Brealey, Myers. Principles of Corporate Finance. 7th edition

Подождите немного. Документ загружается.

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

IX. Financial Planning and

Short−Term Management

29. Financial Analysis and

Planning

© The McGraw−Hill

Companies, 2003

to managers and employees alike. The economic role of reported earnings is anal-

ogous to an annually-baked pie that is divided among the important stakeholders

(government, employees, shareholders and managers alike), the size of the pie

having first been determined with prudential regard for the financial stability of

the corporation.... Reporting a loss would eliminate bonus, dividend and tax dis-

tributions, to the chagrin of all the stakeholders.”

1

Another difference is the way that taxes are shown in the income statement.

For example, in Germany taxes are paid on the published profits and the depre-

ciation method must therefore be approved by the revenue service. That is not so

in Anglo-Saxon countries, where the numbers shown in the published accounts

are generally not the basis for calculating the company’s tax payments. For in-

stance, the depreciation method used to calculate the published profits may dif-

fer from the depreciation method used by the tax authorities.

Sometimes the effect of these differences in accounting rules can be substantial.

When the German car manufacturer, Daimler-Benz, decided to list its shares on the

New York Stock Exchange in 1993, it was required to revise its accounting practices

to conform to U.S. standards. While it reported a modest profit in the first half of

1993 using German accounting rules, it reported a loss of $592 million under U.S.

rules, primarily because of differences in the treatment of reserves.

Countries also differ in the amount and accuracy of the information disclosed in

a company’s financial statements. For example, the Russian company, Lukoil, owns

some of the largest oil reserves in the world and has 120,000 employees. Yet until re-

cently its income statement reported just four numbers, with no accompanying

notes. A study by LaPorta et al. rated a sample of countries on the quality of their ac-

counting standards.

2

Table 29.1 provides an extract from their results. In general,

they concluded that company accounts were more informative in those countries

with a Scandinavian or English legal tradition and less so in those with a French or

German tradition. However, there was a huge variation within each of these groups.

818 PART IX

Financial Planning and Short-Term Management

1

See R. J. Ball, “Daimler-Benz (DaimlerChrysler) AG: Evolution of Corporate Governance from a Code-

law ‘Stakeholder’ to a Common-law ‘Shareholder Value’ System,” Graduate School of Business, Uni-

versity of Chicago.

2

LaPorta et al., “Law and Finance,” Journal of Political Economy 106 (December 1998), pp. 1113–1155.

Country Legal Tradition Rating

Sweden Scandinavian 83

United Kingdom English 78

United States English 71

France French 69

Hong Kong English 69

Switzerland German 68

Japan German 65

Germany German 62

South Korea German 62

Mexico French 60

India English 57

Peru French 38

Egypt French 24

TABLE 29.1

Country ratings on quality of accounting standards

(a high figure indicates high quality).

Source: LaPorta et al., “Law and Finance,” Journal of Political

Economy 106 (December 1998), 1113–1155.

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

IX. Financial Planning and

Short−Term Management

29. Financial Analysis and

Planning

© The McGraw−Hill

Companies, 2003

Your task is to assess the financial standing of the Executive Paper Corporation.

Perhaps you are a financial analyst with Executive Paper and are helping to de-

velop a five-year financial plan. Perhaps you are employed by a rival company that

is contemplating a takeover bid for Executive Paper. Or perhaps you are a banker

who needs to assess whether the bank should lend to the company. In each case

your first step is to assess the company’s current condition. You have before you the

latest balance sheet, income statement, and sources and uses of funds.

The Balance Sheet

Executive Paper’s balance sheet in Table 29.2 provides a snapshot of the company’s

assets and the sources of the money used to buy those assets.

The items in the balance sheet are listed in declining order of liquidity. For ex-

ample, you can see that the accountant lists first those assets which are most likely

to be turned into cash in the near future. They include cash itself, marketable

securities and receivables (that is, bills to be paid by the firm’s customers), and

