Brealey, Myers. Principles of Corporate Finance. 7th edition

Подождите немного. Документ загружается.

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

IX. Financial Planning and

Short−Term Management

29. Financial Analysis and

Planning

© The McGraw−Hill

Companies, 2003

848 PART IX Financial Planning and Short-Term Management

depreciation is 10 percent of fixed assets at the start of the year. Fixed costs are ex-

pected to remain at $56, and variable costs, at 80 percent of revenue. The company’s

policy is to pay out two-thirds of net income as dividends and to maintain a book

debt ratio of 25 percent of total capital.

a. Produce a set of financial statements for 2007. Assume that net working capital will

equal 50 percent of fixed assets.

b. Now assume that the balancing item is debt and that no equity is to be issued.

Prepare a completed pro forma balance sheet for 2007. What is the projected debt

ratio for 2003?

32. The financial statements of Eagle Sport Supply are shown in Table 29.15. For simplicity,

“Costs” include interest. Assume that Eagle’s assets are proportional to its sales.

a. Find Eagle’s required external funds if it maintains a dividend payout ratio of

60 percent and plans a growth rate of 15 percent in 2003.

b. If Eagle chooses not to issue new shares of stock, what variable must be the

balancing item? What will its value be?

c. Now suppose that the firm plans instead to increase long-term debt only to $1,100

and does not wish to issue any new shares of stock. Why must the dividend

payment now be the balancing item? What will its value be?

33. a. What is the internal growth rate of Eagle Sports (see problem 32) if the dividend pay-

out ratio is fixed at 60 percent and the equity-to-asset ratio is fixed at 2/3?

b. What is the sustainable growth rate?

34. Bio-Plasma Corp. is growing at 30 percent per year. It is all-equity-financed and has

total assets of $1 million. Its return on equity is 20 percent. Its plowback ratio is

40 percent.

a. What is the internal growth rate?

b. What is the firm’s need for external financing this year?

c. By how much would the firm increase its internal growth rate if it reduced its

payout rate to zero?

d. By how much would such a move reduce the need for external financing? What do

you conclude about the relationship between dividend policy and requirements for

external financing?

CHALLENGE

QUESTIONS

1. Take another look at Geomorph Trading’s balance sheet in quiz question 9, and con-

sider the following additional information:

Visit us at www.mhhe.com/bm7e

Current Assets Current Liabilities Other Liabilities

Cash 15 Payables 35 Deferred tax 32

Inventories 35 Taxes due 10 Unfunded pensions 22

Receivables 50 Bank loan 15 R&R reserve 16

100 60 70

The “R&R reserve” covers the future costs of removal of an oil pipeline and environ-

mental restoration of the pipeline route.

There are many ways to calculate a debt ratio for Geomorph. Suppose you are eval-

uating the safety of Geomorph’s debt and want a debt ratio for comparison with the ra-

tios of other companies in the same industry. Would you calculate the ratio in terms of

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

IX. Financial Planning and

Short−Term Management

29. Financial Analysis and

Planning

© The McGraw−Hill

Companies, 2003

CHAPTER 29 Financial Analysis and Planning 849

Visit us at www.mhhe.com/bm7e

total liabilities or total capitalization? What would you include in debt—the bank loan,

the deferred tax account, the R&R reserve, the unfunded pension liability? Explain the

pros and cons of these choices.

2. Take any firm whose financial statements are shown on the Market Insight database

(www

.mhhe.com/edumarketinsight

) and make some plausible forecasts for future

growth and the asset base needed to support that growth. Then use a spreadsheet pro-

gram to develop a five-year financial plan. What financing is needed to support the

planned growth? How vulnerable is the company to an error in your forecasts?

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

IX. Financial Planning and

Short−Term Management

30. Short−Term Financial

Planning

© The McGraw−Hill

Companies, 2003

CHAPTER THIRTY

850

SHORT-TERM

F I N A N C I A L

P L A N N I N G

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

IX. Financial Planning and

Short−Term Management

30. Short−Term Financial

Planning

© The McGraw−Hill

Companies, 2003

MOST OF THIS book is devoted to long-term financial decisions such as capital budgeting and the

choice of capital structure. Such decisions are called long-term for two reasons. First, they usually in-

volve long-lived assets or liabilities. Second, they are not easily reversed and therefore may commit

the firm to a particular course of action for several years.

