Simon Benninga. Financial Modelling 3-rd edition

Подождите немного. Документ загружается.

68 Chapter 2

Kraft could use its cash to pay off part of its debt, so that the effective

debt fi nancing of the fi rm is its fi nancial debt minus cash. However, the

implementation of this particular piece of theory is largely a judgment

call—we may not want to attribute all cash to the possibility of paying

off debt, and we may want to compute the fi rm’s cost of borrowing as

opposed to the interest it earns on cash. In the preceding spreadsheet

we illustrated both methods (cells B13 and B19).

2.8.2 Method 2: The Rating-Adjusted Yield on Kraft’s Debt

From Kraft’s fi nancial statements, we learn that in August 2006, Kraft

was rated BBB+ (see box).

Kraft’s Financial Rating

The following is taken from Kraft’s fi nancial statements and shows

that Kraft is rated approximately BBB+:

Credit Ratings. Following a $10.1 billion judgment on March 21,

2003, against Altria Group, Inc.’s domestic tobacco subsidiary,

Philip Morris USA Inc., the three major credit rating agencies took

a series of ratings actions resulting in the lowering of the Company’s

short-term and long-term debt ratings, despite the fact the Company

is neither a party to, nor has exposure to, this litigation. The

Company’s credit ratings by Moody’s at December 31, 2005, were

“P-2” for short-term debt and “A3” for long-term debt, with stable

outlook. The Company’s credit ratings by Standard & Poor’s at

December 31, 2005 were “A-2” for short-term debt and “BBB+”

for long-term debt, with stable outlook. The Company’s credit

ratings by Fitch Rating Services at December 31, 2005 were “F-2”

for short-term debt and “BBB+” for long-term debt, with stable

outlook. As a result of the rating agencies’ actions, borrowing costs

have increased. None of the Company’s debt agreements requires

accelerated repayment in the event of a decrease in credit ratings.

The credit rating downgrades by Moody’s, Standard & Poor’s and

Fitch Rating Services had no impact on any of the Company’s

other existing third-party contracts.

