situation, where to yield is regarded as a sign of cor-

porate weakness.

2 ‘Skeletons’ appear in cupboards with alarming frequency. The disastrous takeover

by Ferranti of International Signal Corporation (see Chapter 4) was a good example

of a badly researched acquisition that ultimately destroyed the acquirer.

3 Acquirers often fail to plan and execute properly the integration of their targets, fre-

quently neglecting the organisational and internal cultural factors. Inadequate

knowledge about the target’s business should be corrected in the process of due

diligence. Lees (1992) explains how all too often this aspect is overlooked.

Yet many companies have sound acquisition records. Their targets are carefully

selected, they rarely get involved in competitive auctions, they often have the sense to

walk away from deals when they realise the gravity of the likely integration problems,

and they seem able quickly and successfully to integrate acquisitions once deals are

completed. What these companies have in common is a coherent strategic approach to

acquisitions.

20.8 THE STRATEGIC APPROACH

Most successful acquirers see their acquisitions as part of a long-term strategic process,

designed to contribute towards overall corporate development. This requires acquirers

to approach acquisitions only after a careful analysis of their own underlying strengths,

and to identify candidates that satisfy chosen criteria and, most importantly, provide

‘strategic fit’ with the company’s existing activities.

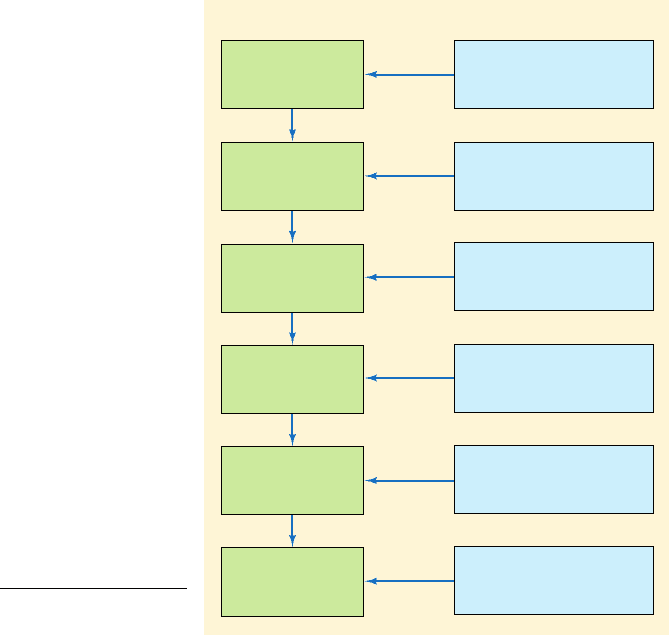

Figure 20.1 displays a simple strategic framework within which a thorough-going

acquisition programme might be conducted. It begins with a full strategic review of

the company as it stands, and its strategic options, followed by a detailed consideration

of the role of acquisitions (i.e. the reasons why an acquisition target may be selected),

leading to the process of selecting and bidding for the chosen prey, and culminating in

the often neglected activities of post-merger integration and post-audit.

■ Objectives

Formulating strategy should begin with an expression of corporate objectives, concen-

trating on maximising shareholder wealth. Many firms now publish mission state-

ments, but these are usually somewhat vague expressions of the image that the

company would like to portray, often largely for internal consumption in order to moti-

vate staff (Klemm et al., 1991). If, in building the desired image, the company’s man-

agers fail to earn at least the cost of equity, they will themselves invite the risk of

takeover. Strategy concerns the examination of alternative routes to achieving the ulti-

mate aim, and then the optimal way of executing the chosen path. Achieving long-term

goals usually involves expansion of the enterprise, a route often preferred by managers

for personal motives.

■ Internal or external growth?

There are two main ways of achieving growth: (1) by self-development of new prod-

ucts, markets and processes (internal growth) and (2) by acquisition (external

growth). Although both of these routes are usually expensive in executive time and

resources, external growth has the advantage of securing quick access to new markets

CFAI_C20.QXD 10/28/05 5:25 PM Page 558

.

Chapter 20 Acquisitions and restructuring 559

Formulation

of corporate

strategy

Assess role

of acquisition

Screen, evaluate,

select

Make approach

and

complete deal

Integration

Post

audit

• Corporate objectives

• Self analysis

• Strategic options

• Acquisition approaches

• Acquisition criteria

• Analyse potential targets

• Valuation

• Identify specific target

Bid(s) if quoted;

approach and

negotiate if unquoted

Jones’ integration

sequence (see below)

Did we do it correctly?

