Voit J. The Statistical Mechanics of Financial Markets

Подождите немного. Документ загружается.

262 9. Theory of Stock Exchange Crashes

to the decline of the DAX over the entire four month Russian debt crisis

period in autumn 1998! This was the largest crash of the century.

3. Other important crashes took place in 1929, and at the outbreak of World

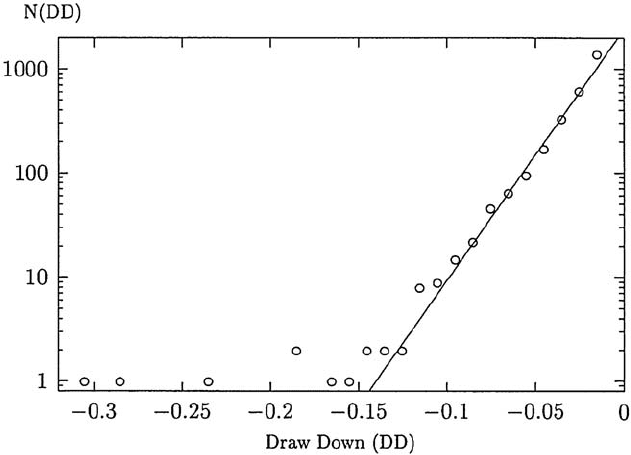

War 1. Figure 9.3 shows the largest weekly drawdowns of the Dow Jones

in this century. The biggest crash was 1987, followed by World War 1,

and the 1929 crash. Notice that on this scale, the Asian and Russian

crisis are completely negligible, and contribute to the leftmost points in

this figure. (Of course, they are no longer negligible when the variations

of the Asian or Moscow stock exchanges are plotted.)

Figure 9.3 uses an exponential distribution to fit the weekly drawdowns

of the Dow Jones index. If this procedure is endorsed, crashes would appear

as outliers: they would not be subject to the same rules as “ordinary” large

drawdowns and be governed by separate mechanisms. Indeed, this point of

view has been defended in the recent research literature by several groups,

and we will discuss it in the present chapter.

Notice, however, that the assumption of an exponential distribution is ar-

bitrary, to some extent, and that statistics is difficult on singular events such

as a major crash. In the framework of stable L´evy distributions, discussed in

Chap. 5, crashes would be part of the statistical analysis, and not be gener-

ated by exceptional mechanisms. This may also apply to power-law statistics

Fig. 9.3. Number of large negative weekly price variations of the Dow Jones in

the 20

th

century. By courtesy of D. Sornette. Reprinted from D. Sornette and A.

Johansen: Eur. Phys. J. B 1, 141 (1998),

c

1998 EDP Sciences

9.2 Examples 263

with nonstable tail exponents. Most likely, in such frameworks, crashes will

not be predictable.

Theories based on exceptional mechanisms underlying crashes therefore

can only be tested on their predictive power.

For all crashes, various economic “causes” have been discussed in the lit-

erature. Hull [10] lists a variety of such possibilities. For the 1987 crash, e.g.,

it was observed that investors moved from stocks to bonds, as the return of

bonds increased to almost 10% in summer 1987. Another cause may have

been the increasing portfolio hedging, using index options and futures, com-

bined with the implementation on computers which generated automatic sell

orders once the index fell below a certain limit. This effect has been mod-

elled explicitly in the computer simulation by Kim and Markowitz [176], cf.

Sect. 8.3.1. Changes in the US tax legislation may have contributed. Rising

inflation and trade deficits weakened the US dollar throughout 1987, and

this may have pushed overseas investors to sell US stocks. Finally, one may

think about imitation and herd behavior. However, it seems to be a common

feature of the major crashes that no single economic factor can be identified

reliably as the triggering event.

Looking at the behavior of the market operators, a crash occurs when

a synchronization of the individual actions takes place. In normal market

activity, the individual buy and sell orders are not strongly correlated, and

rather weak price or index variations result. In a crash, on the other hand,

all operators decide to sell, and there are no compensating buy orders which

would maintain market equilibrium. The market seems to behave collectively.

