Pike Robert, Neal Bill. Corporate finance and investment: decisions and strategy

Подождите немного. Документ загружается.

.

Chapter 4 Valuation of assets, shares and companies 115

£m £m

Assets employed

Freehold property 4.0

Plant and equipment 2.0

Current assets:

stocks 1.5

debtors 3.0

cash 0.1

4.6

Total assets 10.6

Creditors payable within one year (3.0

)

Total assets less current liabilities 7.6

Creditors payable after one year (1.0

)

Net assets 6.6

Financed by

Ordinary share capital (25p par value) 2.5

Revaluation reserve 0.5

Profit and loss account 3.6

Shareholders’ funds 6.6

Sales revenue £500,000

Operating costs (£300,000

)

(after depreciation of £50,000)

Operating profit £200,000

Taxation @ 30% (£60,000

)

Profit after tax £140,000

Further information:

(a) Carbo’s pre-tax earnings for the year ended 31 December 2005 were £2.0 million.

(b) Corporation Tax is payable at 33 per cent.

(c) Depreciation provisions were £0.5 million. This was exactly equal to the funding required to replace

worn-out equipment.

(d) Carbo has recently tried to grow sales by extending more generous trade credit terms. As a result, about

a third of its debtors have only a 50 per cent likelihood of paying.

(e) About half of Carbo’s stocks are probably obsolete with a resale value as scrap of only £50,000.

(f) Carbo’s assets were last revalued in 1994.

(g) If the bid succeeds, Rundum will pay off the presently highly overpaid Managing Director of Carbo for

£200,000 and replace him with one of its own ‘high-flyers’. This will generate pre-tax annual savings of

£60,000 p.a.

(h) Carbo’s two divisions are roughly equal in size. The industry P:E ratio is 8:1 for packaging and 12:1 for

building materials.

Required

(a) Value Carbo using a net asset valuation approach.

(b) Value Carbo using a price:earnings ratio approach.

3 Lazenby plc has been set up to exploit an opportunity to import a new product from overseas. It has issued

two million ordinary shares of par value 25p, sold at a 25 per cent premium. Its projected accounts show the

following annual operating figures:

Notes:

(i) Shareholders require a return of 10 per cent p.a.

(ii) Replacement investment is financed out of depreciation provisions and is fully tax-allowable.

(iii) 2% of sales should be written off as bad debts.

(iv) Bad debt write-offs are 50 per cent tax-allowable.

Continued

Carbo’s Balance Sheet for the year ending 31 December 2005 shows the following:

CFAI_C04.QXD 10/28/05 2:29 PM Page 115

.

116 Part I A framework for financial decisions

Required

Value each share in Lazenby:

(a) assuming perpetual life.

(b) over a ten-year horizon.

4 Brosnan plc generates free cash flows of £5 million p.a. after allowing for tax and depreciation, which is used

for reinvestment. It has issued 10 million shares. Shareholders require a 12 per cent return.

Required

Value each share:

(i) assuming all free cash flows are distributed as dividend.

(ii) assuming 50 per cent of FCFs are retained, with a return on retained earnings of 15 per cent.

(iii) as for (ii), but assuming 10 per cent return on reinvestment.

(iv) assuming that FCFs grow at 7.5 per cent for each of the first three future years, then at 5 per cent thereafter.

Note: assume all cash flows are perpetuities.

5 Insert the missing values in the following table:

gbR

(i) £8.44 £0.35 ? 8.5% 0.5 17% 13.0 %

(ii) £4.98 £0.20 £0.219 ? 0.6 16% 14.0 %

(iii) ? £0.10 £0.108 8.0 % 0.4 20% 15.0 %

(iv) £2.75 ? £0.220 10.0 % 0.5 20% 18.0 %

(v) £10.20 £0.60 £0.610 2.0 % ? 10% 8.0 %

(vi) £0.60 £0.05 £0.054 8.0 % 0.8 20% ?

