Pike Robert, Neal Bill. Corporate finance and investment: decisions and strategy

Подождите немного. Документ загружается.

.

Chapter 20 Acquisitions and restructuring 545

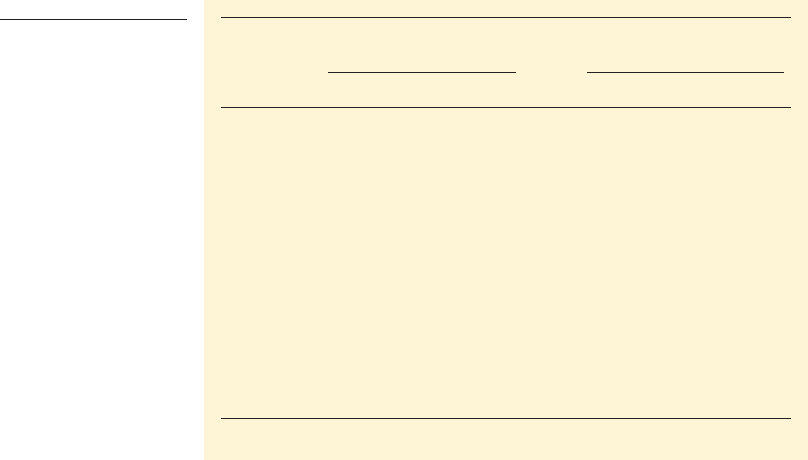

Table 20.3

Cross-border acquisi-

tions involving UK

companies

UK firms acquired UK firms’ acquisitions

by foreign firms of foreign firms

Year Number Value Number Value

1992 210 4,139 679 7,264

1993 267 5,187 521 9,213

1994 202 5,213 422 15,164

1995 131 12,817 365 11,967

1996 133 9,513 442 13,377

1997 193 15,717 464 19,176

1998 252 32,413 569 54,917

1999 252 60,860 590 111,193

2000 227 64,618 557 181,285

2001 162 24,382 371 41,473

2002 117 16,798 262 26,626

2003 129 9,309 243 20,756

2004 171 29,815 278 20,321

Source: National Statistics, 2005 (First Release, www.statistics.gov.uk).

acquisitions by UK firms of overseas enterprises. Although it is by no means one-way

traffic, in most years, UK firms’ involvement in takeover activity as acquirors out-

weighs their involvement as acquirees. Again, 2000 was the peak year in both cate-

gories by value.

However, 2001 saw a substantial drop in world merger activity, falling from

$3.5 trillion in 2000 to $1.75 trillion, marking an end to eight straight years of increased

activity. Three main reasons were put forward for this:

■ Companies whose finances were damaged by the worsening economic recession

had insufficient cash resources to hunt prey.

■ Stock market volatility made it difficult to assess market values, and hence, bid

valuations.

■ Increasingly uncertain business conditions increased the difficulty of predicting the

future profitability of acquisitions.

2001 was described as ‘the year of the broken promise’ because many large take-overs

failed to come to fruition. Among the jilted partners were German media giant

Bertelsmann and EMI, British banks Abbey National and Lloyds TSB, telecom giants

Alcatel and Lucent, and, notoriously, Dynergy and Enron. Moreover, the European

competition authorities blocked the takeover of Honeywell by GE on the grounds that

competition would be harmed within Europe, thus raising the prospect of more active

scrutiny of future amalgamations. However, on the EU front the reverse has occurred.

Following three dramatic reversals of its policy decisions in the European Court of First

Instance in 2002, the EU has introduced a new merger Directive which many regard as

more ‘friendly’ towards merging firms. This may help to explain the uptick in activity

involving UK firms in 2004.

■ The regulation of takeovers

UK takeovers are regulated in three ways, two of them formal and the third informal.

First, the UK statutory provisions as laid down in the Fair Trading Act 1973 and the

Competition Act 1998 give responsibility for dealing with mergers to three entities:

■ The Secretary of State for Trade and Industry (the SOS).

CFAI_C20.QXD 10/28/05 5:25 PM Page 545

.

546 Part V Strategic financial decisions

■ The Director General of Fair Trading (the DGFT).

■ The Competition Commission (the CC).

