Jacques I. Mathematics for Economics and Business

Подождите немного. Документ загружается.

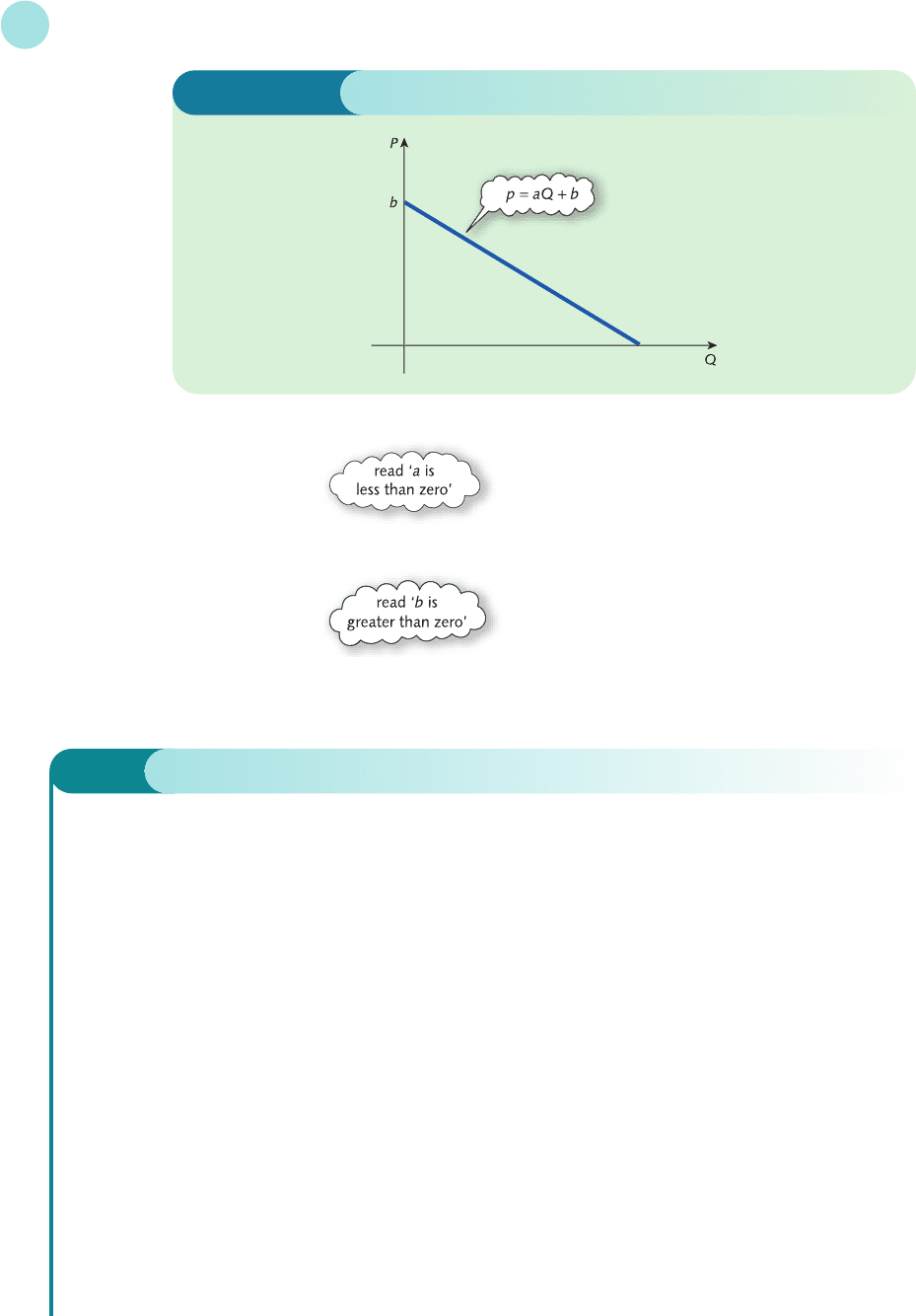

In symbols we write

a < 0

It is also apparent from the graph that the intercept, b, is positive: that is,

b > 0

In fact, it is possible in th

eory for the demand curve to be horizontal with a = 0. This cor-

responds to perfect competition and we shall return to this special case in Chapter 4.