CHAPTER 29

Financial Analysis and Planning 819

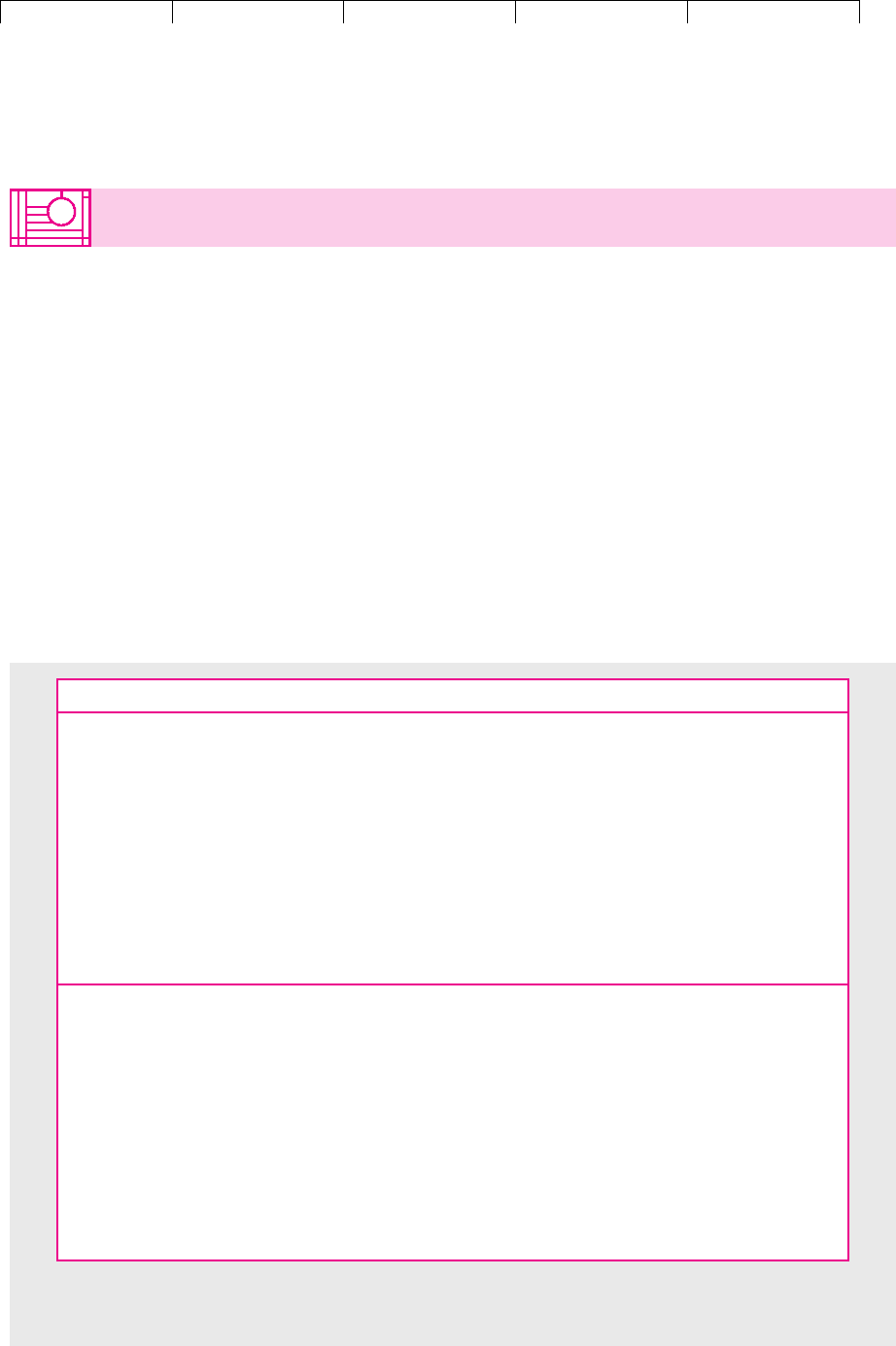

29.2 EXECUTIVE PAPER’S FINANCIAL STATEMENTS

Assets Dec 1998 Dec 1999 Change

Current assets:

Cash & securities 75 110 35

Receivables 433.1 440 6.9

Inventory 339.9 350 10.1

Total current assets 848 900 52

Fixed assets:

Property, plant, and equipment 929.5 1,000 70.5

Less accumulated depreciation 396.7 450 53.3

Net fixed assets 532.8 550 17.2

Total assets 1,380.8 1,450 69.2

Liabilities and Shareholders’ Equity Dec 1998 Dec 1999 Change

Current liabilities:

Debt due within 1 year 96.6 100 3.4

Payables 349.9 360 10.1

Total current liabilities 446.5 460 13.5

Long-term debt 425 450 25

Shareholders’ equity 509.3 540 30.7

Total liabilities & shareholders’ equity 1,380.8 1,450 69.2

Other financial information:

Market value of equity 598 708

Average number of shares (millions) 14.16 14.16

Share price ($) 42.25 50.00

TABLE 29.2

The balance sheet of Executive Paper Corporation (figures in $ millions).

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

IX. Financial Planning and

Short−Term Management

29. Financial Analysis and

Planning

© The McGraw−Hill

Companies, 2003

inventories of raw materials, work in process, and finished goods. These assets are

all known as current assets.