Would we do it again?

Key Elements

Figure 20.1

A strategic framework

(based on Payne, 1985)

or productive capacity. However, firms should not overlook intermediate strategies,

such as licensing, whereby a royalty is paid to the developer of new technology in

exchange for rights to exploit it, or joint ventures, where an existing company could

be partially acquired, or a totally new one set up in partnership with another firm.

The decision to grow internally or externally will depend partly on an analysis of

the strengths, weaknesses, opportunities and threats (SWOTs) of the firm. This self-

analysis should make the potential acquirer aware of any competitive advantages it

enjoys over rival companies. Competitive advantage stems from two sources: cost

advantage, where products are virtually similar, and product differentiation.

Exploitation of each of these creates value for shareholders. When areas of competitive

advantage have been identified, the company can decide whether to build upon exist-

ing strengths or to attempt to develop distinctive competence in areas of perceived

weakness. This evaluation may also result in a decision to divest certain activities

where no obvious advantage is possessed, or where too many resources would be

required to sustain an advantage.

Porter (1987) examined the acquisition record of 33 large diversified US companies.

The criterion for judging ‘success’ was the subsequent divestment rate of earlier acqui-

sitions. The main finding was that successful acquirers almost invariably diversify into

related fields, and vice versa. In other words, diversifications into activities unrelated

to the core business of the acquirer carry much greater risks of failure. Even compa-

nies with successful ‘related diversification’ records achieved poor results when they

wandered into unrelated fields. Porter concluded that the corporate portfolio strategy

of many diversifying companies had failed because most diversifiers fail ‘to think in

terms of how they really add value’.

CFAI_C20.QXD 10/28/05 5:25 PM Page 559

.

560 Part V Strategic financial decisions

■ Acquisition criteria

The bidder should next assess what specific role it hopes the acquisition will perform.

Table 20.5, drawn from a publication (Making an Acquisition) by the merchant bank 3i

(Investors in Industry), which specialises in offering acquisition advice, lists possible

strategic reasons for acquisition with suggested routes to achieving the stated aims.

At this stage, the company should reassess the alternatives to merger, in view of the

many difficulties involved. Taking over another company is rather like moving to a

larger, more expensive house. Mergers involve considerable disruptions during the

planning and bidding phase; costs, such as legal advice and the printing and publish-

ing of documents; possible exposure to increased financial risk; and the upheavals of

integration. Just as some marriages do not survive the strains of house-moving, some

companies often fail to recover after the stress of merger. Having identified the specif-

ic role of the acquisition, the company can now consider whether it can be achieved in

other, perhaps more cost-effective ways.

Harrison (1987) suggests that, for every merger motive, there are several alternative

ways of achieving the same end. For example, if the aim is sales growth, this can be

achieved by internal expansion or by a joint venture. If the aim is to improve earnings

per share, a loss-making subsidiary can be shut down or efficiency-enhancing measures

can be implemented. If it is wished to use spare cash, this can be invested in marketable

securities and trade investments, or even returned to shareholders as dividends, or in

the form of share repurchases. If an improvement in management skills is sought,

appropriately skilled personnel can be bought in to replace existing managers, outside

consultants can be used for advice, or incentive and bonus schemes can be introduced.

In short, if the decision to grow by acquisition is made, the potential acquirer must be

very sure that the stipulated aims are unattainable by alternative measures.

Table 20.5

Strategic opportunities

Where you are How to get to where you want to be

■ Growing steadily but in a mature ■ Acquire a company in a younger

market with limited growth market with a higher growth rate

prospects

■ Marketing an incomplete product ■ Acquire a company with a

range, or having the potential to complementary product range

sell other products or services to

your existing customers

■ Operating at maximum productive ■ Acquire a company making

capacity similar products operating

substantially below capacity

■ Under-utilising management ■ Acquire a company into which

resources your talents can extend

■ Needing more control of suppliers ■ Acquire a company which is,

or customers or gives access to, a significant

customer or supplier

■ Lacking key clients in a targeted ■ Acquire a company with the right

sector customer profile

■ Preparing for flotation but needing ■ Acquire a suitable company which

to improve your Balance Sheet will enhance earnings per share

■ Needing to increase market share ■ Acquire an important competitor

■ Needing to widen your capability ■ Acquire a company with the key

talents and/or technology

Source:

3i (Investors in Industry).

CFAI_C20.QXD 10/28/05 5:25 PM Page 560

.

