Brealey, Myers. Principles of Corporate Finance. 7th edition

Подождите немного. Документ загружается.

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

IX. Financial Planning and

Short−Term Management

30. Short−Term Financial

Planning

© The McGraw−Hill

Companies, 2003

overstate the firm’s current cash tax liability,

5

and after-tax cash flow from oper-

ations is therefore understated.

Second, income statements record sales when made, not when the customer’s

payment is received. Think of what happens when Dynamic sells goods on credit.

The company records a profit at the time of sale, but there is no cash inflow until

the bills are paid. Since there is no cash inflow, there is no change in the company’s

cash balance, although there is an increase in working capital in the form of an in-

crease in accounts receivable. No net addition to cash would be shown in a sources

and uses statement like Table 30.4. The increase in cash from operations would be

offset by an increase in accounts receivable.

Later, when the bills are paid, there is an increase in the cash balance. However,

there is no further profit at this point and no increase in working capital. The in-

crease in the cash balance is exactly matched by a decrease in accounts receivable.

That brings up an interesting characteristic of working capital. Imagine a com-

pany that conducts a very simple business. It buys raw materials for cash,

processes them into finished goods, and then sells these goods on credit. The whole

cycle of operations looks like this:

858 PART IX

Financial Planning and Short-Term Management

5

The difference between taxes reported and paid to the Internal Revenue Service shows up on the bal-

ance sheet as an increased deferred tax liability. The reason that a liability is recognized is that acceler-

ated depreciation and other devices used to reduce current taxable income do not eliminate taxes; they

only delay them. Of course, this reduces the present value of the firm’s tax liability, but still the ultimate

liability has to be recognized. In the sources and uses statements an increase in deferred taxes would be

treated as a source of funds. In the Dynamic Mattress example we ignore deferred taxes.

Cash

Receivables

Finished goods

Raw materials

If you draw up a balance sheet at the beginning of the process, you see cash. If you

delay a little, you find the cash replaced by inventories of raw materials and, still

later, by inventories of finished goods. When the goods are sold, the inventories

give way to accounts receivable, and finally, when the customers pay their bills, the

firm draws out its profit and replenishes the cash balance.

There is only one constant in this process, namely, working capital. The compo-

nents of working capital are constantly changing. That is one reason why (net)

working capital is a useful summary measure of current assets and liabilities.

The strength of the working-capital measure is that it is unaffected by seasonal

or other temporary movements between different current assets or liabilities. But

the strength is also its weakness, for the working-capital figure hides a lot of inter-

esting information. In our example cash was transformed into inventory, then into

receivables, and back into cash again. But these assets have different degrees of risk

and liquidity. You can’t pay bills with inventory or with receivables, you must pay

with cash.

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

IX. Financial Planning and

Short−Term Management

30. Short−Term Financial

Planning

© The McGraw−Hill

Companies, 2003

The past is interesting only for what one can learn from it. The financial manager’s

problem is to forecast future sources and uses of cash. These forecasts serve two

purposes. First, they provide a standard, or budget, against which subsequent per-

formance can be judged. Second, they alert the manager to future cash-flow needs.

Cash, as we all know, has a habit of disappearing fast. Look, for example, at Fi-

nance in the News, which describes how Ford’s large cash surplus rapidly turned

into a shortage. Ford’s financial manager needed to plan for this deficiency.

Preparing the Cash Budget: Inflow

There are at least as many ways to produce a quarterly cash budget as there are to

skin a cat. Many large firms have developed elaborate corporate models; others use

a spreadsheet program to plan their cash needs. The procedures of smaller firms may

be less formal. But there are common issues that all firms must face when they fore-

cast. We will illustrate these issues by continuing the example of Dynamic Mattress.

Most of Dynamic’s cash inflow comes from the sale of mattresses. We therefore

start with a sales forecast by quarter

6

for 2002:

859

FINANCE IN THE NEWS

FORD’S DISAPPEARING CASH MOUNTAIN

At the end of 1998 Ford had $23.8 billion in cash

and marketable securities and only $9.8 billion in

debt. But in the next three years Ford went on a

shopping spree that resulted in the expenditure of

more than $13 billion on acquisitions, such as Volvo

Cars and Land Rover. In the same period Ford

spent a total of $20 billion on new products and

other capital projects. Within three years Ford’s

huge cash mountain had halved.

