Brealey, Myers. Principles of Corporate Finance. 7th edition

Подождите немного. Документ загружается.

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

VI. Options 23. Warrants and

Convertibles

© The McGraw−Hill

Companies, 2003

bonds, it may pay to convert before the final exercise date in order to pick up the

extra cash income.

Forcing Conversion

Companies usually retain an option to buy back or “call” the convertible bond at a

preset price. If the company calls the bond, the owner has a brief period, usually

about 30 days, within which to convert the bond or surrender it.

15

If a bond is sur-

rendered, the investor receives the call price in cash. But if the share price is higher

than the call price, the investor will convert the bond instead of surrendering it.

Thus a call can force conversion if the stock price is high enough.

Most convertible bonds provide for two or more years of call protection. During

this period the company is not permitted to call the bonds. However, many con-

vertibles can be called early, before the end of the call protection, if the stock price

has risen enough to provide a nice conversion profit. For example, a convertible

with a call price of $40 might be callable early if the stock price trades above $65

for at least two weeks.

Calling the bond obviously does not affect the total size of the company pie, but

it can affect the size of the individual slices. In other words, conversion has no ef-

fect on the total value of the firm’s assets, but it does affect how asset value is dis-

tributed among the different classes of security holders. Therefore, if you want to

maximize your shareholders’ slice of the pie, you must minimize the convertible

bondholders’ slice. That means you must not call the bonds if they are worth less

than the call price, for that would be giving the bondholders an unnecessary pres-

ent. Similarly, you must not allow the bonds to remain uncalled if their value is

above the call price, for that would not be minimizing the value of the bonds.

