Simon Benninga. Financial Modelling 3-rd edition

Подождите немного. Документ загружается.

2

Calculating the Cost of Capital

2.1 Overview

In this chapter we discuss the calculation of the fi rm’s weighted average

cost of capital (WACC). The WACC has two important uses in fi nance:

•

When used as the discount rate for a fi rm’s anticipated free cash fl ows

(FCF), the WACC gives the enterprise value of the fi rm. FCF is discussed

at length in Chapters 3 and 4. At this point it suffi ces to say that the FCF

is the cash fl ow generated by the fi rm’s core business activities. These

chapters also show how to apply the WACC to the valuation of fi rms.

•

The WACC is also the appropriate risk-adjusted discount rate for fi rm

projects whose riskiness is similar to the average riskiness of the fi rm’s

cash fl ows. When used in this context, the WACC is often referred to as

the fi rm’s hurdle rate.

The WACC is a weighted average of the fi rm’s cost of equity r

E

and its

cost of debt r

D

, with the weights created by the market values of the

fi rm’s equity (E) and debt (D):

WACC

E

ED

r

D

ED

rT

EDC

=

+

+

+

−()1

where r

E

is the fi rm’s cost of equity, r

D

is the fi rm’s cost of debt, E is the

market value of the fi rm’s equity, D is the market value of the fi rm’s debt,

and T

C

is the fi rm’s corporate tax rate.

This chapter discusses the computation of r

E

and r

D

and shows detailed

examples of how to compute the fi rm’s WACC. The reader should be

warned that the application of the models discussed requires a good deal

of judgment—computing the WACC is equal parts science and art!

We consider two models for calculating the cost of equity r

E

, the dis-

count rate applied to equity cash fl ows. Each model has variations that

are explored throughout the chapter:

•

The Gordon model calculates the cost of equity based on the antici-

pated cash fl ows paid to the shareholders of the fi rm. Variations on this

model include multiple growth rates and the defi nition of the equity cash

fl ows.

•

The capital asset pricing model (CAPM) calculates the cost of equity

based on the correlation between the fi rm’s equity returns and the

40 Chapter 2

returns of a large, diversifi ed, market portfolio. As we will see, the CAPM

can also be used to calculate the cost of the fi rm’s debt. Variations on

this model include the tax framework in which the model is defi ned.

The other component of the cost of capital is the cost of debt r

D

, the

anticipated future cost of the fi rm’s borrowing. This book contains three

models to calculate the cost of debt; two of these models are discussed

in this chapter and a third method is discussed separately in Chapter

28:

•

The cost of debt r

D

is most commonly computed by using the fi rm’s

current interest payments divided by its average debt.

•

An alternative method is to compute r

D

by imputing the fi rm’s cost of

debt from a rating-adjusted yield curve.

•

Finally, we can compute the expected return on the fi rm’s bonds as a

proxy for its cost of debt; we discuss this method separately in Chapter

28.

A Terminological Note As noted in Chapter 1, “cost of capital” is a

synonym for the “appropriate discount rate” to be applied to a series of

cash fl ows. In fi nance “appropriate” is most often a synonym for “risk-

adjusted.” Hence another name for the cost of capital is the “risk-adjusted

discount rate” (RADR).

2.2 The Gordon Dividend Model

The Gordon dividend model

1

derives the cost of equity from the follow-

ing deceptively simple statement:

The value of a share is the present value of the future anticipated

dividend stream from the share, where the future anticipated dividends

are discounted at the appropriate risk-adjusted cost of equity r

E

.

The simplest application of the Gordon model is the case where the

anticipated future growth rate of dividends is constant. Suppose that the

1. This model is named after M. J. Gordon, who fi rst published this formula in a

paper entitled “Dividends, Earnings, and Stock Prices,” Review of Economics and

Statistics 41.

41 Calculating the Cost of Capital

current stock price is P

0

, the current dividend is Div

0

, and the anticipated

growth rate of future dividends is g. The Gordon model states that the

stock price equals the discounted (at the appropriate cost of equity r

E

)

future dividends:

P

g

r

g

r

g

r

EE E

0

2

2

3

3

1

1

1

1

1

1

=

+

+

+

∗+

+

+

∗+

+

+

Div Div Div Div

01 1

() ()

()

()

()

11

0

Div

∗+

+

+

=

∗+

+

=

∞

∑

()

()

...