The remaining assets on the balance sheet consist of long-term, usually illiquid,

assets such as pulp and paper mills, office buildings, and timberlands. The balance

sheet does not show up-to-date market values of these long-term assets. Instead,

the accountant records the amount that each asset originally cost and then, in the

case of plant and equipment, deducts a fixed annual amount for depreciation. The

balance sheet does not include all the company’s assets. Some of the most valuable

ones are intangible, such as patents, reputation, a skilled management, and a well-

trained labor force. Accountants are generally reluctant to record these assets in the

balance sheet unless they can be readily identified and valued.

Now look at the right-hand portion of Executive Paper’s balance sheet, which

shows where the money to buy the assets came from.

3

The accountant starts by look-

ing at the liabilities, that is, the money owed by the company. First come those lia-

bilities that need to be paid off in the near future. These current liabilities include debts

that are due to be repaid within the next year and payables (that is, amounts owed

by the company to its suppliers).

The difference between the current assets and current liabilities is known as the

net current assets or net working capital. It roughly measures the company’s poten-

tial reservoir of cash. For Executive Paper in 1999

The bottom portion of the balance sheet shows the sources of the cash that was

used to acquire the net working capital and fixed assets. Some of the cash has come

from the issue of bonds and leases that will not be repaid for many years. After all

these long-term liabilities have been paid off, the remaining assets belong to the

common stockholders. The company’s equity is simply the total value of the net

working capital and fixed assets less the long-term liabilities. Part of this equity has

come from the sale of shares to investors and the remainder has come from earn-

ings that the company has retained and invested on behalf of the shareholders.

Table 29.2 provides some other financial information about Executive Paper. For

example, it shows the market value of the common stock. It is often helpful to com-

pare the book value of the equity (shown in the company’s accounts) with the mar-

ket value established in the capital markets.

The Income Statement

If Executive Paper’s balance sheet resembles a snapshot of the firm at a particular

point in time, its income statement is like a video. It shows how profitable the firm

has been over the past year.

Look at the summary income statement in Table 29.3. You can see that during

1999 Executive Paper sold goods worth $2,200 million and that the total costs of

producing and selling these goods were $1,980 million. In addition to these out-of-

pocket expenses, Executive Paper also made a deduction of $53.3 million for the

value of the fixed assets used up in producing the goods. Thus Executive Paper’s

earnings before interest and taxes (EBIT) were

900 460 $440

million

Net working capital current assets current liabilities

820 PART IX

Financial Planning and Short-Term Management

3

The British and Americans can never agree whether to keep to the left or the right. British accountants

list liabilities on the left and assets on the right.

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

IX. Financial Planning and

Short−Term Management

29. Financial Analysis and

Planning

© The McGraw−Hill

Companies, 2003

Of this sum $42.5 million went to pay the interest on the short- and long-term

debt (remember debt interest is paid out of pretax income) and a further $49.7 mil-

lion went to the government in the form of taxes. The $74.5 million that was left

over belonged to the shareholders. Executive Paper paid out $43.8 million as divi-

dends and reinvested the remaining $30.7 million in the business.

Sources and Uses of Funds

Table 29.4 shows where Executive Paper raised funds and how it spent them.

4

Be-

side each row in the table we have added a brief note on how the figure is calcu-

lated. We will explain each item in turn.

