Pike Robert, Neal Bill. Corporate finance and investment: decisions and strategy

Подождите немного. Документ загружается.

.

Chapter 5 Investment appraisal methods 125

What does an expected NPV of £4,252 from the Lara proposal really mean? The project’s

future cash flows are sufficient for the firm to pay all costs associated with financing the proj-

ect and to provide an adequate return to shareholders. From the shareholders’ viewpoint, it

means that the firm could borrow £44,252 (the cost plus the NPV) to purchase the machine

and pay out a dividend today of £4,252, and still have sufficient funds from the project to pay

off the interest at 14 per cent p.a. and annual repayments (see Table 5.2).

In practice, it is unlikely that the lender will agree to a repayment schedule that exactly

matches the expected annual cash flows of the project. It is also somewhat imprudent to

pay as a dividend the whole of the expected NPV before the project commences! However,

in theory at least, the proposal creates wealth of £4,252 and the shareholders are that much

better off than they were prior to the decision. Note that we assume that borrowing and

lending rates of interest are the same. We discuss in later chapters how the discount rate is

estimated; suffice it to say that it is the required rate of return that investors can expect on

comparable alternative investment in the market-place.

5.4 INTERNAL RATE OF RETURN

Managers frequently ask: ‘What rate of return am I getting on my investment?’ To cal-

culate the correct return, or yield, requires us to find the rate that equates the present

value of future benefits to the initial cash outlay. We call this the internal rate of return

(IRR), or DCF yield.

The IRR is that discount rate, r, which, when applied to project cash flows pro-

duces a net present value of zero. It is found by solving the equation for r:

Where the IRR exceeds the required rate of return the project should be

accepted.

Suppose a savings scheme offers a plan whereby, for an initial investment of £100,

you would receive £112 at the year end. The IRR is thus 12 per cent:

If another scheme offered a single payment of £148 in three years’ time, from an ini-

tial investment of £100, the IRR is found by solving:

or

Turning to the present-value interest factor (PVIF) table (Appendix C) for three

years and looking for the rate that comes closest to 0.6757, we find that the IRR for the

investment is approximately 14 per cent. The same approach is used to find the IRR

for capital investment, but here the annual cash flows may differ. We find the IRR by

solving for the rate of return at which the present value of the cash inflows equals the

present value of the cash outflows. That is, we have to solve for

This is the same as finding the rate of return that produces an NPV of zero.

I

o

X

1

1 r

X

2

11 r2

2

p

X

n

11 r2

n

1

11 r2

3

£100

£148

0.6757

£10011 r2

3

£148

r 12%

£10011 r2 £112

1r 7 k2,

a

n

t 0

X

t

11 r2

t

0

1X

t

2,

DCF yield

The rate of return that equates

the present value of future cash

flows with the initial invest-

ment outlay

CFAI_C05.QXD 10/28/05 4:11 PM Page 125

.

126 Part II Investment decisions and strategies

In our earlier example, the Lara produced an NPV of £4,252 at 14 per cent. Given a

‘normal’ pattern of cash flows, i.e. an outlay followed by cash inflows, we can see that

as the discount rate increases, the NPV falls. Trial and error will give us the discount

rate that yields a zero NPV.

Trying 18 per cent, as shown in Table 5.3, gives a positive NPV of £976. Trying 20

per cent gives a negative NPV of £510. Clearly the IRR giving a zero NPV falls between

18 and 20 per cent, probably closer to 20 per cent. Using linear interpolation, we esti-

mate the IRR by applying the formula:

where is the rate of interest and the NPV for the first guess, and and the NPV

for the second guess. Applying the formula:

Note that the calculation includes the class interval, in this case

If we had chosen two discount rates further apart, such as 10 and 25 per cent, the

linear approximation would be less accurate:

Even over a range of 15 per cent the accuracy is to within 1 per cent of the true IRR.