()

()

1

1

1

1

4

4

1

g

r

g

r

E

t

E

t

t

Provided that |g| < r

E

, the expression

Div

0

∗+

+

=

∞

∑

()

()

1

1

1

g

r

t

E

t

t

can be reduced

to

Div

0

()1+

−

g

rg

E

(see the following box for derivation). Thus, given a

constant anticipated dividend growth rate, we derive the Gordon model

cost of equity:

P

g

rg

gr

E

E0

1

=

+

−

<

Div

, provided

0

()

Note the proviso at the end of this formula: In order for the infi nite sum

on the fi rst line of the formula to have a fi nite solution, the growth rates

of the dividends must be less than the discount rate. In our discussion of

the Gordon model with supernormal growth rates (section 2.4), we

return to the case where this condition is not satisfi ed.

Euler’s Formula for the Sum of a Geometric Series: Recalling

High School Algebra

The Gordon formula in this chapter, both in its standard form and

for supernormal growth (section 2.4), derives from a formula for

the sum of a geometric series due to the Swiss mathematician

Leonhard Euler (1707–83). This formula is a staple of high school

algebra. Euler showed that the sum of a geometric series:

S a aq aq aq

aq

q

q

n

n

=+ + + +

=

−

−

<

−21

1

1

1

...

()

, provided

42 Chapter 2

Solving the previous expression for r

E

gives a simple expression for

the Gordon-model cost of capital:

r

g

P

g

E

=

+

()

+

Div

0

1

0

To apply this formula, consider a fi rm whose current dividend is

Div

0

= $3 per share and whose share price is P

0

= $50. Suppose the

dividend is anticipated to grow by 12 percent per year. Then the fi rm’s

cost of equity r

E

is 17.6 percent:

The term a is the fi rst term of the series, q is commonly called the

ratio of the terms, and n is the number of terms. We leave the deri-

vation to you; the application to the Gordon formula is

Div

Lim

Div

0

0

∗+

+

=

+

+

⎛

⎝

⎜

⎞

⎠

⎟

−

+

+

⎛

⎝

⎜

⎞

⎠

⎟

→∞

()

()

1

1

1

1

1

1

1

g

r

g

r

g

r

t

E

t

n

EE

n

⎡⎡

⎣

⎢

⎤

⎦

⎥

−

+

+

⎛

⎝

⎜

⎞

⎠

⎟

=

+

−

+

+

<

=

∞

∑

1

1

1

1

1

g

r

g

rg

g

r

E

t

EE

Div

, provided

1

1

0

()

11

Note that in this formulation

a

g

r

E

=

+

+

⎛

⎝

⎜

⎞

⎠

⎟

Div

0

1

1

,

q

g

r

E

=

+

+

⎛

⎝

⎜

⎞

⎠

⎟

1

1

, and

n = ∞.

