Геєць О.В., Домрачев В.М., Лондар С.Л. Основи банківської справи та управління кредитними ризиками

Подождите немного. Документ загружается.

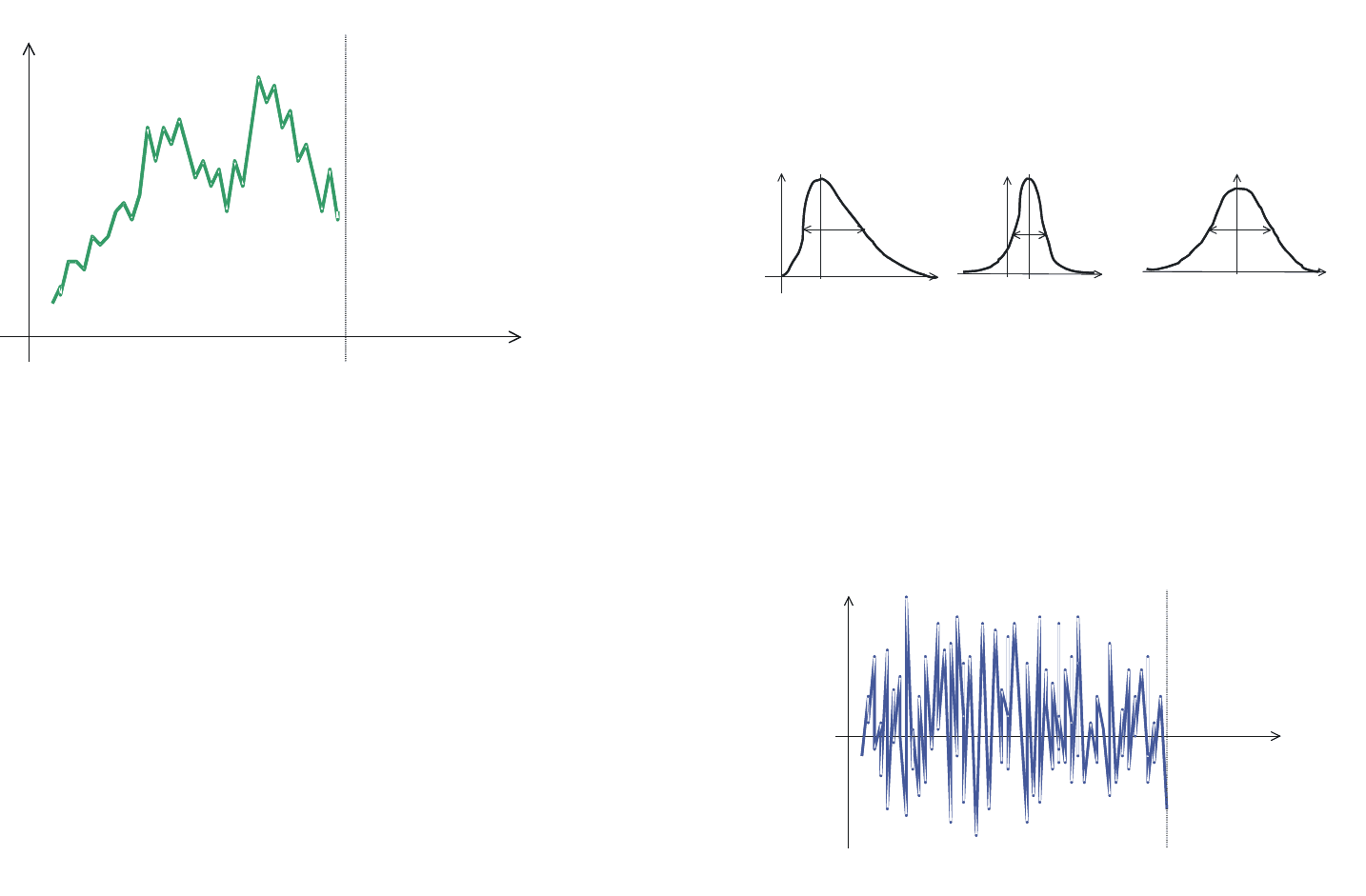

— Íà ñê³ëüêè â³äñîòê³â ö³íà çì³íþºòüñÿ ïðîòÿãîì äîáè.

Íàãàäàºìî äåÿê³ â³äîìîñò³, îòðèìàí³ ó êóðñ³ âèùî¿ ìàòåìàòèêè

ùîäî ìîæëèâèõ ðîçïîä³ë³â âèïàäêîâèõ âåëè÷èí, ÿê³ íåîáõ³äíî äëÿ

îö³íþâàííÿ äîïóñòèìîãî ä³àïàçîíà çì³íè ö³íè.

Ïåðøà êðèâà (à), çàçâè÷àé, õàðàêòåðèçóº âèãëÿä ðîçïîä³ëó êðåäèò-

íîãî ðèçèêó: ³ìîâ³ðí³ñòü âåëèêèõ âòðàò íèçüêà, ³ìîâ³ðí³ñòü íåâåëèêèõ

âòðàò âèñîêà. Äðóãà êðèâà ìຠâèãëÿä ðîçïîä³ëó ðèíêîâîãî ðèçèêó:

³ìîâ³ðí³ñòü âòðàò ð³âíîì³ðíî â³äõèëÿºòüñÿ â³ä ñåðåäíüîãî çíà÷åííÿ m,

òðåòÿ êðèâà â³äïîâ³äຠçíà÷åííþ m=0.