Linear Equations

50

Figure 1.14

Example

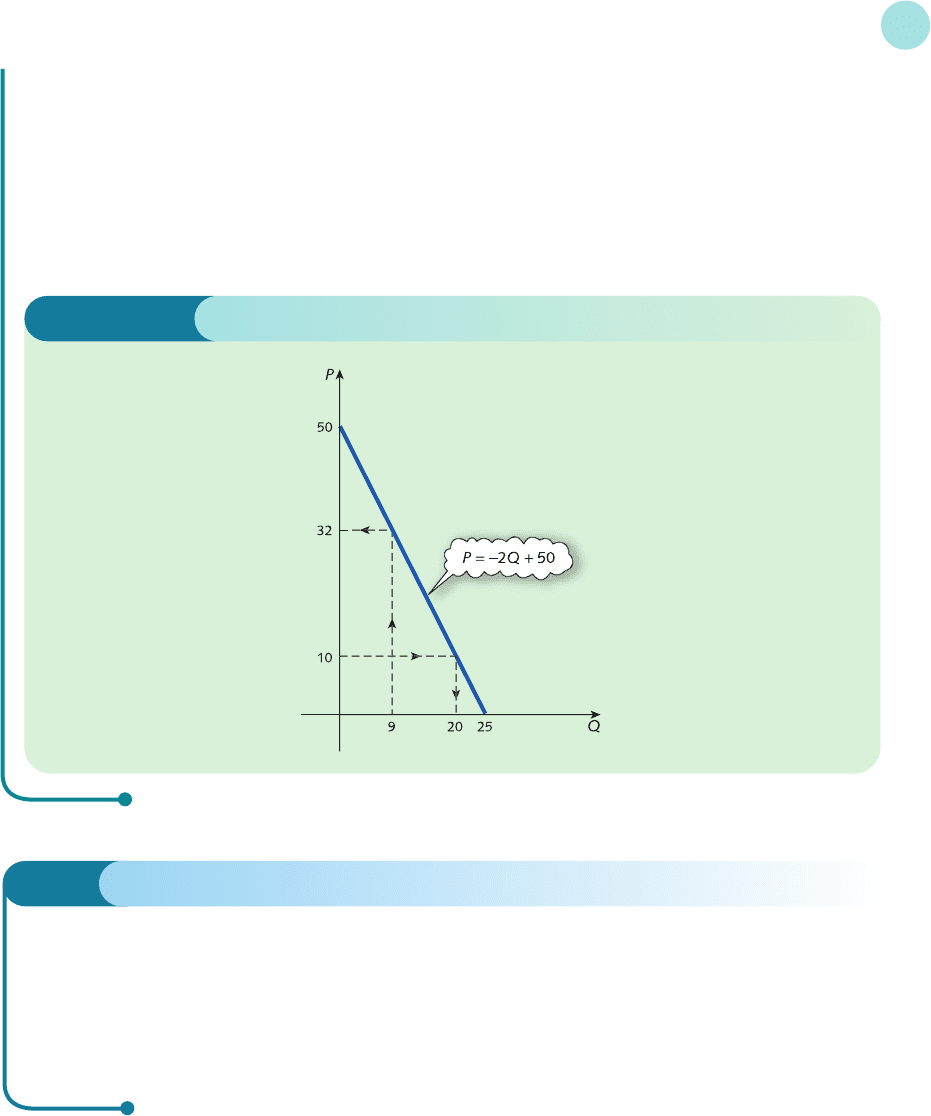

Sketch a graph of the demand function

P =−2Q + 50

Hence, or otherwise, determine the value of

(a) P when Q = 9

(b) Q when P = 10

Solution

For the demand function

P =−2Q + 50

a =−2, b = 50, so the line has a slope of −2 and an intercept of 50. For every 1 unit along, the line goes down

by 2 units, so it must cross the horizontal axis when Q = 25. (Alternatively, note that when P = 0 the

equation reads 0 =−2Q + 50, with solution Q = 25.) The graph is sketched in Figure 1.15.

(a) Given any quantity, Q, it is straightforward to use the graph to find the corresponding price, P. A line

is drawn vertically upwards until it intersects the demand curve and the value of P is read off from the

vertical axis. From Figure 1.15, when Q = 9 we see that P = 32. This can also be found by substituting

Q = 9 directly into the demand function to get

P =−2(9) + 50 = 32

MFE_C01c.qxd 16/12/2005 10:56 Page 50

(b) Reversing this process enables us to calculate Q from a given value of P. A line is drawn horizontally

until it intersects the demand curve and the value of Q is read off from the horizontal axis. Figure 1.15

indicates that Q = 20 when P = 10. Again this can be found by calculation. If P = 10 then the equation reads

10 =−2Q + 50

−40 =−2Q (subtract 50 from both sides)

20 = Q (divide both sides by −2)

