Pike Robert, Neal Bill. Corporate finance and investment: decisions and strategy

Подождите немного. Документ загружается.

.

Chapter 21 Managing currency risk 595

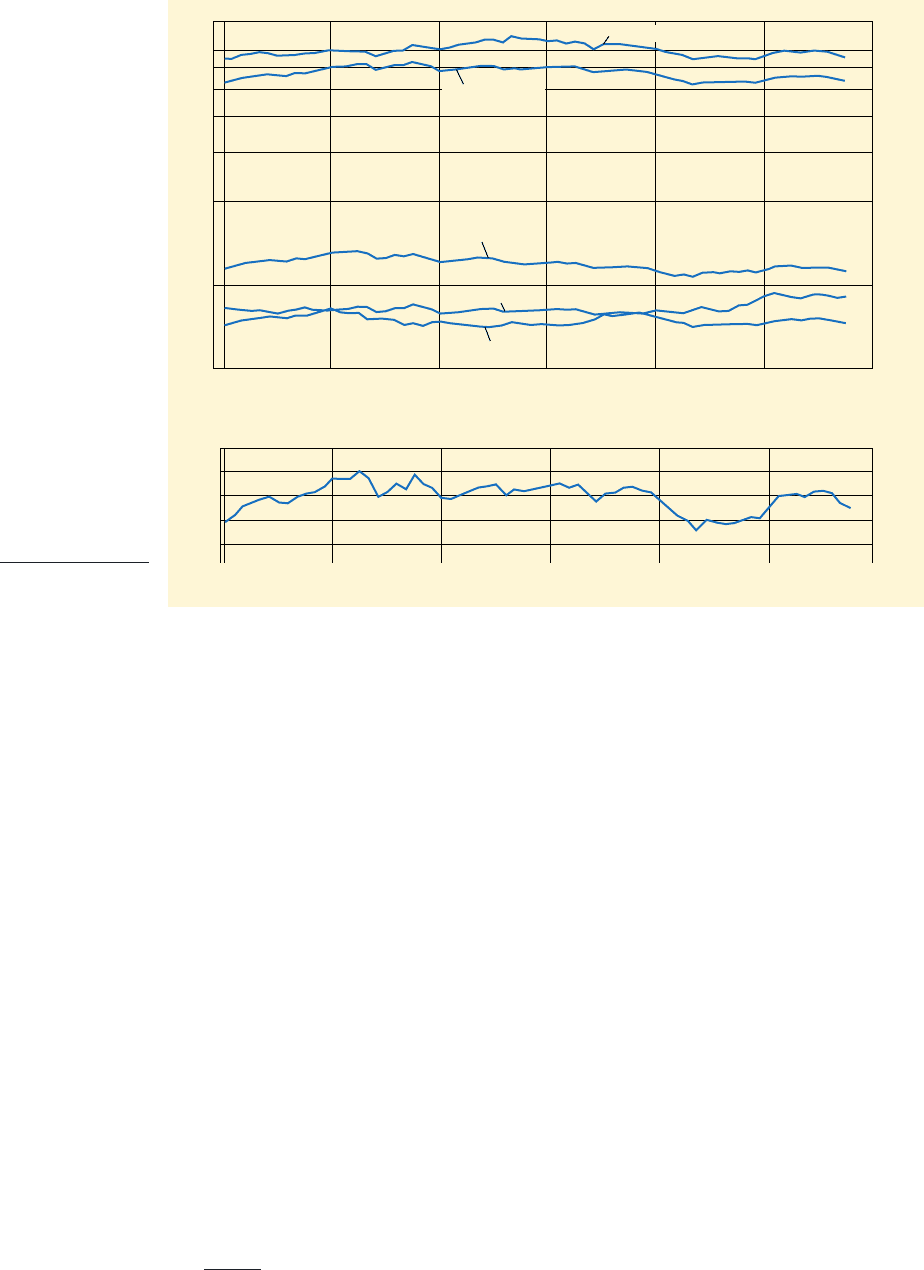

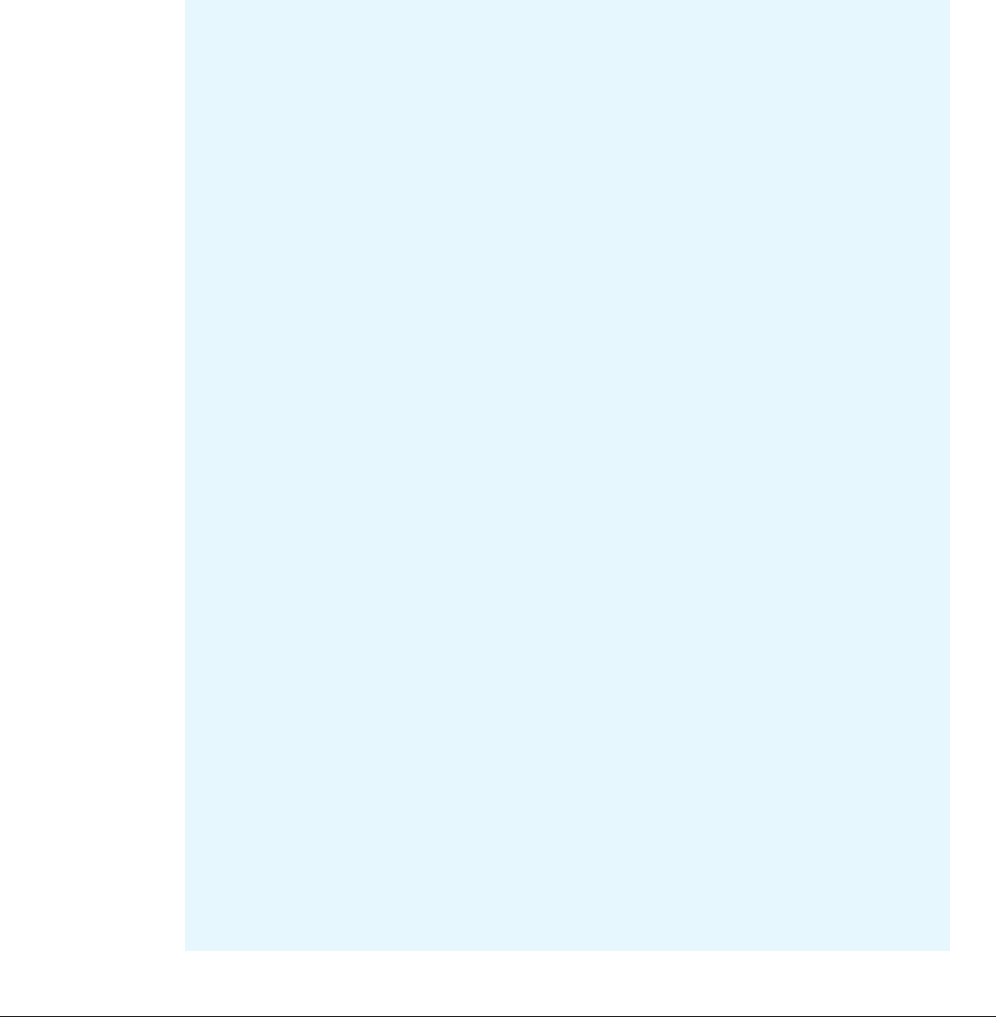

Figure 21.1

Sterling exchange

rates, 1999–2004*

Danish Kronor

14

12

10

8

6

4

2

1

14

12

10

8

6

4

2

1

115

110

105

100

95

115

110

105

100

95

Sterling exchange rate index Average 1990 = 100

Euro

Swiss franc

Swedish Kronor

US dollar

Source: Economic Trends, January 2005.

purchases is hedged by selling or purchasing foreign currency forward.’ But it

acknowledges that ‘foreign exchange contracts do not generally extend beyond 12

months’.

Not all companies are so prudent. In March 1998, Britain’s largest maker of cara-

vans, ABI Leisure plc, went into receivership. The trigger was the insolvency of its

French distributor in January 1998, yet well before this event, ABI was reeling from

foreign currency problems.

In August 1997, several senior ABI managers resigned after an internal investiga-

tion revealed major errors in foreign currency management. ABI made more than half

of its profits overseas, yet not only had foreign currency exposures not been hedged,

excess foreign currency balances had not been converted back into sterling at a time

when the pound’s upward surge was undermining earnings. As a result, an expected

profit for 1997 of was transformed into a reported loss of – a

case of a basically sound company brought down by financial mis-management, i.e.

failure to hedge.

Some firms actively court foreign exchange risks. In October 2003, Nintendo,

the Japanese videogame producer, reported its first-ever loss of large-

ly as a result of the strength of the yen. Nintendo keeps much of its foreign earn-

ings in local currencies to take advantage of better interest rates outside Japan.

This policy resulted in losses of some on foreign currency transac-

tions as the yen rose strongly against the US dollar. We will see later why such a

policy is misguided.

