Simon Benninga. Financial Modelling 3-rd edition

Подождите немного. Документ загружается.

558 Chapter 20

r = 4 percent, and the stock’s volatility is σ = 25 percent. The Black-

Scholes price of this option is $0.51:

2

3

4

5

6

7

8

9

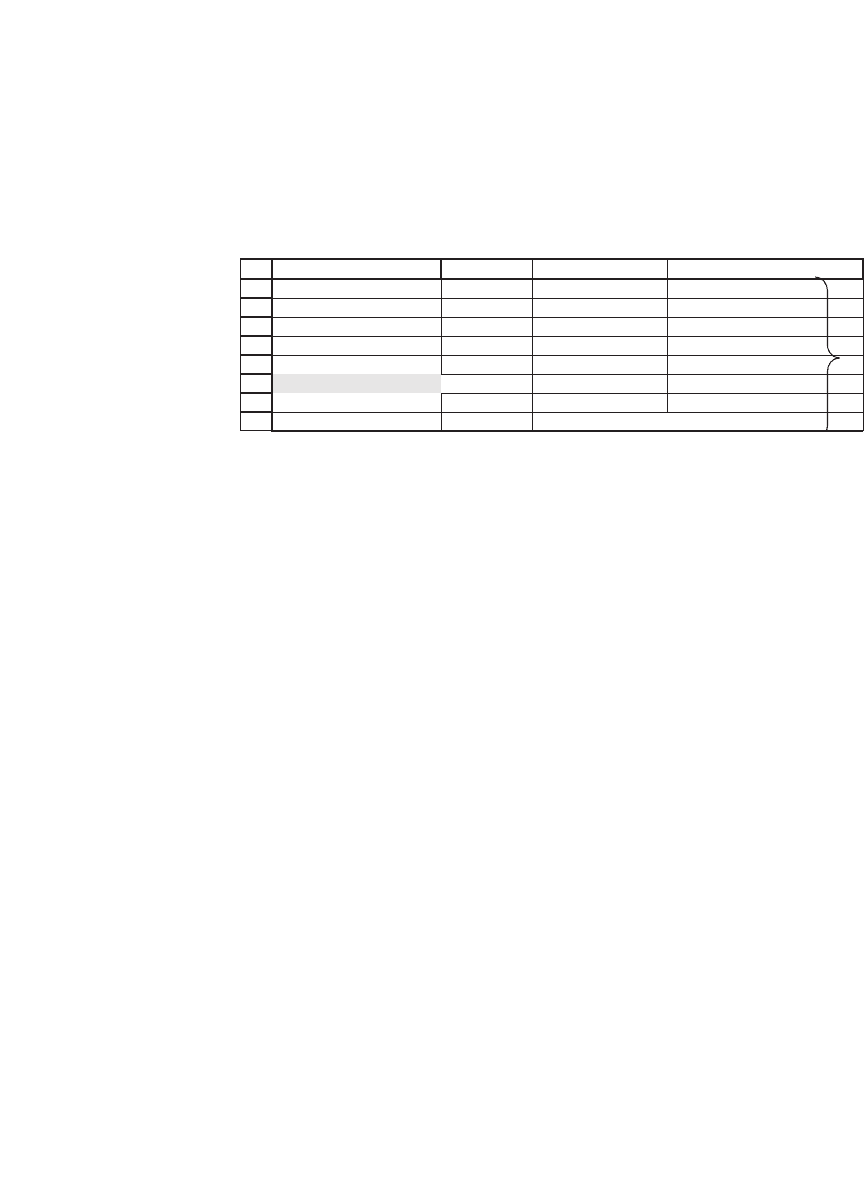

DCBA

S, current stock price 40.00

X, exercise 45.00

r, interest rate 4.00%

k, dividend yield 0.00%

T, expiration 0.2308 <-- =12/52 Initial

Sigma 25%

BS value 0.51 <-- =bsmertoncall(B2,B3,B6,B4,B5,B7)

Note that we use the formula BSMertoncall but with the dividend yield

k = 0 percent, so that this is in effect a regular BS call option.

We decide to create this option by replicating, on a week-to-week

basis, the BS option-pricing formula using delta hedging.

•

At the beginning, 12 weeks before the option’s expiration, we deter-

mine our stock/bond portfolio according to the formula Call = SN(d

1

) −

Xe

−rT

N(d

2

), so that we have a dollar amount SN(d

1

) of shares in the

portfolio and have borrowing of Xe

−rT

N(d

2

). Having determined the

portfolio holdings at the beginning of the 12-week period, we now deter-

mine our portfolio holdings for each of the successive weeks as in the

following steps.

•

In each successive week we set the stock holdings in the portfolio

according to the formula SN(d

1

), but we set the portfolio borrowing so

that the net cash fl ow of the portfolio is zero. Note that SN(d

1

) = SΔ

Call

,

hence the name “delta hedging.”

•

At the end of the 12-week period, we liquidate the portfolio.