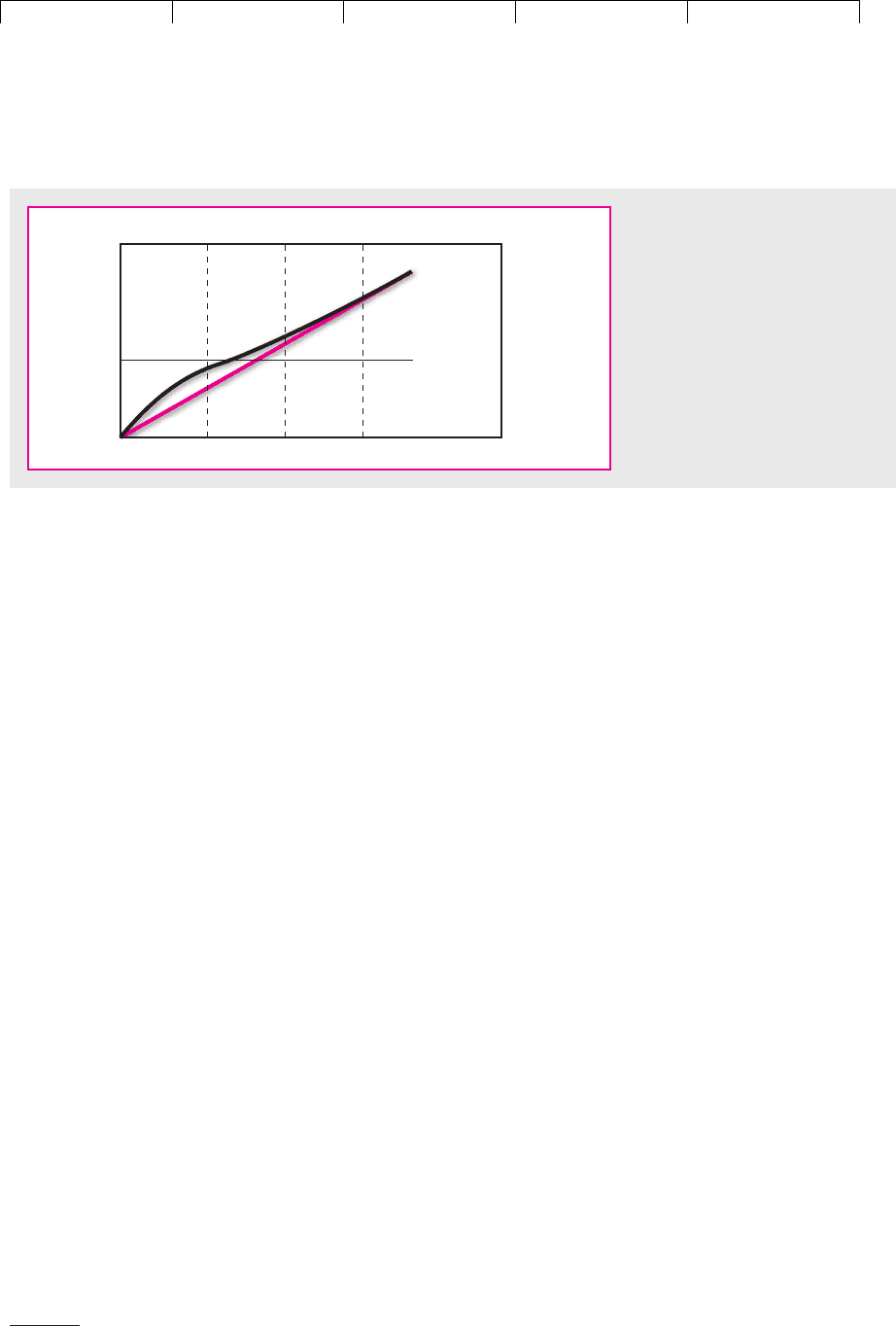

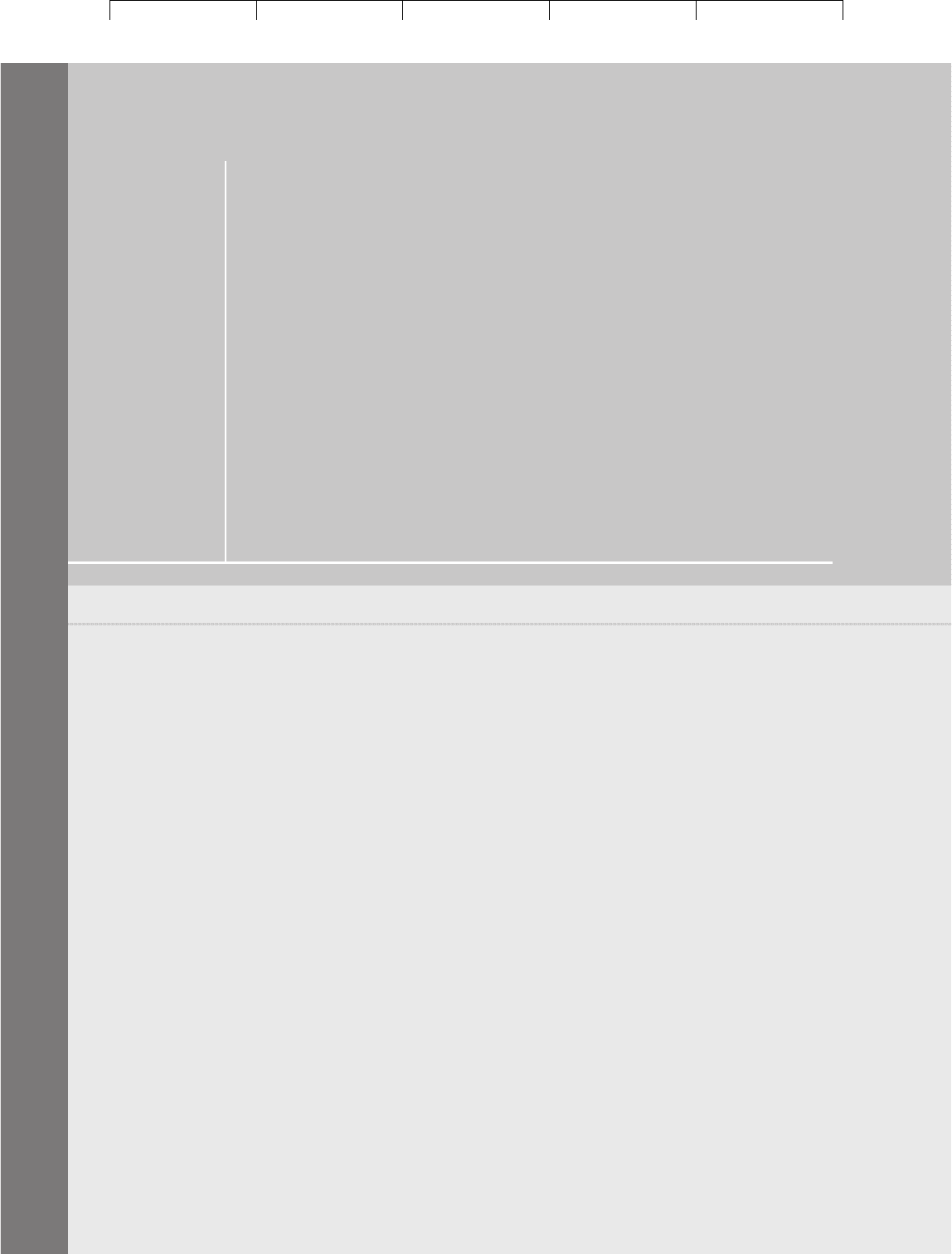

Let’s apply this reasoning to specific cases. Refer to Figure 23.4, which matches

Figure 23.3(c) but has the call price drawn in as a horizontal line. Consider the firm

values corresponding to three stock prices, marked A, B, and C:

• At price A, the convertible is “out of the money.” Calling the bond leads to

redemption for cash and hands bondholders a free gift equal to the difference

between the call price and the convertible value. Therefore the company

should not call.

