Pike Robert, Neal Bill. Corporate finance and investment: decisions and strategy

Подождите немного. Документ загружается.

.

Chapter 21 Managing currency risk 605

This inequality signifies the scope for risk-free profit via covered interest arbitrage.

Uncovered arbitrage is where the arbitrageur does not sell forward, but takes a gamble

on how the spot rate changes over the year. In the example, he or she would earn bigger

profits if the spot rate in one year turned out to be lower than This distinction

highlights the difference between hedging and speculation. However, although differ-

ences in agios can persist for a while, transactions costs may preclude profitable arbitrage.

$1.55:£1.

Self-assessment activity 21.5

If interest rates are higher in London than New York by 2.5 per cent p.a. and today’s spot

rate is $1.4455 vs. what would you expect the three-month forward quotation to be if

IRP applied?

(Answer in Appendix A at the back of the book)

£1,

■ The Open Fisher Theory

The ‘Open Fisher’ Theory, sometimes called the ‘International Fisher’ Theory, claims

that the difference between the interest rates offered on identical bonds in different cur-

rencies represents the market’s estimate of the future changes in the exchange rates

over the period of the bond. The theory is particularly important in the case of fixed-

rate bonds having a long life to maturity, say, five to fifteen years’ duration.

Suppose that a firm wishes to raise for a one-year period. It approaches

a bond broker and is offered the following loan alternatives:

1 A loan in GBP at 12 per cent p.a.

2 A USD loan at 5 per cent p.a.

The Open Fisher Theory asserts that the interest rate difference represents the mar-

ket’s ‘best estimate’ of the likely future change in the exchange rates between the cur-

rencies over the next year. In other words, the market expects GBP to depreciate by

around 7 per cent against USD over the next year.

To understand this, recall the relationship between ‘real’ and ‘money’ interest rates

encountered in Chapter 6. The Fisher Effect concerns the relationship between expec-

tations regarding future rates of inflation and domestic interest rates – investors’

expectations about future price level changes will be translated directly into nominal

market interest rates. In other words, rational lenders will expect compensation not

only for waiting for their money, but also for the likely erosion in real purchasing

power. For example, if in the UK, the real rate of interest that balances the demand and

supply for capital is 5 per cent, and people in general expect inflation of 10 per cent

p.a., then the nominal rate of interest will be about 15 per cent (actually 15.5 per cent).

Recall that real and nominal interest rates are connected by the Fisher formula:

where P is the real interest rate, I is the expected general inflation rate and M is the mar-

ket interest rate.

The Open Fisher Theory asserts that all countries will have the same real interest

rate, i.e. in real terms, all securities of a given risk will offer the same yield, although

nominal or market interest rates may differ due to differences in expected inflation

rates. It can be more precisely expressed by amalgamating the PPP and IRP theories:

11 US inflation rate2

11 UK inflation rate2

Spot rate

11 US interest rate2

11 UK interest rate2

Spot rate Forward rate

11 P2

11 I2 11 M2

£50 million

uncovered arbitrage

Interest arbitrage without the

use of the forward market to

lock in future values of

proceeds

CFAI_C21.QXD 3/15/07 7:47 AM Page 605

.

606 Part VI International finance

For example, suppose the London and New York interest rates are 12 per cent and 5

per cent, respectively, as quoted by our bond brokers, and the respective expected rates

of inflation are 10 per cent and 3 per cent. If the spot rate is then the Open Fisher

Theory predicts a depreciation in the pound as expressed by the forward rate thus:

In other words, when the spot rate is this combination of inflation rates and

interest rates is consistent with a forward rate of as calculated earlier.