69 Calculating the Cost of Capital

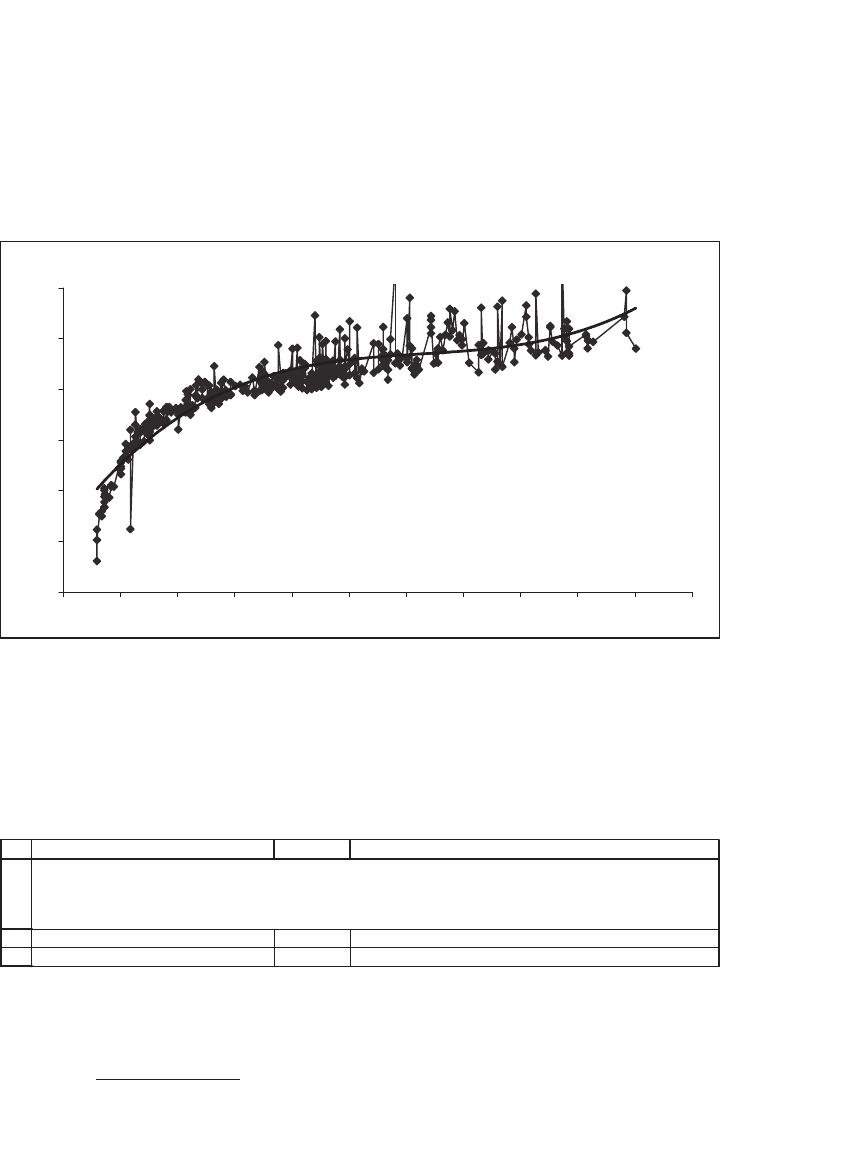

The polynomial regression line describes about 85 percent of the vari-

ability of the yields as a function of the time to maturity.

13

Assuming a

fi ve-year average maturity for Kraft’s debt, the cost of borrowing for

Kraft is 5.31 percent.

We can impute the marginal cost of Kraft’s debt from a yield curve

for the appropriate debt. Following is such a yield curve, compiled from

data available on Yahoo:

BBB Bond Yields, 11Aug06

y = 0.0001x

3

– 0.0023x

2

+ 0.0152x + 0.0221

R

2

= 0.8479

1%

2%

3%

4%

5%

6%

7%

01234567891011

Maturity

Yield

1

2

3

CBA

Average time to maturity (years) 5

Yield 5.31% <-- =0.0001*B2^3-0.0023*B2^2+0.0152*B2+0.0221

COMPUTING KRAFT'S r

D

FROM A YIELD CURVE

YTM=0.0001*time

3

-0.0023*time

2

+0.0152*time+0.0221

13. For more details, see Chapter 27.

70 Chapter 2

2.9 Computing the WACC: Three Cases

In each the next three sections we compute the weighted average cost

of capital for a different company. Each case illustrates some pitfalls of

WACC computations. We make no claims for scientifi c accuracy—instead

we are trying to show you, the fi nancial analyst, that the computation of

a fi rm’s cost of capital requires a considerable number of judgment

calls.

Here are the three cases:

1. Kraft Corporation (section 2.10) illustrates a large divergence between

the Gordon r

E

and the CAPM r

E

. The question ultimately is what share-

holders expect—do they think that the market variability of their stock

investment is indicative of the riskiness of the stock, or did they invest

in Kraft because of its history of payouts to shareholders?

2. Tyson Foods (section 2.11) has not changed its dividend payout per

share for four years. Its equity payouts, however, exhibit considerable

growth but also large variations over time. On a before-tax basis, the

company’s cost of equity r

E

appears to be lower than its cost of debt

r

D

.

3. Cascade Corporation (section 2.12) illustrates a case of negative lever-

age: The company has more cash than it does debt.

2.10 Computing the WACC for Kraft Corporation

In section 2.8 we discussed Kraft’s cost of debt r

D

. In this section we

restrict ourselves to the discussion of the fi rm’s cost of equity r

E

and its

WACC.

