Simon Benninga. Financial Modelling 3-rd edition

Подождите немного. Документ загружается.

58 Chapter 2

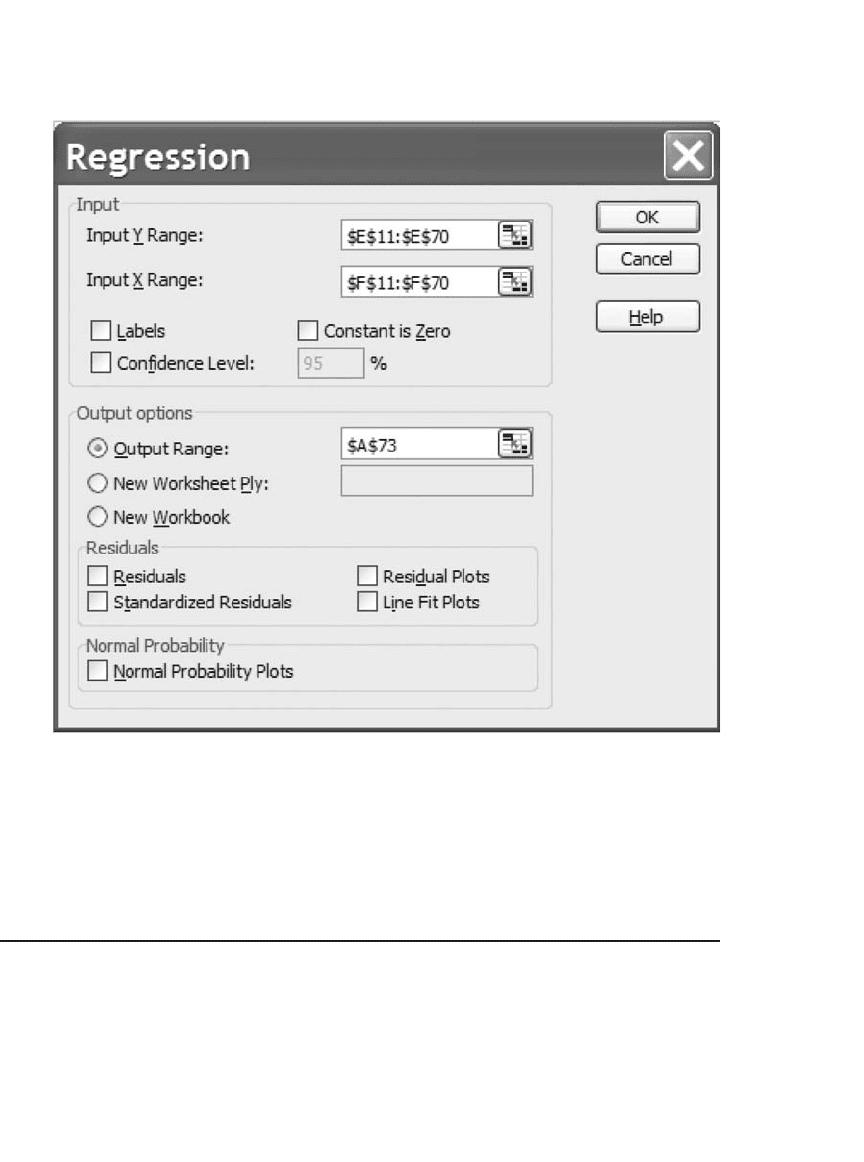

Rows 73–90 were produced from Tools|Data Analysis|Regression

using the following values:

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

65

66

67

68

69

70

71

72

73

74

75

76

77

78

79

80

81

82

83

84

85

86

87

88

89

90

ABCDEFGHI

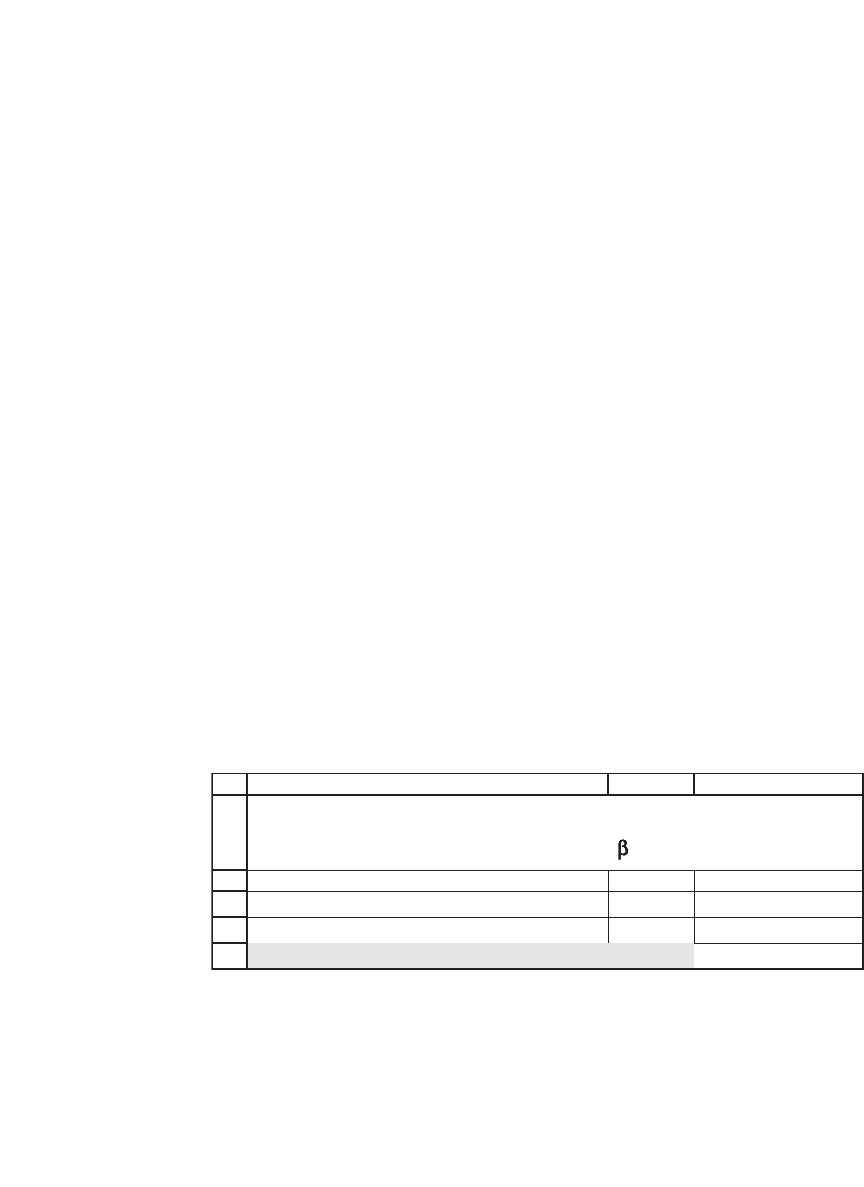

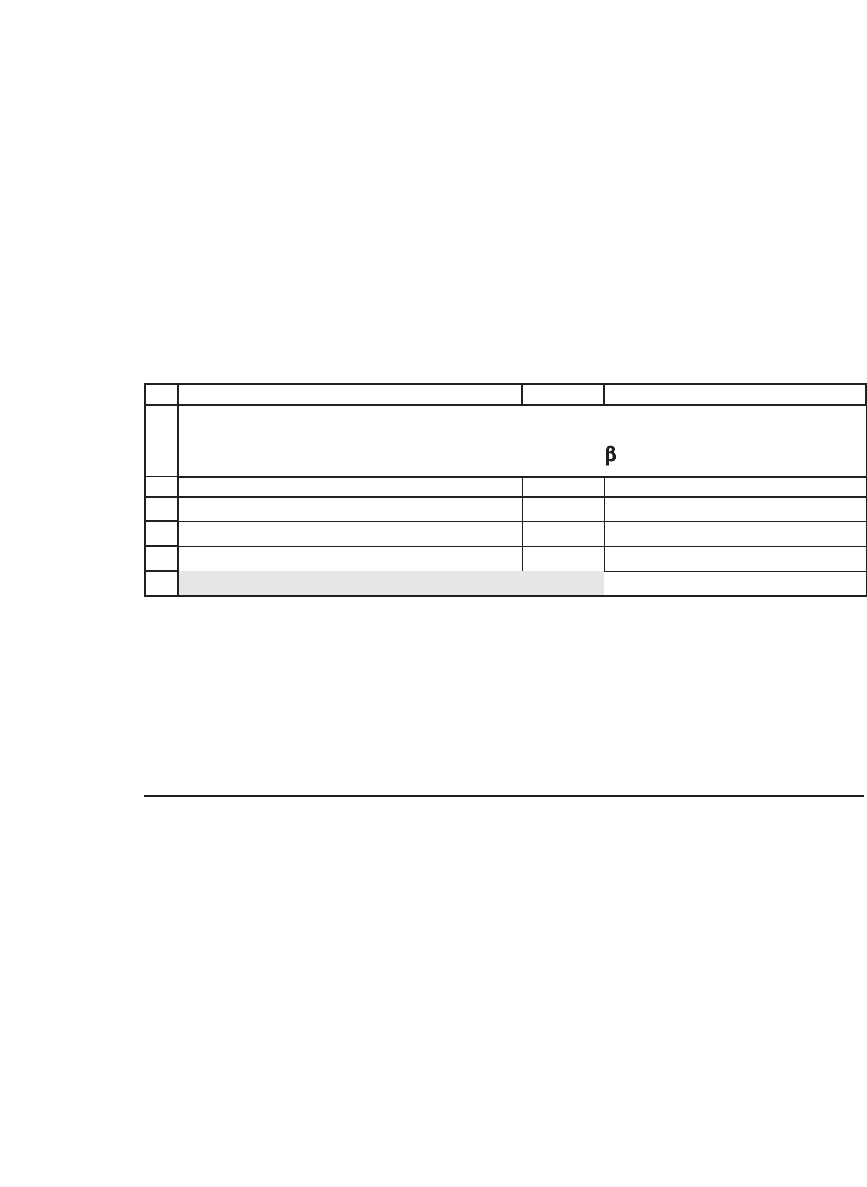

Alpha -0.0029 <-- =INTERCEPT(E11:E70,F11:F70)

Beta 2.2516 <-- =SLOPE(E11:E70,F11:F70)

R-squared 0.5304 <-- =RSQ(E11:E70,F11:F70)

t for alpha -0.243762 <-- =tintercept(E11:E70,F11:F70)

t for beta 8.094164 <-- =tslope(E11:E70,F11:F70)