The task of this chapter is to explain the various types of exchange risk and how

they can be managed.

£215 million

£16 million,

£5.6 million£4.5 million

*NB – based on a log scale (Japanese yen not shown)

CFAI_C21.QXD 3/15/07 7:47 AM Page 595

.

596 Part VI International finance

Self-assessment activity 21.1

What is the distinction between a foreign exchange ‘speculator’ and a ‘hedger’? How would

you describe Corus, ABI and Nintendo?

(Answer in Appendix A at the back of the book)

21.2 THE STRUCTURE OF EXCHANGE RATES: SPOT AND

FORWARD RATES

*

Most currency transactions are conducted between firms and individuals on one hand,

and banks which make a market, i.e. quote an exchange rate in a variety of currencies,

on the other. As in any other market, the two parties set a price – in this case, the

exchange rate is the price of one currency in terms of another. There are two ways of

quoting the resulting price, which is often a source of confusion:

■ The direct quote gives the exchange rate in terms of the number of units of the

home currency required to purchase one unit of the foreign currency.

■ The indirect quote gives the price in terms of how many units of the foreign cur-

rency can be bought with one unit of the home currency.

In London, dealers usually use the indirect quote, (although this is changing). When we

hear that the sterling/US dollar exchange rate (the so-called ‘cable rate’) is $2.00, this

means that each pound can buy two units of the ‘greenback’, the US dollar. The corre-

sponding direct quote would be which indicates measures how many units of

sterling that one US dollar can purchase. The direct quotation is simply the reciprocal

of the indirect quotation.

In continental Europe, the direct quotation is used. In the USA, dealers generally

use the indirect quotation when dealing with European banks, except for ones in

London.

It is also misleading to talk of ‘the exchange rate’ between currencies because there

always exists a spectrum of rates according to when delivery of the currency transact-

ed is required.

The simplest rate to understand is the spot market rate that the bank quotes for

‘immediate’ (in practice, within two days) delivery. For example, on 19 October,

2004, the closing quotation for the spot rate for Swiss Francs (CHF) against sterling

(GBP) was

The first figure is the rate at which the currency can be purchased from the bank and

the higher one is the rate at which the bank sells CHF. The difference (0.16 centimes),

or spread, provides the bank’s profit margin on transactions. At times of great volatil-

ity in currency markets, the spread usually widens to reflect the greater risk in cur-

rency trading.

It is also possible to buy and sell currency for delivery and settlement at specified

future dates. This can be done via the forward market, which sets the rate applicable

for advance transactions. On the above day, the following terms were quoted for CHF

delivery in one month:

87.0 75.0 prem

2.2172 2.2188

£0.50

*Throughout the following sections, we use standard international abbreviations for currencies (based

on SWIFT money transmission codes), e.g. pound etc. We also fre-

quently use the abbreviation FX to denote foreign exchange (rates).

US dollar USD,sterling GBP,

CFAI_C21.QXD 3/15/07 7:47 AM Page 596

.

Chapter 21 Managing currency risk 597

Self-assessment activity 21.2

The closing spot rates and forward quotations on 9 November 2001 for GBP versus two

other currencies were as shown below. Calculate the forward outrights.

Closing rates Forward quotation

Eurozone dis

Canada prem

Source: Guardian, 19 October 2004.

(Answer in Appendix A at the back of the book)

49.0 39.02.2617 2.2628

15.0 17.01.4406 1.4413

The numbers are referred to as ‘points’ with each point representing 1 per cent of a

centime, or 0.0001 of a CHF. The ‘prem’ means that the CHF is selling at a forward pre-

mium, i.e. it is ‘predicted’ to appreciate versus sterling.

The quotation given is not an exchange rate as such, but a ‘prediction’ of how the

CHF spot exchange rate will change over the relevant period: in this case, appreciate

against sterling. The rate itself (called an ‘outright’) is found by deducting the expect-

ed premium from the spot rate (or adding a discount to it). In this case, subtraction is

required because the market expects that one unit of sterling will purchase fewer CHF

in the future, i.e.

Notice that the spread widens from 0.16 centimes (or 16 points) to 0.28 centimes

(28 points). This is a reflection of the greater risk associated with more distant trans-

actions. An important point to note is that, when a forward transaction is entered

into, there exists a contractual obligation to deliver the currency that is legally bind-

ing on both parties. The rate of exchange incorporated in the deal is thus fixed.

Hence, a forward contract is a way of locking in a specific exchange rate, and is

appealing when there is great uncertainty about the future course of exchange rates.