The stock and the bond positions for each of the 12 weeks are computed

in the following spreadsheet:

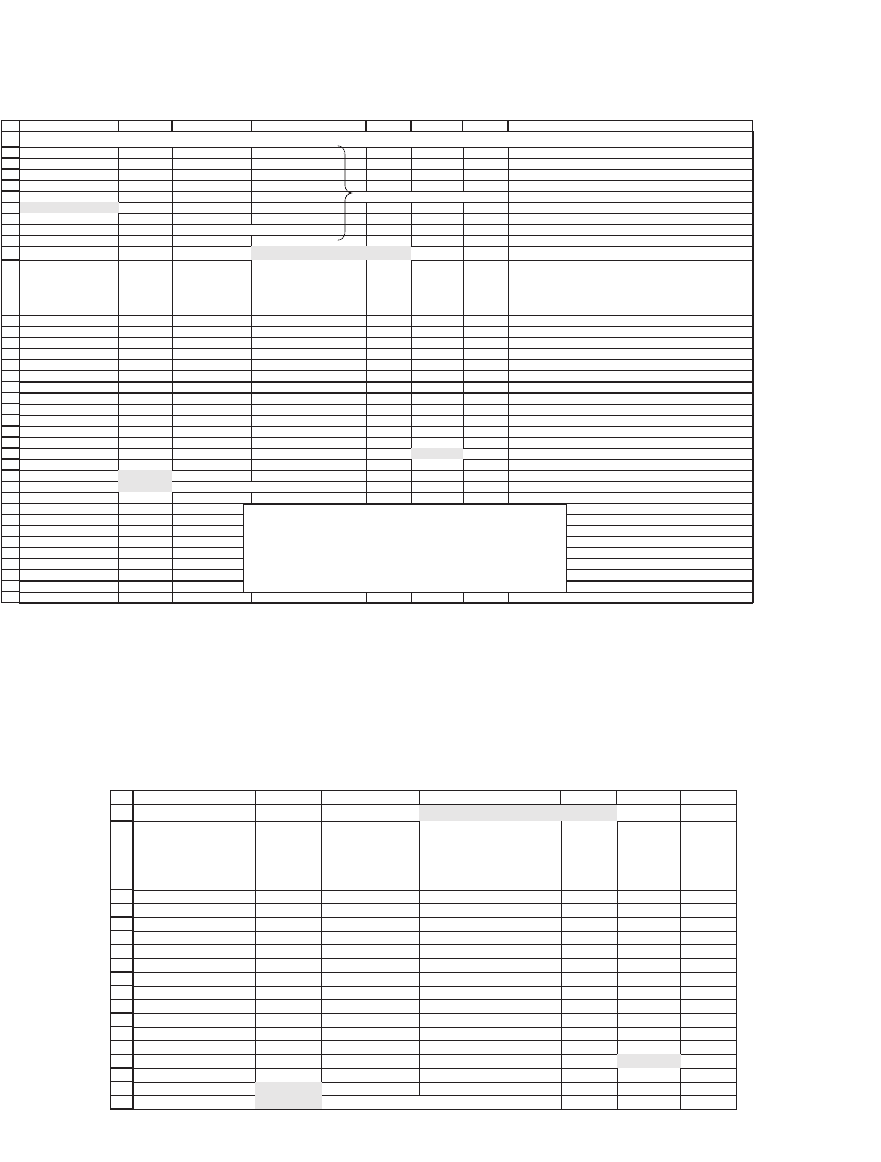

559 Option Greeks

The delta hedge would be perfect if we rebalanced our portfolio con-

tinuously. However, here we have rebalanced only weekly. Had we a

perfect hedge, the portfolio would have paid off max[S

Terminal

− X, 0] (cell

B27); the actual hedge payoff (cell B28) is slightly different.

Pressing [Ctrl] + a works a macro that puts in a new set of random

numbers and runs a different simulation of the stock prices:

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

37

38

GFEDCBA H

S, current stock price 40.00

X, exercise 45.00

r, interest rate 4.00%

k, dividend yield 0.00%

T, expiration 0.2308 <-- =12/52 Initial pricing of call using BS formula

Sigma 25%

BS value 0.51 <-- =bsmertoncall(B2,B3,B6,B4,B5,B7)

Weeks until expiration

Time until

expiration Stock price

Stock = <--

=C13*deltacall(C13,$B$3,

B13,$B$4,0,$B$7) Bond

Porfolio

value

Portfolio

cash flow

12 0.2308 40.000 7.98 -7.47 0.51 0.51

11 0.2115 39.615 6.51 -6.13 0.38 0.05 <-- =(D13*C14/C13-D14)+E13*EXP($B$4*(B13-B14))-E14

10 0.1923 40.607 8.46 -7.96 0.50 0.04 <-- =(D14*C15/C14-D15)+E14*EXP($B$4*(B14-B15))-E15

9 0.1731 38.963 4.00 -3.81 0.19 -0.04 <-- =(D15*C16/C15-D16)+E15*EXP($B$4*(B15-B16))-E16

8 0.1538 38.813 3.15 -3.02 0.14 0.04

7 0.1346 40.563 6.17 -5.89 0.28 -0.01

6 0.1154 41.377 7.71 -7.37 0.34 0.06

5 0.0962 43.321 14.89 -14.15 0.74 -0.04

4 0.0769 42.791 11.08 -10.63 0.45 0.10

3 0.0577 43.509 13.53 -13.03 0.51 0.12

2 0.0385 45.547 28.18 -26.95 1.23 -0.10

1 0.0192 46.943 42.06 -40.00 2.06 0.01

0 0.0000 47.101 2.17 <-- =D24*C25/C24+E24*EXP($B$4*(B24-B25))

Hedged position payoff 2.17 <-- =F25

Actual call payoff 2.10 <-- =MAX(C25-B3,0)

DELTA HEDGING A CALL

Hedging portfolio

At initial date, the stock and bond positions are set using the Black-Scholes

formula: Stock = SN(d

1

), Bond = -X*exp(-rT)N(d

2

).

