Pike Robert, Neal Bill. Corporate finance and investment: decisions and strategy

Подождите немного. Документ загружается.

.

Chapter 6 Project appraisal – applications 155

6.5 TAXATION IS A CASH FLOW

In Chapter 2, we introduced the subject of taxation and its broad implications for finan-

cial management. In this section, we examine in greater depth the taxation considera-

tions for capital investment projects.

Recall that in the UK, Corporation Tax is assessed by the Inland Revenue on the prof-

its of the company after certain adjustments. While it is not calculated on a project basis

by the Inland Revenue, the actual tax bill will increase with every new project offering

additional profits and reduce with every project offering losses. Corporation Tax is

charged on the profits, gains and income of an accounting period, usually the period

for which accounts are made up annually. In arriving at taxable profits, a deduction is

made for capital allowances on certain types of capital investment. Following the prin-

ciple outlined earlier of identifying the incremental cash flow, we need to ask: by how

much will the Corporation Tax bill for the company change each year as a result of the

decision? To answer this, we must consider the tax charged on project operating prof-

its and the tax relief obtained on the capital investment outlay.

■ Taxation implications of Tiger 2000 for Woosnam plc

Woosnam plc invests in a new piece of equipment, the Tiger 2000, costing £40,000 on

1 January 2000. It intends to operate the equipment for four years when the scrap value

will be zero. Expected net cash flows from the project are £10,000 in the first year and

£20,000 for each of the next three years. The discount rate is 15 per cent and the rate of

Corporation Tax is 30 per cent.

No tax position

If we ignore taxation (perhaps Woosnam is making losses and is unlikely to pay tax for

some time), the net present value of the project’s pre-tax cash flows is £8,390, as shown in

Table 6.5. The positive NPV suggests that, on economic grounds, it should be accepted.

With Corporation Tax but no capital allowances

Most companies have to pay Corporation Tax, and a large company, like Woosnam plc,

will pay at the rate of 30 per cent of taxable profits. A recent change is that this tax is

now paid in the same year as the related profits, usually by quarterly instalments.

Hitherto, companies enjoyed a tax delay of at least a year, which meant that the tax pay-

ment would typically lag a full year behind the investment cash flows to which they

relate. Most investments attract a capital allowance (equivalent to a depreciation

charge) which reduces the tax bill. At this stage, we assume that the Tiger 2000 does not

attract any capital allowances.