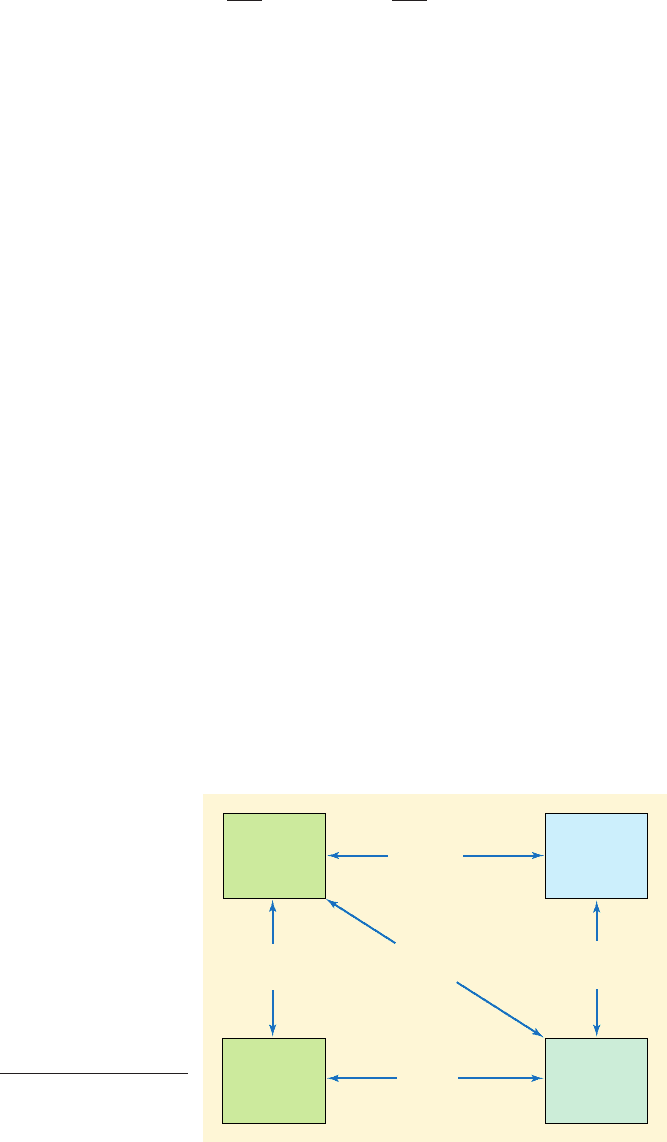

These economic theories are interlocking or mutually reinforcing, as shown by the

‘equilibrium grid’ in Figure 21.2. Several other factors, such as the timing of the

change, tax and exchange controls can also affect the relative movement of curren-

cies, but the major factor influencing the movements in exchange rates is claimed to

be the expected future movement in inflation rates, which is signalled by current dif-

ferentials in interest rates.

■ The international (Efficient Markets Hypothesis EMH)

The EMH claims that, in an efficient market, all publicly-available information is very

quickly incorporated into the value of any financial instrument. In other words, past

information is of no use in valuation. Any change in value is due to future events,

which are, by definition, unknowable at the present time. Past trends in exchange rates

cannot provide any useful information to assist in predicting future rates.

This theory applies only to information-efficient markets. Currencies operating

within a system of fixed average rates (or maximum permitted bands of fluctuation),

such as the former European exchange rate mechanism (ERM), are operating within

a controlled market, so the EMH will not apply fully. Where markets are information-

efficient, the EMH casts doubt on the ability of treasurers to make profits out of using

exchange rate forecasts.

This section of the chapter has provided a brief sketch of some economic theories rel-

evant to devising a foreign exchange management strategy. We will shortly try to

design such a strategy by applying these theories to the various types of foreign

exchange exposure outlined earlier. But because these theories may not always apply

(and some people think they rarely, if ever, apply), it is helpful to examine approach-

es to forecasting FX rates.

$1.5:£1,

$1.6:£1,

1.05

1.12

1.6 1.5

1.03

1.10

1.6

$1.6:£1,

Inflation

rate

differentials

Open

Fisher

Theory

Expected

change in

exchange

rate

Forward

premium or

discount

Interest

rate

differentials

Purchasing

Power

Parity

Theory

Interest

Rate

Parity

Theory

Expectations

Theory

Fisher

Effect

Figure 21.2

Interlocking theories

in international

economics

CFAI_C21.QXD 3/15/07 7:47 AM Page 606

.

Chapter 21 Managing currency risk 607

21.6 EXCHANGE RATE FORECASTING

First of all, consider why firms may want to forecast future exchange rates. There are

both short-term and long-term reasons for this:

■ To help decide whether to protect outstanding current assets and liabilities from

potential foreign exchange losses.

■ To assist in quoting prices in foreign currency when constructing an international

price list.

■ To aid working capital management, e.g. accurate exchange rate forecasts may assist

the decision regarding the most efficient timing of transmitting currency in situations

where the firm is able to lead and lag payments.

■ To evaluate foreign investment projects requiring exchange rate forecasts over sev-

eral years.

Because FX forecasts are required for both short- and long-term purposes, they may

require continuous revision. In addition, long-term forecasts for investment appraisal

purposes often require more intensive analysis of a range of different scenarios. In gen-

eral, the firm’s FX forecasting needs hinge on:

■ The pattern of its trading and investment activities, i.e. its degree of globalisation.

■ The required frequency of forecast revision.

■ The internal resources and expertise available for forecasting analysis.

■ Approaches to FX forecasting

There are two broad approaches to FX prediction: (a) Fundamental Analysis, which

bases forecasts on the financial and economic theories outlined earlier and (b) Technical

Analysis, which is based on analysis and projection of time series trends.

