Brealey, Myers. Principles of Corporate Finance. 7th edition

Подождите немного. Документ загружается.

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

VI. Options 23. Warrants and

Convertibles

© The McGraw−Hill

Companies, 2003

MANY DEBT ISSUES are either packages of bonds and warrants or convertibles. The warrant gives its

owner the right to buy other company securities. A convertible bond gives its owner the right to ex-

change the bond for other securities.

There is also convertible preferred stock—it is often used to finance mergers, for example. Con-

vertible preferred gives its owner the right to exchange the preferred share for other securities.

What are these strange hybrids, and how should you value them? Why are they issued? We will an-

swer each of these questions in turn.

643

23.1 WHAT IS A WARRANT?

A significant proportion of private placement bonds and a smaller proportion of

public issues are sold with warrants. In addition, warrants are sometimes sold with

issues of common or preferred stock; they are also often given to investment

bankers as compensation for underwriting services or used to compensate credi-

tors in the case of bankruptcy.

1

In April 1995 B.J. Services, a firm servicing the oil industry, issued 4.8 million

warrants as partial payment for an acquisition. Each of these warrants allowed the

holder to buy one share of B.J. Services for $30 at any time before April 2000. When

the warrants were issued, the shares were priced at $19, so that the price needed to

rise by more than 50 percent to make it worthwhile to exercise the warrants.

Warrant holders are not entitled to vote or to receive dividends. But the exer-

cise price of a warrant is automatically adjusted for any stock dividends or stock

splits. So, when in 1998 B.J. Services split its stock 2 for 1, each warrant holder

was given the right to buy two shares and the exercise price was reduced to

30 ⫼ 2 ⫽ $15.00 per share. By the time that the warrants finally expired in April

2000, the share price had reached $70 and so a warrant to buy two shares was

worth 2 ⫻ ($70 ⫺ $15) ⫽ $110.

Valuing Warrants

As a trained option spotter (having read Chapter 20), you have probably already

classified the B.J. Services warrant as a five-year American call option exercisable

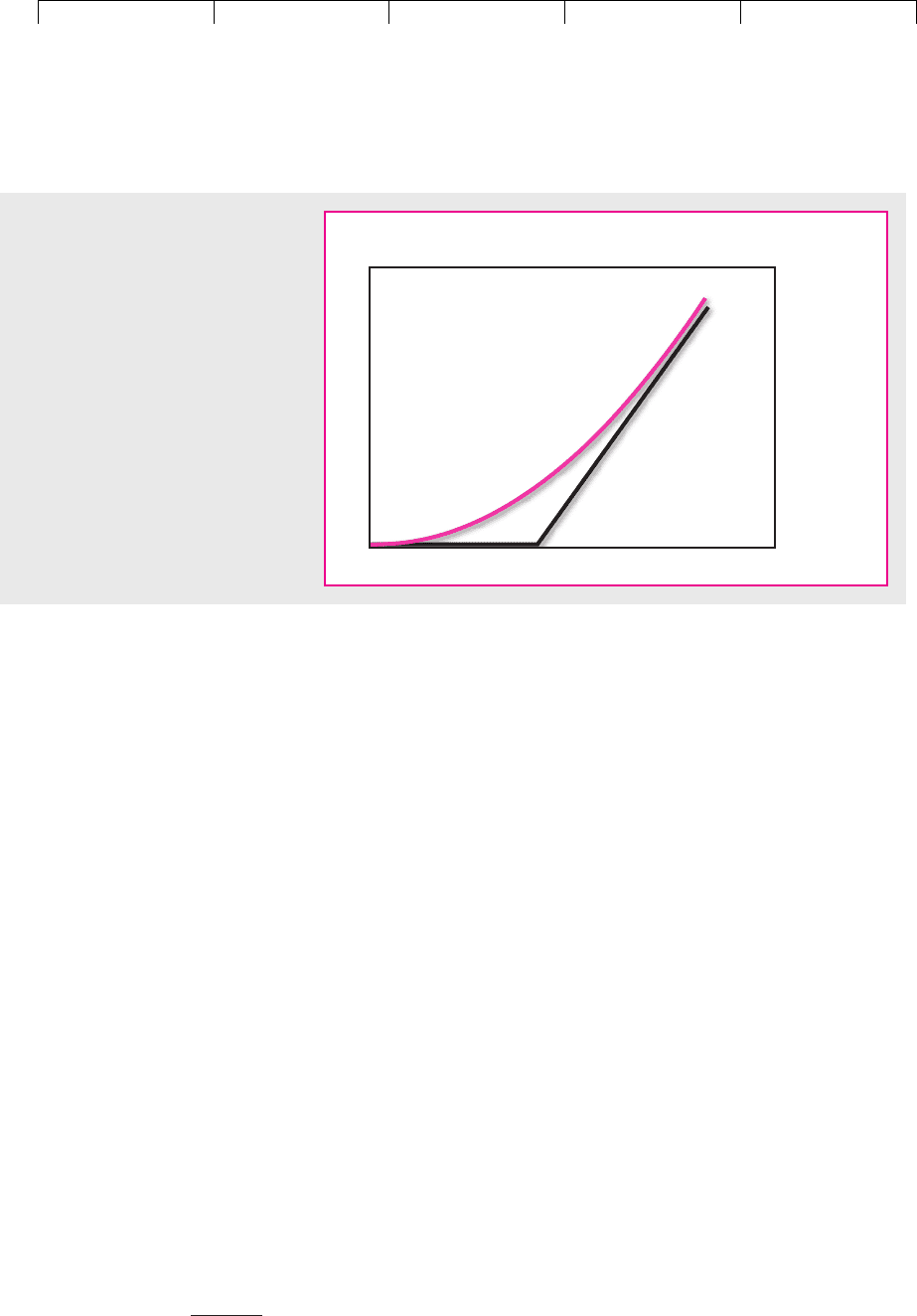

at $15 (after adjustment for the 1998 stock split). You can depict the relationship be-

