Бауэрс Н., Гербер Х., Джанс Д., Несбитт С., Хикман Дж. Актуарная математика

Подождите немного. Документ загружается.

Приложение

5

НЕКОТОРЫЕ

МАТЕМАТИЧЕСКИЕ

ФОРМУЛЫ,

ПРИМЕНЯЕМЫЕ

В

АКТУАРНОЙ

МАТЕМАТИКЕ

l

{3(t>

F(t)

=

f(x,

t)

dx,

a:(t)

dF(t)

jf;J(t)

д

d d

dt =

-8

f(x,

t)

dx

+ f(f3(t),

t)

-d

f3(t)

- f(Q(t),

t)

-d

Q(t).

a:(t)

t t t

Ис'Чuслен.uе

1Сон.е'Чн.'Ых

раз'Н,остеЙ.

(а)

Операторы

сдвига:

Мы

не

ставим

здесь

цели

напомнить

известные

стандартные

формулы

и

методы,

но

указываем

те

из

них,

которые

могут

быть

менее

привычны

для

студентов-актуариев.

Интеграл,'ьн.ое

ис'Численuе.

Если

то

E(f(x)] =

f(x

+

1).

(Ь)

Операторы

конечных

разностей:

Ilf(x)

=

f(x

+

1)

-

f(x)

=

(Е

-1)f(x).

(с)

Кратные

операторы

конечных

разностей:

n

Il

n

f(x)

=1l(1l

п-l

f(x») =

(Е

_1)П

f(x)

=

EC

k

(

_1)n-k

f(x

+k).

k=O

(d)

Оператор конечных

разностей,

примененный

к

про:изведению:

Il[j(x)g(x») =

f(x

+

1)llg(x)

+

g(x)llf(x).

(е)

Обратный

к

разностному

оператору:

если

Ilf(x)

=

у(х),

то

Il

-1

у

(х)

=

f(x)

+

ш(х),

где

ш(х)

=

ш(х

+1).

Прило:же'Н,u.я..

(а)

Представление

полинома (формула

Ньютона).

Пусть

рп(х)

-

полином

степени

n.

Тогда

n

рп

(х)

=

2:

с:

-

а

Il

k

рп

(а).

(Ь)

Суммирование

рядов:

k=O

если

IlF(x)

=

f(x),

то

f(1)

=

Р(2)

-

Р(1),

f(2)

=

F(З)

-

Р(2),

f(n)

=

Р(n

+1) -

Р(n),

n

п+l

L

f(x)

=

Р(n

+

1)

-

Р(1)

=

Il

-1

f(x)ll

.

х=1

(с)

Суммирование

по

частям:

n

I

n+l

1 I

n

+

1

~

g(x)llf(x)

=

f(x)g(x)

1 -

Il

-

[f(x

+

1)6.у(х»)

1 .

[Доказательство:

просуммиру:йте

обе

части

равенства

ДЛЯ

Il[f(x)g(x»)

по

х

от

1

до

n.]