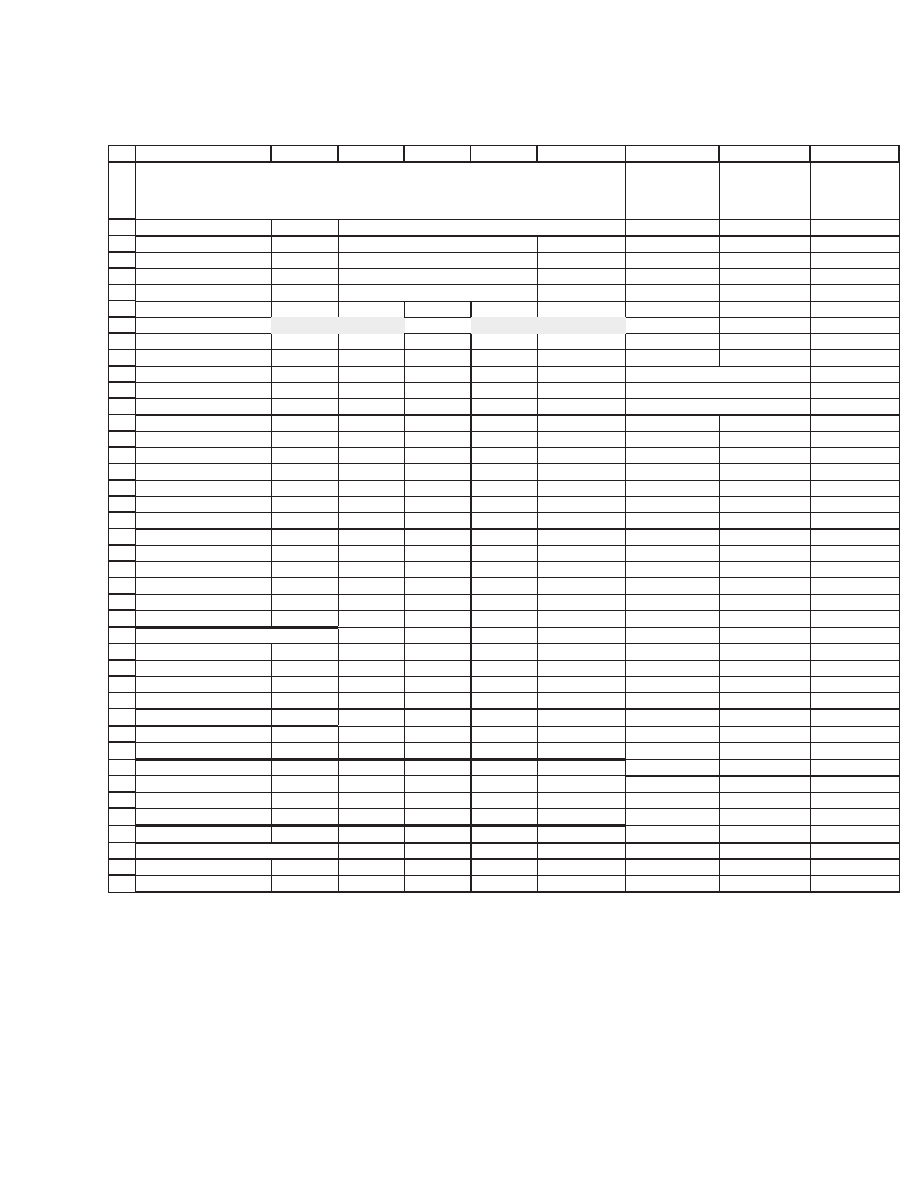

Date Intel SP500 Intel SP500

9-Jan-01 35.38 1366.01

1-Feb-01 27.32 1239.94 -0.2585 -0.0968 <-- =LN(C11/C10)

1-Mar-01 25.17 1160.33 -0.0820 -0.0664 <-- =LN(C12/C11)

2-Apr-01 29.57 1249.46 0.1611 0.0740 <-- =LN(C13/C12)