The system relies on flexible interpretation of the regulations, and intervention at

the discretion of the authorities. In principle, mergers are judged as to whether they

are against the ‘public interest’. In practice, this means whether they are likely to

reduce competition. The burden of proof lies on the authorities to prove that the merg-

er is harmful, rather than the parties having to prove that it is beneficial. The authori-

ties are heavily dependent on information provided by the parties to the merger.

The role of the DGFT is to:

■ assess mergers that come to his attention, e.g. by complaints or by notification by

the firms involved.

■ consider whether a merger qualifies for reference to the CC for more detailed inves-

tigation, i.e. whether worldwide assets taken over exceed million, or whether a

UK market share above 25 per cent is to be created.

■ hear the view of interested parties relating to qualifying mergers.

■ advise the SOS on whether qualifying mergers should be referred to the CC for

investigation whether the merger is against the public interest.

■ where appropriate, advise the SOS on accepting ‘statutory undertakings’, e.g. prom-

ises to divest assets, in lieu of reference to the CC.

■ advise the SOS on action in response to the CC report.

■ seek undertakings from the parties involved.

■ monitor compliance with undertakings.

The Secretary of State’s role is:

■ to decide whether a merger should be referred to the CC.

■ to decide whether to accept undertakings in lieu of reference.

■ to receive and publish the CC report.

■ to decide on action in response to the report.

In response to an adverse report, the SOS may decide:

■ to block the merger.

■ to require the parties to meet certain conditions before approval.

The role of the CC is:

■ to hear evidence from all interested parties

■ to weigh the evidence to decide whether the merger may operate against the pub-

lic interest.

■ if so, to recommend possible remedies

■ to submit the report to the SOS.

The Department of Trade and Industry website (www.dti.gov.uk/cp/ukmergerguide.htm)

carries a detailed flow chart that summarises these activities and shows how they

interrelate.

The second mode of regulation is under the competition policy of the European

Union, set out in Articles 81 (formerly Article 85) and 82 (formerly 86) of the Treaty of

Rome. Article 82 prohibits the abuse of a dominant firm position insofar as it may

affect trade between member states. The EC Merger Regulation (ECMR) provides that

a merger that creates a dominant position, as a result of which competition would be

significantly impeded, shall be declared incompatible with the common market. The

Regulation applies to all mergers with a ‘Community Dimension’, defined in terms of

turnover levels. The ECMR was designed to provide ‘one-stop’ merger control to

avoid the risk of mergers being investigated under two or more jurisdictions. National

authorities may not normally apply their own competition laws to mergers falling

within the ECMR, which are investigated by the Competition Commission.

£70

CFAI_C20.QXD 10/28/05 5:25 PM Page 546

.

Chapter 20 Acquisitions and restructuring 547

In 2002, the EU was forced to overhaul its procedures after losing three court cases

in which the plaintiffs had challenged the prohibition of their respective mergers. The

Court of First Instance (CFI) criticised both the EU’s procedures and also the quality

of its economic analysis, especially its reliance on the theory of ‘collective dominance’.

The EU’s interpretation of this was that a reduction in the number of competitors in an

industry would necessarily lead to anti-competitive behaviour by the survivors, which

was not necessarily so, according to the CFI. In response, the EU has introduced a

tighter Merger Regulation that came into force in May 2004, which incorporated clear-

er guidelines for firms wishing to merge, including access to official files and to the

investigating officials themselves. The Competition Commission also created a new

post of Chief Economist to enhance the economic expertise at its command. (For fuller

details on EU merger policy, see www.europa.eu.int.)

The third control on takeovers is operated by the Takeover Panel, formed in 1968

to counter the perceived inadequacy of the statutory mechanisms for regulating the

conduct of both parties in the takeover process. The Panel consists of representatives

from City and other leading business institutions, such as the CBI, the Stock Exchange

and the ICAEW accounting body, thus representing the main associations whose

members are involved in takeovers, whether as advisers, shareholders or regulators.

The Panel promulgates and administers the City Code, a set of rules originally with

no force of law, reflecting what those most closely involved with takeovers regard as

best practice. It does, however, have some sanctions to enforce its authority, such as

public reprimands, which damage the reputation of violators of the Code, perhaps

leading to the collapse of the bid and, for financial advisers, to long-term loss of busi-

ness. The Panel’s ultimate sanction is to request its members to withdraw the facilities

of the City from offenders, although this is extremely rare (it has only happened once).