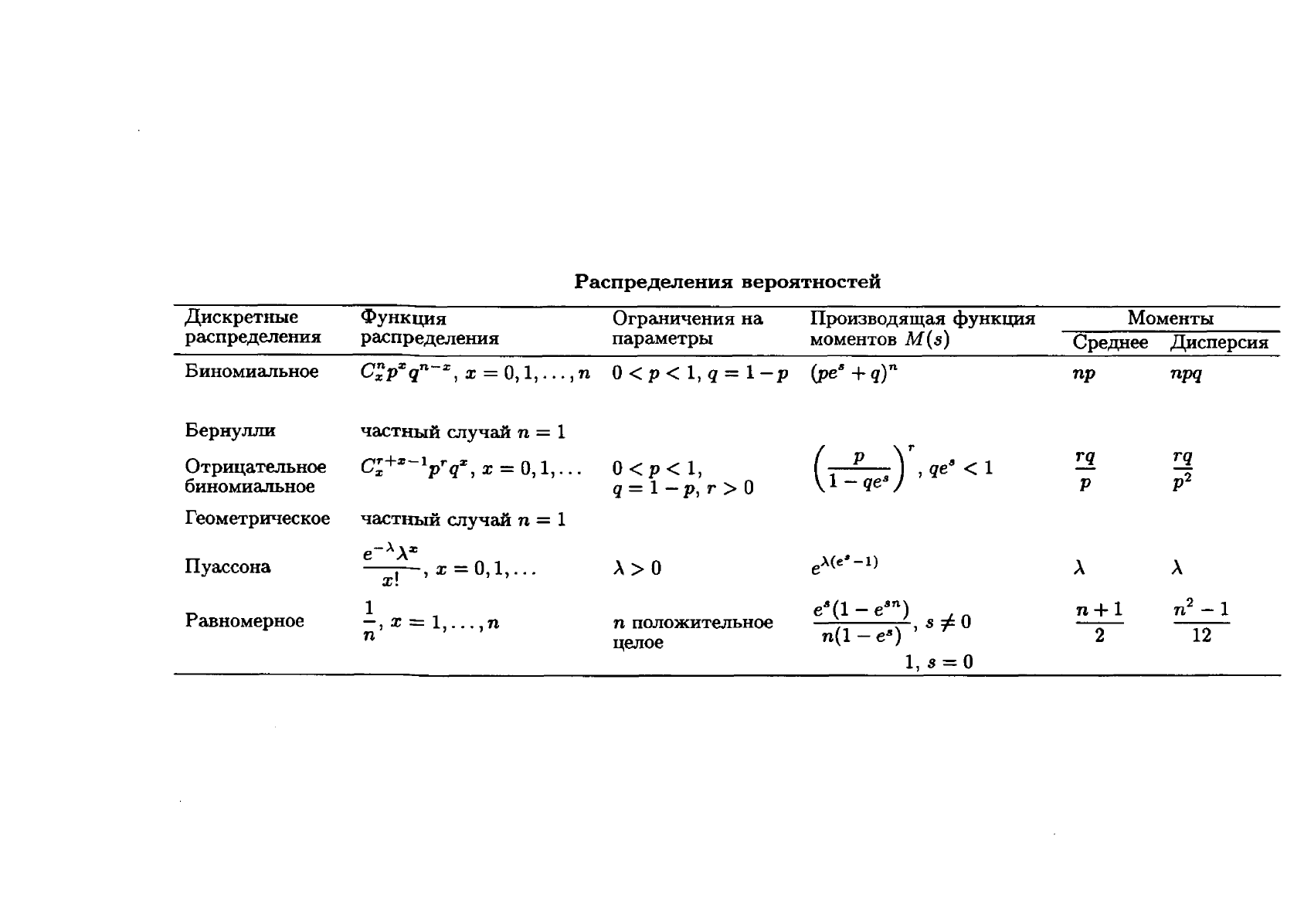

Распределения

вероятностей

Дискретные

ФУНкция

Ограничения

на

Производящая

функция

Моменты

распределения

распределения

параметры

моментов

М

(э)

СредНее

Дисперсия

Биномиальное

СП

:е

n-:е

О

1

0<

Р

< 1, q =

1-

Р

(РеВ

+q)n

пр

npq

:еР

q ,

х

= , ,

...

,n

Бернулли

частный

случай

n = 1

Отрицательное

cr+:e-l

r

ж

О

1

0<

р

< 1,

(

Р

)',

qe'

< 1

rq rq

ж

pq,x=,

,

...

р2

биномиальное

q = 1 -

р,

r >

О

1-

qe

B

р

Геометрическое

частный

случай

n = 1

Пуассона

e->'л

Z

,

х

=

0,1,

...

Л>О

e>.(e·-l)

л

Л

х!

1

е

В

(l

_е

аn

)

n+1

n

2

-1

Равномерное

-,х=1,

...