1

2

3

4

5

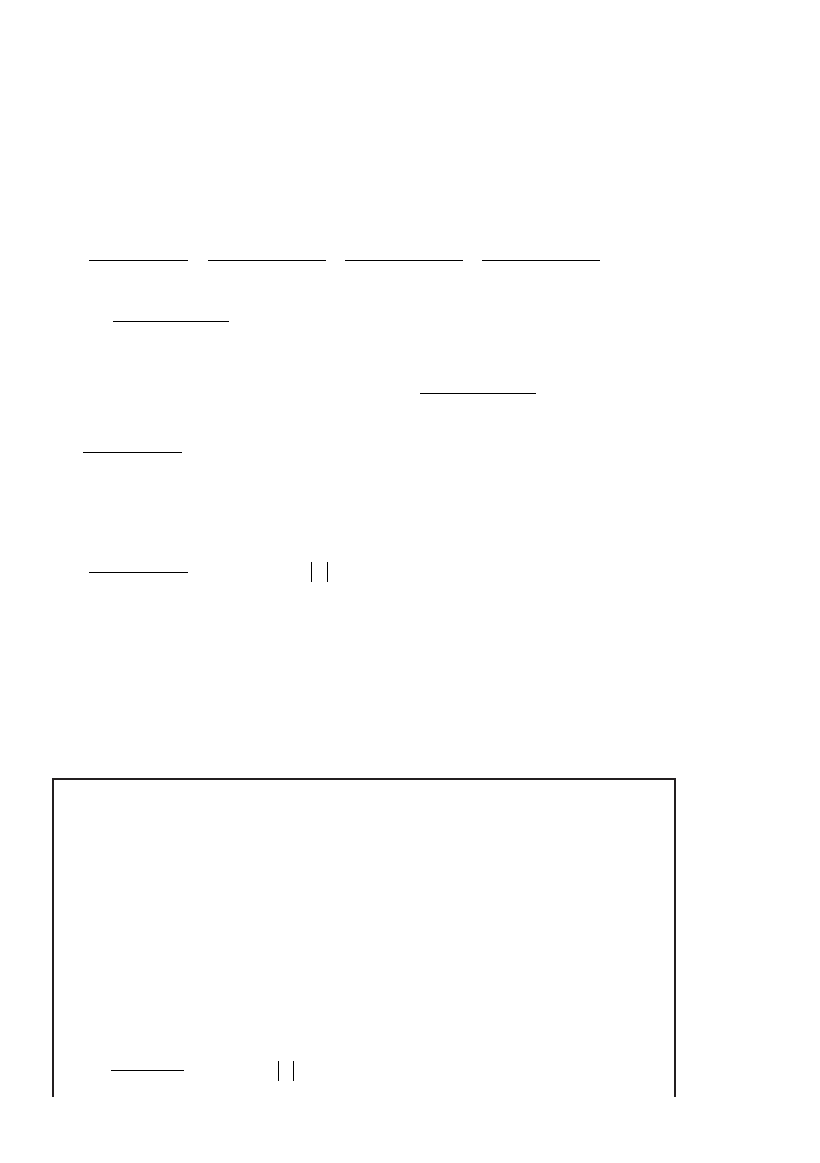

CBA

Current share price, P

0

60

Current dividend, D

0

3

Anticipated dividend growth rate 12%

Gordon model cost of equity, r

E

17.60% <-- =B3*(1+B4)/B2+B4

THE GORDON MODEL COST OF EQUITY

43 Calculating the Cost of Capital

The annualized growth rate of Kellogg’s historical dividends may be

either 1.90 percent or 3.61 percent, depending on the period taken. For

purposes of computing the cost of equity r

E

, the question is which of

these rates better predicts future anticipated dividend growth rates.

2

In

the following spreadsheet we allow for both possibilities. The calculations

use Kellogg’s stock price at the end of May 2006, P

0

= $48.28.