2.10.1 Computing the Kraft r

E

Using the Gordon Model

The computation of Kraft’s cost of equity using the Gordon model for

only its per-share dividends gives a very high r

E

, as shown in the following

spreadsheet:

71 Calculating the Cost of Capital

When we examine the cash fl ows to equity holders, the picture becomes

even more complicated. Kraft has paid out hefty amounts to sharehold-

ers over the past four years, but it has fi nanced these payouts at least

partially by a huge stock offering in 2002:

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

CBA

Stock price, end 2005 27.75

Current dividend, D

0

0.92 <-- =B25*4

Gordon cost of equity, r

E

Using growth rate Dec01-Dec05 19.15% <-- =B3*(1+B29)/B2+B29

Using growth rate Dec03-Dec05 16.79% <-- =B3*(1+B32)/B2+B32

Date

Dividends

per share

20-Dec-01 0.130

13-Mar-02 0.130

26-Jun-02 0.130

12-Sep-02 0.150

19-Dec-02 0.150

12-Mar-03 0.150

25-Jun-03 0.150

11-Sep-03 0.180

18-Dec-03 0.180

11-Mar-04 0.180

23-Jun-04 0.180

10-Sep-04 0.205

20-Dec-04 0.205

11-Mar-05 0.205

24-Jun-05 0.205

2-Sep-05 0.230

22-Dec-05 0.230

Quarterly growth, Dec01-Dec05 3.63% <-- =(B25/B9)^(1/16)-1

Annualized 15.33% <-- =(1+B28)^4-1

Quarterly growth, Dec03-Dec05 3.11% <-- =(B25/B17)^(1/8)-1

Annualized 13.04% <-- =(1+B31)^4-1

KRAFT: COST OF EQUITY r

E

BASED ON DIVIDENDS

Computing the growth rate of dividends

72 Chapter 2

Using our formula for a two-stage Gordon model (see Section 2.2) we

arrive at a cost of equity r

E

of 12.64 percent. This formula incorporates

a guesstimate of 10 percent for a high growth rate of equity payouts over

the next three years, followed by a normal growth rate of 6 percent. Were

we to use 20 percent and 6 percent we would get r

E

= 14.46 percent

(not shown).

2.10.2 Kraft’s r

E

Using the CAPM

Kraft has a b equal to 0.47. Using a market price-earnings multiple to

compute E(r

M

) as illustrated on page 65, we compute r

E

= 6.82 percent

using the classic CAPM and 6.05 percent using the tax-adjusted CAPM:

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

FEDCBA

Shares outstanding 1,669,880,755

Share price, end 2005 27.75

Equity value, E 46,339,190,951 <-- =B2*B3

End 2005 total equity payout 2,612,000,000 <-- =E18

High growth rate, g

high

10.00% <-- Guess

Number of high-growth years 3 <-- Guess

Normal growth rate, g

normal

6% <-- Guess

Cost of equity, r

E,

using the

function twostagegordon

12.64% <-- =twostagegordon(B4,B5,B7,B8,B9)

Date

Stock

repurchases

Dividends paid Stock issuance

Cash flow to

e

q

uit

y

holders

31-Dec-01 170,000,000 225,000,000 395,000,000 <-- =B14+C14-D14

31-Dec-02 372,000,000 936,000,000 8,425,000,000 -7,117,000,000 <-- =B15+C15-D15

31-Dec-03 372,000,000 1,089,000,000 1,461,000,000

31-Dec-04 688,000,000 1,280,000,000 1,968,000,000

31-Dec-05 1,175,000,000 1,437,000,000 2,612,000,000

Growth rates

Four year 62.14% 58.97% 60.36% <-- =(E18/E14)^(1/4)-1

Two year 77.72% 14.87% 33.71% <-- =(E18/E16)^(1/2)-1

KRAFT: COST OF EQUITY r

E

BASED ON CASH FLOW TO EQUITY

1

2

3

4

5

6

7

8

9

10

11

12

13

CBA

Market price/earnings multiple, December 2005 18

Equity cash flow payout ratio 50.00%

Anticipated growth of equity cash flow 6.00%

Expected market return, E(r

M

)