By most standards Ford remained relatively con-

servatively capitalized, but the outlook for the au-

tomobile industry was worsening rapidly. In the

first nine months of 2001 Ford recorded a loss of

nearly $5 billion, so that its operations became a

cash drain rather than a source of cash. At the same

time the company needed to set aside $3 billion to

cover potential costs associated with alleged vehi-

cle safety problems. As Ford faced a potential cash

shortage, the company sought to conserve cash by

halving its dividend payment and pruning its capi-

tal expenditure program.

Source: Ford Motor’s cash drain is described in “Ford Motor’s Cash

Goes Subcompact,” The Wall Street Journal, November 6, 2001.

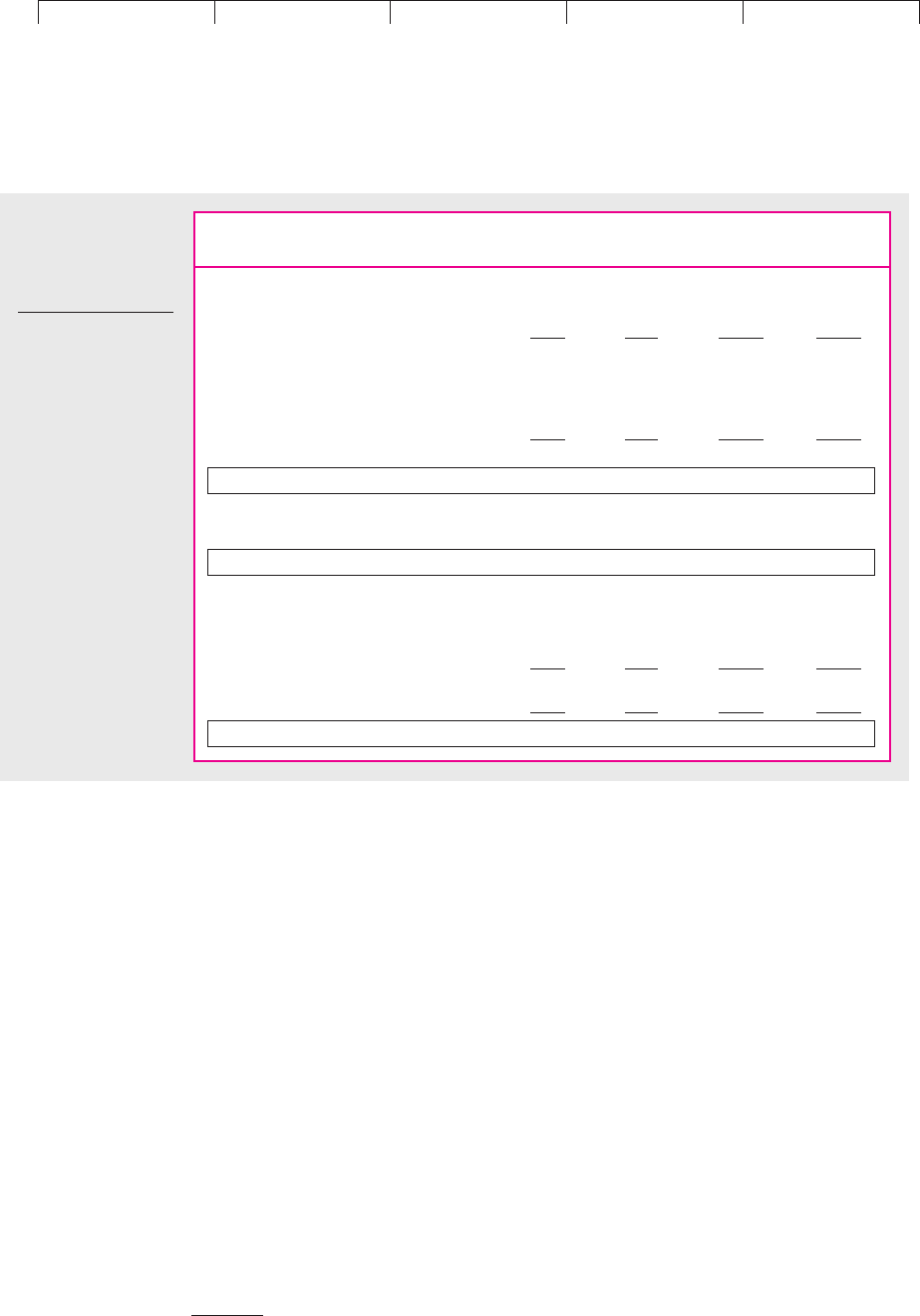

30.4 CASH BUDGETING

6

Most firms would forecast by month instead of by quarter. Sometimes weekly or even daily forecasts

are made. But presenting a monthly forecast would triple the number of entries in Table 30.7 and sub-

sequent tables. We wanted to keep the examples as simple as possible.