,n

n

положительное

) , s

1=

о

--

n

целое

n(1 -

еВ

2

12

1 s =

О

1

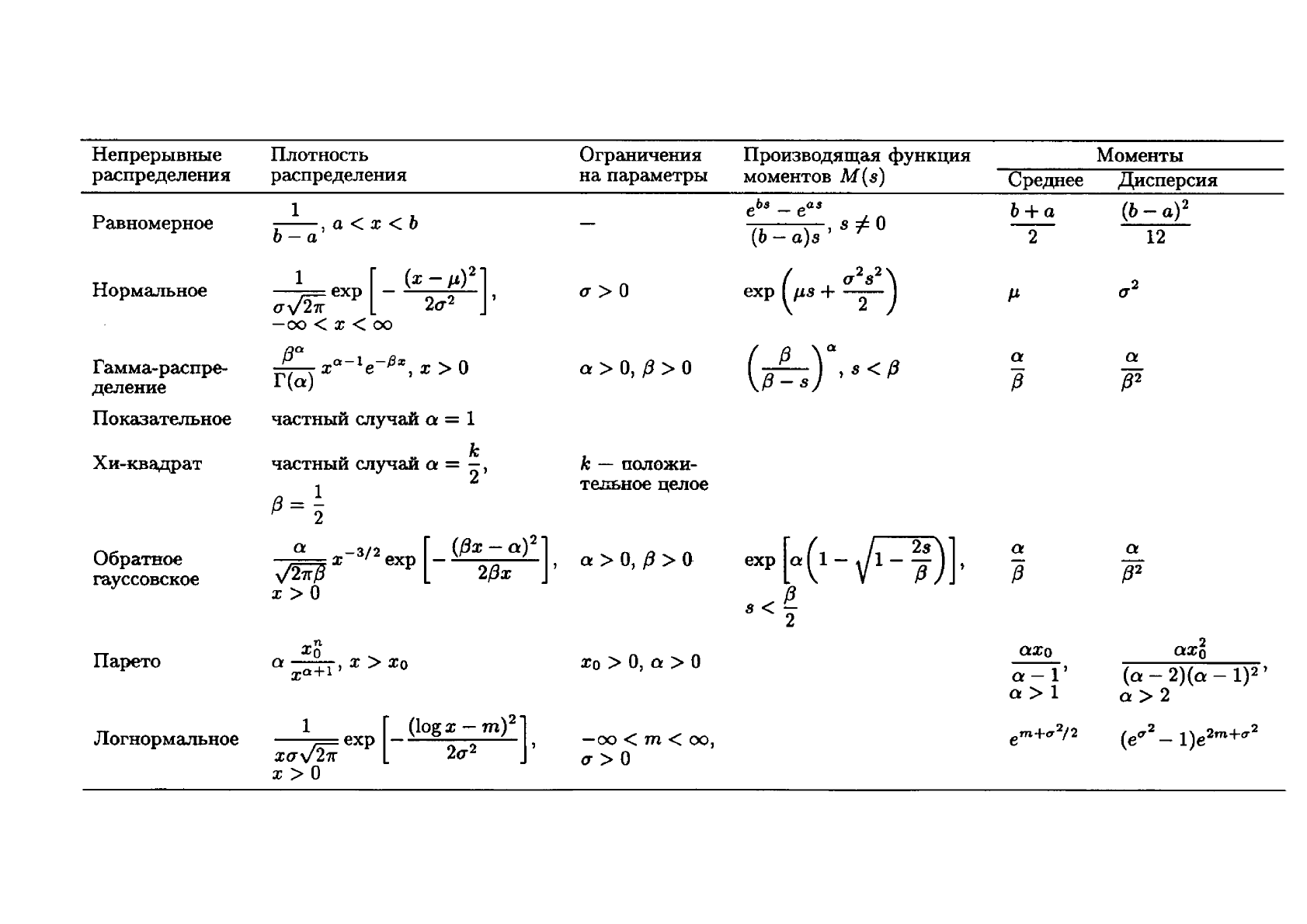

Непрерывные

llлОТНОСТЬ

Ограничения

Производящая

функция

Моменты

распределения

распределения

на

параметры

моментов

М

(s)

Среднее

Дисперсия

1

е

ЬЭ

_

ео.

а

Ь+а

(Ь

-

а)2

Равномерное

-Ь--'

а

<

х

<

Ь

-

(Ь

_

а)а

' s #

о

--

-а

2 12

Нормальное

1

[(Х_I')2]

0->0

(

и

2

•

2

)

0-2

0-V'2iГ

ехр

-

2и2

'

ехр

p.s

+

-2-

Р.

-00

<

х

<

00

Гамма~распр~

(30

0-1

-j3;c

>

о

а

>

О,

(3 >

о

(/

.)",.<р

а а

Г(а)

х

е

,

х

(3

(32

деление

Показательное

частный

случай

а

= 1

Хи-квадрат

u u k

k -

положи-

частныи

случаи

а

=

'2)

fЗ=!

Te.zrьнoe

целое

2

Обратное

'"

-З/2

[(рх_",)2]

а

>

О,

f3

>

о

exp["'(l-Jl

~)],

а а

..j21ГP

х ехр

-

2fЗх

'

- -

гауссовское

f3

(32

Х>О

8 <

f3

2

Парето

Ха

Ха

>

О,

а

>

О

аХа

ax~

а

х

О

+1 '

Х

>

Ха

а-1'

(а

-

2)(а

-

1)2

)

а>1

а>2

Логнорма.льное

1 [

(logx

-

т)2]

-00

<

т

<

00,

е

т

+

с72

/

2

(е

с72

_

1)е

2т

+

с72

ехр

-

xo-V'2iГ

20-2'

и>О

Х>О

Приложение

6

ЛИТЕРАТУРА

Actuarial Society of America.

(1947)

International

Actuarial Notation, Transactions

о/

the Actuarial Society

о!

Атепса,

ХLVПI:166-176.

Allen J.

М.

(1907)

Оп

the

Relation between

the

Theories of Compound

Interest

and

Life Contingencies,

Joumal

о/

the Institute

о/

Actuaries, 41:305-337.

Allison G.

О.,

Winklevoss

Н.

Е.

(1975)

The

Interrelationship among Inflation Rates,

Interest

Rates,

and

Pension Costs,

Transactions

о/

the Society

о/

Actuaries,

ХХУII:197-210.

Anderson J.