From spot to forward

Spot and forward rates for other currencies against GBP are thus connected as follows:

Forward rates, therefore, appear to be an assessment of how the currency market

expects two currencies to move in relation to each other over a specified time period,

and are sometimes regarded as a prediction of the future spot rate at the end of that

period. As we shall see, this is not entirely a correct interpretation.

The reader may wish to visit the website (www.bis.org) of the Bank of International

Settlements (BIS) for statistics on the volume of trading on these markets. The average

daily turnover in April 2004 was US$621 billion in spot transactions and US$208 billion

in outright forward transactions (BIS, 2004).

Forward rate spot rate c

plus forward discount 1denoted by ‘dis’2

OR

minus forward premium 1denoted by ‘prem’2.

Spot

2.2172 2.2188

F>w premium

ˇˇˇ 10.0087 0.00752

2.2085 2.2113

CFAI_C21.QXD 3/15/07 7:47 AM Page 597

.

598 Part VI International finance

21.3 FOREIGN EXCHANGE EXPOSURE

Foreign exchange exposures occur in three forms:

1 Transaction exposure

2 Translation exposure

3 Economic exposure

■ Transaction exposure

Transaction exposure is concerned with the exchange risk involved in sending money

over a currency frontier. It occurs when cash, denominated in a foreign currency, is con-

tracted to be paid or received at some future date.

For example, a UK company might contract to buy US$45 million worth of com-

puter chips from a US company over a three-year period. When the contract is set up,

the rate of exchange between the dollar and the pound is US$1.50 to but what will

happen in a year or two’s time? What if the rate of exchange alters to US$1.25 to in

a year’s time?

The US$45 million was equivalent to at the beginning of Year 1,

but after the fall in the value of the pound against USD the cost of the contract in GBP

rises to Such a substantial rise in costs could easily eliminate the

UK company’s profit margin.

Similar risks apply to expected cash inflows. If the UK company was due to receive

50 million Canadian dollars (CAD) and the CAD actually rose from C$2.2 to to

C$2.0 to the UK company would gain on the contract (i.e. the differ-

ence between the expected income of (C$50/2.2) and the actual income of

(C$50/2.0)).

Thus, unexpected changes in exchange rates can inflict substantial losses (and pro-

vide unexpected gains) unless action is taken to control the risk.

■ Translation exposure

Translation exposure is the exposure of a multinational’s consolidated financial accounts

to exchange rate fluctuations. If the assets and liabilities of, say, the Australian subsidiary

of a UK parent firm are translated into sterling at year-end at a rate different from the

start-year rate, exchange losses or gains will be reflected in the new Balance Sheet, and

will also affect the Profit and Loss Account. Similarly, the earnings of the subsidiary

when translated into sterling are also affected by exchange rate changes.

Whereas transaction exposure is concerned with the effect on cash flows into the par-

ent company’s currency, translation exposure affects Balance Sheet values, and to a less-

er extent (because assets typically exceed profits or cash flow in magnitude) the Profit

and Loss Account.

Examples of items that a treasurer might consider to be subject to translation exposure

if denominated in foreign currency are debts, loans, inventory, shares in foreign compa-

nies, land and buildings, plant and equipment, as well as the subsidiary’s retained profits.

If the CAD falls in value by 3 per cent between the date an export contract is signed

and the date the dollars are received in the UK, this represents a real loss to the UK

company if no action is taken to hedge the exchange risk. But is a real loss sustained

by a UK company with a Canadian subsidiary if C$30 million of its capital stock or

C$10 million of its inventory are being held in Toronto at the time of a devaluation of

the CAD against GBP? This question has been much debated during the last 30 years.

It is often argued that because translation risk is a purely accounting issue, i.e. it

relates to past transactions, it has no impact on the economic value of the firm and thus

there is no need to hedge, i.e. people already know about it in an efficient market.

However, it may become a problem if there are plans to realise assets held overseas

£25 m

£22.72 m

£2.28 million£1,

£1

$45 m>1.25 £36 m.

$45>1.50 £30 m

£1

£1,

translation exposure

Exposure to the risk of adverse

currency movements affecting

the domestic currency value of

the firm’s consolidated finan-

cial statements

CFAI_C21.QXD 3/15/07 7:47 AM Page 598

.

