Simon Benninga. Financial Modelling 3-rd edition

Подождите немного. Документ загружается.

568 Chapter 20

−−

−

↑

[([]) ([])]SN d X X e N d X

rT

12Call Call Call

Short call

−− + −

[]

()

−

↑

SN d X X e N d X

rT

([ ])

12Put Put Put

Long put

=− + −

↑

SNd X N d X(([ ]) ( [ ]))

11Call Put

Short stock possition

Call Call Put P

++−

−

eXNdX XNdX

rT

[([]) ([

22uut

Long bond position

])]

↑

We rewrite this expression in terms of Greeks:

−+−

↑

SNd X N d X[([ ]) ( [ ])]

11Call Put

Short stock position

−+−

−

↑

eXNdX XNdX

rT

[([]) ([])]

Call Call Put Put

Long bond po

22

ssition

Call Call Put Put

=− − +

−

SX Xe

r

[()()]ΔΔ

TT

X NdX X N dX[([]) ([])]

Call Call Put Put22

+−

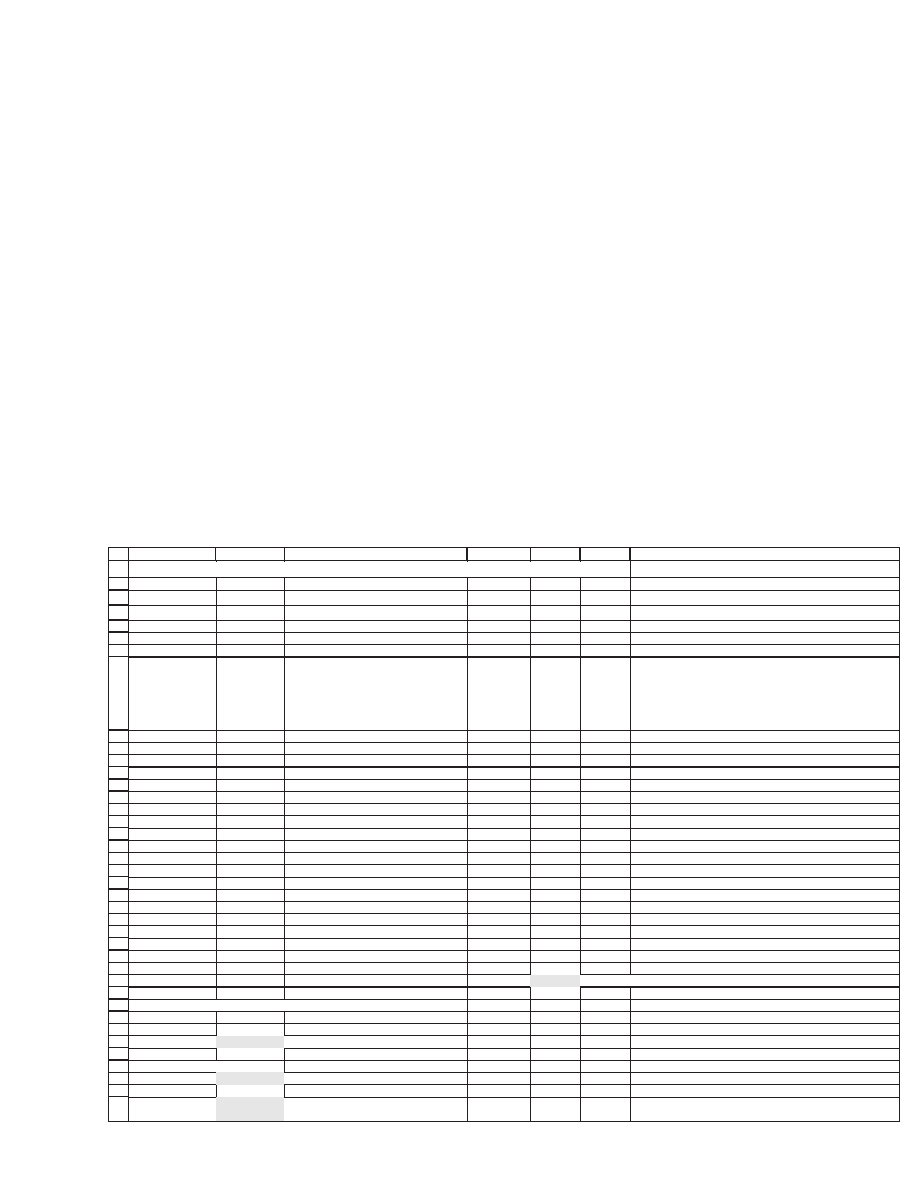

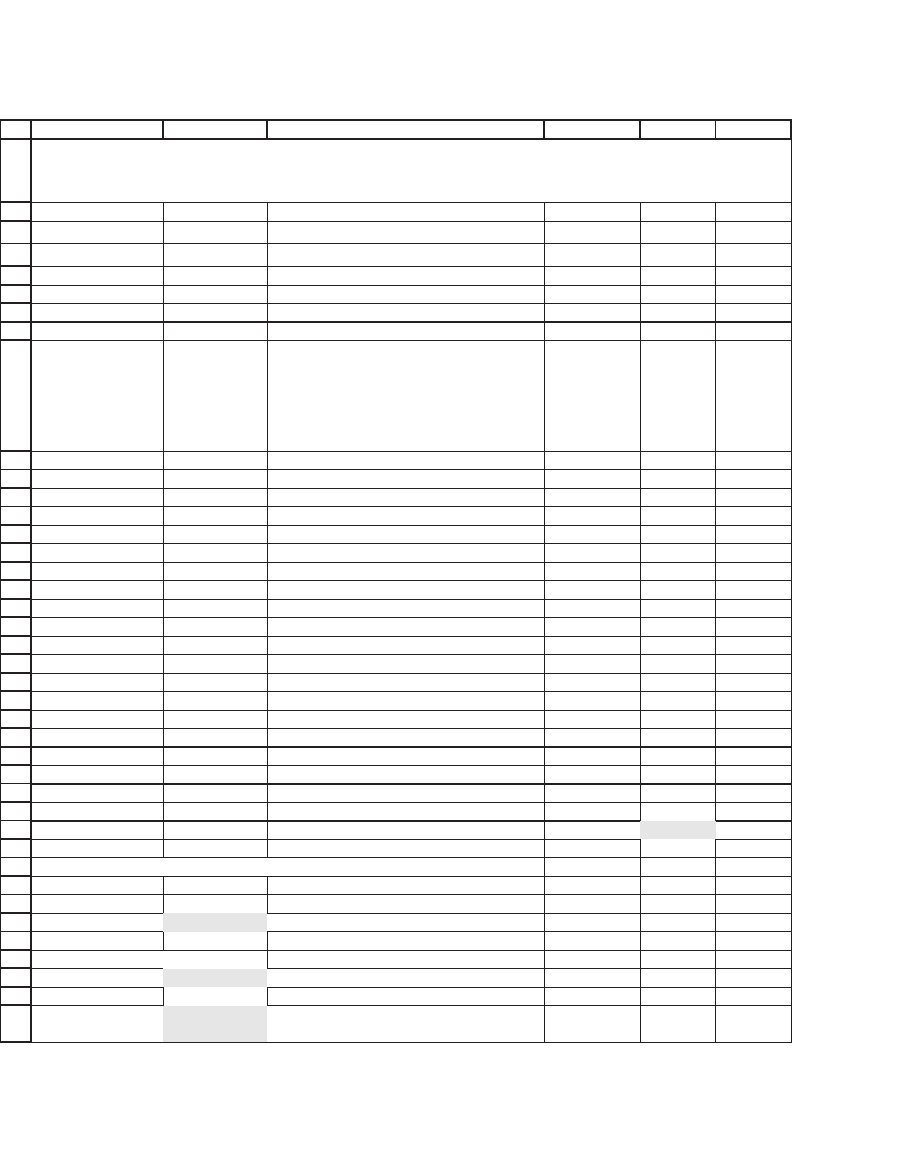

Here’s a run of a simulated position over the course of a year. In this

simulation the position is updated every Δt = 0.05; assuming 250 trading

days in a year, this is approximately every 12 days.