(a) Fundamental analysis

This approach is sub-divided into two analytical perspectives:

(i) The balance of payments (BOP) perspective

This regards a country’s BOP (more accurately, its balance of payments on current

account) as an indicator of likely pressure on its exchange rate. When a country, say, the

UK, spends more on foreign-produced goods and services than its export earnings, the

resulting deficit on current account increases the probability of depreciation of its cur-

rency. Overseas residents accumulate monetary claims on sterling – when they convert

into their own currencies, this will exert downward pressure on the GBP (and vice

versa for a surplus of exports over imports).

Analysts who focus on the BOP try to evaluate not only the country’s ongoing BOP

performance but also the determinants of international competitiveness, such as

prospects for inflation, e.g. a government budget deficit and how it is financed, and

underlying productivity movements.

(ii) The asset market approach

This examines the willingness of foreign residents to hold claims on the domestic cur-

rency in monetary form. Their willingness depends on relative real interest rates and

on a country’s prospects for economic growth and the profitability of its industry and

commerce. The asset market perspective could explain the continuing strength of the

USD during the ‘Greenspan Boom’ of the 1990s, during which the USA received a mas-

sive inflow of overseas funds seeking a home in the stock markets, helping to offset the

continuing gaping US current account deficit.

Technical Analysis

The intensive scrutiny of

charts of foreign exchange rate

movements attempting to

identify persistent patterns

CFAI_C21.QXD 3/15/07 7:47 AM Page 607

.

608 Part VI International finance

Any factor expected to increase real returns on investment, e.g. technological progress

such as the rise of e-commerce, promising higher corporate profitability is thus likely to

lead to relative exchange rate appreciation (and vice versa).

In practice, it is difficult to disentangle the various fundamental pressures on exchange

rates to identify the true reasons for their movements. Some argue that short-term move-

ments are largely determined by the relative attractiveness of international asset markets,

interest rates and the expectations of market players plus a dose of speculation, while in

the long-term, equilibrium exchange rates depend on PPP.

(b) Technical analysis

Technical analysts conduct intensive scrutiny of charts to identify trends in foreign

exchange rate movements. These chartists focus on both price and volume data to

ascertain whether past trends are likely to persist into the future. The underlying prem-

ise behind Chartism is that future FX rates are based on past rates. Chartists assert that

FX movements can be split into three temporal categories:

(i) day-to-day movements, mainly random ‘noise’

(ii) short-term movements, which extend from a few days to periods lasting several

months

(iii) long-term movements, characterised by persistent upward and/or downward

trends.

The longer the forecasting time horizon, the less accurate the prediction is likely to be.

However, for most firms, a major part of their forecasting needs are short-to-medium term,

so ‘expert’ forecasting may have some role to play. Forecasting for the long-term howev-

er, depends on the economic fundamentals of exchange rate determination, although

some people believe in the existence of long-term waves in currency movements (at least,

when they float!). A major flaw of technical analysis is that it is purely mechanical with

no attempt to provide supporting theory regarding explanation of causation.

Research by Chang and Osler (1999) suggests that technical analysis is largely a waste

of time and money for trades in most currency pairs. They studied the performance of a

particular dealing rule, the so-called ‘head and shoulders’ pattern. This pattern is

formed when a market price forms three peaks, a high one (the head) flanked by two

lower ones (the shoulders). When the price rises through the second neckline, many

technical analysts treat this as a buy signal. During 1973–94, this rule would not have

worked except for JPY–USD and DEM–USD trades, where profits at annualised rates of

19 per cent and 13 per cent would have been made. Possibly, this is because with the

widespread use of these techniques, such patterns often become self-fulfilling prophe-

cies. However, even for these trading pairs, much simpler trading rules, such as buying

when a price was above its recent trading levels, would have generated superior returns.

■ Forecasting in practice

Most leading banks offer FX forecasting services and many MNCs employ in-house

forecasting staff. The value of these activities is open to question, but this really depends

on the motivation for forecasting. A long-term forecast may be needed to underpin an

investment decision in a foreign country. A forecast based on long-term fundamentals

may not need to be perfectly accurate but may help in analysing more fully the risks sur-

rounding the decision and its implementation.

Conversely, short-term forecasts may be needed to hedge debtors or creditors for

settlement in a month or so. In such cases, long-term fundamentals may be less impor-

tant than market-related technical factors, e.g. closing of positions, political factors or

‘sentiment’ in the market. The required degree of accuracy increases as the prospect of

loss is more immediate and less remedial action is possible. In general, long-term fore-

casts are based on economic models reflecting fundamentals, while short-term forecasts

CFAI_C21.QXD 3/15/07 7:47 AM Page 608

.

Chapter 21 Managing currency risk 609

A forecasting fiasco

During mid-to-late 1999, after an early flurry, the euro fell sharply from its opening

value of against the USD, reaching It was widely felt that the euro had

been oversold and would recover rapidly during 2000. Table 21.2 shows a selection of

forecasts made by 17 leading banks in November 1999 of the euro’s value twelve

months ahead, i.e. in November 2000.