tween the value of the warrant and the value of the common stock with our stan-

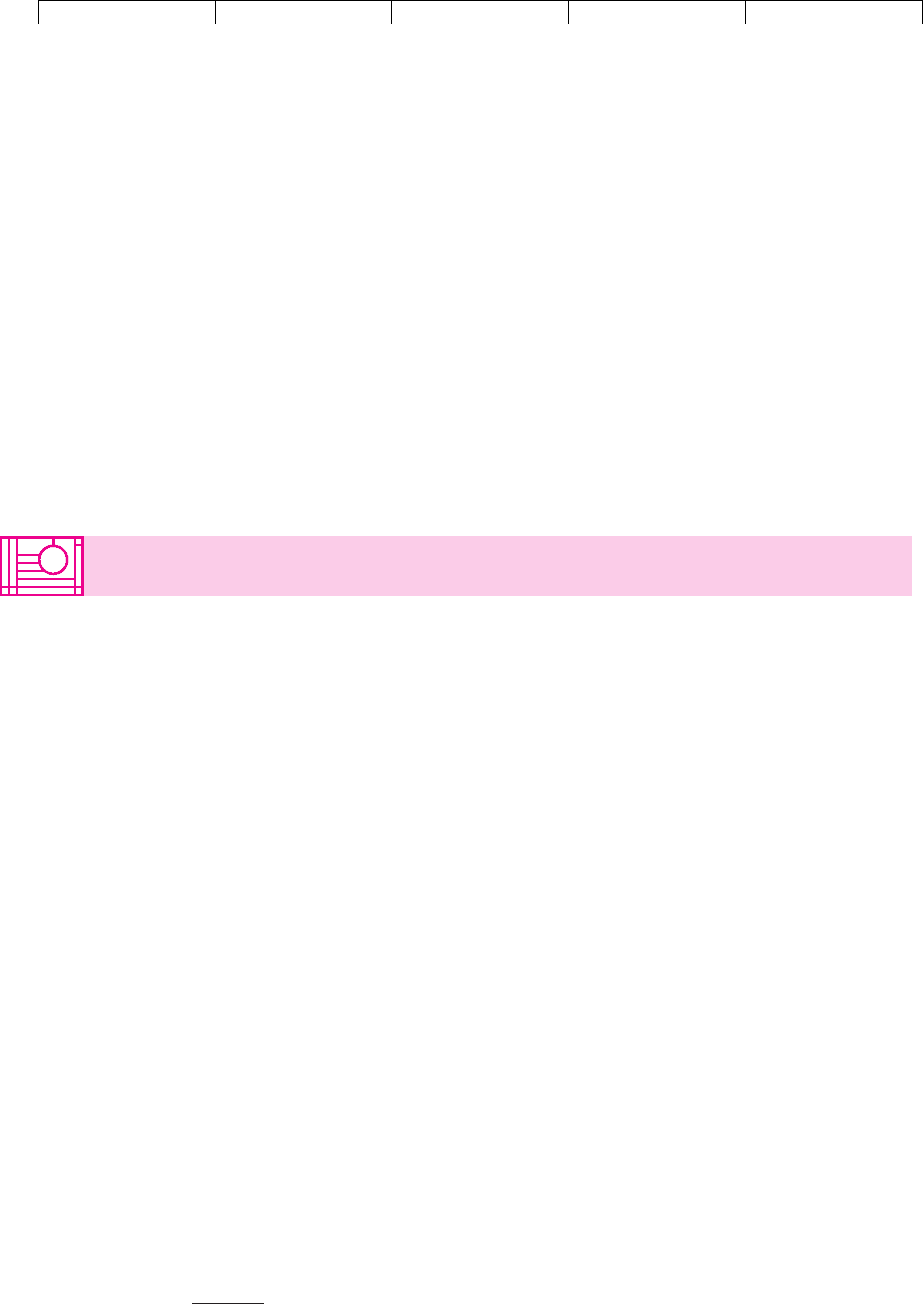

dard option shorthand, as in Figure 23.1. The lower limit on the value of the war-

rant is the heavy line in the figure.

2

If the price of B.J. Services stock is less than $15,

the lower limit on the warrant price is zero; if the price of the stock is greater than

$15, the lower limit is equal to the stock price minus $15. Investors in warrants

sometimes refer to this lower limit as the theoretical value of the warrant. It is a mis-

leading term, because both theory and practice tell us that before the final exercise

date the value of the warrant should lie above the lower limit, on a curve like the

one shown in Figure 23.1.

1

The term warrant usually refers to a long-term option issued by a company on its own stock or bonds, but

investment banks and other financial institutions also issue “warrants” to buy the stock of another firm.

2

Do you remember why this is a lower limit? What would happen if, by some accident, the warrant

price was less than the stock price minus $15? (See Section 20.3.)

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

VI. Options 23. Warrants and

Convertibles

© The McGraw−Hill

Companies, 2003

The height of this curve depends on two things. As we explained in Section 20.3,

it depends on the variance of the stock returns per period (

2

) times the number of

periods before the option expires (

2

t). It also depends on the rate of interest (r

f

)

times the number of option periods (t). Of course as time runs out on a warrant, its

price snuggles closer and closer to the lower bound. On the final day of its life, its

price hits the lower bound.

Two Complications: Dividends and Dilution

If the warrant has no unusual features and the stock pays no dividends, then the

value of the option can be estimated from the Black–Scholes formula described in

Section 21.3.