Chapter 21 Managing currency risk 599

and/or if earnings cannot be profitably reinvested in the location where they arise,

and the parent wishes to repatriate them. (Arguably, these upcoming cash movements

essentially reflect a transaction exposure rather than a translation exposure.) Moreover,

a policy of ‘benign neglect’ tends to overlook possible effects on key performance

measures and ratios, especially EPS, in relation to reporting overseas earnings, and

gearing, via reported asset and liability values.

A multinational company may have significant borrowings in several currencies. If

foreign currencies have been used to acquire assets located overseas, then, should GBP

decline in value, any adverse effect on the GBP value of borrowing will be offset by a

beneficial effect on the sterling value of overseas assets. In this respect, the overseas

borrowing is ‘naturally’ hedged, and no further action is required.

However, the UK company may face limits on its total borrowing which could be

violated by adverse foreign exchange rate movements. For example, a weaker domes-

tic currency, relative to currencies in which debt is denominated, could adversely

affect borrowing capacity and the cost of capital.

Say a company has debt expressed in both GBP and USD, as in the following capi-

tal structure:

Equity

Loan stock: sterling

Loan stock: (US$80 m)

Total

The valuation of the USD loan is translated at the exchange rate of the rate

ruling at the end of the financial year. At this juncture, the gearing ratio (debt-to-equity)

is Imagine there is a covenant attaching to the sterling

loan which limits the gearing ratio to 30 per cent. If GBP falls to, say, the

company has a problem. Its USD-denominated debt now represents a liability of

and the debt-to-equity ratio rises to:

The borrowing limit has been breached. To avoid this situation occurring, the com-

pany could borrow in a range of currencies that might move in different directions rel-

ative to GBP, with adverse movements offset by favourable ones. For example, British

Airways, a highly geared company, borrows in yen (JPY) and USD as well as GBP, thus

mixing a so-called ‘currency cocktail’.

■ Economic exposure

Economic exposure is also known as long-term cash flow or operating exposure.

Imagine a UK company which buys goods and services from abroad and sells its goods

or services into foreign markets. If the exchange rate between sterling and foreign cur-

rencies shifts over time, then the value of the stream of foreign cash flows in sterling

will alter through time, thus affecting the sterling value of the whole operation.

In general, a UK company should try to buy goods in currencies falling in value

against GBP and sell in currencies rising in value against GBP.

Of course, the transactions exposure could be eliminated by denominating all its

contracts in GBP, which shifts the risk to the trading partner. However, this tactic can-

not remove economic exposure. The foreign company will convert the GBP cost of

purchases and sales into its own currency for comparison with purchases or sales from

companies in other countries using other currencies. Management of economic expo-

sure involves looking at long-term movements in exchange rates and attempting to

hedge long-term exchange risk by shifting out of currencies that are moving to the

detriment of the long-term profitability of the company. It is worth noting that many

economic exposures are driven by political factors, e.g. changes in overseas govern-

ments resulting in different economic policies such as taxation.

1£50 m £61.5 m2 £350 m 32%

$80 m>1.30 £61.5 m,

$1.30:£1,

1£100 m>£350 m2 28.5%.

$1.60:£1,

£450 m

£50 m

£50 m

£350 m

CFAI_C21.QXD 3/15/07 7:47 AM Page 599

.

600 Part VI International finance

Self-assessment activity 21.3

Distinguish between translation, transaction and economic exposure.

(Answer in Appendix A at the back of the book)

21.4 SHOULD FIRMS WORRY ABOUT EXCHANGE RATE CHANGES?

According to the theory of Purchasing Power Parity (PPP), the answer to this question

is ‘no’.

PPP says that the purchasing power of any currency should be equivalent in any

location. It is based on the Law of One Price, which asserts that identical goods must

sell at the same price in different markets, after adjusting for the exchange rate. For

example, if the market rate of exchange between USD and GBP is a micro-

computer could not sell for very long at simultaneous prices of, say, in London

and $2,000 (i.e. ) in New York. People would buy in the ‘cheap’ market (New

York) and ship the goods to London, thus tending to equilibrate the two prices at, say,

a London price of and a New York price of $2,080 (In reality, transport

and other transaction costs may prevent the precise operation of PPP.)

The Law of One Price states that, for tradeable goods and services, the

■ Exchange rate changes

If relative price levels change, for example, UK prices inflate at 10 per cent p.a. and US

prices inflate at 3 per cent p.a., the Law of One Price states that there should be a fall

in the value of the against the USD of about 7 per cent, in order to restore PPP.

Taking our microcomputer example, after one year, the price will rise to

while the US price becomes This implies that the

exchange rate should move to:

which represents a depreciation in GBP of 6.4 per cent.