Chapter 20 Acquisitions and restructuring 561

Most firms with corporate planning departments exercise a continuous review of

the key members of the industry in which they operate and also of related and, often,

unrelated areas. Some firms are known to ‘track’ several dozen potential takeover can-

didates, assessing their various strengths and weaknesses, and estimating the likely

net value obtainable if they were acquired. Such target companies are continually

cross-checked against a set of possible acquisition criteria.

When the decision to expand by acquisition is taken, the corporate planning staff

should be able rapidly to provide a short-list of candidates, expressing the SWOTs of

each, especially its vulnerability to takeover at that time. It is common for defending

managements to dismiss takeover bids as ‘opportunistic’ in a pejorative way. For an

acquisitive company that adopts the strategic approach, this means ‘well-timed’, as

such companies are continually seeking opportune moments to launch a bid, espe-

cially when the stock market rating of the target appears low. The joint takeover by the

former GEC and Siemens of Plessey was opportunistic, in the sense that the target’s

return on capital was relatively low due to a recent substantial investment pro-

gramme. Whether the market had correctly valued Plessey is arguable, but the bidders

undoubtedly spotted a favourable opportunity to acquire Plessey at a time when its

performance looked weak in relation to the market, thus eliminating a major competi-

tor for lucrative British Telecom contracts.

■ Bidding (and defending)

Bidding is an exercise in applied psychology. Readiness to bid implies an assessment

that the target is either undervalued as it stands or would be worth more under alter-

native management. In such cases, the bid itself provides new information about

prospective value, and the bidder should expect to have to pay above the market price

to secure control. However, it is often unclear before the event how much of a bid pre-

mium, if any, is already built into the market price as the market attempts to assess the

probability of a bidder emerging and succeeding with its offer. The trick in mounting

profitable takeover bids is to promise to use assets more effectively in order to entice

existing shareholders to sell, without making such extravagant claims that the target’s

market price moves up too sharply before the acquisition is completed. Conversely, to

accentuate the difficulties of reorganising the target could be regarded as disingenu-

ous or even call into question the wisdom of the bid itself, leading to a fall in the bid-

der’s own share price. The following box summarises some of the defence tactics

which a bidder may encounter.

Choose your weapons! Takeover defence tactics

Takeover strategy is not a one-sided affair. Very few takeovers are recommended at once by

the directors of target companies. Even if they expect to lose the fight, the incumbents usu-

ally reject the initial bid in the hope of attracting better terms. The first line of defence,

therefore, is rejection because the bid is too low, or because the proposed union ‘lacks

industrial logic’.

Once defenders have had time to marshal their resources and get their public relations act

together, more effective defences can be adopted. Some are more credible than others, and some

are illegal in the UK but common in the USA. Typical defence ploys by UK firms are:

■ Revalue assets – this is often a waste of time, as the market should already have assessed

the market value.

■ Denigrate the profit and share price record of the bidder, and hence the quality of its man-

agement. This invites retaliation in kind.

Continued

CFAI_C20.QXD 10/28/05 5:25 PM Page 561

.

562 Part V Strategic financial decisions

News Corp unveils poison pill defence strategy

Murdoch’s board acts to ward off any Liberty Media bid after Malone raises voting interest

FT

News Corp, the media group

led by Rupert Murdoch, yester-

day unveiled a ‘poison pill’ to

ward off a potential takeover

bid from Liberty Media.

Under the plan, approved at

a weekend board meeting,

News Corp shareholders would

be offered deeply discounted

stock under an 8-for-1 rights

issue in response to any

approach from a predator. The

move follows last week’s share

options deal by Liberty Media,

the media investment group

controlled by John Malone, to

raise its voting interest in

News Corp from 9 per cent to

a possible 17 per cent.

Mr Malone, Liberty’s chair-

man and controlling sharehold-

er, had assured Mr Murdoch

that he was not planning a hos-

tile approach.

Yesterday, officials at Liberty,

whose other assets include

49 percent of the Discovery

Network, insisted the company

was ‘a News Corp ally’. Liberty

will face further questions

on its intentions when it

announces third quarter

results today.

News Corp acted amid fears

that Liberty could emerge as

its largest voting shareholder –

eclipsing the Murdoch family’s

29.5 per cent controlling stake.