At each subsequent date t, the stock position is adjusted to S

t

*

Δ

call

. The bond

position is adjusted so that the net cash flow of the portfolio is zero.

At the final date, the stock and bond portfolios are liquidated.

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

FEDCBA

G

Weeks until expiration

Time until

expiration Stock price

Stock = <--

=C13*deltacall(C13,$B$3,

B13,$B$4,0,$B$7) Bond

Porfolio

value

Portfolio

cash flow

12 0.2308 40.000 7.98 -7.47 0.51 0.51

11 0.2115 38.989 5.15 -4.87 0.28 0.01

10 0.1923 41.125 10.00 -9.38 0.61 -0.05

9 0.1731 39.905 5.98 -5.67 0.31 0.00

8 0.1538 40.264 6.17 -5.87 0.30 0.06

7 0.1346 40.158 5.14 -4.91 0.23 0.06

6 0.1154 42.966 14.06 -13.31 0.75 -0.17

5 0.0962 43.185 14.21 -13.51 0.69 0.12

4 0.0769 41.125 4.58 -4.43 0.15 -0.14

3 0.0577 40.246 1.47 -1.44 0.03 0.01

2 0.0385 40.765 1.02 -1.00 0.02 0.03

1 0.0192 40.573 0.06 -0.06 0.00 0.01

0 0.0000 40.709 0.00

Hedged position payoff 0.00 <-- =F25

Actual call payoff 0.00 <-- =MAX(C25-B3,0)

