Pike Robert, Neal Bill. Corporate finance and investment: decisions and strategy

Подождите немного. Документ загружается.

.

Chapter 21 Managing currency risk 615

to exploration and the US operation would transfer $11 million likewise, resulting in

total flows of only $14 million.

Some experts dispute whether netting is a true hedging technique, rather than a

cost-saving device, especially where the netted currency differs from the parent’s

reporting currency. However, if it does result in lower values of currency being

shipped across the exchanges, then it is undeniable that it is capable of saving consid-

erable banking and money transmission costs.

Matching is similar in concept to netting, but involves third parties as well as intra-

group affiliates. A company tries to match its currency inflows by amount and timing

with its expected outflows. For example, a company exporting to the USA and thus

anticipating USD receipts could match this payable by arranging a USD outflow, per-

haps by contracting to import from the same country. Clearly, as with netting, a two-

way flow of currency is desirable – ’natural matching’. However, ‘parallel matching’

can be achieved by matching in terms of currencies that tend to move closely togeth-

er over time, e.g. matching USD outflows to Canadian dollar inflows. Matching can

also be achieved by offsetting Balance Sheet items against Profit and Loss Account

items. For example, a company with a long-term cash inflow stream in USD may also

borrow in USD, to create an offsetting outflow of interest and capital payments.

Leading and lagging currency payments is done to speed up or delay payments

when a change in the value of a currency is expected. This involves forecasting future

exchange rate movements, and therefore carries an element of speculation. Where

payables are involved, the transfer is speeded up if the foreign currency is expected to

appreciate against the domestic currency and slowed down if the overseas currency is

expected to depreciate. A UK company importing from the USA during late 2003,

when the USD was falling against sterling, may well have tried to lag payments.

Leading and lagging within a group of companies is relatively easy to arrange, but

when dealing with other firms, this can be problematic. A customer buying on credit

will advance payment only if offered an inducement such as a discount for early pay-

ment. The same applies to delaying payment to an external supplier – the danger is

loss of goodwill. Even for intra-firm transactions, there may still be local regulations

and currency controls that limit flexibility.

Currency transfers by companies into and out of less-developed countries,

whose currencies tend to be weak, are closely scrutinised by the governments of

those countries because of the destabilising effect they may have on their curren-

cy. In some cases, they are illegal, both for their ability to exacerbate currency

weakness and also because of the effect on local minority shareholders of an over-

seas subsidiary. Leading a payment from the overseas subsidiary to the UK parent

will raise the GBP profits of the parent, but lower the overseas currency profits of

the subsidiary thus damaging local shareholders’ interests, which risks alienating

Table 21.3

Oilex’s internal

currency flows

Paying subsidiary ($m)

UK US Norway Total Net

Receiving UK – 10 4

subsidiary US 5 – 2

($m) Norway 12 8 –

Total 41

Net 14113

61817

1420

117

314

natural matching

A natural match is achieved

where the firm has a two-way

cash flow in the same currency

due to the structure of its

operations, e.g. selling in a

currency in which it sources

supplies

CFAI_C21.QXD 3/15/07 7:47 AM Page 615

.

616 Part VI International finance

local opinion and antagonising the host government. This is one reason why repa-

triation of profits from overseas subsidiaries is often closely controlled by foreign

governments.

re-invoicing centre

A corporate subsidiary set up

usually in an off-shore location

to manage transaction expo-

sure arising from trade

between separate divisions

of the parent firm

Self-assessment activity 21.7

Delete as appropriate.

Leading is advancing outflows in a strong/weak currency and advancing inflows in a

strong/weak currency. Lagging is delaying inflows in a strong/weak currency and delaying

outflows in a strong/weak currency.

(Answer in Appendix A at the back of the book)

The UK exporter might also consider a pre-emptive price variation. If it expects GBP

to strengthen against the currency of an overseas customer, it may raise the contract

price. However, this may have adverse consequences for sales, especially if competi-

tors are prepared to shoulder currency risk by accepting payment in the overseas cur-

rency. Conversely, the acceptability of this ploy may be greater if the exporter quotes

a price based on the forward rate rather than the spot rate when setting the value of

the contract. Generally, however, such price variations require a strong competitive

position in overseas markets. For this reason, another such device, switching the cur-

rency in which the contract is denominated to a third currency, say USD, also has to be

used with caution. However, traders in basic commodities have no such flexibility,

since most of these are priced in USD.