С.

Н.

(1959) Gross

Premium

Calculations

and

Profit Measurement for Nonparticipating Insurance,

Transactions

о!

the Society

о/

Actuaries, XI:357-394.

Arrow

К.

J.

(1963)

Uncertainty

and

the

Welfare

of

Medical

Саге,

Атепсаn

Econoтic

Review, 53:941-

973.

Balducci

а.

(1921) Correspondence.

Joumal

о/

the Institute

о/

Actuaries, 52:184.

Bartlett

D.

К.

(1965) Excess

Ratio

Distributions in Risk Theory, Transactions

о/

the Society

о/

Actuaries!

XVIL:435-463.

Batten

R. W.

(1978) Mortality

ТаЫе

Construction. Englewood Cliffs, N.J.: Prentice Hall.

Beard R.

Е.,

Pentikainen

Т.,

Pesonen

Е.

(1984)

Risk

Theory. 3rd ed. New York:

Chapman

&

НаН.

Becker

D.

N.

(1991) Statistical Tests of

the

Lognormal Distribution as

а

Basis for

Interest

Rate

Changes,

Transactions

о/

the Society

о/

Actuaries, XLIII:7-57.

Beekman J.

А.

(1969)

А

Ruin

Function Approximation. Transactions

о/

the Society

о!

Actuaries, XXI:41-

48.

Beekman J.

А.

(1974) Two Stochastic Processes. New York: Halsted Press.

Beekman J.

А.,

Bowers

N.

L.

(1972) An Approximation

to

the

Finite Time

Ruin

Function, Skandinavisk Aktuarietidskri/t,

41-56, 128-137.

BeHhouse D. R.,

Panjer

Н.

Н.

(1980) Stochastic Modelling of Interest

Rates

with

Applications

to

Life Contingencies, Jour-

nal

о/

Risk

and Insurance, 47:91-110.

Bellman R.

Е.,

Kalaba

R.

Е.,

Lockett J.

(1966)

Nuтerical

Inversion

о/

the Laplace

Trans/orт:

Applications

to

Biology, Economics,

Engineering, and Physics. New York: American EIsevier.

Приложение

6

615

Bicknell W. S.,

Nesbitt

С.

J.

(1956)

Premiums

and

Reserves in Multiple Decrement Theory, Transactions

о/

the Society

о/

Actuaries, VIII:344-377.

Biggs J.

Н.

(1969) Alternatives in Variable

Annuity

Benefit Design, Transactions

о/

the Society

о/

Actuaries, XXI:495-517.

Black F., Scholes

М.

(1973)

The

Pricing of Options

and

Corporate Liabilities,

Joumal

о/

Political

Есоnоту,

81:637-659.

Boermeester J.

М.

(1956) Frequency Distribution of Mortality Costs, Transactions

о/

the Society

о/

Actuaries,

VIII:1-9.

Bohman

Н.,

Esscher F.

(1963, 1964) Studies in Risk Theory with Numerical Illustrations Concerning Distribution

Functions

and

Stop-Loss Premiums, Skandinavisk Aktuarietidskrijt, 173-225, 1-40.

Borch

К.

(1960)

An

Attempt

to

Determine

the

Optimum

Amount of Stop-Loss Reinsurance, Trans-

actions

о/

the 16th International Gongress

о/

Actuaries, 1:597-610.

Borch

К.

(1974)

The

Mathematical Theory

o/Insurance.

Lexington, Mass.: Lexington Books.

Bowers N.

L.

(1966) Expansions of Probability Density Functions as

а

Sum

of

аашта

Densities with

Applications in Risk Theory,

Transactions

о/

the Society

о/

Actuaries, XVIII:125-137.

Bowers

N.

L.

(1967) An Approximation

to

the

Distribution of

Annuity

Costs, Transactions

о/

the Society

о/

Actuaries, XIX:295-309.

Bowers

N.

L.

(1969)

Ап

Upper Bound for

the

Net Stop-Loss

Premium,

Transactions

о/

the Society

о/

Actuaries,

XXI:211~218.

Bowers N. L., Jr., Hickman J.

С,

Nesbitt

С.

J.

(1976)

Introduction

to

the

Dynamics

of

Pension Funding, Transactions

о/

the Society

о/

Actuaries, XXVIII:177-203.

Bowers

N.

L., Jr., Hickman J.

С.,

Nesbitt

С.

J.

(1979)

ТЬе

Dynamics of Pension Funding: Contribution Theory, Transactions

о/

the Society

о/

Actuaries, XXXI:93-119.

Boyle

Р.

Р.

(1992) Options and the Management

о/

Financial Risk. Schaumburg, IlI.: Society of Actua-

rles.

Brenner

Н.

Р.,

et

al.

(1988)

Li/e

Insurance Accounting.