1.3 • Supply and demand analysis

51

Practice Problem

2 Sketch a graph of the demand function

P =−3Q + 75

Hence, or otherwise, determine the value of

(a) P when Q = 23

(b) Q when P = 18

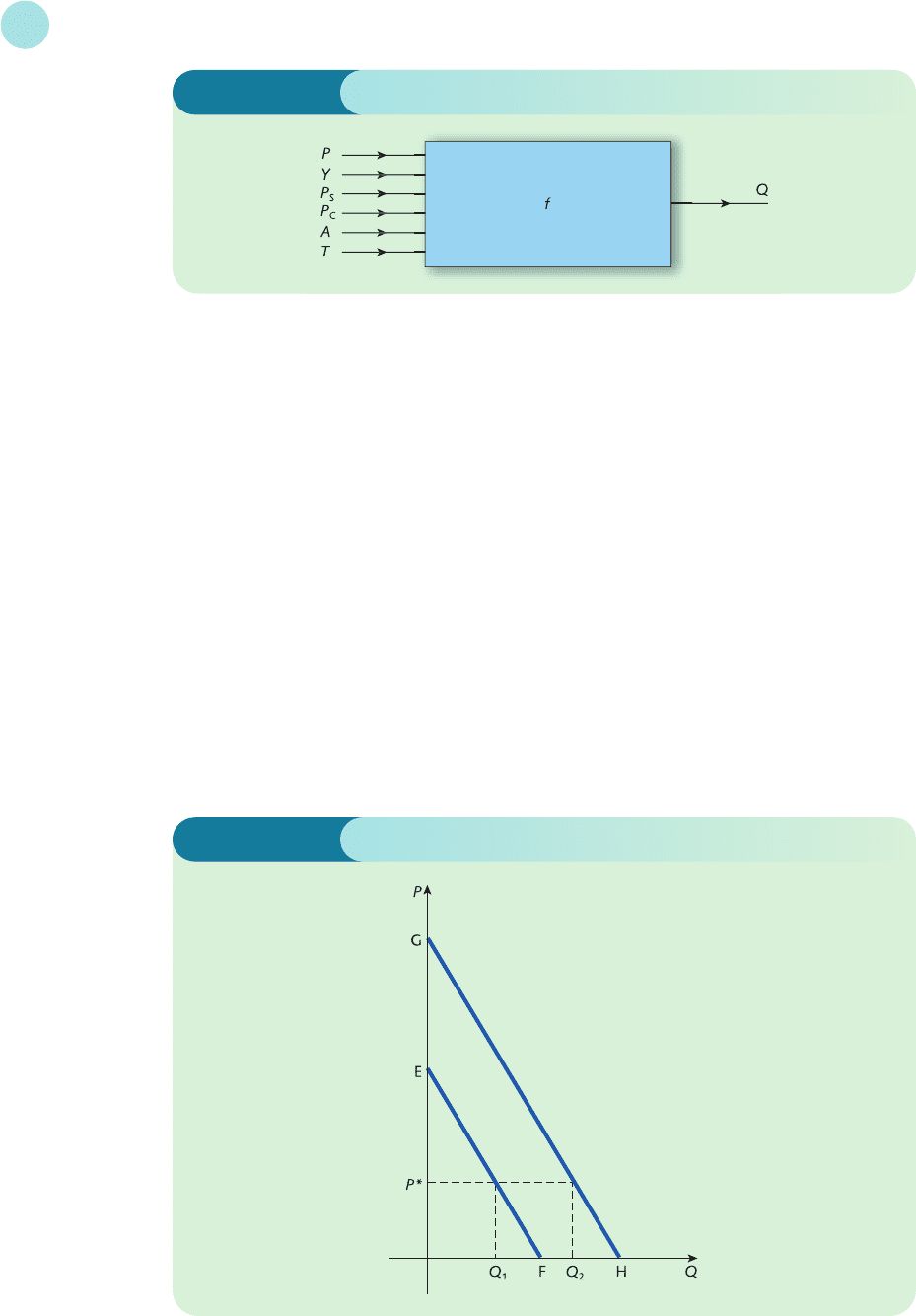

The model of consumer demand given so far is fairly crude in that it assumes that quantity

depends solely on the price, P, of the good being considered. In practice, Q depends on other

factors as well. These include the incomes of consumers, Y, the price of substitutable goods, P

S

,

the price of complementary goods, P

C

, advertising expenditure, A, and consumers’ tastes, T. A

substitutable good is one that could be consumed instead of the good under consideration. For

example, in the transport industry, buses and taxis could obviously be substituted for each

other in urban areas. A complementary good is one that is used in conjunction with other

Figure 1.15

MFE_C01c.qxd 16/12/2005 10:56 Page 51

goods. For example, music CDs and hi-fi systems are consumed together. Mathematically, we

say that Q is a function of P, Y, P

S

, P

C

, A and T. This is written

Q = f(P, Y, P

S

, P

C

, A, T )

where the variables inside the brackets are separated by commas. In terms of a ‘black box’ dia-

gram, this is represented with six incoming lines and one outgoing line as shown in Figure 1.16.