CHAPTER 23

Warrants and Convertibles 653

15

Companies may also reserve the right to force conversion of warrants.

A B C

Value of convertible

Call price

Stock price

FIGURE 23.4

The decision to call a convertible.

The financial manager should call

at price C but wait at prices A and

B. (Note: The conversion value is

the straight upward-sloping line.)

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

VI. Options 23. Warrants and

Convertibles

© The McGraw−Hill

Companies, 2003

• Suppose call protection ends with price at level C. Then the financial manager

should call immediately, forcing the convertible value down to the call price.

16

• What if call protection ends with price at level B, barely above the call price?

In this case the financial manager will probably wait. Remember, if a call is

announced, bondholders have a 30-day period in which to decide whether to

convert or redeem. The stock price could easily fall below the call price during

this period, forcing the company to redeem for cash. Usually calls are not

announced until the stock price is about 20 percent above the call price. This

provides a safety margin to ensure conversion.

17

Do companies follow these simple guidelines? On the surface they don’t, for

there are many instances of convertible bonds selling well above the call price. But

the explanation seems to lie in the call-protection period, during which companies

are not allowed to call their bonds. Paul Asquith found that most convertible bonds

that are worth calling are called as soon as possible after this period ends.

18

The

typical delay for bonds that can be called is slightly less than four months after the

conversion value first exceeds the call price.

654 PART VI

Options

16

The financial manager might delay calling for a time at price C if interest payments on the convert-

ible debt are less than the extra dividends that would be paid after conversion. This delay would reduce

cash payments to bondholders. Nothing is lost if the financial manager always calls “on the way down”

if stock price subsequently falls toward level B. Note that investors may convert voluntarily if dividends

after conversion exceed interest on the convertible bond.

17

See P. Asquith and D. Mullins, “Convertible Debt: Corporate Call Policy,” Journal of Finance 46 (Sep-

tember 1991), pp. 1273–1290.

18

See P. Asquith, “Convertible Bonds Are Not Called Late,” Journal of Finance 50 (September 1995),

pp. 1275–1289.

23.3 THE DIFFERENCE BETWEEN WARRANTS

AND CONVERTIBLES

We have dwelt on the basic similarity between warrants and convertibles. Now let

us look at some of the differences:

1. Warrants are usually issued privately. Packages of bonds with warrants or

preferred stock with warrants tend to be more common in private

placements. By contrast most convertible bonds are issued publicly.

2. Warrants can be detached. When you buy a convertible, the bond and the

option are bundled up together. You cannot sell them separately. This may

be inconvenient. If your tax position or attitude to risk inclines you to

bonds, you may not want to hold options as well. Sometimes warrants are

also “nondetachable,” but usually you can keep the bond and sell the

warrant.

3. Warrants may be issued on their own. Warrants do not have to be issued in

conjunction with other securities. Often they are used to compensate

investment bankers for underwriting services. Many companies also give

their executives long-term options to buy stock. These executive stock

options are not usually called warrants, but that is exactly what they are.

Companies can also sell warrants on their own directly to investors, though

they rarely do so.

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

VI. Options 23. Warrants and

Convertibles

© The McGraw−Hill

Companies, 2003

4. Warrants are exercised for cash. When you convert a bond, you simply

exchange your bond for common stock. When you exercise warrants, you

generally put up extra cash, though occasionally you have to surrender the

bond or can choose to do so. This means that bond–warrant packages and

convertible bonds usually have different effects on the company’s cash flow

and on its capital structure.

5. A package of bonds and warrants may be taxed differently. There are some tax

differences between warrants and convertibles. Suppose that you are

wondering whether to issue a convertible bond at 100. You can think of this

convertible as a package of a straight bond worth, say, 90 and an option

worth 10. If you issue the bond and option separately, the IRS will note that

the bond is issued at a discount and that its price will rise by 10 points over

its life. The IRS will allow you, the issuer, to spread this prospective price

appreciation over the life of the bond and deduct it from your taxable profits.

The IRS will also allocate the prospective price appreciation to the taxable

income of the bondholder. Thus, by issuing a package of bonds and warrants

rather than a convertible, you may reduce the tax paid by the issuing

company and increase the tax paid by the investor.

19

CHAPTER 23 Warrants and Convertibles 655

19

See J. D. Finnerty, “The Case for Issuing Synthetic Convertible Bonds,” Midland Corporate Finance Jour-

nal 4 (Fall 1986), pp. 73–82.