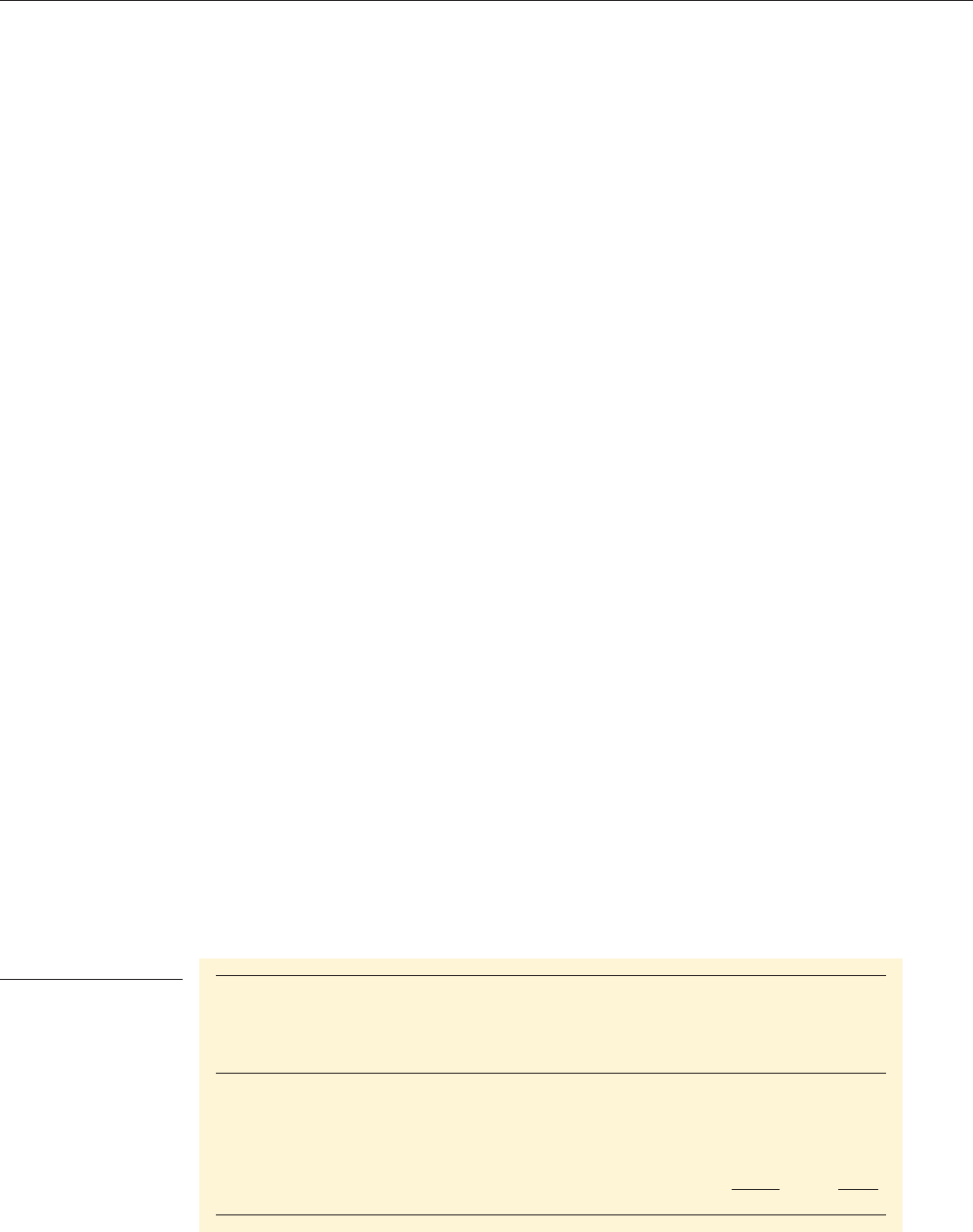

Table 6.5

Project Tiger 2000

(assuming no capital

allowances)

(1) (2) (3) (4) (1 4) (3 4)

Pre-tax Tax @ After-tax Discount PV PV

cash flows 30% cash flows factor pre-tax post-tax

Year £ £ @ 15% £ £

0 (40,000) – (40,000) 1.0 (40,000) (40,000)

1 10,000 (3,000) 7,000 0.869 8,690 6,083

2 20,000 (6,000) 14,000 0.756 15,120 10,584

3 20,000 (6,000) 14,000 0.657 13,140 9,198

4 20,000 (6,000) 14,000 0.572 1

1,440 8,008

NPV 8,390 (6,127)

CFAI_C06.QXD 10/26/05 11:27 AM Page 155

.

