Simon Benninga. Financial Modelling 3-rd edition

Подождите немного. Документ загружается.

78 Chapter 2

2.12.1 Computing Cascade’s r

E

Using the Gordon Model

Cascade’s dividends are approximately quarterly but somewhat irregular.

In 2001, for example, the company paid no dividends. In the following

spreadsheet we have calculated three dividend growth rates, using the

daily growth as a basis for the annual growth rate. Not only is the dividend

irregular, but also annual growth rates (and, of course, the corresponding

Gordon model r

E

) differ widely depending on the base date used:

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

37

38

39

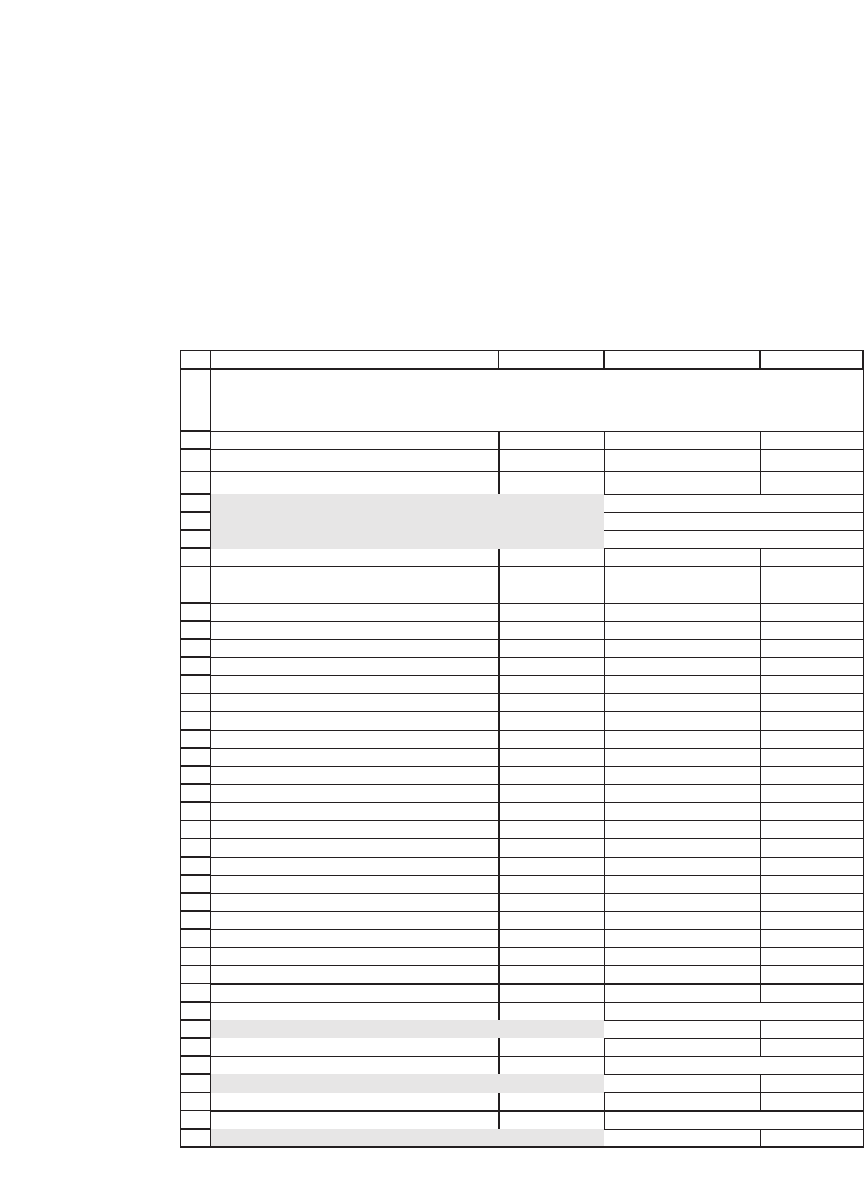

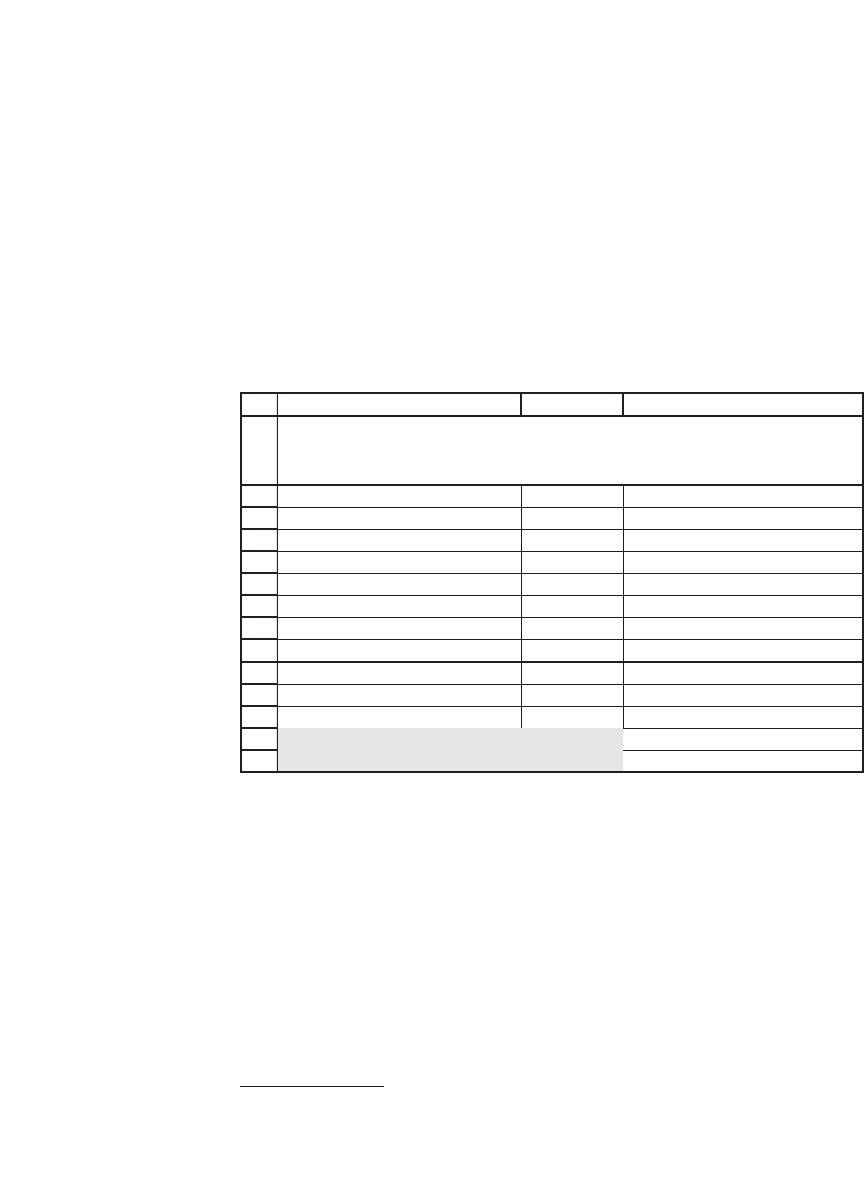