20

Here is another “Heads I win, tails you lose” argument. You are an investor. Your broker calls you with

an offer of ABC company warrants. ABC’s share price is $10; the warrants expire in one year, have an ex-

ercise price of $10, and are selling at $1. Your broker points out that you are likely to make much larger

percentage gains from buying the warrants rather than the shares. For example, if over the next year the

share price rises by 20 percent to $12, the warrants will be worth $2, a gain of 100 percent. On the other

hand, if the share price falls, the most that you can lose as a warrant holder is $1. How do you respond?

23.4 WHY DO COMPANIES ISSUE WARRANTS

AND CONVERTIBLES?

You are approached by an investment banker who is anxious to persuade you that

your company should issue warrants. She points out that the exercise price of the

warrants could be set at 20 percent above the current stock price, so that you would

effectively be selling stock at a hefty premium. And, if it turns out that the warrants

are never exercised, the proceeds from their sale would become a clear profit to the

company. Are you convinced?

You hear many similar arguments for issuing warrants and convertibles, but you

should always be suspicious of any “Heads I win, tails you lose” argument. If the

shareholder inevitably wins, the warrant holder must lose. But that doesn’t make

sense. Surely there must be some price at which it makes sense to buy warrants.

20

Suppose that your company’s stock is priced at $100 and that you are consider-

ing an issue of warrants exercisable at $120. You believe that you can sell these war-

rants at $10. If the stock price subsequently fails to reach $120, the warrants will not

be exercised. You will have sold warrants for $10 each, which with the benefit of

hindsight proved to be worthless to the buyer. If the stock price reaches $130, say,

the warrants will be exercised. Your firm will have received the initial payment of

$10 plus the exercise price of $120. On the other hand, it will have issued to the war-

rant holders stock worth $130 per share. The net result is a standoff. You have re-

ceived a payment of $130 in exchange for a liability worth $130.

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

VI. Options 23. Warrants and

Convertibles

© The McGraw−Hill

Companies, 2003

Think now what happens if the stock price rises above $130. Perhaps it goes to

$200. In this case the warrant issue will end up producing a loss of $70. This is not

a cash outflow but an opportunity loss. The firm receives $130, but in this case it

could have sold stock for $200. On the other hand, the warrant holders gain $70:

They invest $130 in cash to acquire stock that they can sell, if they like, for $200.

Our example is oversimplified—for instance, we have kept quiet about the time

value of money and risk—but we hope it has made the basic point. When you sell

warrants, you are selling options and getting cash in exchange. Options are valu-

able securities. If they are properly priced, this is a fair trade; in other words, it is a

zero-NPV transaction.

Some managers look on convertibles as “cheap debt.” Others regard them as a

deferred sale of stock at an attractive price. These arguments also are misleading.

We have seen that a convertible is like a package of a straight bond and an option.

The difference between the market value of the convertible and that of the straight

bond is therefore the price investors place on the call option. The convertible is

“cheap” only if this price overvalues the option.

What then of the other managers—those who regard the issue as a deferred

sale of common stock? A convertible bond gives you the right to buy stock by

giving up a bond.

21

Bondholders may decide to do this, but then again they

may not. Thus issue of a convertible bond may amount to a deferred stock is-

sue. But if the firm needs equity capital, a convertible issue is an unreliable way

of getting it.

Taken at their face value the motives of these managers are irrational. Con-

vertibles are not just cheap debt, nor are they a deferred sale of stock. But we

suspect that these simple phrases encapsulate some more complex and rational

motives.

Notice that convertibles tend to be issued by the smaller and more speculative

firms. They are almost invariably unsecured and generally subordinated. Now

put yourself in the position of a potential investor. You are approached by a small

firm with an untried product line that wants to issue some junior unsecured debt.

You know that if things go well, you will get your money back, but if they do not,

you could easily be left with nothing. Since the firm is in a new line of business,

it is difficult to assess the chances of trouble. Therefore you don’t know what the

fair rate of interest is. Also, you may be worried that once you have made the

loan, management will be tempted to run extra risks. It may take on additional

senior debt, or it may decide to expand its operations and go for broke on your

money. In fact, if you charge a very high rate of interest, you could be encourag-

ing this to happen.

What can management do to protect you against a wrong estimate of the risk

and to assure you that its intentions are honorable? In crude terms, it can give you

a piece of the action. You don’t mind the company running unanticipated risks as

long as you share in the gains as well as the losses.

22

656 PART VI Options

21

That is much the same as already having the stock together with the right to sell it for the convertible’s

bond value. In other words, instead of thinking of a convertible as a bond plus a call option, you could

think of it as the stock plus a put option. Now you see why it is wrong to think of a convertible as equiv-

alent to the sale of stock; it is equivalent to the sale of both stock and a put option. If there is any possi-

bility that investors will want to hold onto their bond, the put option will have some value.