In 2006, a new EU Directive on Takeover Bids is due to come into force. This is very

largely based on the existing UK City Code, but with one important difference in that

it is has statutory backing. Accordingly, in January 2005, the Takeover Panel

announced how it would comply with the new directive. It stated that it ‘would intend

to exercise its power to seek a court order only as a matter of last resort, or in urgent

cases’, i.e. business will be pretty much as usual.

■ The chronology of a hostile bid

The following schedule details the necessary timing of bids and provision of informa-

tion as required by the City Code.

Day 1: bid announced. Bidder has 28 days in which to make a formal offer to tar-

get’s shareholders.

Day 14 after formal offer is made: deadline for target company to publish its ‘defence

document’.

Day 21 after formal offer: first date at which the contest can be ended. Bidder must

disclose how many of target’s shares have been voted in its favour. If over 50 per

cent, bidder has won; if less, it may choose to walk away.

18 days later: last day for defender to produce new arguments to encourage share-

holder loyalty.

4 days later: last day for bidder to increase its offer. Beyond this, bidder cannot buy

any of target’s shares that will take its stake above 30 per cent.

14 days later: by 5 p.m., bidder must declare how many shares have been voted in its

favour. If over 50 per cent, the bidder has won. If less, the target remains independ-

ent. The bidder is barred from making a further bid within one calendar year.

Normally, the maximum time span allowed for the whole process is 60 days,

although the Takeover Panel may ‘stop the clock’ pending clarification of key points.

In the event of a reference to the MMC, the process is halted sine die to await its report.

CFAI_C20.QXD 10/28/05 5:25 PM Page 547

.

548 Part V Strategic financial decisions

This can take upwards of six months, during which the initial ‘urge to merge’ has been

known to evaporate.

The behaviour of defending managers is tightly circumscribed:

1 Shareholders must be given equal access to relevant information to enable them to

make an informed decision.

2 Shareholders must be given adequate information to reach a decision, and no rele-

vant information should be withheld.

3 Directors must not act out of personal interest, either to frustrate or to encourage a

bidder.

4 Directors are prohibited from taking action to frustrate a bona fide offer without the

approval of shareholders.

5 The company must not seek to influence the market price of its shares by offering

finance or guarantees to others to induce them to buy its shares.

The bidder must also observe certain rules:

1 Any stakeholding above 3 per cent must be openly declared.

2 In the past, bidders and their advisers often made ‘dawn raids’ on the market to

capture a major stake in the target before people realised that a bid was under way.

Companies are now prohibited from acquiring, in any seven-day period, shares that

would raise their aggregate stake above 15 per cent.

3 If a company accumulates over 30 per cent of the shares, it must make a formal bid

to remaining shareholders at a price no less than the highest price paid in the pre-

vious twelve months.

20.3 MOTIVES FOR TAKEOVER

Managers seeking to maximise the wealth of shareholders should continually seek to

exploit value-creating opportunities. There are two situations when managers feel able

to enrich shareholders via takeovers:

1 When managers believe that the target company can be acquired at less than its ‘true

value’. This implies disbelief in the ability of the capital market consistently to

value companies correctly. If a company is thought to be undervalued on the mar-

ket, there may well be opportunities for ‘asset-stripping’, i.e. selling off the com-

ponents of the taken-over company for a combined sum greater than the purchase

price.

2 When managers believe that two enterprises will be worth more if merged than if operated

as two separate entities. Thus for two companies, A and B:

The principle of value additivity would refute this unless the amalgamation result-

ed in some form of synergy or more effective utilisation of the assets of the combined

companies.

In practice, it is very difficult to differentiate between these two explanations for

merger, especially as many mergers result in only partial disposals, when activities

that appear to fit more neatly into existing operations are retained. Companies are val-

ued by the market on the basis of information that their managements release regard-

ing market prospects, value of assets, R&D activity, and so on. Market participants

may suspect that an under-performing company could be operated more efficiently by

an alternative management team, but until a credible bidder emerges, poor results

may simply be reflected in a poor stock market rating.

V

A B

7 V

A

V

B

value additivity

The notion that other things

being equal, the combined

present value of two entities is

their separate present values

added together

CFAI_C20.QXD 10/28/05 5:25 PM Page 548

.