But there is a problem when warrants are issued against dividend-paying stocks.

The warrant holder is not entitled to dividends. In fact the warrant holder loses every

time a cash dividend is paid because the dividend reduces stock price and thus re-

duces the value of the warrant. It may pay to exercise the warrant before maturity in

order to capture the extra income.

3

Remember that the Black–Scholes option-valuation formula assumes that the

stock pays no dividends. Thus it will not give the theoretically correct value for

a warrant issued by a dividend-paying firm. However, we showed in Chapter 21

how you can use the one-step-at-a-time binomial method to value options on

dividend-paying stocks.

Another complication is that exercise of the warrants increases the number of

shares. Therefore, exercise means that the firm’s assets and profits are spread over

a larger number of shares. Firms with significant amounts of warrants or convert-

ibles outstanding are required to report earnings on a “fully diluted” basis, which

recognizes the potential increase in the number of shares.

644 PART VI

Options

3

This cannot make sense unless the dividend payment is larger than the interest that could be earned

on the exercise price. By not exercising, the warrant holder keeps the exercise price and can put this

money to work.

Value of

warrant

Actual warrant

value prior to

expiration

Stock price

Exercise price = $15

Theoretical

value (lower

limit on

warrant value)

FIGURE 23.1

Relationship between the value of the

B.J. Services warrant and stock price.

The heavy line is the lower limit for

warrant value. Warrant value falls to

the lower limit just before the option

expires. Before expiration, warrant

value lies on a curve like the one

shown here.

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

VI. Options 23. Warrants and

Convertibles

© The McGraw−Hill

Companies, 2003

This problem of dilution never arises with call options. If you buy or sell an op-

tion on the Chicago Board Options Exchange, you have no effect on the number of

shares outstanding.

Example: Valuing United Glue’s Warrants

United Glue has just issued a $2 million package of debt and warrants. Here are

some basic data that we can use to value the warrants:

• Number of shares outstanding (N): 1 million

• Current stock price (P): $12

• Number of warrants issued per share outstanding (q): .10

• Total number of warrants issued (Nq): 100,000

• Exercise price of warrants (EX): $10

• Time to expiration of warrants (t): 4 years

• Annual standard deviation of stock price changes (): .40

• Rate of interest (r): 10%

• United stock pays no dividends.

Suppose that without the warrants the debt is worth $1.5 million. Then investors

must be paying $.5 million for the warrants:

500,000 ⫽ 2,000,000 ⫺ 1,500,000

Table 23.1 shows the market value of United’s assets and liabilities both before

and after the issue.

Now let us take a stab at checking whether the warrants are really worth the

$500,000 that investors are paying for them. Since the warrant is a call option to buy