First Second Third Fourth

Quarter Quarter Quarter Quarter

Sales ($ millions) 87.5 78.5 116 131

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

IX. Financial Planning and

Short−Term Management

30. Short−Term Financial

Planning

© The McGraw−Hill

Companies, 2003

But sales become accounts receivable before they become cash. Cash flow comes

from collections on accounts receivable.

Most firms keep track of the average time it takes customers to pay their bills.

From this they can forecast what proportion of a quarter’s sales is likely to be con-

verted into cash in that quarter and what proportion is likely to be carried over to the

next quarter as accounts receivable. Suppose that 80 percent of sales are “cashed in”

in the immediate quarter and 20 percent are cashed in in the next. Table 30.7 shows

forecasted collections under this assumption.

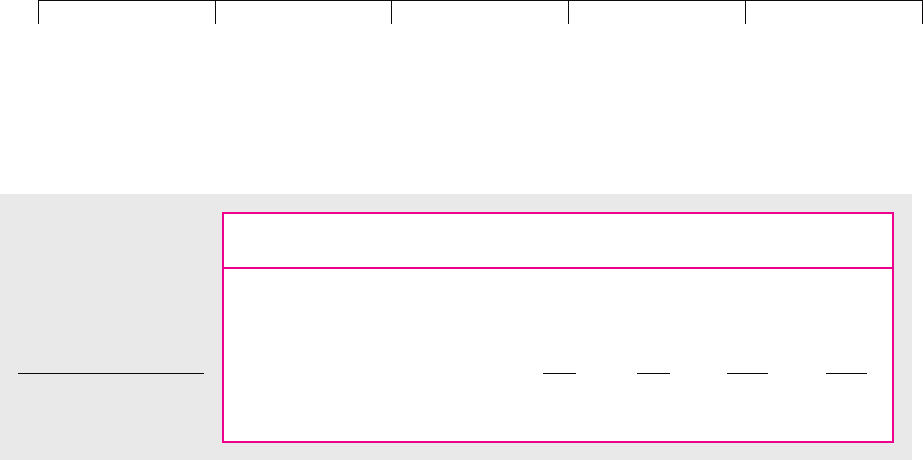

In the first quarter, for example, collections from current sales are 80 percent of

$87.5, or $70 million. But the firm also collects 20 percent of the previous quarter’s

sales, or .2(75) ⫽ $15 million. Therefore total collections are $70 ⫹ $15 ⫽ $85 million.

Dynamic started the first quarter with $30 million of accounts receivable. The

quarter’s sales of $87.5 million were added to accounts receivable, but collections of

$85 million were subtracted. Therefore, as Table 30.7 shows, Dynamic ended the

quarter with accounts receivable of $30 ⫹ 87.5 ⫺ 85 ⫽ $32.5 million. The general

formula is

Ending accounts receivable ⫽ beginning accounts receivable

⫹ sales ⫺ collections

The top section of Table 30.8 shows forecasted sources of cash for Dynamic Mat-

tress. Collection of receivables is the main source, but it is not the only one. Perhaps

the firm plans to dispose of some land or expects a tax refund or payment of an in-

surance claim. All such items are included as “other” sources. It is also possible that

you may raise additional capital by borrowing or selling stock, but we don’t want

to prejudge that question. Therefore, for the moment we just assume that Dynamic

will not raise further long-term finance.

Preparing the Cash Budget: Outflow

So much for the incoming cash. Now for the outgoing cash. There always seem to

be many more uses for cash than there are sources. For simplicity, we have con-

densed the uses into four categories in Table 30.8.

1. Payments on accounts payable. You have to pay your bills for raw materials,

parts, electricity, etc. The cash-flow forecast assumes all these bills are paid

on time, although Dynamic could probably delay payment to some extent.