Chapter 20 Acquisitions and restructuring 549

■

How different types of acquisition create value

Acquisitions can be split into three types:

1 Horizontal integration – where a company takes over another from the same industry

and at the same stage of the production process: for example, a hotel chain acquiring

a competitor e.g. Greene King’s acquisition of Belhaven Brewer, in 2005. The motiva-

tion is usually enhancement of market power and/or to obtain production economies.

2 Vertical integration – where the target is in the same industry as the acquirer, but

operating at a different stage of the production chain, either nearer the source of

materials (backward integration) or nearer to the final consumer (forward integra-

tion), e.g. Ford’s takeover of Kwikfit.

3 Conglomerate or unrelated diversification – where the target is in an activity

apparently dissimilar to the acquirer although some activities such as marketing

may overlap (known as concentric diversification in this case). These takeovers are

often said to lack ‘industrial logic’, but can lead to economies in the provision of

company-wide services such as Head Office administration and access to capital

markets on improved terms, i.e. financial economies.

In reality, most mergers are difficult to classify into such neat categories, as they are

motivated by a complex interplay of factors, which will hopefully enhance the value

of the bidder’s equity. The more specific reasons cited for launching takeover bids usu-

ally reflect the anticipated benefits that a merger is expected to generate:

1 To exploit scale economies. Larger size is usually expected to yield production economies

if manufacturing operations can be amalgamated, marketing economies if similar

distribution channels can be utilised, and financial economies if size confers access

to capital markets on more favourable terms.

2 To obtain synergy. This term is often used to include any gains from merger, but, strict-

ly, it refers to benefits unrelated to scale. Gains may emerge from a particular way of

combining resources. One company’s managers may be especially suited to operat-

ing another company’s distribution systems, or the sales staff of one company may be

able to sell another company’s, perhaps closely related, product as part of a package.

3 To enter new markets. For firms that lack the expertise to develop different products,

or do not possess the outlets required to access different market segments, takeover

may be a simpler, and certainly a quicker, way of expanding.

The Daimler–Chrysler merger in 1998 was driven by the desire by each firm to

‘fill in’ its product line – Daimler was strong in highly-engineered luxury vehicles

while Chrysler’s expertise lay in volume production of automobiles and the fast-

growing market for sports utility vehicles (SUVs). In December 2001, Britain’s

Compass group, the world’s largest catering company, made a million cash

acquisition of Seiyo Food Systems, Japan’s third-largest contract catering firm, in

order to strengthen its presence in Asia.

4 To provide ‘critical mass’. As many product markets have become more global and the

lifespan of products has tended to diminish, greater emphasis has to be placed on

R&D activities. In some industries, such as aerospace, telecommunications and

pharmaceuticals, small enterprises are simply unable to generate the cash flows

required to finance R&D and brand investment. This factor was largely responsible

for the sale by Fisons and Boots of their drug-development activities in 1994 to

much larger German companies. There is also a credibility effect. For example, com-

panies may be unwilling to use small firms as a source of components when their

future survival, and hence ability to supply, is suspect.

5 To impart or restore growth impetus. Maturing firms whose growth rate is weakening

may look to younger, more dynamic companies both to obtain a quick, short-term

growth ‘fix’, and also for entrepreneurial ideas to achieve higher rates of growth in

the longer term. BAT used the substantial cash flows from its mature tobacco business

to acquire Allied Dunbar (pensions) and Eagle Star (insurance) in the UK and Farmers

in the USA, perceiving the financial services sector as a potential growth area.

£200

CFAI_C20.QXD 10/28/05 5:25 PM Page 549

.

550 Part V Strategic financial decisions

6 To acquire market power. Obtaining higher earnings is easier if there are fewer com-

petitors. Competition-reducing takeovers are likely to be investigated by the reg-

ulatory authorities, but are often justified by the need to enhance ability to

compete internationally on the basis of a more secure home market, as in the case

of the three-way merger of European steel firms mentioned earlier. In addition,

backward vertical integration, mergers undertaken to capture sources of raw

materials (e.g. US oil firm Chevron’s acquisition of Unocal in 2005 to increase its

exploration and production capability), and forward vertical integration to secure

new outlets for the company’s products have the effect of increasing the firm’s

grasp over the whole value chain, and are thus competition-reducing in a wider

sense. Many past brewery takeovers were mounted not to obtain production

capacity, but to secure access to the target’s estate of tied public houses, and to

acquire brands, as in the case of Scottish and Newcastle’s purchase of Theakstons.