An increasing synchronization, or correlation, is observed in physics when

a phase transition, especially a critical point, is approached. Examples are the

transition from a paramagnet to a ferromagnet, or from an ordinary metal to

superconductivity. Certainly, there are important differences, in that crashes

take place as a function of time while the critical points in physics usually

are reached by careful fine-tuning of an external control parameter. The idea

of critical points has been generalized to self-organized critical points in open

nonequilibrium systems [79], and the question is if stock exchange crashes

can be considered as critical points, or self-organized critical points, as they

occur in physics.

There are other nonequilibrium situations in nature whose phenomenol-

ogy seems to be similar to market crashes, and where ideas and models about

phase transitions and critical points have been formalized, too: earthquakes

and material failure. We shall discuss them in the following section, before re-

turning to the (admittedly phenomenological) description of stock exchange

crashes.

264 9. Theory of Stock Exchange Crashes

9.3 Earthquakes and Material Failure

Earthquakes and material failure are both characterized by a slow building

up of strains, and a sudden discharge. The idea of these phenomena being

critical points in time has been discussed in the literature for some time.

There is some evidence for this view, although it is still controversial.

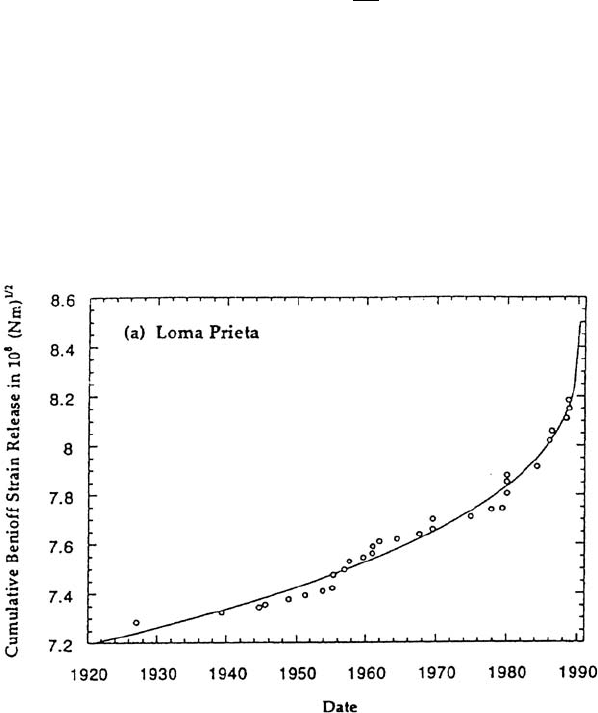

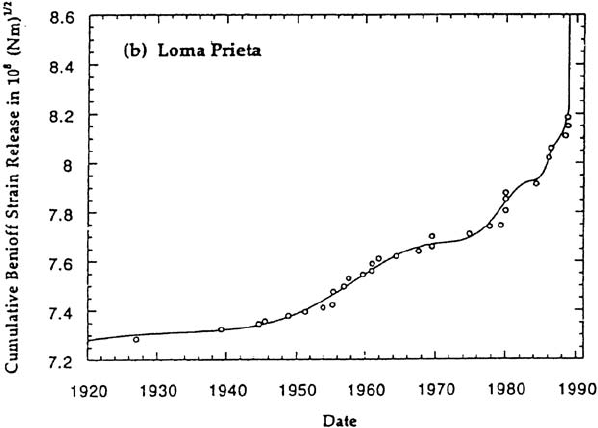

1. Figure 9.4 shows the cumulative Benioff strain prior to the earthquake

occurring on October 18, 1989 near Loma Prieta (northern California).

