Simon Benninga. Financial Modelling 3-rd edition

Подождите немного. Документ загружается.

368 Chapter 13

Benchmark

portfolio

returns

Variance-

covariance

matri

⎡

⎣

⎢

⎢

⎤

⎦

⎥

⎥

=

xx

Benchmark

portfolio

proportions

Normalizin

⎡

⎣

⎢

⎢

⎤

⎦

⎥

⎥

⎡

⎣

⎢

⎢

⎤

⎦

⎥

⎥

∗

gg

factor

Risk-free

rate

Variance-

covariance

matrix

Be

+

=

⎡

⎣

⎢

⎢

⎤

⎦

⎥

⎥

nnchmark

portfolio

proportions

SP500 expected return

⎡

⎣

⎢

⎢

⎤

⎦

⎥

⎥

∗

−−

⎡

⎣

⎢

⎢

⎤

⎦

⎥

⎥

Risk-free rate

Benchmark

portfolio

proportions

Vari

T

aance-

covariance

matrix

Benchmark

portfolio

proportion

⎡

⎣

⎢

⎢

⎤

⎦

⎥

⎥

ss

The normalizing factor

⎡

⎣

⎢

⎢

⎤

⎦

⎥

⎥

⎛

⎝

⎜

⎜

⎜

⎞

⎠

⎟

⎟

⎟

⎛

⎝

⎜

⎜

⎜

⎜

⎞

⎠

⎟

⎟

⎟

⎟

↑

+

Risk-free

rate

13.6.2 What’s the Upshot?

If we believe that the world portfolio is effi cient (and in the absence of

further information, there is little reason to believe otherwise), then the

anticipated returns from each of its components are given by the Black-

Litterman model, by the risk-free rate, and by an additional assumption

on expected returns (in our case, the expected return of the S&P 500

index). The exercises for this chapter explore some other variations to

the latter assumption.

13.7 Summary

Applying portfolio theory is not merely a matter of using historical

market data to derive covariances and expected returns. Blindly applying

sample data to derive optimal portfolios (as in section 13.2) usually leads

to absurd results. The Black-Litterman approach gets around these

absurdities by fi rst assuming that—in the absence of analyst opinions and

other information—the benchmark market weights and current risk-free

interest rate correctly predict the future asset returns. The resulting asset

returns can then be adjusted for opinions and confi dence in opinions to

derive an optimal portfolio.

369 The Black-Litterman Approach to Portfolio Optimization

Exercises

1. You have decided to create your own index of high-beta components of the Dow-

Jones 30 Industrials. Using Yahoo’s stock screener, you come up with the following

data.

1

2

3

4

5

6

7

8

9

10

64

65

66

67

ABCDEFGHIJKLMNO

3M

Company

MMM

Alcoa

AA

American

Express

AXP

American

International

Group

AIG

Caterpillar

CAT

Dupont

DD

Exxon

XOM

Hewlett

Packard

HPQ

Home

Depot

HD

Honeywell

HON

Intel

INTC

IBM

McDonalds

MCD

Merck

MRK

Market cap ($B) 65.66 39.11 77.91 180.72 55.7 49.08 519.89 126.75 78.37 47.55 146.76 172.03 62.88 106.93

Beta 1.07 1.37 1.06 1.17 1.98 1.06 1.13 1.6 1.2 1.3 1.9 1.81 1.37 1.16

Stock prices

2-Jul-02 56.69 24.41 29.46 61.98 20.21 35.54 32.85 13.22 29.07 28.77 17.76 67.04 22.57 38.95

1-Aug-02 56.56 22.64 30.12 60.89 19.73 34.46 31.88 12.54 31.00 26.78 15.78 71.94 21.67 39.67

3-Sep-02 49.78 17.41 26.05 53.08 16.83 30.84 28.69 10.96 24.61 19.37 13.14 55.65 16.11 36.16

1-Oct-02 57.47 19.91 30.46 60.70 18.64 35.27 30.27 14.84 27.23 21.41 16.37 75.34 16.52 42.91

2-Apr-07 82.31 35.32 60.52 69.75 72.32 48.81 79.04 42.07 37.66 53.95 21.39 101.81 48.28 51.06

1-May-07 87.96 41.28 64.82 72.34 78.25 52.32 83.17 45.63 38.65 57.91 22.18 106.60 50.55 52.06