Delayed payment is sometimes called stretching your payables. Stretching is

one source of short-term financing, but for most firms it is an expensive

860 PART IX

Financial Planning and Short-Term Management

First Second Third Fourth

Quarter Quarter Quarter Quarter

1. Receivables at start of period 30 32.5 30.7 38.2

2. Sales 87.5 78.5 116 131

3. Collections:

Sales in current period (80%) 70 62.8 92.8 104.8

Sales in last period (20%) 15* 17.5 15.7 23.2

Total collections 85 80.3 108.5 128.0

4. Receivables at end of period

4 ⫽ 1 ⫹ 2 ⫺ 3 32.5 30.7 38.2 41.2

TABLE 30.7

To forecast Dynamic

Mattress’s collections on

accounts receivable, you

have to forecast sales

and collection rates

(figures in $ millions).

*Sales in the fourth quarter

of the previous year were

$75 million.

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

IX. Financial Planning and

Short−Term Management

30. Short−Term Financial

Planning

© The McGraw−Hill

Companies, 2003

source, because by stretching they lose discounts given to firms that pay

promptly. This is discussed in more detail in Section 32.1.

2. Labor, administrative, and other expenses. This category includes all other

regular business expenses.

3. Capital expenditures. Note that Dynamic Mattress plans a major capital

outlay in the first quarter.

4. Taxes, interest, and dividend payments. This includes interest on presently

outstanding long-term debt but does not include interest on any additional

borrowing to meet cash requirements in 2002. At this stage in the analysis,

Dynamic does not know how much it will have to borrow, or whether it

will have to borrow at all.

The forecasted net inflow of cash (sources minus uses) is shown in the box in

Table 30.8. Note the large negative figure for the first quarter: a $46.5 million fore-

casted outflow. There is a smaller forecasted outflow in the second quarter, and then

substantial cash inflows in the second half of the year.

The bottom part of Table 30.8 (below the box) calculates how much financing Dy-

namic will have to raise if its cash-flow forecasts are right. It starts the year with $5

million in cash. There is a $46.5 million cash outflow in the first quarter, and so Dy-

namic will have to obtain at least $46.5 ⫺ 5 ⫽ $41.5 million of additional financing.

CHAPTER 30

Short-Term Financial Planning 861

First Second Third Fourth

Quarter Quarter Quarter Quarter

Sources of cash:

Collections on accounts receivable 85 80.3 108.5 128

Other 0 0 12.5 0

Total sources 85 80.3 121 128

Uses of cash:

Payments on accounts payable 65 60 55 50

Labor, administrative, and other expenses 30 30 30 30

Capital expenditures 32.5 1.3 5.5 8

Taxes, interest, and dividends 4 4 4.5 5

Total uses 131.5 95.3 95 93

Sources minus uses ⫺46.5 ⫺15.0 ⫹26 ⫹35

Calculation of short-term financing requirement:

1. Cash at start of period 5 ⫺41.5 ⫺56.5 ⫺30.5

2. Change in cash balance (sources less uses) ⫺46.5 ⫺15.0 ⫹26 ⫹35

3. Cash at end of period*

1 ⫹ 2 ⫽ 3 ⫺41.5 ⫺56.5 ⫺30.5 ⫹4.5

4. Minimum operating cash balance 5 5 5 5

5. Cumulative short-term financing required

†

5 ⫽ 4 ⫺ 3 46.5 61.5 35.5 .5

TABLE 30.8

Dynamic Mattress’s cash budget for 2002 (figures in $ millions).

*Of course, firms cannot literally hold a negative amount of cash. This is the amount the firm will have to raise to pay its bills.

†

A negative sign would indicate a cash surplus. But in this example the firm must raise cash for all quarters.

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

IX. Financial Planning and

Short−Term Management

30. Short−Term Financial

Planning

© The McGraw−Hill

Companies, 2003

This would leave the firm with a forecasted cash balance of exactly zero at the start

of the second quarter.

Most financial managers regard a planned cash balance of zero as driving too close

to the edge of the cliff. They establish a minimum operating cash balance to absorb un-

expected cash inflows and outflows. We will assume that Dynamic’s minimum oper-

ating cash balance is $5 million. That means it will have to raise the full $46.5 million

cash outflow in the first quarter and $15 million more in the second quarter. Thus its

cumulative financing requirement is $61.5 million in the second quarter. This is the

peak, fortunately: The cumulative requirement declines in the third quarter by $26

million to $35.5 million. In the final quarter Dynamic is almost out of the woods: Its

cash balance is $4.5 million, just $.5 million shy of its minimum operating balance.