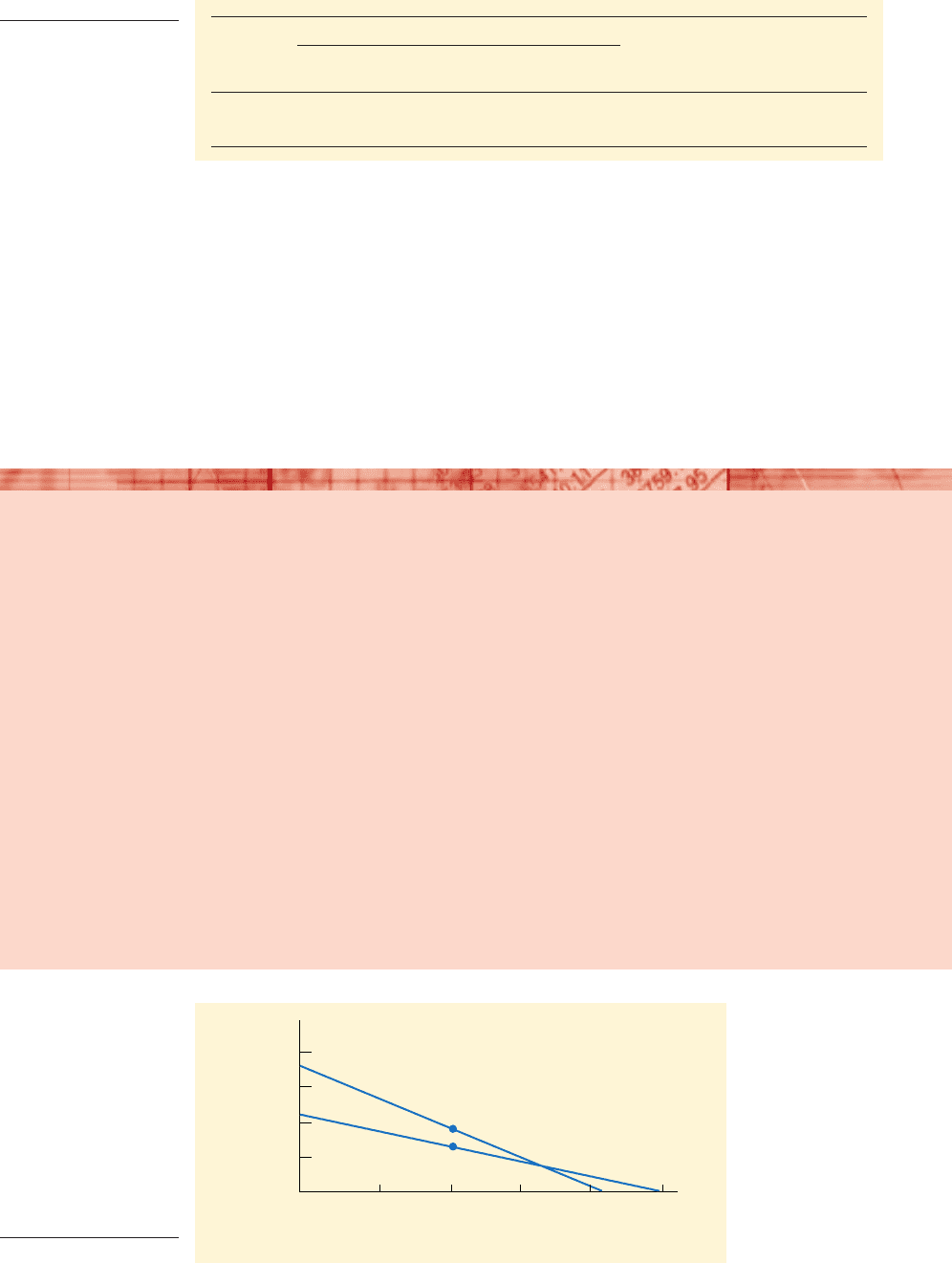

In the Lara example, the NPV at various rates of interest is shown in Figure 5.1. The

graph shows a clearer relationship between IRR and NPV. We also have an idea of the

break-even rate of interest – or IRR – at around 19–20 per cent, as calculated earlier.

The IRR of 19.31 per cent is well above the required rate of 14 per cent and the project

is, therefore, wealth-creating.

Most managers have access to computer spreadsheets that solve the equation in a

fraction of a second and avoid tedious manual effort. However, our analysis explains

the logic behind the computer calculation.

For the Carling proposal, the IRR calculation is much more straightforward as the

annual cash flows are constant.