Short-term financial decisions generally involve short-lived assets and liabilities, and usually they

are easily reversed. Compare, for example, a 60-day bank loan for $50 million with a $50 million is-

sue of 20-year bonds. The bank loan is clearly a short-term decision. The firm can repay it two months

later and be right back where it started. A firm might conceivably issue a 20-year bond in January and

retire it in March, but it would be extremely inconvenient and expensive to do so. In practice, such a

bond issue is a long-term decision, not only because of the bond’s 20-year maturity but also because

the decision to issue it cannot be reversed on short notice.

A financial manager responsible for short-term financial decisions does not have to look far into

the future. The decision to take the 60-day bank loan could properly be based on cash-flow forecasts

for the next few months only. The bond issue decision will normally reflect forecasted cash require-

ments 5, 10, or more years into the future.

Managers concerned with short-term financial decisions can avoid many of the difficult conceptual

issues encountered elsewhere in this book. In a sense, short-term decisions are easier than long-term

decisions, but they are not less important. A firm can identify extremely valuable capital investment op-

portunities, find the precise optimal debt ratio, follow the perfect dividend policy, and yet founder be-

cause no one bothers to raise the cash to pay this year’s bills. Hence the need for short-term planning.

We start the chapter with an overview of the major classes of short-term assets and liabilities. We

show how long-term financing decisions affect the firm’s short-term financial planning problem. We

describe how financial managers trace changes in cash and working capital, and we look at how they

forecast month-by-month cash requirements or surpluses and develop short-term financing strate-

gies. We conclude by examining more closely the principal sources of short-term finance.

851

30.1 THE COMPONENTS OF WORKING CAPITAL

Short-term, or current, assets and liabilities are collectively known as working cap-

ital. Table 30.1 gives a breakdown of current assets and liabilities for all manufac-

turing corporations in the United States in 2000. Note that current assets are larger

than current liabilities. Net working capital (current assets less current liabilities)

was positive.

Current Assets

One important current asset is accounts receivable. When one company sells goods

to another company or a government agency, it does not usually expect to be paid

immediately. These unpaid bills, or trade credit, make up the bulk of accounts re-

ceivable. Companies also sell goods on credit to the final consumer. This consumer

credit makes up the remainder of accounts receivable. We will discuss the manage-

ment of receivables in Chapter 32. You will learn how companies decide which cus-

tomers are good or bad credit risks and when it makes sense to offer credit.

Another important current asset is inventory. Inventories may consist of raw

materials, work in process, or finished goods awaiting sale and shipment. Firms

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

IX. Financial Planning and

Short−Term Management

30. Short−Term Financial

Planning

© The McGraw−Hill

Companies, 2003

invest in inventory. The cost of holding inventory includes not only storage cost

and the risk of spoilage or obsolescence but also the opportunity cost of capital,

that is, the rate of return offered by other, equivalent-risk investment opportu-

nities.

1

The benefits of holding inventory are often indirect. For example, a large

inventory of finished goods (large relative to expected sales) reduces the chance

of a “stockout” if demand is unexpectedly high. A producer holding a small

finished-goods inventory is more likely to be caught short, unable to fill orders

promptly. Similarly, large inventories of raw materials reduce the chance that an

unexpected shortage would force the firm to shut down production or use a

more costly substitute material.

Bulk orders for raw materials lead to large average inventories but may be

worthwhile if the firm can obtain lower prices from suppliers. (That is, bulk orders

may yield quantity discounts.) Firms are often willing to hold large inventories of

finished goods for similar reasons. A large inventory of finished goods allows

longer, more economical production runs. In effect, the production manager gives

the firm a quantity discount.