The Customs and Excise Survey in 2001 revealed that 29 per cent of UK exports and

34 per cent of imports were invoiced in USD.

Risk-sharing is a contractual arrangement whereby the buyer and seller agree in

advance to share between them the impact of currency movements. This is recom-

mended when the two parties want to build a long-term relationship. However, if

exchange rate variations exceed tolerable limits, the arrangement may have to be

re-negotiated.

It might work like this. Firm X supplies Firm B in another country. They may agree

that all transactions will be made at the ruling spot rate between the two parties’

respective currencies. If, however, the rate at settlement varies by up to, say, 5 per cent

either side of the original spot rate, X may accept the transaction exposure. If the rate

varies by, say 5–10 per cent of the original spot, they may share the difference equally,

but for variations in excess of 10 per cent, the agreement may become void. Harley

Davidson is known to operate this policy with foreign importers.

Re-invoicing centres. A re-invoicing centre (RIC) is a separate corporate subsidiary

that manages from one location, often off-shore, all the transaction exposure arising

from intra-company trading.

For example, a manufacturing unit may sell goods to distribution subsidiaries of its

parent firm indirectly by selling first to the re-invoicing centre, which then re-sells the

goods to the distribution subsidiary. Title to the goods passes to the RIC but the goods

are shipped directly from the manufacturing subsidiary to the distributor. The RIC

thus manages the transactions on paper but keeps no physical stocks. All transactions

exposure resides with the RIC.

A problem may arise due to allegations of profit-shifting via transfer pricing. To

avoid such allegations, the RIC may sell at cost plus a commission for its services. The

resale price is commonly the manufacturer’s price times the forward exchange rate for

the date when settlement by the distributor is expected.

price variation

Adjustment of a firm’s pricing

policy to take into account

expected foreign exchange rate

movements

risk-sharing

An arrangement where the

two parties to an

import/export deal agree to

share the risk, and thus the

impact of unexpected

exchange rate movements

CFAI_C21.QXD 3/15/07 7:47 AM Page 616

.

Chapter 21 Managing currency risk 617

foreign currency swap

A way of using the forward

markets to adjust the maturity

date of an initially agreed con-

tract with a bank

RICs offer the major benefit of concentrating the management of all FX transactions

in one location. As a result, the multinational corporation (MNC) can develop special-

ist expertise in judging which hedging technique is optimal at any one time. However,

it should avoid conducting business with other firms in its country of location in order

to establish non-resident status.

The most widely used external hedging technique is the forward contract. It involves

pre-selling/buying a specific amount of currency at a rate specified now for delivery at

a specified time in the future. It is a way of totally removing risk of currency variation

by locking in the rate quoted today by the forward market. However, there remain the

risks of the trading partner (credit risk) defaulting and that of failure of the bank that

arranges the deal (counterparty risk).

Consider the case of a UK exporter entering an export contract in February for

$10 million with a company in Denver. The companies agree on payment in three

months time, i.e. in May. The current spot rate is valuing the contract at

If the exporter is concerned by the possibility of a decline in the

USD versus GBP, it will look carefully at the rate quoted for 3-month delivery of

USD. Assume the forward market quotes ‘2c discount’. The forward outright is

thus:

If the exporter believes in the predictive accuracy of the forward market, it may

decide to sell forward the anticipated $10 million receipt for

This involves taking a discount on the current spot value of the deal. Hedging costs

the exporter a little over 1 per cent of the original value of the deal (although

a higher proportion of his profits), but this may look trivial beside the losses that could

materialise if GBP strengthens further than this. Conversely, the exporter is excluded

from any gains if the USD appreciates in value.

If the exporter is unsure about the precise payment date by its customer, it may

enter a forward option. In this case, the bank leaves the currency settlement date open,

but books the deal at the worst forward rate ruling over the period concerned. Say the

two companies had agreed on payment ‘sometime over the next three months’, but the

exporter knows that the customer may delay payment for six months. The relevant

forward quotations are:

1 month: 0.5c dis Outright: 1.6050

2 months: 1.0c dis Outright: 1.6100

3 months: 2.0c dis Outright: 1.6200

6 months: 3.0c dis Outright: 1.6300

The worst rate for the exporter is the six-month rate, so the deal will be booked for

again a minor increase in cost. If the customer pays up at any

other time, the bank is committed to paying the exporter the amount agreed in the for-

ward contract when the $10 million is handed over.