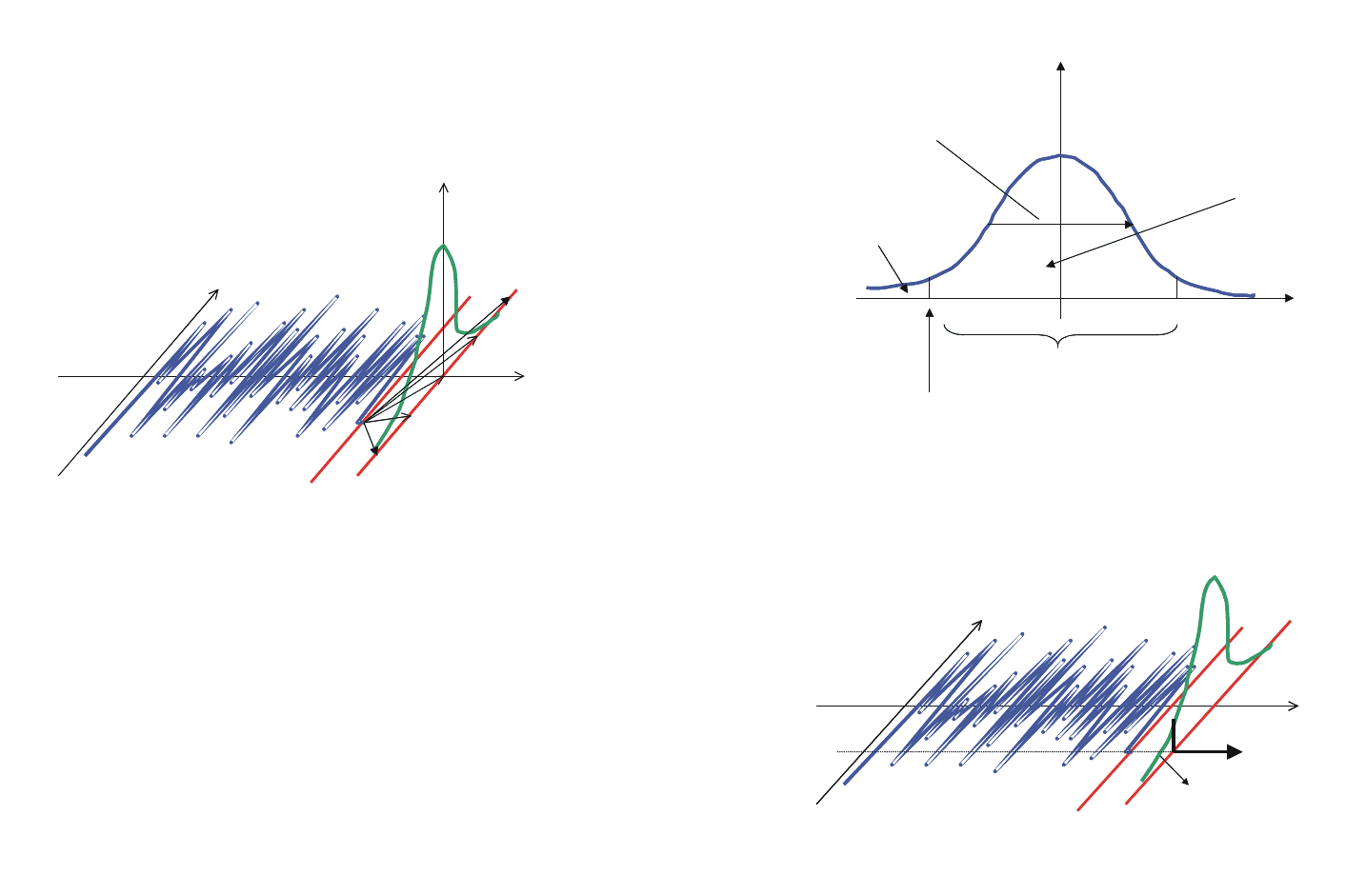

Ðîçãëÿíåìî äèíàì³êó çì³íè çíà÷åííÿ ëîãàðèôìó ïðèáóòêó ó ÷àñ³

ïðè çì³í³ ö³íè.

221

Ç íàâåäåíî¿ ³íôîðìàö³¿ âèïëèâàþòü ïåâí³ âèñíîâêè:

• Âåëè÷èíó (òðåíä) ö³íè âàæêî ïåðåäáà÷èòè.

• Òðàäèö³éí³ ìåòîäè ïðîãíîçóâàííÿ íå ñïðàöüîâóþòü, ¿õ ìîæíà

çàñòîñîâóâàòè ëèøå ó äîâãîñòðîêîâ³é ïåðñïåêòèâ³.

• Ùîá çíàéòè ð³øåííÿ, ìè ïîâèíí³ îö³íèòè Ç̲ÍÓ Ö²ÍÈ.

• Êîëè íåìîæëèâî ïðîãíîçóâàòè òðåíäè, ìîæíà îáìåæèòè ìàé-

áóòí³ âòðàòè íàøèì ð³øåííÿì íà îñíîâ³ ³íôîðìàö³¿ ïðî âåëè÷èíó

çì³íè ö³íè.

5.4.3. Ç̲ÍÀ Ö²ÍÈ

Äëÿ îö³íþâàííÿ ïîòð³áíî¿ äëÿ ïðèéíÿòòÿ ð³øåííÿ âåëè÷èíè

çì³íè ö³íè âèêîðèñòîâóþòü:

• Âèì³ð àáñîëþòíî¿ çì³íè ö³íè ∆Ñ

t

= C

t

—C

t-1

.

• ³äíîñíó çì³íó ö³íè (%) C

t

= ∆C

t

/C

t-1.

• Ëîãàðèôì â³äíîñíî¿ çì³íè ö³íè ln(C

t

/C

t-1

) = ln(C

t

) — ln(C

t-1

).

• Iíòåðïðåòàö³ÿ:

— Ùîäåííà çì³íà ö³íè ó â³äñîòêàõ.

220

Çì³íà ö³íè,

íàïðèêëàä çà çàêîíîì

áðîóí³âñüêîãî ðóõó

äí³

ñüîãîäí³

Âèì³ð ö³íè

(êóðñ âàëþòè,ö³íà àêö³é )

(

)

?

Ùî ñòàíåòüñÿ íàñòóïíîãî äíÿ?

C

t

/C

t-1

: lnN(m, s ) Z

t

= ln(C

t

/C

t-1

) : N(m,

σ

)

f(C

t

/C

t-1

)

f(ln(C

t

/C

t-1

))

C

t

/C

t-11

σ

Z

t

m

σ

⇒

(Z

t

-m) /

0

1

Ñòàíäàðòíèé íîðìàëüíèé

ðîçïîä³ë

ïðîñòèé ó âèêîðèñòàíí³

ZU

t

= : N(0,1)

-

Ëîãàðèôì

⇒

)

Ñòàíäàðòèçàö³ÿ

⇒

à) á)

â)

σ

?