The next step is to develop a short-term financing plan that covers the forecasted

requirements in the most economical way possible. We will move on to that topic

after two general observations:

1. The large cash outflows in the first two quarters do not necessarily spell

trouble for Dynamic Mattress. In part, they reflect the capital investment

made in the first quarter: Dynamic is spending $32.5 million, but it should

be acquiring an asset worth that much or more. In part, the cash outflows

reflect low sales in the first half of the year; sales recover in the second half.

7

If this is a predictable seasonal pattern, the firm should have no trouble

borrowing to tide it over the slow months.

2. Table 30.8 is only a best guess about future cash flows. It is a good idea to

think about the uncertainty in your estimates. For example, you could

undertake a sensitivity analysis, in which you inspect how Dynamic’s cash

requirements would be affected by a shortfall in sales or by a delay in

collections. The trouble with such sensitivity analyses is that you are

changing only one item at a time, whereas in practice a downturn in the

economy might affect, say, sales levels and collection rates. An alternative

but more complicated solution is to build a model of the cash budget and

then to simulate to determine the probability of cash requirements

significantly above or below the forecasts shown in Table 30.8.

8

If cash

requirements are difficult to predict, you may wish to hold additional cash

or marketable securities to cover a possible unexpected cash outflow.

862 PART IX

Financial Planning and Short-Term Management

7

Maybe people buy more mattresses late in the year when the nights are longer.

8

In other words, you could use Monte Carlo simulation. See Section 10.2.

30.5 THE SHORT-TERM FINANCING PLAN

Dynamic’s cash budget defines its problem: Its financial manager must find short-

term financing to cover the firm’s forecasted cash requirements. There are dozens

of sources of short-term financing, but for simplicity we assume that Dynamic has

just two options.

Options for Short-Term Financing

1. Bank loan: Dynamic has an existing arrangement with its bank allowing it to

borrow up to $38 million at an interest cost of 10 percent a year or 2.5

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

IX. Financial Planning and

Short−Term Management

30. Short−Term Financial

Planning

© The McGraw−Hill

Companies, 2003

percent per quarter. The firm can borrow and repay whenever it wants to as

long as it does not exceed its credit limit.

2. Stretching payables: Dynamic can also raise capital by putting off paying its

bills. The financial manager believes that Dynamic can defer the following

amounts in each quarter:

CHAPTER 30

Short-Term Financial Planning 863

First Second Third Fourth

Quarter Quarter Quarter Quarter

Amount deferrable 52 48 44 40

($ millions)

Thus, $52 million can be saved in the first quarter by not paying bills in that

quarter. (Note that the cash-flow forecasts in Table 30.8 assumed that these

bills will be paid in the first quarter.) If deferred, these payments must be

made in the second quarter. Similarly, up to $48 million of the second

quarter bills can be deferred to the third quarter, and so on.

Stretching payables is often costly, even if no ill will is incurred. The reason is

that suppliers may offer discounts for prompt payment. Dynamic loses this dis-

count if it pays late. In this example we assume the lost discount is 5 percent of the

amount deferred. In other words, if a $100 payment is delayed, the firm must pay

$105 in the next quarter.

Dynamic’s Financing Plan

With these two options, the short-term financing strategy is obvious. Use the bank

loan first, if necessary up to the $38 million limit. If there is still a shortage of cash,

stretch payables.

Table 30.9 shows the resulting plan. In the first quarter the plan calls for bor-

rowing the full amount available from the bank ($38 million) and stretching $3.5

million of payables (see lines 1 and 2 in the table). In addition the company sells

the $5 million of marketable securities it held at the end of 1999 (line 8). Thus it

raises 38 ⫹ 3.5 ⫹ 5 ⫽ $46.5 million of cash in the first quarter (line 10).

In the second quarter, the plan calls for Dynamic to continue to borrow $38 mil-

lion from the bank and to stretch $19.7 million of payables. This raises a further $16.2

million after paying off the $3.5 million of bills deferred from the first quarter.