In our previous discussion it was implicitly assumed that the variables Y, P

S

, P

C

, A and T are

held fixed. We describe this situation by calling Q and P endogenous variables, since they are

allowed to vary and are determined within the model. The remaining variables are called

exogenous, since they are constant and are determined outside the model.

Let us return now to the standard demand curve shown in Figure 1.17 as the line EF. This is

constructed on the assumption that Y, P

S

, P

C

, A and T are all constant. Notice that when the

price is P* the quantity demanded is Q

1

. Now suppose that income, Y, increases. We would

normally expect the demand to rise because the extra income buys more goods at price P*. The

effect is to shift the demand curve to the right because at price P* consumers can afford the

larger number of goods, Q

2

. From Figure 1.17 we deduce that if the demand curve is

Linear Equations

52

Figure 1.16

Figure 1.17

MFE_C01c.qxd 16/12/2005 10:56 Page 52

P = aQ + b

then a rise in income causes the intercept, b, to increase.

We conclude that if one of the exogenous variables changes then the whole demand curve

moves, whereas if one of the endogenous variables changes, we simply move along the fixed

curve.

Incidentally, it is possible that, for some goods, an increase in income actually causes the

demand curve to shift to the left. In the 1960s and 1970s, most western economies saw a decline

in the domestic consumption of coal as a result of an increase in income. In this case, higher

wealth meant that more people were able to install central heating systems which use alter-

native forms of energy. Under these circumstances the good is referred to as an inferior good.

On the other hand, a superior good is one whose demand rises as income rises. Cars and elec-

trical goods are obvious examples of superior goods. Currently, concern about global warming

is also reducing demand for coal. This factor can be incorporated as part of taste, although it is

difficult to handle mathematically since it is virtually impossible to quantify taste and so to

define T numerically.

The supply function is the relation between the quantity, Q, of a good that producers

plan to bring to the market and the price, P, of the good. A typical linear supply curve is

indicated in Figure 1.18. Economic theory indicates that, as the price rises, so does the supply.

Mathematically, P is then said to be an increasing function of Q. A price increase encourages

existing producers to raise output and entices new firms to enter the market. The line shown

in Figure 1.18 has equation

P = aQ + b

with slope a > 0 and intercept b > 0. Note that when the market price is equal to b the supply

is zero. It is only when the price exceeds this threshold level that producers decide that it is

worth supplying any good whatsoever.

Again this is a simplification of what happens in the real world. The supply function does

not have to be linear and the quantity supplied, Q, is influenced by things other than price.

These exogenous variables include the prices of factors of production (that is, land, capital,

labour and enterprise), the profits obtainable on alternative goods, and technology.

1.3 • Supply and demand analysis

53

MFE_C01c.qxd 16/12/2005 10:56 Page 53

In microeconomics we are concerned with the interaction of supply and demand. Figure

1.19 shows typical supply and demand curves sketched on the same diagram. Of particular

significance is the point of intersection. At this point the market is in equilibrium because the

quantity supplied exactly matches the quantity demanded. The corresponding price, P

0

, and

quantity, Q

0

, are called the equilibrium price and quantity.

In practice, it is often the deviation of the market price away from the equilibrium price that

is of most interest. Suppose that the market price, P*, exceeds the equilibrium price, P

0

. From

Figure 1.19 the quantity supplied, Q

S

, is greater than the quantity demanded, Q

D

, so there is

excess supply. There are stocks of unsold goods, which tend to depress prices and cause firms

to cut back production. The effect is for ‘market forces’ to shift the market back down towards

equilibrium. Likewise, if the market price falls below equilibrium price then demand exceeds

supply. This shortage pushes prices up and encourages firms to produce more goods, so the

market drifts back up towards equilibrium.