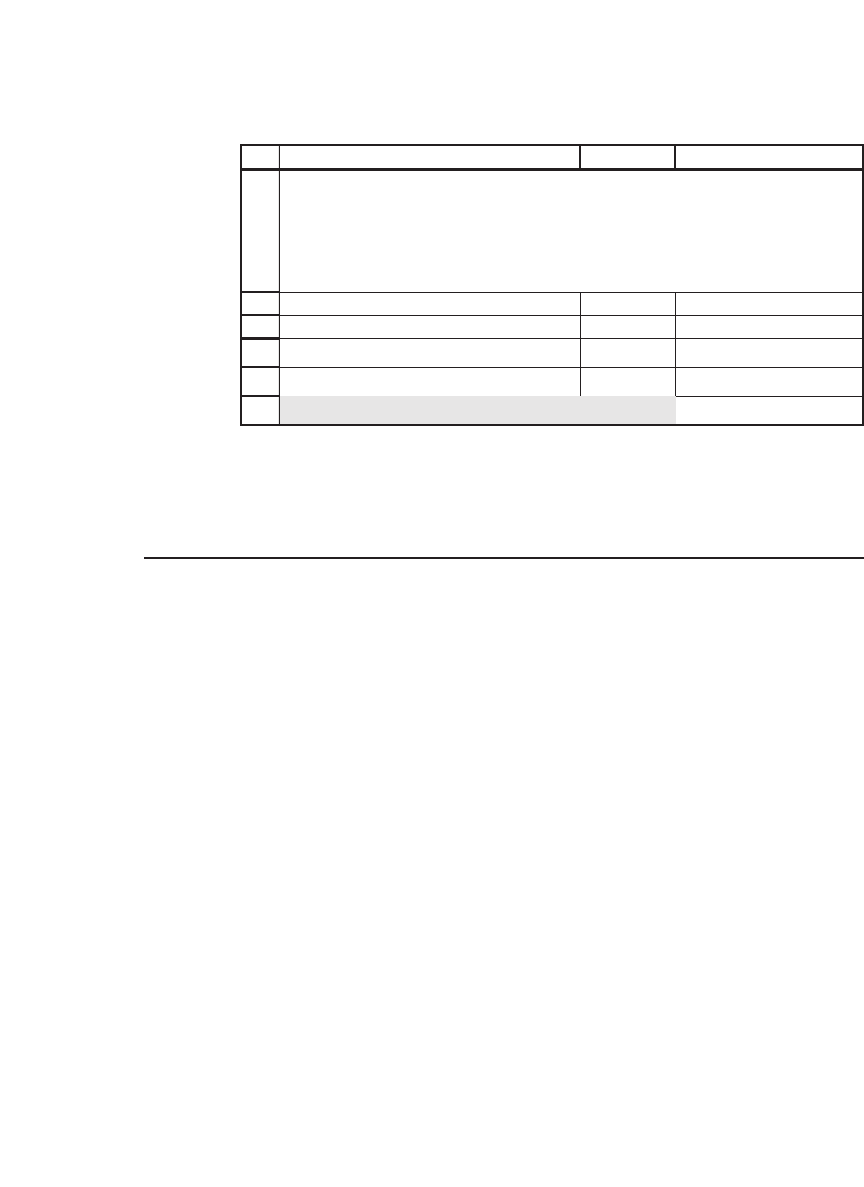

CBA

D

Share price, 31-Jan-06 50.69

Current dividend, D

0

0.60 <-- =B29*4

Gordon cost of equity, r

E

Using growth since 16-Feb-99 7.32% <-- =B3*(1+B33)/B2+B33

Using growth since 02-Jan-04 18.11% <-- =B3*(1+B36)/B2+B36

Using growth since 29-Dec-04 26.10% <-- =B3*(1+B39)/B2+B39

Date

Dividends

per share

Days between

dividend payments

16-Feb-99 0.10

18-May-99 0.10 91 <-- =A11-A10

17-Aug-99 0.10 91 <-- =A12-A11

1-Dec-99 0.10 106

22-Feb-00 0.10 83

16-May-00 0.10 84

24-Aug-00 0.10 100

29-Nov-02 0.10 827

26-Mar-03 0.10 117

25-Jun-03 0.10 91

18-Sep-03 0.10 85

2-Jan-04 0.11 106

29-Mar-04 0.11 87

23-Jun-04 0.11 86

20-Sep-04 0.11 89

29-Dec-04 0.12 100