If foreign exchange markets operate freely without government intervention, goods

that can be easily traded on international markets, such as oil, are highly likely to obey

the Law of One Price, although transport costs between markets may explain a con-

tinued price discrepancy. However, not all goods can be easily transported. Most

notably, with land and property, which are physically impossible to shift, a sustained

price discrepancy may apply between markets. In the longer term, however, even

these differentials may close as investors and property speculators perceive that one

market is cheap relative to the other.

PPP may be expected to operate broadly in the longer term for most goods and

services, although it can be distorted by government intervention in the foreign

exchange markets and the formation of currency blocs. The authorities in these cases

are attempting to smooth out the effects and hence minimise the dislocation to busi-

ness activity that sudden swings in currency values might cause. However, while

exchange controls and official intervention can delay any adjustment necessary to

reflect differential rates of inflation, the required change will eventually take place.

Accepting PPP and the Law of One Price, we arrive at a remarkable conclusion

regarding the need to hedge FX risks – there is no need to worry! The Stonewall plc

example explains the mechanics.

$2,142

£1,430

$1.5:£1

$>£$2,080 11.032 $2,142.£1,430,

£1,30011.12 £

£

1£ price of a good $>£ exchange rate2 USD price of a good

1£1,3002.£1,300

£1,250

£1,500

$1.6:£1,

CFAI_C21.QXD 3/15/07 7:47 AM Page 600

.

Chapter 21 Managing currency risk 601

Example: Stonewall plc

A British-based firm, Stonewall plc has a factory in Baltimore, USA. It plans to produce

and sell goods to generate a net cash inflow of $180 million at today’s prices over the

coming trading year. For simplicity, we assume all transactions are completed at year-

end, and that any price adjustments resulting from inflation also occur at year-end.

At the current exchange rate of US$1.50 vs. the sterling value of its planned

Stonewall is worried about the $US falling due to the

annual rate of inflation in the US of 6 per cent compared to 3 per cent in the UK.

Concern about exposure to foreign exchange risk seems justified – with these infla-

tion rates, PPP predicts the US$ will decline to:

At this exchange rate, the sterling value of the US$ cash flow is

a fall of about 3 per cent on the start-year valuation. But should sleep be lost

over this?

The answer is ‘yes’ if selling prices within the USA remained static. However, prices

within the USA are not static – the reason why the FX rate will change is due to infla-

tion at a higher rate in the USA relative to the UK.

With US prices rising at 6 per cent, the US$ cash flow ought to rise to

Converted to sterling at the year-end rate, this is worth

This is precisely equal to its sterling-denominated value at the end of one

year with UK price inflation at 3%

So what has been lost from inflation affecting the relative value of sterling and $US?

The answer is nothing if PPP operates! Should the firm take precautions against FX

exposure? The answer is ‘no’ – why should it bother when it is automatically protect-

ed by market adjustments? Should the firm try to forecast future rates of exchange, e.g.

by comparing the respective inflation rates? It could, but again, it is a waste of time, at

least in theory, as the rate of $1.544 should already be quoted in the market for one-

year forward deals.

However, it is not always this simple. In reality, prices rise in a continuous process

rather than in a series of end-year adjustments. The policy of benign neglect only

works if prices of the traded goods are adjusted pari passu as prices in general alter and

the exchange rate ‘crawls’ in the appropriate direction, by the appropriate amount and

if the movement is synchronised.

In reality, FX rates adjust in response to relative inflation rates at the national level,

as measured by a basket of goods. The basket may well inflate at a different rate from

the goods traded. Indeed, competitive conditions may be so powerful that firms may

be unable to raise prices even to compensate for inflation. For these reasons, most

firms seek protection against FX movements.

1£120 m 1.03 £123.6 m2.

£123.6 m.

1$190.8 m>1.5442 $190.8 m.

$180 m 11.062

£116.58 m,

1$180 m>1.5442

$1.50 11.06>1.032 $1.544 after one year.

sales 1$180 m>1.502 £120 m.

£1,

21.5 ECONOMIC THEORY AND EXPOSURE MANAGEMENT

The first step in currency management is to identify the transaction, translation and

economic exposure to which the company is subject. The second step is to decide how

the exposure should be managed. Should the risk be totally hedged, or should some

degree of risk be accepted by the company?