Hedging Portfolio

560 Chapter 20

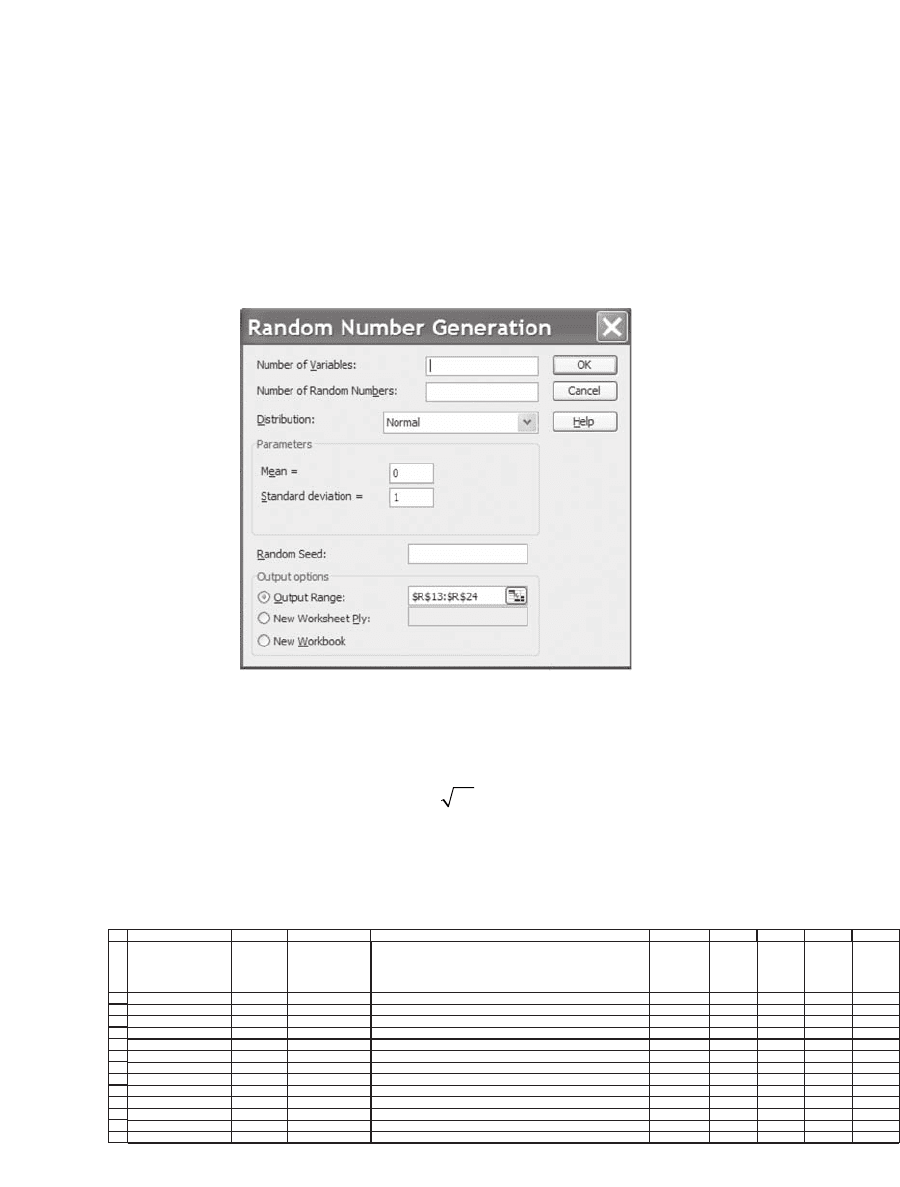

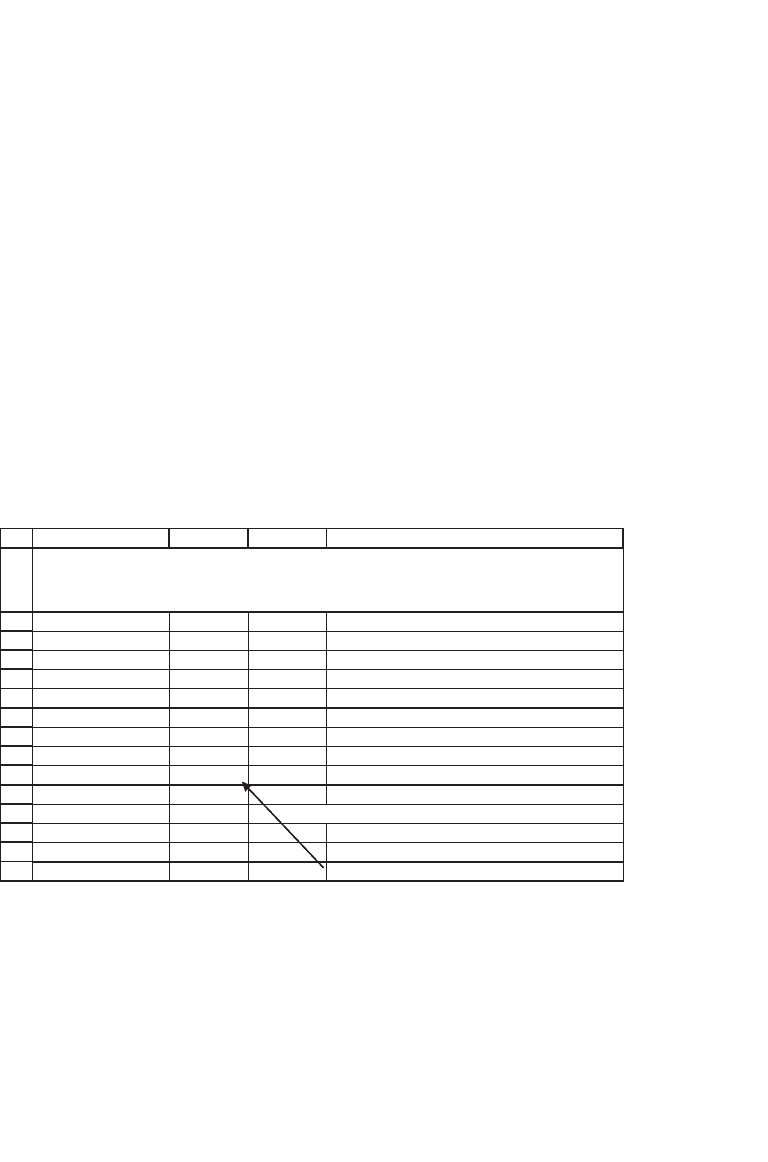

20.3.1 Simulating the Stock Prices

To simulate the stock prices we use a technique explained in Chapter 18.

Tools|Data Analysis|Random Number Generation. We use this Excel

tool to produce 12 random numbers that are distributed normally with

mean equal to 0 and standard deviation equal to 1.

In the spreadsheet simulation of delta hedging, the random numbers

appear in column R. The stock price $40 in cell C12 is the initial stock

price; each subsequent stock price is computed by

SttZ

Previous

∗∗+∗∗exp[ ]μΔ Δσ

where μ (in our example, 20 percent) is the stock’s mean return, σ (25

percent) is the standard deviation of the stock’s returns, and Z is the

random number generated by our simulation.

11

12

13

14

15

16

17

18

19

20

21

22

23

24

ABC D QRST

Weeks until expiration

Time until

expiration Stock price

Standard

normal

random

numbers

12 0.2308 40.000

11 0.2115 41.710 <-- =C12*EXP($U$13*(B12-B13)+$U$14*SQRT(B12-B13)*R13) 1.096416 mu 20%

10 0.1923 42.093 <-- =C13*EXP($U$13*(B13-B14)+$U$14*SQRT(B13-B14)*R14) 0.152941 sigma 25%

9 0.1731 43.380 <-- =C14*EXP($U$13*(B14-B15)+$U$14*SQRT(B14-B15)*R15) 0.757611

8 0.1538 45.231 1.094604

7 0.1346 48.050 1.632943

6 0.1154 48.296 0.035924

5 0.0962 47.363 -0.67341

4 0.0769 47.728 0.110728

3 0.0577 46.838 -0.653959

2 0.0385 47.186 0.102266

1 0.0192 46.586 -0.480061

0 0.0000 49.257 1.497197

U

561 Option Greeks

By recording the keystrokes of the random number generator (see the

next subsection) and making a few changes, we are able to do this simula-

tion many times:

Sub run_random()

‘ Keyboard Shortcut: Ctrl+a

ActiveSheet.Range(“$R$13:$R$24”). _

ClearContents

Application.Run “ATPVBAEN.XLA!Random”, _

ActiveSheet.Range(“$r$13:$r$24”) _

, , , 2, , 0, 1

End Sub

Note that we assigned the keystrokes [Ctrl] + a to run the macro.

20.3.2 Recording Keystrokes to Create VBA Program

We briefl y review the simple technique of recording a macro in Excel.