1-May-01 25.86 1255.82 -0.1341 0.0051

1-Jun-01 28 1224.38 0.0795 -0.0254

2-Jul-01 28.54 1211.23 0.0191 -0.0108

1-Aug-05 25.24 1220.33 -0.0506 -0.0113

1-Sep-05 24.19 1228.81 -0.0425 0.0069

3-Oct-05 23.06 1207.01 -0.0478 -0.0179

1-Nov-05 26.27 1249.48 0.1303 0.0346

1-Dec-05 24.57 1248.29 -0.0669 -0.0010

3-Jan-06 25.9 1285.45 0.0527 0.0293

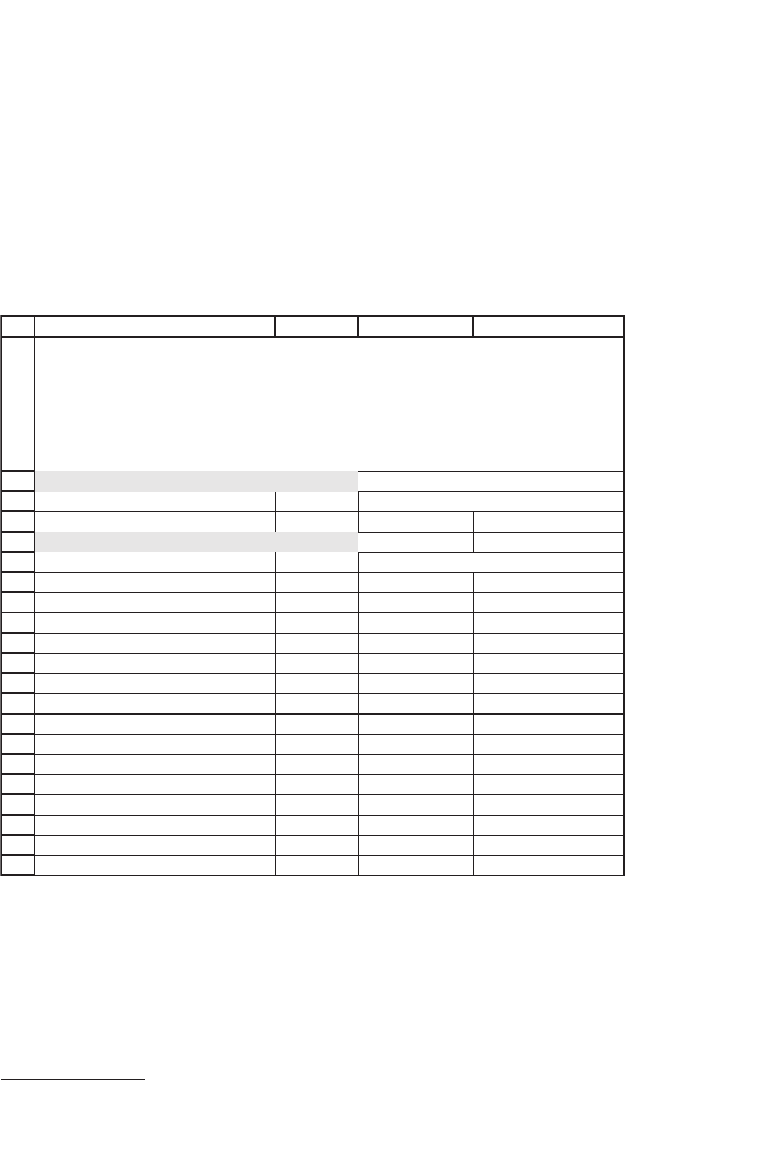

SUMMARY OUTPUT

Regression Statistics

Multiple R 0.728302

R Square 0.530423

Adjusted R Square 0.522327

Standard Error 0.092677

Observations 60

ANOV

A

df SS MS F Significance F

Regression 1 0.5627 0.5627 65.5155 0.0000

Residual 58 0.4982 0.0086

Total 59 1.0609

Coefficient

s

t

andard Err

o

t Stat P-value Lower 95% Upper 95% Lower 95.0% Upper 95.0%

Intercept -0.0029 0.0120 -0.2438 0.8083 -0.0269 0.0210 -0.0269 0.0210

X Variable 1 2.2516 0.2782 8.0942 0.0000 1.6948 2.8084 1.6948 2.8084

COMPUTING BETA FOR INTEL

Monthly returns for Intel and SP500, 2001-2006

Prices Returns

59 Calculating the Cost of Capital

While Tools|Data Analysis|Regression produces a lot of data, it has

one major drawback: The output is not automatically updated when the

underlying data changes. For this reason we prefer to use the other

methods illustrated.

2.6 Using the Security Market Line to Calculate Intel’s Cost of Equity

In the capital asset pricing model, the security market line (SML) is used

to calculate the risk-adjusted cost of capital. In this section we consider

two SML formulations. The difference between these two methods has

60 Chapter 2

to do with the way taxes are incorporated into the cost-of-capital

equation.

2.6.1 Method 1: The Classic Security Market Line

The classic CAPM formula uses an SML equation that ignores taxes:

Cost of equity, rr Er r

Ef M f

=+ −

β

[( ) ]

Here r

f

is the risk-free rate of return in the economy, and E(R

M

) is the

expected rate of return on the market. The choice of values for the SML

parameters is often problematic. A common approach is to choose

•

r

f

equal to the risk-free interest rate in the economy (for example, the

yield on Treasury bills).

•

E(r

M

) equal to the historic average of the market return, defi ned as the

average return of a broad-based market portfolio. There is an alternative

approach based on market multiples; both of these are discussed in

section 2.7.

