Simon Benninga. Financial Modelling 3-rd edition

Подождите немного. Документ загружается.

28 Chapter 1

1

2

3

4

5

6

7

8

9

10

11

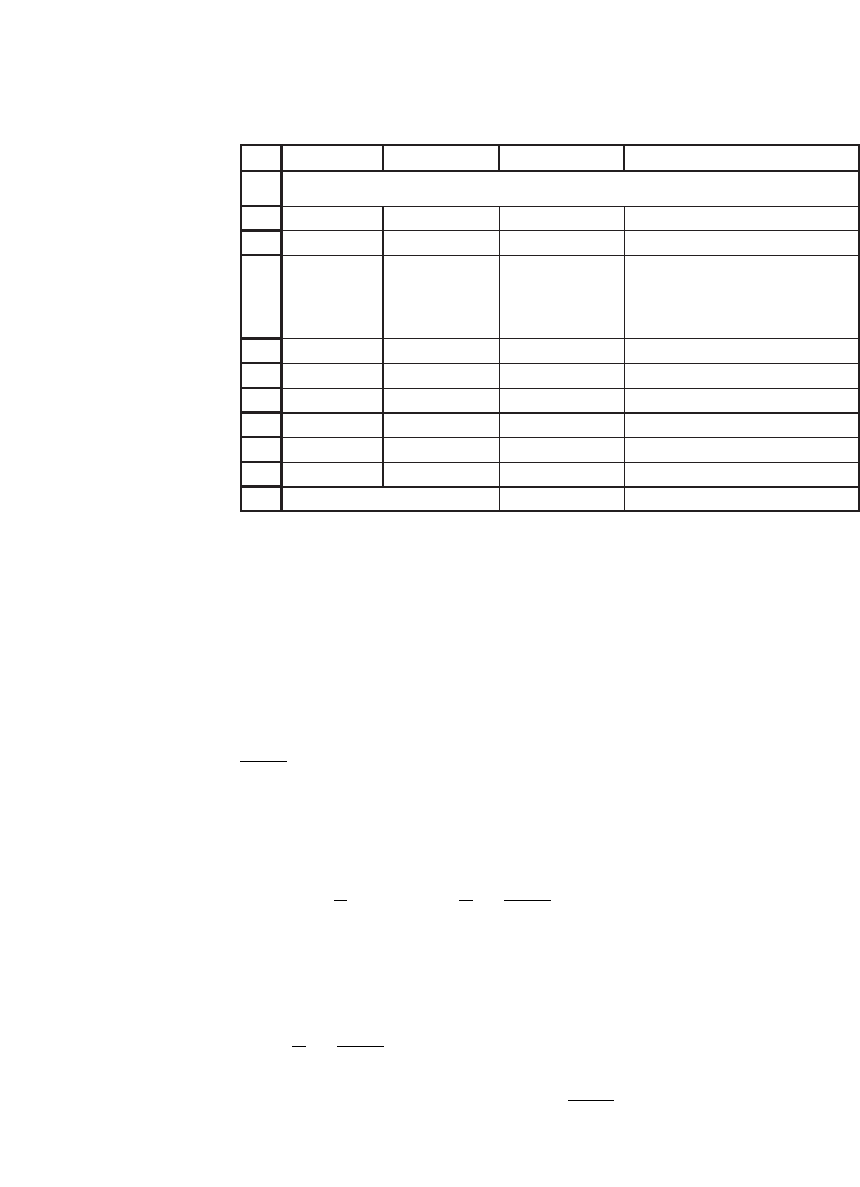

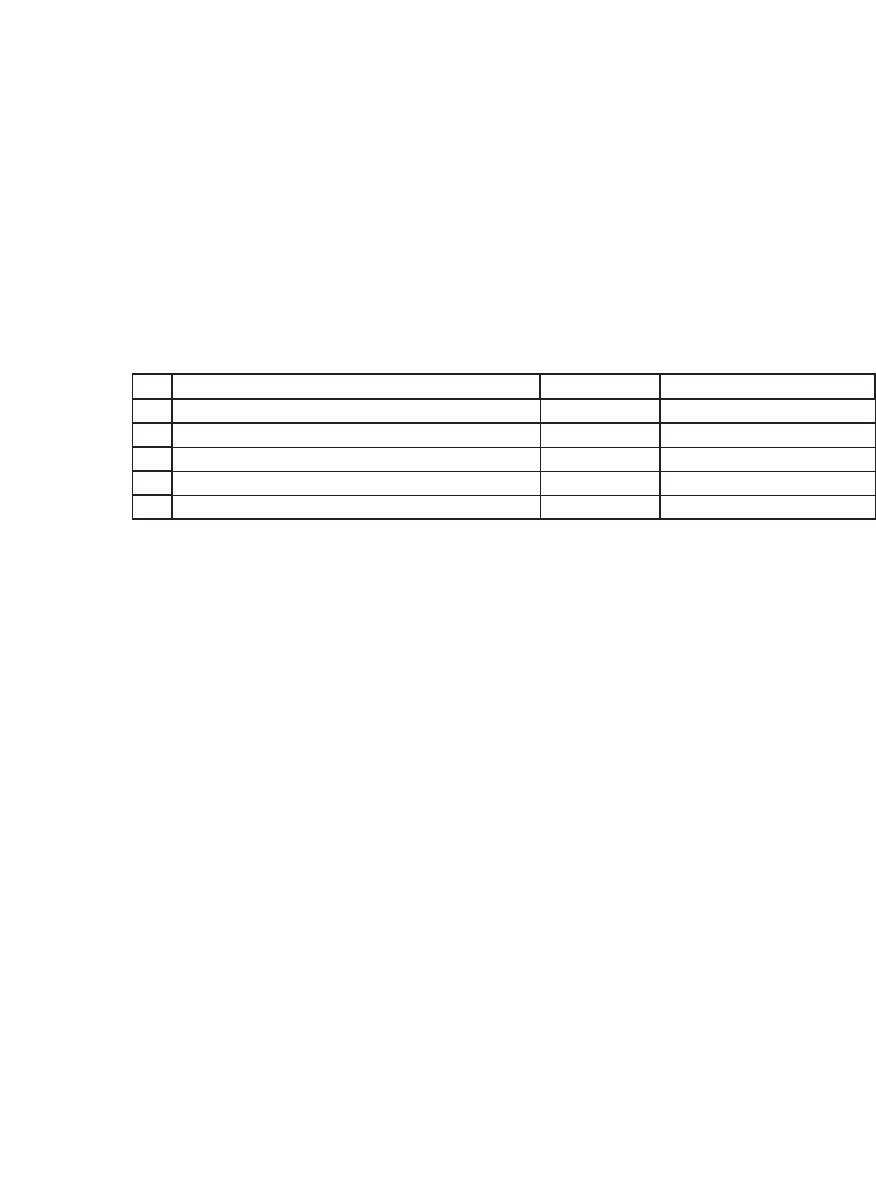

AB C D

Interest 8%

Year Cash flow

Continously

discounted

PV

1 100 92.312 <-- =B5*EXP(-$B$2*A5)

2 200 170.429 <-- =B6*EXP(-$B$2*A6)

3 300 235.988

4 400 290.460

5 500 335.160

Present value 1,124.348 <-- =SUM(C5:C9)

CONTINUOUS DISCOUNTING

1.8.3 Calculating the Continuously Compounded Return from Price Data

Suppose at time 0 you had $1,000 in the bank and suppose that one year

later you had $1,200. What was your percentage return? Although the

answer may appear obvious, it actually depends on the compounding

method. If the bank paid interest only once a year, then the return would

be 20 percent:

1 200

1 000

120

,

,

%−=

However, if the bank paid interest twice a year, you would need to

solve the following equation to calculate the return:

1 000 1

2

1 200

2

1 200

1 000

1 9 5445

2

12

,,

,

,

%∗+

⎛

⎝

⎜

⎞

⎠

⎟

=⇒=

⎛

⎝

⎜

⎞

⎠

⎟

−=

rr

/

.

The annual percentage return when interest is paid twice a year is there-

fore 2

*

9.5445% = 19.089%.

In general, if there are n compounding periods per year, you have to

solve

r

n

n

=

⎛

⎝

⎜

⎞

⎠

⎟

−

1 200

1 000

1

1

,

,

/

and then multiply the result appropriately. If n

is very large, this converges to

r =

⎛

⎝

⎜

⎞

⎠

⎟

=ln .

1 200

1 000

18 2322

,

,

%

:

29 Basic Financial Calculations

1.8.4 Why Use Continuous Compounding?

All this may seem somewhat esoteric. However, continuous compound-

ing/discounting is often used in fi nancial calculations. In this book, it is

used to calculate portfolio returns (Chapters 8–15) and in practically all

of the options calculations (Chapters 16–24).