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

37

38

39

FEDCBA G

5S 5.00

X

Call

70.00

X

Put

49.04

4r.00%

Sigma 40%

Time until

expiration

Stock price

Stock =-

B9*(calldelta(B9,$B$3,A9,$B$5,$B$6)-

putdelta(B9,$B$4,A9,$B$5,$B$6)) Bond

Porfolio

value

Portfolio

cash flow

1.00 55.00 -36.28 36.28 0.00 0.00

0.95 53.57 -34.75 35.77 1.02 0.00 <-- =(C9*B10/B9-C10)-(D10-D9*EXP($B$5*(A9-A10)))

0.90 52.39 -33.49 35.34 1.85 0.00 <-- =(C10*B11/B10-C11)-(D11-D10*EXP($B$5*(A10-A11)))

0.85 48.07 -30.81 35.49 4.68 0.00 <-- =(C11*B12/B11-C12)-(D12-D11*EXP($B$5*(A11-A12)))

0.80 49.46 -30.98 34.84 3.86 0.00

0.75 50.33 -30.86 34.25 3.39 0.00

0.70 50.54 -30.40 33.73 3.33 0.00

0.65 58.10 -34.27 33.12 -1.15 0.00

0.60 55.71 -31.57 31.90 0.32 0.00

0.55 67.93 -43.58 37.04 -6.54 0.00

0.50 66.69 -40.90 35.23 -5.67 0.00

0.45 73.10 -50.24 40.71 -9.53 0.00

0.40 78.79 -60.20 46.84 -13.36 0.00

0.35 72.21 -47.38 39.15 -8.23 0.00

0.30 77.20 -57.29 45.86 -11.43 0.00

0.25 73.30 -48.65 40.20 -8.45 0.00

0.20 85.78 -77.08 60.44 -16.65 0.00

0.15 80.97 -69.22 57.01 -12.20 0.00

0.10 82.00 -74.69 61.72 -12.97 0.00

0.05 99.59 -99.59 70.72 -28.87 0.00 <-- =(C27*B28/B27-C28)-(D28-D27*EXP($B$5*(A27-A28)))

0.00 89.31 -18.44 <-- =C28*B29/B28+D28*EXP($B$5*(A28-A29))

Check: Collar payoff to client at time 0

Short call payoff -19.31 <-- =-MAX(B29-B3,0)

Long put payoff 0.00 <-- =MAX(B4-B29,0)

Total -19.31 <-- =SUM(B32:B33)

Payoff to bank from delta hedge

-18.44 <-- =E29

Terminal cash

flow to bank

0.86 <-- =-B34+B37

DELTA HEDGING A COLLAR

569 Option Greeks

Here’s what happens in this spreadsheet:

•

The initial (row 9) stock and bond positions are determined by the

Black-Scholes formula. The stock position is −S[Δ

Call

(X

Call

) − Δ

Put

(X

Put

)],

and the bond position is e

−rT

[X

Call

N(d

2

[X

Call

]) + X

Put

N(−d

2

[X

Put

])]. Not

surprisingly, the net value of this portfolio is zero—this is the way we

determined the collar X

Call

and X

Put

.

•

In each of the subsequent rows, the stock position is determined by the

Black-Scholes formula, and the bond position is determined so that the

net cash fl ow of the position is zero:

Bonds Stock_position

Stock_price

Stock_price

Stock_p=∗−

−

−

t

t

t

1

1

oosition

Determined by

Black-Scholes

Cash flow into

t

↑

↑

stocks

Bond_position exp

+∗∗

−t

rt

1

()Δ

↑↑

−Value today of 1 bond positiont

•

At the terminal date (row 29), the portfolio is liquidated:

Stock_position Stock_position

Stock_price

Terminal Previous

T

=∗

eerminal

Previous

Previous

Stock_price

Bond_position exp+∗∗(rtΔ ))

•

At the terminal date, the purchaser of the collar collects on his short

position in the call and his long position in the put (cell B34). The bank

collects its position value (cell E29 or B37). The bank’s net cash fl ow on

termination is the difference between these two (cell B39). To under-

stand this last cell, consider that the client’s collar payoff is the bank’s

income: In the particular example shown here, the client has a negative

cash fl ow of $19.31, which he pays to the bank. The bank’s position shows

a negative payoff of $18.44, so that the bank makes $0.86 on the

collar.

2

Here’s another run of this same simulation. This time the client’s put

pays off and the bank has to cover the loss.

2. Of course, if the hedge were adjusted continuously, it would be perfect. This is the

essence of the proof of the Black-Scholes theorem (for details, see Jarrow and Rudd,

Option Pricing, Irwin, 1983, Chapter 8).