lnZ

t

äí³

t

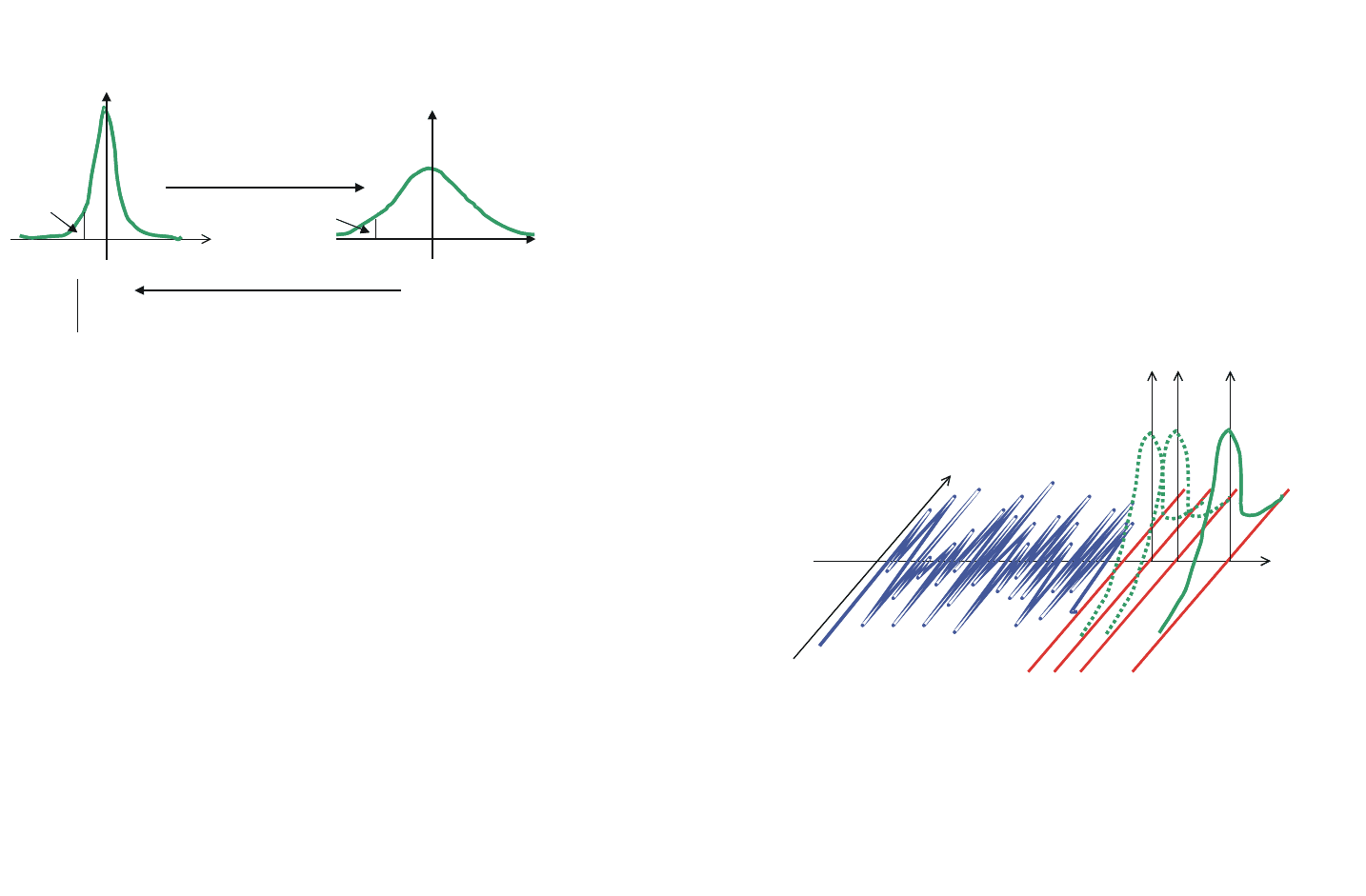

Íà ä³àãðàì³, ïîäàí³é íèæ÷å, ïîäàíî ðîç’ÿñíåííÿ äåÿêèõ âàæëè-

âèõ òåðì³í³â ó ãðàô³÷íîìó âèãëÿä³.

5.4.5. VALUE-AT-RISK

Âèÿâëÿºòüñÿ, ùî ìàòåìàòè÷íî Value-at-risk íå º ÷èìîñü iíøèì,

í³æ âèçíà÷åííÿì êðèòè÷íîãî çíà÷åííÿ ðîçïîä³ëó!

223

Ìîæå öå çâè÷àéíèé õàîñ?!

Çíà÷åííÿ ëîãàðèôìó ïðèáóòêó ó ÷àñ³ ìຠâèãëÿä «ñåéñìîãðàìè»,

ÿêà ïîä³áíà äî ÷àñòîêîëó ç âîëîññÿ! (äîâãå âîëîññÿ âèðîñòàº

ïîâ³ëüí³øå, í³æ êîðîòêå).

«Ñåéñìîãðàìà» oñöèëþº íàâêîëî äåÿêîãî ñåðåäíüîãî çíà÷åííÿ!

Äèñïåðñ³ÿ ñêà÷ê³â âèçíà÷ຠâåëè÷èíó «ñòàíäàðòíîãî â³äõèëåííÿ»,

ÿêå, ÿê ìè âæå çàçíà÷àëè âèùå, çâåòüñÿ «âîëàòèëüí³ñòþ» («volatility»).

5.4.4. вÂÅÍÜ ÇÍÀ×ÈÌÎÑÒ²

Ïðè âèçíà÷åíí³ äîïóñòèìî¿ âåëè÷èíè çì³íè ö³íè ñë³ä îö³íèòè

ð³âåíü çíà÷èìîñò³. Çðîçóì³ëî, ùî äóæå âåëèê³ ñòðèáêè ìàþòü äóæå ìà-

ëåíüêó ³ìîâ³ðí³ñòü, âîíè ïðîñòî ìàëî³ìîâ³ðí³ ÷è íåìîæëèâ³.

Ïðèéìàºìî ð³øåííÿ ïðî òå, ùî áóäåìî ðîçóì³òè ï³ä äóæå ìàëåíü-

êîþ ³ìîâ³ðí³ñòþ: öå òàê³ ñòðèáêè (à çíà÷èòü ³ ð³âåíü âòðàò), ÿê³ ïðàê-

òè÷íî íåìîæëèâ³.

Ìè âèð³øóºìî, ñê³ëüêè êàï³òàëó íàì íåîáõ³äíî, ùîá çàïîá³ãòè

öèì ìîæëèâèì âòðàòàì.

Îáðàíèé íàìè ð³âåíü äóæå ìàëåíüêî¿ ³ìîâ³ðíîñò³ é íàçèâàþòü ð³â-

íåì çíà÷èìîñò³.

222

ln(Z

t

)

äí³

ñüîãîäí³ íàñòóïíîãî

äíÿ

Va R

α

f(lnZ

t

)

ln(Z

t

)

äí³

ñüîãîäí³ íàñòóïíîãî

äíÿ

Ñêà÷êè ç

ìàëîþ³ìîâ³ðí³ñòþ

Z

t

f(Z

t

)

α -çíà÷èìèé

ð³âåíü

1- α äîâ³ð÷èé ³íòåðâàë

(confidence level)

Äîâ³ð÷èé ³íòåðâàë (

Confidence interval)

Êðèòè÷íå çíà÷åííÿ u

α

Ñòàíäàðòíå â³äõèëåííÿ

(âîëàòèëüí³ñòü )

Ñåðåäíå

f(Z

t

)

α

5.4.6. ²ÍÒÅÐÏÐÅÒÀÖ²ß VAR-ÌÅÒÎÄÀ

VaR-ìåòîä äຠð³âåíü âòðàò, ÿêèé ìîæå â³äáóòèñÿ ç ³ìîâ³ðí³ñòþ α.

(Íàïðèêëàä: ç â³äêðèòîþ âàëþòíîþ ïîçèö³ºþ ó âàëþò³ â 1 ãðí. çà îäèí

äåíü ìè ìîæåìî âòðàòèòè á³ëüø í³æ 2,33*σ ãðí. ç ³ìîâ³ðíîñòþ 0.01).

²íòåðïðåòàö³ÿ, ùî VaR-ìåòîä äຠîáñÿã ìàêñèìàëüíèõ çáèòê³â ïðè

çàäàíîìó ð³âí³ çíà÷èìîñò³, º íåïðàâèëüíîþ.

Aëüòåðíàòèâí³ âèçíà÷åííÿ:

— ñüîãîäí³ çáèòêè äîñÿãíóòü çíà÷åííÿ VaR ç ³ìîâ³ðí³ñòþ 0.01;

— ñüîãîäí³ çáèòêè íå äîñÿãíóòü çíà÷åííÿ VaR ç ³ìîâ³ðí³ñòþ 0.99.

5.4.7. AÃÐÅÃÀÖ²ß Ó ×ÀѲ

Ùî ðîáèòè, êîëè ìè íå ö³êàâèìñÿ VaR çà äåíü, à áàæàºìî çíàòè

VaR çà 10 äí³â?