22

See M. J. Brennan and E. S. Schwartz, “The Case for Convertibles,” Journal of Applied Corporate Finance

1 (Summer 1988), pp. 55–64.

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

VI. Options 23. Warrants and

Convertibles

© The McGraw−Hill

Companies, 2003

CHAPTER 23 Warrants and Convertibles 657

Convertible securities and warrants make sense whenever it is unusually costly

to assess the risk of debt or whenever investors are worried that management may

not act in the bondholders’ interest.

23

You can also think of a convertible issue as a contingent issue of equity. If a com-

pany’s investment opportunities expand, its stock price is likely to increase, al-

lowing the financial manager to call and force conversion of a convertible bond

into equity. Thus the company gets fresh equity when it is most needed for expan-

sion. Of course, it is also stuck with debt if the company does not prosper.

24

The relatively low coupon rate on convertible bonds may also be a convenience

for rapidly growing firms facing heavy capital expenditures. They may be willing

to give up the conversion option to reduce immediate cash requirements for debt

service. Without the conversion option, lenders might demand extremely high

(promised) interest rates to compensate for the probability of default. This would

not only force the firm to raise still more capital for debt service but also increase

the risk of financial distress. Paradoxically, lenders’ attempts to protect themselves

against default may actually increase the probability of financial distress by in-

creasing the burden of debt service on the firm.

25

23

Changes in risk ought to be more likely when the firm is small and its debt is low-grade. If so, we

should find that the convertible bonds of such firms offer their owners a larger potential ownership

share. This is indeed the case. See C. M. Lewis, R. J. Rogalski, and J. K. Seward, “Understanding the De-

sign of Convertible Debt,” Journal of Applied Corporate Finance 11 (Spring 1998), pp. 45–53.

24

Jeremy Stein points out that an issue of a convertible sends a better signal to investors than a straight

equity issue. As we explained in Chapter 15, announcement of a common stock issue prompts worries

of overvaluation and usually depresses stock price. Convertibles are hybrids of debt and equity and

send a less negative signal. If the company is likely to need equity, its willingness to issue a convertible,

and to take the chance that stock price will rise enough to allow forced conversion, also signals man-

agement’s confidence. See J. Stein, “Convertible Bonds as Backdoor Equity Financing,” Journal of Fi-

nancial Economics 32 (1992), pp. 3–21.

25

This fact led to an extensive body of literature on “credit rationing.” A lender rations credit if it is ir-

rational to lend more to a firm regardless of the interest rate the firm is willing to promise to pay. Whether

this can happen in efficient, competitive capital markets is controversial. We discussed credit rationing

in Chapter 18. For a review of this literature, see E. Baltensperger, “Credit Rationing: Issues and Ques-

tions,” Journal of Money, Credit and Banking 10 (May 1978), pp. 170–183.

SUMMARY

Visit us at www.mhhe.com/bm7e

Instead of issuing straight bonds, companies may sell either packages of bonds and

warrants or convertible bonds.

A warrant is just a long-term call option issued by the company. You already

know a good deal about valuing call options. You know from Chapter 20 that call

options must be worth at least as much as the stock price less the exercise price.

You know that their value is greatest when they have a long time to expiration,

when the underlying stock is risky, and when the interest rate is high.

Warrants are somewhat trickier to value than call options traded on the options

exchanges. First, because they are long-term options, it is important to recognize

that the warrant holder does not receive any dividends. Second, dilution must be

allowed for.

A convertible bond gives its holder the right to swap the bond for common

stock. The rate of exchange is usually measured by the conversion ratio—that is, the

number of shares that the investor gets for each bond. Sometimes the rate of

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

VI. Options 23. Warrants and

Convertibles

© The McGraw−Hill

Companies, 2003

658 PART VI Options

exchange is expressed in terms of the conversion price—that is, the face value of the

bond that must be given up in order to receive one share.

Convertibles are like a package of a bond and a call option. When you evaluate the

conversion option, you must again remember that the convertible holder does not re-

ceive dividends and that conversion results in dilution of the common stock. There

are two other things to watch out for. One is the problem of default risk. If the com-

pany runs into trouble, you may have not only a worthless conversion option but also

a worthless bond. Second, the company may be able to force conversion by calling the

bond. It should do this when the market price of the convertible reaches the call price.