570 Chapter 20

571 Option Greeks

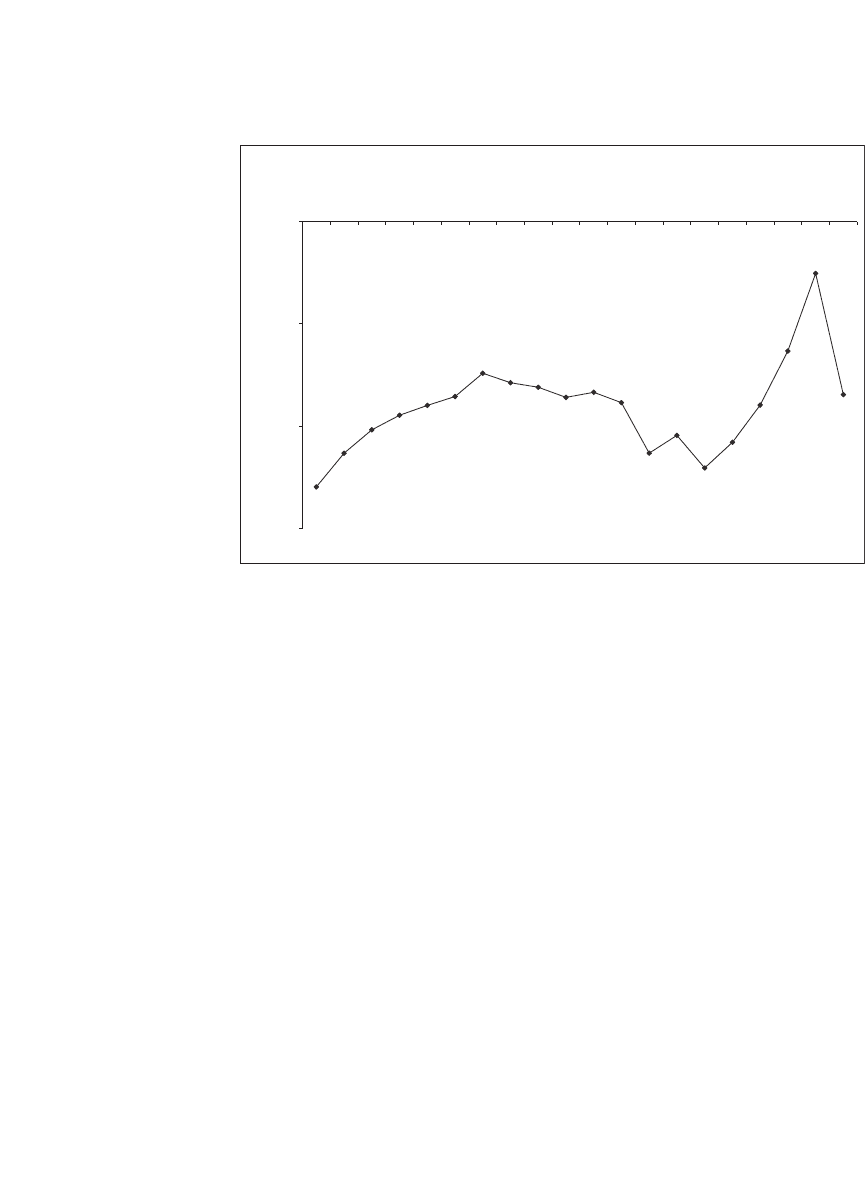

20.4.3 Making the Collar Gamma Neutral

As the option gets closer to expiration, the hedge position can become

extremely sensitive to small changes in the stock price, meaning that the

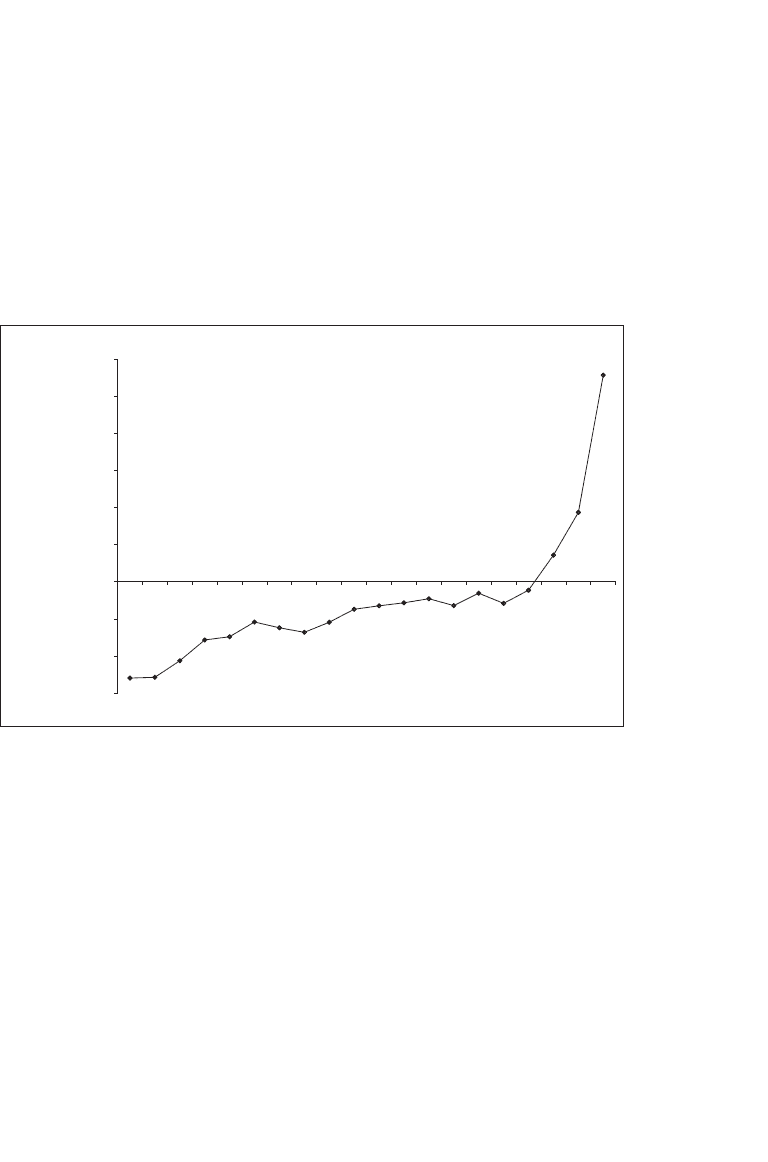

gamma of the collar can grow enormously. In the following example, the

gamma explodes toward the end of the hedging period:

Exploding Collar Gamma

(absolute value)

0.001

0.010

0.100

1.000

10.000

100.000

1,000.000

10,000.000

100,000.000

1,000,000.000

1.00

0.95

0.90

0.85

0.80

0.75

0.70

0.65

0.60

0.55

0.50

0.45

0.40

0.35

0.30

0.25

0.20

0.15

0.10

0.05

Time to expiration

This need not always be the case—here’s another simulation of the price

path without an exploding gamma:

572 Chapter 20

There are two solutions to this problem:

•

We could (should?) increase our hedging frequency as we get closer to

the collar expiration date.

•

We could (should?) change our hedge strategy in order to temper the

hedge gamma, as we get closer to the option maturity.

We explore both solutions in the following subsections.

20.4.4 Increasing the Hedge Frequency

The main problem of the hedge seems to be for the last 10–15 percent

of the expiration period. Since the initial options have maturity T = 1,

we have to be very careful during the one or two months of the hedging

period. Delta hedging the position more often may work, though it is

easy to come up with counterexamples:

Moderate Collar Gamma

(absolute value)