156 Part II Investment decisions and strategies

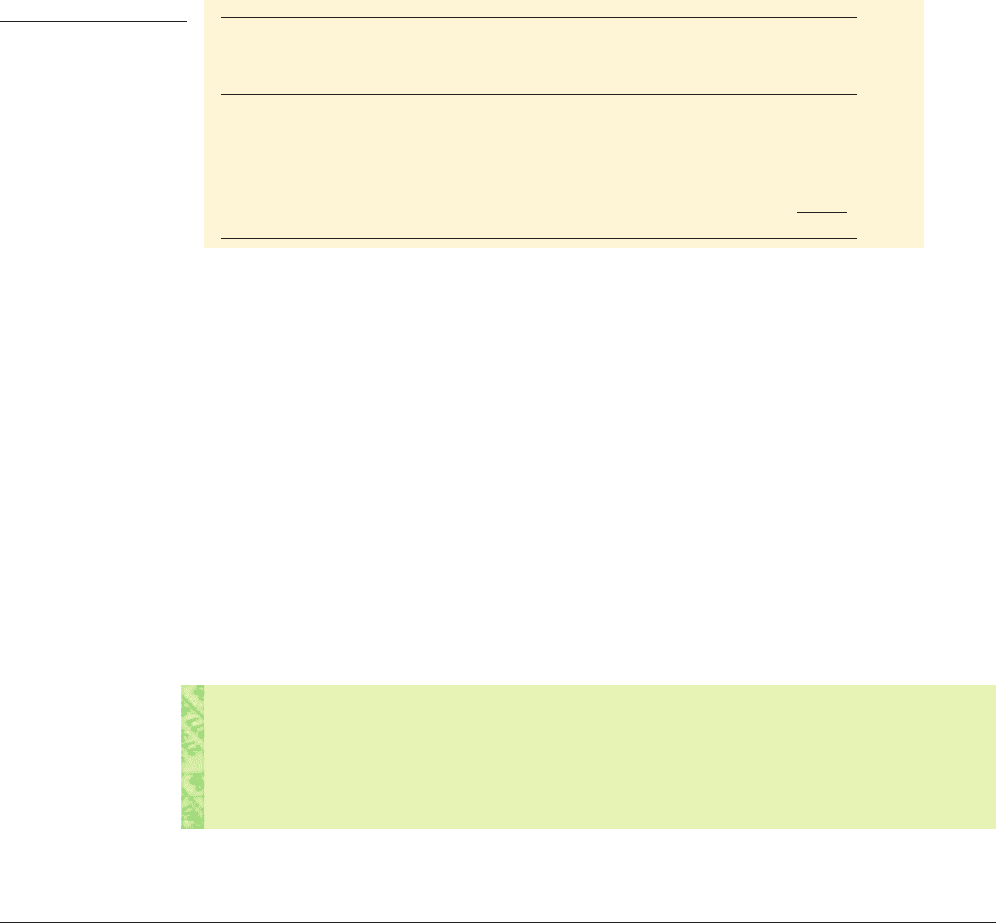

Table 6.6

Woosnam plc – Tiger

2000 tax reliefs

Tax written-down Writing-down 30%

End of value allowance tax relief

accounting year £ £ £

1– Initial outlay 40,000

WDA at 25% 10,000 10,000 3,000

30,000

2– WDA at 25% 7,500 7,500 2,250

22,500

3– WDA at 25% 5,625 5,625 1,688

16,875

4– Sale proceeds –

Balancing allowance 16,875 16,875 5,062

40,000 12,000

Table 6.5 shows that after deducting tax to be paid, the NPV for the project falls

sharply to –£6,127. It is no longer economically viable.

With corporation tax and capital allowances

For many types of capital investment, tax relief is granted on capital expenditure

incurred. In the United Kingdom, this is in the form of a first-year allowance and subse-

quent annual writing-down allowances (WDAs). The first-year allowance is a govern-

ment incentive to encourage firms to invest and has in the past been as high as 100 per

cent. Currently, for large companies, it is as follows:

Plant and machinery 25 per cent on the reducing balance

Industrial buildings 4 per cent on the initial cost

So for expenditure on machinery of £1,000, the allowance would be as follows:

Written-down value

Year Tax allowance (£) at year-end (£)

1 750

2 562

3 etc. 422, etc.

Clearly, the tax allowances diminish over time. Companies are allowed to write

assets down for tax purposes to their disposal value. Any discrepancy between written-

down value (WDV) and disposal value may trigger a tax liability (balancing charge)

or qualify for tax relief (balancing allowance). In the above example, disposal of the

asset for £500 after three years would mean that the capital allowances have been over-

generous to the extent of £78 (i.e. disposal value of £500 – WDV of £422). This balanc-

ing charge of £78 would then be subject to Corporation Tax. Disposal for, say, £300

would qualify the company for a balancing allowance of £122 (i.e. £422 – £300), a loss

that would be set against the taxable profits.

Let us return to the Woosnam plc example, this time assuming that the Tiger 2000

attracts a 25 per cent writing-down allowance. Table 6.6 calculates the WDAs. Tax is

payable in the same year as the investment cash flows to which they relate.

The difference between what the investment finally sold for (in this case zero) and

the balance at the start of the year is a balancing allowance, which is treated in the

25% 562

ˇˇˇ 141,

25% 750

ˇˇˇ 188

25% 1,000 250

annual writing-down

allowances (WDAs)

Allowances for depreciation on

capital expenditure allowed for

tax purposes

CFAI_C06.QXD 10/26/05 11:27 AM Page 156

.