VaR çà 10 äí³â âèçíà÷ຠâòðàòè, ÿê³ ìîæóòü òðàïèòèñü ïðîòÿãîì 10

äí³â ç ³ìîâ³ðí³ñòþ 0.01,

VaR(10) = P

0

σ

(10) u

α

.

225

Ïðè àíàë³ç³ VaR-ìåòîä³â íàéá³ëüø ÷àñòî âèêîðèñòîâóþòü ñòàíäàð-

òèçîâàíèé âèãëÿä:

Îòæå, çíàþ÷è VaR, ìè ìîæåìî ïðèéíÿòè ð³øåííÿ ïðî äîïóñòèìó

äëÿ íàñ çì³íó ö³íè.

×è º VaR-ìoäåëü ñêëàäíîþ?

Äóìêà, ùî VaR-ìîäåëü ñêëàäíà, ïîøèðþºòüñÿ ô³íàíñîâèìè ìàòå-

ìàòèêàìè! Ñïðàâä³ VaR-ìîäåëü º ïîð³âíÿíî ïðîñòîþ.

Ïðîñòà VaR-ìîäåëü äëÿ FX âàëþòíîãî ðèçèêó [äëÿ îäí³º¿ âàëþòè]

ìîæå áóòè çáóäîâàíà òàê:

1) Âèçíà÷àºìî ³ñíóþ÷ó âàëþòíó ïîçèö³þ P

0

= W

0

*k

0

(ïåðâ³ñíó ö³íó

âàëþòè).

2) Ðîçãëÿäàºìî âàëþòíó ïîçèö³þ ïðîòÿãîì îñòàíí³õ n ðîáî÷èõ

äí³â k = [k

1

, k

2

, ..., k

n

].

3) Ðîçðàõîâóºìî [ùîäåííå] ñòàíäàðòíå â³äõèëåííÿ [âîëàòèëü-

í³ñòü] σ.

4) Ïðèïóñêàºìî, íàïðèêëàä, α = 0.01, ç ñòàòèñòè÷íèõ òàáëèöü

ìàºìî u

α

= 2.33.

5) Ðîçðàõîâóºìî VaR = P

0

σ u

α

[Öå ³ º M O Ä E Ë Ü!].

224

N(m,

σ

)

N(0,1

)

VaR

u

α

σ

u

α

f(lnZ

t

)

f[(lnZ

t

)/

σ

]

α

α

ñòàíäàðòèçàö³ÿ

äåñòàíäàðòèçàö³ÿ

)

α

f(lnZ

t

)

ln(Z

t

)

äí³

çàðàç

1 2 ... 10 äí³â

.....

Ðîçðàõóíîê ó ðàç³ (åìï³ðè÷íî¿) êîðåëÿö³¿ (çàëåæíîñò³) ì³æ êóðñàìè

âàëþò:

•Ðîçðàõóíîê ó ðàç³ (åìï³ðè÷íî¿) êîðåëÿö³¿ (çàëåæíîñò³) ì³æ êóð-

ñàìè âàëþò

•Êîëè êîðåëÿö³ÿ r = 1, âèùåíàâåäåíà ôîðìóëà ìຠâèãëÿä

•Êîëè êîðåëÿö³ÿ r = 0, âèùåíàâåäåíà ôîðìóëà ìຠâèãëÿä

Móëüòèâàëþòíèé âàð³àíò.

Ïðèïóñòèìî, ùî áàíê ìຠâ³äêðèòó âàëþòíó ïîçèö³þ â òðüîõ âà-

ëþòàõ:

W

1

, W

2

i W

3

.

³äïîâ³äíî ¿õ êóðñè ìàþòü òàê³ çíà÷åííÿ: K

1t

, K

2t

i K

3t

.

Ïðèïóñòèìî, ùî êîæíà âàëþòà ìຠîêðåìó ïîâåä³íêó ÿê îäíî-

âèì³ðíà:

Oäíîâèì³ðíèé ðîçïîä³ë:

Z

1t

= ln(K

1t

/K

1t-1

) : N(0, σ

1

),

Z

2t

= ln(K

2t

/K

2t-1

) : N(0, σ

2

),

Z

3t

= ln(K

3t

/K

3t-1

) : N(0, σ

3

).

Òðèâèì³ðíèé ðîçïîä³ë: Z = [Z

1

Z

1

Z

1

] : N(0, Σ).

227

Äëÿ ðîçðàõóíêó íàì íåîáõ³äíî ñïîñòåð³ãàòè âàëþòíó ïîçèö³þ ïðî-

òÿãîì äåñÿòèäåííèõ ïåð³îä³â. Ðîçðàõóíîê àíàëîã³÷íèé ðîçðàõóíêó ùî-

äåííîãî VaR. Ìàþ÷è ðîçðàõóíîê σ (1), ëåãêî ðîçðàõóâàòè σ (10):

Äåñÿòèäåííèé VaR ìîæå áóòè ðîçðàõîâàíèé ç ùîäåííîãî VaR:

5.4.8. AÃÐÅÃÀÖ²ß Â ÐÎÇвDz ÂÀËÞÒ

ßê ðîçðàõóâàòè êîíñîë³äîâàíèé VaR, à ñàìå VaR äëÿ USD òà EUR,

óçÿòèõ ðàçîì?

VaR

(USD)

+ VaR

(EUR)

— ó ðàç³ êîëè ïðè ïàä³ííÿ êóðñó USD êóðñ

EUR çðîñòຠ(ïðèïóùåííÿ êîðåëÿö³¿ êóðñ³â âàëþò).

ó ðàç³ êîëè êóðñè USD òà EUR íåçàëåæí³

(â³äñóòí³ñòü êîðåëÿö³¿).

226

.

22

(USD) (EUR)

USD/EUR (USD) (EUR)

VaR + 2 * r * VaR *VaR + VaR

=

22

(USD) (EUR)

(USD) (EUR)

VaR + 2 * VaR *VaR + VaR

2

(USD) (EUR) (USD) (EUR)

= (VaR +VaR ) =VaR +VaR

.

22

(USD) (EUR)

(USD) (EUR)

VaR + 2 * 0 *VaR *VaR +VaR =

.

22

(USD) (EUR)

= VaR +VaR

(10) = 10 (1).σσ

αα

σσ

00

VaR(10)= P (10)u = P (1) 10u = 10VaR(1).

Àêòèâè

Çîáîâ’ÿçàííÿ

’

USD

EUR

Va R

(USD)

Va R

(EUR)

Ïîçàáàëàíñ

—

22

(USD) (EUR)

VaR +VaR

5.4.10. ²Íز ÔÀÊÒÎÐÈ ÐÈÇÈÊÓ

Àíàëîã³÷íî äî ðîçðàõóíêó VaR äëÿ âàëþòíî¿ ïîçèö³¿, ìè ìîæåìî

ðîçðàõóâàòè:

• VaR äëÿ ïðîöåíòíî¿ ñòàâêè,

• VaR äëÿ âàðòîñò³ ö³ííèõ ïàïåð³â,

• VaR äëÿ âàðòîñò³ òîâàð³â òà ïîñëóã òîùî.