Without a poison pill, ana-

lysts said Liberty could end

up with 49 per cent of News

Corp’s voting interests by

swapping its 421.6 m Class A

ordinary shares for Class B

voting stock. News Corp can-

not prevent Liberty increas-

ing its voting stake to 17 per

cent under last week’s share-

swap but a rights issue would

be triggered if Liberty acquired

more than an additional 1 per

cent of the company. The poi-

son pill could also be activated

if any other predator gained

more than 15 per cent of vot-

ing stock.

■ Promise a dividend increase – this calls past dividend policy into question, and bidders usu-

ally offer this anyway.

■ Publish improved profit forecasts – a dangerous ploy, since the forecast has to be plausible

yet attractive, and once made, the company has to deliver. Companies that repel raiders but

fail to meet profit forecasts are susceptible to further bids.

■ Seek a White Knight – an alternative suitor that will acquire the target on more favourable

terms (mainly for the management?).

■ Lobby the competition authorities.

The following defences mostly originated in the USA and some are difficult to reconcile

with the City Code:

■ The Crown Jewels defence – selling-off the company’s most attractive assets.

■ Issuing new shares into friendly hands – this, of course, requires shareholder agreement.

■ The Pacman defence – launching a counter-bid for the raider.

■ Golden Parachutes – writing such attractive severance terms for managers that the bidder

will recoil at the prospective expense.

■ Tin Parachutes – offering excessively attractive severance terms for blue collar workers.

■ Launching a bid for another company – if successful, this will increase the size of the firm,

making it less digestible for the bidder.

■ Leveraged buy-out – the purchase of the company by its own management using large

amounts of borrowed funds.

■ Poison pills – undertaking methods of finance that the bidder will find unattractive to

unwind, e.g. large issues of convertibles that the bidder will have to honour.

■ Repurchasing of shares to drive up the share price and increase the cost of the takeover

(common now in the UK), although not allowed once an informal approach has been made

(although it can be promised if the bid fails).

CFAI_C20.QXD 10/28/05 5:25 PM Page 562

.

Chapter 20 Acquisitions and restructuring 563

Probably the most difficult part of takeover strategy and execution is the integration of

the newly acquired company into the parent. In the case of contested bids, the acquir-

er will normally have only a limited amount of information to guide its integration

plans and should not be too shocked to encounter unforeseen problems regarding the

quality of the target’s assets and personnel. The difficulty of integration depends on the

extent to which the acquirer wants to control the operations of the target. If only limit-

ed control is required, as in the case of unrelated acquisitions, integration will probably

be restricted to meshing the financial reporting systems of the component companies.

Conversely, if full integration of common manufacturing activities is required, integra-

tion assumes a different order of complexity.

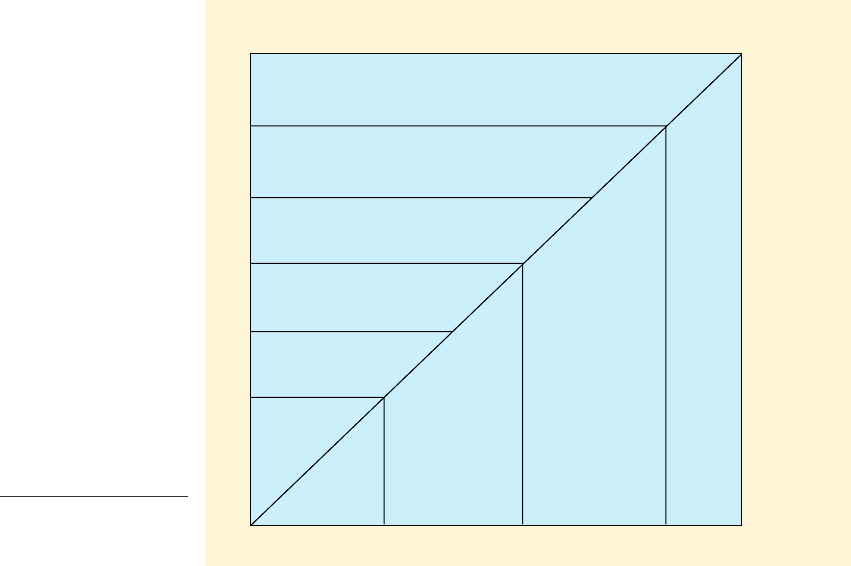

Jones (1982, 1986) points out that the degree of complexity of integration depends

on the type of acquisition: for example, whether it is a horizontal takeover of a very

similar company, requiring a detailed plan for integrating supply, production and dis-

tribution; or, at the other extreme, a purely conglomerate acquisition where there is lit-

tle or no overlap of functions. The relationship between type of acquisition, overlap of

activity (split into financial, manufacturing and marketing) and the resulting degree of

integrative complexity is shown in Figure 20.2. Because we believe that integration is

perhaps the most important part of the acquisition process, we devote most of the fol-

lowing section to further analysis of this issue.