28-Mar-05 0.12 89

1-Jul-05 0.12 95

4-Oct-05 0.15 95

3-Jan-06 0.15 91

Computing the growth rate of dividends

Daily growth, 16-Feb-99 - 03-Jan-06 0.0161% <-- =(B29/B10)^(1/(A29-A10))-1

Annualized 6.07% <-- =(1+B32)^365-1

Daily growth, 02-Jan-04 - 03-Jan-06 0.0424% <-- =(B29/B21)^(1/(A29-A21))-1

Annualized 16.73% <-- =(1+B35)^365-1

Daily growth, 29-Dec-04 - 03-Jan-06 0.060% <-- =(B29/B25)^(1/(A29-A25))-1

Annualized 24.62% <-- =(1+B38)^365-1

CASCADE: COST OF EQUITY r

E

BASED ON DIVIDENDS

Dividend growth rate computed on daily basis

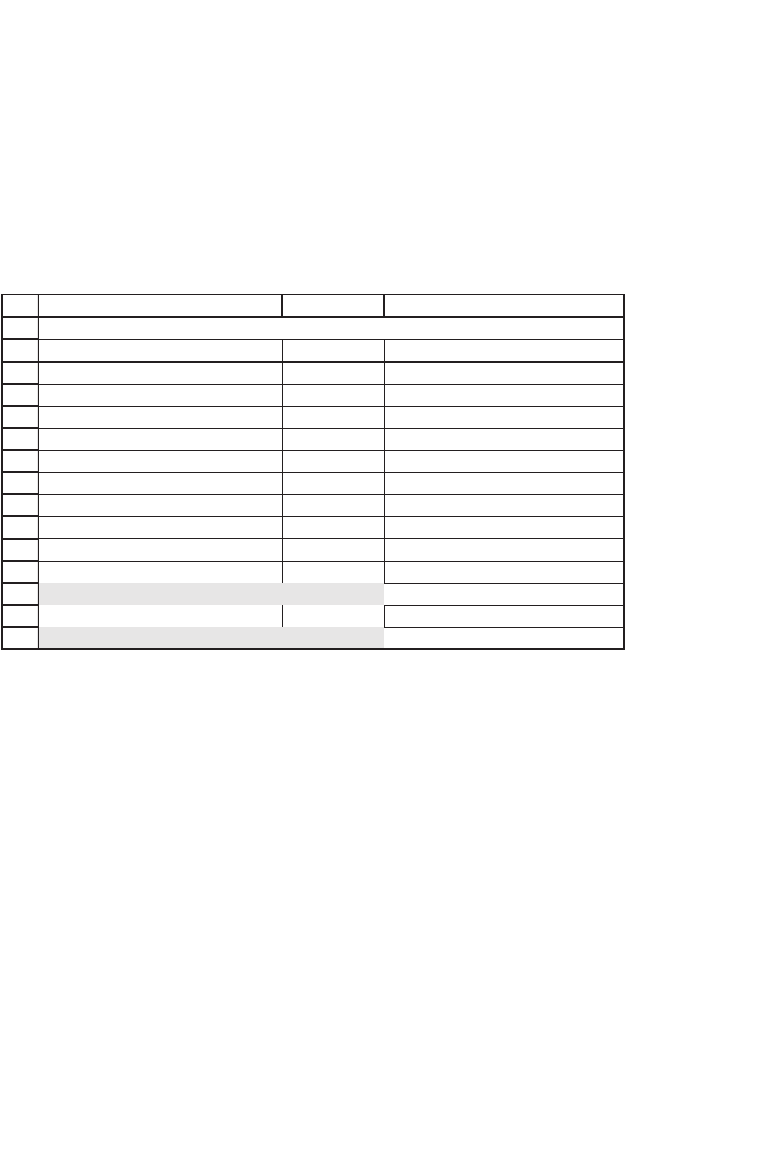

79 Calculating the Cost of Capital

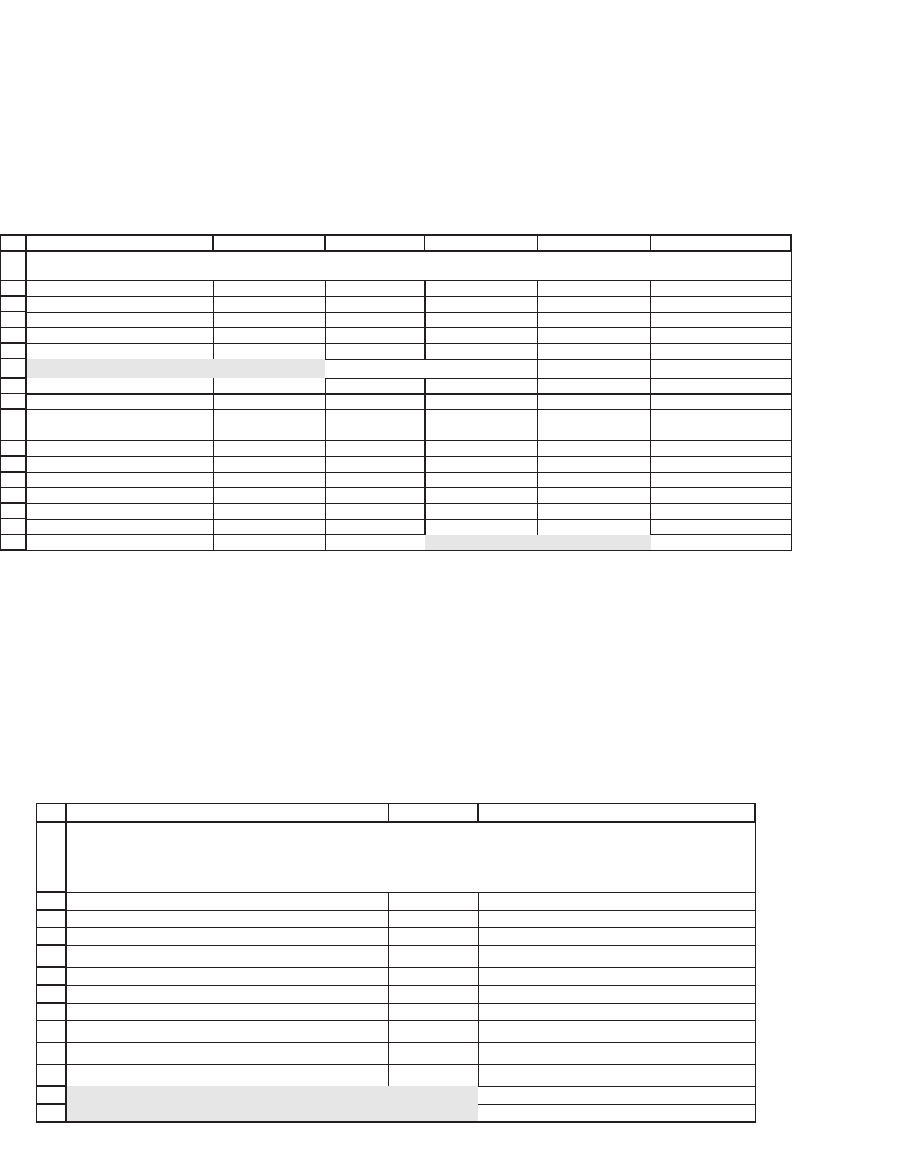

Annual cash fl ows to equity are smoother than the dividend payouts.