The actual spot rate on 1 November 2000 was per USD. Similar shortfalls were

recorded against other major currencies. Subsequently, the euro did recover to 0.96 in

early 2000, but slipped back to 0.88 in April that year. The forward market was pre-

dicting in November 1999 a 3 cents appreciation in the euro. These figures remind us

that the ‘experts’ like the FX markets sometimes get things wrong, but warn us that, at

times, all the experts get things badly wrong – and so do the markets.

;0.86

;1.05.;1.17

tend to rely on technical analysis. Chartists often attempt to correlate exchange rate

changes with various other factors regardless of the economic rationale for the co-

movement.

■ FX forecasting and market efficiency

The likelihood of forecasts being consistently useful or profitable depends on whether

the FX markets are efficient. The more efficient the market, the more likely that FX rates

are random walks, with past behaviour having no bearing on future movements. The

less efficient the market, the more likely that forecasters will ‘get lucky’ and stumble on

a key relationship that happens to hold for a while. Yet, if such a relationship really

exists, others will soon discover and exploit it, and the market will regain its efficiency

regarding that item of information.

■ The role of central banks

A key requirement of market efficiency is that all market players are rational wealth

seekers. This is often not the case with a major market participant, the central bank

that tries to raise or lower its currency by buying or selling in the open market, often

in defiance of market trends and sentiment. Evidence exists that at times when central

banks intervene, markets become less efficient and it is possible to make money by bet-

ting against them. This happened most notably on ‘Black Wednesday’ in 1992 when

sterling was evicted from the ERM despite the Bank of England spending billions of

GBP worth of foreign exchange. However, these opportunities are likely to be only

very short-term phenomena.

Table 21.2

Twelve-month forecasts to 1 November 2000

Bank US$ vs. euro

American Express 1.15

Bank of Montreal 1.09

Barclays Bank 1.10

CCF 1.10

Citibank 1.15

Commerzbank 1.18

Dresdner Kleinwort Benson 1.18

Goldman Sachs 1.22

Hanseatic Bank 1.20

CFAI_C21.QXD 3/15/07 7:47 AM Page 609

.