2,

200 1, 980 53.3 $166.7 million

EBIT Total revenues costs depreciation

CHAPTER 29 Financial Analysis and Planning 821

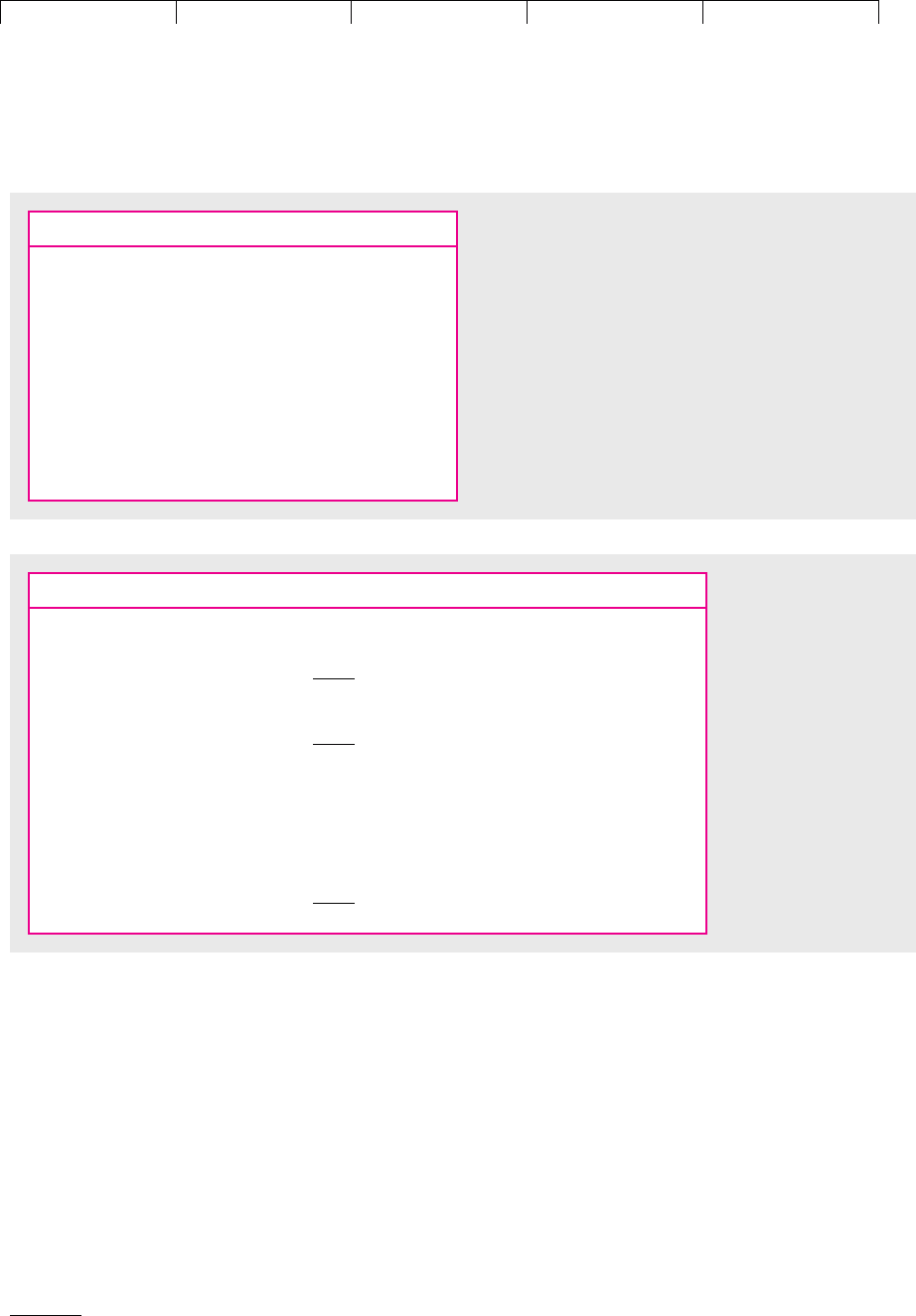

$ Millions

Revenues 2,200

Costs 1,980

Depreciation 53.3

EBIT 166.7

Interest 42.5

Tax 49.7

Net income 74.5

Dividends 43.8

Retained earnings 30.7

Earnings per share, dollars 5.26

Dividend per share, dollars 3.09

TABLE 29.3

The 1999 income statement of Executive Paper

Corporation (figures in $ millions).

4

Notice that in a Sources and Uses of Funds table the different components of net working capital are not

separated out. When we discuss short-term planning in Chapter 30, we will show how to draw up a

Sources and Uses of Cash table, which separates out different items of net working capital.

$ Millions Notes:

Sources:

Net income 74.5 See Table 29.3

Depreciation 53.3 See Table 29.3

Operating cash flow 127.8

Issues of long-term debt 25.0 See Table 29.2: 450 425

Issues of equity 0 See Tables 29.2 and 29.3:

540 509.3 (74.5 43.8)

Total sources 152.8

Uses:

Investment in net working 38.5 See Table 29.2: (900 460)

capital (848 446.5)

Investment in fixed assets 70.5 See Table 29.2: 1000 929.5

Dividends 43.8 See Table 29.3

Total uses 152.8

TABLE 29.4

Sources and uses of

funds for Executive

Paper Corporation,

1999 (figures in

$ millions).

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

IX. Financial Planning and

Short−Term Management

29. Financial Analysis and

Planning

© The McGraw−Hill

Companies, 2003

Look first at the uses of funds. The money that Executive Paper generates is ei-

ther invested in net working capital and fixed assets or it is paid out to sharehold-

ers as dividends. Thus

Table 29.2 shows that in 1999 Executive Paper started the year with net working

capital of million. By the end of the year it had grown to

million. So the company invested an additional $38.5 million

in working capital. Over the same period fixed assets rose from $929.5 million

to $1,000 million, an increase of $70.5 million. Finally, the income statement in

Table 29.3 shows that Executive Paper distributed $43.8 million as dividends.