Öå ìîæíà çðîáèòè îêðåìî ç ê³íöåâîþ àãðåãàö³ºþ êîæíîãî VaR-

ìåòîäó â êîíñîë³äîâàíèé VaR, ÷è îäíî÷àñíî ÷åðåç ìàòðè÷íó ôîðìóëó.

5.4.11. ÍÀIJÉͲÑÒÜ VAR-ÌÅÒÎÄÓ

Íå ñë³ä äîâ³ðÿòè VaR ïîâí³ñòþ, àäæå öåé ìåòîä òàêîæ ìຠñëàáê³

ì³ñöÿ! Çîêðåìà:

• Çâåñòè âñ³ áàíê³âñüê³ ðèçèêè äî ºäèíîãî íåìîæëèâî.

• Çàì³íà ðåàëüíîãî ðîçïîä³ëó íîðìàëüíèì º äóæå ñèëüíèì ñïðî-

ùåííÿì.

• Äëÿ çàñòîñóâàííÿ VaR-ìåòîäó íåîáõ³äíå äîâãå ñïîñòåðåæåííÿ

ïðîöåñó îñöèëÿö³¿ çì³ííèõ ôàêòîð³â.

Òîìó VaR-ìåòîä ÷àñòî âèêîðèñòîâóþòü îäíî÷àñíî ç³ ñòðåñ-àíà-

ë³çîì, ðîçãëÿäàþ÷è ð³çí³ ìîæëèâ³ ñöåíà𳿠çáóðþþ÷îãî (øîêîâîãî)

âïëèâó áàãàòüîõ çîâí³øí³õ ôàêòîð³â ³ íàøî¿ ðåàêö³¿ íà ö³ çáóðåííÿ.

²ñíóº áàãàòî ìîäèô³êàö³é VaR-ìåòîäó.

Êð³ì òîãî, VaR, íàïðèêëàä, ïîãàíî àíàë³çóº ãàëóçåâ³ ðèçèêè. Íå-

îáõ³äíî çàñòîñîâóâàòè VaR-ìåòîä äî êîæíüî¿ ç ãàëóçåé ³ ïîò³ì êîí-

ñîë³äóâàòè ðåçóëüòàòè ç óðàõóâàííÿì êîðåëÿö³éíî¿ ìàòðèö³. Àëå âçà-

ºìîçâ’ÿçêè ãàëóçåé ó ðèíêîâ³é åêîíîì³ö³ ì³íëèâ³ ³ íå çàâæäè

ï³ääàþòüñÿ îáðàõóíêó.

Áàçåëüñüêèé êîì³òåò äîçâîëÿº áàíêàì ðîçðîáëÿòè ñâî¿ VaR-ìîäåë³.

229

Çàãàëüíà âàðò³ñòü ïîðòôåëÿ ñüîãîäí³ t=0 ñêëàäຠâ íàö³îíàëüí³é

âàëþò³

P

0

= W

1

* K

10

+ W

2

* K

20

+ W

3

* K

30

= P

1

+ P

2

+ P

3

.

Ìîæëèâà çì³íà âàðòîñò³ ñêëàäàº

∆

t

(P

0

) = P

1

* Z

1t

+ P

2

* Z

2t

+ P

3

*Z

3t

= ∆ P

t

.

Êîëè ∆t º ë³í³éíîþ êîìá³íàö³ºþ íîðìàëüíî ðîçïîä³ëåíèõ çì³í-

íèõ Z

1t

, Z

2t

òà Z

3t

, òî âîíà òåæ ìຠíîðìàëüíèé ðîçïîä³ë

P = [P

1

P

2

P

3

] — âåêòîð âàëþòíî¿ ïîçèö³¿, íà ñüîãîäí³ îá÷èñëåíèé

ó íàö³îíàëüí³é âàëþò³, S — êîâàð³àö³éíà ìàòðèöÿ ëîãàðèôì³â â³äíîñ-

íèõ çì³í â³äïîâ³äíèõ êóðñ³â âàëþò (α=0.01),

Ñïðîùåííÿ: êîëè S º ä³àãîíàëüíîþ ìàòðèöåþ (â³äñóòíÿ êîðå-

ëÿö³ÿ ì³æ êóðñàìè âàëþò), âèùåíàâåäåíà ôîðìóëà ìຠâèãëÿä

5.4.9. ÂÈÌÎÃÈ ÄÎ ÊÀϲÒÀËÓ Ç ÁÎÊÓ ÏÎÊÐÈÒÒß

ÂÀËÞÒÍÎÃÎ ÐÈÇÈÊÓ

ʳíöåâîþ ìåòîþ ðîçðàõóíêó ç âèêîðèñòàííÿì VaR-ìåòîäó º âèç-

íà÷åííÿ âèìîã äî êàï³òàëó áàíêó — âåëè÷èíè êàï³òàëó, ÿêà äîïîìîæå

âðÿòóâàòè áàíê ó ðàç³ ðåàë³çàö³¿ î÷³êóâàíèõ çáèòê³â.

Âèìîãè äî êàï³òàëó ìîæóòü âñòàíîâëþâàòèñü êîæíèì áàíêîì îê-

ðåìî, íàïðèêëàä â³äïîâ³äíî äî âèðàçó

Ëåãêî áà÷èòè, ùî âèìîãà äî êàï³òàëó ó 3 ðàçè ïåðåâèùóº òó, ÿêà

ðîçðàõîâàíà çà VaR-ìåòîäîì!

228

.∆

T

t : N(0, (PSP ))

.

⋅

T

VAR = 2.33 (PSP )

−−

=

⋅⋅

∑

60

1i

i1

max(VaR ,k 1 / 60 VaR ),

äå k

=< >

3,4 .

22 2 2 22 2 2 2

11 2 2 33 1 2 3

VAR 2.33 (P P P ) VaR VaR VaR .

=⋅ σ+σ+σ= + +

• ßê³ íåîáõ³äíî íàêëàñòè îáìåæåííÿ íà ôàêòîðè ä³ÿëüíîñò³ áàí-

êó, ùîá ó ðàç³ ðåàë³çàö³¿ íàéã³ðøîãî ñöåíàð³þ áàíê ìàâ ì³í³ìàëüí³

çáèòêè?

Ñòðåñ-òåñò íå äຠâ³äïîâ³ä³ íà ïèòàííÿ ñòîñîâíî ³ìîâ³ðíîñò³ òîãî

÷è ³íøîãî ñöåíàð³ÿ. Ñòðåñ-òåñò ÷àñòî ðîçãëÿäàºòüñÿ â ñóêóïíîñò³ ç

VaR-ìåòîäîì.

Áàíêó íåîáõ³äíî íàâ÷èòèñÿ ïðîãíîçóâàòè ìàéáóòí³é ðîçâèòîê.

Íèæ÷å ìè ðîçãëÿíåìî ïîâåä³íêó áàíêó ó ðàç³ óðàõóâàííÿ ðèçèêó.

Ñòðàòåã³ÿ áàíêó íà ðèíêó ïîëÿãຠó ïðèéíÿòò³ ð³øåíü â³äíîñíî

çì³íè åêçîãåíèõ çì³íèõ ó â³äïîâ³äíîñò³ ç ïåâíèì ñöåíàð³ºì.