The task of inventory management is to assess these benefits and costs and to

strike a sensible balance. In manufacturing companies the production manager is

best placed to make this judgment. Since the financial manager is not usually di-

rectly involved in inventory management, we will not discuss the inventory prob-

lem in detail.

The remaining current assets are cash and marketable securities. The cash con-

sists of currency, demand deposits (funds in checking accounts), and time deposits

(funds in savings accounts). The principal marketable security is commercial pa-

per (short-term, unsecured notes sold by other firms). Other securities include U.S.

Treasury bills and state and local government securities.

In choosing between cash and marketable securities, the financial manager faces

a task like that of the production manager. There are always advantages to holding

large “inventories” of cash—they reduce the risk of running out of cash and hav-

ing to raise more on short notice. On the other hand, there is a cost to holding idle

852 PART IX

Financial Planning and Short-Term Management

Current Assets Current Liabilities

Cash 156.3 Short-term loans 228.4

Marketable securities 104.4 Accounts payable 357.3

Accounts receivable 527.2 Accrued income taxes 55.5

Inventories 510.7 Current payments due 85.3

on long-term debt

Other current assets 248.9 Other current liabilities 507.4

Total 1547.5 Total 1233.9

Net working capital (current assets ⫺ current liabilities) ⫽ $1,547.5 ⫺ 1,233.9

⫽ $313.6 billion

TABLE 30.1

Current assets and liabilities

for U.S. manufacturing

corporations, first quarter,

2001 (figures in $ billions).

Source: U.S. Census Bureau,

Quarterly Financial Report for

Manufacturing, Mining and

Trade Corporations, First

Quarter, 2001 (www.census.

gov/prod/www/abs/qfr-mm).

1

How risky are inventories? It is hard to generalize. Many firms just assume inventories have the same

risk as typical capital investments and therefore calculate the cost of holding inventories using the

firm’s average opportunity cost of capital. You can think of many exceptions to this rule of thumb how-

ever. For example, some electronics components are made with gold connections. Should an electron-

ics firm apply its average cost of capital to its inventory of gold? (See Section 11.1.)

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

IX. Financial Planning and

Short−Term Management

30. Short−Term Financial

Planning

© The McGraw−Hill

Companies, 2003

cash balances rather than putting the money to work in marketable securities. In

Chapter 31 we will tell you how the financial manager collects and pays out cash

and decides on an optimal cash balance.

Current Liabilities

We have seen that a company’s principal current asset consists of unpaid bills from

other companies. One firm’s credit must be another’s debit. Therefore, it is not sur-

prising that a company’s principal current liability often consists of accounts

payable, that is, outstanding payments to other companies. A firm that delays pay-

ing its bills is in effect borrowing money from its suppliers. So companies that are

strapped for cash sometimes solve the problem by stretching payables.

To finance its investment in current assets, a company may rely on a variety of

short-term loans. Banks and finance companies are the largest source of such loans,

but companies may also issue short-term debt, called commercial paper. We will de-

scribe the different kinds of short-term debt toward the end of the chapter.

CHAPTER 30

Short-Term Financial Planning 853

30.2 LINKS BETWEEN LONG-TERM AND SHORT-TERM

FINANCING DECISIONS

All businesses require capital, that is, money invested in plant, machinery, invento-

ries, accounts receivable, and all the other assets it takes to run a business efficiently.

Typically, these assets are not purchased all at once but obtained gradually over time.

Let us call the total cost of these assets the firm’s cumulative capital requirement.