PVIFA

1r, 4 yrs2

£50,000

£17,000

2.9411

£17,000 PVIFA

1r, 4 yrs2

£50,000

IRR 10% a

£7,972

£7,972 £3,860

15% b 20.1%

at 25%, NPV £3,860

at 10%, NPV £7,972

120% 18%2 2%.

IRR 18% a

£976

£976 £510

2% b 19.31%

N

2

,r

2

N

1

r

1

IRR r

1

a

N

1

N

1

N

2

1r

2

r

1

2b

Table 5.3

IRR calculations for

Lara proposal

Year Cash flow (£) PVIF at 18% PV (£) PVIF at 20% PV (£)

0 (40,000) 1.0 (40,000) 1.0 (40,000)

1 16,000 0.84746 13,559 0.83333 13,333

2 16,000 0.71818 11,490 0.69444 11,111

3 16,000 0.60863 9,738 0.57870 9,259

4 12,000 0.51579 6,189 0.48225 5,787

NPV 976 (510)

IRR 18% a

976

976 510

2%b 19.31%

CFAI_C05.QXD 10/28/05 4:11 PM Page 126

.

Chapter 5 Investment appraisal methods 127

8

7

6

5

4

3

2

1

0

–1

–2

–3

–4

–5

–6

51015 2025

Internal rate of return (%)

NPV (£000)

£7,972

£4,252 NPV at 14%

IRR 19.31%

£(3,860)

Figure 5.1

Lara proposal: NPV–IRR

graph

Referring to annuity tables (Appendix D), we find that for four years at 13 per cent,

the factor is 2.9745, and at 14 per cent it is 2.9137. The IRR is therefore between 13 and

14 per cent. This return falls just below the 14 per cent requirement, making it an

uneconomic proposal.

5.5 PROFITABILITY INDEX

Another method for evaluating capital projects is the profitability index (PI), some-

times called the benefit–cost ratio.

The profitability index

The profitability index is the ratio of the present value of project benefits to the present

value of initial costs. The decision rule is that projects with a PI greater than 1.0 are

acceptable.

Referring back to the present values calculated in Table 5.1, we can find for the Lara

proposal:

PI

PV benefits

PV outlay

£44,252

£40,000

1.1063

Prince makes 500% profit on Canary Wharf

Prince Al Waleed Bin Talal Bin Abdul Aziz, the

Saudi prince said to be the richest businessman

outside the US, yesterday revealed that he had

realised 500 per cent profit by selling most of his

stake in Canary Wharf.

The Prince was one of a group of investors who

funded Canary Wharf chairman Paul Reichmann to

buy back the 85-acre estate in London’s docklands

from its bankers in 1995 for £800 million.

When Canary Wharf emerged from adminis-

tration in 1993, it had attracted interest from

few potential tenants and most investors gave it

little chance of success.

On Tuesday the Prince completed the sale of

two-thirds of his stake, raising £122 million. The

Prince calculates that the internal rate of return,

over the five years of the investment, has been a

healthy 47.7 per cent per year. He will retain the

remaining third of his investment. ‘He likes it,’ a

spokesman said. Asked how the money will be

reinvested, a spokesman said, ‘Very wisely.’

Source: Based on Norma Cohen, Financial Times, 18 January 2001.

CFAI_C05.QXD 10/28/05 4:11 PM Page 127

.

128 Part II Investment decisions and strategies

5.6 PAYBACK PERIOD

Over the years, managers have come to rely upon a number of rule-of-thumb approach-

es to analyse investments. Two of the most popular methods are the payback period

and the accounting rate of return.

The payback period (PB) is the period of time taken for the future net cash inflows

to match the initial cash outlay.

Table 5.4 gives the cumulative cash flows for the two projects in our earlier exam-

ple. After two years, the cumulative cash flow for Lara has reduced to but by

the end of the third year it has improved to The project therefore breaks even,

or pays back, in two and a half years. Similarly, the Carling pays back in 2.9 years.

Many companies set payback requirements for capital projects. For example, if all

projects are required to pay back within three years, both the Lara and Carling are

acceptable.

A number of modifications to simple payback are possible. Discounted payback

addresses the problem of comparing cashflows in different time periods. It calculates

$8,000.

$8,000;

Self-assessment activity 5.2

What are the three main DCF methods and how do you know when to accept a capital

project with each?