Durham,

N.C.: Insurance Accounting

and

Systems Asso-

ciation.

Brillinger D. R.

(1961)

А

Justification of Some Common Laws of Mortality, Transactions

о/

the Society

о/

Actuaries, XIII:116-119.

Buchta

С.

(1994) An Elementary Proof of

the

Schuette-Nesbitt Formula, Bulletin

о/

the Swiss Associa-

tion

о/

Actuaries, 219-220.

Biihlmann

Н.

(1970) Mathematical Methods in Risk

ТЬеоту.

New York: Springer.

Carriere J. F.

(1994) Dependent Decrement

ТЬеоту,

Transactions

о/

the Society

о/

Actuaries, XLVI:45-65.

616

Приложение

6

Chalke

S.

А.

(1991) Maero Pricing:

А

Comprehensive

Product

Development Process, Transactions

о/

the

Society

о/

Actuaries, XLIII:137-194.

Chalke

S.

А.,

Davlin

М.

F.

(1983) Universal Life Valuation

and

Nonforfeiture:

А

Generalized Model, Transactions

о/

the Society

о/

Actuaries, XXXV:249-298.

Chamberlin

С.

(1982)

The

Proficient

Instrument

-

а

New Appraisal of

the

Commutation

Function in

the

Context

of

Pension

Fund

Work,

Joumal

о/

the /nstitute

о/

Actuaries

Students'

Society,

25:1-46.

Chapin W. L.

(1976)

Toward

Adjustable Individual Life Policies, Transactions

о/

the Society

о/

Actuaries,

XXVIII:237-269.

Chiang

С.

L.

(1968) Introduction to Stochastic Processes

in

Biostatistics. New York:

John

Wiley

and

Sons.

Christiansen

S.

L.

(1992)

А

Praetical Guide

to

Interest

Rate

Generators for

С-3

Risk, Transactions

о/

the

Society

о/

Actuaries, XLIV:101-134.

Cody D. D.

(1981) An

Expanded

Financial

Structure

for

Ordinary

Dividends, Transactions

o/the

Society

о/

Actuaries, XXXIII:313-338.

Committee

оп

Ordinary Insurance

and

Annuities.

(1982)

П.

1975-80 Basic Tables

with

Appendix of Age-Last

Birthday

Basic Tables,

ТВА

1982

Reports, 56-81.

Cram~r

Н.

(1930)

Оп

the Mathematical Theory

о/

Risk. Stockholm: Centraltryckeriet.

Cummins J. D.

(1973) Development

о/

Li/e Ins'/J,rance

SШ'rеndеr

Vаlu.ея

in

the United States. Homewood,

Ill.: Richard D. Irwin.

DeGroot

М.

Н.

(1970)

Optiтal

Statistical Decisions. New York:

McGraw-Нill.

[Имеется

перевод:

Де

Гро

от

М.

Оптимальные

статистические

решения.

-

М.,

Мир,

1974.]

DeGroot

М.

Н.

(1986) Probability and Statistics. 2nd ed. Reading, Mass.: Addison-Wesley.

DeVylder F.

(1977) Martingales

and

Ruin

in

а

Dynamic Risk Process, Scandinavian

Actuarial

Joumal,

217-225.

Dropkin

L.

В.

(1959) Some Considerations in Automobile

Rating

Systems Utilizing Individual Driving

Records,

Proceedings

о/

the Casualty Actuarial Society, XLVI:165-176.

Dubourdieu J.

(1952) Theorie

Matheтatique

des Assurances. Paris:

Gauthier

Villars.

Duncan, R.

М.

(1952)

А

Retirement

System

Granting

Unit Annuities

and

Investing in Equities, Transactions

о/

the Society

о/

Actuaries, IV:317-344.

Elandt-Johnson R.

С.,

Johnson

N.

L.

(1980) Survival Models and Data Analysis. New York:

John

Wiley

and

Sons.

Fama

Е.

F.

(1970) Efficient Capital Markets:

А

Review of Theory

and

Empirical Work,

Joumal

01

Finance, 25:383-417.

Приложение

6

617

Fassel

Е.

С.

(1956)

Premium

Rates

Varying

Ьу

РоНсу

Size, Transactions

о/

the Society

о/

Actuaries,

VIII:390-419.

Feller

W.

(1966)

Аn

Introduction to Prohability Theory and Its Applications. Vol.

11.

New York:

John

Wiley

and

Sons.

[Имеется

перевод:

Феллер

В.

Введение

в

теорию

вероятностей

и

ее

приложения.

Т.

2.

-

М.:

Мир,

1984.]

Feller

W.

(1968)

Аn

Introdu.ction to Probability Theory and Its Applicatians. Vol.

1.

3rd

ed. New York:

John

Wiley

and

Sons.