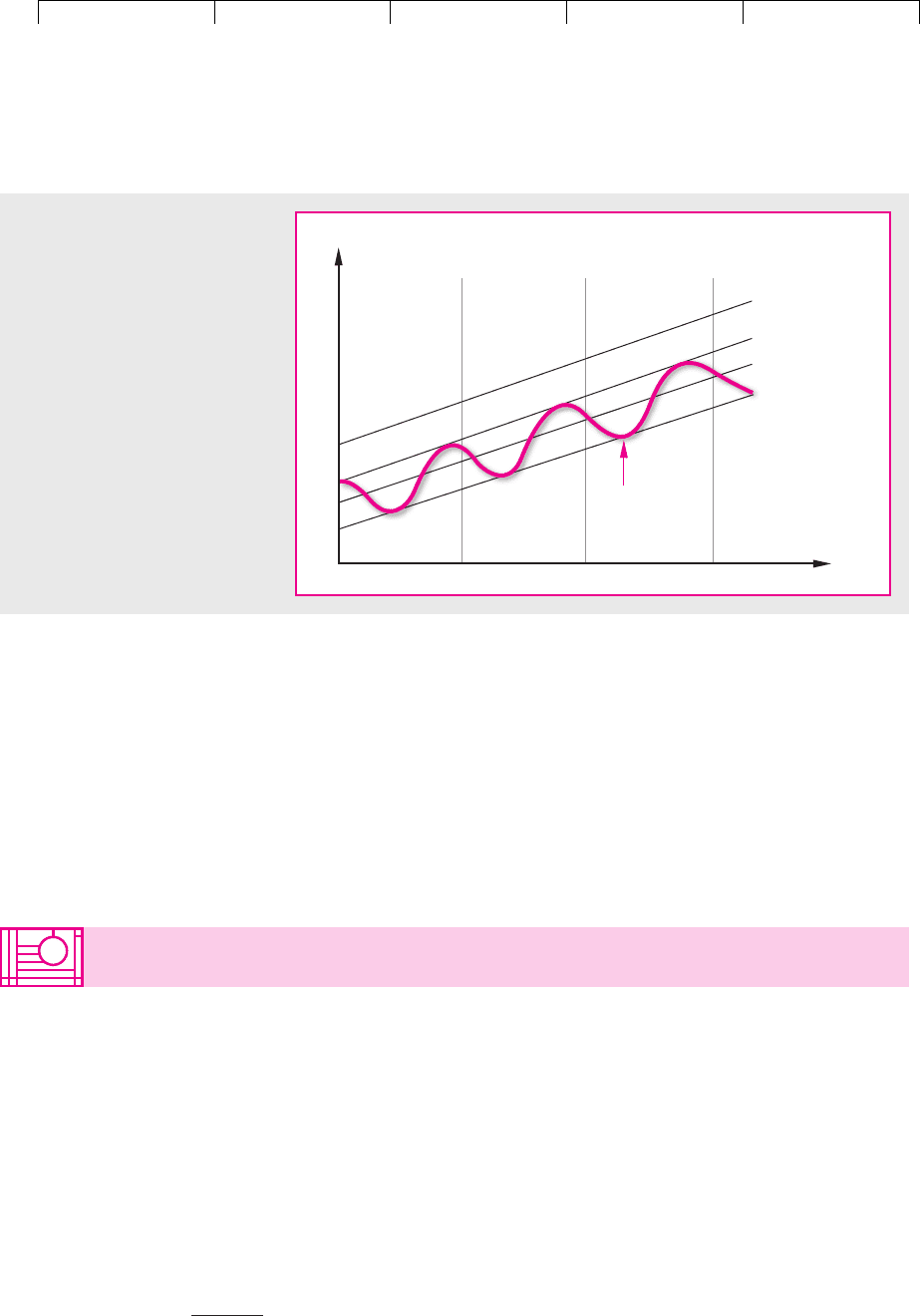

Most firms’ cumulative capital requirement grows irregularly, like the wavy line

in Figure 30.1. This line shows a clear upward trend as the firm’s business grows.

But there is also seasonal variation around the trend: In the figure the capital re-

quirements peak late in each year. Finally, there would be unpredictable week-to-

week and month-to-month fluctuations, but we have not attempted to show these

in Figure 30.1.

The cumulative capital requirement can be met from either long-term or short-

term financing. When long-term financing does not cover the cumulative capital

requirement, the firm must raise short-term capital to make up the difference.

When long-term financing more than covers the cumulative capital requirement,

the firm has surplus cash available for short-term investment. Thus the amount of

long-term financing raised, given the cumulative capital requirement, determines

whether the firm is a short-term borrower or lender.