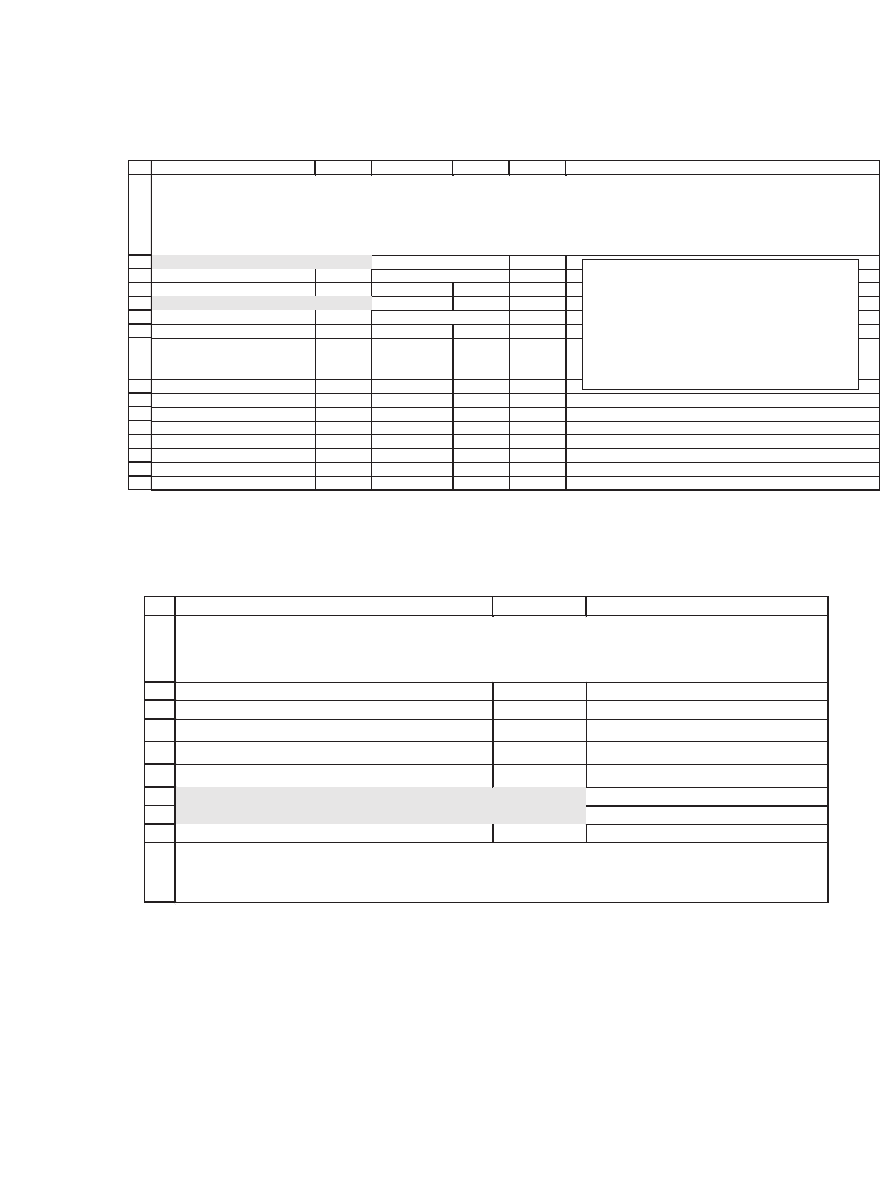

The following spreadsheet fragment illustrates the classic CAPM cost

of equity:

1

2

3

4

5

BA

C

Intel beta 2.2516

Risk free rate, r

f

4.93%

Expected market return, E(r

M

)

9.88%

Intel cost of equity, r

E,Intel

16.31% <-- =B3+B2*(B4-B3)

COMPUTING THE COST OF EQUITY FOR INTEL

C

lassic CAPM: r

E

= r

f

+ *[ E(r

M

)-r

f

]

The computation of E(r

M

) is discussed in section 2.7. The risk-free rate

r

f

is computed from Yahoo data—we take the yield on the short-term

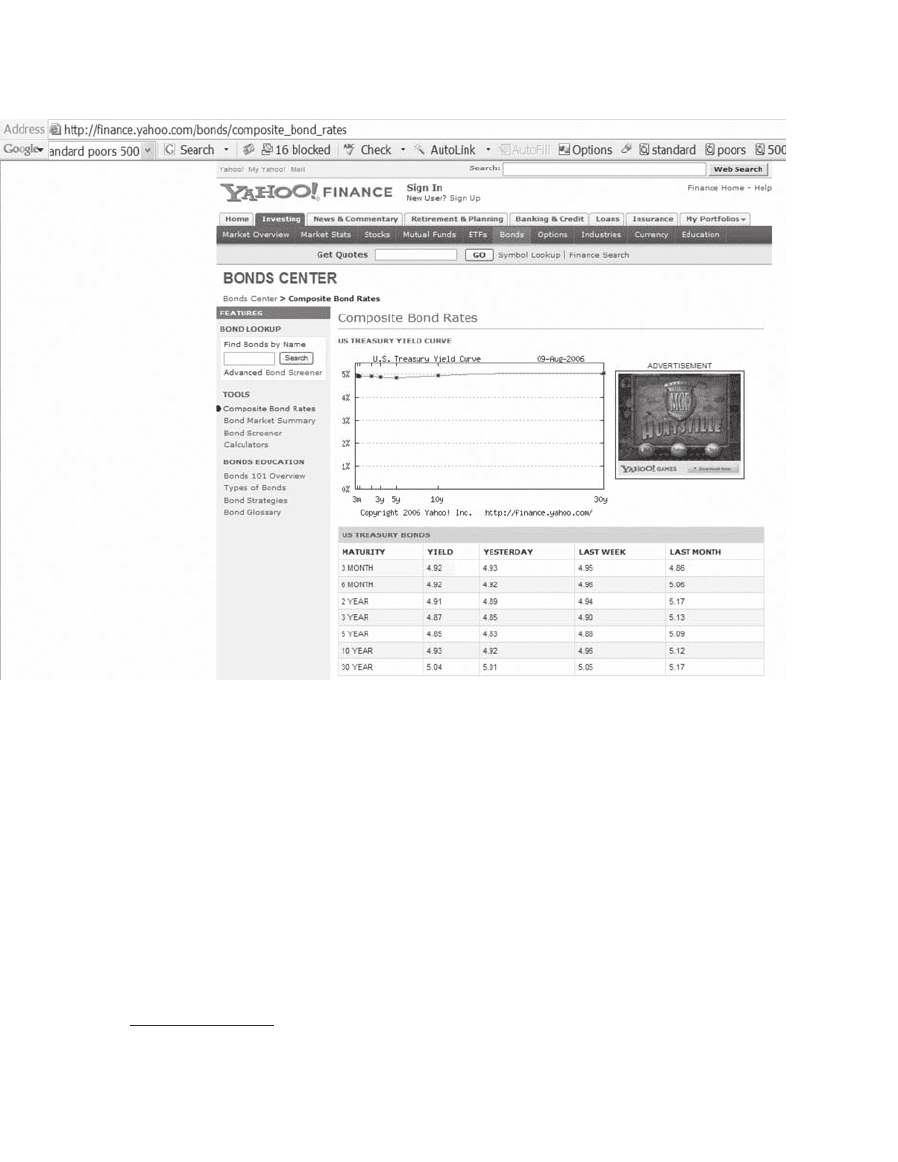

Treasury bills as a proxy for the market risk-free rate:

61 Calculating the Cost of Capital

2.6.2 Method 2: The Tax-Adjusted Security Market Line

The classic CAPM approach makes no allowance for taxation. Benninga

and Sarig (1997) show that the SML has to be adjusted for the marginal

corporate tax rate in the economy.