Why raise $16.2 million when Dynamic needs only an additional $15 million to

finance its operations? The answer is that the company must pay interest on the

borrowings that it undertook in the first quarter and it foregoes interest on the mar-

ketable securities that were sold.

9

In the third and fourth quarters the plan calls for Dynamic to pay off its debt and

to make a small purchase of marketable securities.

Evaluating the Plan

Does the plan shown in Table 30.9 solve Dynamic’s short-term financing problem?

No: The plan is feasible, but Dynamic can probably do better. The most glaring

weakness is its reliance on stretching payables, an extremely expensive financing

9

The bank loan calls for quarterly interest of .025 ⫻ 38 ⫽ $.95 million; the lost discount on the stretched

payables amounts to .05 ⫻ 3.5 ⫽ $.175 million; and the interest lost on the marketable securities is

.02 ⫻ 5 ⫽ $.1 million.

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

IX. Financial Planning and

Short−Term Management

30. Short−Term Financial

Planning

© The McGraw−Hill

Companies, 2003

device. Remember that it costs Dynamic 5 percent per quarter to delay paying

bills—20 percent per year at simple interest. The first plan would merely stimulate

the financial manager to search for cheaper sources of short-term borrowing.

The financial manager would ask several other questions as well. For example:

1. Does the plan yield satisfactory current and quick ratios?

10

Its bankers may

be worried if these ratios deteriorate.

11

2. Are there intangible costs of stretching payables? Will suppliers begin to

doubt Dynamic’s creditworthiness?

3. Does the plan for 2002 leave Dynamic in good financial shape for 2003?

(Here the answer is yes, since Dynamic will have paid off all short-term

borrowing by the end of the year.)

4. Should Dynamic try to arrange long-term financing for the major capital

expenditure in the first quarter? This seems sensible, following the rule of

thumb that long-term assets deserve long-term financing. It would also

reduce the need for short-term borrowing dramatically. A counterargument

is that Dynamic is financing the capital investment only temporarily by short-

term borrowing. By year-end, the investment is paid for by cash from

operations. Thus Dynamic’s initial decision not to seek immediate long-

864 PART IX

Financial Planning and Short-Term Management

First Second Third Fourth

Quarter Quarter Quarter Quarter

New borrowing:

1. Bank loan 38.0 0.0 0.0 0.0

2. Stretching payables 3.5 19.7 0.0 0.0

3. Total 41.5 19.7 0.0 0.0

Repayments:

4. Bank loan 0.0 0.0 4.3 33.7

5. Stretching payables 0.0 3.5 19.7 0.0

6. Total 0.0 3.5 24.0 33.7

7. Net new borrowing 41.5 16.2 ⫺24.0 ⫺33.7

8. Plus securities sold 5.0 0.0 0.0 0.0

9. Less securities bought 0.0 0.0 0.0 0.4

10. Total cash raised 46.5 16.2 ⫺24.0 ⫺34.1

Interest payments*

11. Bank loan 0.0 1.0 1.0 0.8

12. Stretching payables 0.0 0.2 1.0 0.0

13. Interest on securities sold

†

0.0 0.1 0.1 0.1

14. Net interest paid 0.0 1.2 2.0 0.9

15. Cash required for operations

‡

46.5 15.0 ⫺26.0 ⫺35.0

16. Total cash required 46.5 16.2 ⫺24.0 ⫺34.1

TABLE 30.9

Dynamic Mattress’s

financing plan

(figures in $ millions).

Note: Column sums

subject to rounding

error.

*We assume that the

first interest payment

occurs one quarter after

a loan is taken out.

†

Dynamic sold $5 million

of marketable securities

in the first quarter. The

yield is assumed to be 2

percent per quarter.

‡

From Table 30.8.

10

These ratios are discussed in Chapter 29.

11

We have not worked out these ratios explicitly, but you can infer from Table 30.9 that they would be

fine at the end of the year but relatively low in midyear, when Dynamic’s borrowing is high.

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

IX. Financial Planning and

Short−Term Management

30. Short−Term Financial

Planning

© The McGraw−Hill

Companies, 2003

term financing may reflect a preference for ultimately financing the

investment with retained earnings.