(Answer in Appendix A at the back of the book)

Table 5.4

Payback period

calculation

Lara cash flow Carling cash flow

Year Annual Cumulative Annual Cumulative

0 Cost (40,000) (40,000) (50,000) (50,000)

1 Cost savings 16,000 (24,000) 17,000 (33,000)

2 Cost savings 16,000 (8,000) 17,000 (16,000)

3 Cost savings 16,000 8,000 17,000 1,000

4 Cost savings 12,000 20,000 17,000 18,000

Payback: Lara

Carling

2

16,000

17,000

years 2.9 years

2

8,000

16,000

years 2.5 years

while for the Carling proposal:

From this we see that the Lara is acceptable on financial grounds as the PI exceeds

1. The higher the PI, the more attractive the project. For independent projects, the PI

gives the same advice as NPV and IRR methods, although there are important reser-

vations when projects are ‘mutually exclusive’ (see Section 5.8).

The PI can also be expressed as the net present value per £1 invested, i.e.

If NPV per £1 invested exceeds zero, then the project should be accepted.

PI

NPV

PV of outlays

PI

£49,533

£50,000

0.9906

discounted payback

Period of time the present value

of a project’s annual net cash

flows take to match the initial

cost outlay

payback period

Period of time a project’s annu-

al net cash flows take to match

the initial cost outlay

CFAI_C05.QXD 10/28/05 4:11 PM Page 128

.

Chapter 5 Investment appraisal methods 129

how quickly discounted cash flows recoup the initial investment. Referring back to the

NPV calculation for the Lara, the discounted payback period at 14 per cent interest is

approximately three and a half years (see below). The cumulative present values

recoup the initial outlay only in the final year.

Year Present value @14% Cumulative PV

0 (40,000) (40,000)

1 14,035 (25,965)

2 12,312 (13,653)

3 10,800 (2,853)

Payback period 3.5 years

4 7,105 4,252

NPV 4,252

A fuller discussion of the popularity of the payback period will be given in Chapter 7.

However, we should note that this approach has some serious problems as a measure of

investment worth:

1 The time-value of money is ignored (except in the case of discounted payback).

2 Cash flows arising after the payback period are ignored.

3 The payback period criterion that firms stipulate for assessing projects has little the-

oretical basis. How do firms justify setting, say, a two-year payback requirement?

5.7 ACCOUNTING RATE OF RETURN

A key ratio in analysing accounts is the return on capital employed, or ROCE. This is

calculated as:

This indicates a company’s efficiency in generating profits from its asset base. All

new investment should at least match existing assets in terms of its earning power.

However, the annual ROCE on a project will change each year. Typically, it is less prof-

itable in the early years but improves over time as the project’s sales build up and as

the book value of the asset (i.e. cost less depreciation) declines.

The accounting rate of return (ARR) seeks to provide a measure of project prof-

itability over the entire asset life. It compares the average profit of the project with the

book value of the asset acquired. The ARR can be calculated on the original capital

invested or on the average amount invested over the life of the asset.

Accounting rate of return

Returning to our example, suppose the depreciation policy is to depreciate assets

over their useful lives on a straight-line basis. The annual depreciation for the Lara will

be £10,000 (i.e. £40,000 over four years) and for the Carling, £12,500. The annual prof-

it from the proposals will be the annual cash saving less the annual depreciation. The

ARRs based on initial capital invested for the two proposals are shown in Table 5.5.

Alternatively, we could base the calculation of ARR on the average investment,

found by summing the opening and closing asset values and dividing by 2. This

ARR 1average investment2

Average annual profit

Average capital invested

100

ARR 1total investment2

Average annual profit

Initial capital invested

100

Profit before interest and tax

Capital employed

100

accounting rate of return

Return on investment over the

whole life of a project

return on capital employed

Operating profit expressed as a

percentage of capital employed

CFAI_C05.QXD 10/28/05 4:11 PM Page 129

.

130 Part II Investment decisions and strategies

would yield answers for the Lara and Carling of 25 per cent and 18 per cent, respec-

tively, double the returns based on the initial capital. (In our case, the residual values

are zero.)