The cumulative Benioff strain ε(t) is defined as

ε(t)=

N(t)

n=1

E

n

. (9.1)

n is the number of small earthquakes from some starting date t = 0 until

t,andE

n

is the energy liberated in quake n. The appearance of energy

under the square-root can simply be understood in terms of a spring

obeying Hooke’s law: at a given strain ε, the energy stored in the spring

is E =(f/2)ε

2

where f is the spring constant. Fig. 9.4 also shows a fit

of ε(t) to a power law in time-to-failure

ε(t)=A + B|t

f

− t|

µ

,A>0 ,B<0 , 0 <µ<1 . (9.2)

Fig. 9.4. Cumulative Benioff strain before the Loma Prieta earthquake in 1989

(dots) and fit to a power law (solid line). By courtesy of D. Sornette. Reprinted

from D. Sornette and C. G. Sammis: J. Phys. I (France) 5, 607 (1995),

c

1995 EDP

Sciences

9.3 Earthquakes and Material Failure 265

Power laws are the hallmarks of critical points, and the fit apparently

supports the idea of a critical point occurring in time. Notice that ε(t)

stays finite at t

f

but dε(t)/dt →∞as t → t

f

. Notice that the deviations

between the measured points and the power-law fit do not look exactly

random. There are hints of oscillatory behavior.

2. Both the cumulative Benioff strain, and the concentration of Cl

−

ions,

before the earthquake in Kobe (Japan) on January 17, 1995, show a

similar increase [210]. Again, oscillations seem to be superposed on the

smooth power-law variation of (9.2).

3. On a laboratory scale, acoustic emissions recorded before the failure of

materials under increasing load show similar variations.

For earthquakes and material failure, models have been developed which

substantiate power-law behavior, and thus the critical point hypothesis, and

even additional oscillations as the critical point is approached. Their most

important ingredient is their hierarchical structure.

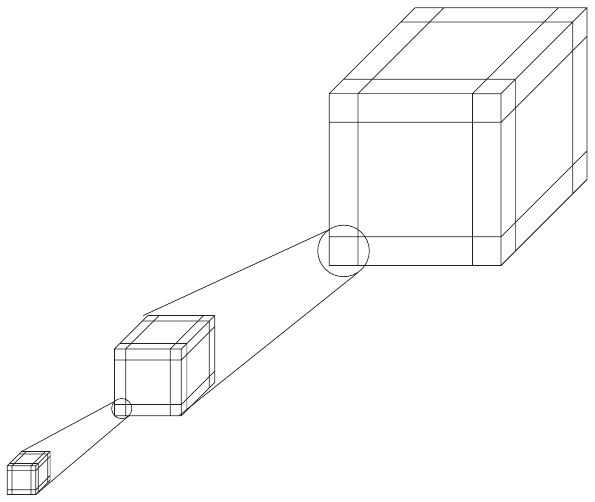

An important model for the description of earthquakes is due to All`egre

et al. [211], and pictured schematically in Fig. 9.5. One starts from a cube

formed by joining eight bars by bolts in the corners of the cube. On the next

level, eight bigger bars form a bigger cube, and eight of the small cubes of

Fig. 9.5. The All`egre model

266 9. Theory of Stock Exchange Crashes

the preceding level are used as bolts to join the bars. This rule is continued

to ever larger scales. The load on the bars and bolts of the biggest cube is

distributed over all levels of the hierarchy. If this load is increased, the weakest

bolt which is on the lowest level may break. Eventually, more than one bolt

will break. This will lead to a redistribution of the load on the next level of

hierarchy, and bolts may fail there, too, either immediately, or once the load

is increased further, and so on. Finally, the highest levels of the hierarchy will

break, resulting in a catastrophic event.

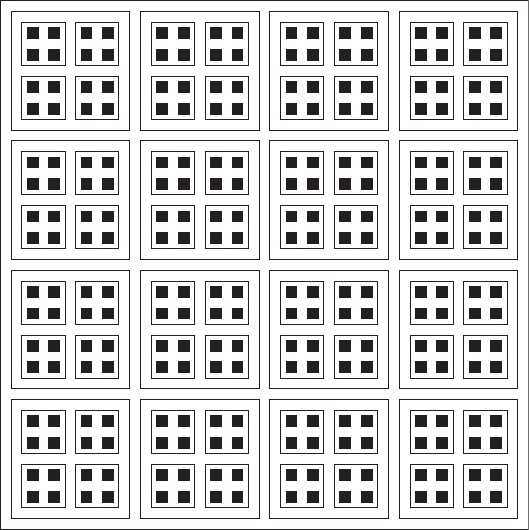

Similar ideas may be invoked for the failure of materials, e.g., composed

of fibers. Figure 9.6 illustrates a hierarchical model for a fiber bundle. The

cross-section of the bundle is shown, and the fibers are oriented perpendicular

to the figure. The mechanism for failure of such a bundle under increasing

load is rather similar to that of the cubic structures of the All`egre model.