Another way of covering uncertainty over settlement dates is to undertake a foreign

currency swap. The Bank of International Settlements (BIS, www.bis.org) defines a swap as

follows:

Foreign exchange swaps commit two counterparties to the exchange of two cash flows

and involve the sale of one currency for another in the spot market with the simultane-

ous repurchase of the first currency in the forward market.

$10 m>1.63 £6.13 m,

£80,000,

$10 m>1.62 £6.17 m.

Spot $1.60 plus 2.0c $1.62 : £1

£6.25 m.$10 m>1.6

$1.6 : £1,

21.9 EXTERNAL HEDGING TECHNIQUES

credit risk

The risk that a foreign

customer might not pay up as

agreed on time or at all.

counterparty risk

The risk that the bank which is

party to a hedging transaction

such as a forward contract

may not deliver the agreed

amount of currency at the

agreed time

CFAI_C21.QXD 3/15/07 7:47 AM Page 617

.

An exporter can take forward cover to a specified date, but if a later settlement date

than this is agreed, it can extend the contract to the newly agreed date. For example,

a forward–forward swap is needed if our exporter covers ahead from February until

May, but if in March, a firm settlement date is agreed for June. Contractually, it has to

meet the first contract maturing in May, and then take cover for a further month. This

is done in March by buying $10 million two months forward, i.e. for delivery in May

to meet the existing contract, and by selling $10 million three months forward for

delivery in June. In this case, the exporter swaps the maturity date and ends up hold-

ing three separate contracts. Instead, it could adopt the riskier alternative of a

spot–forward swap, fulfilling the May contract by buying the $10 million on the spot

market, and also arranging to sell $10 million one month forward, i.e. in June. The BIS

estimated average daily swap transactions at US$944 billion in April 2004, 50 per cent

of total non-derivatives trading (US$1,880 billion).

Money market cover involves the exporter creating a liability in the form of a

short-term loan in the same currency that it expects to receive. The amount to bor-

row will be sufficient to make the amount receivable coincide with the principal of

the loan plus interest. Assume the Eurodollar rate of interest, the annual rate payable

on loans denominated in USD, is 8 per cent, i.e. 2.00 per cent over three months. The

UK exporter would borrow This would be converted into

GBP at the spot rate – in our example, – to realise

This looks like a considerable discount on the spot value of the export deal

but the GBP proceeds of this operation can be invested for three months to defray

the cost. Obviously, if the exporter could invest at a rate in excess of 8 per cent p.a.,

it would profit from this, but IRP should make this impossible, i.e. if USD sells at a

forward discount, interest rates in New York should exceed those in London. If USD

should unexpectedly fall in value against GBP, lower than expected receipts from the

US contract are offset by the lower GBP payment required to repay the Eurodollar

loan.

An alternative to a one-off loan to cover a specific contract is for the exporter to

operate an overdraft denominated in one or a set of overseas currencies. The trader

will aim to maintain the balance of the overdraft as sales are made, and use the sales

proceeds as and when received to reduce the overdraft. This is a convenient technique

where a company makes a series of small overseas sales, many with uncertain pay-

ment dates. A converse arrangement, i.e. a currency bank deposit account, may be

arranged by a company with receivables in excess of payables.

International invoice finance is a fast-expanding business among UK traders,

amounting to a total of (measured by client turnover figures) in 2004. This

comprised of export invoice discounting (13 per cent growth on 2003) and

in export factoring (9 per cent growth on 2003). The international factor can

provide many services to the small company, including absorbing the exchange rate

risk. Once a foreign contract is signed, the factor pays, say, 80 per cent of the foreign

value to the UK exporter in GBP. If the exchange rate moves against the UK company

before receipt of the foreign currency, the factor absorbs the loss. In compensation, the

factor also takes any gain arising from a change in rates. Factors make use of overseas

‘correspondent’ factors, enabling clients to benefit from expert local knowledge of

overseas buyers’ credit-worthiness. Overseas factoring is usually expensive but offers

the benefits of lower administration and credit collection costs.

Export receivables that involve settlement via Bills of Exchange can also be dis-

counted with a bank in the customer’s country and the foreign currency proceeds

repatriated at the relevant spot rate. Alternatively, the bill can be discounted in the

exporter’s home country, enabling the exporter to receive settlement directly in home

currency.