Lines A, B, and C in Figure 30.1 illustrate this. Each depicts a different long-term

financing strategy. Strategy A always implies a short-term cash surplus. Strategy C

implies a permanent need for short-term borrowing. Under B, which is probably

the most common strategy, the firm is a short-term lender during part of the year

and a borrower during the rest.

What is the best level of long-term financing relative to the cumulative capital

requirement? It is hard to say. There is no convincing theoretical analysis of this

question. We can make practical observations, however. First, most financial man-

agers attempt to “match maturities” of assets and liabilities. That is, they finance

long-lived assets like plant and machinery with long-term borrowing and equity.

Second, most firms make a permanent investment in net working capital (current

assets less current liabilities). This investment is financed from long-term sources.

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

IX. Financial Planning and

Short−Term Management

30. Short−Term Financial

Planning

© The McGraw−Hill

Companies, 2003

The Comforts of Surplus Cash

Many financial managers would feel more comfortable under strategy A than strat-

egy C. Strategy A

⫹

(the highest line) would be still more relaxing. A firm with a sur-

plus of long-term financing never has to worry about borrowing to pay next month’s

bills. But is the financial manager paid to be comfortable? Firms usually put surplus

cash to work in Treasury bills or other marketable securities. This is at best a zero-

NPV investment for a taxpaying firm.

2

Thus we think that firms with a permanent

cash surplus ought to go on a diet, retiring long-term securities to reduce long-term

financing to a level at or below the firm’s cumulative capital requirement. That is, if

the firm is on line A

⫹

, it ought to move down to line A, or perhaps even lower.

854 PART IX

Financial Planning and Short-Term Management

Dollars

Cumulative

capital

requirement

Year 1 Year 2 Year 3

Time

A

+

B

C

A

FIGURE 30.1

The firm’s cumulative capital require-

ment (colored line) is the cumulative

investment in all the assets needed

for the business. In this case the

requirement grows year by year, but

there is seasonal fluctuation within

each year. The requirement for

short-term financing is the differ-

ence between long-term financing

(lines A

⫹

, A, B, and C) and the cumu-

lative capital requirement. If long-

term financing follows line C, the

firm always needs short-term

financing. At line B, the need is

seasonal. At lines A and A

⫹

, the firm

never needs short-term financing.

There is always extra cash to invest.

2

If there is a tax advantage to borrowing, as most people believe, there must be a corresponding tax dis-

advantage to lending, and investment in Treasury bills has a negative NPV. See Section 18.1.