0.001

0.010

0.100

1.000

1.00

0.95

0.90

0.85

0.80

0.75

0.70

0.65

0.60

0.55

0.50

0.45

0.40

0.35

0.30

0.25

0.20

0.15

0.10

0.05

Time to expiration

573 Option Greeks

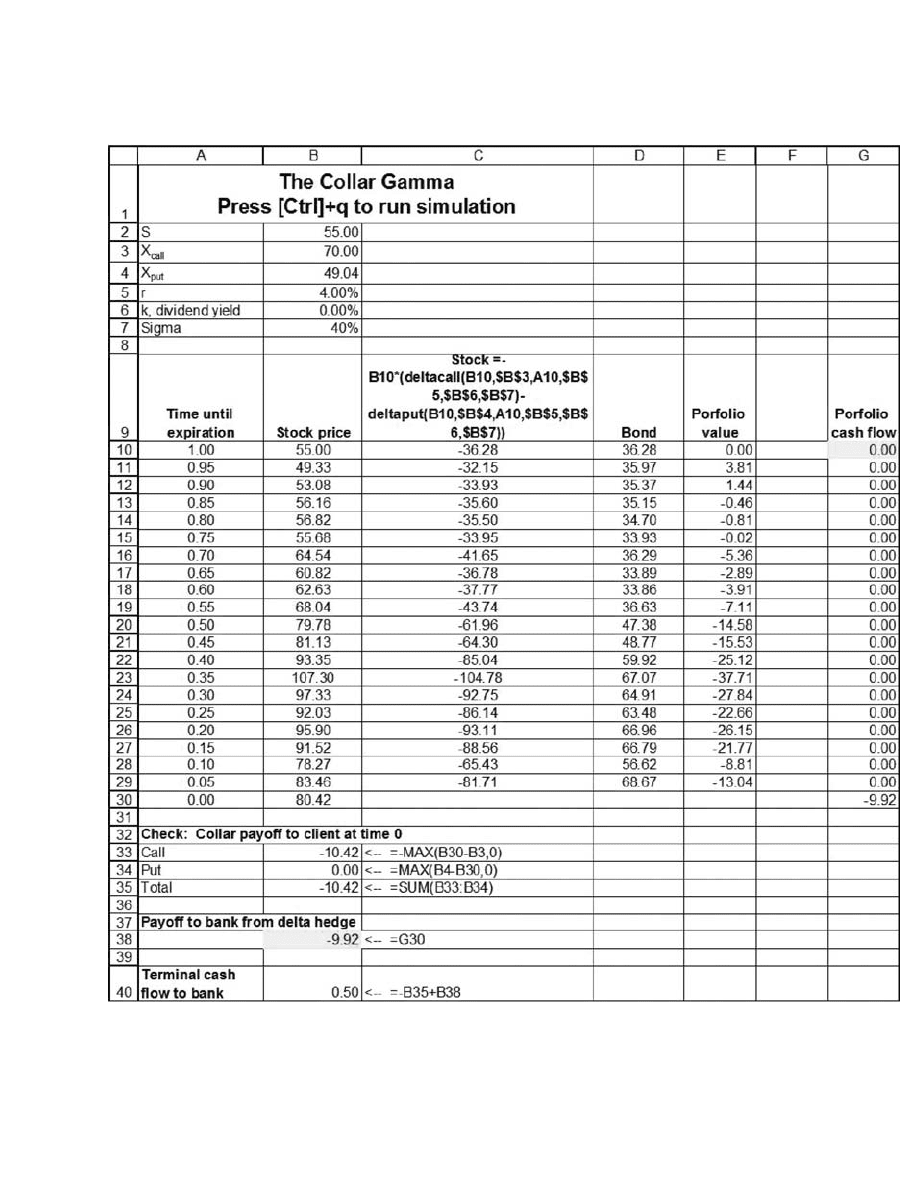

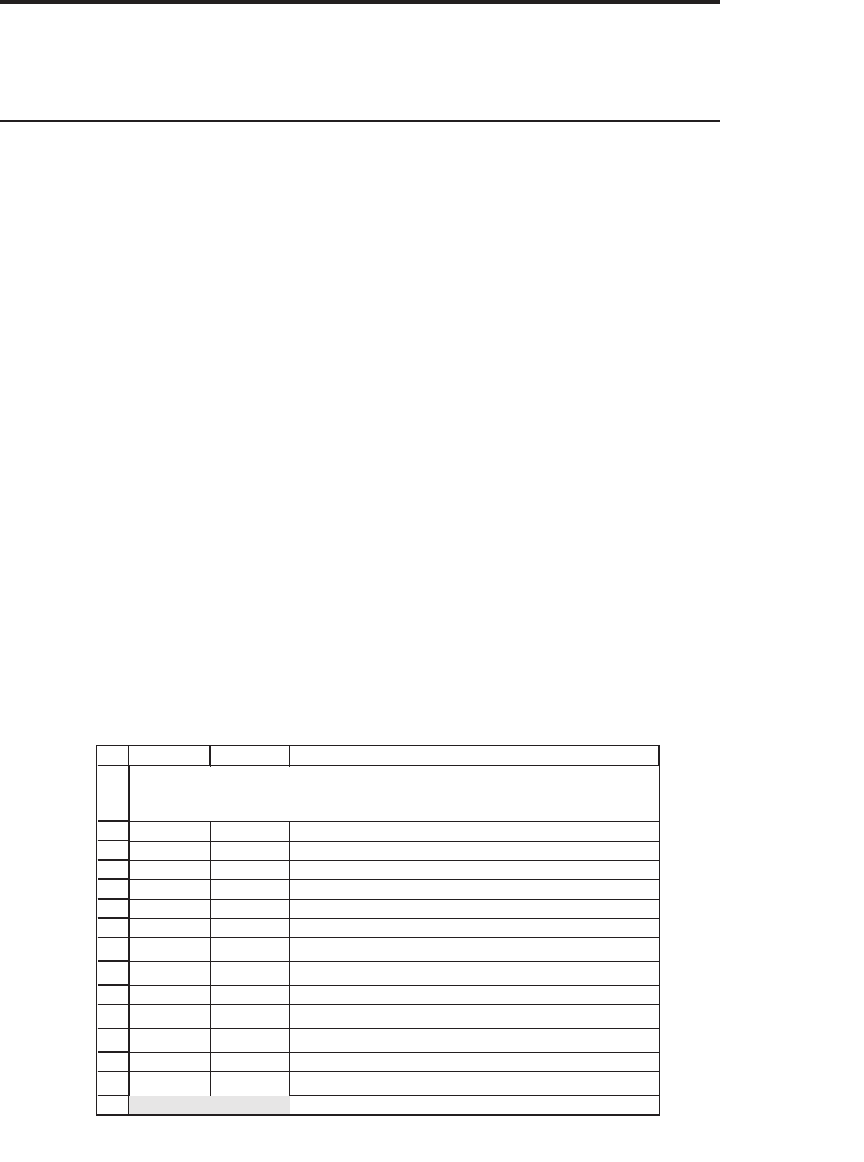

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

37

38

39

40

EDCBA

F

S 55.00

X

Call

70.00

X

Put

49.04

r 4.00%

k, dividend yield 2.00%

Sigma 40%

Time until

expiration

Stock price

Stock =-

B10*(deltacall(B10,$B$3,A10,$B$5,$B$

6,$B$7)-

deltaput(B10,$B$4,A10,$B$5,$B$6,$B$

7)) Bond

Porfolio

value

Portfolio

cash flow

0.20 55.00 -18.29 18.29 0.00 0.00

0.19 53.62 -18.43 18.90 0.47 0.00

0.18 54.12 -17.55 17.85 0.30 0.00

0.17 54.65 -16.60 16.74 0.14 0.00

0.16 50.15 -21.44 22.96 1.51 0.00

0.15 51.18 -19.49 20.58 1.08 0.00

0.14 50.05 -21.20 22.72 1.52 0.00

0.13 51.20 -18.76 19.80 1.04 0.00