The cost of equity r

E

based on the annual cash fl ow to equity is 10.46

percent:

2.12.2 Cascade’s r

E

Using the CAPM

Cascade has a b equal to 1.65. Using a market price-earnings multiple to

compute E(r

M

) as illustrated on page 65, we compute r

E

= 11.55 percent

using the classic CAPM and 12.59 percent using the tax-adjusted

CAPM:

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

FEDCBA

Shares outstanding 12,536,000

Share price, 31-Jan-06 50.69

Equity value, E 635,449,840 <-- =B2*B3

2005 total equity payout 3,904,000 <-- =E16

Growth rate of payouts 9.78% <-- =E17

Cost of equity, r

E

10.46% <-- =B5*(1+B6)/B4+B6

Date

Stock

re

p

urchases

Dividends paid Stock issuance

Cash flow to

e

q

uit

y

holders

1/31/2001 0 2,448,000 2,448,000

1/31/2002 1,354,000 0 1,354,000

1/31/2003 1,396,000 1,200,000 73,000 2,523,000

1/31/2004 0 4,936,000 1,299,000 3,637,000

1/31/2005 5,478,000 1,616,000 3,862,000

1/31/2006 6,691,000 2,787,000 3,904,000

Growth rate 9.78% <-- =(E16/E11)^(1/5)-1

CASCADE: COST OF EQUITY r

E

BASED ON CASH FLOW TO EQUITY

1

2

3

4

5

6

7

8

9

10

11

12

13

CBA

Market price/earnings multiple, December 2005 18

Equity cash flow payout ratio 50.00%

Anticipated growth of equity cash flow 6.00%

Expected market return, E(r

M

)

8.94% <-- =B3*(1+B4)/B2+B4

Cascade cost of equity calculations

Cascade beta 1.65 <-- From Yahoo

Cascade tax rate, T

C

32.42% <-- Computed from Cascade financials

Risk free rate, r

f

4.93%

Cascade cost of equity, r

E,Cascade

Classic CAPM 11.55% <-- =B10+B8*(B5-B10)

Tax-adjusted CAPM 12.59% <-- =B10*(1-B9)+B8*(B5-B10*(1-B9))

COMPUTING THE COST OF EQUITY r

E

FOR CASCADE USING THE

MARKET PRICE/EARNINGS MULTIPLE TO COMPUTE E(r

M

)

80 Chapter 2

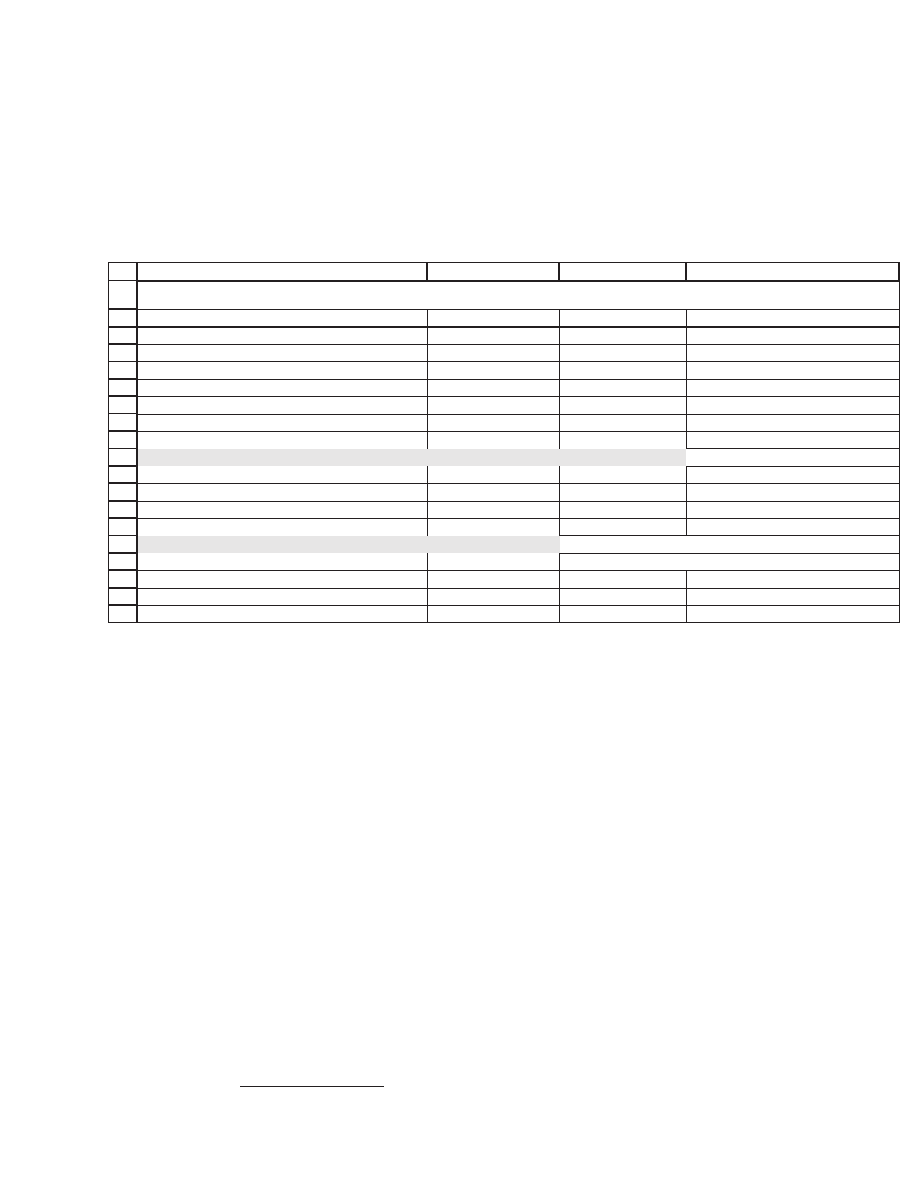

2.12.3 Cascade’s Cost of Debt r

D

Looking at the following spreadsheet, it is obvious that there are con-

ceptual problems computing Cascade’s cost of debt:

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

BA DC

2006/01/31 2005/01/31

Cash and cash equivalents 35,493,000 30,482,000

Marketable securities 23,004,000 1,503,000

Notes payable to banks 4,741,000 2,461,000

Current portion of long-term debt 12,681,000 12,916,000

Long-term debt, net of current portion 12,500,000 25,187,000

Total debt 29,922,000 40,564,000

Interest expense 2,741,000 3,570,000

Interest income 979,000 562,000

Interest cost 7.78% <-- =B12/AVERAGE(B10:C10)

Interest income 2.97% <-- =B13/AVERAGE(B3:C3)

Debt net of cash -5,571,000 10,082,000 <-- =C10-C3

Debt net of cash and marketable securities -28,575,000 8,579,000

COMPUTING THE COST OF DEBT r

D

FOR CASCADE

The problems are these:

•

Cascade has large amounts of cash. Taking this cash into account, the

company—as of 31 January 2006—has negative leverage (cell B18).