1

2

3

4

5

6

7

8

9

10

11

12

13

43

44

45

46

47

48

49

50

51

CBA

Dividend growth rate, quarterly

last 5 years 0.47% <-- =(B51/B31)^(1/20)-1

last 10 years 0.89% <-- =(B51/B11)^(1/40)-1

Dividend growth rate, annualized

Last 5 years 1.90% <-- =(1+B3)^4-1

Last 10 years 3.61% <-- =(1+B4)^4-1

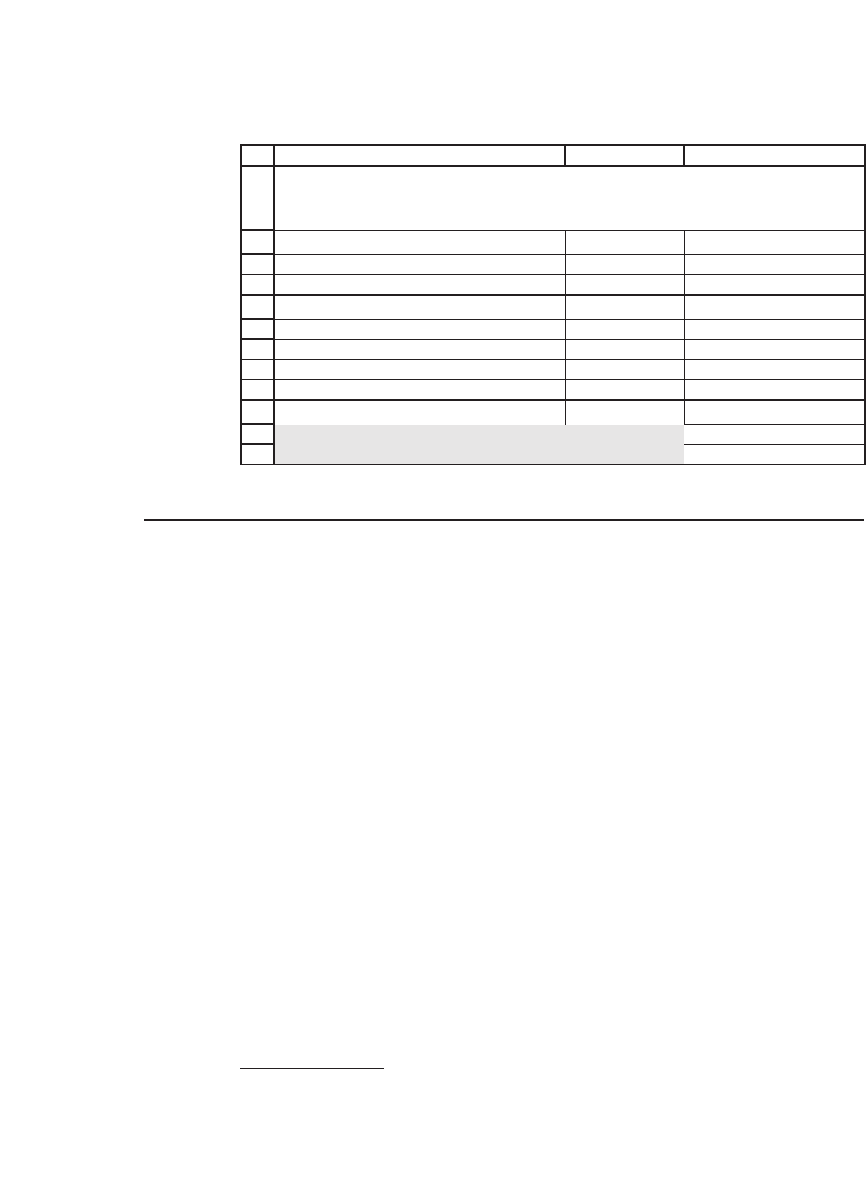

Date Dividends

29-May-96 0.195

28-Aug-96 0.210

26-Nov-96 0.210

27-May-04 0.253

27-Aug-04 0.253

23-Nov-04 0.253

25-Feb-05 0.253

27-May-05 0.253

30-Aug-05 0.278

29-Nov-05 0.278

27-Feb-06 0.278

30-May-06 0.278

KELLOGG DIVIDENDS, MAY1996 - MAY2006

2. Or perhaps neither does! Perhaps we are better off using another story altogether to

predict future anticipated dividend growth. We could use a pro forma model (discussed

in Chapter 3) to predict the fi rm’s anticipated dividend payout.