A benefit of this profitability measure is that managers feel they understand it. It

makes sense to use an investment evaluation measure that is broadly consistent with

return on capital employed, which is the primary business ratio. However, the ARR

has some definite drawbacks. Suppose the Lara proposal is expected to continue into

Year 5, yielding a profit of £1,000 in that year. Common sense suggests that this would

make the proposal more attractive. However, the new ARR actually declines from 25

to 21 per cent as a result of averaging over five rather than four years.

It also takes no account of the size and life of the investment, or the timing of cash

flows. Moreover, this approach is based on profits rather than cash flows, the significance

of which we discuss in the next chapter. Such important weaknesses make ARR inap-

propriate as a main investment appraisal method, particularly when comparing projects.

ARR

1£6,000 £6,000 £6,000 £2,000 £1,0002>5

1£40,000 02>2

100 21%

5.8 RANKING MUTUALLY EXCLUSIVE PROJECTS

Table 5.5

Calculation of the ARR

on total assets

Year

1234Average ARR

Project

Lara

Cash flow (£) 16,000 16,000 16,000 12,000 –

Depreciation* (£) (10,000) (10,000) (10,000) (10,000) –

Accounting 6,000 6,000 6,000 2,000 5,000

profit (£)

Carling

Cash flow (£) 17,000 17,000 17,000 17,000 –

Depreciation* (£) (12,500) (12,500) (12,500) (12,500) –

Accounting 4,500 4,500 4,500 4,500 4,500

profit (£)

*Straight-line depreciation is used in each case.

9%

4,500>50,000

12

1

2

%

5,000>40,000

Self-assessment activity 5.3

List four capital budgeting methods for evaluating project proposals. Identify the main

strengths and drawbacks of each.

(Answer in Appendix A at the back of the book)

Suppose the manufacturers of the Lara also make the Bruno – a larger, more powerful,

but more erratic model – offering a further 50 per cent in cost savings each year, but

costing a further 50 per cent to purchase. The NPV will be 50 per cent greater than the

Lara, but the other measures of performance – based on ratios or percentages – will be

the same, as shown in Table 5.6.

CFAI_C05.QXD 10/28/05 4:11 PM Page 130

.

Chapter 5 Investment appraisal methods 131

Table 5.6

Comparison of various

appraisal methods

Lara Bruno Carling

Net present value (£) 4,252 6,378 (467)

Internal rate of return (%) 19.3 19.3 13.5

Profitability index 1.1 1.1 0.99

Payback period (years) 2.5 2.5 2.9

Accounting rate of return (%) 25.0 25.0 18.0

In ranking mutually exclusive capital projects, we can reject the Carling for hav-

ing a negative NPV and performance indicators that are consistently inferior to the

alternatives. While the Bruno and Lara are, pound-for-pound, identical, the Bruno cre-

ates £2,126 additional wealth and is preferred.

Under the conditions typically found in business, no single method is ideal, which

is why three or four different measures are often calculated. The ready availability of

spreadsheet packages with graphics facilities makes this a straightforward and inex-

pensive procedure. Investment appraisal techniques are tools to assist managers in

assessing the worth of a given project.

■ NPV or IRR?

In many cases, the choice of DCF method has no effect on the investment advice, and

it is simply a matter of personal preference. In certain circumstances, however, the

choice does matter. We shall consider three such situations:

1 Mutually exclusive projects.

2 Variable discount rates.

3 Unconventional cash flows.

■ Mutually exclusive projects

The decision to accept or reject a project cannot always be separated from other invest-

ment projects. For example, a company may have a spare plot of land that could be

used to build a warehouse or a sports centre. In such cases, the problem is to evaluate

mutually exclusive alternatives.

The earlier worked examples comparing the Lara, Carling and Bruno proposals are

mutually exclusive. Recall that, while the Lara and Bruno offered the same IRR, the lat-

ter offered a much higher NPV because it was on a larger scale. The weakness of IRR

is that it ignores the scale of the project. It implies that firms would prefer to make a

60 per cent IRR on an investment of £1,000 than a 30 per cent return on a £1 million

project. Clearly, project scale should be taken into consideration, which is why we rec-

ommend the NPV method when assessing mutually exclusive projects of different size

or duration.

■ Variable discount rates

It is common to discount cash flows at a constant rate of return throughout a project’s life.