30.3 TRACING CHANGES IN CASH AND WORKING

CAPITAL

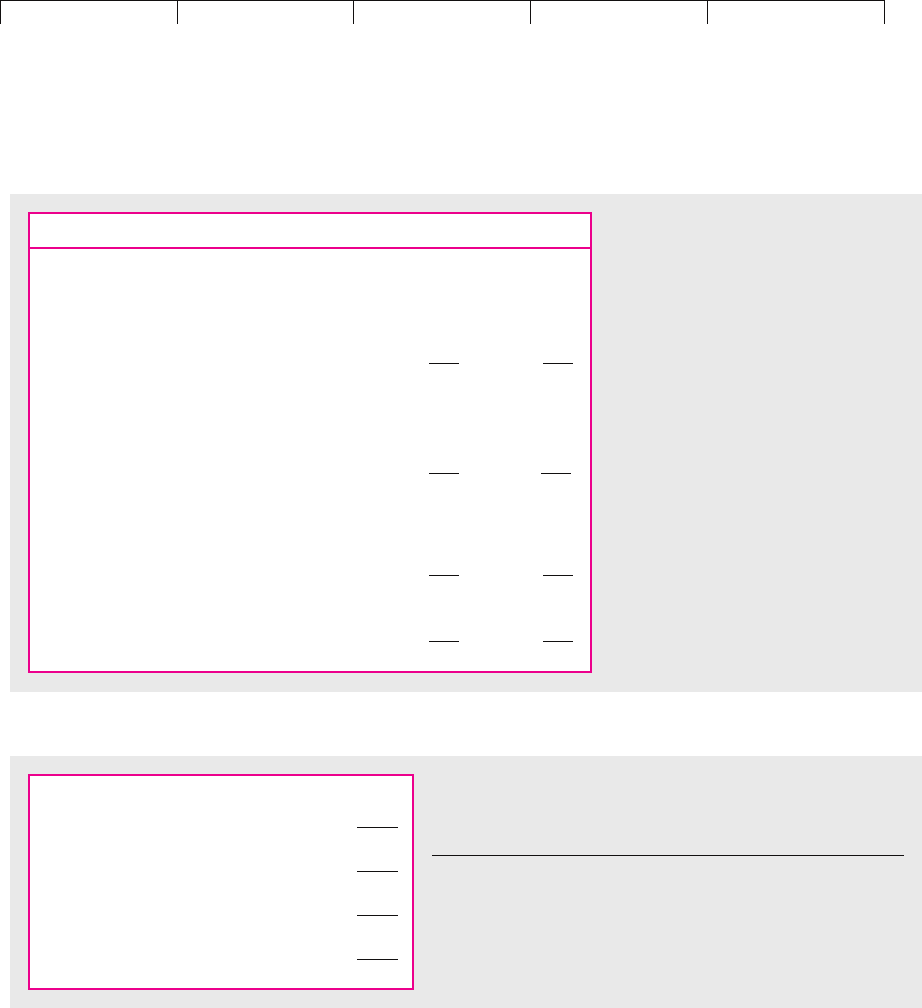

Table 30.2 compares 2000 and 2001 year-end balance sheets for Dynamic Mattress

Company. Table 30.3 shows the firm’s income statement for 2001. Note that Dynamic’s

cash balance increased by $1 million during 2001. What caused this increase? Did the

extra cash come from Dynamic Mattress Company’s additional long-term borrowing,

from reinvested earnings, from cash released by reducing inventory, or from extra

credit extended by Dynamic’s suppliers? (Note the increase in accounts payable.)

The correct answer is “all the above.” Financial analysts often summarize

sources and uses of cash in a statement like the one shown in Table 30.4. The state-

ment shows that Dynamic generated cash from the following sources:

1. It issued $7 million of long-term debt.

2. It reduced inventory, releasing $1 million.

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

IX. Financial Planning and

Short−Term Management

30. Short−Term Financial

Planning

© The McGraw−Hill

Companies, 2003

3. It increased its accounts payable, in effect borrowing an additional $7

million from its suppliers.

4. By far the largest source of cash was Dynamic’s operations, which

generated $16 million. See Table 30.3, and note: Income ($12 million)

understates cash flow because depreciation is deducted in calculating

income. Depreciation is not a cash outlay. Thus, it must be added back in

order to obtain operating cash flow.

Dynamic used cash for the following purposes:

1. It paid a $1 million dividend. (Note: The $11 million increase in Dynamic’s

equity is due to retained earnings: $12 million of equity income, less the

$1 million dividend.)

CHAPTER 30

Short-Term Financial Planning 855

2000 2001

Current assets:

Cash 4 5

Marketable securities 0 5

Inventory 26 25

Accounts receivable 25 30

Total current assets 55 65

Fixed assets:

Gross investment 56 70

Less depreciation ⫺16 ⫺20

Net fixed assets 40 50

Total assets 95 115

Current liabilities:

Bank loans 5 0

Accounts payable 20 27

Total current liabilities 25 27

Long-term debt 5 12

Net worth (equity and retained earnings) 65 76

Total liabilities and net worth 95 115

TABLE 30.2

Year-end balance sheets for 2000 and

2001 for Dynamic Mattress Company

(figures in $ millions).

Sales 350

Operating costs ⫺321

29

Depreciation ⫺4

25

Interest ⫺1

Pretax income 24

Tax at 50% ⫺12

Net income 12

TABLE 30.3

Income statement for Dynamic Mattress Company, 2001 (figures

in $ millions).