The most sophisticated external hedging facilities involve derivatives such as options,

futures and swaps. These are treated in more detail below.

£0.9 billion

£3.3 billion

£4.2 billion

1£6.25 m2,

1$9.80 m>1.62 £6.13 m.$1.6 : £1

1$10 m>1.02 $9.80 m2.

618 Part VI International finance

forward–forward swap

Where the original forward

contract is supplemented by

new contracts that have the

effect of extending the maturi-

ty date of the original one

spot–forward swap

A less comprehensive forward

swap that involves speculation

on the future spot market

CFAI_C21.QXD 3/15/07 7:47 AM Page 618

.

Chapter 21 Managing currency risk 619

call option

A financial derivative that gives

the buyer the right but not the

obligation to buy a particular

commodity or currency at a

specific future date

■ Currency options

A currency option confers the right, but (unlike the forward contract) not the obligation,

to buy or sell a fixed amount of a particular currency at or between two specified future

dates at an agreed exchange rate (the strike price).

A call option gives the purchaser of the option the right to buy, while a put option

gives the right to sell. In each case, the buyer of the option pays the ‘writer’ of the

option a premium. Options traded through exchanges are written in specified con-

tract sizes: for example, on the Philadelphia Stock Exchange (PHLX), GBP is dealt

in lot or contract sizes of 31,250 units, i.e. Most exchanges offer a limited

number of alternative exercise prices and maturity dates. PHLX also trades USD

options against the Australian dollar (contract size A$100,000), Canadian dollar

(C$100,000), Japanese Yen (12,500,000) and the Swiss Franc (125,000), as well as euro

contracts (62,500). Delivery dates are for the quarter months of March, June,

September and December plus the two immediately upcoming months. For non-

standard options, the would-be purchaser may have to shop around for a cus-

tomised quotation on the over-the-counter (OTC) market. This may be necessary

for unusual or ‘exotic’ currencies.

A‘European option’ can be exercised only at the specified maturity date, while an

‘American option’ can be exercised at any time up to the specified expiry date. If an

option is not exercised, it lapses and the premium is lost. However, the appeal of an

option is that the maximum loss is limited to the cost of the premium, while the pur-

chaser retains the upside potential. The size of the premium depends on the difference

between the current exchange rate and the strike price (for an unlikely strike price,

premiums will be very low), the volatility of the two currencies, the period to maturi-

ty and, for OTC contracts, the size of the contract.

Here is an example of how a trader could use a currency option for hedging pur-

poses. A UK exporter sells goods for $11.875 million to a customer in Baltimore in

January 2005 for settlement in March. The contract is worth when valued

at spot of but the exporter is concerned that sterling might appreciate before

settlement, thus eroding the profit margin. In this case, it might purchase a call option

on GBP, i.e. an option to sell USD in exchange for GBP. The premiums in cents per

option unit that were available at the Chicago Mercantile Exchange CCME on 3

January 2005 are shown in Table 21.4.

Clearly, the stronger the position of USD, the more expensive the option. The

exporter can lock in the spot rate, or purchase protection against the rate rising above

the current spot by various amounts. This requires it to take a view on the most likely

adverse movements. Choosing the $1.91 strike price gives the exporter insurance

$1.90 : £1,

£6.25 million

£31,250.

Table 21.4

Sterling /US$ options

US $/UK£ Options (CME)

Strike price CALLS PUTS

3 Jan Jan. Feb. Mar. Jan. Feb. Mar.

1890 2.27 – 3.30 0.60 1.56 2.30

1900 0.62 2.67 3.00 1.05 2.64 3.20

1910 0.51 2.21 2.50 1.67 2.50 3.29

1920 0.72 1.24 1.92 2.41 3.11 4.40

Previous day’s data: volume, 29; calls, 17 puts, 46; open interest, 10,036

(Reuters/CME)

Source: Financial Times, 4 January 2005.

over-the-counter

An over-the-counter transac-

tion, e.g. the purchase of an

option, where the terms are

tailor-made to suit the require-

ments of the purchaser

CFAI_C21.QXD 3/15/07 7:47 AM Page 619

.

620 Part VI International finance

against the exchange rate going higher than $1.91. The cost of purchasing March

options is:

i.e. at spot.