Thus, in total, Executive Paper invested or paid out as dividends 38.5 70.5

43.8 $152.8 million.

Where did the funds come from? There are two sources—the cash generated

from operations and new money raised from investors:

The income statement shows that in 1999 the company generated $127.8 million

from operations. This included $53.3 million of depreciation (remember deprecia-

tion is not a cash outflow) and $74.5 million of net income. This left a deficiency of

million that Executive Paper needed to raise from the capital

market. You can see from the balance sheet that Executive Paper raised this $25 mil-

lion by an issue of long-term debt (debt increased from $425 million to $450 mil-

lion). Executive Paper did not issue new equity capital in 1999. So why does the

balance sheet show an increase in equity of million? The an-

swer is that this increase in equity came from income that the company retained

and plowed back on behalf of its shareholders

. dividends 74.5 43.8 $30.7

million2

1retained earnings net income

540 509.3 $30.7

152.8 127.8 $25

new issues of equity

Total sources of funds operating cash flow new issues of long-term debt

900 460 $440

848 446.5 $401.5

in fixed assets dividends paid to shareholders

Total uses of funds investment in net working capital investment

822 PART IX

Financial Planning and Short-Term Management

29.3 MEASURING EXECUTIVE PAPER’S FINANCIAL

CONDITION

Executive Paper’s financial statements provide you with the basic information to

assess its current financial standing. However, financial statements typically con-

tain large amounts of data—far more than is contained in the simplified statements

for Executive Paper. To condense these data into a convenient form, financial man-

agers generally focus on a few key financial ratios.

Table 29.5 summarizes the key financial ratios for Executive Paper.

5

We

will explain how to calculate these ratios and use them to shed light on five

questions:

• How much has the company borrowed? Is the amount of debt likely to result

in financial distress?

• How liquid is the company? Can it easily lay its hands on cash if needed?

5

In addition to the ratios that we describe below, Table 29.5 includes a few other ratios that you may well

encounter. Some are simply alternative ways to express the same result; others are variations on a theme.

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

IX. Financial Planning and

Short−Term Management

29. Financial Analysis and

Planning

© The McGraw−Hill

Companies, 2003

• How productively is the company using its assets? Are there any signs that the

assets are not being used efficiently?

• How profitable is the company?

• How highly is the firm valued by investors? Are investors’ expectations

reasonable?