7 To reduce dependence on existing, perhaps volatile activities. In Chapter 10, we conclud-

ed that risk reduction per se as a motive for diversification may be misguided. There

is no reason why two enterprises owned by one company should have greater value

unless the amalgamation produces scale economies or some other synergies. If

shareholder portfolio formation is a substitute for corporate diversification, there is

no point in acquiring other companies to reduce risk – rational shareholders will

already have diversified away specific risk, and market risk is undiversifiable.

There are two major qualifications to this argument. First, diversification into over-

seas securities may lower market risk, given that different economies, and hence

stock markets, are not perfectly correlated (Madura, 1995). Second, it is possible

that achieving greater size via conglomerate diversification may lower the costs of

financial distress.

8 To obtain a stock market listing. This is achieved via a ‘reverse takeover’ in which an

unlisted firm acquires a smaller listed firm. This ‘back-door’ method of achieving a

listing is conducted by the listed firm issuing new shares in order to acquire the

unlisted firm. Because of the difference in size, the bidder has to issue so many

shares that the shareholders in the unlisted company emerge with a majority stake

in the expanded firm.

■ The ‘market for management control’

Several of the above motives for merger suggest that some companies can be more effi-

ciently operated by alternative managers. A more general motive for merger is thus to

weed out inefficient personnel. There are three ways in which the market mechanism

can penalise managerial inefficiency:

1 Insolvency, which usually involves significant costs.

2 Shareholder revolt, which is difficult to organise given the diffusion of ownership

and the general reluctance of institutional investors to interfere in operational

management.

3 The takeover process, which may be regarded as a ‘market for managerial con-

trol’. The threat of takeover provides a spur to inefficient managers, while remov-

ing inefficient managers lowers costs and removes barriers to more effective

utilisation of assets. Theory suggests that incompetently managed firms will be

acquired at prices that ensure the owners of the acquirer suffer no loss in value. If

a bid premium over the market price is payable, this should be recoverable from

the higher cash flows generated from more efficient asset utilisation. To this

extent, takeover activity is seen by authors such as Jensen (1984) as a perfectly

healthy expression of the workings of the market system, potentially benefiting

all parties.

CFAI_C20.QXD 10/28/05 5:25 PM Page 550

.

Chapter 20 Acquisitions and restructuring 551

■

Managerial motives for takeover

The motive of diversification to reduce risk suggests a second possible explanation for

takeover activity. With the divorce of ownership and control, and the consequent high

level of managerial autonomy, managers are relatively free to follow activities and poli-

cies, including acquisition of other firms, which enhance their own objectives, both in

monetary and non-pecuniary forms.

Managerial salaries and perquisites are usually higher in large and growing firms,

and since growth by acquisition is usually easier and swifter than organic growth,

managers may view acquisition with some eagerness. If acquisitions are ‘managerial’

in this sense, then acquirers may be prepared to expend ‘excessive’ amounts to gain

ownership of target companies simply to secure deals that promote managerial well-

being, but at the expense of shareholder value. If this explanation is correct, acqui-

sitions may result in a transfer of wealth from shareholders of acquiring firms to

shareholders of acquired companies, even when presented as promoting the best

interests of the former.

Takeovers may also be related to the way managers are remunerated. In the 1980s,

UK managers were increasingly paid by results, with the commonest criterion of per-

formance being growth in EPS. This is a notoriously unreliable measure of perform-

ance, as it is not only dependent on accounting conventions, but relatively easy to

manipulate. For example, shutting down a loss-making activity can raise reported EPS.

Self-assessment activity 20.1

Suggest some ‘managerial’ motives for growth by takeover.