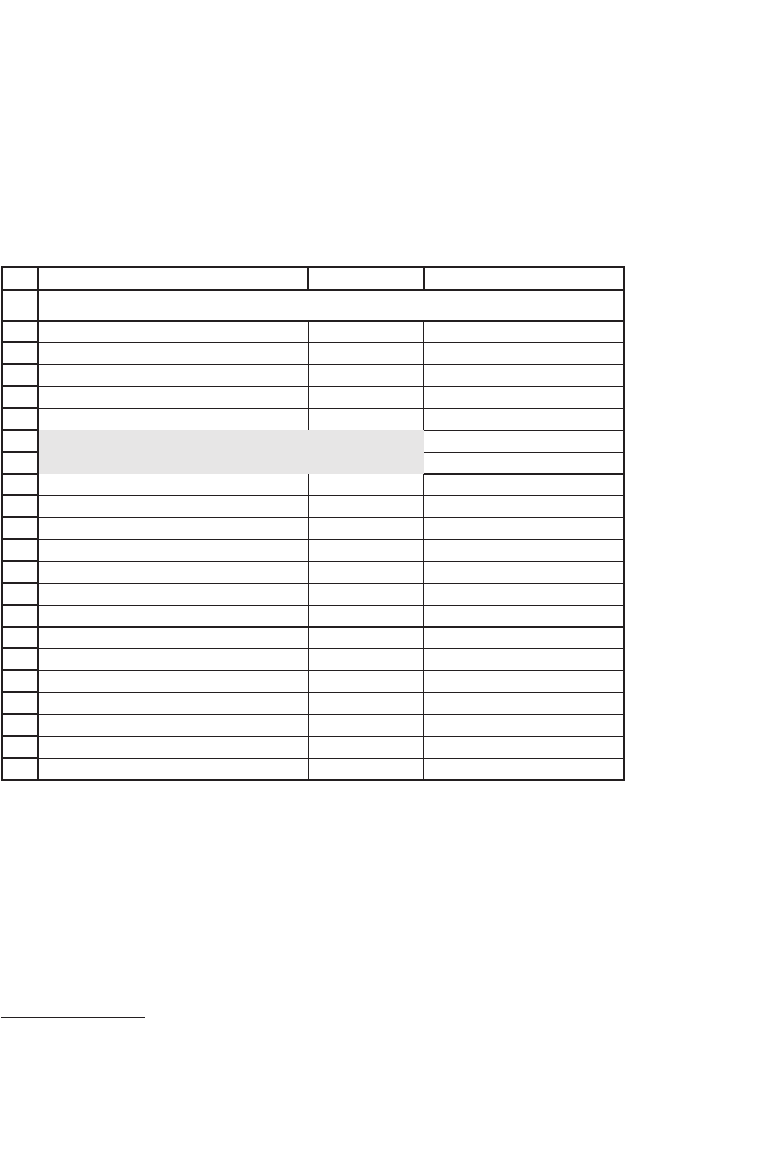

2.2.1 Using the Gordon Model to Compute the Cost of Equity for Kellogg

We apply the Gordon model to Kellogg, whose 10-year dividend history

is given in the following spreadsheet (note that some of the data have

been hidden):

44 Chapter 2

2.3 Adjusting the Gordon Model to Account for All Cash Flows to Equity

As illustrated in the preceding section, the Gordon model is computed

on a per-share basis and for dividends only. However, for purposes of

valuing the fi rm’s equity, the Gordon model should be extended to

include all cash fl ows to equity. In addition to dividends, cash fl ows to

equity include at least two additional components:

•

Share repurchases now account for around 50 percent of the total cash

disbursed by American corporations to their shareholders.

3

•

The issuance of stock by the fi rm is an important negative cash fl ow to

equity. In many fi rms the most important instance of stock issuance is

the exercise by employees of their stock options. On occasion companies

both issue stock and repurchase it; Johnson & Johnson (discussed in this

section) and Wachovia Bank (discussed in section 2.4.1) are both cases

in point.

In order to account for these additional cash fl ows to equity, we have

to rewrite the Gordon model in terms of total equity value. The basic

valuation model of Gordon now becomes

1

2

3

4

5

6

7

8

9

10

11

12

BA

C

Kellogg stock price, P

0,

30 May 2006

48.28

Current dividend

Quarterly 0.278

Annualized dividend, Div

0

1.112 <-- =B4*4

Dividend growth rate, g

Last 5 years 1.90%

Last 10 years 3.61%

Gordon model cost of equity r

E

Using last 5 years' growth 4.25% <-- =B5*(1+B7)/B2+B7

Using last 10 years' growth 6.00% <-- =B5*(1+B8)/B2+B8

COMPUTING KELLOGG'S r

E

WITH THE GORDON MODEL

3. Dittmar, A. K., and R. F. Dittmar, 2004. “Stock Repurchase Waves: An Explanation of

the Trends in Aggregate Corporate Payout Policy.” Working paper, University of

Michigan.