The previous spreadsheet has a column of random normal deviates in

column R. These numbers, generated by Tools|Data Analysis|Random

Number Generation, give us a series of random stock prices in column

C. Each stock price S

t

is defi ned by

SS t tZ

tt

=+

−1

exp[ ]μσΔΔ

, where μ

and σ are given in cells T14 and T15:

12

13

14

15

16

17

18

19

20

21

22

23

24

25

RSTU

Standard

normal

random

numbers

1.385106

-0.389564 mu 20%

0.601965 sigma 25%

-1.302831

-0.222169

1.16092

0.462537

1.212907

-0.465775

0.368848

1.209403

0.759856

-0.014038

562 Chapter 20

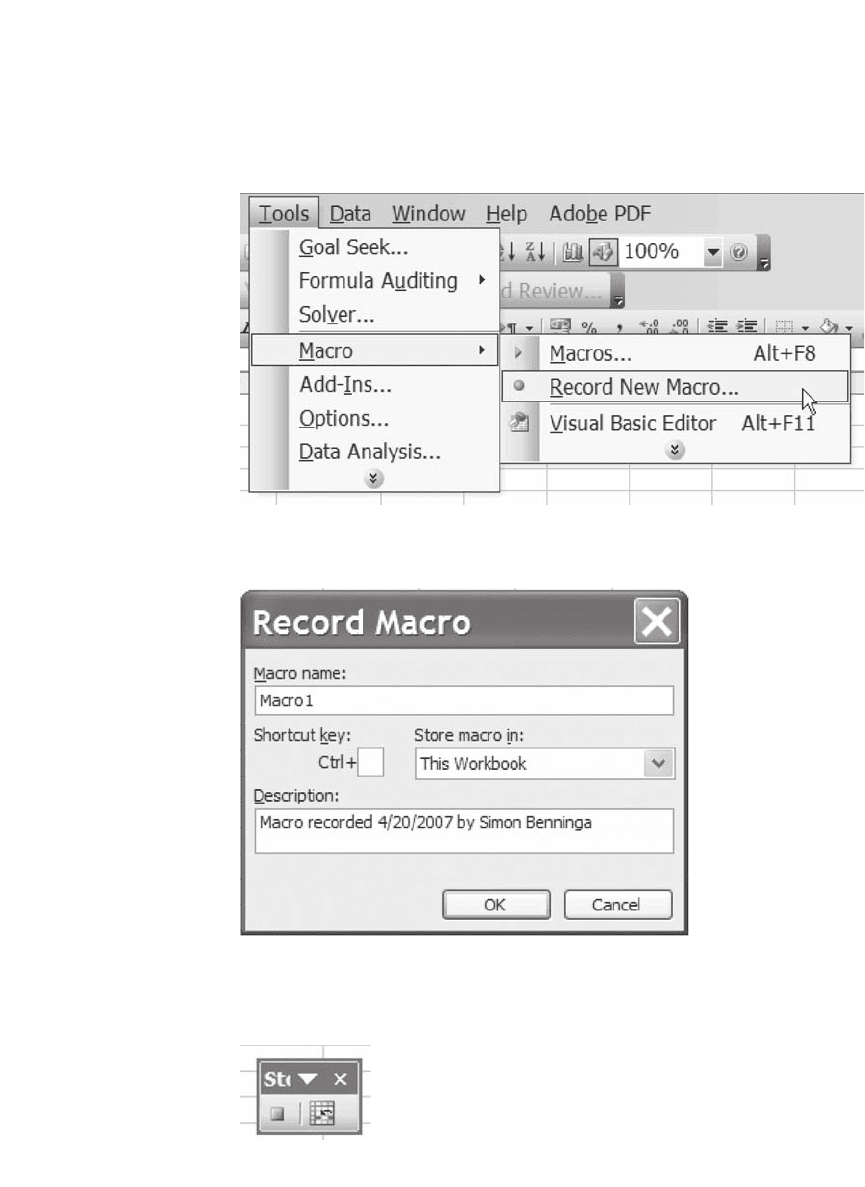

To record the macro, push Tools|Macro|Record New Macro:

This brings up the following screen.

After pressing OK, a Stop recording button will appear on the

spreadsheet:

563 Option Greeks

Now push the correct buttons to create the column of random numbers,

using Tools|Data Analysis|Random Number Generation, with the screen

as indicated in the previous subsection. This procedure replaces the

numbers in cells R13:R24. When you are fi nished, push the Stop record-

ing button. Now go to the VBA editor ([Alt]+F11) and see what you’ve

recorded:

Sub run_random()

‘

‘ Sub Macro1()

‘

‘ Macro1 Macro

‘ Macro recorded 4/20/2007 by Simon Benninga

‘

‘ Keyboard Shortcut: Ctrl+a

‘

Range(“R13:R24”).Select

Selection.ClearContents

Application.Run “ATPVBAEN.XLA! _

Random”, , , , 2, , 0, 1

End Sub

(Note that before we ran Tools|Data Analysis|Random Number Genera-

tion, we actually cleared range R13:R24. This step prevents the message

asking if we want to replace the data. The deletion of the range was

faithfully recorded by Excel.)