(Answer in Appendix A at the back of the book)

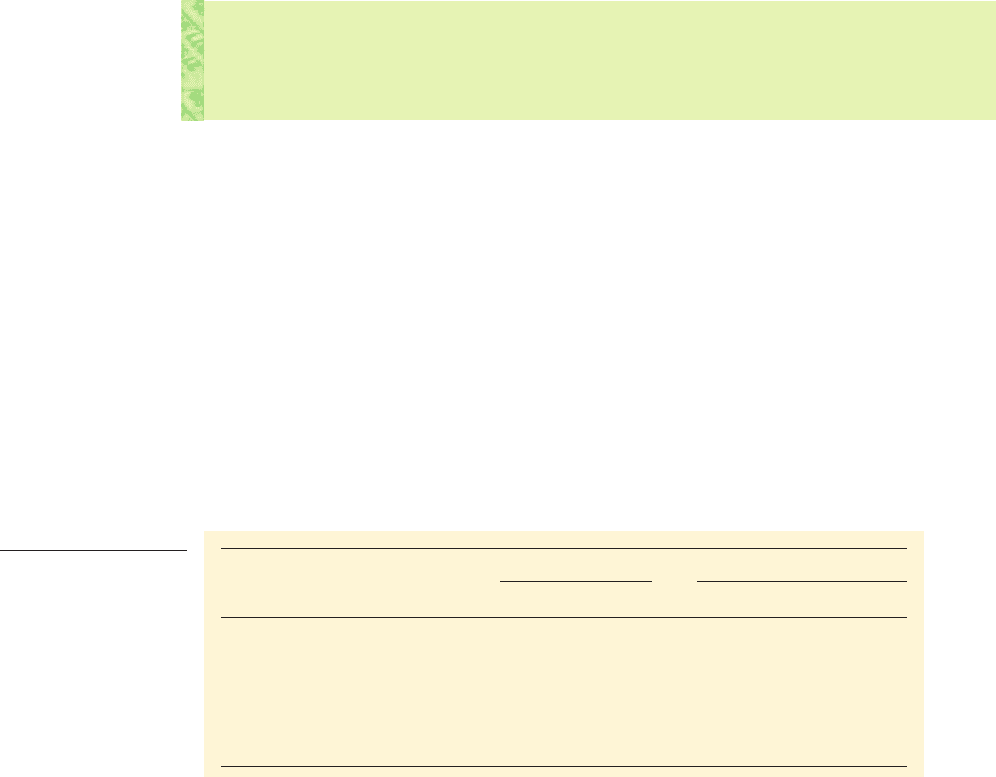

■ How to increase EPS by takeover: Hawk takes over Vole

A common means of increasing EPS has been to acquire other companies with lower

P:E ratios than one’s own, these being companies out of favour with the market, either

through poor performance or because too little was known about them. The acquisition

of such companies, in certain conditions, can raise both EPS and share price. Consider

the example in Table 20.4. Hawk, with a P:E ratio of 20, reflecting strong growth expec-

tations, contemplates the takeover of Vole, whose P:E ratio is only 10. Hawk proposes to

make an all-share offer. If it were able to obtain Vole at the current market price, it would

have to issue 5 million shares to Vole’s shareholders in exchange for their 20 million

shares, i.e.

Table 20.4 shows the impact of the exchange if the P:E ratio of the expanded company

were to remain at 20. The new EPS is resulting in a post-bid share

price of and an overall market value of million. This apparently magical

effect seems to have generated wealth of million. If it works out this way, the£21

£441£4.20,

1£22 m>105 m2 21p,

15 million £42 120 million £12 £20 million.

Table 20.4

Hawk and vole

Pre-bid Post-bid

Hawk Vole

Number of shares 100 m 20 m 105 m

Earnings after tax £22 m

EPS 20p 10p 21p

P:E ratio 20:1 10:1 20:1

Share price £4.20

Capitalisation (market value) £441 m

105 m £4.20£20 m£400 m

20 21p£1£4

£22 m 105 m

£20 m £2 m£2 m£20 m

100 m 5 m

Hawk Vole

CFAI_C20.QXD 10/28/05 5:25 PM Page 551

.