610 Part VI International finance

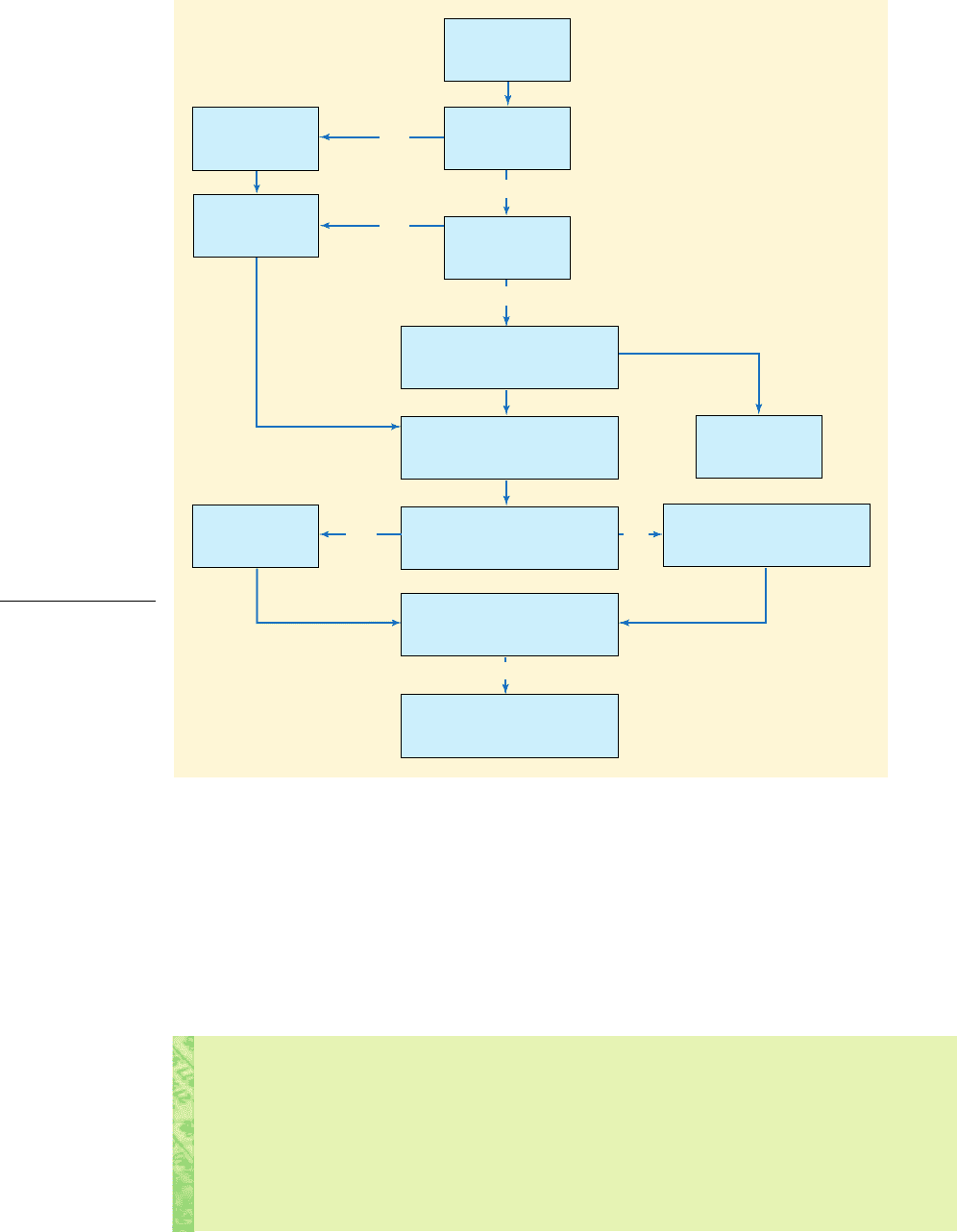

21.7 DEVISING A FOREIGN EXCHANGE MANAGEMENT (FEM) STRATEGY

■ Hedging translation exposure: Balance Sheet items

Total exchange exposure is made up of cash flowing across a national frontier plus the

assets and liabilities of the company that are denominated in a foreign currency.

An international treasurer who does not believe the theories outlined above, might

decide to hedge all foreign currency transactions plus the total net worth of all foreign

subsidiaries. This strategy is over-elaborate and very expensive, but is adopted by

many companies, particularly those dealing in currencies that fluctuate widely in value

over short periods.

Figure 21.3 illustrates a more systematic approach. The basic strategy is to remove

from consideration all items that are self-hedging so far as exchange rate risk is con-

cerned, and to concentrate attention on those cash flows, assets and liabilities that are

subject to exchange rate risk in the short term.

We start with a position where all cash flows, assets and liabilities denominated

in foreign currency values are assumed to be subject to exposure. Let us now try to

eliminate some of these items from the exposure equation. First, we eliminate all

non-monetary assets such as land, buildings and inventory. These should float in

value with internal inflation. The rate of adjustment in value will vary, internationally

traded goods will jump in local value faster than the value of land, but eventually the

Table 21.2 Continued

HSBC Midland 1.20

Lloyds TSB 1.18

NatWest Group 1.16

Royal Bank of Scotland 1.15

Societé Générale 1.08

Warburg Dillon Read 1.14

Mean 1.15

Range 1.22–1.08

Spot rate November 1 1999 1.05

Forward rate (one year) 1.08

Source: Corporate Finance, December 1999

The jury is still out on FX forecasting – it should not be possible to outguess the

market, but sometimes it works: the question is ‘when?’ Meanwhile, some busi-

nesspeople derive comfort from having ‘expert’ forecasts available, possibly as a

focus of blame! The implications for hedging are hazy – if one believes in PPP in the

short-term, then hedging is pointless, but PPP seems only to operate in the longer-

term and with unclear time lags. So, for peace of mind, most firms try to devise a

hedging strategy.

The Economist magazine publishes an annual survey (usually in April) on PPP. This

is based on the global price of a Big Mac (The Big Mac Index), and purports to identify –

in a tongue-in-cheek fashion – cases where PPP does not apply between currencies.

This has recently been extended to cover the worldwide price of Starbucks coffee, to

widen the range of goods examined. Results are broadly similar although, of course, a

more rigorous approach would scrutinise the prices of a standard ‘basket’ of goods, as

in national price indices.

CFAI_C21.QXD 3/15/07 7:47 AM Page 610

.

Chapter 21 Managing currency risk 611

Consider hedging cash flows

and fixed interest loans if they

are short-term

DESIGN INFORMATION

SYSTEM TO CONTROL

SHORT TERM CASH FLOWS

Do you believe that

future exchange rates

can be forecast?

Select suitable INTERNAL

FEM hedging devices to

cover exposure

But what

about long-

term loans?

Decide on required

degree of exposure

in each currency

Decision:

minimize

exposure

Hedge net

worth

Hedge the

net monetary

position

No

No

No

Yes

Yes

Yes

What is exposed

to exchange

rate risk?

Do you believe in

the PPP theory?

For the balance

Select suitable EXTERNAL

FEM hedging devices to cover

balance of exposure

Do you believe

in the IRPT?