9

Denoting the corporate tax rate by

T

C

, the tax-adjusted SML is

Cost of equity =−+ −−rT ErrT

fC MfC

()[()()]11

β

This formula can be applied by substituting r

f

(1 − T

C

) for r

f

in the classic

CAPM. Note that the tax-adjusted cost of equity has a lower intercept

and a higher slope than the classic CAPM.

9.

The logic of the Benninga-Sarig approach is outlined in our book Corporate Finance:

A Valuation Approach (McGraw-Hill, 1997). A more formal derivation of the model is

given in “Risk, Returns and Values in the Presence of Differential Taxation,” co-

authored with Oded Sarig. Journal of Banking and Finance 27.

62 Chapter 2

•

The intercept is r

f

(1 − T

C

) instead of r

f

.

•

The slope is E(r

M

) − r

f

(1 − T

C

) instead of E(r

M

) − r

f

. Note that the slope

can be written as the classic CAPM slope plus T

C

r

f

:

Er r T Er r Tr

Mf C Mf Cf

() ( )[() ]−−= −+1

For Intel, the tax-adjusted approach gives a somewhat higher cost of

equity:

1

2

3

4

5

6

CBA

Intel beta 2.2516

Intel tax rate, T

C

31.29% <-- Computed from Intel financials

Risk free rate, r

f

4.93%

Expected market return, E(r

M

)

9.88%

Intel cost of equity, r

E,Intel

18.00% <-- =B4*(1-B3)+B2*(B5-B4*(1-B3))

COMPUTING THE COST OF EQUITY FOR INTEL

Tax-adjusted CAPM: r

E

= r

f

(1-T

C

)+ *[ E(r

M

)-r

f

(1-T

C

)]

Although the tax-adjusted CAPM is more consistent with an economy

with taxation, we confess that—given the uncertainties surrounding cost-

of-capital computations—the difference between the classic CAPM and

the tax-adjusted CAPM may not be worth the trouble.

2.7 Three Approaches to Computing the Expected Return on the Market E(r

M

)

A critical computation for the CAPM cost of equity is the expected

return on the market E(r

M

). There are three major approaches to com-

puting this number:

1. The historical return on a major market index

2. The historical market risk premium

3. The Gordon model

All three approaches are illustrated in this section, and their effect on

computing the Intel cost of equity is illustrated at the end of this

section.

63 Calculating the Cost of Capital

2.7.2 Computing the Market Risk Premium E(r

M

) − r

f

Directly

We can also compute the market risk premium directly. This procedure

requires a bit more work: In the following spreadsheet we add to the

preceding Vanguard data, data from the St. Louis Federal Reserve Bank

on three-month Treasury bill rates.

2.7.1 E(r

M

) as the Historical Average Return on a Market Portfolio

A simple approach to computing E(r

M

) is to take it as the average of the

historical returns of a major market index. In the following computation

we illustrate this approach by using Vanguard’s 500 Index Fund as a

proxy for the market.

10

The annualized return on this fund since 1987 is

9.98 percent:

10. The Vanguard fund’s prices incorporate dividends on the S&P 500.

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

ABCD

Average monthly return 0.83% <-- =AVERAGE(C10:C241)

Monthly standard deviation 4.34% <-- =STDEVP(C10:C241)

Annualized return 9.98% <-- =12*B2

Annualized standard deviation 15.05% <-- =SQRT(12)*B3

Date Price Return

1-Apr-87 17.32

1-May-87 17.49 0.98% <-- =LN(B10/B9)

1-Jun-87 18.37 4.91% <-- =LN(B11/B10)

1-Jul-87 19.28 4.83% <-- =LN(B12/B11)

3-Aug-87 20.02 3.77% <-- =LN(B13/B12)

1-Sep-87 19.56 -2.32%

1-Oct-87 15.31 -24.50%

2-Nov-87 14.06 -8.52%

1-Dec-87 15.12 7.27%

4-Jan-88 15.75 4.08%

1-Feb-88 16.48 4.53%

1-Mar-88 15.98 -3.08%

4-Apr-88 16.14 1.00%

MEASURING E(r

M

) USING HISTORICAL DATA

D

erived from prices for the Vanguard 500 Index Fund

(symbol: VFINX)

These prices include dividends; April 1987–August 2006

64 Chapter 2

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

ABCDE F

Average monthly risk premium 0.46% <-- =AVERAGE(E10:E241)

Monthly standard deviation 4.34% <-- =STDEVP(E10:E241)

Annualized risk premium 5.50% <-- =12*B2

Annualized standard deviation 15.04% <-- =SQRT(12)*B3

Date Price Return

Treasury

bill rate

Market

risk

premium

1-Apr-87 17.32

1-May-87 17.49 0.98% 0.47% 0.51% <-- =C10-D10

1-Jun-87 18.37 4.91% 0.47% 4.44% <-- =C11-D11

1-Jul-87 19.28 4.83% 0.47% 4.36%

3-Aug-87 20.02 3.77% 0.47% 3.29%

1-Sep-87 19.56 -2.32% 0.50% -2.83%

1-Oct-87 15.31 -24.50% 0.53% -25.03%

2-Nov-87 14.06 -8.52% 0.51% -9.03%

MEASURING THE MARKET RISK PREMIUM E(r

M

) - r

f

USING HISTORICAL DATA

Vanguard 500 Index Fund (symbol: VFINX) minus Treasury Bills

April 1987 - August 2006

All measurements relate to monthly returns on SP500, r

Mt

, and the Treasury bill rate r

ft

Methodological note: I have used the St. Louis FRED

data for 3-month Treasury bills; this data is

annualized, and I have divided it by 12 to get the

monthly returns. Since the data can be taken as an

ex ante return, the April 1987 rate is attributed to May

1987.