5. Perhaps the firm’s operating and investment plans can be adjusted to make

the short-term financing problem easier. Is there any easy way of deferring

the first quarter’s large cash outflow? For example, suppose that the large

capital investment in the first quarter is for new mattress-stuffing machines

to be delivered and installed in the first half of the year. The new machines

are not scheduled to be ready for full-scale use until August. Perhaps the

machine manufacturer could be persuaded to accept 60 percent of the

purchase price on delivery and 40 percent when the machines are installed

and operating satisfactorily.

6. Dynamic may also be able to release cash by reducing the level of other

current assets. For example, it could reduce receivables by getting tough

with customers who are late paying their bills. (The cost is that in the future

these customers may take their business elsewhere.) Or it may be able to get

by with lower inventories of mattresses. (The cost is that it may lose

business if there is a rush of orders that it cannot supply.)

Short-term financing plans are developed by trial and error. You lay out one plan,

think about it, and then try again with different assumptions on financing and in-

vestment alternatives. You continue until you can think of no further improvements.

Trial and error is important because it helps you understand the real nature of the

problem the firm faces. Here we can draw a useful analogy between the process of

planning and Chapter 10, “A Project Is Not a Black Box.” In Chapter 10 we described

sensitivity analysis and other tools used by firms to find out what makes capital in-

vestment projects tick and what can go wrong with them. Dynamic’s financial man-

ager faces the same kind of task: not just to choose a plan but to understand what can

go wrong with it and what will be done if conditions change unexpectedly.

12

A Note on Short-Term Financial Planning Models

Working out a consistent short-term plan requires burdensome calculations.

13

For-

tunately much of the arithmetic can be delegated to a computer. Many large firms

have built short-term financial planning models to do this. Smaller companies like Dy-

namic Mattress do not face so much detail and complexity and find it easier to

work with a spreadsheet program on a personal computer. In either case the fi-

nancial manager specifies forecasted cash requirements or surpluses, interest rates,

credit limits, etc., and the model grinds out a plan like the one shown in Table 30.9.

The computer also produces balance sheets, income statements, and whatever spe-

cial reports the financial manager may require.

Smaller firms that do not want custom-built models can rent general-purpose

models offered by banks, accounting firms, management consultants, or special-

ized computer software firms.

CHAPTER 30

Short-Term Financial Planning 865

12

This point is even more important in long-term financial planning. See Chapter 29.

13

If you doubt that, look again at Table 30.9. Notice that the cash requirements in each quarter depend

on borrowing in the previous quarter, because borrowing creates an obligation to pay interest. Also,

borrowing under a line of credit may require additional cash to meet compensating balance require-

ments; if so, that means still more borrowing and still higher interest charges in the next quarter. More-

over, the problem’s complexity would have been tripled had we not simplified by forecasting per quar-

ter rather than by month.

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

IX. Financial Planning and

Short−Term Management

30. Short−Term Financial

Planning

© The McGraw−Hill

Companies, 2003

Most of these models are simulation programs.

14

They simply work out the con-

sequences of the assumptions and policies specified by the financial manager. Op-

timization models for short-term financial planning are also available. These mod-

els are usually linear programming models. They search for the best plan from a

range of alternative policies identified by the financial manager.

As a matter of fact, we used a linear programming model developed by Pogue

and Bussard

15

to generate Dynamic Mattress’s financial plans. Of course, in that

simple example we hardly needed a linear programming model to identify the best

strategy. It was obvious that Dynamic should always use the line of credit first,

turning to the second-best alternative (stretching payables) only when the limit on

the line of credit was reached. The Pogue–Bussard model nevertheless did the

arithmetic quickly and easily.

Optimization helps when the firm faces complex problems with many interde-

pendent alternatives and restrictions for which trial and error might never identify

the best combination of alternatives.

Of course the best plan for one set of assumptions may prove disastrous if the

assumptions are wrong. Thus the financial manager has to explore the implications

of alternative assumptions about future cash flows, interest rates, and so on. Lin-

ear programming can help identify good strategies, but even with an optimization

model the financial plan is still sought by trial and error.

866 PART IX

Financial Planning and Short-Term Management

30.6 SOURCES OF SHORT-TERM BORROWING

Dynamic solved the greater part of its cash shortage by borrowing from a bank. But

banks are not the only source of short-term loans. Finance companies are also a ma-

jor source of cash, particularly for financing receivables and inventories.

16

In addi-

tion to borrowing from an intermediary like a bank or finance company, firms also

sell short-term commercial paper or medium-term notes directly to investors. It is

time to look more closely at these sources of short-term funds.