Both models show some kind of critical behavior, and power laws, as the

load on the structure is increased. Their criticality is different, however, from

the ordinary critical points of physics in one important aspect. Power laws are

related to scale invariance. Critical points associated with phase transitions

in standard physical systems (magnetism, superconductivity, etc.) exhibit

Fig. 9.6. A hierarchical model of a fiber bundle

9.3 Earthquakes and Material Failure 267

continuous scale invariance. Under a change of scale x → x

= λx,scale

invariance of a system implies that a function f (x) reproduces itself, perhaps

up to some prefactor, i.e.,

f(x)=µf(x

)=µf(λx) , (9.3)

with real λ, µ. This equation is solved by power laws,

f(x)=Cx

α

, (9.4)

which lead to the condition

λ

α

µ =1, i.e., α = −ln µ/ ln λ. (9.5)

Physically, continuous scale invariance comes out because the properties at

the phase transition are determined completely by a diverging correlation

length (the “synchronization” mentioned above), which is much larger than

typical lattice constants, or nearest-neighbor distances. Notice that the un-

derlying structures or Hamiltonians of such systems are not scale invariant,

and that scale invariance only results from the spontaneous collective behav-

ior.

As is obvious from Figs. 9.5 and 9.6, there can be no continuous scale in-

variance in hierarchical models. If they are continued to infinity, there will be

no scale on which the “microscopic” structural details can become negligible

because collective behavior would set in on much longer length scales. Un-

like the models of statistical mechanics, however, hierarchical systems have a

built-in discrete scale invariance. Under a discrete rescaling, x → x

= λ

n

x

with λ

n

= λ

n

0

, they reproduce themselves. For example, we have λ

0

=2

for the structure in Fig. 9.6. An important consequence of discrete scale in-

variance is that critical exponents can become complex [212]. These complex

exponents naturally come out of (9.5) when rewritten as

λ

α

µ =exp(2πin) , i.e., α

n

= −

ln µ

ln λ

+

2πin

ln λ

. (9.6)

A priori, any n is permissible in (9.6). However, for the usual critical phe-

nomena, solutions with n = 0 can be discarded because they would imply

the existence of typical scales in the problem, which contradicts the scale

invariance postulated to be at the origin of the power-law behavior. On a

hierarchical structure, such an objection is not possible, and complex expo-

nents must be allowed. As a consequence, when finite n are kept, a series of

log-periodic oscillations is superposed on the power-law behavior

(t

f

− t)

α

→ (t

f

− t)

α

,

1+

∞

n=1

c

n

cos

2πn

ln λ

ln |t

f

− t|

-

(9.7)

Such oscillations have indeed been observed both in earthquakes and fi-

nancial data. An important practical advantage of the modified scaling law

268 9. Theory of Stock Exchange Crashes

(9.7) is that the determination, and in particular, a possible prediction of

t

f

, i.e., the time to failure or to an earthquake, become much more accurate

if log-periodic oscillations lock in on the data in a fit. The disadvantage is

that the number of fit parameters to be used on a noisy data set increases

significantly, at least from four (pure power law) to seven [including the first

log-periodic oscillation, cf. (9.8) below]. Under these circumstances, there

may be many apparently equally good fits, and their interpretation as well

as the selection of a “best” fit, become a nontrivial problem [213]. Analyzing

the data in Fig. 9.4 a posteriori by fitting them to a pure power law such

as (9.2), one would “predict” the Loma Prieta earthquake to have occurred

at t

f

= 1990.3 ± 4.1. Using the first log-periodic oscillations, the prediction

becomes t

f

= 1989.9 ± 0.8, i.e., is both significantly closer to the actual date

of the earthquake, and carries a much smaller error bar. Figure 9.7 shows a

fit to the same data as in Fig. 9.4 but using log-periodic corrections, showing

the kind of agreement that can be reached. Similar fits can also be done on

Kobe data [210].