Figure 21.3

Flow chart demon-

strating a logical

approach towards

devising a foreign

exchange manage-

ment strategy

(based on McRae,

1996)

Self-assessment activity 21.6

Langer plc is worried about a fall in the Australian dollar by 5 per cent, compared to the

present A$2.75 per that might inflict translation losses regarding its A$100 million

assets located in Adelaide. Why should it not worry?

(UK inflation is 2 per cent. Australian inflation is 7 per cent.)

(Answer in Appendix A at the back of the book)

£1,

prices of all of these non-monetary assets will rise to compensate for the fall in value

of the local currency. PPP relates inflation differences to changes in exchange rates.

In time, the asset or liability denominated in the foreign currency will rise in value

sufficiently to compensate for the fall in the foreign currency value. In other words,

the owner of the asset could sell it for more foreign currency units, each command-

ing a lesser value than before. The total in terms of home currency will remain

unchanged.

CFAI_C21.QXD 3/15/07 7:47 AM Page 611

.

612 Part VI International finance

Non-monetary assets are thus self-hedging at least in the long term. If the asset has

to be sold in the short term and the foreign cash exchanged into local currency, the

amount then becomes a part of transaction exposure. A real loss might be involved.

Short-term loans can, for the most part, also be considered self-hedged. The higher

or lower interest rate on the foreign currency loan is a kind of insurance policy against

the future fall or rise of the ‘away’ currency in terms of the ‘home’ currency. A forward

contract could be taken out to cover the risk, but this would be a needless expense

(given that spreads are wider on forward transactions), since the forward rate is an

unbiased predictor of the future spot rate. On average, the forward contracts would

make neither a profit nor a loss.

Long-term loans are more problematic. A fervent believer in the Open Fisher

Theory would claim that the long-term loan, like the short, is also self-hedged. The

interest rate difference is the market’s best guess as to the future changes in the value

of the currency. A lower-rate loan suggests a higher capital sum to repay in the home

currency. A higher-rate loan suggests a smaller capital sum.

If in doubt about monetary assets or liabilities being self-hedging, one solution is to

calculate the ‘net monetary asset position’ in each currency and make sure it is either

in balance or in the ‘right’ direction. In other words, if it is predicted that a currency will

fall in value against GBP, the firm should owe money in that currency. If it is predicted that a

currency will rise in value against GBP, then it should be owed money in that currency. This

might require some juggling with the financing mix of the firm via ‘currency swaps’,

which we discuss later in the chapter.

The key problem in currency risk management is thus to identify the various types of expo-

sure facing the company and then to hedge any unwanted exposure risks. Non-monetary

assets and short-term loans in foreign currency are for the most part self-hedged. The

exchange risk involved in financing with foreign loans and bonds is less clear. With

regard to transaction exposure, a currency information system needs to be designed

and installed to identify estimated short-term cash flow exposure in each currency.

■ Transaction exposure: hedging the cash flows

The first step in identifying and hedging cash flow exposure in foreign currency is to

set up a currency information system. The control of currency is much simplified if this

information system is centralised, but this is not a necessary condition of efficient cur-

rency management.

Once this system is in place, the company must decide whether it (1) believes that

future exchange rates can be forecast, and (2) will permit speculation in currency. If

the answer to either question is ‘no’, then the company must seek to minimise the

exposure position in all currencies. If a profit-maximising strategy is adopted, the

company will use currency forecasts to decide on an optimal position in each foreign

currency. If the company believes that currency forecasting is impossible, or not

profitable, then it has to adopt a risk-minimising policy. The aim will be to reduce

exposure in all currencies to a minimum unless the cost of this policy is prohibitive.

Once the estimated cash flows in each currency have been identified, the next step is to

consolidate the data. The individual flows are netted to arrive at the estimated net balance

in each currency for each future period. Monthly estimates for six months ahead are the

most common requirement, but large companies holding, or trading in, many currencies

may require weekly or even daily reports (especially if speculative positions are opened).

If the company believes that currency forecasting is both possible and profitable, it

must decide, in the light of current currency forecasts, the degree of imbalance desirable

in each currency in which it trades. Even if forecasting is thought to be possible and prof-

itable, the company might decide to prohibit currency speculation as a matter of princi-

ple. Many UK multinationals take this position. In the past, US multinationals have been

currency information

system

An information system set up

to identify values that are

exposed to currency risk, e.g.

cash in- and outflows and

asset and liability values

risk-minimising policy

A foreign exchange policy

designed to eliminate as far as

possible, the firm’s exposure to

currency risk.

CFAI_C21.QXD 3/15/07 7:47 AM Page 612

.

Chapter 21 Managing currency risk 613

more willing than similar UK companies to speculate in currency, but research by Belk

and Glaum (1990) suggests that attitudes among UK treasurers may have changed.