Bank Loans

To finance its investment in current assets, a company may rely on a variety of

short-term loans. Obviously, if you approach a bank for a loan, the bank’s lending

officer is likely to ask searching questions about your firm’s financial position and

its plans for the future. Also, the bank will want to monitor the firm’s subsequent

progress. There is, however, a good side to this. Other investors know that banks

14

Like the simulation models described in Section 10.2, except that the short-term planning models

rarely include uncertainty explicitly. The models referred to here are built and used in the same way as

the long-term financial planning models described in Section 29.4.

15

G. A. Pogue and R. N. Bussard, “A Linear Programming Model for Short-Term Financial Planning un-

der Uncertainty,” Sloan Management Review, 13 (Spring 1972), pp. 69–99.

16

Finance companies are firms that specialize in lending to businesses or individuals. They include inde-

pendent firms, such as Household Finance, as well as subsidiaries of nonfinancial corporations, such as

General Motors Acceptance Corporation (GMAC). In their lending finance companies compete with

banks. However, they raise funds not by attracting deposits, as banks do, but by issuing commercial pa-

per and other longer-term securities.

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

IX. Financial Planning and

Short−Term Management

30. Short−Term Financial

Planning

© The McGraw−Hill

Companies, 2003

are hard to convince, and, therefore, when a company announces that it has

arranged a large bank facility, the share price tends to rise.

17

Bank loans come in a variety of flavors.

18

Here are a few of the ways that they

differ.

Commitment Companies sometimes wait until they need the money before they

apply for a bank loan, but nearly three-quarters of commercial bank loans are made

under commitment. In this case the company establishes a line of credit that allows

it to borrow from the bank up to an established limit. This line of credit may be an

evergreen credit with no fixed maturity, but more commonly it is a revolving credit

(revolver) with a fixed maturity of up to three years.

Credit lines are relatively expensive, for in addition to paying interest on any

borrowings the company must pay a commitment fee on the unused amount. In

exchange for this extra cost, the firm receives a valuable option: It has guaranteed

access to the bank’s money at a fixed spread over the general level of interest rates.

This amounts to a put option, because the firm can sell its debt to the bank on fixed

terms even if its own creditworthiness deteriorates or the cost of credit rises. The

growth in the use of credit lines is changing the role of banks. They are no longer

simply lenders; they are also in the business of providing companies with liquid-

ity insurance.

Many companies discovered the value of this insurance in 1998, when Russia

defaulted on its borrowings and created turmoil in the world’s debt markets. Com-

panies in the United States suddenly found it much more expensive to issue their

own debt to investors. Those who had arranged lines of credit with their banks

rushed to take advantage of them. As a result, new debt issues languished, while

bank lending boomed.

19

Maturity Most bank loans are for only a few months. For example, a company

may need a short-term bridge loan to finance the purchase of new equipment or the

acquisition of another firm. In this case the loan serves as interim financing until

the purchase is completed and long-term financing is arranged. Often a short-term

loan may be needed to finance a temporary increase in inventory. Such a loan is de-

scribed as self-liquidating; in other words, the sale of goods provides the cash to re-

pay the loan.

Banks also provide longer-term loans, known as term loans. A term loan typi-

cally has a maturity of four to five years. Usually the loan is repaid in level

amounts over this period, though there is sometimes a large final balloon pay-

ment or just a single bullet payment at maturity. Banks can accommodate the re-

payment pattern to the anticipated cash flows of the borrower. For example, the

first repayment might be delayed a year until the new factory is completed. Term

loans are often renegotiated before maturity. Banks are willing to do this if the

CHAPTER 30

Short-Term Financial Planning 867

17

See C. James, “Some Evidence on the Uniqueness of Bank Loans,” Journal of Financial Economics 19

(1987), pp. 217–235.

18

The results of a survey of the terms of business lending by banks in the United States are published

quarterly in the Federal Reserve Bulletin (see www.federalreserve.gov/releases/E2/).

19

The rush to draw on bank lines of credit is described in M. R. Saidenberg and P. E. Strahan, “Are Banks

Still Important for Financing Large Businesses?” Federal Reserve Bank of New York, Current Issues in Eco-

nomics and Finance 5 (August 1999), pp. 1–6.