8.94% <-- =B3*(1+B4)/B2+B4

Kraft cost of equity calculations

Kraft beta 0.4700 <-- From Yahoo

Kraft tax rate, T

C

29.37% <-- Computed from Kraft financials

Risk free rate, r

f

4.93%

Kraft cost of equity, r

E,Kraft

Classic CAPM 6.82% <-- =B10+B8*(B5-B10)

Tax-adjusted CAPM 6.05% <-- =B10*(1-B9)+B8*(B5-B10*(1-B9))

COMPUTING THE COST OF EQUITY r

E

FOR KRAFT USING THE

MARKET PRICE/EARNINGS MULTIPLE TO COMPUTE E(r

M

)

73 Calculating the Cost of Capital

So what is Kraft’s WACC? Is it in the range of 5–6 percent or in the

range of 12–14 percent? One way to get a feel for the answer to this

question is to look at other companies in the same sector. In section 2.11

we examine the WACC for Tyson’s, another company in the food sector.

All of the estimates for Tyson’s WACC are in the lower range of Kraft’s

estimates. If this is indicative (and we think it is), then we conclude that

Kraft’s WACC is somewhere between 5.64 and 6.26 percent.

2.11 Computing the WACC for Tyson Foods

Tyson Foods (stock symbol TSN) is primarily a producer of meats, but

the company also has a large processed foods segment. Tyson’s dividends

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

BAC

Shares outstanding 1,669,880,755

Share price, end 2005 27.75

Equity value, E 46,339,190,951

Net debt, D 10,884,000,000

WACC based on Gordon per-share dividends and interest from financial statements

Cost of equity, r

E

16.79% <-- ='Page 71'!B6

Cost of debt, r

D

5.50% <-- ='Page 67'!B13

Tax rate, T

C

29.37% <-- ='Kraft 10K, 2005'!B160

WACC 14.33% <-- =$B$4/($B$4+$B$5)*B8+$B$5/($B$4+$B$5)*B9*(1-$B$10)

WACC based on Gordon equity payouts and interest from financial statements

Cost of equity, r

E

14.46% <-- ='Page 72, top'!B11

Cost of debt, r

D

5.50% <-- ='Page 67'!B13

Tax rate, T

C

29.37% <-- ='Kraft 10K, 2005'!B160

WACC 12.45% <-- =$B$4/($B$4+$B$5)*B14+$B$5/($B$4+$B$5)*B15*(1-$B$10)

WACC based on classic CAPM and interest from financial statements

Cost of equity, r

E

6.82% <-- ='Page 72, bottom'!B12

Cost of debt, r

D

5.50% <-- ='Page 67'!B13

Tax rate, T

C

29.37% <-- ='Kraft 10K, 2005'!B160

WACC 6.26% <-- =$B$4/($B$4+$B$5)*B20+$B$5/($B$4+$B$5)*B21*(1-$B$10)

WACC based on tax-adjusted CAPM and interest from financial statements

Cost of equity, r

E

6.05% <-- ='Page 72, bottom'!B13

Cost of debt, r

D

5.50% <-- ='Page 67'!B13

Tax rate, T

C

29.37% <-- ='Kraft 10K, 2005'!B160

WACC 5.64% <-- =$B$4/($B$4+$B$5)*B26+$B$5/($B$4+$B$5)*B27*(1-$B$10)

COMPUTING THE WACC FOR KRAFT

2.10.3 So What Is Kraft’s WACC?

The preceding analysis produces four estimates for the WACC of Kraft—

the Gordon estimates are high and the CAPM estimates are low:

74 Chapter 2

per share have stood still for the past four years, though its cash fl ows to

equity show some growth over this same period. As we will see, the cor-

respondence between the Gordon estimate for the company’s cost of

equity r

E

and the CAPM estimates are much closer for Tyson than for

Kraft.