Linear Equations

54

Figure 1.18

Figure 1.19

MFE_C01c.qxd 16/12/2005 10:56 Page 54

1.3 • Supply and demand analysis

55

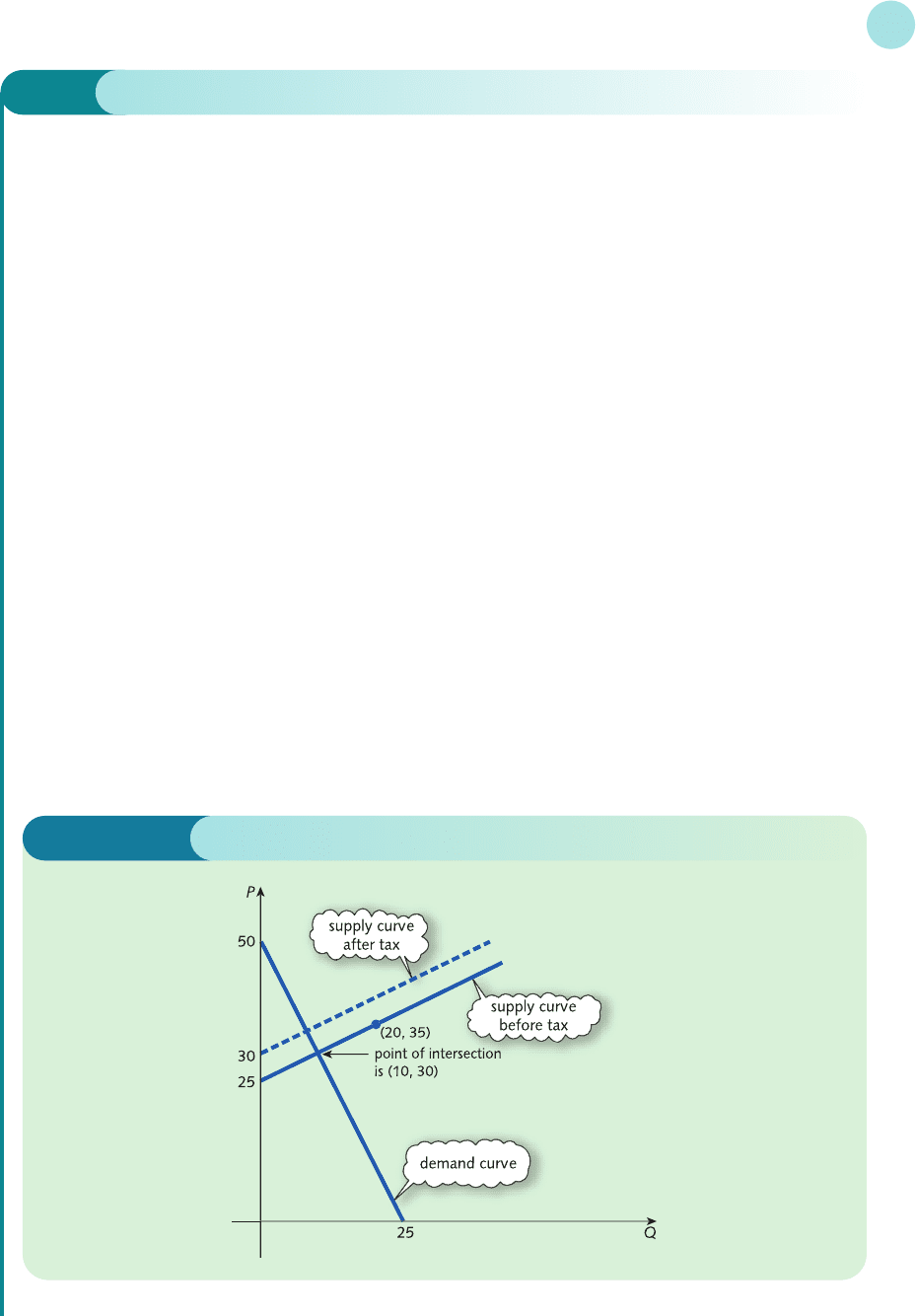

Example

The demand and supply functions of a good are given by

P =−2Q

D

+ 50

P =

1

/2Q

S

+ 25

where P, Q

D

and Q

S

denote the price, quantity demanded and quantity supplied respectively.

(a) Determine the equilibrium price and quantity.

(b) Determine the effect on the market equilibrium if the government decides to impose a fixed tax of $5

on each good.

Solution

(a) The demand curve has already been sketched in Figure 1.15. For the supply function

P =

1

/2Q

S

+ 25

we have a =

1

/2, b = 25, so the line has a slope of

1

/2 and an intercept of 25. It therefore passes through

(0, 25). For a second point, let us choose Q

S

= 20, say. The corresponding value of P is

P =

1

/2(20) + 25 = 35

so the line also passes through (20, 35). The points (0, 25) and (20, 35) can now be plotted and the

supply curve sketched. Figure 1.20 shows both the demand and supply curves sketched on the same

diagram. The point of intersection has coordinates (10, 30), so the equilibrium quantity is 10 and the

equilibrium price is 30.

It is possible to calculate these values using algebra. In equilibrium, Q

D

= Q

S

. If this common value

is denoted by Q then the demand and supply equations become

P =−2Q + 50 and P =

1

/2Q + 25

Figure 1.20

MFE_C01c.qxd 16/12/2005 10:56 Page 55

This represents a pair of simultaneous equations for the two unknowns P and Q, and so could be solved

using the elimination method described in the previous section. However, this is not strictly necessary

because it follows immediately from the above equations that

−2Q + 50 =

1

/

2

Q + 25

since both sides are equal to P. This can be rearranged to calculate Q:

−2

1

/2Q + 50 = 25 (subtract

1

/2Q from both sides)

−2

1

/2Q =−25 (subtract 50 from both sides)

Q = 10 (divide both sides by −2

1

/2)

Finally, P can be found by substituting this value into either of the original equations.