0.12 50.71 -19.42 20.65 1.23 0.00

0.11 48.61 -24.11 26.15 2.04 0.00

0.10 50.83 -18.55 19.49 0.95 0.00

0.09 47.75 -26.65 28.73 2.08 0.00

0.08 44.94 -34.04 37.70 3.66 0.00

0.07 45.97 -32.46 35.36 2.90 0.00

0.06 41.06 -39.37 45.75 6.38 0.00

0.05 40.60 -39.75 46.59 6.84 0.00

0.04 38.35 -38.27 47.33 9.06 0.00

0.03 36.60 -36.58 47.40 10.82 0.00

0.02 36.28 -36.27 47.43 11.16 0.00

0.01

35.73

-35.72 47.45 11.73 0.00

0.00 36.36 11.11 <-- =C29*

B

Check: Collar payoff to client at time 0

Short call payoff 0.00 <-- =-MAX(B30-B3,0)

Long put payoff 12.68 <-- =MAX(B4-B30,0)

Total 12.68 <-- =SUM(B33:B34)

Payoff to bank from delta hedge

11.11 <-- =E30

Terminal cash

flow to bank

-1.56 <-- =-B35+B38

MODERATING THE COLLAR GAMMA

This example starts with T = 0.20 and hedges every Delta_t = 0.01

Repeated simulation of this hedge shows that it works quite well.