1-Jun-07 86.79 40.53 61.03 70.03 77.97 50.84 83.88 44.62 39.35 56.28 23.74 105.25 50.76 49.80

2-Jul-07 90.21 43.08 64.51 69.04 83.20 52.62 91.94 48.54 39.39 60.96 24.55 114.81 52.09 49.02

HIGH-BETA INDEX FROM DOW-JONES 30 COMPONENTS

a. Compute the variance-covariance matrix of returns.

b. Assuming that the risk-free rate is 5.25% annually (= 5.25%/12 = 0.44% monthly),

and that the expected high-beta index annual return is 12% (= 1% monthly),

compute the Black-Litterman monthly expected returns for each stock.

2. You are an analyst investing in the high-beta DJ30 portfolio from the previous

exercise. You believe that the monthly return of MMM will be 1%. What are your

recommended optimal portfolio proportions?

3. Another analyst believes that HD will return only 0.5% per month over the next

year. What are her recommended portfolio proportions?

14

Event Studies

1

14.1 Overview

Event studies are one of the most powerful and widely used applica-

tions of the capital asset pricing model (CAPM) discussed in Chapters

8–11. An event study is an attempt to determine whether a particular

event in the capital market or in the life of a company has affected a

company’s stock market performance. The event-study methodology

aims to separate company-specifi c events from market- and industry-

specifi c events, and has often been used as evidence for or against market

effi ciency.

An event study aims to determine whether an event or announcement

caused an abnormal movement in a company’s stock price. The abnormal

returns (AR) are calculated as the difference between a stock’s actual

return and its expected return, where the stock’s expected return is typi-

cally measured using the market model, which relies only on a stock’s

market index to estimate its expected return.

2

Using the market model

can measure the correlation between an individual stock’s return and its

corresponding market returns. In some cases, we sum the abnormal

returns to arrive at the cumulative abnormal return (CAR), which mea-

sures the total impact of an event through a particular time period, also

called the event window.

14.2 Outline of an Event Study

In this section we outline the methodology of an event study. In suc-

ceeding sections we apply the methodology to a number of different

cases.