The international treasurer must devise a hedging strategy to control exposure to

exchange rate changes. The precise strategy adopted is likely to be influenced by cer-

tain economic theories that have evolved over the last century, and the extent to which

they are considered valid. These theories are as follows:

1 The Purchasing Power Parity Theory (PPP).

2 The Expectations Theory.

CFAI_C21.QXD 3/15/07 7:47 AM Page 601

.

602 Part VI International finance

3 The Interest Rate Parity Theory (IRP).

4 The Open, or International, Fisher Theory.

5 The international version of the Efficient Markets Hypothesis (EMH).

We will provide brief sketches of these important contributions to the literature of

international economics.

■ Purchasing Power Parity (PPP)

In the last section we encountered the Law of One Price and Purchasing Power Parity.

PPP and the Law of One Price have important implications for the relationship between

spot and forward rates of exchange. If people possessed perfect predictive ability, and

the rates of inflation were certain, the market could specify with total precision the

appropriate exchange rate between USD and GBP for delivery in the future (i.e. the for-

ward rate of exchange).

More specifically, PPP states that foreign exchange rates will adjust in response to

international differences in inflation rates and so maintain the Law of One Price. Thus

the forward rate should be:

If the spot rate between sterling and the US$ is $1.60 vs. and people expect UK

inflation at 10 per cent and only 3 per cent in the USA, this implies a one-year forward

rate of:

In this example, the forward rate is predicting the spot rate that should apply in the

future. If buyers and sellers of foreign exchange can rely on the currency markets to

operate in this way, the risks presented by differential inflation rates could be removed

by using the forward market. Forecasting future spot rates would then be a trivial

exercise.

Unfortunately, the forward rate has been shown to be a poor predictor of the future

spot rate. Yet it has also been shown to be an unbiased predictor in that, although the

forward rate often underestimates and often overestimates the future spot rate, it does

not consistently do either. In the long run, the differences between the forward rate

prediction for a given date and the future spot rate on that date sum to zero. If the for-

ward market operates in this way, firms can regard today’s forward rate as a reason-

able expectation of the future spot rate. This is the Expectations Theory.

Levich (1989) found that in the early 1980s the forward rate of GBP vs. USD tended

to underestimate the strength of the USD, but during 1985–87, the forward rate over-

estimated the strength of the dollar. However, taking the 1980s as a whole, the data

suggested that the forward rate on average was very close to the future spot rate.

$1.6 : £1 spot rate 11.032> 11.102 $1.5 : £1.

£1,

Forward rate Spot rate

11 US inflation rate2

11 UK inflation rate2

Self-assessment activity 21.4

Use the Law of One Price and PPP to predict the relative local prices of a cup of coffee and

the future sterling/dollar spot rate under the following conditions:

■ Price now in

■ Price now in

■ Exchange rate for USD vs.

■ UK inflation is 4 per cent; US inflation is 2 per cent

(Answer in Appendix A at the back of the book)

GBP $1.50 : £1

London £1.00

New York $1.50

CFAI_C21.QXD 3/15/07 7:47 AM Page 602

.

Chapter 21 Managing currency risk 603

■

Interest Rate Parity (IRP)

Interest Rate Parity is concerned with the difference between the spot exchange rate

(the rate applicable for transactions involving immediate delivery) and the forward

exchange rate (the rate applicable for transactions involving delivery at some future

specified time) between two currencies. Suppose the spot rate for USD to GBP is

and the one-year forward rate is Here, the USD is selling at a 10 cent

premium – it is more expensive in terms of GBP for forward deals. The currency mar-

ket thus expects the USD to rise in value against GBP during the year by about 6.7%.

IRP converts this expected rise in the value of the USD against GBP into a difference

in the rate of interest in the two countries. The rate of interest on one-year bonds denom-

inated in USD will be lower than bonds otherwise identical in risk, but denominated in

GBP. The difference will be determined by the premium on the forward exchange rate.

If depreciation of GBP against USD is expected, this should be reflected in a comparable

interest rate disparity as borrowers in London seek to compensate lenders for exposure

to the risk of currency losses. In other words, interest rates offered in different locations

tend to become equal, to compensate for expected exchange rate movements.

The equilibrium relationship that operates under IRP is given by:

For example, if the interest rate available in London is 12 per cent p.a., the figures

in our example will indicate a US interest rate as follows:

So the US interest rate is (i.e.) 5% p.a.

This is an interesting result. A New Yorker attracted by high UK interest, who is

tempted to place money on deposit for a year in London, will find that what is gained

on the interest rate differential will be lost on the adverse movement of GBP against

USD over the year. To appreciate this ‘swings and roundabouts’ argument, consider the

following figures, which relate to the two investment options that the investor faces:

1 Invest in GBP:

January Convert $1,000 into GBP

Invest for one year in London at 12%:

December Convert back to USD @ 1.5 $1,050.

vs.