552 Part V Strategic financial decisions

beneficiaries are the two sets of shareholders: Hawk’s existing shareholders find their

100 million shares valued at a price higher by 20p, i.e. million in total, and Vole’s

former shareholders find they now hold shares valued at million, rather than the

value of million placed on Vole prior to the bid, i.e.:

This so-called ‘boot-strapping’ effect may simply be ‘financial illusion’ because

it is unlikely to occur quite like this in reality. First, it assumes the absence of a

bid premium. In practice, Hawk would have to offer above the market price to

tempt Vole’s shareholders into selling, thus altering the balance of gain. Second, it

assumes that the market applies the same P:E ratio to the expanded group as the

pre-bid ratio for Hawk. If no synergies were expected, then the likely post-bid P:E

ratio is the total pre-bid value of the two firms relative to their total pre-bid earn-

ings, i.e.:

However, if Hawk is expected to reorganise Vole and impart the same growth impe-

tus expected from Hawk itself, the P:E ratio post-bid could exceed this figure, and

approach Hawk’s pre-bid P:E value of 20. If this occurs, then both groups of share-

holders can enjoy the value created by the expectation of a more efficient operation of

Vole’s assets and higher cash flows thereafter. Conversely, expectations of integration

difficulties might offset such gains.

It does not follow that a higher EPS will lead to a higher share price. If the acquisi-

tion moved Hawk into riskier areas of operation, its activity Beta should rise accord-

ingly and the higher expected cash flows will be discounted at a higher required

return. Similarly, if instead of financing the bid by a share exchange, Hawk had bor-

rowed the required million, then the share price might not rise if the greater gear-

ing and accompanying financial risk resulted in a higher equity Beta. The suspicion

remains that many acquisitions, including some of the ‘mega-mergers’ of the 1980s,

ostensibly undertaken to raise the acquirer’s share price, were really undertaken for

‘managerial’ reasons (see Gregory, 1997).

Certainly, the subsequent difficulties experienced in post-merger integration and

operation do not support the view that mergers are always in the best interests of the

bidders’ shareholders (see below).

£20

1£400 m £20 m2

1£20 m £2 m2

£420 m

£22 m

19.09

Total gain

ˇ

£21 m

Gains to Vole’s shareholders

ˇˇˇ

£1 m

Gains to Hawk’s shareholders £20 m

£20

£21

£20

20.4 FINANCING A BID

Table 20.1 showed data on the three main ways of financing takeovers: cash, issue of

ordinary shares and fixed-interest securities (loan stock, convertibles and preference

shares). Clearly, the first two methods predominate, although their relative importance

varies over time. As a rule of thumb, share exchange is favoured when the stock mar-

ket is high and rising, while cash offers are used more when interest rates are relative-

ly low or falling, given that many cash offers are themselves financed by the acquirer’s

Self-assessment activity 20.2

Suggest how managerial pay schemes might encourage takeovers against the interests of

shareholders.

(Answer in Appendix A at the back of the book)

CFAI_C20.QXD 10/28/05 5:25 PM Page 552

.

Chapter 20 Acquisitions and restructuring 553

borrowing. This pattern is illustrated clearly by the figures for the early 2000s, when the

stock market was depressed and interest rates low and falling. Increasingly, however,

bidders offer their targets a choice of cash or shares, or even a three-way choice between

straight cash, cash with shares, or shares alone.

For example, in 1991, when bidding for its main UK competitor, Tootal, the textile

company Coats Viyella offered two alternatives. Shareholders of Tootal could either opt

for a full cash consideration of 80p per share, which would not qualify them to receive

an imminent dividend of 3p per share, or accept 83.3p per share in cash and paper,

based on the Coats share price at the date of the offer. The second option involved

in cash and 23 newly issued Coats shares for every 100 Tootal shares owned.

Such complex offers are designed to appeal to the widest possible body of share-

holders. The chosen package depends on the balance of relative advantages and

disadvantages of the different methods, from both the bidder’s and the target

shareholders’ viewpoints.

■ Cash

Everyone understands a cash offer. The amount is certain, there being no exposure to

the risk of adverse movement in share price during the course of the bid. The targeted

shareholders are more easily able to adjust their portfolios than if they received shares,

which involve dealing costs when sold. Because no new shares are issued, there is no

dilution of earnings or change in the balance of control of the bidder (unless, in the case

of borrowed capital, creditors insist on restrictive covenants). Moreover, if the return

expected on the assets of the target exceeds the cost of borrowing, the EPS of the bid-

der may increase, although perceptions of increased financial risk may mitigate this

apparent benefit. A disadvantage from the recipient’s viewpoint is possible liability to

Capital Gains Tax (CGT).