(vii) £1.47 £0.12 £0.133 10.5% 0.7 ? 19.5%

Note: answers may have some minor rounding errors.

k

e

D

1

D

o

P

o

6 Leyburn plc currently generates profits before tax of £10 million, and proposes to pay a dividend of £4 mil-

lion out of cash holdings to its shareholders. The rate of Corporation Tax is 30 per cent. Recent dividend

growth has averaged 8 per cent p.a. It is considering retaining an extra £1 million in order to finance new

strategic investment. This switch in dividend policy will be permanent, as management believe that there will

be a stream of highly attractive investments available over the next few years, all offering returns of around

20 per cent after tax. Leyburn’s shares are currently valued ‘cum-dividend’. Shareholders require a return of

14 per cent. Leyburn is wholly equity-financed.

Required

(a) Value the equity of Leyburn assuming no change in retention policy.

(b) What is the impact on the value of equity of adopting the higher level of retentions? (Assume the new

payout ratio will persist into the future.)

7 The most recent Balance Sheet for Vadeema plc is given below. Vadeema is a stock market-quoted company

that specialises in researching and developing new pharmaceutical compounds. It either sells or licenses its

discoveries to larger companies, although it operates a small manufacturing capability of its own, accounting

for about half of its turnover:

Balance Sheet as at 30 June 2005

Assets employed £m £m £m

Fixed assets

Tangible 50

Intangible 120

170

Current assets

Stock and work in progress 80

Debtors 20

Bank 5

105

Current liabilities

Trade creditors (10)

Bank overdraft (20

)(30)

CFAI_C04.QXD 10/28/05 2:29 PM Page 116

.

Chapter 4 Valuation of assets, shares and companies 117

Net current assets 75

10% loan stock (40

)

Net assets 205

Financed by

Ordinary shares capital (25p par value) 100

Share premium account 50

Revenue reserves 55

Shareholders’ funds 205

Obtain the latest annual report and accounts of a company of your choice.* Consult the Balance Sheet and deter-

mine the company’s net asset value.

■ What is the composition of the assets, i.e. the relative size of fixed and current assets?

■ What is the relative size of tangible fixed and intangible fixed assets?

■ What proportion of current assets is accounted for by stocks and debtors?

■ What is the company’s policy towards asset revaluation?

■ What is its depreciation policy?

Now consult the financial press to assess the market value of the equity. This is the current share price times the

number of ordinary shares issued. (The notes to the accounts will indicate the latter.)

■ What discrepancy do you find between the NAV and the market value?

■ How can you explain this?

■ What is the P:E ratio of your selected company?

■ How does this compare with other companies in the same sector?

■ How can you explain any discrepancies?

■ Do you think your selected company’s shares are under- or over-valued?

* Most large companies post their Annual Reports and Accounts on their websites. The commonest address forms of UK companies

are: companyname.co.uk or companyname.com.

Practical assignment

Further information:

1 2004–05, Vadeema made sales of £300 million, with a 25 per cent net operating margin (i.e. after deprecia-

tion but before tax and interest).

2 The rate of corporate tax is 33 per cent.

3 Vadeema’s sales are quite volatile, having ranged between £150 million and £350 million over the previ-

ous five years.

4 The tangible fixed assets have recently been revalued (by the directors) at £65 million.

5 The intangible assets include a major patent (responsible for 20 per cent of its sales) which is due to expire

in April 2006. Its book value is £20 million.

6 50 per cent of stocks and work-in-progress represents development work for which no firm contract has

been signed (potential customers have paid for options to purchase the technology developed).

7 The average P:E ratio for quoted drug research companies at present is 22:1 and for pharmaceutical man-

ufacturers is 14:1. However, Vadeema’s own P:E ratio is 20:1.

8 Vadeema depreciates tangible fixed assets at the rate of £5 million p.a. and intangibles at the rate of £25 mil-

lion p.a.

9 The interest charge on the overdraft was 12 per cent.

10 Annual fixed investment is £5 million, none of which qualifies for capital allowances:

Required

(a) Determine the value of Vadeema using each of the following methods:

(i) net asset value

(ii) price:earnings ratio

(iii) discounted cash flow (using a discount rate of 20 per cent)

(b) How can you reconcile any discrepancies in your valuations?

(c) To what extent is it possible for the Stock Market to arrive at a ‘correct’ valuation of a company like Vadeema?

CFAI_C04.QXD 10/28/05 2:29 PM Page 117

.

CFAI_C04.QXD 10/28/05 2:29 PM Page 118

.