Äëÿ öüîãî ìåíåäæåðè áàíêó ïîâèíí³ ïðîàíàë³çóâàòè ð³çí³ ìîæëèâ³

ñöåíà𳿠ðîçâèòêó ìàêðîåêîíîì³÷íîãî îòî÷åííÿ, ïîâåä³íêè êîíêó-

ðåíò³â òà ê볺íò³â áàíêó.

Ðîçãëÿíåìî çì³íí³, ÿê³ âèçíà÷àþòü ñòàí åêîíîì³÷íî¿ ñèñòåìè (ðè-

çèê³â áàíêó):

Ìåíåäæåðàì íåîáõ³äíî ïðîàíàë³çóâàòè ïåðåë³ê ñöåíàð³¿â ðîçâèòêó

ïîä³é íàâêîëî áàíêó:

Ïðè öüîìó êîæíîìó ñöåíàð³þ â³äïîâ³äàþòü ñâî¿ — ³ìîâ³ð-

í³ñòü çä³éñíåííÿ òà — ö³íí³ñòü (êîøòîðèñíà). Çàãàëîì â³äî-

áðàæåííÿ Scån

i

íå º ôóíêö³ºþ (íàâ³òü âèïàäêîâîþ), íàïðèêëàä ó ðàç³

îïö³îí³â öå ñêîð³øå àëãîðèòì.

²ìîâ³ðí³ñòü ìîæå áóòè, íàïðèêëàä, îáðàõîâàíà ÿê ðåçóëüòàò çàñòî-

ñóâàííÿ VaR-ìåòîäó. Âèá³ð áàíêîì êîíêðåòíîãî ô³íàíñîâîãî ³íñòðó-

ìåíòó ïðèçâîäèòü äî ïåâíèõ ô³íàíñîâèõ ðåçóëüòàò³â (äîõîäè/âèòðà-

òè), ÿê³ ðîçãëÿäàþòüñÿ ÿê ö³íí³ñòü.

Ïðèêëàäè ñöåíàð³¿â, ÿê³ â³äïîâ³äàþòü äåÿêèì òèïàì ðèçèê³â, íà-

âåäåíî â òàáëèö³.

Ñöåíàð³é — öå ñèòóàö³ÿ íà ðèíêó, ÿêà ïðåäñòàâëåíà â³äîáðàæåí-

íÿì çà äîïîìîãîþ âåêòîðà. Ñöåíàð³é õàðàêòåðèçóºòüñÿ ìîæëèâîþ ñè-

òóàö³ºþ íà ðèíêó ó ìàéáóòíüîìó, íàïðèêëàä, çðîñòàííÿì ÷è ñïàäîì

ö³í íà òîé ÷è ³íøèé àêòèâ.

ª ïåâí³ ðåêîìåíäàö³¿ ñòîñîâíî âèáîðó ñöåíàð³¿â:

231

5.4.12. ²ÍÑÒÐÓÌÅÍÒÈ ÓÏÐÀÂ˲ÍÍß ÐÈÇÈÊÎÌ

²íñòðóìåíòàìè äëÿ ï³äòðèìêè ð³øåíü â óïðàâë³íí³ ðèçèêîì º

òàê³:

• Value-at-Risk (VaR).

• Capital-at-Risk (CaR).

• Daily Earnings-at-Risk (DEaR).

• Cash Flow-at-Risk (CFaR).

• Stress Testing (ñòðåñ-òåñòè).

• Àíàë³ç ñöåíàð³¿â.

• Êîíñîë³äàö³ÿ (çâåäåííÿ) ì³ðè ðèçèêó.

³äïîâ³äíî äî ñòàíó ðèíêó îáèðàþòüñÿ ð³çí³ ³íñòðóìåíòè.

Áàíêè ÷àñòî âèêîðèñòîâóþòü VaR-ìåòîä ðàçîì ç³ ñòðåñ-àíàë³çîì,

ðîçãëÿäàþ÷è ð³çí³ ìîæëèâ³ ñöåíà𳿠çáóðþþ÷îãî (øîêîâîãî) âïëèâó

áàãàòüîõ çîâí³øí³õ ôàêòîð³â ³ íàøî¿ ðåàêö³¿ íà ö³ çáóðåííÿ.

Ñòðåñ-òåñò — öå ïðîöåñ ñèòóàö³éíîãî ìîäåëþâàííÿ òà ³íñòðóìåíò

óïðàâë³ííÿ ðèçèêîì.

Ñòðåñ-òåñò ïîâèíåí âèÿâèòè òà ³äåíòèô³êóâàòè ïî䳿, ÿê³ ìîæóòü

³ñòîòíî âïëèâàòè íà áàíê ÷è íà îêðåì³ àñïåêòè áàíê³âñüêî¿ ä³ÿëüíîñò³.

Êîæíèé áàíê âèêîðèñòîâóº ñâî¿ ìîäåë³ òà ìåòîäè àíàë³çó ðèçèêó.

Ó ñòðåñ-òåñò³ âàæëèâ³ äâà àñïåêòè: ÿê³ñíèé òà ê³ëüê³ñíèé. Ñöåíà-

ð³é ñòðåñ-òåñòó ïîâèíåí âèçíà÷èòè ä³àïàçîí çì³í ïàðàìåòð³â (³íñòðó-

ìåíò³â, ôàêòîð³â), ÿê³ ìîæóòü òàê âïëèíóòè íà áàíê, ùî óïðàâë³ííÿ

áàíêîì ñòຠíåìîæëèâèì, ÷è âèêëèêàòè íàäâåëèê³ çáèòêè, íåçâàæàþ-

÷è íà òå ùî ö³ ïî䳿 ìàëî³ìîâ³ðí³. ʳëüê³ñíà îö³íêà ïîâèííà âèçíà÷è-

òè äîñòàòí³ñòü êàï³òàëó äëÿ çàáåçïå÷åííÿ ñòàá³ëüíîñò³ áàíêó.

×àñòî ñòðåñ-òåñòè ïîâ’ÿçóþòü ³ç âñòàíîâëåííÿì ë³ì³ò³â íà ïåâí³

ôàêòîðè ä³ÿëüíîñò³ áàíêó.

ðåçóëüòàò³ ñòðåñ-òåñò ïîâèíåí äîïîìîãòè áàíêó â³äïîâ³ñòè íà

òàê³ ïèòàííÿ:

• ßê³ çáèòêè ïîíåñå áàíê ó ðàç³ ïåâíîãî ñöåíàð³þ?

• ßêèì º íàéã³ðøèé ç ìîæëèâèõ ñöåíàð³ºâ ðîçâèòêó ïîä³é?

230

[]

=∈

G

1ni

r r ,...,r , r R.

()

′

=∈

GG

ii

r Scen r , i 1,...,N .

()

′

µ

G

i

r

()

′

G

i

price r

Çàãàëüíà ñõåìà ïðèéíÿòòÿ ð³øåííÿ ç óïðàâë³ííÿ ðèçèêàìè

Àíàë³ç ñöåíàð³¿â ÷àñòî âèêîðèñòîâóºòüñÿ äëÿ ðîçâ’ÿçàííÿ çàäà÷³

óïðàâë³ííÿ ïîðòôåëåì àêòèâ³â áàíêó. Íåõàé çíà÷åííÿ ïîðòôåëÿ àê-

òèâ³â áàíêó (êðåäèòíîãî ïîðòôåëÿ, ïîðòôåëÿ ö³ííèõ ïàïåð³â) â íà-

ñòóïíèé ÷àñ t äîð³âíþº Ó ÿêîñò³ âïëèâàþ÷èõ ÷èííè-

ê³â ìîæóòü ðîçãëÿäàòèñÿ ð³çí³ ôàêòîðè, íàïðèêëàä ñêëàäîâ³ ïîðòôåëÿ

(credit metrics).