You hear a variety of arguments for issuing warrants or convertibles. Convert-

ible bonds and bonds with warrants are almost always junior bonds and are fre-

quently issued by risky companies. We think that this says something about the

reasons for their issue. Suppose that you are lending to an untried company. You

are worried that the company may turn out to be riskier than you thought or that

it may issue additional senior bonds. You can try to protect yourself against such

eventualities by imposing very restrictive conditions on the debt, but it is often

simpler to allow some extra risk as long as you get a piece of the action. The con-

vertible and bond–warrant package give you a chance to participate in the firm’s

successes as well as its failures. They diminish the possible conflicts of interest be-

tween bondholder and stockholder.

FURTHER

READING

The items listed in Chapters 20 and 21 under “Further Reading” are also relevant to this chapter, in

particular Black and Scholes’s discussion of warrant valuation.

Ingersoll’s work represents the “state of the art” in valuing convertibles:

J. E. Ingersoll: “A Contingent Claims Valuation of Convertible Securities,” Journal of Finan-

cial Economics, 4:289–322 (May 1977).

Ingersoll also examines corporate call policies on convertible bonds in:

J. E. Ingersoll: “An Examination of Corporate Call Policies on Convertible Securities,” Jour-

nal of Finance, 32:463–478 (May 1977).

Brennan and Schwartz’s paper was written about the same time as Ingersoll’s and reaches essentially

the same conclusions; they also present a general procedure for valuing convertibles:

M. J. Brennan and E. S. Schwartz: “Convertible Bonds: Valuation and Optimal Strategies for

Call and Conversion,” Journal of Finance, 32:1699–1715 (December 1977).

Two useful articles on warrants are:

E. S. Schwartz: “The Valuation of Warrants: Implementing a New Approach,” Journal of Fi-

nancial Economics, 4:79–93 (January 1977).

D. Galai and M. A. Schneller: “Pricing of Warrants and the Value of the Firm,” Journal of Fi-

nance, 33:1333–1342 (December 1978).

Asquith’s analysis of the effect of call protection provides evidence that firms’decisions on calling con-

vertibles are more rational than was previously believed:

P. Asquith: “Convertible Bonds Are Not Called Late,” Journal of Finance, 50:1275–1289 (Sep-

tember 1995).

For nontechnical discussions of the pricing of convertibles and the reasons for their use, see:

M. J. Brennan and E. S. Schwartz: “The Case for Convertibles,” Journal of Applied Corporate

Finance, 1:55–64 (Summer 1988).

C. M. Lewis, R. J. Rogalski, and J. K. Seward, “Understanding the Design of Convertible

Debt,” Journal of Applied Corporate Finance, 11:45–53 (Spring 1998).

Visit us at www.mhhe.com/bm7e

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

VI. Options 23. Warrants and

Convertibles

© The McGraw−Hill

Companies, 2003

CHAPTER 23 Warrants and Convertibles 659

QUIZ

1. Associated Elk warrants entitle the owner to buy one share at $40.

a. What is the “theoretical” value of the warrant if the stock price is: (i) $20? (ii) $30?

(iii) $40? (iv) $50? (v) $60?

b. Plot the theoretical value of the warrant against the stock price.

c. Suppose the stock price is $60 and the warrant price is $5. What would you do?

2. In 1994 Viacom made a typical issue of warrants. Each warrant could be exercised be-

fore 1999 at a price of $70 per share. In September 1998 the stock price was $57 per share.

a. Did the warrant holder have a vote?

b. Did the warrant holder receive dividends?

c. If the stock was split 3 for 1, how would the exercise price be adjusted?

d. Suppose that instead of adjusting the exercise price after a 3-for-1 split, the

company gives each warrant holder the right to buy three shares at $70 apiece.

Would this have the same effect? Would it make the warrant holder better or

worse off?

e. What is the “theoretical” value of the warrant?

f. Before maturity is the warrant worth more or less than the “theoretical” value?

g. Other things equal, would the warrant be more or less valuable if:

i. The company increased its rate of dividend payout?

ii. The interest rate declined?

iii. The stock became riskier?

iv. The company extended the exercise period?

v. The company reduced the exercise price?

h. A few companies issue perpetual warrants that have no final exercise date.

Suppose that Viacom warrants were perpetual. In what circumstances might it

make sense for investors to exercise their warrants?

i. If the stock price rises 5 percent, would you expect the price of a warrant to rise by

more or less than 5 percent?

3. Company X has outstanding 1,000 shares and 200 warrants. Each warrant can be

converted into one share at an exercise price of $20. What will be the total market

value of X’s shares after the warrants mature if the share price on that date is (a) $15,

(b) $25?

4. Maple Aircraft has issued a 4

3

⁄

4 percent convertible subordinated debenture due 2008.