But this may not always be appropriate. The required rate of return is linked to underly-

ing interest rates and cash flow uncertainties, both of which can change over time.

This presents little difficulty in the case of NPV: different discount rates can be set

for each period. The IRR method, however, is compared against a single required rate

of return and cannot handle variable rates.

CFAI_C05.QXD 10/28/05 4:11 PM Page 131

.

132 Part II Investment decisions and strategies

■ Unconventional cash flows

There are three basic cash flow profiles:

Type Cash flow pattern Example

Conventional Outlay followed by inflows Capital project

Reverse Inflow followed by outflow Loan

Unconventional More than one change of sign Two-stage development project

For a reverse cash flow pattern, such as a loan where cash is received and interest

paid in subsequent periods, the IRR can be usefully applied. But in interpreting the

result, remember that the lower the rate of return the better, so the decision rule is to

accept the loan proposal if the IRR is below the required rate of return.

Unconventional cash flow patterns create particular difficulty for the IRR approach.

Consider the following project cash flows and NPV calculation at 10 per cent required

rate of return.

£ PVIF at 10% PV (£ 000)

Initial outlay 0 1.00

Year 1 0.909 327

2 0.826

3 0.751 130

NPV 0

With an NPV of zero, the IRR is, by definition, 10 per cent. But at certain other rates,

such as 20 per cent and 30 per cent, the NPV is still zero!

Multiple solutions may occur where there are multiple changes of sign. In our

example there are three changes in sign – from negative cash flow at the start to posi-

tive in Year 1, negative in Year 2 and positive in Year 3. While a conventional project

has only one IRR, unconventional projects may have as many IRRs as there are

changes in the cash flow sign.

173,000

357432,000

360,000

100100,000

12

12

12

To summarise, the use of NPV and IRR is a matter of personal preference in most

instances. But where the evaluation is for mutually exclusive projects, where the dis-

count rate is not constant throughout the project’s life, or where an unconventional

cash flow pattern is suspected, we recommend use of the net present value approach.

To underline the superiority of NPV we need to examine the respective reinvestment

assumptions of the two methods.

The NPV method assumes that all cash flows can be reinvested at the firm’s cost of

capital. This is entirely sensible, since the discount rate is an opportunity cost of capi-

tal that should reflect the alternative use of funds. The IRR method assumes that a pro-

ject’s annual cash flows can be reinvested at the project’s internal rate of return. Thus,

a project offering a 30 per cent IRR, given a 12 per cent cost of capital, assumes that

interim cash flows are compounded forward at the project’s rate of return (30 per cent)

rather than at the cost of capital (12 per cent). In effect, therefore, the IRR method

Self-assessment activity 5.4

Why do problems arise in evaluating mutually exclusive projects? What approach would

you recommend in such circumstances?

(Answer in Appendix A at the back of the book)

CFAI_C05.QXD 10/28/05 4:11 PM Page 132

.

Chapter 5 Investment appraisal methods 133

includes a bonus of the assumed benefits accruing from the reinvestment of interim

cash flows at rates of interest in excess of the cost of capital. This is a serious error for

projects with IRRs well above the cost of capital.

Consider the mutually exclusive investment proposals given in Table 5.7. X and Y

each cost £18,896. Project rankings reveal that X has the higher internal rate of return

but the lower net present value. Figure 5.2 shows how this apparent anomaly occurs.

(Strictly speaking, the graphs should be curvilinear.)

While Project Y has the higher NPV when discounted at 10 per cent, it has the lower

IRR, the two projects intersecting in the graph at around 17 per cent. Wherever there

is a sizeable difference between the project IRR and the discount rate, this problem

becomes a distinct possibility.

0 5 10 15 20 25

Rate of interest (%)

20,000

15,000

10,000

5,000

Project Y

Project X

8,290

6,463

NPV (£)

Intersection point (17%)

Figure 5.2

NPV and IRR compared

Table 5.7

Comparison of mutually

exclusive projects

Cash flows (£)

Undiscounted NPV

Proposal Year 0 Year 1 Year 2 Year 3 Year 4 cash flow IRR at 10%

X 8,000 8,000 8,000 8,000 13,104 25% 6,463

Y 0 4,000 8,000 26,164 19,268 22% 8,290

18,896

18,896

Harry Potter and the global sales hopes of Coca-Cola

When the long-awaited Harry Potter movie

opened one of the biggest stars was not even

seen on film. As millions enjoy Harry Potter and

the Philosopher’s Stone, Coca-Cola is assuming

the role of exclusive marketing partner.