There’s another reason to use continuous compounding—its ease of

calculation. Suppose, for example, that your $1,000 grew to $1,500 in one

year and nine months. What’s the annualized rate of return? The easiest—

and most consistent—way to fi nd this answer is to calculate the continu-

ously compounded annual return. Since 1 year and 9 months equals 1.75

years, this return is

1 000 1 75 1 500

1

175

1 500

1 000

23 1694,,

,

,

%∗∗=⇒=

⎡

⎣

⎢

⎤

⎦

⎥

=exp[ . ]

.

ln .rr

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

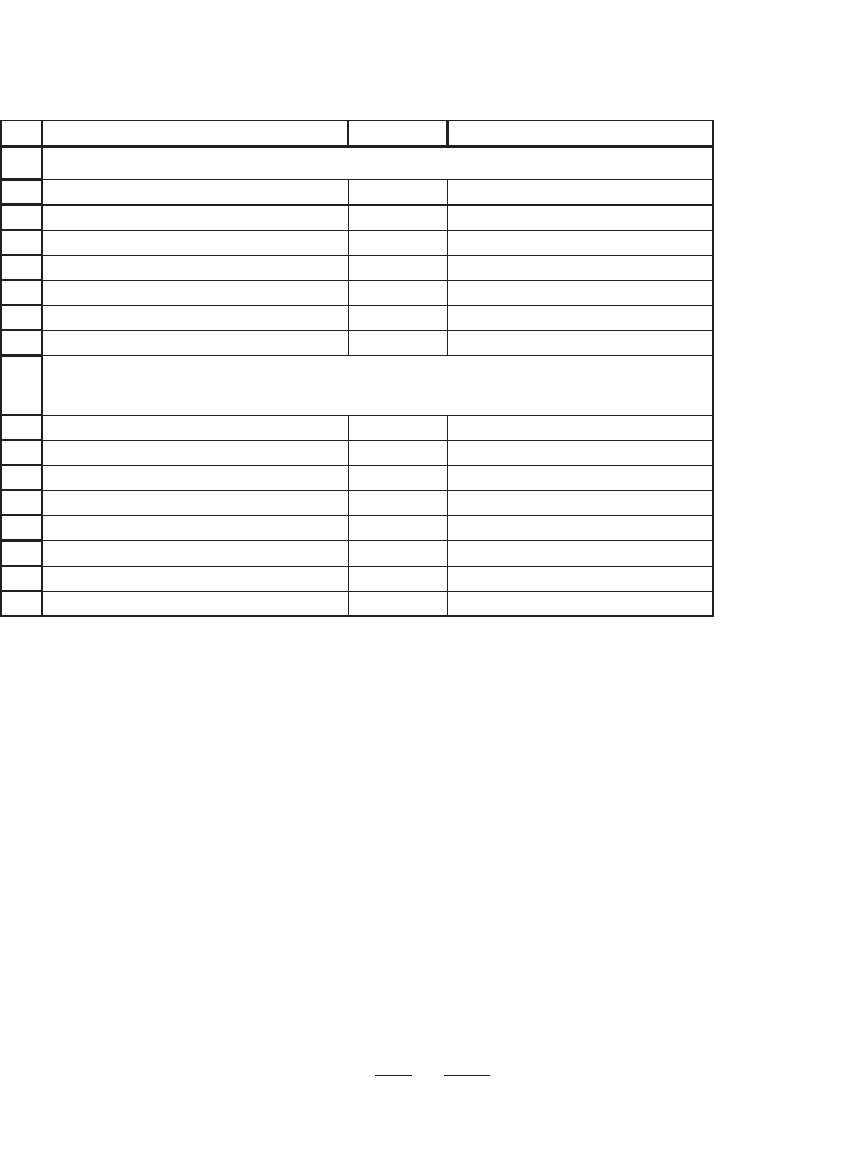

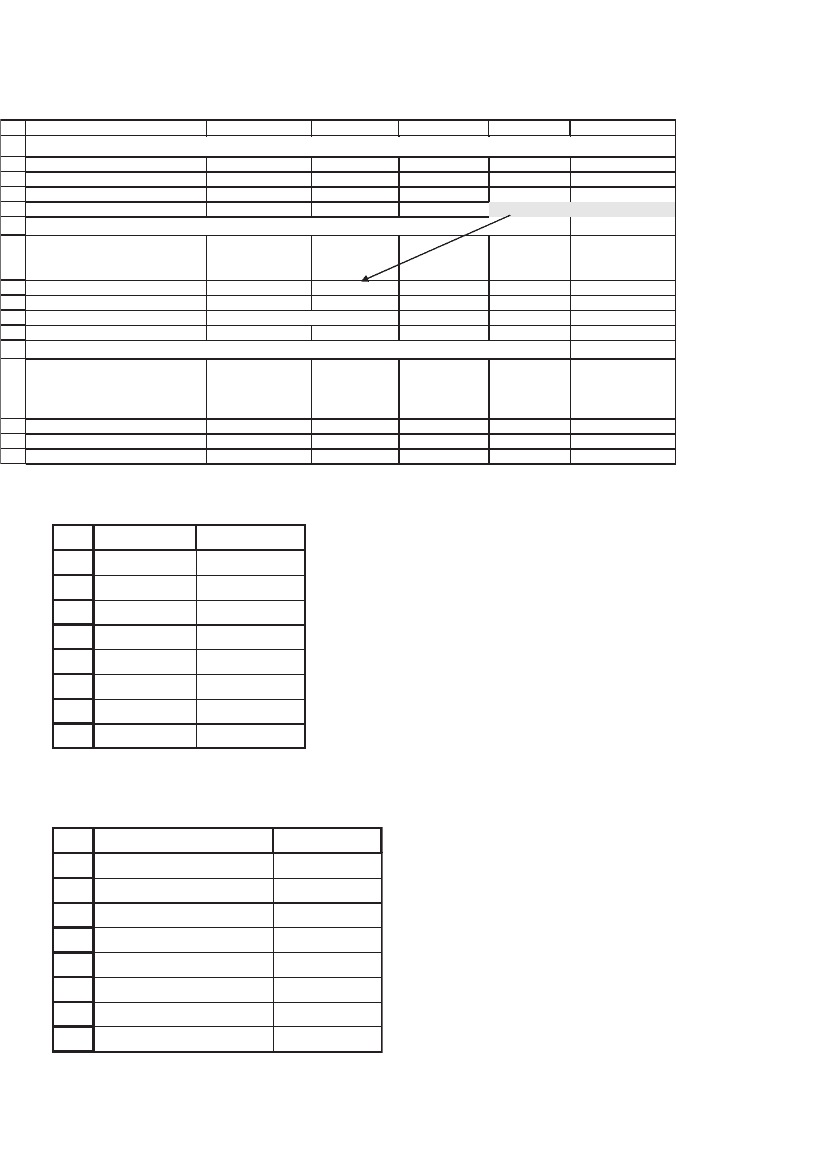

ABC

Initial deposit 1,000

End-of-year value 1,200

Number of compounding periods 2

Implied annual interest rate 19.09% <-- =((B3/B2)^(1/B4)-1)*B4

Continuous return 18.23% <-- =LN(B3/B2)

Number of compounding periods Rate

19.09% <-- =B5, data table header

1 20.00%

2 19.09%

4 18.65%

8 18.44%

20 18.32%

1,000 18.23%

CALCULATING RETURNS FROM PRICES

Implied annual interest rate with n compounding periods

30 Chapter 1

1.9 Discounting Using Dated Cash Flows

Most of the computations in this chapter consider cash fl ows that occur

at fi xed periodic intervals. Typically we look at cash fl ows that occur on

dates 0, 1, . . . , n, where the period indicates an annual, semiannual, or

other fi xed interval. Two Excel functions, XIRR and XNPV, allow us to

do computations on cash fl ows which occur on specifi c dates that need

not be at even intervals.

7

In the following example we compute the IRR of an investment of

$1,000 made on 1 January 2006 with payments on specifi c dates:

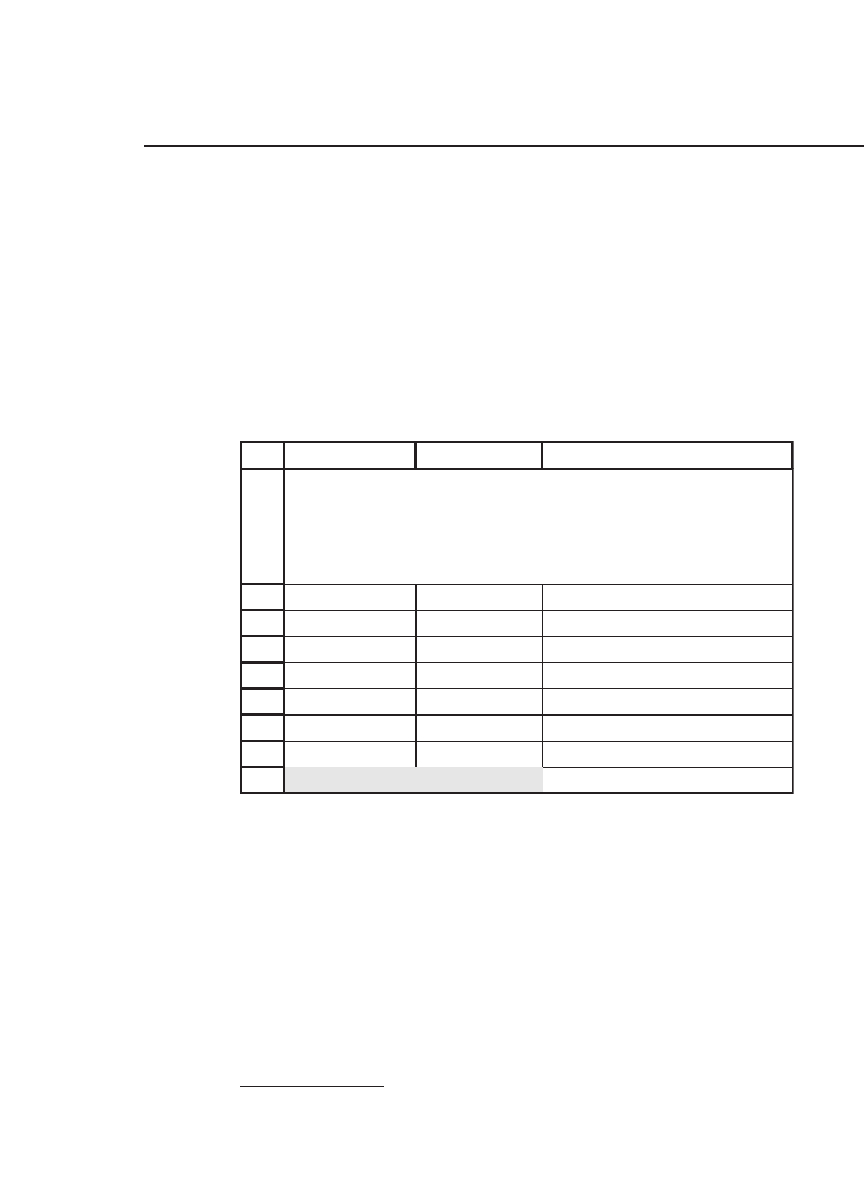

1

2

3

4

5

6

7

8

9

AB C

Date Cash flow

1-Jan-06 -1,000

3-Mar-06 150

4-Jul-06 100

12-Oct-06 50

25-Dec-06 1,000

IRR 37.19% <-- =XIRR(B3:B7,A3:A7)

USING XIRR TO COMPUTE THE

ANNUALIZED INTERNAL RATE OF

RETURN

The function XIRR outputs an annualized return. It works by comput-

ing the daily IRR and annualizing it, XIRR = (1 + DailyIRR)

365

− 1.

XNPV computes the net present value of a series of cash fl ows occur-

ring on specifi c dates.

7. If you do not see these functions, add them in by going to Tools|Add-ins on the tool

bar and checking Analysis ToolPak.

31 Basic Financial Calculations

1

2

3

4

5

6

7

8

9

10

11

12

13

AB C

Annual discount rate 12%

Date Cash flow

1-Jan-06 -1,000

3-Mar-07 100

4-Jul-07 195

12-Oct-08 350

25-Dec-09 800

Net present value 16.80 <-- =XNPV(B2,B5:B9,A5:A9)

USING XNPV TO COMPUTE THE NET

PRESENT VALUE

Note that

XNPV

has a different syntax from

NPV

!

XNPV

requires all the cash flows, including the initial cash flow,

whereas

NPV

assumes that the first cash flow occurs one period

hence.

Exercises

1. You are offered an asset costing $600 that has cash fl ows of $100 at the end of each

of the next 10 years.

a. If the appropriate discount rate for the asset is 8 percent, should you purchase

it?

b. What is the IRR of the asset?

2. You just took a $10,000, fi ve-year loan. Payments at the end of each year are fl at

(equal in every year) at an interest rate of 15 percent. Calculate the appropriate

loan table, showing the breakdown in each year between principal and interest.