45 Calculating the Cost of Capital

Market value of equity

Cash flow to equity

0

=

∗+

+

=

∞

∑

()

()

1

1

1

g

r

t

E

t

t

where g is anticipated growth rate of cash fl ow to equity.

This gives the formula for the cost of equity r

E

as

r

g

gifg r

EE

=

+

()

+<

Cash flow to equity

Market value of equity

,

0

1

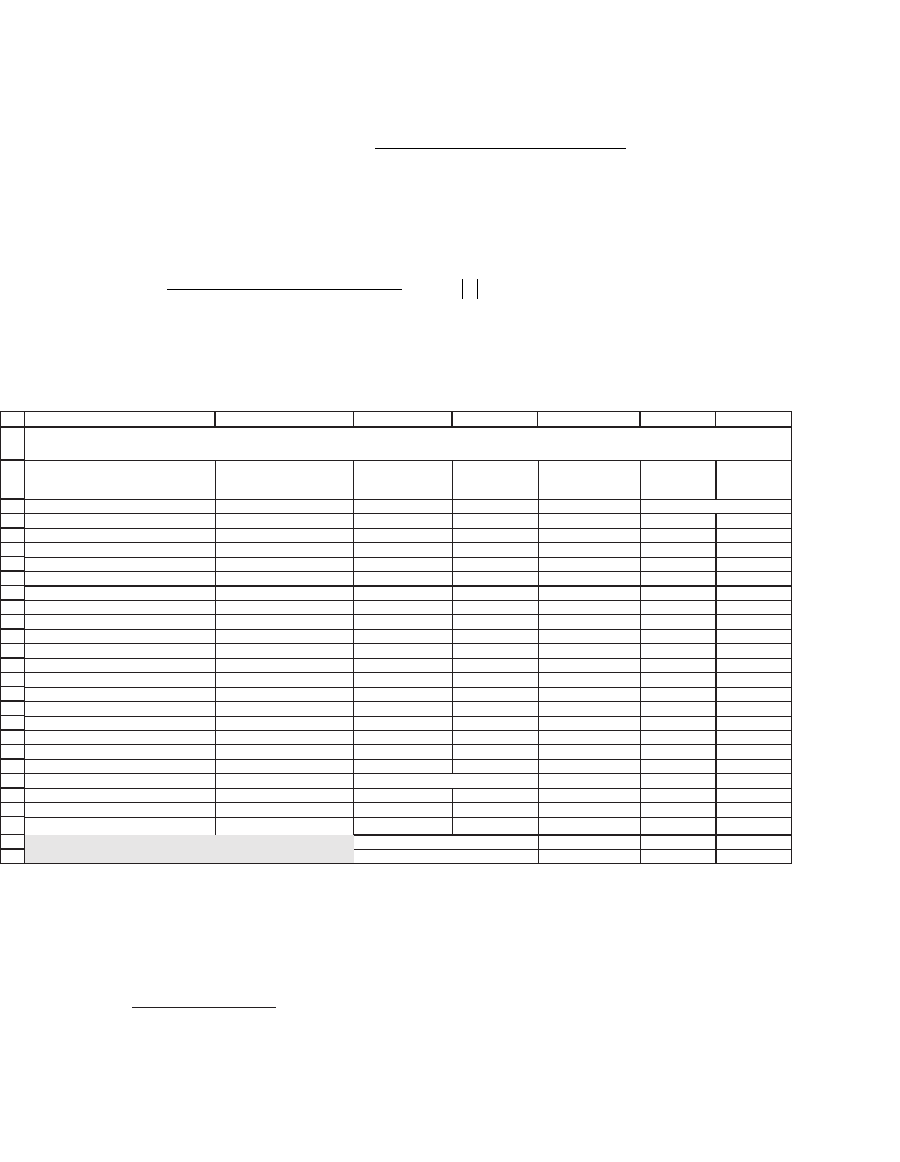

As an example, we consider the following data for Johnson &

Johnson:

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

CBADEF

G

Year ending Dividends

Repurchase of

common stock

Stock issues

Cash flow to

equity

Year on

year growth

31-Dec-95 827,000,000 322,000,000 -112,000,000 1,037,000,000 <-- =SUM(B3:D3)