•

Cascade also has large amounts of marketable securities, which—if we

think of them as essentially liquid assets that could be used to pay off

debt—make the leverage even more negative (cell B19). We could be

less aggressive about the company’s negative leverage by excluding the

company’s marketable securities from its net debt, but we consider that

this item also refl ects a “cashlike” asset and hence should be subtracted

from Cascade’s debt (another judgment call!).

These considerations force us to make a decision about Cascade’s cost

of debt r

D

and its leverage for purpose of computing its WACC.

14

14. The company’s fi nancial statements do not report its debt rating, so we do not use

this method for computing r

D

.

81 Calculating the Cost of Capital

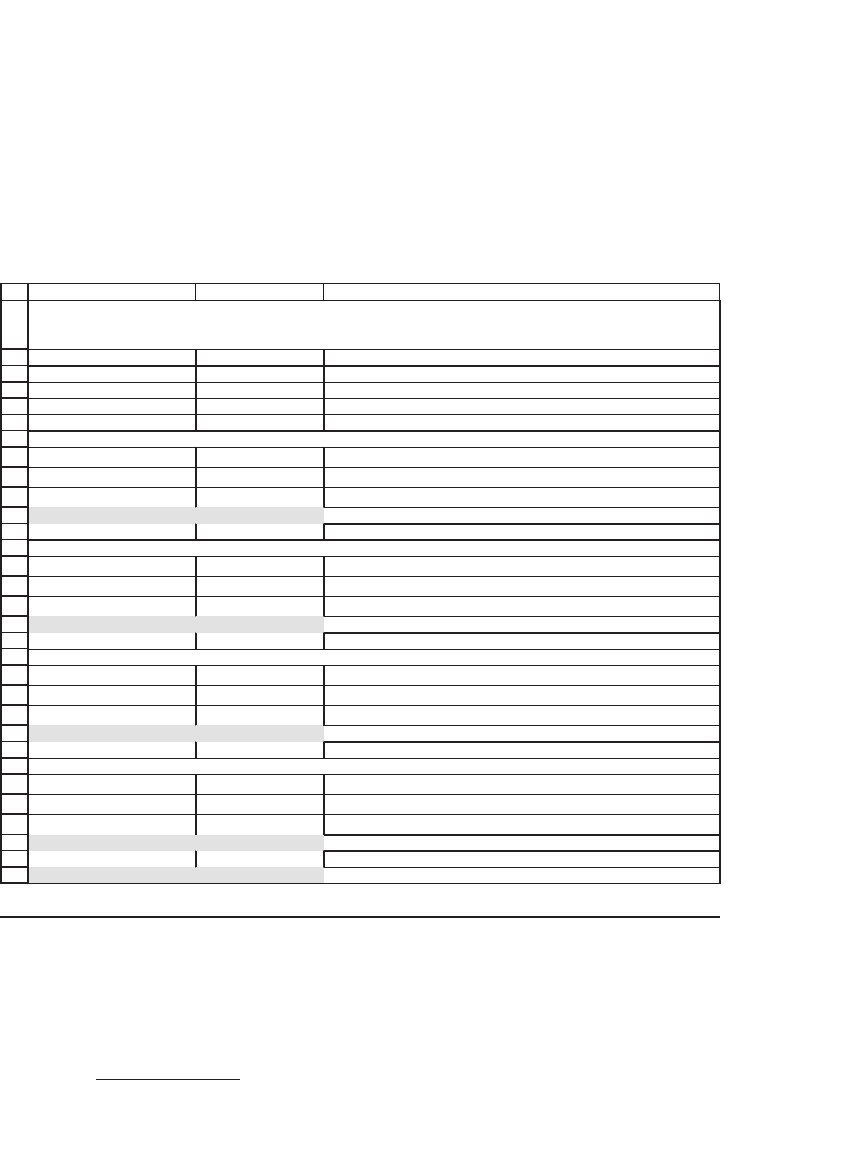

2.12.4 Cascade’s WACC

Here are our estimates of the WACC for Cascade. In line with our analy-

sis of the company’s fi nancial structure, we conclude that it has negative

leverage. We reject the Gordon r

E

based solely on dividends as unreason-

ably high and conclude that Cascade’s WACC is 11.83 percent.

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

BAC

Shares outstanding 12,536,000 <-- ='Page 79, top'!B2

Share price, end 2005 50.69 <-- ='Page 78'!B2

Equity value, E 635,449,840 <-- =B2*B3

Net debt, D -28,575,000 <-- ='Page 80'!B19

WACC based on Gordon per-share dividends and interest from financial statements

Cost of equity, r

E

18.11% <-- ='Page 78'!B6

Cost of debt, r

D

7.78% <-- ='Page 80'!B15

Tax rate, T

C

32.42% <-- ='Page 79, bottom'!B9

WACC 18.71% <-- =$B$4/($B$4+$B$5)*B8+$B$5/($B$4+$B$5)*B9*(1-B10)

WACC based on Gordon equity payouts and interest from financial statements

Cost of equity, r

E

10.46% <-- ='Page 79, top'!B7

Cost of debt, r

D

7.78% <-- ='Page 80'!B15

Tax rate, T

C

32.42% <-- ='Page 79, bottom'!B9

WACC 10.70% <-- =$B$4/($B$4+$B$5)*B14+$B$5/($B$4+$B$5)*B15*(1-B16)

WACC based on classic CAPM and interest from financial statements

Cost of equity, r

E

11.55%

Cost of debt, r

D

7.78%

Tax rate, T

C

32.42%

WACC 11.85% <-- =$B$4/($B$4+$B$5)*B20+$B$5/($B$4+$B$5)*B21*(1-B22)

WACC based on tax-adjusted CAPM and interest from financial statements

Cost of equity, r

E

12.59%

Cost of debt, r

D

7.78%

Tax rate, T

C

32.42%

WACC 12.94% <-- =$B$4/($B$4+$B$5)*B26+$B$5/($B$4+$B$5)*B27*(1-B28)

Estimated WACC?