the United stock, we can use the Black–Scholes formula to value the warrant. It

Each warrant costs investors

500,000

100,000

⫽ $5

Cost of warrants ⫽ total amount of financing ⫺ value of loan without warrants

CHAPTER 23 Warrants and Convertibles 645

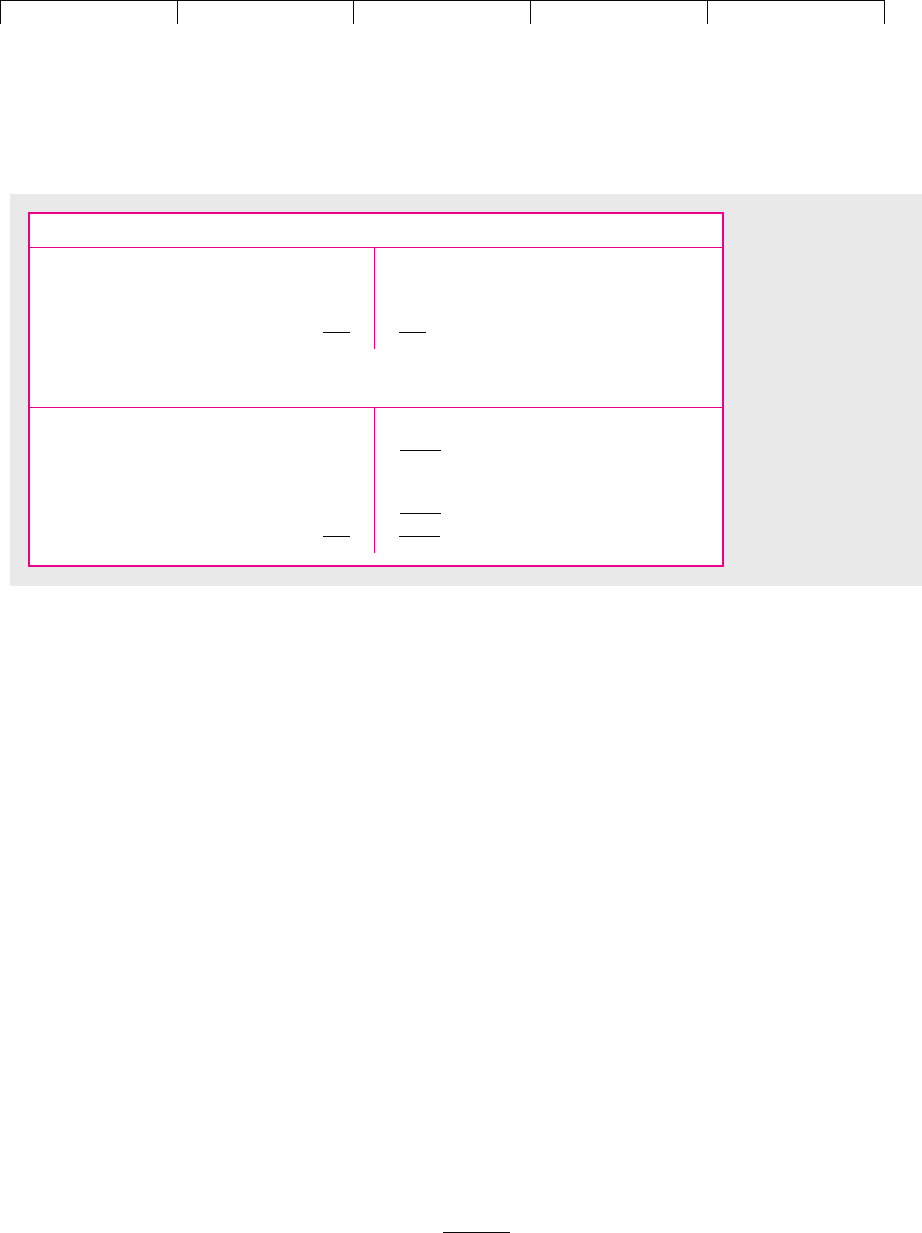

Before the Issue

Existing assets $16 $ 4 Existing loans

12 Common stock

(1 million shares

at $12 a share)

Total $16 $16 Total

After the Issue

Existing assets $16 $ 4 Existing loans

New assets financed 1.5 New loan without warrants

by debt and warrants 2 5.5 Total debt

.5 Warrants

12 Common stock

12.5 Total equity

Total $18 $18.0 Total

TABLE 23.1

United Glue’s market

value balance sheet

(in $ millions).

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

VI. Options 23. Warrants and

Convertibles

© The McGraw−Hill

Companies, 2003

turns out that a four-year call to buy United stock at $10 is worth $6.15.

4

Thus the

warrant issue looks like a good deal for investors and a bad deal for United. In-

vestors are paying $5 a share for warrants that are worth $6.15.

How the Value of United Warrants Is Affected by Dilution

Unfortunately, our calculations for United warrants do not tell the whole story.

Remember that when investors exercise a traded call or put option, there is no

change in either the company’s assets or the number of shares outstanding. But,

if United’s warrants are exercised, the number of shares outstanding will in-

crease by Nq ⫽ 100,000. Also the assets will increase by the amount of the exer-

cise money (Nq ⫻ EX ⫽ 100,000 ⫻ $10 ⫽ $1 million). In other words, there will

be dilution. We need to allow for this dilution when we value the warrants.

Let us call the value of United’s equity V:

If the warrants are exercised, equity value will increase by the amount of the exer-

cise money to V ⫹ NqEX. At the same time the number of shares will increase to

N ⫹ Nq. So the share price after the warrants are exercised will be

At maturity the warrant holder can choose to let the warrants lapse or to exer-

cise them and receive the share price less the exercise price. Thus the value of the

warrants will be the share price minus the exercise price or zero, whichever is the

higher. Another way to write this is

This tells us the effect of dilution on the value of United’s warrants. The warrant

value is the value of 1/(1 ⫹ q) call options written on the stock of an alternative

firm with the same total equity value V, but with no outstanding warrants. The alter-

native firm’s stock price would be equal to V/N—that is, the total value of United’s

⫽

1

1 ⫹ q

maximum a

V

N

⫺ EX, 0b

⫽ maximum a

V/N ⫺ EX

1 ⫹ q

, 0b

⫽ maximum a

V ⫹ NqEX

N ⫹ Nq

⫺ EX, 0b

Warrant value at maturity ⫽ maximum 1share price ⫺ exercise price, zero2

Share price after exercise ⫽

V ⫹ NqEX

N ⫹ Nq

Value of equity ⫽ V ⫽ value of United’s total assets ⫺ value of debt

646 PART VI Options

4

In Chapter 21 we saw that the Black–Scholes formula for the value of a call is

where

Plugging the data for United into this formula gives

and

Appendix Table 6 shows that , and . Therefore, estimated warrant value ⫽

..865 ⫻ 12 ⫺ .620 ⫻ 110/1.1

4

2⫽ $6.15

N1d

2

2⫽ .620N1d

1

2⫽ .865

d

2

⫽ 1.104 ⫺ .40 ⫻ 24 ⫽ .304d

1

⫽ log 312/110/1.1

4

24/1.40 ⫻ 242⫹ .40 ⫻ 24/2 ⫽ 1.104

N1d

1

2⫽ cumulative normal probability function

d

2

⫽ d

1

⫺ 2t

d

1

⫽ log 3P/PV1EX24/2t ⫹ 2t/2

3N1d

1

2⫻ P 4⫺ 3N1d

2

2⫻ PV1EX24

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

VI. Options 23. Warrants and

Convertibles

© The McGraw−Hill

Companies, 2003

equity (V) divided by the number of shares outstanding (N).

5

The stock price of

this alternative firm is more variable than United’s stock price. So when we value

the call option on the alternative firm, we must remember to use the standard de-

viation of the changes in V/N.

Now we can recalculate the value of United’s warrants allowing for dilution.

First we find the stock price of the alternative firm:

Also, suppose the standard deviation of the share price changes of this alternative

firm is * ⫽ .41.

6

The Black–Scholes formula gives a value of $6.64 for a call option on a stock with

a price of $12.50 and a standard deviation of .41. The value of United warrants is

equal to the value of 1/(1 ⫹ q) call options on the stock of this alternative firm. Thus

warrant value is

This is a somewhat lower value than the one we computed when we ignored dilu-

tion but still a bad deal for United.