I've use 3-month instead of 1-month because there

are lots of data problems with the latter.

Applying the risk premium directly to the computation of Intel’s cost

of equity gives the following:

1

2

3

4

5

6

7

8

9

10

CBA

Intel beta 2.2516

Historical market risk premium 5.50%

Intel tax rate, T

C

31.29% <-- Computed from Intel financials

Risk free rate, r

f

4.93%

Intel cost of equity, r

E,Intel

Classic CAPM 17.31% <-- =B5+B2*B3

Tax-adjusted CAPM 19.24% <-- =B5*(1-B4)+B2*(B3+B4*B5)

COMPUTING THE COST OF EQUITY FOR INTEL USING THE

MARKET RISK PREMIUM E(r

M

) - r

f

Note

: The tax-adjusted model in cell B8 uses the equivalence

E(r

M

) - r

f

(1-T

C

) = E(r

M

) - r

f

+ T

C

*r

f

2.7.3 Calculating the Expected Return on the Market E(r

M

) Using the Gordon

Model

The 9.98 percent return for E(r

M

) approximates the historic market

return in the United States for 1987–2006. Historic averages are appro-

priate if we think that the future anticipated rates of return will corre-

spond to the historic average. However, we may want to take current

market data to calculate directly the future anticipated market yield.

65 Calculating the Cost of Capital

As Benninga and Sarig show, the Gordon model gives us an approach

for doing so.

11

Recall that the model says that the cost of equity r

E

is

given by

r

g

P

g

E

=

+

()

+

Div

0

1

0

This formula also applies to the market portfolio, so that we can write

r

g

P

g

M

=

+

()

+

Div

0

1

0

interpreting Div

0

, P

0

, and g to be the current dividend, price, and growth

rate of the market portfolio. Rewriting this formula, assuming that the

fi rm pays out a constant proportion a of its earnings as dividends, indicat-

ing by EPS

0

the current earnings per share, and interpreting g to be the

earnings growth of the fi rm, gives us

Er

aEPS g

P

g

ag

PEPS

g

M

()

()

/

=

∗+

()

+=

∗+

+

0

000

1

1

The term on the right-hand side of this equation, P

0

/EPS

0

, is the price-

earnings ratio of the market. We can use this formula to compute E(r

M

)

and thus tie the cost of equity to currently observable market parameters.

Here is an implementation:

11. A fuller exposition of this model can be found in Chapter 9 of Benninga and Sarig

(1997).

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

CBA

Market price/earnings multiple, August 2006 17

Equity cash flow payout ratio 50.00%

Anticipated growth of market equity cash flow 6.00%

Expected market return, E(r

M

)

9.12% <-- =B3*(1+B4)/B2+B4

Intel cost of equity calculations

Intel beta 2.2516

Intel tax rate, T

C

31.29% <-- Computed from Intel financials

Risk free rate, r

f

4.93%

Intel cost of equity, r

E,Intel

Classic CAPM 14.36% <-- =B10+B8*(B5-B10)

Tax-adjusted CAPM 16.29% <-- =B10*(1-B9)+B8*(B5-B10*(1-B9))

COMPUTING THE COST OF EQUITY FOR INTEL USING THE MARKET

PRICE/EARNINGS MULTIPLE TO COMPUTE E(r

M

)

Note

: Price/Earnings ratio for S&P 500 from http://www.bullandbearwise.com

66 Chapter 2

2.8 Calculating the Cost of Debt

Thus far in this chapter we have shown several methods for computing

the cost of equity r

E

. We now turn to calculating the cost of debt r

D

. In

principle, r

D

is the marginal cost to the fi rm (before corporate taxes) of

borrowing an additional dollar. In practice the cost of debt often turns

out to be more diffi cult to calculate than the cost of equity. There are at

least three ways of calculating the fi rm’s cost of debt. We will state them

briefl y and then go on to illustrate the application of two of the methods

that, although they may not be theoretically perfect, are often used in

practice:

•

As a practical matter, the cost of debt can often be approximated by

taking the average cost of the fi rm’s existing debt. The problem with this

method is that it runs the danger of confusing the past costs with the

future anticipated cost of debt that we actually want to measure.

•

We can use the yield of similar-risk, newly issued corporate securities.

If a company is rated A and has mostly medium-term debt, then we can

use the average yield on medium-term, A-rated debt as the fi rm’s cost

of debt. Note that this method is somewhat problematic because the

yield on a bond is its promised return, whereas the cost of debt is the

expected return on a fi rm’s debt. Since there is usually a risk of default,

the promised return is generally higher than the expected return.

•

We can use a model that estimates the cost of debt from data about

the fi rm’s bond prices, the estimated probabilities of default, and the

estimated payoffs to bondholders in case of default. This method requires

a lot of work and is mathematically nontrivial; we postpone its discussion

until Chapter 28. For cost of capital calculations it would be used in

practice only if the fi rm we are analyzing has signifi cant amounts of risky

debt.

The fi rst two methods are relatively easy to apply, and in many cases

the problems or errors that are encountered in these methods are not

critical.