CHAPTER 29

Financial Analysis and Planning 823

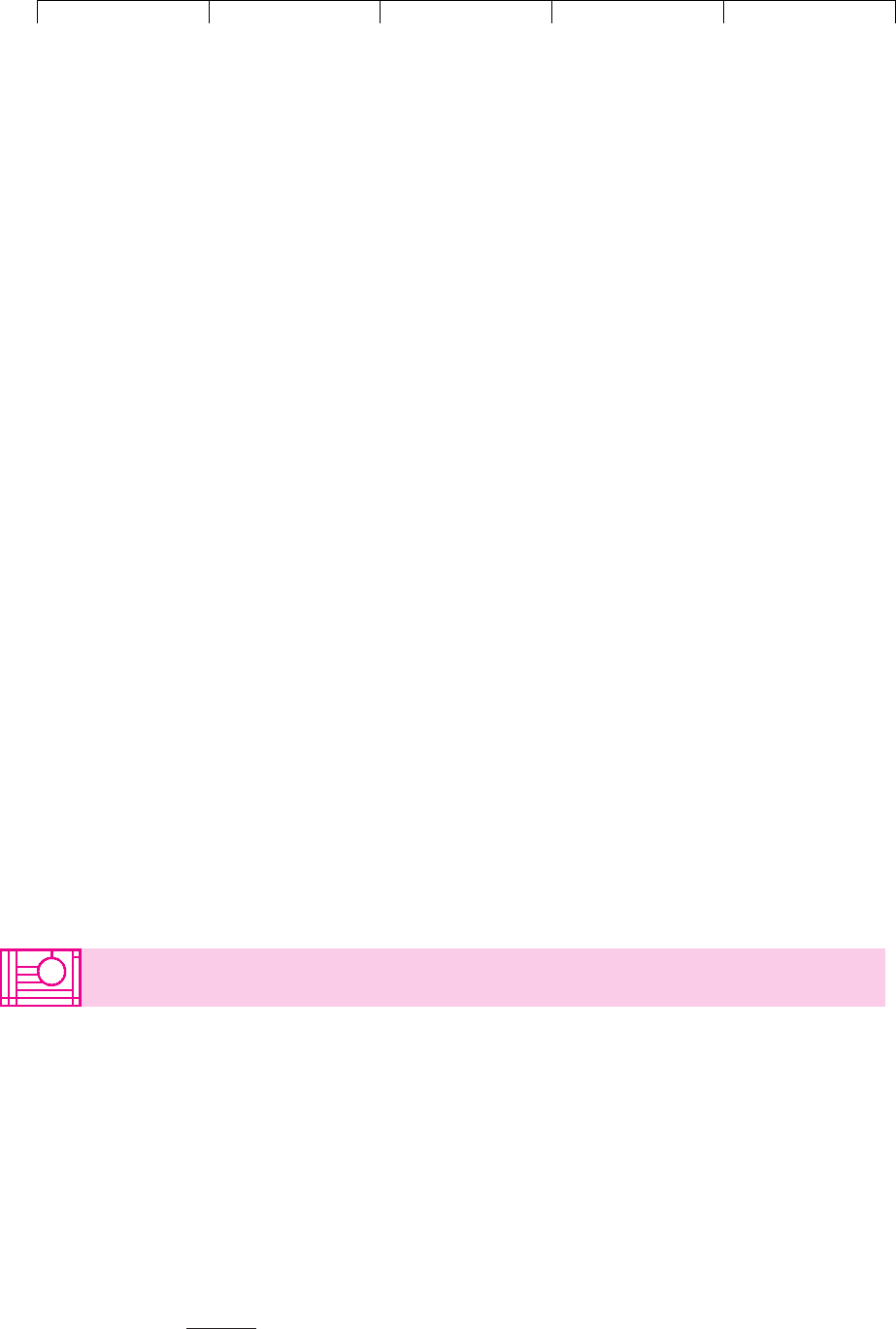

Executive Paper

Paper Industry

†

Leverage Ratios:

Debt ratio (Long-term debt leases)/(long-term .45 .53

debt leases equity)

Debt ratio (including (Long-term debt short-term debt .50 .56

short-term debt)* leases)/(long-term debt short-term debt

leases equity)

Debt–equity ratio (Long-term debt leases)/equity .83 1.12

Times-interest-earned (EBIT depreciation)/interest 5.2 2.9

Liquidity Ratios:

Net-working-capital- (Current assets current liabilities)/total assets .30 .06

to-total assets*

Current ratio Current assets/current liabilities 2.0 1.3

Quick ratio (Cash short-term securities receivables)/ 1.2 .7

current liabilities

Cash ratio (Cash short-term securities)/current liabilities .2 .1

Interval measure* (Cash short-term securities receivables)/ 101.4 61.7

(costs from operations/365)

Efficiency Ratios:

Sales-to-assets ratio Sales/average total assets 1.55 .90

Sales-to-net-working- Sales/average net working capital 5.2 14.1

capital*

Days in inventory Average inventory/(cost of goods sold/365) 63.6 59.1

Inventory turnover* Cost of goods sold/average inventory 5.7 6.2

Average collection Average receivables/(sales/365) 72.4 45.9

period (days)

Receivables turnover* Sales/average receivables 5.0 8.0

Profitability Ratios:

Net profit margin (EBIT tax)/sales 5.3% 0.5%

Return on assets (ROA) (EBIT tax)/average total assets 8.3% 0.4%

Return on equity (ROE) Earnings available for common stockholders/ 14.2% 10.3%

average equity

Payout ratio Dividend per share/earnings per share .6 n.a.

Market-Value Ratios:

Price–earnings ratio (P/E) Stock price/earnings per share 9.5 n.a

Dividend yield Dividend per share/stock price 6.2% 1.8%

Market-to-book ratio Stock price/book value per share 1.3 3.6

TABLE 29.5

Financial ratios for Executive Paper and the paper industry, 1999.

*This ratio is an extra bonus not discussed in Section 29.2.

†

1999 ratios for U.S. paper and allied products.

Source: Compustat.

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

IX. Financial Planning and

Short−Term Management

29. Financial Analysis and

Planning

© The McGraw−Hill

Companies, 2003

When you calculate a company’s financial ratios, you need some criteria to decide

whether they are a cause for concern or a matter for congratulation. Unfortunately,

there is no “right” set of financial ratios to which all companies should aspire. Take,

for example, the company’s capital structure. Debt has both advantages and dis-

advantages, and, even if there were an optimal level of debt for company A, it would

not be appropriate for company B.

When managers review a company’s financial position, they often start by

comparing the current year’s ratios with equivalent figures for earlier years. It

is also helpful to look at how the company’s financial position measures up to

that of other firms in the same industry. Therefore, in Table 29.5 we have

compared the financial ratios of Executive Paper with those for the U.S. paper

industry.