The demand equation gives

P =−2(10) + 50 = 30

As a check, the supply equation gives

P =

1

/2(10) + 25 = 30 ✓

(b) If the government imposes a fixed tax of $5 per good then the money that the firm actually receives

from the sale of each good is the amount, P, that the consumer pays, less the tax, 5: that is, P − 5.

Mathematically, this problem can be solved by replacing P by P − 5 in the supply equation to get the

new supply equation

P − 5 =

1

/2Q

S

+ 25

that is,

P =

1

/

2

Q

S

+ 30

The remaining calculations proceed as before. In equilibrium, Q

D

= Q

S

. Again setting this common

value to be Q gives

P =−2Q + 50

P =

1

/2Q + 30

Hence

−2Q + 50 =

1

/2Q + 30

which can be solved as before to give Q = 8. Substitution into either of the above equations gives P = 34.

(Check the details.)

Graphically, the introduction of tax shifts the supply curve upwards by 5 units. Obviously the

demand curve is unaltered. The dashed line in Figure 1.20 shows the new supply curve, from which

the new equilibrium quantity is 8 and equilibrium price is 34. Note the effect that government taxation

has on the market equilibrium price. This has risen to $34 and so not all of the tax is passed on to the

consumer. The consumer pays an additional $4 per good. The remaining $1 of tax must, therefore, be

paid by the firm.

Linear Equations

56

MFE_C01c.qxd 16/12/2005 10:56 Page 56

1.3 • Supply and demand analysis

57

Practice Problem

3 The demand and supply functions of a good are given by

P =−4Q

D

+ 120

P =

1

/3Q

S

+ 29

where P, Q

D

and Q

S

denote the price, quantity demanded and quantity supplied respectively.

(a) Calculate the equilibrium price and quantity.

(b) Calculate the new equilibrium price and quantity after the imposition of a fixed tax of $13 per

good. Who pays the tax?