3. You are offered an investment with the following conditions:

• The cost of the investment is $1,000.

• The investment pays out a sum X at the end of the fi rst year; this payout grows

at the rate of 10 percent per year for 11 years.

If your discount rate is 15 percent, calculate the smallest X that would entice you

to purchase the asset. For example, as you can see in the following display, X = $100

is too small—the NPV is negative.

32 Chapter 1

4. The following cash-fl ow pattern has two IRRs. Use Excel to draw a graph of the

NPV of these cash fl ows as a function of the discount rate. Then use the IRR func-

tion to identify the two IRRs. Would you invest in this project if the opportunity

cost were 20 percent?

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

AB C

Discount rate 15%

Initial payment 129.2852

NPV -226.52 <-- =B6+NPV(B1,B7:B17)

Year Cash flow

0 -1,000.00

1

100.00 <-- 100

2 110.00 <-- =B7*1.1

3 121.00 <-- =B8*1.1

4 133.10

5 146.41

6 161.05

7 177.16

8 194.87

9 214.36

10 235.79

11 259.37

4

5

6

7

8

9

10

AB

Year Cash flow

0 -500

1600

2300

3300

4200

5-1,000

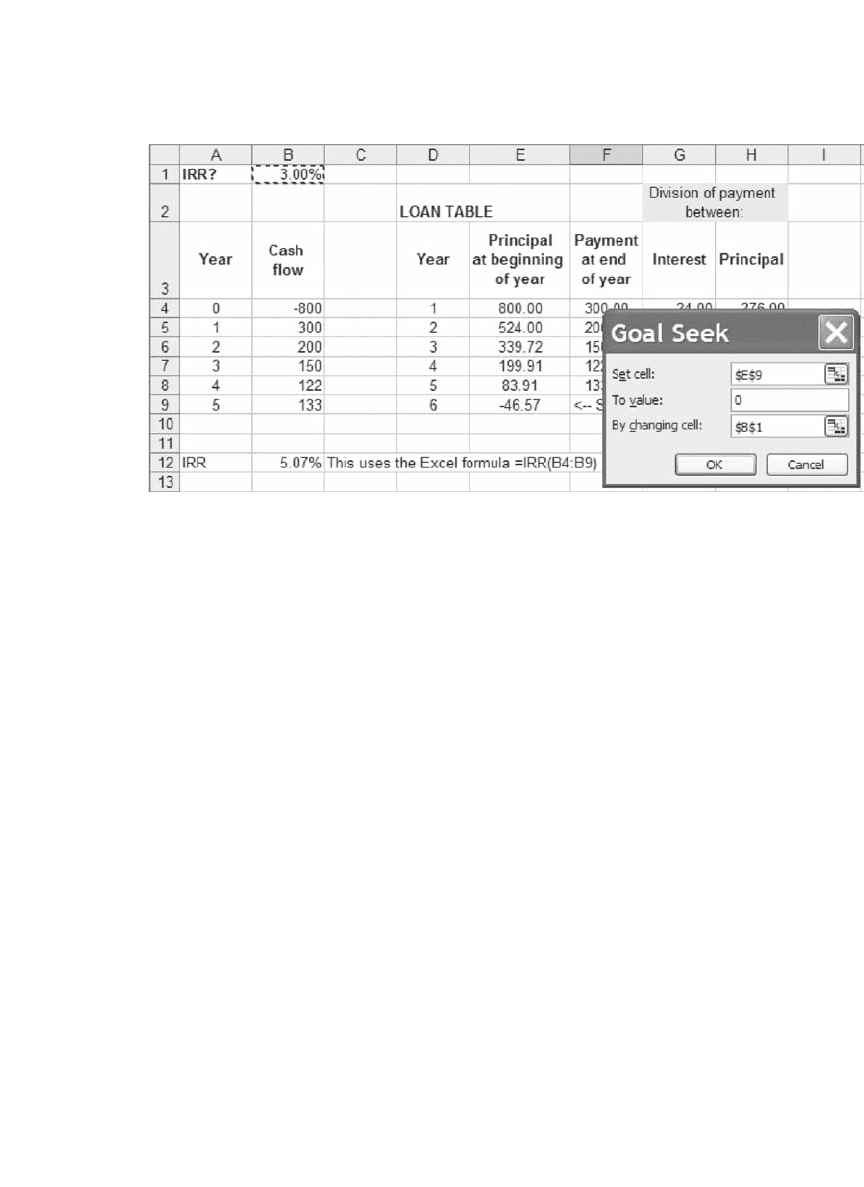

5. In this exercise we solve iteratively for the internal rate of return. Consider an

investment that costs 800 and has cash fl ows of 300, 200, 150, 122, 133 in years 1–5

(see cells A8:B13 in the following spreadsheet). Setting up the loan table shows that

10 percent is greater than the IRR (since the return of principal at the end of year

5 is less than the principal at the beginning of the year).