11.83% <-- =AVERAGE(B29,B23,B17)

COMPUTING THE WACC FOR CASCADE

T

he company has negative leverage

2.13 When the Models Don’t Work

All models have problems, and nothing is perfect.

15

In this section we

discuss some of the potential problems with the Gordon model and with

the capital asset pricing model.

15. “Happiness is the maximum agreement of reality and desire.”—Stalin.

82 Chapter 2

2.13.1 Problems with the Gordon Model

Obviously the Gordon model doesn’t work if a fi rm doesn’t pay divi-

dends and appears to have no intention—in the immediate future—of

paying dividends.

16

But even for dividend-paying fi rms, it may be diffi cult

to apply the model. Particularly problematic, in many cases, is the extrac-

tion of the future dividend payout rate from past dividends.

Consider, for example, the dividend history of Ford Motor Company

in the years 1989–98:

16. Firms cannot intend never to pay dividends, because such an intention would ratio-

nally mean that the value of the shares is zero.

1

2

3

4

5

6

7

8

9

10

11

12

13

14

ABC

Year Dividend

1989 3.00

1990 3.00

1991 1.95

1992 1.60

1993 1.60

1994 1.33

1995 1.23

1996 1.46

1997 1.64

1998 22.81

Growth rate, 1989-1997 -7.27% <-- =(B11/B3)^(1/8)-1

Growth rate, 1989-1998 25.28% <-- =(B12/B3)^(1/9)-1

FORD MOTOR CO. DIVIDEND HISTORY

1989-1998

The problem here is easily identifi able: Ford, whose dividends were in

steady decline until 1997, paid a cash dividend on $21.09 in 1998, in addi-

tion to its regular quarterly dividends (which summed to $1.72 in 1998).

If we use past history to predict the future, any inclusion of the extraor-

dinary cash dividend will cause us to overestimate the future dividend

growth. Excluding the $21.09 dividend, however, also does not refl ect the

actual situation.

It appears that the 10-year history of Ford’s dividends is not, perhaps,

the best guide to its future dividend payout. Several solutions are avail-

able to those wishing to use the Gordon model:

83 Calculating the Cost of Capital

•

If we exclude the extraordinary dividend of $21.09 in 1998, then the

dividend growth over the four years ending in 1998 is a respectable 6.64

percent. If Ford’s anticipated future dividend growth is estimated to be

this rate, then—given its end-1998 stock price of $58.69—the Gordon

model cost of equity is 9.77 percent:

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

ABC

Year Dividend

1989 3.00

1990 3.00

1991 1.95

1992 1.60

1993 1.60

1994 1.33

1995 1.23

1996 1.46

1997 1.64

1998 1.72

Growth rate, 1994-1998 6.64% <-- =(B28/B24)^(1/4)-1

Ford's stock price, end-1998 58.69

Gordon cost of equity 9.77% <-- =B28*(1+B29)/B30+B29

FORD'S DIVIDENDS EXCLUDING THE 1998 $21.09 DIVIDEND

•

A better alternative might be to use Ford’s total payouts to equity,

as illustrated in this chapter. This method does not mean, however, that

we can get away from judgment calls (witness our extensive use of the

two-stage Gordon model).

•

A last alternative to fi nding Ford’s cost of capital is to predict its future

dividends by doing a full-blown fi nancial model for the company. Such

models—illustrated in Chapters 3 and 4—are often used by analysts.

Though they are complicated and time-consuming to build, they take

into account all of the fi rm’s productive and fi nancial activities. Poten-

tially they are, therefore, a more accurate predictor of the dividend.

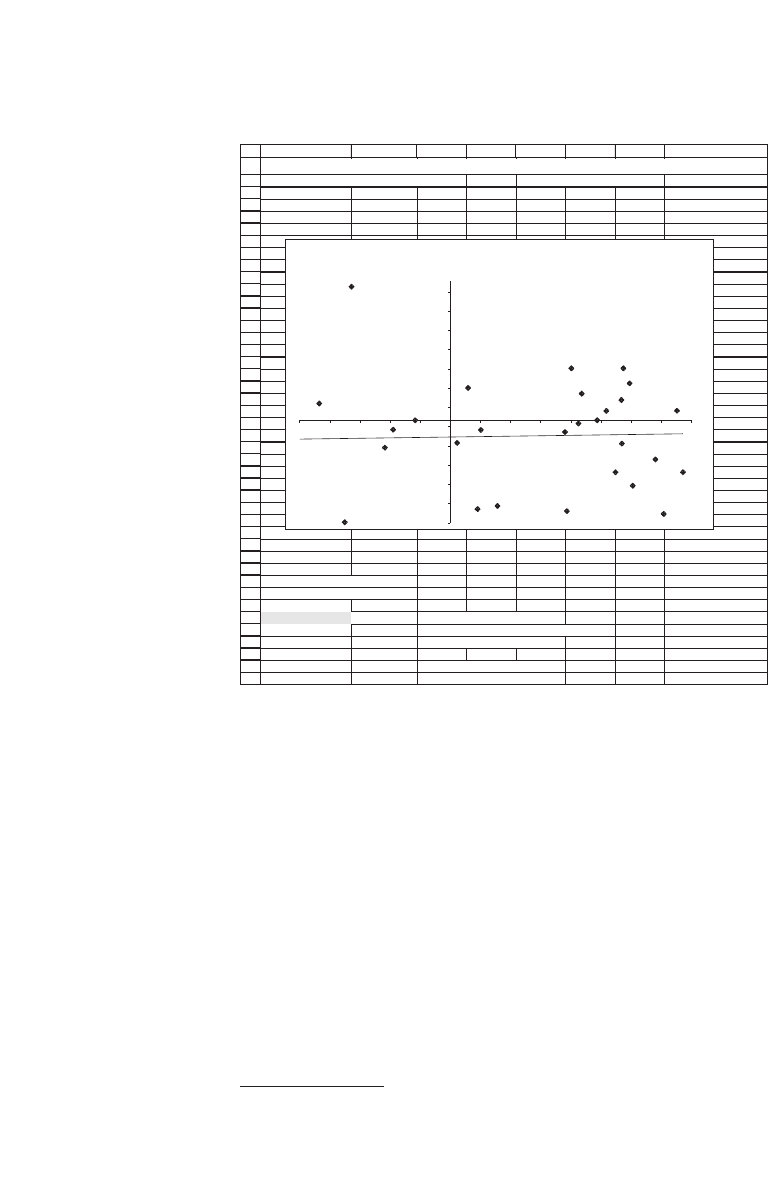

2.13.2 Problems with the CAPM

In the following spreadsheet you will fi nd the return of the S&P 500 and

Big City Bagels. Superimposed on the spreadsheet is a calculation of Big

City’s b, which is computed to be −0.0542.