The next step is to convert the ‘natural’ exposure position arising from normal trad-

ing into the ‘desired’ exposure position. This is done by using various currency hedg-

ing devices, some of which are internal to the firm and others external. Prindl (1978),

who introduced the distinction between internal and external hedging, also pointed

out that internal hedging is almost invariably cheaper than external hedging. The

international treasurer should first adjust the ‘natural’ exposure position using inter-

nal techniques and use the more expensive external techniques only after the internal

hedging possibilities have been exhausted.

BMW bets on rebound for falling US dollar

FT

German carmaker stops

long-term hedging

BMW, the German luxury car-

maker, has stopped all long-term

hedging of the dollar, seeing an

end to the US currency’s two-

year decline.

The company is one of Europe’s

heaviest users of currency hedg-

ing to protect its revenues from

volatile foreign exchange markets.

But it now believes the US cur-

rency is ‘significantly’ underval-

ued and must bounce back.

The dollar has fallen by 29

per cent against the euro in the

past two years, pricing many

European exporters out of US

markets. As the US currency

approached the $1.30 mark

against the euro earlier this

year, European politicians

clamoured for a cut in interest

rates to make the eurozone

more competitive.

BMW said it believed the

‘correct’ value for the dollar was

$1.10 to the euro compared with

$1.22 – the level it reached in

late trading yesterday.

But the carmaker could be

premature in its belief in a dol-

lar rebound as few strategists

are confident of a dollar bounce

in the near-term, and currency

traders remain concerned about

the twin US deficits.

Bob Sinche, head of currency

strategy at Citigroup, said the

‘panic mentality’ that set in as

the dollar fell last year was

diminishing, but few companies

seemed ready to go completely

unhedged. ‘We have not seen a

lot of discussion [from compa-

nies] about whether the

process of dollar weakening

has come to an end,’ he said.

‘The general notion remains

one of concern about the dollar

on a medium-term basis, and

corporates are using periods of

dollar strength to put on some

hedging.’

Volkswagen, Europe’s

biggest carmaker, increased its

hedging at the end of last year

after the falling dollar knocked

from annual

profits.

Pension funds buying US

assets appear to be reducing

their level of hedging, however.

‘There are indications that

institutional [pension fund]

investors do not seem as keen

to hedge their dollar exposure

as they were in 2003 or even

2002,’ said Michael Metcalfe,

currencies strategist at State

Street Bank.

BMW said it was limiting its

use of derivatives to protect

against the weak dollar to short-

term ‘buying on the dips’.

‘We think that the euro will

go down again,’ said Stefan

Krause, finance director. ‘In such

a period of significant under-val-

uation of the US dollar it is

important to remain consistent

and to have the courage not to

hedge at unattractive currency

rates.’

Hedging the dollar has

become important to BMW

because the US last year passed

Germany as the company’s

largest market. But the strength

of the euro against the dollar is

also a wider issue for the

German economy.

Mr Krause said BMW

remained ‘widely’ hedged this

year, with between two-thirds

and all of the US turnover cov-

ered. He also said the company

had other hedging options, such

as cutting the allocation of vehi-

cles to sell.

The company still has short-

term hedges in place for next

year, but surprised analysts by

saying it had not increased these

beyond the one-third of turnover

already covered.

Source: James Mackintosh and Steve Johnson,

Financial Times, 18 March 2004.

;1.2 bn 1£810 m2

CFAI_C21.QXD 3/15/07 7:47 AM Page 613

.

614 Part VI International finance

21.8 INTERNAL HEDGING TECHNIQUES

Internal hedging techniques exploit characteristics of the company’s trading relation-

ships without recourse to the external currency or money markets. Most are simple in

concept and operation.

Netting applies where the head office and its foreign subsidiaries net off intra-

organisational currency flows at the end of each period, leaving only the balance

exposed to risk and hence in need of hedging. Netting is illustrated in the following

simple example.

A UK-based multinational has a German operating subsidiary. In a particular

month, it transfers components worth to Germany. In the same month,

the subsidiary transfers finished goods worth to the UK. With netting,

the company need only make a net currency transfer of rather than mak-

ing two separate transactions totalling As well as reducing exposure,

netting saves transfer and commission costs, but it requires a two-way flow in the

same currency.

Bilateral netting applies where pairs of companies in the same group net off their

own positions regarding payables and receivables, often without the involvement of

the central treasury. If the previous company also had a Swiss subsidiary, a bilateral

netting arrangement could operate between the German and the Swiss subsidiaries.