This analysis has been done after the actual earthquake occurred. What

about using the method to predict a quake? This has also been attempted

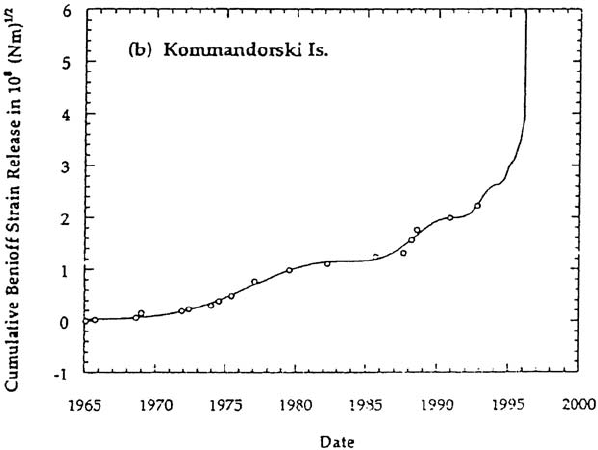

by Sornette and Sammis [213]. Figure 9.8 shows data taken up to 1995 in the

Komandorski islands, a part of the Aleutian islands in Alaska. Also shown

is a fit to (9.7) which produces a (true) prediction of a major earthquake at

Fig. 9.7. Cumulated Benioff strain prior to the Loma Prieta earthquake (dots),

fitted to a power law with log-periodic corrections (solid line). By courtesy of D. Sor-

nette. Reprinted from D. Sornette and C. G. Sammis: J. Phys. I (France) 5, 607

(1995),

c

1995 EDP Sciences

9.3 Earthquakes and Material Failure 269

Fig. 9.8. Cumulated Benioff strain released by earthquakes of magnitude 5.2 or

greater, in the Komandorski segment of the Aleutian islands (dots), and a fit to

a power law with log-periodic corrections (solid line). By courtesy of D. Sornette.

Reprinted from D. Sornette and C. G. Sammis: J. Phys. I (France) 5, 607 (1995),

c

1995 EDP Sciences

t

f

= 1996.3 ± 1.1, i.e., after the submission (January 1995) and publication

(May 1995) of the paper. This prediction is to be compared to one based on

a pure power law, (9.2), giving t

f

= 1998.8 ± 19.7, certainly too inaccurate

to be of any use. Apparently the earthquake did not happen. However, as

communicated to me by D. Sornette, from a considerably refined analysis

method, the authors of the original prediction understand that it was an

artifact of approximations used.

Earthquake predictions have also been attempted using different models,

closer to the standard lines of geophysical research [214]. One model is based

on the hypothesis that an earthquake occurs when a fault has been reloaded

with the stress which was relieved in the most recent earthquake. The time

from one earthquake to the next is the stress drop in the most recent earth-

quake divided by the fault stressing rate. It incorporates directly some of the

physical processes which are believed to be at the origin of earthquakes. This

would convey some degree of predictability to this “recurrence model”. If,

on the other hand, earthquakes occurred completely randomly, their timings

would follow a Poisson distribution.

A test of this recurrence model has been performed in one of the sup-

posedly ideal locations, Parkfield, California [215]. The town of Parkfield is

270 9. Theory of Stock Exchange Crashes

located on the San Andreas fault, one of the most seismically active regions

of the earth. At least five earthquakes of magnitude M

S

= 6 on the Richter

scale [for a definition, cf. (9.16) below], or larger, have occurred in this area

with an average interval of 22 years, the most recent one in 1966. With a pre-

diction of the next earthquake around 1988, in 1986 the US Geological Survey

set up a focused experiment to measure the stress accumulation, capture the

nucleation of the next rupture and watch it propagate. The “problem” today

is that the earthquake never arrived. In fact, the recordings of the experiment

constitute the longest documented period of quiescence at Parkfield. More-

over, using one in-situ data set and one from GPS signals, it was shown that

the stress which was released in the 1966 earthquake had recovered, at the

95% confidence level, by 1987. It continues to increase as a consequence of

continuous fault slippage. When considering a release of stress to the level

just after the 1966 quake, one now is faced with the nightmare idea that the

next major earthquake in the Parkfield region could approach magnitude 7

on the Richter scale [215].