Chapters 5 to 7 examine in depth the investment decision and how it is evaluated. The concepts of

time-value of money and present value are extensively applied. The available methods for assisting

the financial manager to evaluate investment proposals are examined in Chapter 5, both when

capital is freely available and when it is in short supply. Methods of appraisal that do not utilise

discounting procedures are also examined.

In Chapter 6, investment appraisal procedures are applied to practical situations, incorporating the

impact of both taxation and inflation. Consideration is given to identifying the relevant information

for project evaluation, particularly for replacement decisions.

Chapter 7 sets the whole project appraisal system in a strategic perspective and explores the wider

aspects of the investment appraisal system within companies. It dispels the notion that investment

analysis hinges solely on methods of appraisal, and it reveals how companies approach their project

evaluations in practice.

Chapter 5 Investment appraisal methods 121

Chapter 6 Project appraisal–applications 147

Chapter 7 Investment strategy and process 173

INVESTMENT DECISIONS

AND STRATEGIES

Part

II

CFAI_C05.QXD 10/28/05 4:11 PM Page 119

.

CFAI_C05.QXD 10/28/05 4:11 PM Page 120

.

Investment appraisal methods

5

Learning objectives

Having read this chapter, you should have a good grasp of the investment appraisal techniques com-

monly employed in business, and have developed skills in applying them. Particular attention will be

devoted to the following:

■ The three discounted cash flow approaches – net present value, internal rate of return and prof-

itability index.

■ The underlying strengths and limitations of the above methods.

■ How net present value and internal rate of return methods can be reconciled when they conflict.

■ Non-discounting methods.

■ Analysing investments when capital availability is an important constraint.

Cigarettes can damage your wealth

Cigarette companies have for years looked for the Holy

Grail of a smokeless cigarette. R. J. Reynolds Tobacco,

US maker of Camel and other cigarette brands,

launched a smokeless cigarette called Premier. It spent

£210 million developing and marketing the new prod-

uct, which had vast wealth-creating potential and was

socially more acceptable to passive smokers.

After test marketing it for several months, the com-

pany finally recognised that it had created one of the

biggest new product flops on record. With 400 brands

of cigarette in the USA, launching a new product is

costly and risky. But the idea of a smokeless cigarette

was still seen by the company as worth pursuing and

it began trials on a new smokeless cigarette brand,

Eclipse that heats, rather than burns, tobacco. Since

the earlier flop, however, the market has changed,

with passive smoking becoming a bigger issue. Time

will tell whether the Eclipse cigarette brand is

launched successfully and generates a positive net

present value.

CFAI_C05.QXD 10/28/05 4:11 PM Page 121

.

122 Part II Investment decisions and strategies

Self-assessment activity 5.1

Investment projects do not only include investment in plant and equipment or buildings.

Think of some other types of capital projects.

(Answer in Appendix A at the back of the book)

5.1 INTRODUCTION

We saw in Chapters 3 and 4 how investing in capital projects that offer positive net

present values creates additional wealth for the business and its owners. A major com-

pany explains how it employs the NPV approach in assessing capital projects:

We measure all potential projects by their cash flow merit. We then discount projected

cash flows back to present value in order to compare the initial investment cost with a

project’s future returns to determine if it will add incremental value after compensating

for a given level of risk.

There are, however, a number of alternative techniques to the NPV method. The

aim of this chapter is to present the main methods of investment appraisal and to con-

sider their strengths and limitations. In a later chapter, we consider their practical

application in business, large and small.

5.2 CASH FLOW ANALYSIS

The investment decision is the decision to commit the firm’s financial and other

resources to a particular course of action. Confusingly, the same term is often applied

to both real investment, such as buildings and equipment, and financial investment,

such as investment in shares and other securities. While the principles underlying

investment analysis are basically the same for both types of investment, it is helpful for

us to concentrate here on the former category, usually referred to as capital investment.

Our particular emphasis on strategic capital projects concentrates on the allocation of a

firm’s long-term capital resources.

■ Cash flow matters more than profit

Managers in business usually view profit as the best measure of performance. It might,

therefore, be assumed that capital project appraisal should seek to assess whether the

investment is expected to be ‘profitable’. Indeed, many firms do use such an approach.

There are, however, many problems with the profit measure for assessing future

investment performance. Profit is based on accounting concepts of income and

expenses relating to a particular accounting period, based on the matching principle.

This means that income receivable and expenses payable, but not yet received or paid,

along with depreciation charges, form part of the profit calculation.