[Имеется

перевод:

Феллер

В.

1Зведение

в

теорию

вероятностей

и

ее

приложения.

Т.

1.

-

М.:

Мир,

1984.]

Fraser

J.

С.,

Miller

W.

N., Sternhell

С.

М.

(1969) Analysis

of

Basic

Actuarial

Theory

for

Fixed

Premium

Variable Benefit Life Insurance,

Transactions

о/

the Society

о/

Actuaries, XXI:343-78,

and

discussions 379-457.

Fra.sier

W.

М.

(1978)

Second

to

Die

Joint

Life

СавЬ

Values

and

Reserves, The Actuary, 12:3.

Frees

Е.

W.

(1990)

Stochastic

Life Contingencies

with

Solvency Considerations, Transactions

о/

the

Society

о/

Actuaries,

ХLП:91-129.

Frees

Е.

W.,

Carriere

J.

F., Valdez

Е.

(1996)

Annuity

Valuation

with

Dependent

Mortality, Journal

о/

Risk and Insurance, 63:229-

261.

Fretwel1 R. L.,

Hickman

J.

С.

(1964)

Approximate

Probability

Statements

about

Life

Annuity

Costs, Transactions

о/

the

Society

о/

Actuaries, XVI:55-60.

Friedman

М.,

Savage

L.

J.

(1948)

The

Utility

Analysis

of

Choices Involving Risk,

Joumal

о/

Political

Есоnоту,

56:279-

304.

Genest

С.

(1987)

Frank's

Family

of

Bivariate

Distributions,

Biometrika, CXXIV:549-555.

Geoghegan

Т.

J.,

et

al.

(1992)

Report

оп

the

Wilkie Stochastic

Investment

Model,

Joumal

о/

the Institute

о/

Actua-

ries,

119,

Part

П,

No. 473:173-228.

Gerber

Н.

U.

(1973) Martingales

in

Risk

Theory,

Mitteilungen der Vereinigung Schweizerischer Versic-

herungsmathematiker,

LХХПI:

205-16.

Gerber

Н.

U.

(1974)

ТЬе

Dilemma

between

Dividends

and

Safety

and

а

Generalization

of

the

Lundberg-

Cramer

Formulas,

Scandinavian Actuarial Journal, 46-57.

Gerber

Н.

U.

(1976)

А

Probabilistic

Model for (Life) Contingencies

and

а

Delta-Free

Approach

to

Contin-

gency Reserves,

Transactions

о/

the Society

о/

Actuaries,

ХХVПI:127~141.

Gerber

Н.

U.

(1979)

Аn

Introduction

to

Mathematical Risk Theory.

Huebner

Foundation

Monograph 8,

distributed

Ьу

Richard

D. Irwin, Homewood, Ill.

Gerber

Н.

U.

(1980) Principles of

Premium

Calculation

and

Reinsurance, Transactions

о/

the 21st Inter·

national Congress

о/

Actuaries, 1:137-142.

Gerber

Н.

U.,

Jones

D.

А.

(1977) Some

Practical

Considerations

in

Connection v;ith

the

Calculation of Stop-Loss

Pre-

miums,

Transactions

о/

the Society

о/

Actuaries, XXVIII:215-232.

618

Приложение

6

Gerber

Н.

U., Shiu

Е.

S.

(1998)

Оп

the

Time

Value

of

Ruin,

North

Атепсаn

Actuarial

Joumal,

Il, No. 1:48-78.

Giaccotto

С.

(1986) Stochastic Modelling

of

Interest Rates: Actuarial vs.

ЕquiliЬгiuш

Approach,

Journal

Ь/

Risk

and

Insurance,

53:435-453.

Gingery S.

W.

(1952) Special Investigation

of

Group Hospital Expense Insurance Experience,

Transactions

о/

the

Society

о/

Actuaries,

IV:44-112.

Goovaerts

М.

J., DeVylder F.

(1980)

Upper

Bounds

оп

Stop-Loss

Premiums

under Constraints

оп

Claim Size Distributions

as Derived

fгош

Representation Theorems

Cor

Distribution Functions,

Scandinavian

Act'Ua-

rial Journal, 141-148.

Greenwood

М.,

Yule G. U.

(1920)

Ап

Inquiry

into

the

Nature

of Frequency Distributions

Representative

of Multiple

Happenings

with

Particular

Reference

to

the

Occurrence of Multiple

Attacks

of

Disease or

Repeated

Accidents,

Joumal

о/

the

Royal

Statistical

Society, LXXXIII:255-279.

Greville

Т.

N.

Е.

(1948) Mortality Tables Analyzed

Ьу

Cause

of

Death,

Record

о/

the

Атепсаn

Institute

о/

Act'Uaries, XXXVIL:283-294. Discussion in XXXVIII (1949):77-79.