Never has so much been poured into one

movie by one company. Since lengthy negotiations

with Warner Bros Pictures for exclusivity last year,

the beverage group has sunk $150 million into a

global marketing programmes usually preserved

for world sporting events such as the Olympics.

In many ways, Harry Potter is able to do what

Coca-Cola has been attempting for many years –

to reach out to a younger audience while not

alienating adults. That is crucial as Coca-Cola rein-

vents itself as an all-beverage company, offering

from fun juice drinks to gourmet coffees. But Harry

Potter also serves another purpose: instantly elevat-

ing the Coke brand by its sheer popularity world-

wide, something its own advertising campaigns

have failed to do. Such a powerful platform seems

to justify spending nearly 10 per cent of the

group’s global marketing budget on Harry Potter.

The biggest critics Coke has to worry about

are its shareholders. Its share price has been rela-

tively flat since the announcement of the Harry

Potter campaign. ‘Investors are simply looking for

Coke to meet volume goals. That would be

enough,’ says Ms Levy, a spokesperson for the

firm. ‘If this can help re-establish the brand in the

hearts of consumers, then putting 10 per cent of

the budget into Harry Potter won’t be a bad

investment.’

Source: Based on Financial Times, November 15 2001.

CFAI_C05.QXD 10/28/05 4:11 PM Page 133

.

134 Part II Investment decisions and strategies

5.9 INVESTMENT EVALUATION AND CAPITAL RATIONING

We have seen that, under the somewhat limiting assumptions specified, the wealth of a

firm’s shareholders is maximised if the firm accepts all investment proposals that have

positive net present values. Alternatively, the NPV decision rule may be restated as:

accept investments that offer rates of return in excess of their opportunity costs of capi-

tal. The opportunity cost of capital is the return shareholders could obtain for the same

level of risk by investing their capital elsewhere. Implicit in the NPV decision rule is the

notion that capital is always available at some cost to finance investment opportunities.

In this section, we relax another assumption of perfect capital markets to include the

situation where firms are restricted from undertaking all the investments offering posi-

tive net present values. Although individual projects cannot be accepted/rejected on the

basis of the NPV rule, the essential problem remains: namely, to determine the package

of investment projects that offers the highest total net present value to the shareholders.

■ The nature of constraints on investment

In imperfect markets, the capital budgeting problem may involve the allocation of

scarce resources among competing, economically desirable projects, not all of which

can be undertaken. This capital rationing applies equally to non-capital, as well as cap-

ital, constraints. For example, the resource constraint may be the availability of skilled

labour, management time or working capital requirements. Investment constraints may

even arise from the insistence that top management appraise and approve all capital

projects, thus creating a backlog of investment proposals.

■ Hard and soft rationing

Capital rationing may arise either because a firm cannot obtain funds at market rates of

return, or because of internally imposed financial constraints by management.

Externally imposed constraints are referred to as hard rationing and internally imposed

constraints as soft rationing.

The Wilson Committee (1980) found no evidence of any general shortage of finance

for industry at prevailing rates of interest and levels of demand. A survey of managers

(Pike 1983) found that:

1 The problem of low investment essentially derives not from a shortage of finance

but from an inadequate demand for funds.

2 Capital constraints, where they exist, tend to be internally imposed rather than

externally imposed by the capital market.

3 Capital constraints are more acutely experienced by smaller, less profitable and

higher-risk firms.

■ Soft rationing

Why should the internal management of a company wish to impose a capital expendi-

ture constraint that may actually result in the sacrifice of wealth-creating projects? Soft

Self-assessment activity 5.5

Take another look at the graphs in Figure 5.2. How would you explain to a manager that

Project X, with the higher IRR, is actually less attractive than Project Y?

(Answer in Appendix A at the back of the book)

capital rationing

The process of allocating capital

to projects where there is insuf-

ficient capital to fund all value-

creating proposals

CFAI_C05.QXD 10/28/05 4:11 PM Page 134