Note: Dividend ⫽ $1 million; retained earnings ⫽ $11 million.

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

IX. Financial Planning and

Short−Term Management

30. Short−Term Financial

Planning

© The McGraw−Hill

Companies, 2003

2. It repaid a $5 million short-term bank loan.

3

3. It invested $14 million. This shows up as the increase in gross fixed assets in

Table 30.2.

4. It purchased $5 million of marketable securities.

5. It allowed accounts receivable to expand by $5 million. In effect, it lent this

additional amount to its customers.

Tracing Changes in Net Working Capital

Financial analysts often find it useful to collapse all current assets and liabilities

into a single figure for net working capital. Dynamic’s net-working-capital bal-

ances were (in millions):

856 PART IX

Financial Planning and Short-Term Management

Sources:

Issued long-term debt 7

Reduced inventories 1

Increased accounts payable 7

Cash from operations:

Net income 12

Depreciation 4

Total sources 31

Uses:

Repaid short-term bank loan 5

Invested in fixed assets 14

Purchased marketable securities 5

Increased accounts receivable 5

Dividend 1

Total uses 30

Increase in cash balance 1

TABLE 30.4

Sources and uses of cash for Dynamic Mattress

Company, 2001 (figures in $ millions).

3

This is principal repayment, not interest. Sometimes interest payments are explicitly recognized as a

use of funds. If so, operating cash flow would be defined before interest, that is, as net income plus in-

terest plus depreciation.

4

We drew up a sources and uses of funds statement for Executive Paper in Section 29.1.

Current Current Net Working

Assets Less Liabilities Equals Capital

Year-end 2000 $55 ⫺ $25 ⫽ $30

Year-end 2001 $65 ⫺ $27 ⫽ $38

Table 30.5 gives balance sheets which report only net working capital, not indi-

vidual current asset or liability items.

“Sources and uses” statements can likewise be simplified by defining sources as

activities which contribute to net working capital and uses as activities which use

up working capital. In this context working capital is usually referred to as funds,

and a sources and uses of funds statement is presented.

4

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

IX. Financial Planning and

Short−Term Management

30. Short−Term Financial

Planning

© The McGraw−Hill

Companies, 2003

In 2000, Dynamic contributed to net working capital by

1. Issuing $7 million of long-term debt.

2. Generating $16 million from operations.

It used up net working capital by

1. Investing $14 million.

2. Paying a $1 million dividend.

The year’s changes in net working capital are thus summarized by Dynamic Mat-

tress Company’s sources and uses of funds statement, given in Table 30.6.

Profits and Cash Flow

Now look back to Table 30.4, which shows sources and uses of cash. We want to reg-

ister two warnings about the entry called cash from operations. It may not actually

represent real dollars—dollars you can buy beer with.

First, depreciation may not be the only noncash expense deducted in calculat-

ing income. For example, most firms use different accounting procedures in their

tax books than in their reports to shareholders. The point of special tax accounts

is to minimize current taxable income. The effect is that the shareholder books

CHAPTER 30

Short-Term Financial Planning 857

2000 2001

Net working capital 30 38

Fixed assets:

Gross investment 56 70

Less depreciation ⫺16 ⫺20

Net fixed assets 40 50

Total net assets 70 88

Long-term debt 5 12

Net worth (equity and retained earnings) 65 76

Long-term liabilities and net worth* 70 88

TABLE 30.5

Condensed year-end balance sheets for 2000

and 2001 for Dynamic Mattress Company

(figures in $ millions).

*When only net working capital appears on a firm’s

balance sheet, this figure (the sum of long-term

liabilities and net worth) is often referred to as total

capitalization.

Sources:

Issued long-term debt 7

Cash from operations:

Net income 12

Depreciation 4

23

Uses:

Invested in fixed assets 14

Dividend 1

15

Increase in net working capital 8

TABLE 30.6

Sources and uses of funds (net working capital)

for Dynamic Mattress Company, 2001 (figures in

$ millions).