31-Dec-96 974,000,000 412,000,000 -149,000,000 1,237,000,000 19.29% <-- =E4/E3-1

31-Dec-97 1,137,000,000 628,000,000 -225,000,000 1,540,000,000 24.49% <-- =E5/E4-1

31-Dec-98 1,305,000,000 930,000,000 -269,000,000 1,966,000,000 27.66% <-- =E6/E5-1

31-Dec-99 1,479,000,000 840,000,000 -221,000,000 2,098,000,000 6.71%

31-Dec-00 1,724,000,000 973,000,000 -387,000,000 2,310,000,000 10.10%

31-Dec-01 2,047,000,000 2,570,000,000 -514,000,000 4,103,000,000 77.62%

31-Dec-02 2,381,000,000 6,538,000,000 -390,000,000 8,529,000,000 107.87%

31-Dec-03 2,746,000,000 1,183,000,000 -311,000,000 3,618,000,000 -57.58%

31-Dec-04 3,251,000,000 1,384,000,000 -642,000,000 3,993,000,000 10.36%

31-Dec-05 3,793,000,000 1,717,000,000 -696,000,000 4,814,000,000 20.56%

End 2005 equity data

Stock price 61.07

Number of shares 3,119,842,000

Equity value 190,528,750,940 <-- =B16*B17

Equity cash flow, end 2005 4,814,000,000 <-- =E13

Future growth rate

Based on 10-year growth rate 16.59% <-- =(E13/E3)^(1/10)-1

Based on 5-year growth rate 15.82%

Gordon cost of equity, r

E

Based on 10-year growth rate 19.54% <-- =B20*(1+B22)/B18+B22

Based on 5-year growth rate 18.75% <-- =B20*(1+B23)/B18+B23

JOHNSON & JOHNSON, CASH FLOW TO EQUITY, 1995–2005

4. A major problem of computing the total equity cash fl ows is that stock repurchases

and employee stock exercises are only reported in the annual fi nancial statements. Thus

the only data available for these numbers are annual data, whereas dividends are

reported quarterly, and stock price data—used to compute the CAPM beta discussed

in section 2.5—are available on a daily basis.

If we assume that J&J’s historic growth rate of cash fl ow to equity,

16.59 percent, will persist in the indefi nite future, then its cost of equity

is r

E

= 19.54 percent (cell B26).