2.11.1 Computing Tyson’s r

E

Using the Gordon Model

Tyson hasn’t changed its per-share dividend in fi ve years. This fact makes

the computation of the cost of equity r

E

using the dividend model very

simple:

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

ABC

Stock price, 11Aug06 13.45

Current dividend, D

0

0.16 <-- =B25*4

Dividend growth rate 0%

Gordon cost of equity, r

E

1.19% <-- =B3*(1+B4)/B2+B4

Date

Dividends

per share

29-Aug-01 0.04

28-Nov-01 0.04

27-Feb-02 0.04

29-May-02 0.04

28-Aug-02 0.04

26-Nov-02 0.04

26-Feb-03 0.04

28-May-03 0.04

27-Aug-03 0.04

26-Nov-03 0.04

26-Feb-04 0.04

27-May-04 0.04

30-Aug-04 0.04

29-Nov-04 0.04

25-Feb-05 0.04

30-Aug-05 0.04

27-Feb-06 0.04

30-May-06 0.04

TYSON: COST OF EQUITY r

E

BASED

ON DIVIDENDS

75 Calculating the Cost of Capital

When we examine the cash fl ows to equity holders, the picture becomes

somewhat more interesting. Tyson’s annual cash fl ows to equity are

shown in the following spreadsheet; these show a more variable payout

pattern than the per-share dividends:

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

EDCBA F

Shares outstanding 354,820,000

Share price, 11Aug06 13.45

Equity value, E 4,772,329,000 <-- =B2*B3

Current (Aug06) total equity payout 81,631,562 <-- =E18*(1+B7)^0.75

High growth rate, g

high

10.00% <-- Guess

Number of high-growth years 3 <-- Guess

Normal growth rate, g

normal

2% <-- Guess

Cost of equity, r

E,

using the function

twostagegordon

4.18% <-- =twostagegordon(B4,B5,B7,B8,B9)

Date

Stock

re

purchases

Dividends paid Stock issuance

Cash flow to

equity holders

2001 48,000,000 35,000,000 34,000,000 49,000,000 <-- =B14+C14-D14

2002 19,000,000 58,000,000 0 77,000,000 <-- =B15+C15-D15

2003 41,000,000 54,000,000 0 95,000,000

2004 72,000,000 55,000,000 43,000,000 84,000,000

2005 45,000,000 55,000,000 24,000,000 76,000,000

Growth rates

Four year -1.60% 11.96% 11.60% <-- =(E18/E14)^(1/4)-1

Two year 4.76% 0.92% -10.56% <-- =(E18/E16)^(1/2)-1

TYSON: COST OF EQUITY r

E

BASED ON CASH FLOW TO EQUITY

In cell B5 we assume that the August 2006 equity payout is the payout

for the fi nancial year ending October 2005 multiplied by the high growth

rate to the power 0.75. Using the two-stage Gordon model, we arrive at

a cost of equity r

E

= 4.18 percent. This formula incorporates a guesstimate

of 10 percent for a high growth rate of equity payouts over the next three

years, followed by a normal growth rate of 2 percent. Were we to use

10 percent and 5 percent, we would get r

E

= 7.06 percent.

2.11.2 Tyson’s r

E

Using the CAPM

Tyson has a b = 0.20. Using a market price-earnings multiple to compute

E(r

M

) as illustrated on page 65, we compute r

E

= 5.77 percent using the

classic CAPM and 4.60 percent using the tax-adjusted CAPM:

76 Chapter 2

2.11.3 Method 1: Tyson’s Cost of Debt r

D

The average cost of Tyson’s debt in 2005 can be calculated from the

fi nancial statements as 7.22 percent:

1

2

3

4

5

6

7

8

9

10

11

12

13

CBA

Market price/earnings multiple, August 2006 17

Equity cash flow payout ratio 50.00%

Anticipated growth of equity cash flow 6.00%

Expected market return, E(r

M

)

9.12% <-- =B3*(1+B4)/B2+B4

Tyson cost of equity calculations

Tyson beta 0.20 <-- From Yahoo

Tyson tax rate, T

C

29.55% <-- Computed from Tyson financials

Risk free rate, r

f

4.93%

Tyson cost of equity, r

E,Kraft

Classic CAPM 5.77% <-- =B10+B8*(B5-B10)