9.4 Stock Exchange Crashes

In the initial phase of research, the basic postulate of all groups trying to

predict crashes on stock exchanges was that they work according to the same

principles as those of earthquakes, or overarching generalizations thereof.

They would view financial crashes as phase transitions in a hierarchical sys-

tem, characterized by discrete scale invariance, and being increasingly loaded

with time. However, there is no evidence for mean-reversion in stock prices

unlike the assumptions of, e.g., the recurrence model for earthquakes. More

recently, research on financial crashes has gained a momentum of its own,

and the relation to models of earthquakes has loosened somewhat [21].

Following the earthquake analogy, a stock price or index rising in time

would build up some stress in the market. It would be released in a singular

failure event, the crash, which would mark a critical point. If this hypothesis

is endorsed, the variation S(t) of a stock price, resp. index, prior to a crash

should obey

S(t)=A + B(t

f

− t)

α

{1+C cos [ω ln(t

f

− t) − φ]} (9.8)

or more complicated generalizations thereof. φ is the phase of the oscillations.

An alternative or complement to fitting this expression is to analyze the

times of occurrence t

n

of pronounced minima in the price variation which are

predicted to follow a geometric progression

t

n+1

− t

n

t

n

− t

n−1

=exp

2π

ω

< 1 . (9.9)

9.4 Stock Exchange Crashes 271

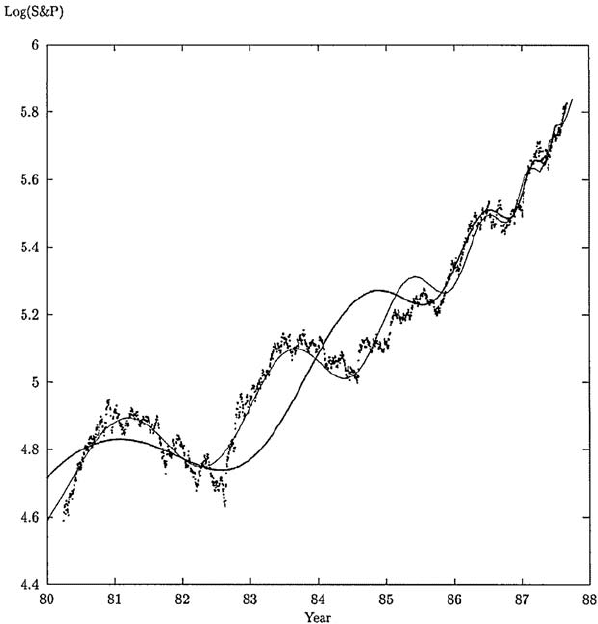

Fig. 9.9. S&P500 index in the seven years preceding the 1987 crash on Wall Street,

and a fit to a power law with log-periodic oscillations. By courtesy of D. Sornette.

Reprinted with permission from Elsevier Science from D. Sornette and A. Johansen:

Physica A 245, 411 (1997)

c

1997 Elsevier Science

Price histories conforming approximately to (9.8) are called log-periodic

power laws. With a positive power-law prefactor B, they correspond to bub-

bles. The understanding then is that a crash is the sudden collapse of a spec-

ulative bubble which has built up over a long time. Imitation and herding

among market participants have pushed market prices of assets significantly

above their fundamental values. The accelerating oscillations in (9.8) then

reflect the competition between the instabilities of the inflating bubble due

to sell orders on the one side, and the synchronization due to herding on the

other side.

Figure 9.9 shows a fit of (9.8) to the S&P500 index in the years preceding

the 1987 crash [216], showing clear signs of log-periodic oscillations. A similar

fit is shown in Fig. 9.10 for the 1929 crash, using the Dow Jones index [216].

While these fits apparently describe the large-scale evolution of the data quite