4

46 Chapter 2

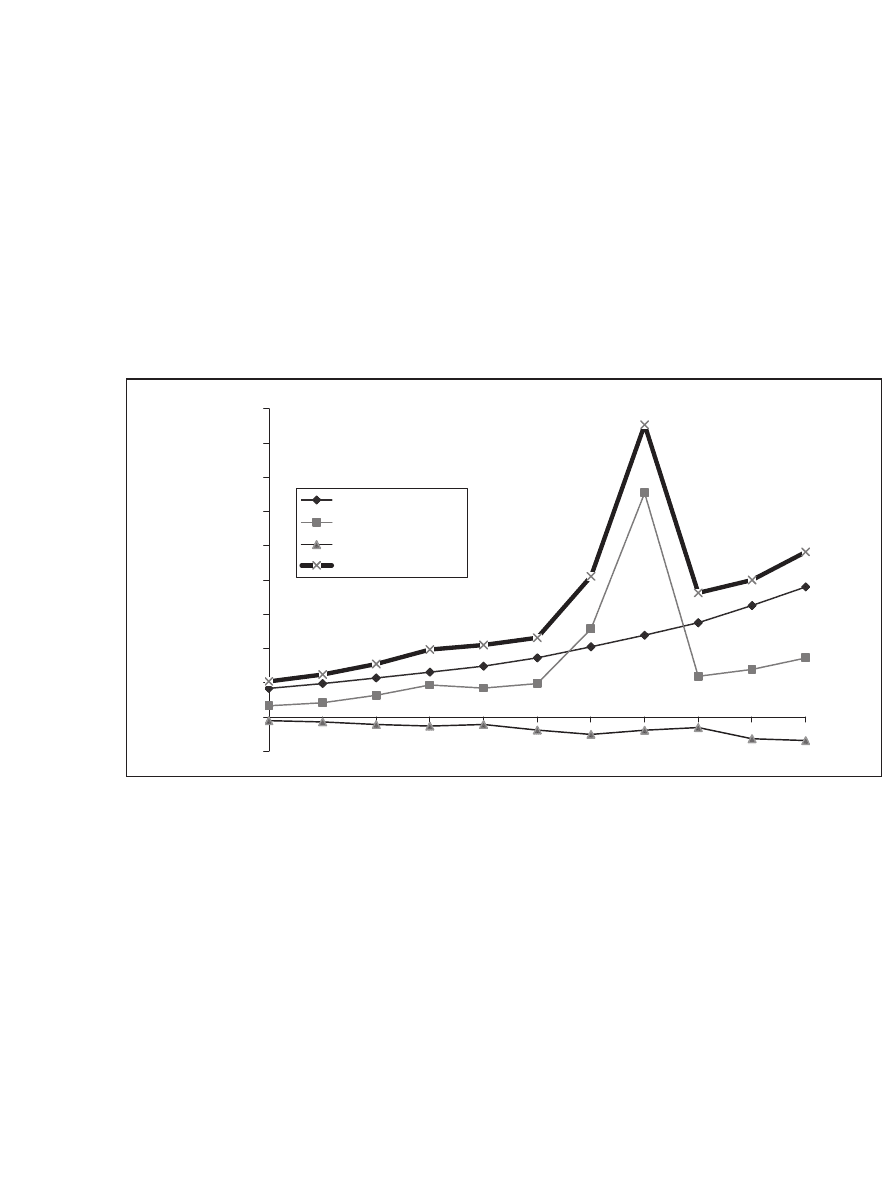

The following graph displays the components of the equity cash fl ows

for JNJ. You can see that the dividends paid out by JNJ are very smooth,

whereas the variabilities of the stock repurchases and stock issuance are

much larger. This is often the case—companies attach great importance

to maintaining a steady, seemingly predictable, dividend, whereas the

true variability of their equity payouts is hidden in other items such as

stock issues and repurchases:

JNJ, CASH FLOW TO EQUITY, 1995–2005

-1,000,000,000

0

1,000,000,000

2,000,000,000

3,000,000,000

4,000,000,000

5,000,000,000

6,000,000,000

7,000,000,000

8,000,000,000

9,000,000,000

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

Total dividends

Stock repurchases

Stock issues

Cash flow to equity

2.3.1 Is JNJ’s r

E

Different When Computed on a Dividend-per-Share Basis

Versus Total Equity Cash Flows?

In this particular case, this cost of equity does not deviate much from the

cost of equity computed on a dividend-per-share basis (though the oppo-

site is often the case):

47 Calculating the Cost of Capital

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

BAC

D

JNJ's stock price, P

0,

31 Dec 2005

61.07

Current dividend

Quarterly 0.33 <-- =B36

Annualized dividend, Div

0

1.32 <-- =B4*4

Dividend growth rate, g

Quarterly Annualized

Growth since 17-Nov-00 3.69% 15.58% <-- =(1+B8)^4-1

Growth since 14-Nov-03 4.06% 17.26% <-- =(1+B9)^4-1

Gordon model cost of equity r

E

Growth since 17-Nov-00 18.08% <-- =B5*(1+C8)/B2+C8

Growth since 14-Nov-03 19.79% <-- =B5*(1+C9)/B2+C9

Date

Dividend per

share

17-Nov-00 0.160

15-Feb-01 0.160

18-May-01 0.180

17-Aug-01 0.180

16-Nov-01 0.180

14-Feb-02 0.180

17-May-02 0.205

16-Aug-02 0.205

15-Nov-02 0.205

13-Feb-03 0.205

16-May-03 0.240

15-Aug-03 0.240

14-Nov-03 0.240

12-Feb-04 0.240

14-May-04 0.285

13-Aug-04 0.285

12-Nov-04 0.285

11-Feb-05 0.285

13-May-05 0.330

19-Aug-05 0.330

18-Nov-05 0.330

COMPUTING JNJ's r

E

BASED ON DIVIDENDS PER SHARE