Consider the case of the Oval Furniture Company with expected annual sales from

its new factory of £400,000 and profits of £60,000. In order to stimulate demand, cus-

tomers are offered two years’ credit. While this decision has no impact on the report-

ed profit, it certainly affects the cash position – no cash flow being received for two

years. Cash flow analysis considers all the cash inflows and outflows resulting from

the investment decision. Non-cash flows, such as depreciation charges and other

accounting policy adjustments, are not relevant to the decision. We seek to estimate the

stream of cash flows arising from a particular course of action and the period in which

they occur.

CFAI_C05.QXD 10/28/05 4:11 PM Page 122

.

Chapter 5 Investment appraisal methods 123

■

Timing of cash flows

Project cash flows will usually arrive throughout the year. For example, if we acquire

a machine with a four-year life on 1 January 2007, the subsequent cash flows related

to it may involve the monthly payment purchases and expenses and daily receipt of

cash from customers throughout each year. Strictly speaking, these cash flows

should be identified on a monthly, even daily, basis and discounted using appropri-

ate discount factors.

In practice, to facilitate the use of annual discount tables, cash flows arising during

the year are treated as occurring at the year end. Thus, while the initial outlay is assumed

to occur at the start of the project (frequently termed Year 0), subsequent cash flows are

deemed to arrive later than they actually arise. This has the effect of producing an NPV

slightly lower than the true NPV, assuming that subsequent cash flows are positive.

Decision-making can be viewed as an incremental activity. Businesses generally

operate as going concerns with fairly clear strategies and well-established manage-

ment processes. Decisions are part of a sequence of actions seeking to move the organ-

isation from its current to its intended position. The same idea is apparent in analysing

projects – the decision-maker must assess how the business changes as a direct result

of selecting the project. Every project can be either accepted or rejected, and it is the

difference between these two alternatives in any time period, t, expressed in cash flow

terms (CF

t

), that is taken into the appraisal.

Incremental analysis

Project CF

t

CF

t

for firm with project CF

t

for firm without project.

5.3 INVESTMENT TECHNIQUES – NET PRESENT VALUE

Discounted cash flow (DCF) analysis is a family of techniques, of which the NPV method

is just one variant. Two other DCF methods are the internal rate of return (IRR) and the

profitability index (PI) approaches. Many managers prefer to use non-discounting

approaches such as the payback and return on capital methods; others use both approach-

es. The following example illustrates the various approaches to investment appraisal.

Example: appraising the Lara and Carling projects

Sportsman plc is a manufacturer of sports equipment. The firm is considering whether to

invest in one of two automated processes, the Lara or the Carling, both of which give rise

to staffing and other cost savings over the existing process. The relevant data relating to

each are given below:

Lara (£) Carling(£)

Investment outlay (payable immediately) (40,000) (50,000)

Year 1 Annual cost savings 16,000 17,000

2 Annual cost savings 16,000 17,000

3 Annual cost savings 16,000 17,000

4 Annual cost savings 12,000 17,000

The required return is 14 per cent p.a.

The investment outlays are obviously additional cash outflows, while the annual cost sav-

ings are cash flow benefits because total annual expenditures are reduced as a result of the

investment.

Should the company invest in either of the two proposals and if so, which is preferable?

CFAI_C05.QXD 10/28/05 4:11 PM Page 123

.

124 Part II Investment decisions and strategies

The NPV solution

The net present value for the Lara machine is found by multiplying the annual cash flows by

the present-value interest factor (PVIF) at 14 per cent (using the tables) and finding the total,

as shown in Table 5.1. An immediate cash outlay (treated as Year 0) is not discounted as it is

already expressed in present value terms. The same factors could be applied to evaluate the

Carling proposal. However, as the annual savings are constant, it is far simpler to use the

present value interest factor for an annuity (PVIFA) at 14 per cent for four years.

Comparison of the two proposals reveals the following:

1 The Lara machine offers a positive NPV of £4,252, and would increase shareholder wealth.

2 The Carling machine offers a negative NPV of £467 and would reduce value.

3 Given that the proposals are mutually exclusive (i.e. only one is required), the Lara pro-

posal should be accepted.