1

1 ⫹ q

⫻ value of call on alternative firm ⫽

1

1.1

⫻ 6.64 ⫽ $6.04

Current share price of alternative firm ⫽

V

N

⫽

12.5 million

1 million

⫽ $12.50

⫽ 18 ⫺ 5.5 ⫽ $12.5 million

⫺ value of loans

Current equity value of alternative firm ⫽ V ⫽ value of United’s total assets

CHAPTER 23 Warrants and Convertibles 647

5

The modifications to allow for dilution when valuing warrants were originally proposed in F. Black

and M. Scholes, “The Pricing of Options and Corporate Liabilities,” Journal of Political Economy 81

(May–June 1973), pp. 637–654. Our exposition follows a discussion in D. Galai and M. I. Schneller,

“Pricing of Warrants and the Valuation of the Firm,” Journal of Finance 33 (December 1978),

pp. 1333–1342.

6

How in practice could we compute *? It would be easy if we could wait until the warrants had

been trading for some time. In that case * could be computed from the returns on a package of all

the company’s shares and warrants. In the present case we need to value the warrants before they

start trading. We argue as follows: The standard deviation of the assets before the issue is equal to

the standard deviation of a package of the common stock and the existing loans. For example, sup-

pose that the company’s debt is risk-free and that the standard deviation of stock returns before the

bond–warrant issue is 38 percent. Then we calculate the standard deviation of the initial assets as

follows:

Now suppose that the assets after the issue are equally risky. Then

Notice that in our example the standard deviation of the stock returns before the warrant issue was

slightly lower than the standard deviation of the package of stock and warrants. However, the warrant

holders bear proportionately more of this risk than do the stockholders; so the bond–warrant package

could either increase or reduce the risk of the stock.

Standard deviation of equity 1*2⫽ 41%

28.5 ⫽

12.5

18

⫻ standard deviation of equity 1*2

Standard deviation

of assets after issue

⫽

proportion of equity

after issue

⫻

standard deviation

of equity 1*2

⫽

12

16

⫻ 38 ⫽ 28.5%

Standard deviation

of initial assets

⫽

proportion in

common stock

⫻

standard deviation

of common stock

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

VI. Options 23. Warrants and

Convertibles

© The McGraw−Hill

Companies, 2003

It may sound from all this as if you need to know the value of United warrants

to compute their value. This is not so. The formula does not call for warrant value

but for V, the value of United’s equity (that is, the shares plus warrants). Given eq-

uity value, the formula calculates how the overall value of equity should be split

up between stock and warrants. Thus, suppose that United’s underwriter advises

that $500,000 extra can be raised by issuing a package of bonds and warrants rather

than bonds alone. Is this a fair price? You can check using the Black–Scholes for-

mula with the adjustment for dilution.

Finally, notice that these modifications are necessary to apply the Black–Scholes

formula to value a warrant. They are not needed by the warrant holder, who must

decide whether to exercise at maturity. If at maturity the price of the stock exceeds

the exercise price of the warrant, the warrant holder will of course exercise.

648 PART VI

Options

7

The Amazon issue consisted of convertible subordinated notes. The term subordinated indicates that the

issue is a junior debt; its holders will be at the bottom of the heap of creditors in the event of default.

Notes are simply unsecured bonds. Therefore there are no specific assets that have been reserved to pay

off the holders in the event of default. There is more about these terms in Section 25.3.

23.2 WHAT IS A CONVERTIBLE BOND?

The convertible bond is a close relative of the bond–warrant package. Many com-

panies choose to issue convertible preferred as an alternative to issuing packages

of preferred stock and warrants. We will concentrate on convertible bonds, but al-

most all our comments apply to convertible preferred issues.

In 1999 Amazon.com issued $1.25 billion of 4 3/4 percent convertible bonds due

in 2009.

7

These could be converted at any time to 6.41 shares of common stock. In

other words, the owner had a 10-year option to return the bond to the company

and receive 6.41 shares of stock in exchange. The number of shares into which each

bond can be converted is called the bond’s conversion ratio. The conversion ratio of

the Amazon bond was 6.41.

To receive 6.41 shares of Amazon stock, the owner had to surrender bonds with

a face value of $1,000. This means that to receive one share, the owner had to sur-

render a face amount of $1,000/6.41 ⫽ $156.01. This figure is called the conversion

price. Anybody who bought the bond at $1,000 to convert it into 6.41 shares paid

the equivalent of $156.01 per share.

At the time of issue the price of Amazon stock was about $120 so the conversion

price was 30 percent higher than the stock price.

Convertibles are usually protected against stock splits or stock dividends. When

Amazon subsequently split its stock 2 for 1, the conversion ratio was increased to

12.82 and the conversion price dropped to $1,000/12.82 ⫽ $78.00.

The Convertible Menagerie

Amazon’s convertible issue is typical, but you may come across more complicated

cases. For example, in November 2000 Tyco raised the record sum of $3.5 billion

from a convertible issue. The Tyco issue was an example of a LYON (liquid yield

option note). A LYON is a callable and puttable, zero-coupon convertible bond

(and you can’t get much more complicated than that).

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

VI. Options 23. Warrants and

Convertibles

© The McGraw−Hill

Companies, 2003

The Tyco issue was a 20-year zero-coupon bond that was convertible at any time

into 10.3 shares. The bonds were issued at a price of $741.65, which gave bond-

holders a yield to maturity of 1.5 percent. When Tyco issued the convertible, cor-

porate bonds were yielding roughly 8 percent. So an investor who converted im-

mediately would be giving up a bond worth $1,000/1.08

20

⫽ $215. Investors who

waited 20 years to convert would be relinquishing a bond worth $1,000 (as long as

the firm is solvent). So the value of the bond that they give up increases each year.