Ó ïðîöåñ³ ïðèéíÿòòÿ ð³øåííÿ ðîçãëÿäàþòüñÿ ð³çí³ ñöåíàð³¿

Çàçâè÷àé, ó ÿêîñò³ ìîäåë³ âèêîðèñòîâóºòüñÿ ë³í³éíà àïðîêñèìàö³ÿ

ç óðàõóâàííÿì ÷óòëèâîñò³ äî îêðåìèõ ôàêòîð³â:

Êîëè Ð º íåïåðåðâíîþ ãëàäêîþ ôóíêö³ºþ, ïðîãíîçîâàíå çíà÷åí-

íÿ ïîðòôåëÿ áóäå äîð³âíþâàòè

233

• ó ñöåíàð³ÿõ ïîâèíí³ ðîçãëÿäàòèñÿ åêñòðàîðäèíàëüí³ ïî䳿, ÿê³

ïîâ’ÿçàí³ ç³ çì³íàìè ôàêòîð³â ðèíêó,

• ñöåíà𳿠ïîâèíí³ áóòè ïîãîäæåí³ ç³ ïðîô³ëåì (ñïåöèô³êîþ) ðî-

áîòè áàíêó,

• ñöåíà𳿠ïîâèíí³ âðàõîâóâàòè ð³çí³ òèïè ðèçèê³â.

Ðîçãëÿíåìî ïðèêëàä ìîæëèâîãî ñöåíàð³þ:

• Ñöåíàð³é íåâåëèêî¿ ðåöåñ³¿ (â ìåæàõ íàéáëèæ÷èõ 12 ì³ñÿö³â).

• Íàñòóïí³ çì³íè ìîæëèâî ñòàíóòüñÿ ïðîòÿãîì íàéáëèæ÷èõ øåñ-

òè ì³ñÿö³â òà áóäóòü ñòàá³ëüíî óòðèìóâàòèñü ïðîòÿãîì ùå øåñòè

ì³ñÿö³â, ï³ñëÿ ÷îãî:

• î÷³êóºòüñÿ çðîñòàííÿ ³íôëÿö³¿ íà 1%;

• ïðèáóòêîâ³ñòü ÎÂÄÏ çðîñòå íà 10%;

• ïðèáóòêîâ³ñòü àêö³é âïàäå â ñåðåäíüîìó íà 20%;

• ïðîöåíòíèé ñïðåä çìåíøèòüñÿ íà îäíó òðåòèíó.

Îòæå, çàãàëüíó ñõåìó ïðèéíÿòòÿ ð³øåííÿ ç óïðàâë³ííÿ ðèçèêàìè

ìîæíà ïðåäñòàâèòè òàêèì ÷èíîì:

232

=

GG

P(r ) P(r,t ).

³

=

G

P( r ), 1,...,k.

()( )

−+∆

δ≡

∆

12 n 1 i i n

i

i

P r ,r ,...,r P r ,...,r ,...,r

.

′′

′′

×δ

∑

n

1n 1n 1ii

i-1

P(r ,...,r ) = P(r ...,r )+ (r - r ) .

Òèï ðèçèêó

Âèì³ð ðèçèêó

Ô³íàíñîâèé

VaR

Ìàêðîåêîíîì³÷í³ ðèçèêè

гçí³ ñöåíà𳿠çì³íè ðèíêîâèõ óìîâ

Êðåäèòíèé

VaR

Êðåäèòíèé ðèçèê

гçí³ ñöåíà𳿠çì³íè ôàêòîð³â, ÿê³ âïëè-

âàþòü íà àêòèâí³ îïåðàö³¿ áàíêó

Êîíöåíòðàö³¿

VaR

Ðèçèê êîíöåíòðàö³¿

Äîäàòêîâ³ ñöåíà𳿠çì³íè ôàêòîð³â êîí-

öåíòðàö³¿, íàïðèêëàä, ãàëóçåâ³ ðèçèêè

òà ðèçèêè êðà¿íè

Áàíêðóòñòâà

VaR

Ðèçèê áàíêðóòñòâà

гçí³ ñöåíàð³¿, ÿê³ ìîæóòü ïðèçâåñòè äî

áàíêðóòñòâà

Ó íîðì³ Êðèòè÷íèé

Ñïåöèô³÷íèé

Ñèñòåìàòè÷íèé

³ñòîðè÷í³ çáóðåííÿ (øîêè) ñóá ’ºêòèâí³

÷àñ

’

Çâåäåíèé

Value-at-Risk

Àíàë³ç

ñöåíàð³¿â

Ïðèéíÿòòÿ

ð³øåííÿ

Value-at-Risk

î

ê

ð

å

ì

è

é

â

è

ì

³

ð

ð

è

ç

è

ê

ó

ê

î

í

ñ

î

ë

³

ä

î

â

à

í

è

é

Ñïèñîê ë³òåðàòóðè

1. Ãðþíèíã Õåííè âàí, Áðàòàíîâè÷ Ñîíÿ Áðàéîâè÷ . Àíàëèç áàíêîâñêèõ ðè-

ñêîâ.. — Ì.: Âåñü Ìèð, 2003. — 289 ñ.

2. Áàêñòåð Í. Ïðèíöèïû óïðàâëåíèÿ êðåäèòàìè. — USAID, 1999. —

550 ñ.

3. Îçèóñ Ì., Ïóòíåì Á. Áàíêîâñêîå äåëî è ôèíàíñîâîå óïðàâëåíèå ðèñêà-

ìè. — Èçä.Èí-òà ýêîí. ðàçâèòèÿ Ìèðîâîãî áàíêà, 1992. — 220 ñ.

4. Ôèíàíñîâûé ìåíåäæìåíò. — Ì.: USAID-RPC, 1998. — 289 c.

5. Áëóìôèëä Ê. Êàê âçÿòü êðåäèò â áàíêå. — Ì.: Èíôðà-Ì, 1996. — 144 ñ.

6. Øèëîâ Ñ., Áàéäèí Å., Øèëîâà Å. Êðàòêèé êóðñ êðåäèòíîãî îôèöåðà. —

Ì.: Èçä-âî ÁÅÊ, 1996. — 160 ñ.

7. Bessis Joel. Risk management in banking. England, John Wiley & Sons Ltd. —

1998, 421 p.

8. Annemarie Gaal, Manfred Plank. Credit Risk Models and Credit Derivatives.

Focus on Austria, 4, 1998, Oesterreichische Nationalbank. Ð.46—56.

9. Guidelines on Market Risk. V.5, Stress Testing, 1999, Oesterreichische

Nationalbank, p.62.

10. Guidelines on Market Risk. V.3, Evaluation of Value-at-Risk Models, 1998,

Oesterreichische Nationalbank. Ð.74.