Chapter 6 Project appraisal – applications 157

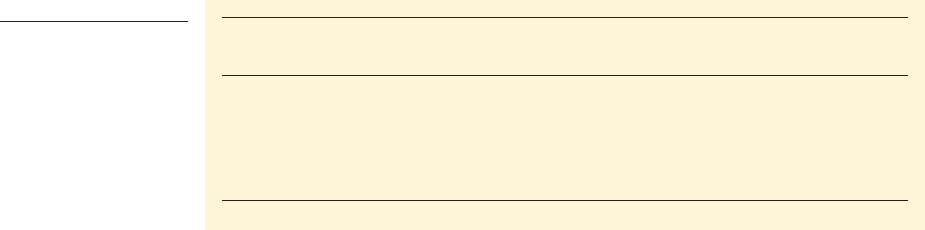

Table 6.7

Woosnam plc – Tiger

2000 with tax relief

Pre-tax Tax relief Net cash

cash flows Tax at on WDA flows Discount PV

Year £ 30% £ £ factor 15% £

0 (40,000) – (40,000) 1.000 (40,000)

1 10,000 (3,000) 3,000 10,000 0.869 8,690

2 20,000 (6,000) 2,250 16,250 0.756 12,285

3 20,000 (6,000) 1,688 15,688 0.657 10,307

4 20,000 (6,000) 5,062 19,062 0.572 10,903

2,185

same way as the writing-down allowance. (We will not introduce further complica-

tions such as the election to pool plant and machinery in this book.) A useful check is

to see that the total WDA (column 3) equals the initial investment, and the tax benefit

(column 4) on this total corresponds, in this case £40,000 at 30% =£12,000.

These cash flows can then be added to the earlier example, as in Table 6.7, showing

that the investment offers a positive NPV of £2,185 after tax.

How would the after-tax NPV differ were Woosnam plc a small or medium-size

company? Such firms currently have a further tax incentive to invest by attracting a

40 per cent initial allowance, rather than 25 per cent. The effect is to reduce the tax bill

in the early years, deferring it to later years. Because later cash flows are less valuable,

this means that the NPV will increase.

Taxation therefore affects cash flows from investments. It is payable on taxable prof-

its arising from the investment decision after deduction of capital allowances.

Self-assessment activity 6.5

Your boss says: ‘We only assess capital projects before tax. Every firm has to pay tax, so we

can ignore it’. Do you agree?

(Answer in Appendix A at the back of the book)

6.6 USE OF DCF TECHNIQUES

It is a common misconception that the discounted cash flow approach is a relatively

recent phenomenon. Historical records reveal an understanding of compound interest

(upon which discounted cash flow techniques are based) as far back as the Old

Babylonian period (c. 1800–1600

BC) in Mesopotamia. The earliest manuscripts setting

out compound interest tables date back to the 14th century, while the first recorded ref-

erence to the net present value rule is found in a book by Stevin published in 1582.

In these early days, the application of discounted cash flow methods was restricted

to financial investments such as loans and life assurance, where either the cash flows

were known or their probabilities could be determined based on actuarial evidence.

Only in the 19th century, with the Industrial Revolution well established, did the scale

of capital investments lead some engineering economists to begin to apply discounted

cash flow concepts to capital assets. However, in practice, these concepts were largely

ignored until the early 1950s in the USA and the early 1960s in the UK.

Surveys between 1975 and 1997 provide a clearer picture of the changing trends in

the practices of larger firms in the UK. Table 6.8 shows that, while all firms surveyed

CFAI_C06.QXD 10/26/05 11:27 AM Page 157

.

158 Part II Investment decisions and strategies

Table 6.8

Capital investment

evaluation methods in

100 large UK firms

1975 1981 1986 1992 1997

Firms using: (%) (%) (%) (%) (%)

Payback 73 81 92 94 66

Average accounting rate of return 51 49 56 50 55

DCF methods (IRR or NPV) 58 68 84 88 100

Internal rate of return 44 57 75 81 84

Net present value 32 39 68 74 97

Sources: Pike (1988, 1996), Arnold and Hatzopoulos (2000)

conduct financial appraisals on capital projects, the choice of method varies consider-

ably, and most firms employ a combination of appraisal techniques.

The use of DCF methods in larger firms increased greatly from 58 per cent in 1975

to 100 per cent by 1997. Hitherto, the IRR method enjoyed much greater popularity

than the theoretically preferred NPV approach. However, in recent years, there has

been a marked acceleration in adoption of the NPV method, with virtually all large

firms now employing it.