2 Invest in USD:

January Invest $1,000 in New York @ 5% $1,050 in December.

Clearly, the rational investor should be indifferent between these two alternatives,

unless interest rates are expected to fall in New York relative to those in London, or the

forward rate is not a good predictor of the spot rate in one year’s time.

One reason why this predictive ability is weakened in practice is intervention in for-

eign exchange markets by governments. In the absence of such intervention, exchange

rates seem to operate so as to smooth out interest rate disparities, but with the creation

of artificial market inefficiencies, there often exist opportunities to arbitrage: for exam-

ple, borrowing money at low interest rates in one market, hoping to repay it before IRP

fully exerts itself. However, many UK corporate treasurers have been wrong-footed by

borrowing apparently cheap money overseas, but having to repay at exchange rates

quite different from those envisaged when raising the loan, because market forces

have eventually asserted themselves to remove the interest rate discrepancy.

£62511.122 £700.

@ 1.6 £625.

11.05 12 .05

11 US interest rate2 1.12

1.5

1.6

1.05

Forward rate Spot rate

11 US interest rate2

11 UK interest rate2

$1.5:£1.$1.6:£1,

CFAI_C21.QXD 3/15/07 7:47 AM Page 603

.

604 Part VI International finance

This equalising process is effected by financial operators called arbitrageurs, who

act upon any short-term disparities. For example, if in the previous example the inter-

est rate disparity were 3 per cent, it would pay to borrow in GBP and purchase US

bonds in London.

Checking the agios: the scope for arbitrage

When currency and money markets are in equilibrium, any difference in interest rates

available through investment in two separate locations should correspond to the dif-

ferential between the spot and forward rates of exchange. The interest rate differential

is called the interest agio, and the spot/forward differential is called the exchange

agio. If these are not equal, arbitrageurs have scope to earn profits.

Consider this example. An investor has to invest for a year. The interest

rate is 8 per cent in London and 5 per cent in New York. The current spot rate of

exchange (ignoring the spread) is and the dollar sells at a one year forward pre-

mium of 5 cents, i.e. the forward outright is What is the best home for the

investor’s money?

He could invest the where interest rates are highest, i.e. place the

on deposit in London to earn interest over one year, thus increasing his cash hold-

ing to Alternatively, he could engage in covered interest arbitrage. This

works as follows:

1 Convert at spot into USD, i.e.

2 Invest $1.6 m at 5 per cent for one year, i.e.

3 Meanwhile, sell this forward over one year, i.e. for delivery in one year:

The guaranteed proceeds from arbitrage are greater by However, this situa-

tion cannot last for very long. As other investors spot the scope for risk-free profits and

rush into the market, their actions will quickly eliminate the opportunity. This is why

spot/forward relationships almost always reflect prevailing interest rate differentials.

For this reason, the forward rate is the product of a technical relationship linking the spot

rate to relative interest rates, rather than a prediction in the true sense.

Equilibrium requires equality between the exchange agio and the interest agio, i.e.

the spot/forward differential should equal the interest rate differential:

where is today’s forward quotation, is today’s spot quotation, is the interest rate

available by investment in USD, and is the interest rate available by investment in GBP.

Note that the interest agio is found by discounting the interest differential over one

year at the UK interest rate. If the period concerned were less than a year – say, three

months – the three-monthly interest rate would be used.

In the above example, the two agios are:

i.e.:

3.125% vs. 2.778%

1.55 1.60

1.60

vs.

0.05 0.08

1.08

i

£

i

$

S

o

F

o

F

o

S

o

S

o

i

$

i

£

1 i

£

£3,871.

$1.68 m>1.55 £1,083,871

$1.6 m 1.05 $1.68 m

£1 m 1.60 $1.6 m

£1 m

£1.08 million.

£80,000

£1 million£1 million

$1.55:£1.

$1.6:£1

£1 million

arbitrageurs

Arbitrageurs attempt to exploit

differences in the values of

financial variables in different

markets e.g. borrowing in a

low cost location and investing

where interest rates are rela-

tively high (interest arbitrage)

covered interest arbitrage

Using the forward market to

lock in the future domestic

currency value of a transaction

undertaken to exploit an inter-

est arbitrage opportunity

CFAI_C21.QXD 3/15/07 7:47 AM Page 604