The Tyco LYON contains two other options. Starting in 2007 the company has

the right to call the bond for cash. The exercise price of this call option starts at

82.34 percent and increases by 1.5 percent each year until it reaches 100 percent in

2014. The bondholders also have an option, for there are five days between 2001

and 2014 on which they can demand repayment of their bonds. The repayment

price starts at 75.28 percent and then is increased by 1.5 percent a year. These put

options help to provide a more solid floor to the issue. Even if interest rates rise and

prices of other bonds fall, LYON holders have a guaranteed price on these five days

at which they can sell their bonds.

8

Obviously, investors who exercise the put give

up the opportunity to convert their bonds into stock; it would be worth taking

advantage of the guarantee only if the conversion price of the bonds was well be-

low the exercise price of the put.

9

Mandatory Convertibles

In recent years a number of companies have issued preferred stock or debt that is

automatically converted into equity after several years. Investors in mandatory con-

vertibles receive the benefit of a higher current income than common stockholders,

but there is a limit on the value of the common stock that they ultimately receive.

Thus they share in the appreciation of the common stock only up to this limit. As

the stock price rises above this limit, the number of shares that the convertible

holder receives is reduced proportionately.

Valuing Convertible Bonds

The owner of a convertible owns a bond and a call option on the firm’s stock. So does

the owner of a bond–warrant package. There are differences, of course, the most im-

portant being the requirement that a convertible owner give up the bond in order to

exercise the call option. The owner of a bond–warrant package can (generally) exer-

cise the warrant for cash and keep the bond. Nevertheless, understanding convert-

ibles is easier if you analyze them first as bonds and then as call options.

Imagine that Eastman Kojak has issued convertible bonds with a total face value

of $1 million and that these can be converted at any stage to one million shares of

common stock. The price of Kojak’s convertible bond depends on its bond value and

its conversion value. The bond value is what each bond would sell for if it could not

be converted. The conversion value is what the bond would sell for if it had to be

converted immediately.

CHAPTER 23

Warrants and Convertibles 649

8

Of course, this guarantee would not be worth much if the company was in financial distress and

couldn’t buy the bonds back.

9

The reasons for issuing LYONs are discussed in J. J. McConnell and E. S. Schwartz, “The Origin of

LYONs: A Case Study in Financial Innovation,” Journal of Applied Corporate Finance 4 (Winter 1992),

pp. 40–47. For a discussion of how to value an earlier LYON issue by Waste Management see