The payback method has declined in popularity in recent years, but remains more

popular with smaller firms. It is clear that firms do not normally rely on any single

appraisal measure, but prefer to employ a combination of simple and more sophisti-

cated techniques. DCF methods therefore complement, rather than substitute for,

traditional approaches.

■ Dangers with DCF

While we have argued that DCF analysis offers a conceptually sound approach for

appraising capital projects, a word of caution is appropriate.

From the emphasis devoted by most textbooks to advanced capital budgeting meth-

ods, one might be forgiven for assuming that successful investment is exclusively

attributable to the correct evaluation method. However, DCF methods often create an

illusion of exactness that the underlying assumptions do not warrant. As top manage-

ment places more weight on the quantifiable element, there is a danger that the

unquantifiable aspects of the decision, which frequently have a critical bearing on a

project’s success or failure, will be devalued. The human element is particularly

important with regard to the project sponsor. The margin between a project’s success

or failure often hinges on the enthusiasm and commitment of the person sponsoring

and implementing it.

Managers cannot afford to treat investment decisions in a vacuum, ignoring the

complexities of the business environment. Any attempt to incorporate such complex-

ities, however, will at best consist of abstractions from reality relying on generalised

and simplified assumptions concerning business relationships and environments. A

fundamental assumption underlying DCF methods is that decision-makers pursue

the primary goal of maximising shareholders’ wealth. For many firms, this may not

be the case.

Critical errors may often be seen in the way DCF theory is applied by managers.

Usually, these errors are biased against investment. For example, many firms do not

adjust their operating cash flows for inflation, but discount them at the money cost of

capital, rather than the real rate of return before inflation. The effect is that cash flows

in later years (typically the strong positive cash flows) are unduly deflated by the high

discount factor, giving a lower net present value than should be the case.

Perhaps even more important, DCF methods ignore the value of investment options.

This key topic is the subject of Chapter 12.

CFAI_C06.QXD 10/26/05 11:27 AM Page 158

.

Chapter 6 Project appraisal – applications 159

Common errors in applying DCF

■ Discount rates are calculated on a pre-tax basis, while operating cash flows are calcu-

lated after tax.

■ Discount rates are increased to compensate for non-economic statutory and welfare

investments.

■ Including interest charges in cash flows.

■ Cash flows are specified in today’s money (excluding inflation), while hurdle rates are

based on the money cost of capital (including inflation).

■ Managerial aversion to uncertainty frequently results in conservative project life and

terminal value assumptions.

■ Use of a single cut-off rate instead of a rate reflecting project risk. This often leads to

rejection of low-risk/low-return replacement projects.

■ Failure to include scrap values.

■ Neglect of working capital movements.

6.7 TRADITIONAL APPRAISAL METHODS

Managers have developed and come to rely upon simple rule-of-thumb approaches to

analysing investment worth. Two of the most popular traditional methods are the pay-

back period and the accounting rate of return, both of which were described in earlier

chapters. Our present concern is to ask whether they have a valuable role to play in the

modern capital budgeting process. Do they offer anything to the decision-maker that

cannot be found in the DCF approaches?

■ Accounting rate of return (ARR)

We discussed the basic application of the ARR approach in Chapter 5. Table 6.8 reports

that a little over half the companies surveyed employ the accounting rate of return

approach in assessing investment decisions. This is not altogether surprising, given that

the rate of return on capital is a very important financial goal in practice.

The ARR can be criticised on at least two counts: it uses accounting profits rather

than cash flows, and it ignores the time-value of money. Nevertheless there has been

a certain amount of support for the ARR in the literature. The absence of ARR leads to

an inconsistency between the methods commonly used to report a firm’s results and

the techniques most frequently employed to appraise investment decisions. This is

most acutely experienced where the divisional manager of an investment centre is

expected to use a DCF approach in reaching investment decisions, while his or her

short-term performance is being judged on a return on investment basis. Little won-

der, then, that the divisional manager generally shows a marked reluctance to enter

into any profitable long-term investment decisions that produce low returns in the

early years.

A common assumption among managers is that the accounting rate of return and

the internal rate of return produce much the same solutions. But while there is a rela-

tionship between a project’s discounted return and the ARR, the relationship is not

simple. Consider an investment costing £10,000 and generating an annual stream of

net cash flows of £3,000. Assuming straight-line depreciation, the relationship between

the internal rate of return and the accounting rate of return calculated on both the total

investment and the average investment is as shown in Table 6.9.