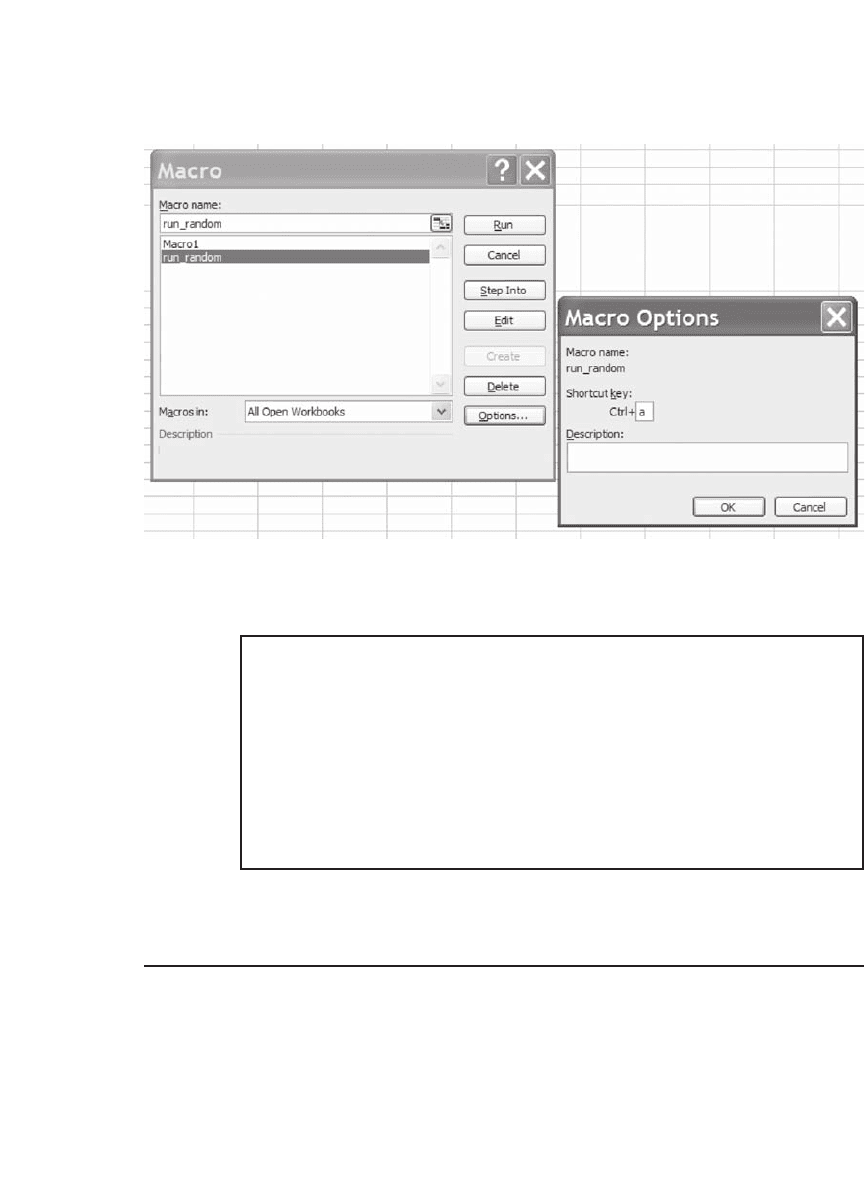

This macro can be edited. Here’s the way the fi nal version appears. We

have renamed the macro run_random and used Tools|Macro|Options to

assign a shortcut key to the macro:

564 Chapter 20

Here’s the fi nal product:

Sub run_random()

‘ Keyboard Shortcut: Ctrl+a

ActiveSheet.Range(“$R$13:$R$24”).

ClearContents

Application.Run “ATPVBAEN.XLA!Random”, _

ActiveSheet.Range(“$r$13:$r$24”), , _

, 2, , 0, 1

End Sub

This macro can now be run repeatedly by pressing [Ctrl] + a.

20.4 Hedging a Collar

A collar is an option strategy designed to protect the holder of a package

of shares against possible price losses. The usual collar is a combination

of a written call plus a purchased put, designed so that the net cost of

the position is zero. Thus the collar provides costless protection to its

565 Option Greeks

holder. Here’s an example: On January 1, 2008, a bank’s client holds

5,000,000 shares of XYZ Corporation. Each share is currently worth $55.

Because the stock is currently restricted, the client cannot sell the shares

until one year from now. However, he is worried that the stock price will

decline, and hence he desires to purchase a collar.

The client asks an investment bank to design the following package:

•

He wants to buy a put on the shares with T = 1 year and exercise price

X

Put

= $49.04.

•

He wants to write a call on the shares with T = 1 year and exercise

price X

Call

= $70.00.

The exercise prices have been set so that the Black-Scholes value of the

call and the put are equal:

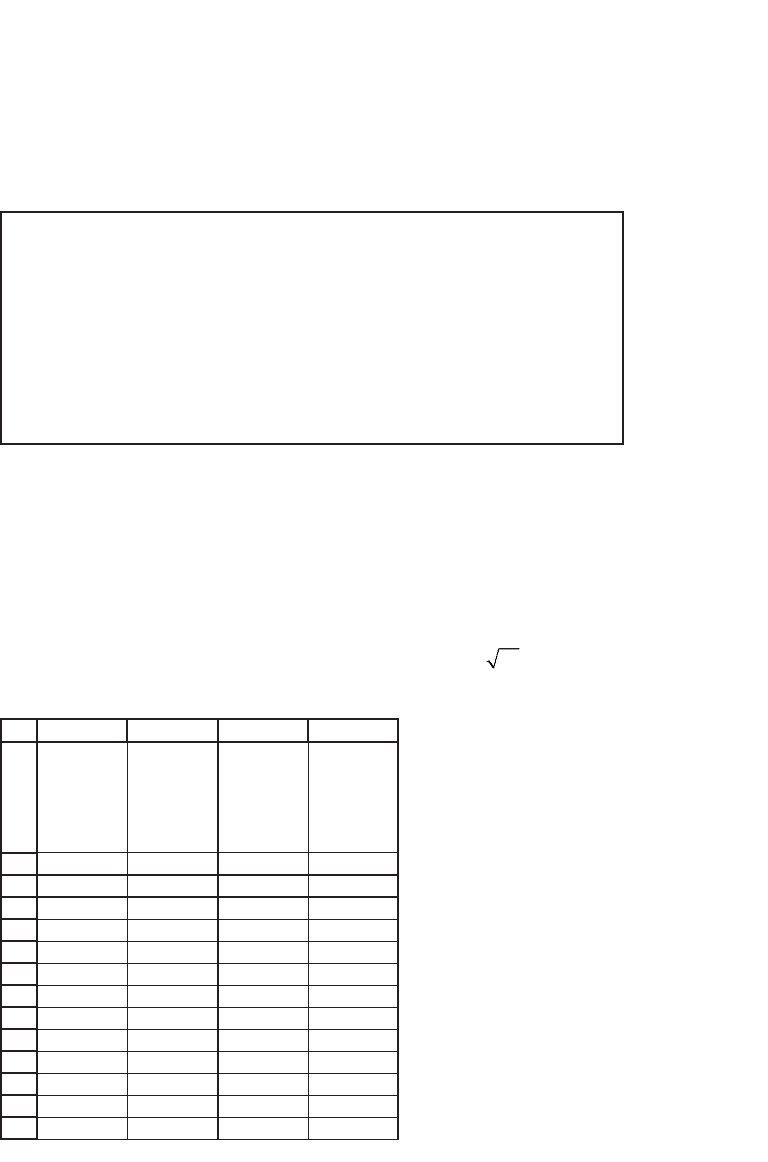

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

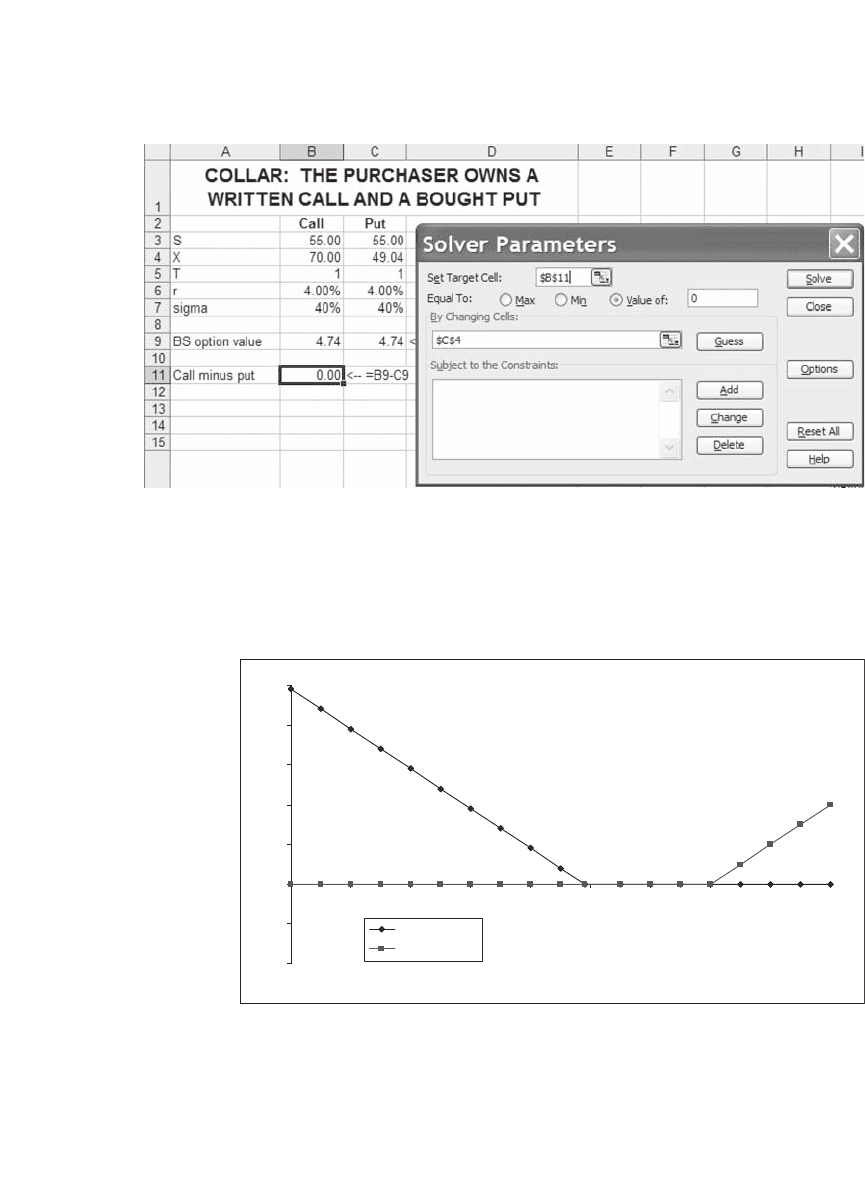

ABC D

Call Put

S 55.00 55.00

X 70.00 49.04

1T1

r, interest 4.00% 4.00%

k, dividend yield 0.00% 0.00%

Sigma 40% 40%

BS option value 4.74 4.74 <-- =bsmertonput(C3,C4,C5,C6,C7,C8)