Multilateral netting is performed by the central treasury where several subsidiaries

interact with the head office. Subsidiaries are required to notify the treasury of the

intra-organisational flows of receivables and payments. Again, a common currency is

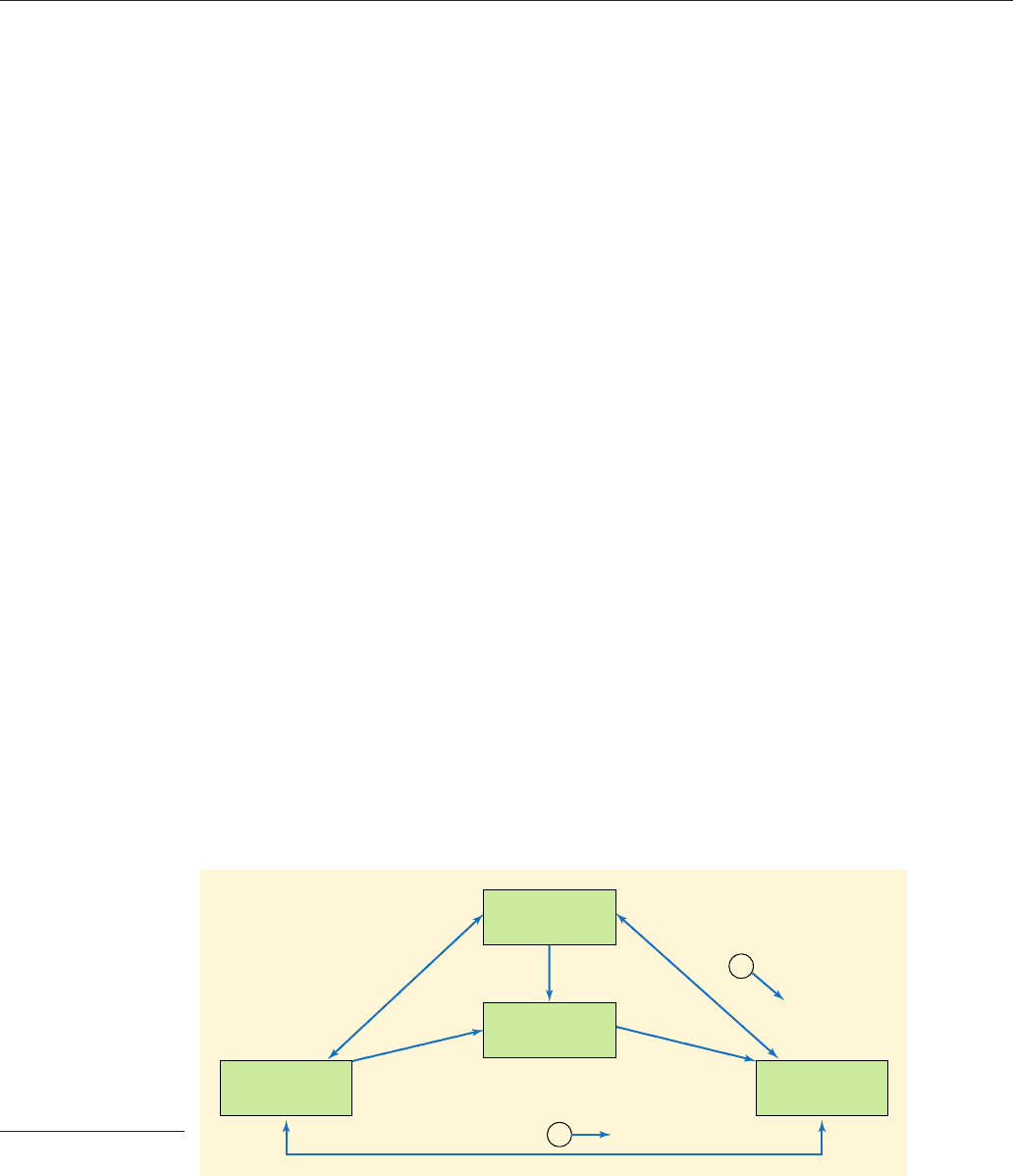

required. To illustrate this, Oilex is a UK-based oil company with an exploration divi-

sion based on Norway, major interests in the USA and chemical plants in the UK. The

group treasury ‘holds the ring’ at the centre of this nexus, as shown in Figure 21.4. All

intra-group transactions are conducted in USD, which is the operating currency of the

oil industry.

Table 21.3 shows transactions expected for one particular month. In total, currency

flows of $41 million would be required with no treasury intervention. By multilateral

netting, the treasury can reduce the exposed flows by $27 million. Such a system pro-

duces greatest benefits when the inter-subsidiary positions are most similar, and where

payments are made directly to the relevant subsidiaries, thus avoiding cash transfers

into and then out of the treasury. In this case, chemicals would transfer $3 million direct

;60 million.

;20 million,

;40 million

;20 million

US Division

Chemicals (UK)

Treasury

Exploration

(Norway)

11

3

410

5 12

2 8

Figure 21.4

Illustration of multilat-

eral netting

CFAI_C21.QXD 3/15/07 7:47 AM Page 614