If the spot rate in March is less than $1.91, the option is not worth exercising and is

said to be ‘out of money’; if spot is $1.91, it is ‘at the money’; while if spot is over $1.92,

say $2.00, the option is ‘in the money’. In the last case, export earnings of $11.875 mil-

lion can be sold at $1.91 to realise compared with a spot value of

Although the option has cost it has prevented the

exporter from losing In this case, there is a net gain,

allowing for the premium, of nearly

It is important to appreciate that options are ‘zero-sum games’ – what the holder wins,

the writer loses, and vice versa. It is relatively unusual to use currency options to hedge

ongoing trading exposures – options are complex, they are often expensive compared to

using the forward market and it is time-consuming to monitor an American option to

judge whether it is worth closing out the position prematurely. Options tend to be used

to cover major isolated expenditures, e.g. the cost of completing the acquisition of an

overseas company or the phased payments in a major overseas construction project.

The PHLX website (www.phlx.com) gives a history of option trading and also a trad-

ing guide, and daily quotations on sterling and euros appear in the Financial Times.

£200,000.

1£6.22 m £5.94 m2 £280,000.

£82,672,$11.875 m>$2.00 £5.94 m.

£6.22 million,

£82,672

Cost of option £31,250 2.50c 200 $156,250

Number of lots required

$11.875 m

$1.90

£31,250 200

Self-assessment activity 21.8

What is the net cost/benefit of an option that is ‘at the money’?

(Answer in Appendix A at the back of the book)

■ Currency futures

In principle, a futures contract can be arranged for any product or commodity, includ-

ing financial instruments and currencies. A currency futures contract is a commitment

to deliver a specific amount of a specified currency at a specified future date for an

agreed price incorporated in the contract. It performs a similar function to a forward

contract, but has some major differences.

Currency futures contracts have the following characteristics:

1 They are marketable instruments traded on organised futures markets.

2 They can be completed (liquidated) before the contracted date, whereas a forward

contract has to run to maturity.

3 They are relatively inflexible, being available for a limited range of currencies and

for standard maturity dates. The world’s largest market for currency futures is the

Chicago Mercantile Exchange (CME). It trades futures in eleven different currencies

for delivery four times each year: March, June, September and December.

4 They are dealt in standard lot sizes, or contracts.

5 The CME requires a down-payment called a ‘performance bond’ or ‘margin’ of

about 1.5 per cent of the contract value, whereas forward contracts involve a single

payment at maturity.

6 They also involve ‘variation payments’, essentially the ongoing losses on the con-

tract to be paid to the exchange on which the contract is dealt.

7 They are usually cheaper than forward contracts, requiring a small commission

payment rather than a buy/sell spread.

CFAI_C21.QXD 3/15/07 7:47 AM Page 620

.

Chapter 21 Managing currency risk 621

It is difficult to ‘tailor make’ a currency future to the precise needs of the parties

involved, which explains why some exchanges, e.g. LIFFE, have now stopped currency

futures trading.

How a currency future works

This is best shown with an example. In June, a UK importer agrees to buy goods worth

$10 million from a firm in Detroit. The sterling/dollar spot rate is valuing the

deal at Settlement is agreed for 15 August, but the importer is

concerned that appreciation of USD will undermine its profitability (it will have to find

more GBP to meet the import cost). On the CME, the market price (i.e. the exchange rate)

for September GBP futures is $1.48, suggesting that the market expects USD to appreciate.

The importer needs eventually to acquire GBP to pay for its imports, so it should

sell (i.e. go short of) GBP by selling GBP futures contracts at $1.48. With the standard

contract size of the number of whole contracts required is:

Note the indivisibility problem – 108 contracts covers exposure of only

This makes hedging by futures unattractive to small

exporters. There is also a timing problem, as the importer has to supply USD before

the expiry of the contract in August. When payment is due, the importer will close out

the contract by arranging a reverse trade, i.e. one with exactly opposite features, which

means buying 108 September GBP futures at the ruling market price. If USD has

strengthened against GBP between June and August, the importer will make a profit

on the futures contract.

Imagine this does happen and the spot rate on 15 August is $1.49 and the September

futures price is $1.475. As payment for the goods is required, the importer converts

GBP for USD on the spot market at a cost of Compared

with the cost of the deal at the June spot rate, it has made a loss of owing to

the feared USD appreciation. However, the importer holds 108 futures contracts,

enabling it to sell GBP at $1.48. To close its position, the importer can buy the same

number of contracts at an exchange rate of $1.475. It will thus make a profit on the

futures market of:

Valued at spot of $1.49, this is worth leaving a net loss of

This demonstrates the difficulty of achieving a perfectly

hedged position with currency futures. Moreover, the futures market may not always

move to the same degree as the spot market, owing to expectations about future exchange

rate movements.