84 Chapter 2

Big City Bagel’s stock is clearly risky—the annualized standard devia-

tion of its returns is 135 percent as compared to about 17 percent for the

S&P 500 over the same period. However, the b of Big City Bagels is

−0.0542, which indicates that Big City has—in a portfolio context—

negative risk. Were this true, it would mean that adding Big City to a

portfolio would lower the portfolio variance enough to justify a below-

risk-free return for Big City. While this might be true for some stocks, it

is hard to believe that—in the long run—the b of Big City is indeed

negative.

17

The R

2

of the regression between Big City’s returns and the S&P 500

is essentially zero, meaning that the S&P 500 simply doesn’t explain any

of the variation in Big City returns. For statistics mavens, the t-statistics

1

2

3

4

5

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

37

38

39

40

41

42

43

44

45

46

47

ABCDEFGH

Date price Date price

May-96 669.12 May-96 46.25

Jun-96 670.63 0.23% Jun-96 38.75 -17.69% <-- =LN(F5/F4)

Nov-96 757.02 7.08% Nov-96 16.25 -73.09%

Dec-96 740.74 -2.17% Dec-96 13.13 -21.36%

Jan-97 786.16 5.95% Jan-97 17.50 28.77%

Feb-97 790.82 0.59% Feb-97 22.50 25.13%

Mar-97 757.12 -4.35% Mar-97 25.63 13.01%

Apr-97 801.34 5.68% Apr-97 30.00 15.76%

May-97 848.28 5.69% May-97 25.00 -18.23%

Jun-97 885.14 4.25% Jun-97 24.38 -2.53%

Jul-97 954.31 7.52% Jul-97 26.25 7.41%

Aug-97 899.47 -5.92% Aug-97 20.94 -22.61%

Sep-97 947.28 5.18% Sep-97 22.50 7.20%

Oct-97 914.62 -3.51% Oct-97 10.16 -79.54%

Nov-97 955.4 4.36% Nov-97 12.50 20.76%

Dec-97 970.43 1.56% Dec-97 6.41 -66.85%

Jan-98 980.28 1.01% Jan-98 5.94 -7.60%

Feb-98 1049.34 6.81% Feb-98 4.38 -30.54%

Mar-98 1101.75 4.87% Mar-98 4.38 0.00%

Apr-98 1111.75 0.90% Apr-98 2.19 -69.31%

May-98 1090.82 -1.90% May-98 2.03 -7.41%

Jun-98 1133.84 3.87% Jun-98 1.00 -70.86%

Jul-98 1120.67 -1.17% Jul-98 1.00 0.00%

Aug-98 957.28 -15.76% Aug-98 0.63 -47.00%

Sep-98 1017.01 6.05% Sep-98 0.38 -51.08%

Oct-98 1098.67 7.72% Oct-98 0.25 -40.55%

Nov-98 1163.63 5.74% Nov-98 0.38 40.55%

Dec-98 1229.23 5.48% Dec-98 0.25 -40.55%

Jan-99 1279.64 4.02% Jan-99 0.38 40.55%

Feb-99 1238.33 -3.28% Feb-99 1.06 104.15%

Mar-99 1286.37 3.81% Mar-99 0.97 -9.23%

Return sigma (monthly) 4.98% 39.09% <-- =STDEV(G5:G38)

Return sigma (annual) 17.27% 135.41% <-- =SQRT(12)*G39

Big City's beta -0.0542 <-- =SLOPE(G5:G38,C5:C38)

-0.1127 <-- =INTERCEPT(G5:G38,C5:C38)

0.0000 <-- =RSQ(G5:G38,C5:C38)

-1.5410 <-- =tintercept(G5:G38,C5:C38)

-0.0391 <-- =tslope(G5:G38,C5:C38)

COMPUTING THE BETA FOR BIG CITY BAGELS

S&P 500 Index Big City Bagels (BIGC)

Regressing Big City Bagel on the S&P 500

Monthly data, May 1996 - March 1999

y = 0.3241x - 0.1308

R

2

= 0.0016

-80%

-65%

-50%

-35%

-20%

-5%

10%

25%

40%

55%

70%

85%

100%

-5%-4%-3%-2%-1%0%1%2%3%4%5%6%7%8%

S&P

Big City

17. A more plausible explanation is that—for the period covered—Big City’s return has

nothing whatsoever to do with the market return.

85 Calculating the Cost of Capital

of the intercept and the slope indicate that neither differs signifi cantly

from zero. In short, the regression of Big City Bagel’s historic returns on

the S&P 500 indicates no connection between the two whatsoever.

What are we to make of this situation? How should we calculate the

cost of capital for Big City? There are several alternatives:

•

We could assume that the Big City b is −0.0542. The company’s tax rate

in March 1999 was essentially zero, so that the classical CAPM and the

tax-adjusted version coincide:

1

2

3

4

5

6

ABC

Big City's beta -0.0542

Risk-free rate, r

f

4.29%

Expected market return, E(r

M

)

9.08%

Cost of equity, r

E

4.03% <-- =B4+B2*(B5-B4)

COMPUTING THE COST OF EQUITY r

E

FOR

BIG CITY BAGELS

March 1999

•

We could assume that the b of Big City is in fact 0; given the standard

deviation of the b estimate for Big City, the b is not statistically different

from zero, so that this assumption makes sense. This means that all of

Big City’s risk is diversifi able and that the correct cost of equity for Big

City is the riskless rate of interest.