12

As a matter of theory, however, both these methods fail to make

12. It bears repeating that calculating the cost of capital requires a large number of

assumptions and does not necessarily give a precise answer. Thus cost of capital esti-

mation is part science and part art. Users of cost of capital estimates should always

do a sensitivity analysis around the numbers calculated. Given the data on the

company you are analyzing, some sloppiness in the cost of capital calculations (with

its accompanying savings in time) may be expedient.

67 Calculating the Cost of Capital

Several aspects of our calculations are worth noting:

•

When calculating the cost of debt r

D

from the fi nancial statements, it

is important to include all fi nancial debt, without distinguishing between

short-term and long-term items. In Kraft’s case we have identifi ed four

such items (rows 5–8). When—in the next chapter—we treat the case of

corporate valuation, we will see that the nonfi nancial items of the fi rm’s

short-term assets and short-term liabilities are included in the free cash

fl ows that are discounted to arrive at the corporate value.

•

In principle, liquid assets such as cash and cash equivalents are negative

debt and should be subtracted from the fi rm’s debt. The idea here is that

proper risk adjustments for the cost of the fi rm’s debt. The third method,

which involves computing the expected return on a fi rm’s debt, is more

in line with standard fi nancial theory, but it is also more diffi cult to apply.

It may not, therefore, be worth the effort. In the remainder of this section,

we apply the fi rst two of these methods to calculate the cost of debt for

Kraft.

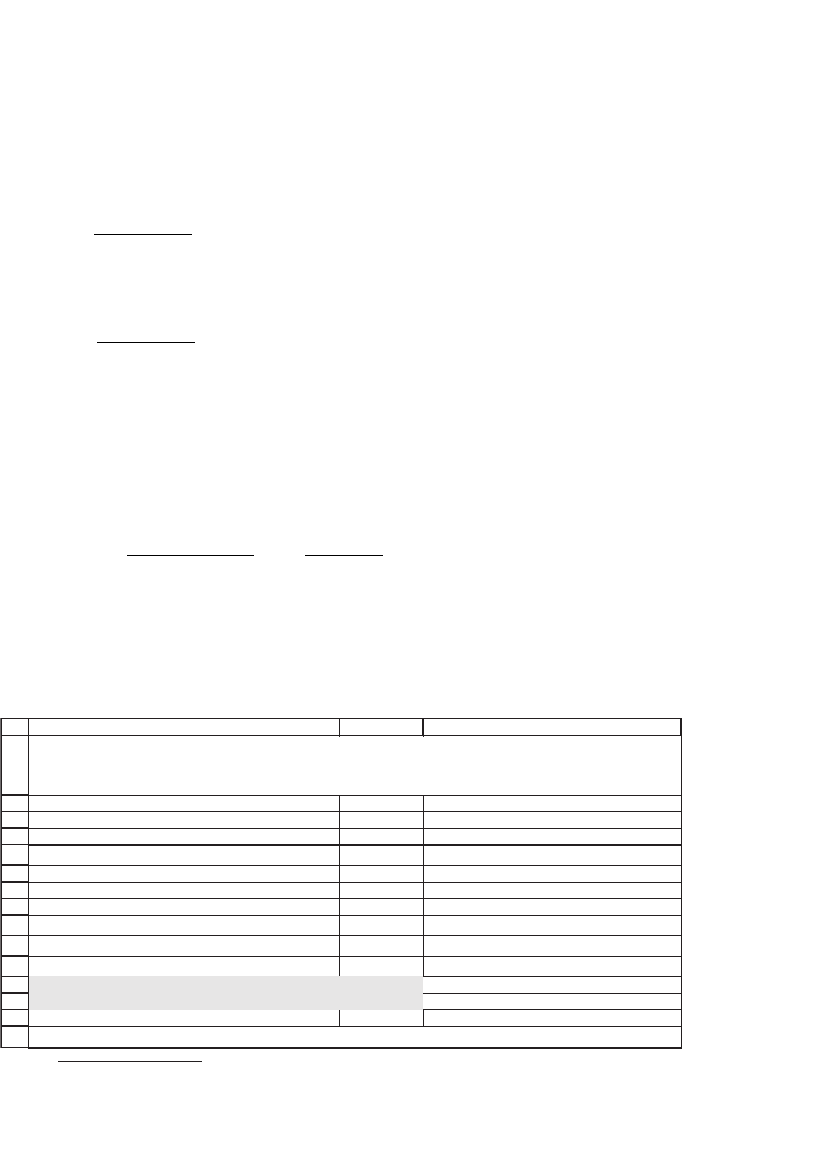

2.8.1 Method 1: Kraft’s Average Cost of Debt

The average cost of Kraft’s debt in 1998 can be calculated from the

fi nancial statements as somewhere between 5.50 and 5.73 percent:

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

DCBA

2005/12/31 2004/12/31

Cash and cash equivalents 316,000,000 282,000,000

Short-term borrowings 805,000,000 1,818,000,000

Current portion of long-term debt 1,268,000,000 750,000,000

Due to Altria Group, Inc., and affiliates 652,000,000 227,000,000

Long-term debt 8,475,000,000 9,723,000,000

Interest and other debt expense, net 636,000,000 666,000,000

Net debt 10,884,000,000 12,236,000,000 <-- =SUM(C5:C8)-C3

Net interest cost 5.50% <-- =B10/AVERAGE(B12:C12)

Total debt 11,200,000,000 12,518,000,000

Cash paid:

Interest 679,000,000 633,000,000

Interest cost 5.73% <-- =B17/AVERAGE(B15:C15)

COMPUTING THE COST OF DEBT FOR KRAFT