33 Basic Financial Calculations

1

2

3

4

5

6

7

8

9

ABCD E FGH

IRR?

10.00%

LOAN TABLE

Year Cash flow Year

Principal

at beginning

of year

Payment

at end of

year

Interest Principal

0 -800 1 800.00 300.00 80.00 220.00

1 300 2 580.00 200.00 58.00 142.00

2 200 3 438.00 150.00 43.80 106.20

3 150 4 331.80 122.00 33.18 88.82

4 122 5 242.98 133.00 24.30 108.70

5 133 6 134.28 <-- Should be zero for IRR

Division of payment

between:

Setting the IRR? cell equal to 3 percent shows that 3 percent is less than the IRR,

since the return of principal at the end of year 5 is greater than the principal at the

beginning of year 5:

1

2

3

4

5

6

7

8

9

ABCD E FGH

IRR?

3.00%

LOAN TABLE

Year Cash flow Year

Principal

at beginning

of year

Payment

at end of

year

Interest Principal

0 -800 1 800.00 300.00 24.00 276.00

1 300 2 524.00 200.00 15.72 184.28

2 200 3 339.72 150.00 10.19 139.81

3 150 4 199.91 122.00 6.00 116.00

4 122 5 83.91 133.00 2.52 130.48

5 133 6 -46.57 <-- Should be zero for IRR

Division of payment

between:

By changing the IRR? cell, fi nd the internal rate of return of the investment.

6. An alternative defi nition of the IRR is the rate that makes the principal at the

beginning of year 6 equal to zero.

9

In the preceding printout cell E9 gives the prin-

cipal at the beginning of year 6. Using the Goal Seek function of Excel, fi nd

the rate that changes this fi gure to zero (the following picture shows how the screen

should look).

9. In general, of course, the IRR is the rate of return that makes the principal in the year

following the last payment equal to zero.

34 Chapter 1

(Of course you should check your calculations by using the Excel IRR function.)

7. Calculate the fl at annual payment required to pay off a fi ve-year loan of $100,000

bearing an interest rate of 13 percent.

8. You have just taken a car loan of $15,000. The loan is for 48 months at an annual

interest rate of 15 percent (which the bank translates to a monthly rate of 15%/12

= 1.25%). The 48 payments (to be made at the end of each of the next 48 months)

are all equal.

a. Calculate the monthly payment on the loan.

b. In a loan table calculate, for each month, the principal remaining on the loan at

the beginning of the month and the split of that month’s payment between inter-

est and repayment of principal.

c. Show that the principal at the beginning of each month is the present value of

the remaining loan payments at the loan interest rate (use the PV function).

9. You are considering buying a car from a local auto dealer. The dealer offers you

one of two payment options:

• You can pay $30,000 cash.

• The “deferred payment plan”: You can pay the dealer $5,000 cash today and a

payment of $1,050 at the end of each of the next 30 months.

As an alternative to the dealer fi nancing, you have approached a local bank, which

is willing to give you a car loan of $25,000 at the rate of 1.25 percent per month.

a. Assuming that 1.25 percent is the opportunity cost, calculate the present value

of all the payments on the dealer’s deferred payment plan.

b. What is the effective interest rate being charged by the dealer? Do this calcula-

tion by preparing a spreadsheet like the one that follows (only part of the

spreadsheet is shown—you have to do this calculation for all 30 months).

35 Basic Financial Calculations

Now calculate the IRR of the numbers in column F; this is the monthly effective

interest rate on the deferred payment plan.

10. You are considering a savings plan that calls for a deposit of $15,000 at the end of

each of the next fi ve years. If the plan offers an interest rate of 10 percent, how

much will you accumulate at the end of year 5?

Do this calculation by completing the following spreadsheet. This spreadsheet does

the calculation twice—once using the FV function and once using a simple table

that shows the accumulation at the beginning of each year.