J. McConnell and E. S. Schwartz, “Taming LYONs,” Journal of Finance 41 (July 1986), pp. 561–576.

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

VI. Options 23. Warrants and

Convertibles

© The McGraw−Hill

Companies, 2003

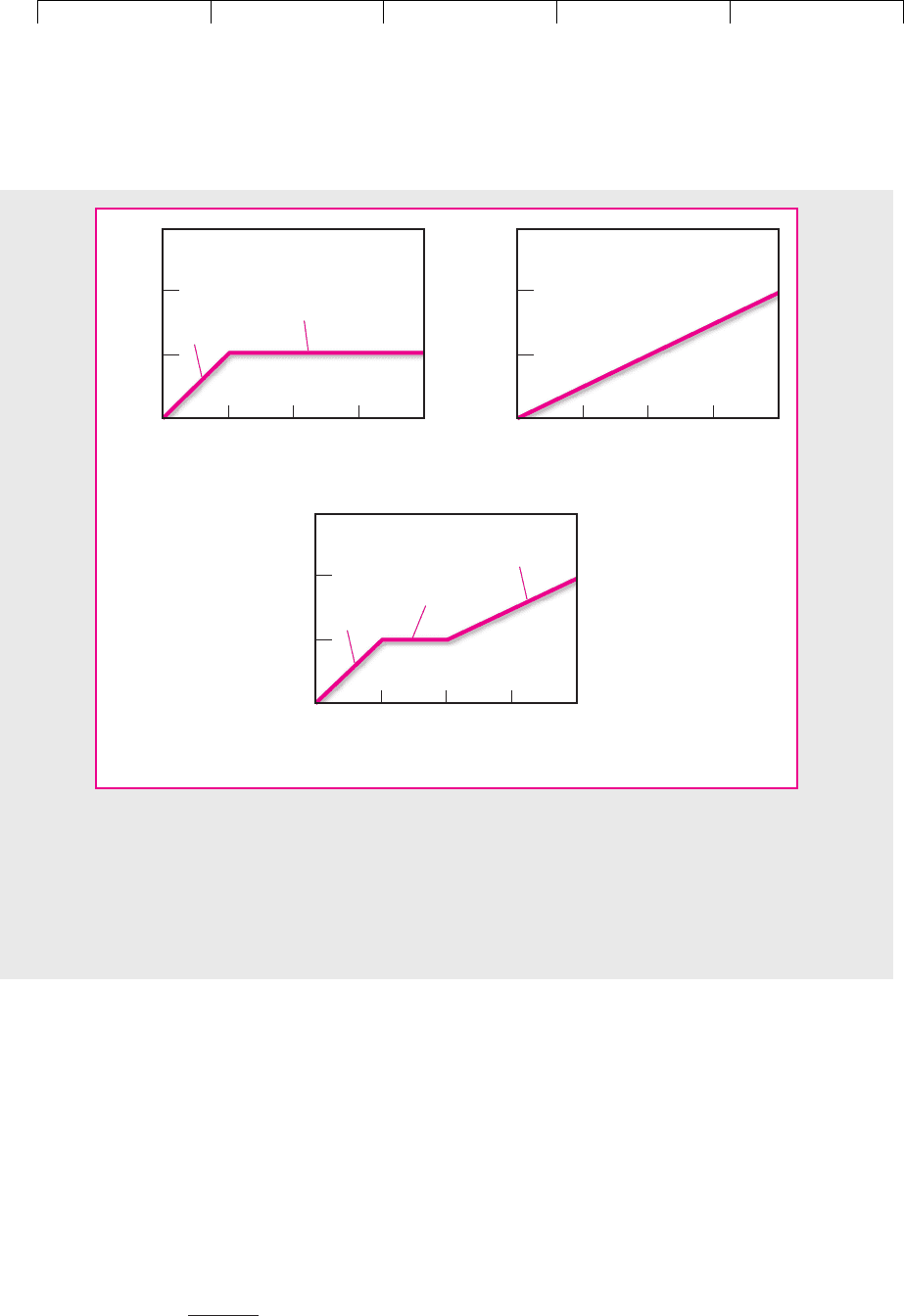

Value at Maturity Figure 23.2(a) shows the possible bond values when the Kojak

convertible matures. As long as the value of the firm’s assets does not fall below

$1 million, the bond will pay off in full. But if the firm value is less than $1 million,

there will not be enough to pay off the bondholders. In the extreme case that the

assets are worthless, the bondholders will receive nothing. Thus the horizontal line

in Figure 23.2(a) shows the payoff if the bond is repaid in full, and the sloping line

shows the payoffs if the firm defaults.

10

You can think of the bond value as a lower bound, or “floor,” to the price of

the convertible. But that floor has a nasty slope and, when the company falls on

hard times, the bonds may not be worth much. For example, we saw earlier how

Amazon.com issued a convertible bond in 1999. Over the following two years

650 PART VI

Options

1

0

01

2

3

2

Value of firm, $ millions

Bond value, $ thousands

3 4

Default

Bond paid

in full

(

a

)

1

0

01

2

3

2

Value of firm, $ millions

Value of convertible,

$ thousands

3 4

(

c

)

1

0

01

2

3

2

Value of firm, $ millions

Conversion value,

$ thousands

3 4

Default

Convert

Bond paid

in full

(

b

)

FIGURE 23.2

(a) The bond value when Eastman Kojak’s convertible bond matures. If firm value is at least

$1 million, the bond is paid off at its face value of $1000; if it is less than $1 million, the bondholders

receive the value of the firm’s assets. (b) The conversion value at maturity. If converted, the value of

the convertible bond rises in proportion to firm value. (c) At maturity the convertible bondholder can

choose to receive the principal repayment on the bond or convert to common stock. The value of the

convertible bond is therefore the higher of its bond value and its conversion value.

10

You may recognize this as the position diagram for a default-free bond minus a put option on the as-

sets with an exercise price equal to the face value of the bonds. See Section 20.1.

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

VI. Options 23. Warrants and

Convertibles

© The McGraw−Hill

Companies, 2003

investors became disenchanted with dot.com companies and Amazon’s stock price

fell by 75 percent to $15. This was well below the conversion price of $78.03. Con-

vertible bondholders might have hoped that the bond value would provide a secure

floor to the value of their investment. Unfortunately, by early 2001 Amazon’s bonds

no longer looked as safe as they once had, and Moody’s placed its convertible in the

junk bond category Caa. By the spring of that year the price of the convertible had

fallen to about $400 and offered a promised yield to maturity of 20 percent.

Figure 23.2(b) shows the possible conversion values at maturity of Kojak’s convert-

ible. We assume that Kojak already has one million shares of common stock out-

standing, so the convertible holders will be entitled to half the value of the firm. For

example, if the firm is worth $2 million,

11

the one million shares obtained by conver-

sion would be worth $1 each. Each convertible bond can be exchanged for 1,000 shares

of stock and therefore would have a conversion value of 1,000 ⫻ 1 ⫽ $1,000.

Kojak’s convertible also cannot sell for less than its conversion value. If it did,

smart investors would buy the convertible, exchange it rapidly for stock, and sell

the stock. Their profit would be equal to the difference between the conversion

value and the price of the convertible.

Therefore, there are two lower bounds to the price of the convertible: its bond

value and its conversion value. Investors will not convert if bond value exceeds

conversion value; they will do so if conversion value exceeds bond value. In other

words, the price of the convertible at maturity is represented by the higher of the

two lines in Figure 23.2(a) and (b). This is shown in Figure 23.2(c).