6

How Much Has Executive Paper Borrowed?

When Executive Paper borrows, it promises to make a series of fixed payments. Be-

cause its shareholders get only what is left over after the debtholders have been

paid, the debt is said to create financial leverage. In extreme cases, if hard times

come, a company may be unable to pay its debts.

The company’s bankers and bondholders also want to make certain that Execu-

tive Paper does not borrow excessively. So, if Executive wishes to take out a new

loan, the lenders will scrutinize several measures of whether the company is bor-

rowing too much and will demand that it keep its debt within reasonable bounds.

Such borrowing limits are stated in terms of financial ratios.

Debt Ratio Financial leverage is usually measured by the ratio of long-term debt

to total long-term capital. Since long-term lease agreements also commit the firm

to a series of fixed payments, it makes sense to include the value of lease obliga-

tions with the long-term debt. For Executive Paper

Another way to say the same thing is that Executive Paper has a debt-to-equity ra-

tio of :

Notice that this measure makes use of book (i.e., accounting) values rather than

market values.

7

The market value of the company finally determines whether

the debtholders get their money back, so you might expect analysts to look at

450/540 .83

Debt– equity ratio

1long-term debt value of leases2

equity

450/540 .83

450/1450 5402 .45

Debt ratio

1long-term debt value of leases2

1long-term debt value of leases equity2

824 PART IX

Financial Planning and Short-Term Management

6

Financial ratios for different industries are published by the U.S. Department of Commerce, Dun and

Bradstreet, The Risk Management Association, and others.

7

In the case of leased assets accountants try to estimate the present value of the lease commitments.

In the case of long-term debt they simply show the face value. This can sometimes be very different

from present value. For example, the present value of low-coupon debt may be only a fraction of its

face value. The difference between the book value of equity and its market value can be even more

dramatic.

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

IX. Financial Planning and

Short−Term Management

29. Financial Analysis and

Planning

© The McGraw−Hill

Companies, 2003

the face amount of the debt as a proportion of the total market value of debt and

equity. On the other hand, the market value includes the value of intangible as-

sets generated by research and development, advertising, staff training, and so

on. These assets are not readily salable, and if the company falls on hard times,

their value may disappear altogether. For some purposes, it may be just as good

to follow the accountant and ignore these intangible assets. This is what lenders

do when they insist that the borrower should not allow the book debt ratio to

exceed a specified limit.

Debt ratios are sometimes defined in other ways. For example, analysts may in-

clude short-term debt or other obligations such as payables. There is a general

point here. There are a variety of ways to define most financial ratios and there is

no law stating how they should be defined. So be warned: Don’t accept a ratio at

face value without understanding how it has been calculated.

Times-Interest-Earned (or Interest Cover) Another measure of financial leverage

is the extent to which interest is covered by earnings before interest and taxes

(EBIT) plus depreciation. For Executive Paper,

8

The regular interest payment is a hurdle that companies must keep jumping if they

are to avoid default. The times-interest-earned ratio measures how much clear air

there is between hurdle and hurdler.

Is Executive Paper’s borrowing in the ballpark of standard practice or is it a mat-

ter for concern? Table 29.5 provides some clues. You can see that the debt ratio is

slightly lower than that of the rest of the paper industry and the times-interest-

earned is significantly higher than that of most companies.

How Liquid Is Executive Paper?

If Executive Paper is borrowing for a short period or has some large bills coming

up for payment, you want to make sure that it can lay its hands on the cash when

it is needed. The company’s bankers and suppliers also need to keep an eye on Ex-

ecutive’s liquidity. They know that illiquid firms are more likely to fail and default

on their debts.

Another reason that analysts focus on liquid assets is that the figures are often

more reliable. The book value of Executive’s newsprint mill may be a poor guide

to its true value, but at least you know what its cash in the bank is worth. Liquid-

ity ratios also have some less desirable characteristics. Because short-term assets

and liabilities are easily changed, measures of liquidity can rapidly become out-of-

date. You may not know what that newsprint mill is worth, but you can be fairly

sure that it won’t disappear overnight.

1166.7 53.32

42.5

5.2

Times-interest-earned

1EBIT depreciation2

interest

CHAPTER 29

Financial Analysis and Planning 825

8

The numerator of times-interest-earned can be defined in several ways. Sometimes depreciation is ex-

cluded. Sometimes it is just earnings plus interest, that is, earnings before interest but after tax. This last

definition seems nutty to us, because the point of interest earned is to assess the risk that the firm won’t

have enough money to pay interest. If EBIT falls below interest obligations, the firm won’t have to

worry about taxes. Interest is paid before the firm pays taxes.