The CME website (www.cme.com) provides a beginner’s guide to using the futures

markets, and prices for USD currency futures are quoted daily in the Financial Times.

■ Currency swaps

The BIS defines currency swaps as follows:

‘A currency swap (or cross-currency swap) commits two counterparties to several

cash flows, which in most cases involve an initial exchange of principal and a final

re-exchange of principal upon maturity of the contract, and in all cases, several

streams of interest payments.

Currency swaps originated from controls applied by the Bank of England over for-

eign exchange movements prior to 1979. Firms wishing to obtain foreign currency to

1£44,743 £22,6512 £22,088.

1$33,750>1.492 £22,651,

Sells

108 £62,500 1.480

$9,990,000

Buys

108 £62,500 1.475

$9,956,250

Profit

$33,750

£44,743,

1$10 m>1.492 $6,711,409.

£62,500 1.482 $9,990,000.

1108

3$10 m>1£62,500 1.4824 108 approx.

£62,500,

$10 m>1.50 £6,666,666.

$1.50 : £1,

currency swaps

Where two or more parties

swap the capital value and

associated interest streams of

their borrowing in different

currencies

CFAI_C21.QXD 3/15/07 7:47 AM Page 621

.

622 Part VI International finance

invest overseas, say in the USA, found they could avoid these controls by entering an

agreement with a US company that operated a subsidiary in the UK. In return for

receiving a loan from the US company to finance its own activity in the USA, the UK

company would lend to the UK-based subsidiary of the US company. The two firms

would agree to repay the loans in the local currency after an agreed period, thereby

locking in a particular exchange rate. The interest rate would be based on prevailing

local rates. Such arrangements were called ’back-to-back loans’ – from the UK compa-

ny’s perspective, they involved agreeing to make a series of future USD payments in

exchange for receiving a flow of GBP income.

After exchange controls were removed in 1979, such loans were replaced by cur-

rency swaps. These need not involve two companies directly. In general terms, a cur-

rency swap is a contract between two parties (e.g. between a bank and an overseas

investor) to exchange payments denominated in one currency for payments denomi-

nated in another. A simple example will illustrate this.