Tax-adjusted CAPM 4.60% <-- =B10*(1-B9)+B8*(B5-B10*(1-B9))

COMPUTING THE COST OF EQUITY r

E

FOR TYSON USING THE

MARKET PRICE/EARNINGS MULTIPLE TO COMPUTE E(r

M

)

1

2

3

4

5

6

7

8

9

10

CBA

D

2005 2004

Cash and cash equivalents 40,000,000 33,000,000

Current debt 126,000,000 338,000,000

Long term debt 2,869,000,000 3,024,000,000

Net debt 2,955,000,000 3,329,000,000 <-- =C5+C4-C3

Interest paid 227,000,000

Interest cost 7.22% <-- =B8/AVERAGE(B6:C6)

COMPUTING THE COST OF DEBT FOR TYSON

2.11.4 Method 2: The Rating-Adjusted Yield on Tyson’s Debt

In August 2006, Tyson was rated BBB. As we did for Kraft, we can impute

a cost of debt for Tyson based on the yield curve of r

D

= 5.31 percent.

2.11.5 Tyson’s WACC

The preceding analysis produces four estimates for the WACC of Tyson.

We have used the company’s historical cost of debt (r

D

= 7.22%) instead

of its rating-adjusted yield, our excuse being that we think the BBB

rating understates the company’s risk.

77 Calculating the Cost of Capital

With the exception of the very low WACC produced by the dividend

r

E

, all the estimates are within the same range. We would feel comfortable

declaring that Tyson’s WACC is somewhere between 5 and 6 percent. If

pressed to come up with a point estimate of the WACC, we would use

the average of the three estimates, 4.94 percent (cell B31).

2.12 Computing the WACC for Cascade Corporation

Cascade Corporation (stock symbol CAE) makes materials-handling

equipment—forks for forklifts, side shifters, paper-roll clamps, rotators,

multiple-load handlers, carton clamps, and other technical equipment.

The company has annual sales of around $500 million and is listed on

the New York Stock Exchange.

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

BAC

Shares outstanding 354,820,000

Share price, end 2005 13.45

Equity value, E 4,772,329,000

Net debt, D 2,955,000,000

WACC based on Gordon per-share dividends and interest from financial statements

Cost of equity, r

E

1.19% <-- ='Page 74'!B5

Cost of debt, r

D

7.22% <-- ='Page 76, bottom'!B10

Tax rate, T

C

29.55% <-- ='Tyson income statement'!B31

WACC 2.68% <-- =$B$4/($B$4+$B$5)*B8+$B$5/($B$4+$B$5)*B9*(1-$B$10)

WACC based on Gordon equity payouts and interest from financial statements

Cost of equity, r

E

4.18% <-- ='Page 75'!B11

Cost of debt, r

D

7.22% <-- ='Page 76, bottom'!B10

Tax rate, T

C

29.55% <-- ='Tyson income statement'!B31

WACC 4.53% <-- =$B$4/($B$4+$B$5)*B14+$B$5/($B$4+$B$5)*B15*(1-$B$10)

WACC based on classic CAPM and interest from financial statements

Cost of equity, r

E

5.77% <-- ='Page 76, top'!B12

Cost of debt, r

D

7.22% <-- ='Page 76, bottom'!B10

Tax rate, T

C

29.55% <-- ='Tyson income statement'!B31

WACC 5.51% <-- =$B$4/($B$4+$B$5)*B20+$B$5/($B$4+$B$5)*B21*(1-$B$10)

WACC based on tax-adjusted CAPM and interest from financial statements

Cost of equity, r

E

4.60% <-- ='Page 76, top'!B13

Cost of debt, r

D

7.22% <-- ='Page 76, bottom'!B10

Tax rate, T

C

29.55% <-- ='Tyson income statement'!B31

WACC 4.79% <-- =$B$4/($B$4+$B$5)*B26+$B$5/($B$4+$B$5)*B27*(1-$B$10)

Estimated WACC?

4.94% <-- =AVERAGE(B29,B23,B17)

COMPUTING THE WACC FOR TYSON