From this example we can see that the accounting rate of return on total investment

consistently understates, and the accounting rate of return on average investment over-

states, the internal rate of return. The case for retaining the accounting rate of return is,

CFAI_C06.QXD 10/26/05 11:27 AM Page 159

.

160 Part II Investment decisions and strategies

Table 6.9

Relationship between

ARR and IRR

Project duration (years) 5 10 20 25

IRR (%) 15.2 27.3 29.8 30

ARR on total investment (%) 10 20 25 27.5

Deviation from IRR

ARR on average investment (%) 20 40 50 55

Deviation from IRR

2520.212.74.8

2.54.87.35.2

£m PV @ 10% (£m)

Yr 1 profit 10

Investment outlay: £60 m

10% capital charge on investment (6

)

Residual income 4

Yr 2 profit 10

Book value of assets: £40 m

10% capital charge (4

)

6

Yr 3 profit 10

Book value of assets: £20 m

10% capital charge (2

)

8

Net present value 14.600

0.751 6.008

0.826 4.956

0.909 3.636

therefore, valid only when applied as a secondary criterion to highlight the likely

impact on the organisation’s profitability upon which the divisional manager is

judged.

Residual income approach: Pluto Electronics

While the average accounting return can be a misleading decision indicator for capital

projects, it is possible to employ a profit-based approach that is in line with net present

value. This involves calculating the Residual Income (RI), the profit less a cost of capital

charge based on the book value of the assets employed.

Pluto Electronics has acquired the rights to manufacture a product for three years

and has set up a new division to do so. The investment outlay is £60 million and annu-

al cash flows are forecast to be £30 million. The company operates a straight-line

depreciation policy and has a cost of capital of 10 per cent.

We can calculate the NPV (£m) as:

The same answer is given by calculating the residual income for each year and dis-

counting at the cost of capital, as shown below. The annual profit is £10 million (i.e. £30

million cash flow less £20 million depreciation).

NPV 60 30

#

PVIFA

10,3

60 130 2.48682 £14.6 m

Residual Income

Operating profit less the charge

for capital

■ Payback period

Most finance texts have condemned the use of the payback period as potentially mis-

leading in reaching investment decisions. However, Table 6.8 shows that it continues to

flourish, being employed by most firms surveyed. Typically, the payback period

required by firms is within 2–4 years (Arnold & Hatzopoulos 2000). Why is payback

so popular? Does it possess certain qualities not so apparent in more sophisticated

approaches?

CFAI_C06.QXD 10/26/05 11:27 AM Page 160

.

Chapter 6 Project appraisal – applications 161

The two main objections to payback (PB)

1 It ignores all cash flows beyond the payback period.

2 It does not consider the profile of the project’s cash flows within the payback period.

Although such theoretical shortcomings could fundamentally alter a project’s ranking and

selection, the payback criterion possesses a number of merits.

1 PB estimates DCF return

The payback period provides a crude measure of investment profitability. When the

annual cash receipts from a project are uniform, the payback reciprocal is the internal

rate of return for a project of infinite life, or a good approximation to this rate for long-

lived projects.

In the case of very long-lived projects where the cash inflows are, on average, spread

evenly over the life of the project, the payback reciprocal is a reasonable proxy for the

internal rate of return. For example, a project offering permanent cash savings and giv-

ing a four-year payback period with relatively stable annual cash returns will have

approximately a 25 per cent internal rate of return (i.e. the reciprocal of payback peri-

od). However, if the project life is only ten years, the IRR would fall to 21 per cent –

some four percentage points below the payback reciprocal. In fact, the payback recip-

rocal consistently overstates the true rate of return for finite project lives.

2 PB considers uncertainty

Whereas more sophisticated techniques attempt to model the uncertainty surrounding

project returns, payback assumes that risk is time-related; the longer the period, the

greater the chance of failure. General economic uncertainty makes the task of forecast-

ing cash flows extremely difficult; but for the most part, cash flows are correlated over

time. If the operating returns are below the expected level in the early years, they will

probably also be below plan in the later years.