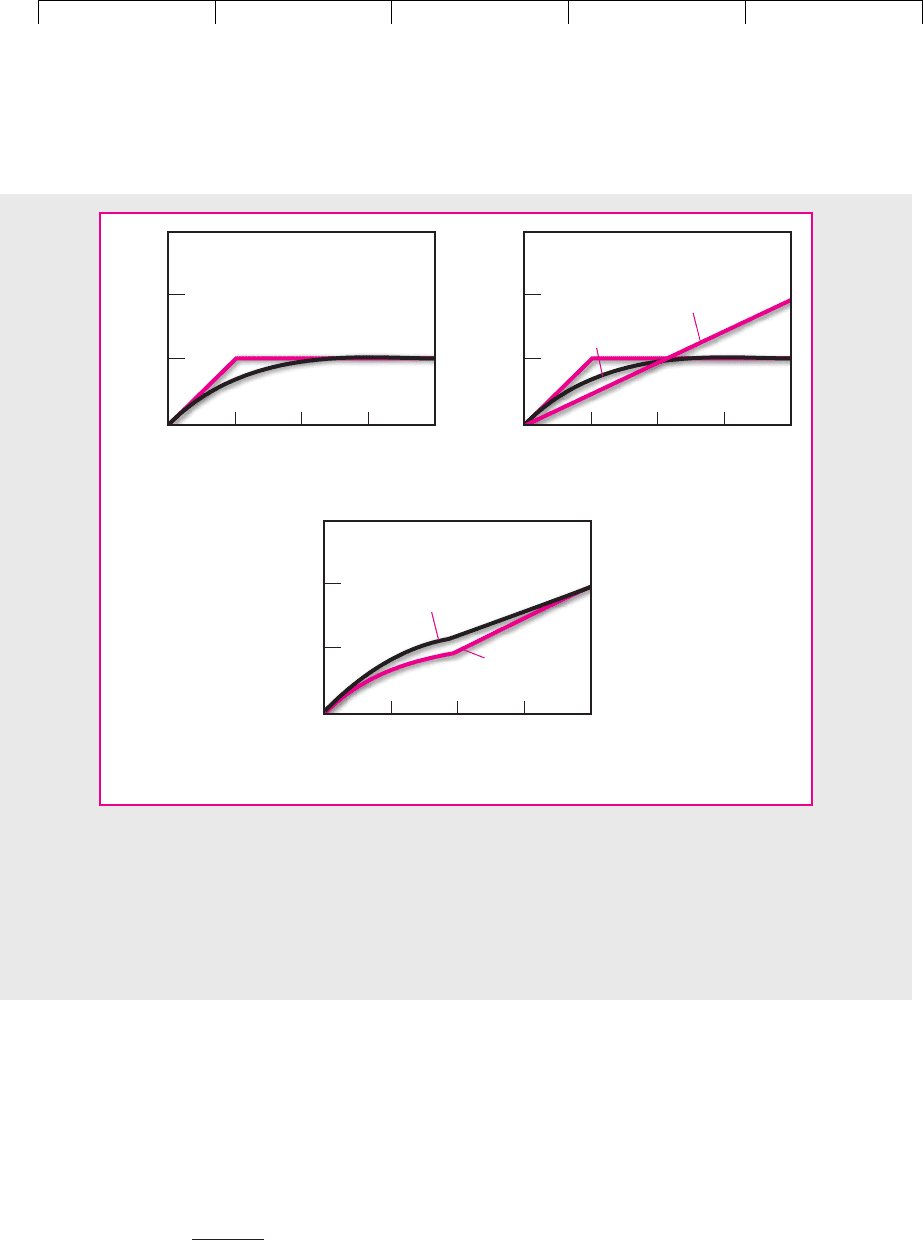

Value before Maturity We can also draw a picture similar to Figure 23.2 when the

convertible is not about to mature. Because even healthy companies may subse-

quently fall sick and default on their bonds, other things equal, the bond value will

be lower when the bond has some time to run. Thus bond value before maturity is

represented by the curved line in Figure 23.3(a).

12

Figure 23.3(b) shows that the lower bound to the price of a convertible before

maturity is again the higher of the bond value and conversion value. However,

before maturity the convertible bondholders do not have to make a now-or-never

choice for or against conversion. They can wait and then, with the benefit of hind-

sight, take whatever course turns out to give them the highest payoff. Thus be-

fore maturity a convertible is always worth more than its lower-bound value. Its

actual selling price will behave as shown by the top line in Figure 23.3(c). The dif-

ference between the top line and the lower bound is the value of a call option on

the firm. Remember, however, that this option can be exercised only by giving up

the bond. In other words, the option to convert is a call option with an exercise

price equal to the bond value.

Dilution and Dividends Revisited

If you want to value a convertible, it is easiest to break the problem down into two

parts. First estimate bond value; then add the value of the conversion option.

When you value the conversion option, you need to look out for the same

things that make warrants more tricky to value than traded options. For example,

CHAPTER 23

Warrants and Convertibles 651

11

Firm value is equal to the value of Kojak’s common stock plus the value of its convertible bonds.

12

Remember, the value of a risky bond is the value of a safe bond less the value of a put option on the

firm’s assets. The value of this option increases with maturity.

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

VI. Options 23. Warrants and

Convertibles

© The McGraw−Hill

Companies, 2003

dilution may be important. If the bonds are converted, the company saves on its

interest payments and is relieved of having to eventually repay the loan; on the

other hand, net profits have to be divided among a larger number of shares.

13

Companies are obliged to show in their financial statements how earnings would

be affected by conversion.

14

Also, you must remember that the convertible owner is missing out on the div-

idends on the common stock. If these dividends are higher than the interest on the

652 PART VI

Options

Bond value

Conversion value

1

0

01

2

3

2

Value of firm, $ millions

Bond value, $ thousands

3 4

(

a

)

1

0

01

2

3

2

Value of firm, $ millions

Lower limit on convertible,

$ thousands

3 4

(

b

)

Lower limit

on value

Value of convertible

1

0

01

2

3

2

Value of firm, $ millions

Value of convertible,

$ thousands

3 4

(

c

)

FIGURE 23.3

(a) Before maturity the bond value of Eastman Kojak’s convertible bond is close to that of a similar

default-free bond when firm value is high, but it falls sharply if firm value falls to a very low level.

(b) If investors were obliged to make an immediate decision for or against conversion, the value of

the convertible would be equal to the higher of bond value or conversion value. (c) Since convert-

ible bondholders do not have to make a decision until maturity, (b) represents a lower limit. The

value of the convertible bond is worth more than either bond value or conversion value.

13

In practice investors often ignore dilution and calculate conversion value as the share price times the

number of shares into which the bonds can be converted. A convertible bond actually gives an option

to acquire a fraction of the “new equity”—the equity after conversion. When we calculated the conver-

sion value of Kojak’s convertible, we recognized this by multiplying the proportion of common stock

that the convertible bondholders would receive by the total value of the firm’s assets (i.e., the value of

the common stock plus the value of the convertible).

14

These “diluted” earnings take into account the extra shares but not the savings in interest payments.