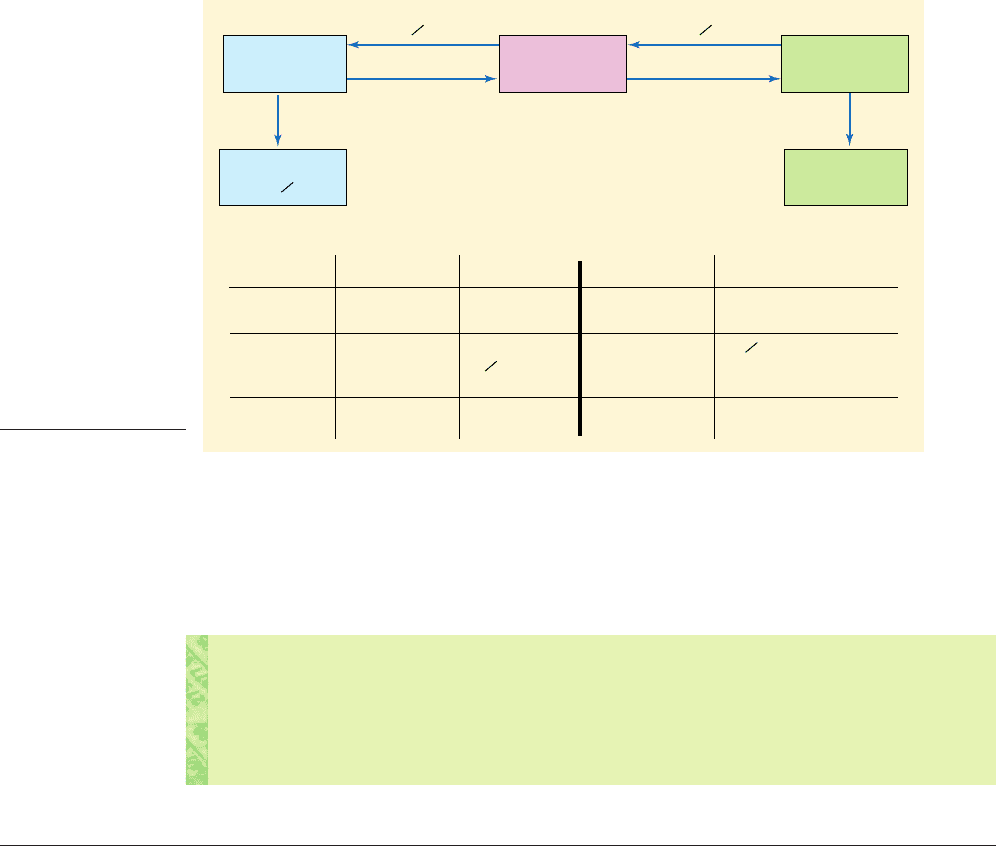

How currency swaps work

Currency swaps are complex. In particular, they require matching up two companies’

mutual requirements in terms of type and amount of currency required and term of

financing. The final agreement will reflect the bargaining power of the parties involved

and is most viable when each party has a differential borrowing advantage in one cur-

rency which it can transfer to the other. This point is important – a currency swap

almost invariably involves an interest rate swap.

To illustrate the process, consider the example of two companies, ABC and XYZ.

ABC, which can borrow in Swiss Francs (CHF) at 5.5 per cent, is seeking USD

financing of $40 million for three years. The Dutch subsidiary of a US bank is pre-

pared to act as intermediary, which involves finding a suitable matching company

which has a borrowing advantage in USD and is seeking CHF finance. Until the

match is found, the bank will be exposed to currency and interest rate risk, which

it may cover by entering the spot market, or possibly using the options market.

Company XYZ emerges as a suitable swap candidate. (More complex swaps might

involve several participant companies if a directly corresponding currency require-

ment cannot be identified.)

XYZ has a borrowing advantage in USD, being able to borrow at 7 per cent, com-

pared to ABC’s borrowing rate of 7.75 per cent. Conversely, XYZ would have to bor-

row in CHF at 6 per cent. XYZ is seeking CHF finance of 52 million. At the ruling

exchange rate of 1.3 CHF per USD, this is an exact match. With the bank’s interme-

diation, the two companies now agree to swap currencies and assume each other’s

interest rate obligations over a three-year term, with transactions conducted via the

bank. Figure 21.5 shows the structure of the swap and the sequence of transactions.

In reality, the two companies would have to pay rather higher interest rates than

those shown in order to yield a profit margin for the bank, sufficient to compensate

it for assuming the risks of either company defaulting on interest payments or re-

exchange of principal.

There are three legs to such deals:

1 Exchange of principal at spot (either notional or a physical transfer) in order to pro-

vide a basis for computing interest.

2 Exchange of interest streams.

3 Re-exchange of principal on terms agreed at the outset.

The principal is fully hedged, unlike the interest rate payments, which may require

hedging perhaps via the forward market.

In the example, the company benefits from lower interest rates and effectively uses

the superior credit rating of the swap specialist to access cheaper finance. Most cur-

rency swaps are undertaken to exploit such interest rate disparities, whereby one

back-to-back loans

A simple form of a swap where

firms lend directly to each

other to satisfy their mutual

currency requirements

CFAI_C21.QXD 3/15/07 7:47 AM Page 622

.

Chapter 21 Managing currency risk 623

21.10 CONCLUSIONS

The globalisation of world trade has forced financial managers to take a keener interest in

managing foreign exchange exposure. There are three types of exposure: transaction expo-

sure, affecting the flow of cash across a currency frontier; translation exposure, affecting

the value of assets and liabilities denominated in a foreign currency; and economic expo-

sure, which is the impact on long-term cash flows of possible changes in exchange rates.

Not all transactions, assets and liabilities denominated in foreign currencies are nec-

essarily exposed to exchange rate risk. The essential skills in currency management are

to identify the assets and cash flows which are at risk and to devise suitable means of

hedging the risks. It is important to differentiate between hedging techniques internal

and external to the firm. Several financial markets have been developed that allow the

international treasurer to hedge foreign exchange risk, and financial instruments such

as swaps, options, futures and forwards can be used for this purpose.