2

3

4

5

6

7

8

9

10

11

DE FG

Month Cash payment

Payment

under

deferred

payment plan

Difference

0 30,000 5,000 25,000 <-- =E3-F3

1 0 1,050 -1,050 <-- =E4-F4

2 0 1,050 -1,050

3 0 1,050 -1,050

H

0 1,050 -1,050

0 1,050 -1,050

0 1,050 -1,050

7 0 1,050 -1,050

8 0 1,050 -1,050

4

5

6

1

2

3

4

5

6

7

8

9

10

11

12

ABC

Annual payment 15,000

Interest rate 10%

Number of years 5

Total va

D

$91,576.50 <-- =FV(B2,B3,-B1,,0)

Year

lue

Accumulation

at begining of

year

Payment at

end of year

Annual

interest

1 0 15,000 0.00

2 15,000 15,000 1,500.00

3 31,500

4

5

6

36 Chapter 1

11. Redo the previous calculation, this time assuming that you make fi ve deposits at

the beginning of this year and the following four years. How much will you accu-

mulate by the end of year 5?

12. A mutual fund has been advertising that, had you deposited $250 per month in the

fund for the last 10 years, you would now have accumulated $85,000. Assuming that

these deposits were made at the beginning of each month for a period of 120 months,

calculate the effective annual return fund investors got.

Hint: Set up the following spreadsheet and then use Goal Seek.

1

2

3

4

5

BA

Monthly payment 250

Number of months 120

Effective monthly return?

Accumulation <-- =FV(B4,B2,-B1,,1)

C

The effective annual return can then be calculated in one of two ways:

• (1 + Monthly return)

12

− 1: This is the compound annual return, which is prefera-

ble, since it makes allowance for the reinvestment of each month’s earnings.

• 12*Monthly return: This method is often used by banks.

13. You have just turned 35, and you intend to start saving for your retirement. Once

you retire in 30 years (when you turn 65), you would like to have an income of

$100,000 per year for the next 20 years. Calculate how much you would have to save

between now and age 65 in order to fi nance your retirement income. Make the fol-

lowing assumptions:

• All savings draw compound interest of 10 percent per year.

• You make the fi rst payment today and the last payment on the day you turn 64

(30 payments).

• You make the fi rst withdrawal when you turn 65 and the last withdrawal when

you turn 84 (20 payments).

14. You currently have $25,000 in the bank, in a savings account that draws 5 percent

interest. Your business needs $25,000, and you are considering two options: (a) Use

the money in your savings account or (b) borrow the money from the bank at

6 percent, leaving the money in the savings account.

Your fi nancial analyst suggests that solution (b) is better. His logic: The sum of the

interest paid on the 6 percent loan is lower than the interest earned at the same

time on the $25,000 deposit. His calculations are illustrated in the following spread-

sheet. Show that this logic is wrong. (If you think about it, it couldn’t be preferable

to take a 6 percent loan when you are getting 5 percent interest from the bank.

However, the explanation may not be trivial.)

37 Basic Financial Calculations

15. Use XIRR to compute the internal rate of return for the following investment:

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

EDCBA

F

Interest earned 5%

Interest paid 6%

Initial deposit 25,000

Year

Principal at

beginning of year

Payment at

end of year

Interest paid

Repayment

of principal

1 25,000.00 13,635.92 1,500.00 12,135.92 <-- =C8-D8

2 12,864.08 13,635.92 771.84 12,864.08

Total interest paid

2,271.84

Year

In savings

account at

beginning of year

End-year

interest

earned

In account at

end of year

1 25,000.00 1,250.00 26,250.00

2 26,250.00 1,312.50 27,562.50

Interest earned

2,562.50

THE 6% LOAN

Savings Account

=PMT($B$3,2,-$B$4)

EXERCISE 14, financial analyst's calculations

1

2

3

4

5

6

7

8

AB

Date Cash flow

30-Jun-07 -899

14-Feb-08 70

14-Feb-09 70

14-Feb-10 70

14-Feb-11 70

14-Feb-12 70

14-Feb-13 1,070

16. Use XNPV to value the following investment. Assume that the annual discount rate

is 15 percent.

4

5

6

7

8

9

10

11

AB

Date Cash flow

30-Jun-07 -500

14-Feb-08 100

14-Feb-09 300

14-Feb-10 400

14-Feb-11 600

14-Feb-12 800

14-Feb-13 -1,800

17. Identify the two internal rates of return of the investment in exercise 16.