The conversion price is $47.00 and the debenture is callable at $102.75 percent of face

value. The market price of the convertible is 91 percent of face value, and the price of

the common is $41.50. Assume that the value of the bond in the absence of a conversion

feature is about 65 percent of face value.

a. What is the conversion ratio of the debenture?

b. If the conversion ratio were 50, what would be the conversion price?

c. What is the conversion value?

d. At what stock price is the conversion value equal to the bond value?

e. Can the market price be less than the conversion value?

f. How much is the convertible holder paying for the option to buy one share of

common stock?

g. By how much does the common have to rise by 2008 to justify conversion?

h. When should Maple call the debenture?

5. a. Pi, Inc., has 30 million shares outstanding and has a net income of $210 million. Cal-

culate Pi’s earnings per share.

b. Pi has also issued $50 million of 5 percent convertible bonds with a face value of

$1,000 each and a conversion ratio of 3.142. How will earnings per share change if

the bonds are converted?

6. True or false?

a. Convertible bonds are usually senior claims on the firm.

b. The higher the conversion ratio, the more valuable the convertible.

Visit us at www.mhhe.com/bm7e

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

VI. Options 23. Warrants and

Convertibles

© The McGraw−Hill

Companies, 2003

660 PART VI Options

c. The higher the conversion price, the more valuable the convertible.

d. If a company splits its stock, the conversion price is increased.

e. Other things equal, if dividend payments rise, bondholders are more likely to

convert before maturity.

f. Convertible bonds do not share fully in a rise in the price of the common stock, but

they provide some protection against a decline.

PRACTICE

QUESTIONS

1. Associated Elk warrants have an exercise price of $40. The share price is $50. The divi-

dend on the stock is $3, and the interest rate is 10 percent.

a. Would you exercise your warrants now or later? State why.

b. If the dividend increased to $5, it could pay to exercise now if the stock price has

low variability and it could be better to exercise later if the stock price has high

variability. Explain why.

2. Moose Stores has outstanding one million shares of common stock with a total market

value of $40 million. It now announces an issue of one million warrants at $5 each. Each

warrant entitles the owner to buy one Moose share for a price of $30 any time within the

next five years. Moose Stores has stated that it will not pay a dividend within this period.

The standard deviation of the returns on Moose’s equity is 20 percent a year, and

the interest rate is 8 percent.

a. What is the market value of each warrant?

b. What is the market value of each share after the warrant issue? (Hint: The value of

the shares is equal to the total value of the equity less the value of the warrants.)

3. Look again at question 2. Suppose that Moose now forecasts the following dividend

payments:

Visit us at www.mhhe.com/bm7e

End of Year Dividend

1$2

23

34

45

56

Reestimate the market values of the warrant and stock.

4. Occasionally firms extend the life of warrants that would otherwise expire unexercised.

What is the cost of doing this?

5. The Surplus Value Company had $10 million (face value) of convertible bonds out-

standing in 2001. Each bond has the following features:

Par or face value $1000

Conversion price $25

Current call price 105 (percent of face value)

Current trading price 130 (percent of face value)

Maturity 2011

Current stock price $30 (per share)

Interest rate 10 (coupon as percent of face value)

a. What is the bond’s conversion value?

b. Can you explain why the bond is selling above conversion value?

c. Should Surplus call? What will happen if it does so?

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

VI. Options 23. Warrants and

Convertibles

© The McGraw−Hill

Companies, 2003

CHAPTER 23 Warrants and Convertibles 661

6. Piglet Pies has issued a zero-coupon 10-year bond that can be converted into 10 Piglet

shares. Comparable straight bonds are yielding 8 percent. Piglet stock is priced at $50 a

share.

a. Suppose that you had to make a now-or-never decision on whether to convert or to

stay with the bond. Which would you do?

b. If the convertible bond is priced at $550, how much are investors paying for the

option to buy Piglet shares?

c. If after one year the value of the conversion option is unchanged, what is the value

of the convertible bond?

7. Iota Microsystems’ 10 percent convertible is about to mature. The conversion ratio is 27.

a. What is the conversion price?

b. The stock price is $47. What is the conversion value?

c. Should you convert?

8. In each case, state which of the two securities is likely to provide the higher return:

a. When the stock price rises (stock or convertible bond?).

b. When interest rates fall (straight bond or convertible bond?).

c. When the specific risk of the stock decreases (straight bond or convertible bond?).

d. When the dividend on the stock increases (stock or convertible bond?).

9. In 1996 Marriott International made an issue of LYONS. The bond matured in 2011, had

a zero coupon, and was issued at $532.15. It could be converted into 8.76 shares. Begin-

ning in 1999 the bonds could be called by Marriott. The call price was $603.71 in 1999

and increased by 4.3 percent a year thereafter. Holders had an option to put the bond

back to Marriott in 1999 at $603.71 and in 2006 at $810.36. At the time of issue the price

of the common stock was about $50.50.

a. What was the yield to maturity on the bond?

b. Assuming that comparable nonconvertible bonds yielded 10 percent, how much

were investors paying for the conversion option?

c. What was the conversion value of the bonds at the time of issue?

d. What was the initial conversion price of the bonds?

e. What is the conversion price in 2005? Why does it change?

f. If the price of the bond in 2006 is less than $810.36, would you put the bond back to

Marriott?

g. At what price can Marriott call the bonds in 2006? If the price of the bond in 2006 is

more than this, should Marriott call them?