Example

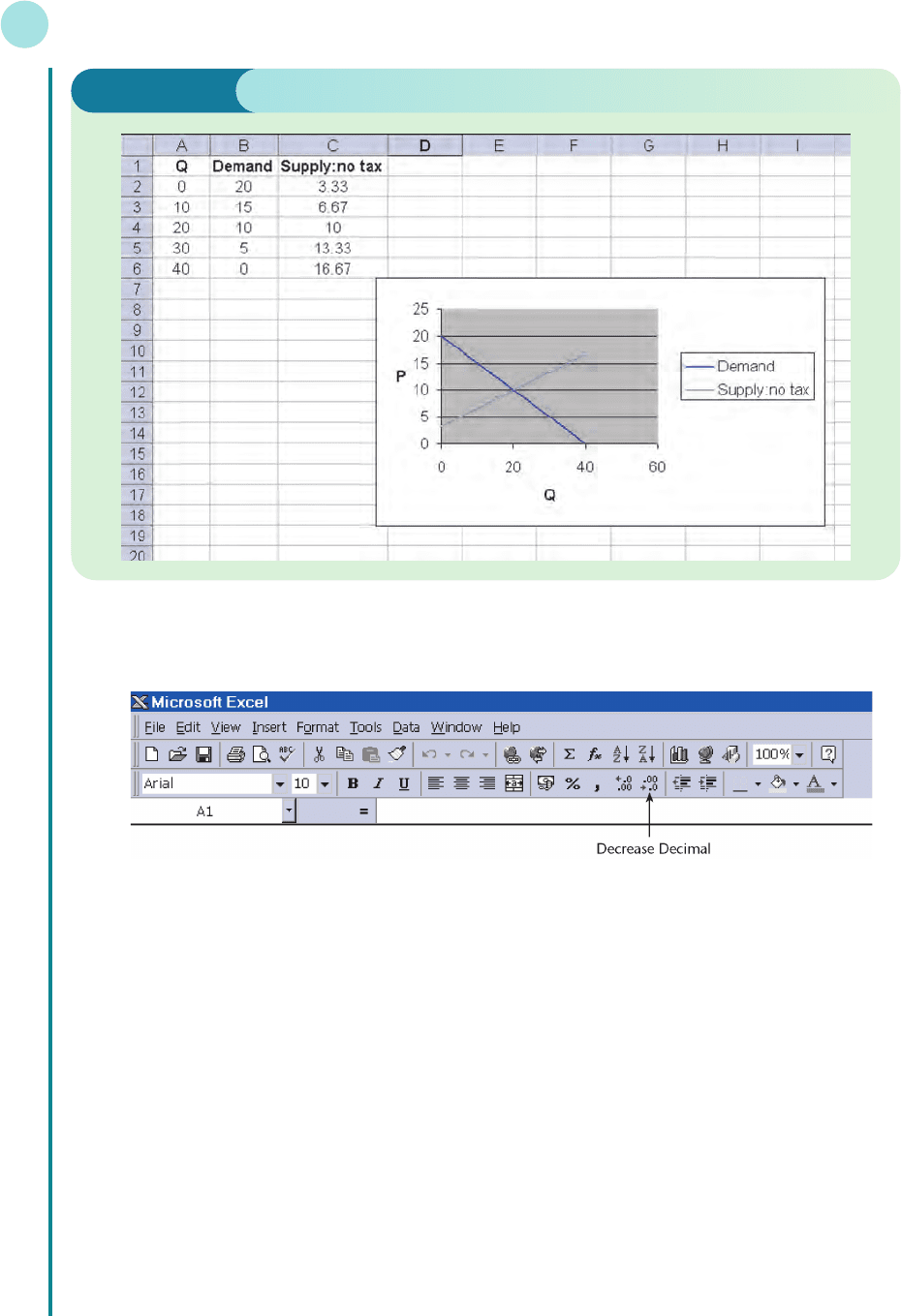

The demand and supply functions of a good are given by

P =−

1

/2Q

D

+ 20

P =

1

/3(Q

S

+ 10)

The government imposes a fixed tax, $

α

, on each good. Determine the equilibrium price and quantity in

the case when

(a)

α

= 0

(b)

α

= 5

(c)

α

= 10

(d)

α

= 2.50

In each case, calculate the tax paid by the consumer and comment on these values.

Solution

(a) In the case when

α

= 0, there is no tax and the demand and supply functions are as given above. In equi-

librium, Q

D

= Q

S

, so by writing this value as Q, we can find the equilibrium position by solving the

simultaneous equations

P =−

1

/

2

Q + 20

P =

1

/3(Q + 10)

In Excel, we first set up a table of values for Q. In Figure 1.21 (overleaf), the label Q has been put in

cell A1, and values from 0 to 40 (going up in steps of 10) occupy cells A2 to A6. At this stage, we need

to enter a formula for calculating the corresponding values of P using each of the equations in turn. As

the first value of Q is in cell A2, we type

=−A2/2 + 20

in cell B2 for the demand function, and

=1/3*(A2 + 10)

in cell C2 for the supply function. By clicking and dragging down the columns, Excel will generate cor-

responding values for demand and supply.

EXCEL

MFE_C01c.qxd 16/12/2005 10:56 Page 57

You will find that the values in the third column look very unfriendly to start with, as they have lots

of figures after the decimal point. However, these can be removed by highlighting these numbers, and

clicking on the Decrease Decimal icon, which can be found on the toolbar:

This has the effect of reducing the number of decimal places by rounding. Each time you click the icon,

another decimal place is removed. As we are dealing with money, we round to 2 decimal places.

Finally, we highlight the contents of the first three columns and use Chart Wizard to create a diagram

showing the demand and supply functions, as shown in Figure 1.21.

From the graph, it can be seen that the lines cross when Q = 20 and P = 10, which gives us the equi-

librium position. This can also be seen by looking at the fourth row of the table.