Greville

Т.

N.

Е.

(1956) Laws

ofMortality

Which Satisfy

а

Uniform Seniority Principle,

Journal

o/the

Instit'Ute

о/

Act'Uaries, 82:114-122.

Guertin

А.

N.

(1965) Life Insurance Premiums,

Joumal

о/

Risk

and

Insurance,

32:23-50.

Halmstad

D. G.

(1972) Underwriting

the

Catastrophe

Accident Hazard,

Transactions

о/

the

Society

о/

Actua-

ries, XXIV:D408-418.

Ha1mstad D. G.

(1976)

Exact

Nuшегicаl

Procedures in Discrete Risk Theory,

Transactions

о/

the

20th

Inter-

national

Congress

о/

Actuaries,

III:557-562.

Hattendorf

К.

(1868)

ТЬе

Risk with Life Assurance,

Е.

А.

Masius's R'Undscha'U der

Versicherungen

(Review

of

Insurances), Leipzigj

translated

Ьу

Trevor

Sibbett

and

reprinted

in

Li/e

Insurance

Mathe-

matics,

Vol. IV,

Part

2 of

History

о/

Actuarial

Science, edited

Ьу

Steven

Haberman

and

Trevor

Sibbett. London: William Pickering, 1995.

Hickman

J.

С.

(1964)

А

Statistical Approach

to

Premiums

and

Reserves in Multiple Decrement Theory,

Transactions

о/

the

Society

о/

Actuaries,

XVI:1-16.

Ноет

J.

М.

(1988)

ТЬе

Versati1ity of

the

Markov

СЬшп

as

а

Tool in

the

Mathematics

of Life Insurance,

Transactions

о/

the

29rd

Intemational

Congress

о/

А

ctuaries, Record of Proceedings, 171-

202.

Hogg R. V.,

Klugman

S.

А.

(1984)

Loss

Distributions. New York:

John

Wiley

and

Sons.

Hooker

Р.

F., Longley-Cook

L.

Н.

(1953)

Li/e

and

Other

Contingencies. Vol.

1.

Cambridge: Cambridge University Press.

Hooker

Р.

F.,

Longley-Cook

L.

Н.

(1957)

Li/e

and

Other

Contingencies. Vol.

П.

Cambridge: Cambridge University Press.

Horn R. G.

(1971) Life Insurance Earnings

and

the

Release

fгош

Risk

РоНсу

Reserve,

Transactions

о/

the

Society

о/

Actuaries,

ХХIII:З91-З99.

Приложение

6 619

Hoskins

J.

Е.

(1929)

А

New Method of

Computing

Non-Participating Premiums, Transactions

о/

the

Actuarial Society

о/

Aтerica,

ХХХ:140-166.

Hoskins J.

Е.

(1939) Asset Shares

and

Their Relation

to

Nonforfeiture Va1ues, Transactions

o/the

Actuarial

Society

о/

Aтerica,

XL:379-393.

Huffman

Р.

J.

(1978) Asset Share Mathematics, Transactions

о/

the Society

о/

Actuaries,

ХХХ:277-296.

Institute

of

Actuaries,

Faculty

of Actuaries,

(1992), Standard Tables

о/

Mortality: The "80"Series.

Institute

of Actuaries, Staple

Inn

НаН,

High Holborn, London

WCIV7QJ,

U.K.;

Faculty

of Actuaries,

23

St. Andrew Square,

Edinburgh

EH21AQ, U.K.

Jackson R.

Т.

(1959) Some Observations

оп

Ordinary

Dividends, Transactions

о/

the Society

о/

Actuaries,

XI:764-796.

Jenkins

W.

А.

(1943)

An

Analysis

of

Self-Selection, among

Annuitants,

Including Comparisons

with

Selec-

tion

among

Insured

Lives, Transactions

о/

the Actuarial Society

о/

Атемса,

XLIV:227-239.

Jetton

М.

F.

(1988)

Interest

Rate

Scenarios, Transactions

o/the

Society

о/

Actuaries, XL,

Part

1:423-437.

Jones

В.

L.

(1994) Actuarial Calculations Using

а

Markov Model, Transactions

о/

the Society

о/

Actua-

ries, XLVI:227-250.

Jordan

С.

W.

(1952) Li/e Contingencies. 2nd ed., 1967. Schaumburg,

111.:

Society of Actuaries.

Kahn

Р.

М.

(1961) Some

Remarks

оп

а

Recent

Paper

Ьу

Borch,

ASTIN

Bulletin, 1:265-272.

Kahn

Р.

М.

(1962)

Ап

Introduction

to

Collective Risk

Theory

and

Its

Application

to

Stop-Loss Reinsu-

rance,

Transactions

о/

the Society

о/

Actuaries, XIV:400-425.