Discounted cash flow, as practised in most firms, ignores this increase in uncertain-

ty over time. Early cash flows, therefore, have an important information content on the

degree of accuracy of subsequent cash flows. By concentrating on the early cash flows,

the payback approach analyses the data where managers have greater confidence. If

such evaluation provides a different signal from DCF methods, it highlights the need

for a more careful consideration of the project’s risk characteristics.

3 PB as a screening device

Payback provides a relatively efficient method for ranking projects when constraints

prevail. The most obvious constraint is the time that managers can devote to initial

product screening. Only a handful of the investment ideas may stand up to serious and

thorough financial investigation. Payback period serves as a simple, first-level screen-

ing device which, in the case of marginal projects, tends to operate in their favour and

permits them to go forward for more thorough investigation.

Many firms also resort to payback period when experiencing liquidity con-

straints. Such a policy may make sense when funds are constrained and better

investment ideas are in the pipeline. The attractiveness of investment proposals

considered during the interim period will be a function more of their ability to pay

back rapidly than of their overall profitability. This does not necessarily lead to

optimal solutions.

IRR

1

payback period

CFAI_C06.QXD 10/26/05 11:27 AM Page 161

.

162 Part II Investment decisions and strategies

Self-assessment activity 6.6

The following reasons for using payback were made by finance executives from three dif-

ferent companies:

‘We use payback in support of other methods. It is not a sufficiently reliable tool to be

used in isolation.’

‘When liquidity is under pressure, payback is particularly relevant.’

‘Payback helps to give some idea of the riskiness of the project – a long time to get

one’s money back is obviously more risky than a short time.’

To what extent do you agree with these views?

4 PB assists communication

Managers feel more comfortable with payback period than with DCF. In the first place,

it is simple to calculate and understand. The non-quantitative manager is reluctant to

rely on the recommendations of ‘sophisticated’ models when he or she lacks both the

time and expertise to verify such outcomes. Confidence in and commitment to a pro-

posal depend to some degree on how thoroughly the evaluation model is compre-

hended. The payback method offers a convenient shorthand for the desirability of each

investment that is understandable at all levels of the organisation: namely, how quick-

ly will the project recover its initial outlay? Some firms use a project classification sys-

tem in which the payback period indicates how rapidly proposals should be processed

and put into operation.

Ultimately, it is the manager – not the method – who makes investment decisions

and is appraised on their outcome. Payback period is particularly attractive to man-

agers not only because it is convenient to calculate and communicate, but also because

it signals good investment decisions at the earliest opportunity.

While the payback concept may lack the refinements of its more sophisticated eval-

uation counterparts, it possesses many endearing qualities that make it irresistible to

most managers; hence its resilience.

■ The appropriate discount rate

So far the examples used have simply stated the project discount rate based on the cost

of capital, the rate of return required by investors. We discuss in some depth the appro-

priate discount rate in later chapters. Here, we outline one approach, the Weighted

Average Cost of Capital (WACC).

This measures the rate of return that the firm must achieve in order to satisfy all of

the people who invest in it. All of these investors incur an opportunity cost when plac-

ing their money in the hands of the firm’s managers. This is the rate of return they

could have achieved on the next best alternative investment.

Example

Wacky Ideas PLC Ltd produces novelty toys. It currently finances its business one-third

through loans and two-thirds through equity and reserves. Looking ahead it does not

expect to change this funding mix. The accountant estimates that the cost of equity is

12 per cent while the after-tax cost of borrowing is lower at 9 per cent. Given this infor-

mation we can calculate the average cost of capital for the company, duly weighted

according to the proportion of capital represented by equity and borrowings respec-

tively. For Wacky this is:

CFAI_C06.QXD 10/26/05 11:27 AM Page 162

.

Chapter 6 Project appraisal – applications 163

Source of capital Proportion Cost of capital Weighted Cost

Equity 8%

Loans 3

%

WACC 11%

9%

33%

12%

67%

The Weighted Average Cost of Capital (WACC) approach multiplies the cost of each

source of capital by the proportion of the total capital it represents. The results are

summed to provide a WACC estimate of 11 per cent in Wacky’s case. If we assume that

each new investment project receives a slice of the total capital in the same 2:1 equi-

ty:borrowing proportion, and that the project has the same level of risk as the typical

investments in the firm, we can apply a discount rate of 11 per cent in calculating the

project’s net present value. We leave the issue of determining the cost of capital for

each source of finance to a later chapter.