574 Chapter 20

20.4.5 Making the Hedge Gamma Neutral

Another strategy is to add another asset to the hedge position, in an

effort to neutralize the Gamma. In this example we have added an out-

of-the-money put to the position to neutralize the large call gamma:

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

EDCBA

Call Put Another put

S 48.00 48.00 48.00

X 70.00 49.04 35.00

r 5.00% 5.00% 5.00%

k, dividend yiel 0.00% 0.00% 0.00%

T 0.0200 0.0200 0.0200

Sigma 40.00% 40.00% 40.00%

Option prices 0.00 1.66 0.00

Delta 0.0000 -0.6304 0.0000 <-- =deltaput(D3,D4,D7,D5,D6,D8)

Gamma 494,472,087 0 1,118,872 <-- =gamma(D3,D4,D7,D5,D6,D8)

Bank position: short call with X = 70.00 + long put with X = 49.04 + put with X = 35.00

Call, X = 70.00 -1

Put, X = 49.04 1

Put, X = 35.00 441.938

Position delta -0.6304 <-- {=SUMPRODUCT(TRANSPOSE(B17:B19),B12:D12)}

Position gamma 0.1553 <-- {=SUMPRODUCT(TRANSPOSE(B17:B19),B13:D13)}

Position cost

Without second put 1.6604 <-- =B17*B10+B18*C10

With second put 1.6604 <-- =B17*B10+B18*C10+B19*D10

Traditional collar delta -0.6304 <-- =-B12+C12

COLLAR HEDGE: DELTA AND GAMMA

in this example we costlessly neutralize a large call gamma

This strategy can be carried out at very little cost, since the put in

question is almost costless (cell D10). Of course, it may not always be

possible to neutralize the gamma costlessly. In this case we would have

to make some compromises.

20.5 Summary

In this chapter we have explored the sensitivities of the option-pricing

formula to its various parameters. Using these Greeks, we have delved

into the intricacies of delta hedging, a useful technique for replicating an

575 Option Greeks

option position with a combination of stocks and bonds. The interested

reader should know that there is much more that can be said about this

topic. Good starting places for further reading are Hull (2006) and Taleb

(1997). An extensive collection of option-pricing formulas including

Greeks can be found in Haug (2006).

Exercises

1. Produce a graph similar to Figure 20.2 for puts.

2. Figure 20.3 shows the call theta as a function of time to maturity. Produce a similar

graph for puts.

3. Although θ is generally negative, there are cases (typically of high interest rates)

where it can be positive:

•

An in-the-money put with a high interest rate

•

An in-the-money call on a currency that has a high interest rate (or—equiva-

lently—an in-the-money call on a stock with a very high dividend payout rate).

Find two examples.

21

Portfolio Insurance

21.1 Overview

Options can be used to guarantee minimum returns from stock invest-

ments. As we showed in our discussion of option strategies in Chapter

16, when you purchase a stock (or a portfolio of stocks) and simultane-

ously purchase a put on the stock (on the portfolio), you are assured that

the dollar return from the purchase will never be lower than the exercise

price on the put. However, it is not always possible to fi nd marketed puts

on all portfolios; in this case the Black-Scholes option-pricing formula

can show us how to replicate a put by a dynamic strategy in which the

investment in a risky asset (be it a single stock or a portfolio) and the

investment in riskless bonds changes over time to mimic the returns of

a put option. Such replication strategies are at the heart of the portfolio

insurance strategies discussed here.

We start by considering the following simple example: You decide to

invest in one share of General Pills stock, which currently costs $56. The

stock pays no dividends. You hope for a large capital gain at the end of

the year, but you worry that the stock’s price may decline. To guard

against a decline in the stock’s price, you decide to purchase a European

put on the stock. The put you purchase allows you to sell the stock at

the end of one year for $50. The cost of the put, $2.38, is derived from

the Black-Scholes model (see Chapter 19) using the following data: S

0

=

$56, X = $50, σ = 30 percent, and r = 8 percent:

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

AB C

S56Stock price

X 50 Exercise price

T 1 Time remaining

r 8.00% Risk-free rate of interest

Sigma 30% Stock volatility

d

1

0.7944 <-- (LN(S/X)+(r+0.5*sigma^2)*T)/(sigma*SQRT(T))

d

2

0.4944

<-- d

1

-Sigma*SQRT(T)

N(d

1

)

0.7865

<-- Uses formula NormSDist(d

1

)

N(d

2

)

0.6895

<-- Uses formula NormSDist(d

2

)

Call price 12.22

<-- S*N(d

1

)-X*exp(-r*T)*N(d

2

)

Put price 2.38 <-- call price - S + X*Exp(-r*T): by Put-Call parity

Black-Scholes Option-Pricing Formula

Applied to General Pills Put