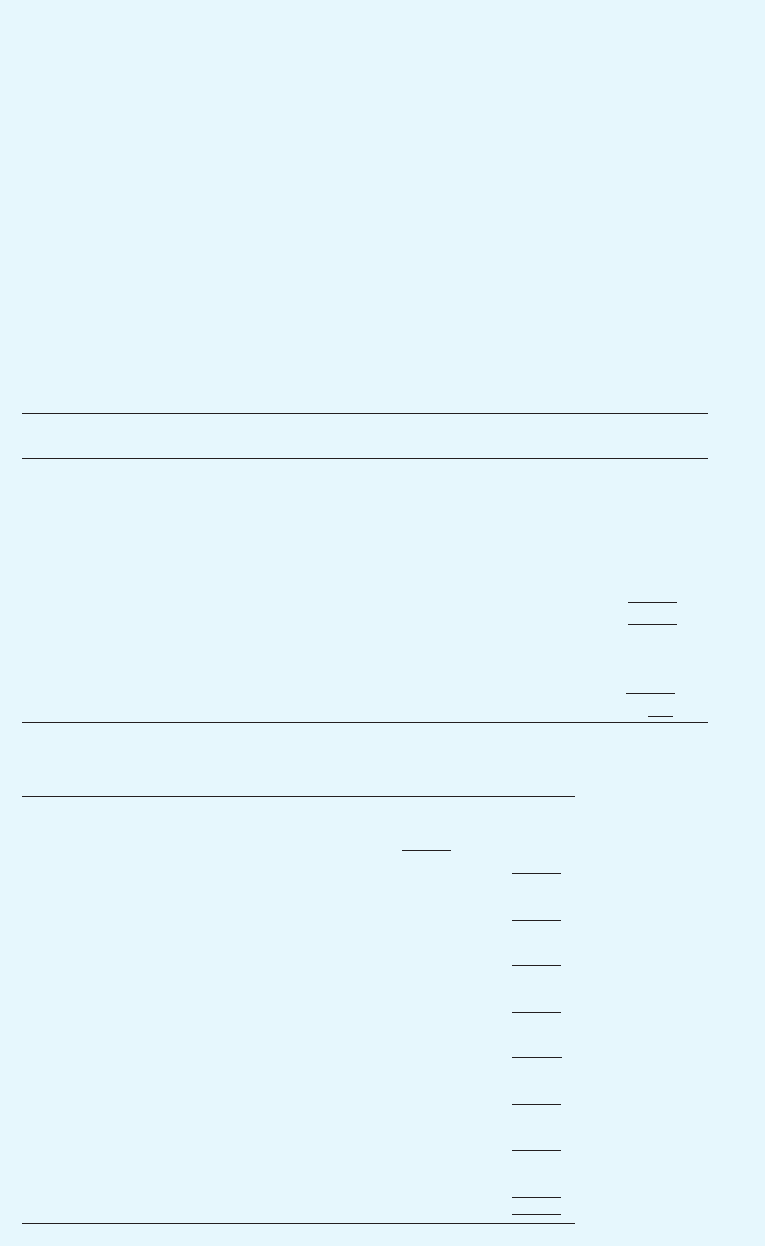

Table 5.1 Net present value calculations

Cash flow PVIF at Present

Year (£) factor 14% value (£)

Lara proposal

0 Outlay (40,000) 1 (40,000)

1 Cost savings 16,000 0.87719 14,035

2 Cost savings 16,000 0.76947 12,312

3 Cost savings 16,000 0.67497 10,800

4 Cost savings 12,000 0.59208 7,105

Net present value at 14% 4,252

Carling proposal

Cost savings 49,533

Outlay (50,000)

Net present value at 14% (467)

£17,000 PVIFA

114%, 4 yrs2

2.9137

Table 5.2 Why NPV makes sense to shareholders

Year 0 Borrow: machine £40,000 £

Pay NPV as dividend £4,252 44,252

1 Interest: £44,252 at 14% 6,195

50,447

Less: repayment (16,000)

(through annual savings) 34,447

2 Interest: £34,447 at 14% 4,822

39,269

Less: repayment (16,000)

23,269

3 Interest: £23,269 at 14% 3,257

26,526

Less: repayment (16,000)

10,526

4 Interest: £10,526 at 14% 1,474

12,000

Less: repayment (12,000)

—

CFAI_C05.QXD 10/28/05 4:11 PM Page 124