One of the most difficult aspects of capital budgeting is identifying and gathering the

relevant information for analysis. This chapter has examined the incremental cash

flow approach to project analysis. Specific attention has been paid to the replacement

decision and to the impact of inflation and taxation on investment decisions.

Key points

■ Include only future, incremental cash flows relating to the investment decision and

its consequences. This implies the following:

1 Only additional fixed overheads are included.

2 Depreciation (a non-cash item) is excluded.

3 Sunk (or past) costs are not relevant.

4 Interest charges are financing (not investment) cash flows and are therefore

excluded from the cash flow profile.

5 Opportunity costs (e.g. the opportunity to rent or sell premises if the proposal is

not acceptable) are included.

■ Replacement decision analysis examines the change in cash flows resulting from the

decision to replace an existing asset with a new asset.

■ Inflation can have important effects on project analysis. Two approaches are possi-

ble: (1) specify all cash flows at ‘money-of-the-day’ (i.e. including inflation) prices

and discount at the money cost of capital, or (2) specify cash flows at today’s prices

and discount at the real (i.e. net of inflation) cost of capital. We recommend the for-

mer in most cases.

■ Taxation is for most organisations a cash flow. Tax is calculated by deducting any

cash benefits from tax relief on the initial capital expenditure from tax payable on

additional cash flows. Care should be taken in estimating the timing of tax cash

flows.

■ In practice, most firms, particularly larger companies, employ a combination of

DCF and traditional appraisal methods.

■ One way of estimating the discount rate to be used is to calculate the firm’s

Weighted Average Cost of Capital.

SUMMARY

CFAI_C06.QXD 10/26/05 11:27 AM Page 163

.

164 Part II Investment decisions and strategies

Table 6.10

Allis plc cash flows for

two projects

Year Forklift trucks Conveyor system

0 (30,000) (66,000)

1 10,000 12,000

2 15,000 20,000

3 18,000 20,000

4 18,000

5 15,000

6 15,000

NPV at 10% 5,010 6,538

Further reading

Most finance texts are not particularly strong on the applied aspects of capital budgeting.

Pohlman et al. (1988) describe cash flow estimation practices in large firms. Levy and Sarnat

(1994) has useful chapters, but the US tax system is employed. For a discussion on the invest-

ment appraisal criteria under low inflation, see the Bank of England (1994). Pointon (1980)

examines the effect of capital allowances on investment, while Hodgkinson (1989) surveys tax

treatment in corporate investment appraisal.

Studies on the investment practices of UK firms are well worth reading. See, for example, Pike

(1982, 1988, 1996), McIntyre and Coulthurst (1985), Mills (1988), Pike and Wolfe (1988) and

Arnold and Hatzopoulos (2000). Useful references on the capital budgeting process are Cooper

(1975), Pinches (1982) and Neale and Holmes (1991). Tomkins (1991) and Butler et al. (1993)

explore the strategic and organisational aspects in greater depth.

replacement chain

approach

The process of comparing like-

for-like replacement decisions

for mutually exclusive projects

with different lives over a com-

mon time period

APPENDIX

THE PROBLEM OF UNEQUAL LIVES: ALLIS PLC

Comparing mutually exclusive projects – such as retaining the old asset or replacing it

with a new one – frequently involves the problem of assessing projects with different

economic lives.

Allis plc is seeking to modernise and speed up its production process. Two propos-

als have been suggested to achieve this: the purchase of a number of forklift trucks and

the acquisition of a conveyor system. The accountant has produced cost savings fig-

ures for the two proposals using a 10 per cent discount rate, shown in Table 6.10.

At first sight, the more expensive conveyor system appears more wealth-creating.

But it is not appropriate to compare projects with different lives without making some

adjustment. Two approaches can be employed for this: the replacement chain approach

and the equivalent annual annuity approach.

The replacement chain approach recognises that while, for convenience, we usually

consider only the time-horizon of the proposal, most investments form part of a

replacement chain over a much longer time-period. We therefore need to compare

mutually exclusive projects over a common period. In the example, this period is six

years, two forklift truck proposals (one following the other) being equivalent to one

conveyor system proposal. Assuming the cash flows for the original forklift trucks

also apply to their replacements in Year 4 (a pretty big assumption, given inflation,

CFAI_C06.QXD 10/26/05 11:27 AM Page 164