•

We could assume that the covariance (or lack thereof) between Big

City and the S&P 500 is not indicative of their future correlation. This

assumption would eventually lead us to conclude that Big City’s risk is

comparable to that of similar companies. A small study of the bs of snack

food companies during the same period shows their bs to be well over

1: New World Coffee has a b of 1.15; Pepsico has a b of 1.42; Starbucks

has a b of 1.84. Thus we might conclude that the b of Big City (in the

sense of its future correlation with the market) would be somewhere

between 1.15 and 1.84. This approach, of course, would give a radically

different cost of equity for Big City:

86 Chapter 2

(For what it’s worth, this author would follow the latter case.)

2.14 Conclusion

In this chapter we have illustrated in detail the application of two models

for calculating the cost of equity: the Gordon dividend model and the

CAPM. We have also considered three of the four practicable models

for calculating the cost of debt. Because the application of these models

includes many judgment calls, our advice is to

•

Always use several models to calculate the cost of capital.

•

If you have time, try to calculate the cost of capital not only for the

fi rm you are analyzing, but also for other fi rms in the same industry.

•

From your analysis try to pick out a consensus estimate of the cost of

capital. Don’t hesitate to exclude numbers (such as Big City’s negative

cost of equity) that strike you as unreasonable.

In sum, the calculation of the cost of capital is not just a mechanistic

exercise!

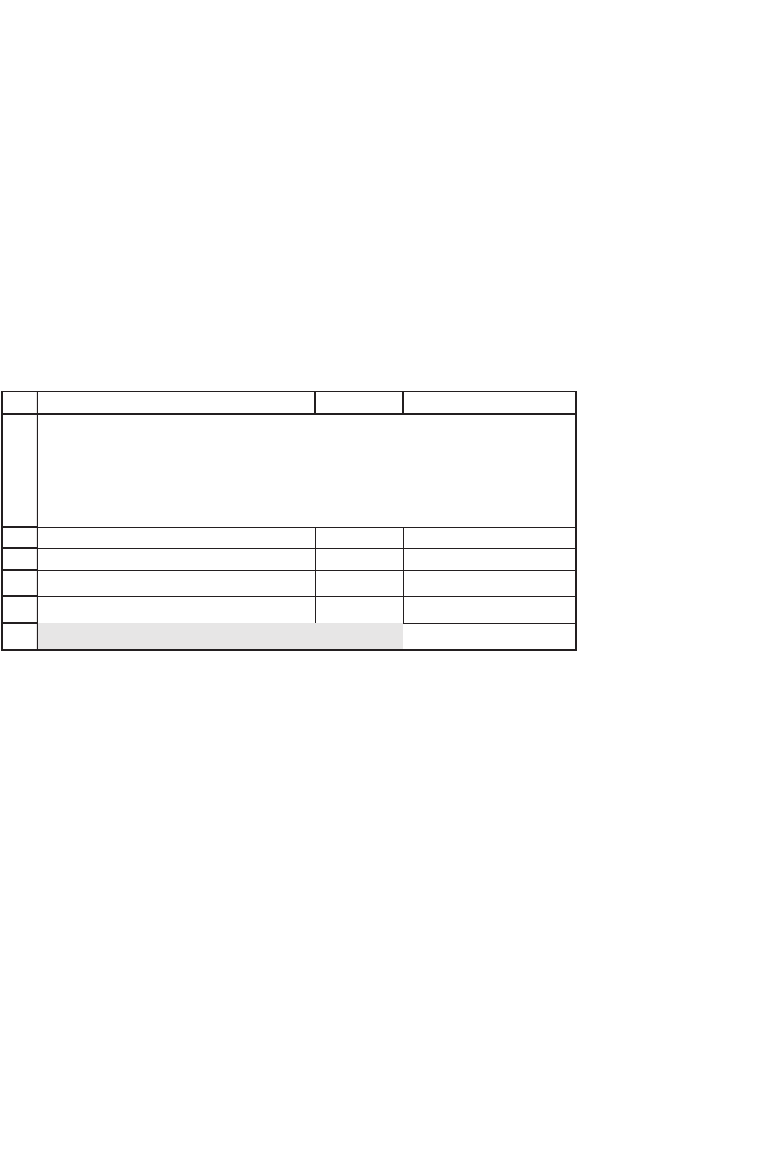

1

2

3

4

5

6

ABC

Big City's beta 1.3000

Risk-free rate, r

f

4.29%

Expected market return, E(r

M

)

9.08%

Cost of equity, r

E

10.52% <-- =B4+B2*(B5-B4)

COMPUTING THE COST OF EQUITY r

E

FOR

BIG CITY BAGELS

Assumes that forward-looking beta = 1.3

87 Calculating the Cost of Capital

Exercises

1. ABC Corporation has a stock price P

0

= 50. The fi rm has just paid a dividend of $3

per share, and intelligent shareholders think that this dividend will grow by a rate

of 5 percent per year. Use the Gordon dividend model to calculate the cost of equity

of ABC.

2. Unheardof, Inc., has just paid a dividend of $5 per share. This dividend is anticipated

to increase at a rate of 15 percent per year. If the cost of equity for Unheardof is

25 percent, what should be the market value of a share of the company?

3. Dismal.Com is a producer of depressing Internet products. The company is currently

not paying dividends, but its chief fi nancial offi cer thinks that starting in three years

it can pay a dividend of $15 per share, and that this dividend will grow by 20 percent

per year. Assuming that the cost of equity of Dismal.Com is 35 percent, value a

share based on the discounted dividends.

4. Consider the following dividend and price data for Chrysler:

1

2

3

4

5

6

7

8

9

10

11

12

13

ABCD

Year

Year-end

stock

price

Dividend

per share

Growth

rate

1986 0.40

1987 0.50 25.00% <-- =C4/C3-1

1988 0.50 0.00% <-- =C5/C4-1

1989 0.60 20.00% <-- =C6/C5-1

1990 0.60 0.00% <-- =C7/C6-1

1991 0.30 -50.00% <-- =C8/C7-1

1992 0.30 0.00%

1993 0.33 10.00%

1994 0.45 36.36%

1995 1.00 122.22%

1996 35.00 1.40 40.00%

CHRYSLER CORPORATION (C)

E

Use the Gordon model to calculate Chrysler’s cost of equity at the end of 1996.