The international treasurer must decide whether or not exchange rates can be fore-

cast with any degree of reliability. With exchange rates floating freely, research sug-

gests that forecasting is not profitable. However, when governments begin to interfere

with the free market, forecasting has proved to be a profitable activity. The dogged, but

ultimately doomed, commitment by international monetary authorities to support

artificially high or low exchange rates may make forecasting worthwhile.

Company

XYZ

Issues $40 m

at 7%

Issues 52 m CHF

at 5 %

Time

Outset

Years 1–3

Pays

Receives

52 m CHF

$40 m

7% on $40

m

5 % on

52 m CHF

$40

m

52 m CHF

$40m

52

m CHF

5 % on 52

m CHF

7% on $40 m

52

m CHF

$40 m

Pays

Receives

End Year 3

Pays

Receives

ABC

Pays

Receives

Pays

Receives

Pays

Receives

XYZ

The sequence of transactions

7%

5 %

1

2

7%

Intermediary

bank

Company

ABC

1

2

5 %

1

2

1

2

1

2

Figure 21.5

Achieving the swap

Self-assessment activity 21.9

Now return to the introductory case on page 593. Can you now explain the apparently dif-

ferent impact of dollar appreciation on these two firms?

(Answer in Appendix A at the back of the book)

party can pass on to another the benefit of superior credit-worthiness. There are two

main forms of currency swap. In a fixed/fixed swap, one party swaps a stream of fixed

interest payments for a corresponding stream of fixed interest payments in another

currency (as in the above example). In a fixed/floating swap, or cross-currency inter-

est swap, one or both payment streams are on a variable basis, e.g. linked to LIBOR.

fixed/fixed swap

A swap agreement where the

parties agree to swap fixed

interest rate commitments

cross-currency interest

swap

A swap agreement where the

parties agree to swap a fixed

interest rate commitment

for a floating interest rate

CFAI_C21.QXD 3/15/07 7:47 AM Page 623

.

624 Part VI International finance

SUMMARY

This chapter examined the nature and sources of a company’s exposure to the risk of

adverse foreign exchange rate movements. It explained a number of widely used

strategies to hedge or safeguard against these risks, applying techniques both internal

to the firm and also available on external capital markets.

Key points

■ Corporate profitability can be seriously affected by adverse movements in foreign

exchange rates.

■ Currency can be transacted for immediate payment on the spot market or for future

delivery via the forward market.

■ The international treasurer is faced with three kinds of foreign exchange exposure:

transaction exposure, translation exposure and economic exposure.

■ Transaction exposure relates to the likely variability in short-term operating cash

flows: for example, the cost of specific imported raw materials and the income from

specific exported goods.

■ Translation exposure relates to the risk of exchange rate movements altering the

sterling value of assets located overseas or the sterling value of liabilities due to be

settled overseas.

■ Economic exposure refers to the ongoing risks incurred by the company in its

choice of long-term contractual arrangements, such as licensing deals or decisions

to invest overseas. These risks are the long-term equivalent of transaction exposure.

■ Companies that trade internationally should devise a foreign exchange strategy.

■ The strategy might depend on the treasurer’s belief in the validity of various inter-

national trade theories: Purchasing Power Parity (PPP), Interest Rate Parity (IRP),

the Expectations Theory and the Open Fisher Theory.

■ PPP states that, allowing for the prevailing exchange rate, identical goods must sell

for a common price in different locations. If inflation rates differ between locations,

exchange rates will adjust to preserve the Law of One Price.

■ IRP asserts that any differences in international interest rates are a reflection of

expected exchange rate movements, so that the interest rate offered in a location

whose currency is expected to depreciate will exceed that in an appreciating cur-

rency location by the amount of the expected exchange rate movement.

■ The forward premium or discount should equal the expected rate of appreciation

or depreciation of a currency.

■ The Open Fisher Theory asserts that investment in different countries will offer the

same expected real interest rate, so that differences in nominal rates of interest can

be explained by expected differences in rates of inflation.

■ Once the exposure position of the company is identified and measured, the treas-

urer must devise a hedging strategy to control the foreign exchange risk faced by

the firm.

■ Many apparent exposures are often self-hedging: for example, holdings of plant

and machinery that can be traded internationally.

■ Generally, internal hedging techniques are cheaper to apply than using the external

markets, which offer various financial instruments for hedging currency risks.

■ Hedging cash flows for long-term investment projects is more problematic, but can

be handled by internal methods.

CFAI_C21.QXD 3/15/07 7:47 AM Page 624