10. “The company’s decision to issue warrants should depend on the management’s fore-

cast of likely returns on the stock.” Do you agree?

11. If the riskiness of the firm’s assets increases, does the value of its convertible rise or fall,

or can’t you say?

12. Financing with convertible debt is especially appropriate for small, rapidly growing, or

risky companies. Explain why.

13. The Pork Barrel Company has issued three-year warrants to buy 12 percent perpetual

debentures at a price of 120 percent. The current interest rate is 12 percent and the stan-

dard deviation of returns on the bond is 20 percent. Use the Black–Scholes model to ob-

tain a rough estimate of the value of Pork Barrel warrants.

CHALLENGE

QUESTIONS

1. The B.J. Services warrant is described in Section 23.1. How would you use the

Black–Scholes formula to compute the value of the warrant immediately after its

issue, assuming a stock price of $19 and a warrant price of $5? Begin by ignoring

the problem of dilution. Then go on to describe how dilution would affect your

calculations.

Visit us at www.mhhe.com/bm7e

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

VI. Options 23. Warrants and

Convertibles

© The McGraw−Hill

Companies, 2003

662 PART VI Options

2. Here is a question about dilution. The Electric Bassoon Company has outstanding

2,000 shares with a total market value of $20,000 plus 1,000 warrants with a total mar-

ket value of $5,000. Each warrant gives its holder the option to buy one share at $20.

a. To value the warrants, you first need to value a call option on an alternative share.

How might you calculate its standard deviation?

b. Suppose that the value of a call option on this alternative share was $6. Calculate

whether the Electric Bassoon warrants were undervalued or overvalued.

3. This question illustrates that when there is scope for the firm to vary its risk, lenders

may be more prepared to lend if they are offered a piece of the action through the issue

of a convertible bond.

Ms. Blavatsky is proposing to form a new start-up firm with initial assets of

$10 million. She can invest this money in one of two projects. Each has the same ex-

pected payoff, but one has more risk than the other. The relatively safe project offers a

40 percent chance of a $12.5 million payoff and a 60 percent chance of an $8 million pay-

off. The risky project offers a 40 percent chance of a $20 million payoff and a 60 percent

chance of a $5 million payoff.

Ms. Blavatsky initially proposes to finance the firm by an issue of straight debt with

a promised payoff of $7 million. Ms. Blavatsky will receive any remaining payoff. Show

the possible payoffs to the lender and to Ms. Blavatsky if (a) she chooses the safe proj-

ect and (b) she chooses the risky project. Which project is Ms. Blavatsky likely to

choose? Which will the lender want her to choose?

Suppose now that Ms. Blavatsky offers to make the debt convertible into 50 per-

cent of the value of the firm. Show that in this case the lender receives the same expected

payoff from the two projects.

4. Occasionally it is said that issuing convertible bonds is better than issuing stock when

the firm’s shares are undervalued. Suppose that the financial manager of the Butternut

Furniture Company does have inside information indicating that the Butternut stock

price is too low. Butternut’s future earnings will in fact be higher than investors expect.

Suppose further that the inside information cannot be released without giving away a

valuable competitive secret. Clearly, selling shares at the present low price would harm

Butternut’s existing shareholders. Will they also lose if convertible bonds are issued? If

they do lose in this case, is the loss more or less than it would be if common stock were

issued?

Now suppose that investors forecast earnings accurately, but still undervalue the

stock because they overestimate Butternut’s actual business risk. Does this change your

answers to the questions posed in the preceding paragraph? Explain.

MINI-CASE

Visit us at www.mhhe.com/bm7e

The Shocking Demise of Mr. Thorndike

It was one of Morse’s most puzzling cases. That morning Rupert Thorndike, the autocratic

CEO of Thorndike Oil, was found dead in a pool of blood on his bedroom floor. He had been

shot through the head, but the door and windows were bolted on the inside and there was

no sign of the murder weapon.

Morse looked in vain for clues in Thorndike’s office. He had to take another tack. He de-

cided to investigate the financial circumstances surrounding Thorndike’s demise.

The company’s capital structure was as follows:

• Debt: $200 million face value. The bonds had a coupon of 5 percent, matured in 10 years,

and offered a yield of 12 percent (the risk-free interest rate was 6 percent).