11. Ron S.Dembo, Andrew Freeman. Seen Tomorrow: weighing financial risk in

everyday life. N.Y.: John Wiley& Sons, 1998 — 280 p.

12. Jorion P. Value at risk. N.Y.: McGraw-Hill, 2001. — 323 p.

13. Rockafeller R.T., S.Uryasev. Optimization of conditional Value-at-Risk. The

Journal of Risk// 2000. — vol.2, ¹3. — Ð.21—41.

14. CreditRisk+. A credit risk management framework, London, Credit Suisse

First Boston International, 1997. — 69 p.

15. Risk Management: a practical guide, RiskMetrics Group, J.P.Morgan.

2000. — 140 p.

16. Vector Model. Fitch Ratings. www.fitchratings.com

17. Christian Bluhm, Christoph Wagner. An Introduction to Credit Risk

Modeling, Ludger Overbeck of Deutsche Bank AG. — Frankfurt, Germany, CRC

Press, September 27, 2002, 304 p.

18. Enrico De Giorgi. Reward — Risk Portfolio Selection and Stochastic

Dominance. — Swiss Federal Institute of Technology. Zurich, 2002. — 25 p.

19. Rating methodology: benchmarking quantitative default risk models.—

London, Moody’s Investors Service. — 2000. — 20 p.

20. Global methodology for CDOs of Equity and Credit default Swaps, —

London, 2STANDARD&POOR’S. 004. — 5 p.

235

Çàâäàííÿ âèáîðó îïòèìàëüíîãî ñöåíàð³ÿ ìîæå áóòè ðîçâ’ÿçàíå

ïðîñòèì ïåðåë³êîì âàð³àíò³â ó ïðîñòîð³ Äëÿ

öüîãî ìîæå áóòè âèêîðèñòàíà ñèñòåìà ï³äòðèìêè ïðèéíÿòòÿ ð³øåíü

(íàïðèêëàä, cèñòåìè Crystal Ball, RiskMetrics, Oracle Treasury and Risk

Management — ðîçðîáêà êîðïîðàö³¿ Oracle, PeopleSoft Deal, Cash and

Risk Management — ðîçðîáêà êîðïîðàö³¿ PeopleSoft ³ Corporate Financial

Management, SAP Banking -ðîçðîáêà êîðïîðàö³¿ SAP AG òîùî).

Ñåðåä â³äîìèõ ïðîãðàì óïðàâë³ííÿ ïîðòôåëüíèì ðèçèêîì ñë³ä çà-

çíà÷èòè ñèñòåìó CvaR Expert (www.rhoworks.com), ïðèçíà÷åíó äëÿ

àíàë³çó ðèçèê³â VaR- òà CVaR-ìåòîäàìè. Ñèñòåìà òàêîæ ðîçðàõîâóº

îïòèìàëüíèé ïîðòôåëü, ì³í³ì³çóþ÷èé VaR â³äíîñíî âêàçàíîãî ÷àñî-

âîãî ãîðèçîíòó.

Îòæå, äëÿ ïðèéíÿòòÿ ð³øåííÿ áàíê ïîâèíåí âèêîðèñòîâóâàòè ñó-

÷àñí³ ñèñòåìè àíàë³çó ñèòóàö³é, ùî ñêëàëèñÿ íà áàíê³âñüêîìó ðèíêó,

òà ñèñòåìè ï³äòðèìêè ïðèéíÿòòÿ ð³øåíü.

234

()

′

′

µ× ⊆×

GG

ii

rprice(r)RR.

Íàâ÷àëüíå âèäàííÿ

Ãåºöü Îëåêñàíäð Âàëåð³éîâè÷

Äîìðà÷åâ Âîëîäèìèð Ìèêîëàéîâè÷

Ëîíäàð Ñåðã³é Ëåîí³äîâè÷

ÎÑÍÎÂÈ ÁÀÍʲÂÑÜÊί

ÑÏÐÀÂÈ ÒÀ ÓÏÐÀÂ˲ÍÍß

ÊÐÅÄÈÒÍÈÌÈ ÐÈÇÈÊÀÌÈ

Íàâ÷àëüíèé ïîñ³áíèê

Ðåäàêòîð

Í.Ì. Òðóø

Êîìï’þòåðíà âåðñòêà òà äèçàéí

Í.Ì. ²âàí÷åíêî

Îôîðìëåííÿ îáêëàäèíêè

².Â. Ñîáîëºâî¿

ϳäïèñàíî äî äðóêó 30.06.2004. Ôîðìàò 60×84

1

/

16.

Ïàï³ð îôñåòíèé. Ãàðí³òóðà NewtonCTT.

Óì. äðóê. àðê. 13,95. Îáë.-âèä. àðê. 11,26.

Òèðàæ 2000 ïðèì. Çàì. ¹

Âèäàííÿ íàäðóêîâàíî ç îðèã³íàëà-ìàêåòà, ï³äãîòîâëåíîãî

Âèäàâíèöòâîì ªâðîïåéñüêîãî óí³âåðñèòåòó.

03179, Óêðà¿íà, Êè¿â-179, âóë. Ì. Óøàêîâà, 8à.

Ðåºñòðàö³éíå ñâ³äîöòâî ÄÊ ¹603 â³ä 19.09.2001 ð.

237

Ç̲ÑÒ

Âñòóï . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .3

². ÎÑÍÎÂÈ ÁÀÍʲÂÑÜÊί ÑÏÐÀÂÈ . . . . . . . . . . . . . . . . . . . . . . . . . .5

Ìîäóëü 1. Ñóòí³ñòü ä³ÿëüíîñò³ áàíê³â . . . . . . . . . . . . . . . . . . . . . . . . . . . .6

Ìîäóëü 2. Îðãàí³çàö³ÿ áàíê³â òà ðîçâèòîê ¿õíüî¿ ä³ÿëüíîñò³ . . . . . . . .26

Ìîäóëü 3. Ïðàâèëà ìåíåäæìåíòó áàíê³â . . . . . . . . . . . . . . . . . . . . . . . .56

Ìîäóëü 4. Ïðàêòè÷í³ ñèòóàö³¿ . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .76

²². ÓÏÐÀÂ˲ÍÍß ÊÐÅÄÈÒÍÈÌÈ ÐÈÇÈÊÀÌÈ . . . . . . . . . . . . . . . .79

Ìîäóëü 1. Ñòðàòåã³ÿ êîìåðö³éíîãî áàíêó â êðåäèòóâàíí³ . . . . . . . . . .80

Ìîäóëü 2. Îðãàí³çàö³éíèé òà ãàëóçåâ³ ðèçèêè . . . . . . . . . . . . . . . . . . .121

Ìîäóëü 3. Îö³íêà ³ óïðàâë³ííÿ ô³íàíñîâèìè ðèçèêàìè . . . . . . . . . .142

Ìîäóëü 4. Ïðîöåñ ïðèéíÿòòÿ ð³øåííÿ ïðî íàäàííÿ êðåäèòó . . . . .170

Ìîäóëü 5. Ìåòîäè âèì³ðþâàííÿ ðèçèêó . . . . . . . . . . . . . . . . . . . . . . .214

Ñïèñîê ë³òåðàòóðè . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .235

236