Call minus put 0.00 <-- =B10-C10

=bsmertoncall(B3,B4,B5,B6,B7,B8)

COLLAR: THE PURCHASER OWNS A WRITTEN CALL

AND A BOUGHT PUT

Given X

call

= 70 for the call, the put exercise price was determined

using Solver:

566 Chapter 20

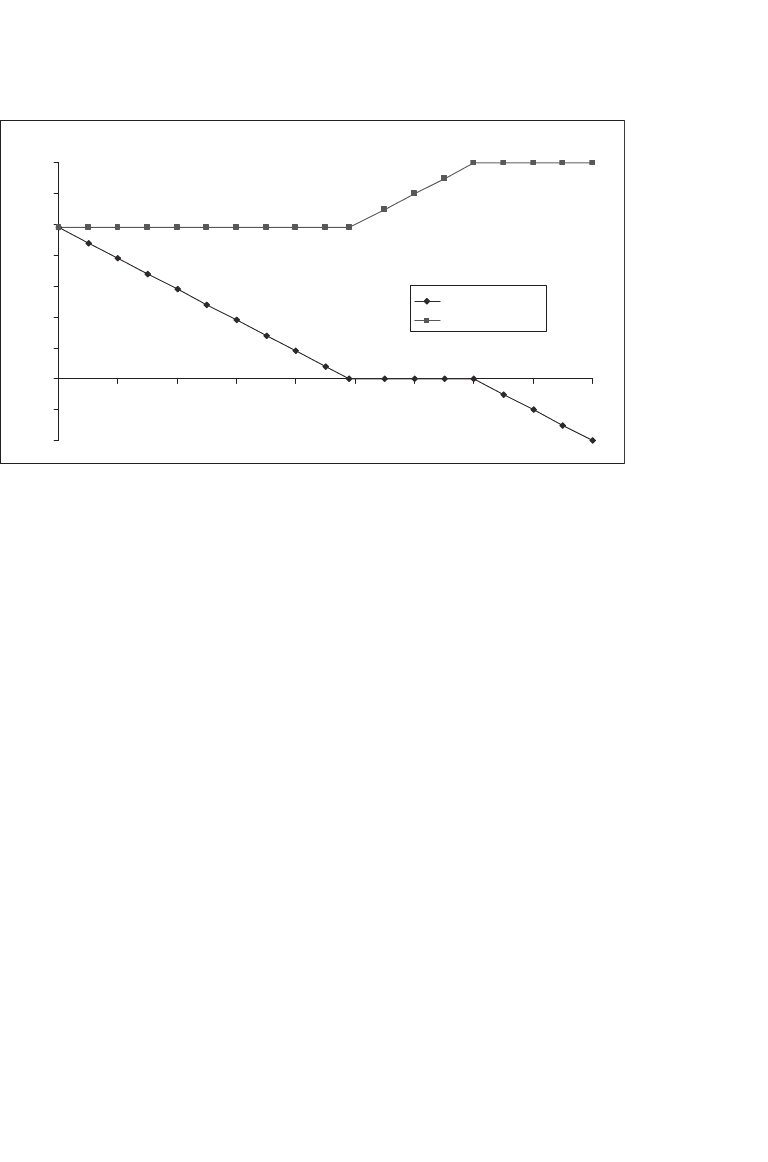

The point of the collar is to give the purchaser upside potential with

limited downside risk. In this example, the terminal payoffs are given

by

Collar Payoff to Holder

Written Call + Bought Put

-20

-10

0

10

20

30

40

50

0 102030405060708090

Terminal stock price, S

T

Written call

Bought put

In addition to his collar, the client has a portfolio of the shares. The

payoffs to the holder of the collar plus the shares are never less than $49.

This is, of course, the protection that the client was seeking.

567 Option Greeks

Collar Payoff + Stock Value to Holder

Holder Never Gets Less Than Collar X

Put

-20

-10

0

10

20

30

40

50

60

70

0 102030405060708090

Terminal stock price, S

T

Collar payoff

Collar + stock

20.4.1 A Slightly Longer Story

Even though the Black-Scholes value of the collar is initially zero, actu-

ally the investment bank sold the collar to the client for $5. There are

several reasons why the client might want to pay this amount:

•

Perhaps there is low liquidity in the options (this is often the case in

longer-term options), so that the bank is actually supplying a valuable

liquidity service.

•

It might be that the options do not actually exist—either because the

particular long-term options in question are not marketed or perhaps

because there are no options on the particular underlying stock (this is

often the case for specifi c portfolios). In this case the bank is actually

creating the options underlying the collar by creating an appropriate

portfolio of stocks and bonds and by changing the portfolio proportions

over time (see next subsection). The creation and constant monitoring

of this portfolio is a service worth paying for.

20.4.2 Delta Hedging the Collar: The Bank’s Problem

The client for the collar is short a call and long a put. The bank wants to

make a similar investment, so that it will parallel the client’s portfolio

and have the money to pay off the client at the maturity of his collar. In

terms of the Black-Scholes formula, this situation turns out to mean that

the net position of the bank is a short stock fi nanced by a bond

investment: