Sioshansi F.P. Smart Grid: Integrating Renewable, Distributed & Efficient Energy

Подождите немного. Документ загружается.

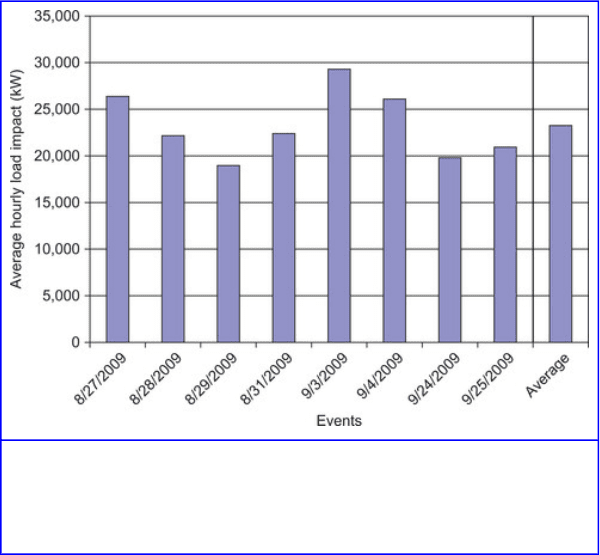

Figure 12.6

Average event-hour CPP load impacts by event—SDG&E.

Source: Braithwait et al. [5]

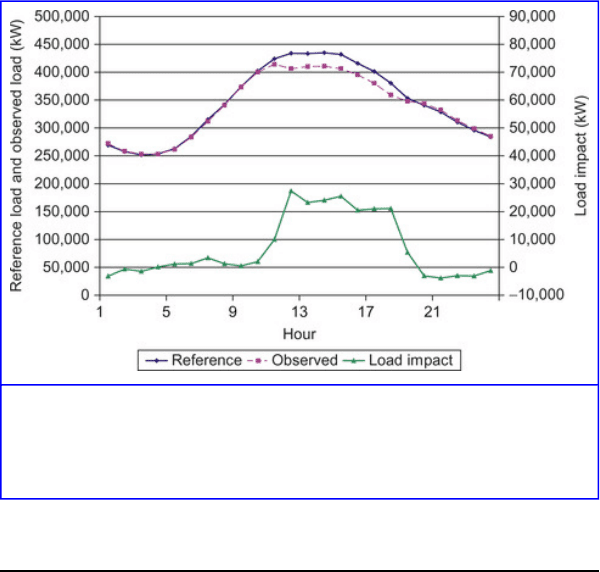

Figure 12.7 illustrates the patterns of the estimated reference

load, observed load, and estimated load impacts (right axis)

for the average event day. Note that unlike the other utilities,

SDG&E's CPP prices apply to seven hours, beginning at 12

noon. Load impacts thus begin an hour earlier than at the

other two utilities. Similarly to PG&E, the reference load

takes on a typical commercial profile due to the large amount

of commercial customer (industry types 5 and 7) load, as

shown in Table 12.6.

611

Figure 12.7

Hourly load impacts for average CPP event day in 2009—SDG&E.

Source: Braithwait et al. [5]

Special Analyses of SDG&E Default CPP

While the voluntary CPP rates had previously required

customers to opt into, or choose to participate in the optional

rate (i.e., take action to enroll), SDG&E's default CPP tariff

provided the first case in which customers were enrolled via

an opt-out process. That is, eligible customers were

automatically enrolled in CPP and were required to take

action to leave the rate and return to the alternative TOU rate.

In addition, under default CPP, customers were given a

capacity reservation option, which allows customers to select

an amount of electric load (in kW) that they wish to protect

from the high CPP price during CPP events, and that they pay

for through a fixed monthly capacity reservation charge,

612

similar to a traditional demand charge. These two factors

provided us with an opportunity to examine two interesting

issues regarding default CPP:

1. Did the load response of customers previously enrolled

in SDG&E's voluntary CPP rate differ from that of newly

defaulted customers?

2. Does consumers' degree of load response appear to be

related to their level of capacity reservation?

We begin by characterizing the differences between the

customer accounts that previously volunteered for CPP and

those that were transitioned to default CPP beginning in 2008.

Table 12.7 and Table 12.8 illustrate the differences in the

average event-hour load impact, industry group makeup, and

price responsiveness of the two groups of customer accounts.

As shown in the last column, the overall percentage price

responsiveness of the previous CPP volunteers was twice that

of the newly defaulted customers (i.e., 10% compared to 5%).

However, the difference appears to be due largely to a change

in industry makeup, particularly a substantially lower share of

load (as shown in the column labeled “% of Max kW”) of

highly responsive customers in the Agriculture, Mining, and

Construction; and Wholesale, Transport, and Other Utilities

industry groups among the newly defaulted customers

compared to the previous volunteers.

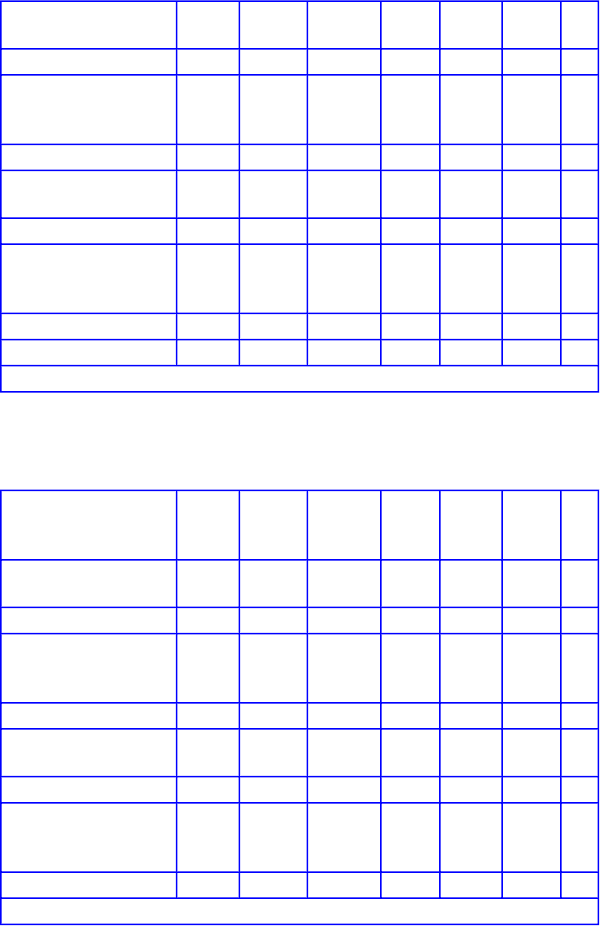

Table 12.7

Characteristics of Customers Previously Enrolled in Voluntary CPP

Industry Type

Num.

of

SAIDs

Sum of

Max

kW

Sum of

Avg.

kWh

% of

Max

kW

Avg.

Size

(kW)

Avg.

Event

LI

%

LI

Source: Braithwait et al. [5].

613

1. Agriculture, Mining

& Construction

4 6,740 2,122 6% 1,685 980 43%

2. Manufacturing 28 8,495 4,723 7% 303 349 6%

3. Wholesale,

Transport, Other

Utilities

107 33,914 13,406 30% 317 3,196 24%

4. Retail stores 25 10,269 7,277 9% 411 163 2%

5. Offices, Hotels,

Health, Services

54 35,822 21,986 32% 663 1,591 6%

6. Schools 56 8,811 3,410 8% 157 0 0%

7. Government,

Entertainment, Other

Services

23 9,274 5,792 8% 403 596 9%

8. Other/Unclassified 0 0 0 n/a n/a 0

TOTAL 297 113,324 58,715 100% 382 6,875 10%

Source: Braithwait et al. [5].

Table 12.8

Characteristics of Customers Newly Defaulted to CPP

Industry Group

Num.

of

SAIDs

Sum of

Max

kW

Sum of

Avg.

kWh

% of

Max

kW

Avg.

Size

(kW)

Avg.

Event

LI

%

LI

1. Agriculture, Mining

& Construction

15 4,947 2,409 1% 330 95 4%

2. Manufacturing 194 84,202 43,487 17% 434 2,624 5%

3. Wholesale,

Transport, Other

Utilities

159 86,294 31,756 17% 543 3,216 10%

4. Retail stores 103 32,375 19,383 7% 314 1,982 7%

5. Offices, Hotels,

Health, Services

427 184,880 112,958 37% 433 6,346 5%

6. Schools 211 45,605 16,826 9% 216 0 0%

7. Government,

Entertainment, Other

Services

167 58,301 28,400 12% 349 2,156 6%

8. Other/Unclassified 7 857 570 0% 122 –35 –6%

Source: Braithwait et al. [5].

614

TOTAL 1,283 497,460 255,789 100% 388 16,384 5%

Source: Braithwait et al. [5].

The two groups of CPP customers also differed in their

decisions regarding capacity reservation level, which may

also have been related to their price responsiveness:

• The previous CPP volunteers accounted for 18.8% of the

default CPP customer accounts in 2009.

• Regarding the capacity reservation level (CRL), 41.5% of

all of the default CPP customer accounts kept the default

level of 50% (meaning half of their expected load was not

exposed to critical prices during event days).

• Of those service accounts that opted to change the

capacity reservation level, 81.7% selected a capacity

reservation level of zero.

• Customers' decision to change their CRL appears to be

related to prior participation in the voluntary CPP rate.

• 80.5% of prior voluntary CPP participants changed their

capacity reservation level (of which 83% selected zero).

• Only 53.3% of the newly defaulted CPP service accounts

changed their capacity reservation level.

Table 12.9 shows observed differences in percentage load

impacts by decisions regarding CRL. The 40% of customers

who kept the default CRL of 50% (first row) produced

average percent load impacts of 3%. In contrast, the nearly

60% of customers (second row) who changed CRL from the

default level of 50% (often to zero, as shown in the third row)

were three times as price responsive as those who kept the

default level (i.e., 9% load impacts compared to 3%).

615

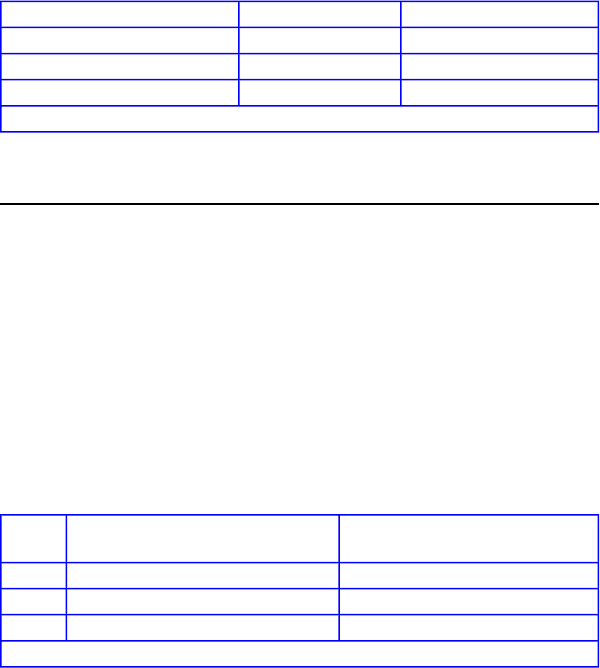

Table 12.9

Differences in Percentage Load Impacts by Subgroups

Customer Type Percent of SAIDs Percent Load Impact

Kept default CRL (50%) 42% 3%

Changed from default CRL 58% 9%

Changed CRL to zero 48% 9%

Source: Braithwait et al. [5].

Concentrations of CPP Load Impacts

The methodology of estimating customer-specific regression

equations and load impacts also provides the capability to

examine the distributions of CPP load impacts across

individual customer accounts, and to determine the

concentration of load impacts among subsets of customers.

Table 12.10 summarizes some of the key indicators of the

concentration of CPP load impacts across the three utilities.

Table 12.10

Concentration of CPP Customer Price Responsiveness

Utility

Share of Customers with LI > 5

kW

Share of %Total LI from Top

5%

PG&E 40% 64%

SCE 59% 55%

SDG&E 35% 74%

Source: Braithwait et al. [5].

The first column in the table reports the percentage of

customers who were estimated to provide load impacts of at

least 5 kW. The 59% value for SCE (compared to 35 and 40%

for SDG&E and PG&E) is consistent with the findings of

greater price responsiveness among SCE's CPP customers.

16

The second column shows the share of load impacts provided

by the top 5% of CPP customers at each utility, where the

616

customers are ranked according to the size of their estimated

load impact. In general, the load impacts are distributed

similarly. Relatively large shares of load impacts are provided

by a relatively few customers. That is, the top 5% of the

customers provide 55–74% of the total program load impacts

across the three utilities. Concentration is greatest at SDG&E,

likely among the former volunteers, while load impacts are

least concentrated at SCE, again reflecting generally broad

price responsiveness.

16

Note that most of SCE's voluntary CPP customers selected the rate

option that has the highest CPP price (in return for a discounted summer

peak demand charge), and have historically included large and flexible

manufacturing and water utility customers who have the ability and

financial incentive to reduce load during CPP event hours.

Perspectives on CPP Participation and Load Impacts

In considering how applicable these CPP load impacts at the

major California utilities are to other utilities and regions,

certain key factors should be kept in mind. First, the results

are based on the actions of those customers who volunteered

for the program or, in the case of SDG&E's default tariff,

elected to stay on the tariff rather than opting out to a TOU

rate. The relatively small overall percentage load reductions

(e.g., 3–5% in 2010) and the concentration of load impacts

among a relatively small fraction of customers are reasonably

consistent with previous price-response findings regarding

RTP for large customers and CPP for residential customers.

17

The next few years will indicate how willing the defaulted

C&I customers at all of the utilities will be to remain on the

CPP tariff in the long term.

617

17

See Goldman et al. [8].

A second factor to keep in mind is that the same pool of

customers from which CPP participants are drawn have the

alternative option of participating in other demand response

programs and receiving financial payments for load

reductions on event days.

18

Thus, if a utility outside of

California were to offer CPP in the absence of alternative DR

programs, it would likely see a different rate of participation

and degree of price responsiveness. However, a number of

utilities operate in the footprint of organized wholesale

markets such as PJM, New York ISO, and ISO New England,

which operate a range of DR programs.

18

In most cases, consumers are not allowed to participate in both CPP and

a DR program, where events are likely to be called on the same days.

Exceptions are some emergency or reliability-based DR programs that

are expected to be called infrequently.

To illustrate how the CPP findings in California depend upon

the alternative DR programs, consider the following

enrollment and load impact information. In 2009,

approximately 2,600 customer accounts participated in CPP at

the three utilities. In 2010, enrollment grew to about 7,100

accounts with the transition to default CPP at PG&E and

SCE.

19

At the same time, aggregator-managed DR programs

in 2010 enrolled more than 5,000 customer accounts, and

SCE and PG&E enrolled 2,500 customer accounts in their

demand-bidding programs (DBP), all from the same pool of

large commercial and industrial customers from which CPP

draws. That is, approximately equal numbers of customers

participated in CPP and in DR programs in 2010.

19

618

See George et al. [9].

The estimated load impacts for the aggregator-managed and

demand-bidding programs in 2010 were 308 MW and 129

MW, respectively. In contrast, total CPP load impacts in 2009

and 2010 were 57 and 73 MW, respectively.

20

An emergency

program, the Base Interruptible Program (BIP), can provide

around 800 MW of load reduction during system

emergencies. With a total system maximum demand for the

three utilities of about 46 GW in 2009, the emergency load

relief from BIP amounts to nearly 2% of the system

maximum demand. The combined price-responsive load

impacts from CPP, DBP, and the aggregator-managed

programs amount to a little more than 1% of the system

maximum demand; CPP load impacts comprise a relatively

small portion of the total.

20

The 2010 load impacts are from George et al. [9].

As a final point of comparison, consider the following

differences in the price responsiveness of the CPP and DR

program customers, as measured by percentage load impacts.

As shown in Table 12.3, the CPP customers at PG&E, SCE,

and SDG&E in 2009 reduced load during CPP events by

3.3%, 18.9%, and 5.6%, respectively. In 2010, after PG&E

and SCE added several thousand newly defaulted customers,

the estimated percentage load impacts at PG&E and SDG&E

remained about the same, while those for SCE dropped to less

than 3%, as the strong price responsiveness of the core

volunteers in 2009 was diluted by less responsive newly

defaulted customers.

In contrast to those relatively small percentage load impacts

for CPP customers, the comparable values for the

619

aggregator-managed programs were much higher, ranging

from 20 to 30%.

21

There are two likely reasons for the larger

relative load impacts for the DR programs compared to CPP.

First, customers receive a combination of capacity credits for

promised load reductions, regardless of whether events are

called, and of energy payments for measured load reductions

during events. The capacity credits likely attract customers

who are willing to commit to reduce load, while penalty

provisions for not meeting commitments, as well as energy

payments for load reductions, provide strong incentives to

perform during events. Second, the third-party aggregators

have an incentive to work with enrolled customers to ensure

that in aggregate they produce the contractual load reductions

agreed upon with the utilities. Our understanding is that in

some cases aggregators assist customers with equipment or

procedures to automate load reductions when events are

called. To the extent that participants in the aggregator

programs are inherently more price responsive than

non-participants, then that portion of the population is

removed from the remaining population from which CPP

draws, thus leaving generally less responsive customers to

participate in CPP.

21

Percentage load impacts for most DBP customers were in the range of

those for CPP (see Braithwait et al. [6]).

Looking Forward

CPP in California

As noted above, enrollment of large C&I customers in CPP in

California increased substantially in 2010, as the utilities

transitioned to default CPP rates. Specifically, SCE moved

620