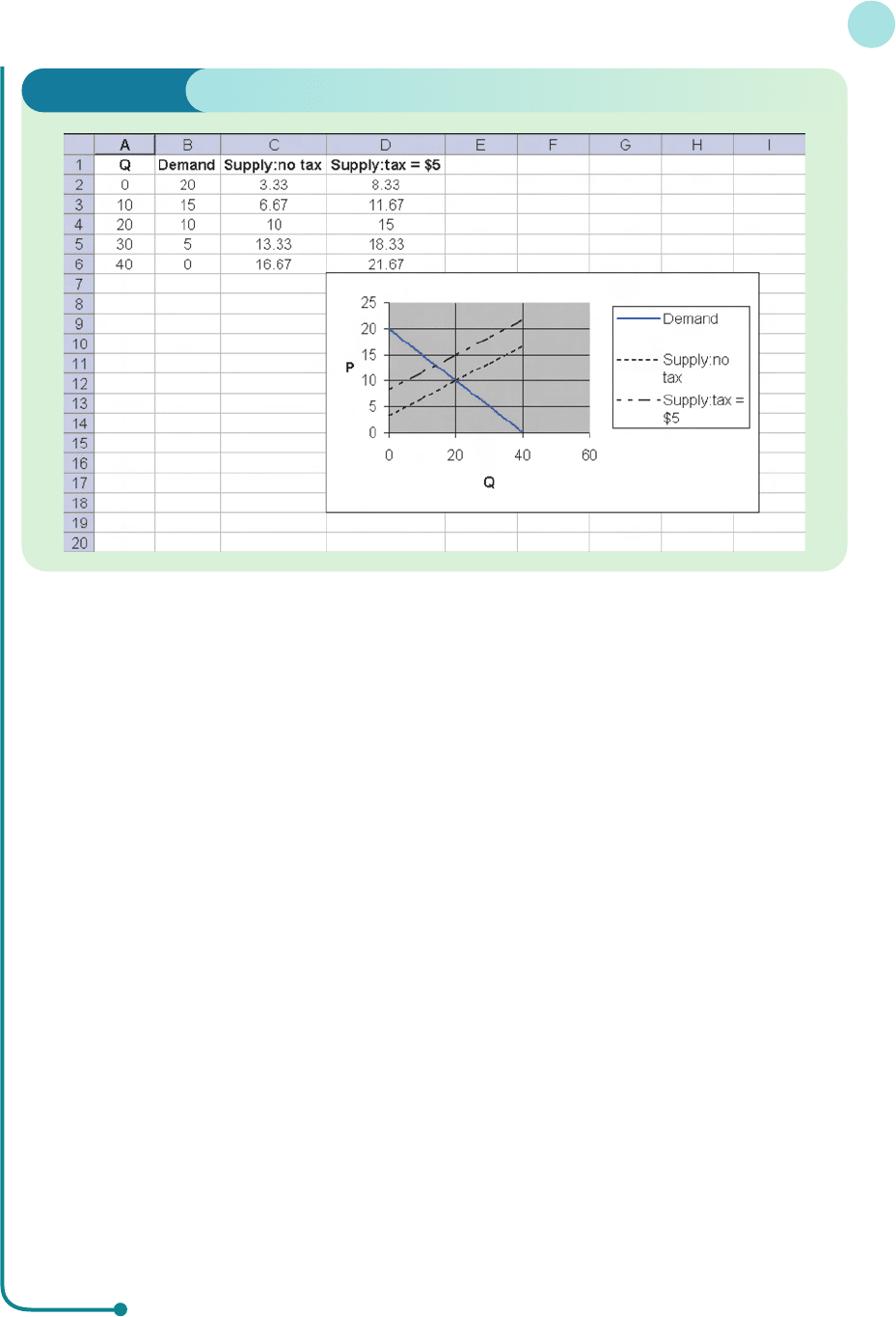

(b) If the government imposes a tax of $5 per item, the company producing the goods now receives $5 less

per item sold. The supply equation now becomes

P − 5 =

1

/3(Q

S

+ 10)

so that

P =

1

/3(Q

S

+ 10) + 5 (add 5 to both sides)

The demand function remains unchanged. We can extend our spreadsheet from part (a) to include an

extra column for this amended supply function, and we can then plot this extra line on the same graph.

This can be done by typing

=1/3*(A2+10)+5

in cell D2, and dragging down to D6.

Linear Equations

58

Figure 1.21

MFE_C01c.qxd 16/12/2005 10:56 Page 58

It is possible to alter the type of line drawn by the Chart Wizard by clicking on the line you wish to

change. This should highlight the points that were plotted. Select Format from the menu bar, and then

click on Data Series, Patterns and finally scroll through the styles of lines available and select the one

required. Figure 1.22 shows the new spreadsheet.

Notice that the effect of the tax is to move the supply line up by 5, and the position of equilibrium

has moved to (14, 13). This means that the price has increased from $10 to $13, with the consumer pay-

ing an additional $3 in tax. The remaining $2 is therefore paid by the company.

(c) The calculations in (b) can obviously be repeated by editing the formula for the supply equation in cell

D2 to

=1/3*(A2+10)+10

The equilibrium quantity and price are now

Q = 8 and P = 16

so the consumer pays $6 of this tax.

(d) Changing D2 to

=1/3*(A2+10)+2.5

gives equilibrium values

Q = 17 and P = 11.5

so the consumer pays $1.50 of the tax.

Notice that, as expected, the consumer pays increasing amounts of tax as the value of α increases.

More significantly, notice that the fraction of the tax paid by the consumer is the same in each case. For

example, in part (c), the consumer pays $6 of the $10 tax, which is

3

/5 of the tax. You might like to check

that in cases (b) and (d) the tax is also split in the ratio of 3:2. We shall investigate this further in

Practice Problem 16 at the end of this section.

1.3 • Supply and demand analysis

59

Figure 1.22

MFE_C01c.qxd 16/12/2005 10:56 Page 59