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

IX. Financial Planning and

Short−Term Management

29. Financial Analysis and

Planning

© The McGraw−Hill

Companies, 2003

Current Ratio Executive Paper’s current assets consist of cash and assets that can

readily be turned into cash. Its current liabilities consist of payments that the company

expects to make in the near future. Thus the ratio of the current assets to the current

liabilities measures the margin of liquidity. It is known as the current ratio:

Rapid decreases in the current ratio sometimes signify trouble. However, they can

also be misleading. For example, suppose that a company borrows a large sum

from the bank and invests it in short-term securities. If nothing else happens, net

working capital is unaffected, but the current ratio changes. For this reason it might

be preferable to net off the short-term investments and the short-term debt when

calculating the current ratio.

Quick (or Acid-Test) Ratio Some assets are closer to cash than others. If trouble

comes, inventories may not sell at anything above fire-sale prices. (Trouble typi-

cally comes because customers are not buying and the firm’s warehouse is stuffed

with unwanted goods.) Thus, managers often focus only on cash, short-term secu-

rities, and bills that customers have not yet paid:

Cash Ratio A company’s most liquid assets are its holdings of cash and mar-

ketable securities. That is why analysts also look at the cash ratio:

Of course, these summary measures of liquidity are just that. They are no substi-

tute for detailed plans to ensure that the company can pay its bills. In the next chap-

ter we will describe how companies forecast their cash needs and draw up a short-

term financial plan to deal with any cash shortage.

How Productively Is Executive Paper Using Its Assets?

Financial analysts employ another set of ratios to judge how efficiently the firm is

using its investment in current and fixed assets. Later in the chapter we will look

at the financial implications of Executive’s ambitious plans to expand output, but

understanding the investment in fixed assets and working capital that is needed to

support Executive Paper’s current output may help to uncover any inconsistencies

in these plans for the future.

Sales-to-Assets (or Asset Turnover) Ratio The sales-to-assets ratio shows how

hard the firm’s assets are being put to use:

Sales

average total assets

2, 200

11, 380.8 1, 4502/2

1.55

Cash ratio

1cash short-term securities2

current liabilities

110

460

.24

110 440

460

1.20

Quick ratio

1cash short-term securities receivables2

current liabilities

Current ratio

current assets

current liabilities

900

460

1.96

826 PART IX Financial Planning and Short-Term Management

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

IX. Financial Planning and

Short−Term Management

29. Financial Analysis and

Planning

© The McGraw−Hill

Companies, 2003

Assets here are measured as the sum of current and fixed assets. Notice that since

assets are likely to change over the course of a year, we use the average of the as-

sets at the beginning and end of the year. Averages are commonly used whenever

a flow figure (in this case, sales) is compared with a stock or snapshot figure (to-

tal assets).

Notice that for each dollar of investment Executive generates $1.55 of sales, a

much higher figure than other paper companies. There are several possible ex-

planations: (1) Executive uses its assets more efficiently; (2) Executive is working

close to capacity, so that it may be difficult to increase sales without additional

invested capital; or (3) compared with its rivals, Executive produces high vol-

ume, low margin products.

9

You need to dig deeper to know which explanation

is correct. Remember our earlier comment—financial ratios help you to ask the

right questions, not to answer them.

Instead of looking at the ratio of sales to total assets, managers sometimes look

at how hard particular types of capital are being put to use. For example, it turns

out that Executive’s ratio of sales to current assets is less than that of other paper

companies. It is the ratio of Executive’s sales to its fixed assets that sets it apart

from its rivals.

Days in Inventory The speed with which a company turns over its inventory is

measured by the number of days that it takes for the goods to be produced and

sold. First convert the cost of goods sold to a daily basis by dividing by 365.

Then express inventories as a multiple of the daily cost of goods sold:

Notice that Executive Paper appears to have a relatively low rate of inventory

turnover. Perhaps there is scope for economizing on the company’s investment

in inventories.

Average Collection Period The average collection period measures how quickly

customers pay their bills:

The collection period for Executive Paper is somewhat longer than the industry av-

erage. The company may have a conscious policy of offering attractive credit terms

to lure business, but it is worth looking at whether the credit manager is lax in chas-

ing up the slow payers.

1433.1 4402/2

2,200/365

72.4 days

Average collection period

average receivables

sales 365

1339.9 3502/2

1,980/365

63.6 days

Days in inventory

average inventory

cost of goods sold 365

CHAPTER 29

Financial Analysis and Planning 827

9

We will see shortly that this last explanation does not hold up. The paper industry in 1999 earned a

negative profit margin.