Finally, the acquisition should be post-audited. The post-audit team should review

the evaluation phase to assess whether, and to what extent, the appraisal was under-

or over-optimistic, and whether appropriate plans were formulated and executed. The

review should centre on what lessons can be learned to guide any subsequent acqui-

sition exercise.

Poor planning and poorly-executed integration are two of the commonest reasons

for takeover failure. All too often, acquisitive companies focus senior management

attention on the next adventure rather than devoting adequate resources to absorbing

the newly acquired firm carefully. It is rash to lay down optimal integration proce-

dures in advance, because the appropriate integration procedures are largely situa-

tion-specific. The ‘right’ way to approach integration depends on the nature of the

company acquired, its internal culture and its strengths and weaknesses (Lees, 1992).

However, Drucker (1981) contends that there are Five Golden Rules to follow in the

integration process:

1 Ensure that acquired companies have a ‘common core of unity’ with the parent. In

his view, mere financial ties between companies are insufficient to obtain a bond.

20.9 POST-MERGER ACTIVITIES

News Corp said Liberty decid-

ed to increase its potential vot-

ing rights without alerting the

company. ‘For this and other rea-

sons the company has put in

place a rights plan to protect the

best interests of all sharehold-

ers,’ the statement added.

News Corp – whose assets

including controlling stakes in

British Sky Broadcasting and

DirecTV, the largest US cable

operator – will need to seek

shareholder approval to renew,

the poison pill arrangements

after 12 months. If the plan is

triggered, News Corp share-

holders will receive rights

allowing them to acquire shares

at a 50 per cent discount.

Analysts at Goldman Sachs

said: ‘Effectively, this is a 8-

for-1 rights issue in which a

hostile acquirer cannot partic-

ipate.’ Mr Malone took options

to acquire stock in News Corp

after the group completed its

re-incorporation from an

Australian-domiciled group to

a full US listing.

Liberty Media declined to

comment on the poison pill.

But some analysts warned

that News Corp’s action would

be seen as defensive. In

Australia, News Corp stock fell

4.3 per cent to A$22.69.

Source: Tim Burt, Financial Times,

19 November 2004.

CFAI_C20.QXD 10/28/05 5:25 PM Page 563

.

564 Part V Strategic financial decisions

The companies should have significant overlapping characteristics like shared tech-

nology or markets in order to exploit synergies.

2 The acquirer should think through what potential skill contribution it can make to

the acquired company. In other words, the takeover should be approached not sole-

ly with the attitude of ‘what’s in it for the parent?’, but also with the view ‘what can

we offer them?’

3 The acquirer must respect the products, markets and customers of the acquired

company. Disparaging the record and performance of less senior management is

likely to sap morale.

4 Within a year, the acquirer should provide appropriately skilled top management

for the acquired company.

5 Again, within a year, the acquirer should make several cross-company promotions.

These are largely common-sense guidelines, with a heavy emphasis on behaviour-

al factors, but many studies have shown that acquirors fail to follow them. A study

undertaken by Hunt and Lees of the London Business School with Egon Zehnder

Associates (Hunt et al. 1987) commented that ‘unless the human element is managed

carefully, there is a serious risk of losing the financial and business advantages that the

acquisition could bring to the parent company’.

■ Jones’s integration sequence

Jones (1986) explains that integration of a new company is a complex mix of corporate

strategy, management accounting and applied psychology. Acquirors should follow an

‘integration sequence’, based on five key steps, the relative weight attaching to each

step depending on the type of acquisition. The sequence is as follows:

1 Decide upon and communicate initial reporting relationships.

2 Achieve rapid control of key factors.

Degree of

integrative

complexity

High

LowFunctional activity changed

Horizontal acquisitions – complete absorption

Horizontal acquisition – overlapping manufacturing

Vertical acquisition

Horizontal acquisition –

overlapping products

or markets

Concentric

acquisition

Conglomerate

acquisition

Marketing

+

Financial

control

Manufacturing

+

Financial

control

Financial

control

Manufacturing + Marketing + Financial control

Class of acquisition

Figure 20.2

Type of acquisition and

integrative complexity

(Jones, 1986)

CFAI_C20.QXD 10/28/05 5:25 PM Page 564