■ Share exchanges

Any liability to CGT is delayed with a share offer, and the cash flow cost to the bidder

is zero, apart from the administration costs involved. However, equity is more costly to

service than debt, especially for a company with taxable capacity, and an issue of new

shares may interfere with the firm’s gearing ratio. There could be an adverse impact on

the balance of control if a major slice of the equity of the bidder came to be held by insti-

tutions looking for an opportunity to sell their holdings. The overhanging threat of a

substantial share sale may depress the share price of the bidder.

■ Other methods

The use of other financing instruments is comparatively rare. When fixed-interest secu-

rities are used, they are usually offered as alternatives to cash and/or ordinary shares.

Convertibles have some appeal because any diluting effect is delayed and the interest

cost on the security, which qualifies for tax relief, can usually be pitched below the

going market rate on loan stock, due to the expectation of capital gain on conversion.

Preference share financing in general is comparatively rare, owing to the lack of tax-

deductibility of preferred dividends and to limited voting rights.

£51.02

Self-assessment activity 20.3

Why might the shareholders of a target company prefer to be paid in cash rather than

shares?

(Answer in Appendix A at the back of the book)

CFAI_C20.QXD 10/28/05 5:25 PM Page 553

.

554 Part V Strategic financial decisions

Evaluating an acquisition is little different from other investments, assuming the

motive of the bid is economic rather than managerial, i.e. designed to maximise the

post-bid value of the expanded enterprise. It would be worthwhile Company A taking

over Company B so long as the present value of the cash flows of the enlarged com-

pany exceeds the present value of the two companies as separate entities:

Thus, measures the increase in value. The net cost to the bid-

der is the value of the amount expended less the value of the target as it stands:

so that the net present value of the takeover decision is the gain less the cost, i.e.:

The NPV will depend on the method of financing and, of course, the terms of the

transaction. Essentially, the bidder is hoping to extract the maximum value of any expect-

ed cost savings and synergies from the takeover for its own shareholders. Conversely, the

offer must be made attractive to the owners of the target to induce them to sell.

■ Fewston plc and Dacre plc

An example will illustrate the way in which the division of the spoils can depend on

the method of financing. Fewston plc is launching a cash bid for Dacre plc, both are

quoted companies and both are ungeared. The market value of Fewston is million

(100 million 50p shares, market price ) and that of Dacre is million (10 million 50p

shares, market price ). Fewston hopes to exploit synergies, etc., worth million

after the takeover. It offers the shareholders of Dacre million in cash. The NPV of

the bid to Fewston is thus:

The overall gain from the takeover (i.e. the synergies of million) is split equally

between the two sets of shareholders. The need to make a higher bid or the appear-

ance of another bidder would tilt the balance of gain towards Dacre’s shareholders.

If the bid is made in the form of a share-for-share offer to the same value, the arithmetic

alters. In this case, Fewston is giving up part of the expanded firm and hence a further

share of the gains to Dacre’s shareholders. Assuming a bid to the same value, Fewston

must offer them shares. This would result in a total share issue of

125 million shares, i.e. Fewston is handing over 20 per cent of the expanded company to

Dacre’s shareholders. In this case, the gain enjoyed by Fewston’s shareholders will be

lower. The NPV of the takeover is still the gain less the cost; but the cost is greater, i.e. the

proportion of the expanded company handed over less the value of Dacre as it stands:

Hence, the NPV of the takeover from Fewston’s perspective is:

NPV 1gain in value cost2 1£20 m £12 m2 £8 m

1£52 m £40 m2 £12 m

Cost a

25 m

100 m 25 m

£260 mb £40 m

1£50 m>£22 25 m

£20

1£200 m £40 m £20 m2 £200 m £50 m £10 m

NPV V

A B

V

A

Outlay

£50

£20£4

£40£2

£200

V

A B

V

A

Outlay

NPV V

A B

1V

A

V

B

2 3Outlay V

B

4

Net cost 3Outlay V

B

4

3V

A B

1V

A

V

B

24

V

A B

7 V

A

V

B

20.5 EVALUATING A BID: THE EXPECTED GAINS FROM TAKEOVERS

CFAI_C20.QXD 10/28/05 5:25 PM Page 554