Keller

J.

В.

(1990) Pricing of Accelerated Benefit Plans, Transactions

о/

the Society

о/

Actuaries,

XLII:259-280.

Kendall

М.,

Stuart

А.

(1977) The Advanced Theory

о/

Statistics. Vol.

1.

4th

ed. New York:

МастШan.

[Имеется

перевод

11

ИЗД.:

Кендалл

М.,

Стьюарт

А.

Теория

распределений.

-

М.:

Наука,

1966.]

Keyfitz N.

(1968) Introduction

to

the

Matheтatics

о/

Population. Reading, Mass.: Addison-Wesley.

Keyfitz

N.

(1977) Applied

Matheтatical

Deтography.

New York:

John

Wiley

and

Sons.

Keyfitz N., Beekman

J.

(1984)

Deтography

through

Probleтs.

New York: Springer.

King G.

(1887) Institute

о/

Actuaries' Textbook.

Part

П.

2nd

ed., 1902. London: Charles

and

Edwin

Layton.

Kischuk R.

К.

(1976) Discussion

of

"Fundamenta1s of Pension Funding", Transactions

о/

the Society

о/

Actuaries, XXVIII:205-21l.

Klein G.

Е.

(1993)

ТЬе

Sensitivity of Cash-Flow Analysis

to

the

Choice

of

Statistical Model for Interest

Rate

Changes, Transactions

о/

the Society

о/

Actuaries, XLV:79-124.

620

Приложение

6

Kornya

Р.

S.

(1983) Distribution

of

Aggregate Claims in

the

Individual Risk

Theory

Model, Transactions

о/

the Society

о/

Actuaries,

ХХХУ:823-836.

Lauer J.

А.

(1967) Apportionable Basis for

Net

Premiums

and

Reserves, Transactions

о/

the Society

о/

Actuaries, XIX:13-23.

Linton

М.

А.

(1919) Analysis

ofthe

Endowment

Premium,

Transactions

o/the

Actuarial Society

о/

Атеп

са,

ХХ:430-439.

London D.

(1988)

Suтvival

Models and Their

Estiтation.

Winsted, Conn.:

АСТЕХ

Publications.

Lukacs

Е.

(1948)

Оп

the

Mathematical

Theory

of

Risk, Journal

о/

the Institute

о/

Actuaries

Students'

Society, 8:20-37.

Lundberg

О.

(1940)

Оп

Random

Processes and Their Application to Sickness and

Accident

Statistics.

Uppsala: Almqvist

and

Wiksells.

Macarchuk

J.

(1969) Some Observations

оп

the

Actuarial Aspects

of

the

Insured Variable

Annuity,

Trans-

actions

о/

the Society

о/

Actuaries, XXI:529-538.

Maclean

J.

В.,

Marshall

Е.

W.

(1937) Distribution

о/

Surplus. Schaumburg, Ill.: Society

of

Actuaries.

Makeham W.

М.

(1874)

Оп

the

Application

of

the

Theory

of

the

Composition

of

Decremental Forces, Journal

о/

the Institute

о/

Actuaries, 18:317-322.

МмвЬаll

А.

W., Olkin

1.

(1967),

А

Multivariate Exponential Distribution, Journal

о/

the

Атепсаn

Statistical Asso-

ciation, 62:30-44.

Marshall

А.

W., Olkin

1.

(1988) Families of Multivariate Distributions,

Joumal

о/

the

Атепсаn

Statistical Associa-

tion, 83:834-841.

McCrory R.

Т.

(1984) Mortality Risk in Life Annuities, Transactions

о/

the Society

01

Actuaries, XXXVI:

309-338.

Menge

W.

О.

(1932) Forces

ofDecrement

in

а

Multiple-Decrement

ТаЫе,

Record

o/the

American

Instit'/J,te

01

Actuaries, XXI:41-46.

Menge W.

О.

(1946) Commissioners Reserve Valuation Method, Record

olthe

Атепсаn

Institute

01

Actua-

пеа,

ХХХУ:258-300.

Mereu J.

А.

(1961) Some Observations

оп

Actuarial Approximations, Transactions

о/

the Society

01

А

ctuaries,

ХПI:87-102.

Mereu J.

А.

(1962)

Annuity

Values Directly from Makeham Constants, Transactions

о/

the Society

о/

А

ct'/J,aries,

XIV:269-286.

Mereu

J.

А.

(1972)

An

AIgorithm for

Computing

Expected Stop-Loss Claims under

а

Group

Life

Contract,

Transactions

о/

the Society

01

Actuaries, XXIV:311-320.

Miller

М.

D.

(1951)

Group

Weekly

Indemnity

Continuation

ТаЫе

Study,

Transactions

о/

the Society

о/

Actuaries,

ПI:31-67.