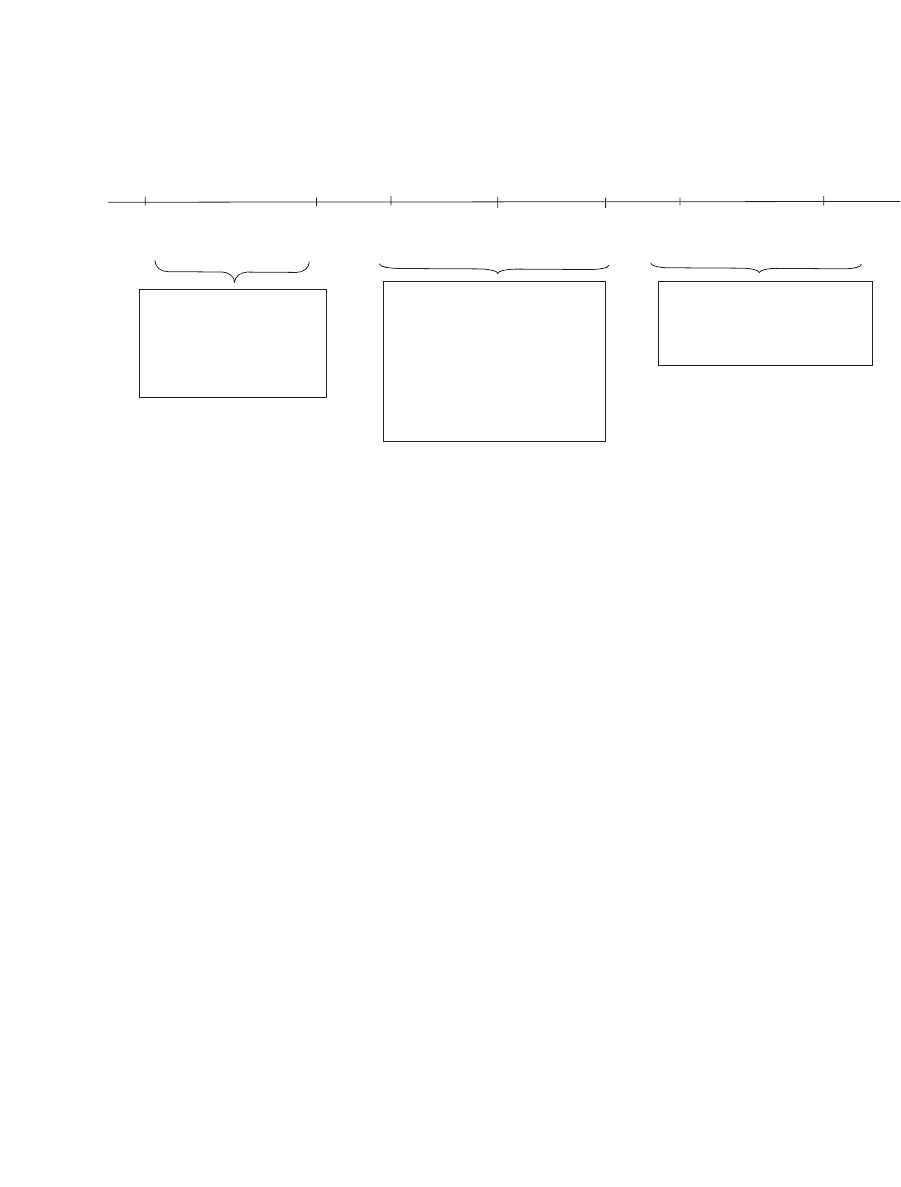

An event study is composed of three time frames: the estimation

window (sometimes referred to as the control period), the event window,

and the postevent window. The following chart illustrates these time

frames:

1. This chapter was coauthored with Torben Voetmann (tvoetmann@cornerstone.com) of

Cornerstone Research.

2. Abnormal returns are also referred to as residual returns, and both terms are used

interchangeably throughout the chapter.

372 Chapter 14

The time line illustrates the timing sequence of an event. The length

of the estimation window (also referred to as the control period) is rep-

resented as T

0

to T

1

. The event occurs at time 0, and the event window

is represented as T

1

+ 1 to T

2

. The length of the postevent window is

represented as T

2

+ 1 to T

3

.

An event is defi ned as a point in time when a company makes an

announcement or when a signifi cant market event occurs. For example,

if we are studying the impact of mergers and acquisitions on the stock

market, the announcement date is normally the point of interest. If we

are examining how the market reacts to earnings restatements, the event

window begins on the date when a company announces its restatements.

A common practice is to expand the event date to two trading days,

the event date and the following trading day. This is done to capture the

market movement if the event was announced immediately before the

market closed or after market closing.

The event window often starts a few trading days before the actual

event day. The length of the event window is centered on the announce-

ment and is normally three, fi ve, or ten days. This procedure enables us

to investigate preevent leakage of information. The postevent window is

most often used to investigate the performance of a company following

announcements such as a major acquisition or an IPO.

The estimation window is also used to determine the normal behavior

of a stock’s return with respect to a market or industry index. The estima-

tion of the stock’s return in the estimation window requires us to defi ne

T

0

T

1

T

1

+ 1

0

T

2

T

2

+ 1 T

3

Start date for

estimation

window

End date for

estimation

window

Start date for

event window

Event

date

End date for

event window

Start date for

postevent

window

End date for

postevent

window

The Event-Study Time Line

Estimation Window

The estimation window is used to

determine the normal behavior of the

stock market factors. Most often

we use the regression R

it

=

α

+

β

R

mt

to

determine this "normal" behavior.

Event Window

We use data from this window, in conjunction

with the

α

and

β

of the stock or stocks to

determine

1. Whether the event announcement was

anticipated or leaked.

2. The "postannouncement effect": How long

it took for the event information to be absorbed

by the market.

Postevent Window

Used to investigate longer term company

performance following the event.

373 Event Studies

a model of “normal” behavior: Most often we use a regression model for

this purpose.

3

The usual length of the estimation window is 252 trading days (or one

calendar year), but you may not always have this many days in your

sample. If not, you need to determine whether the number of observa-

tions you do have is suffi cient to produce robust results. As a guideline,

you should have a minimum of 126 observations; if you have less than

126 observations in the estimation window, it is possible that the para m-

eters of the market model will not indicate the true stock price movem-

ents, and thus the relationship between the stock returns and the market

returns. The estimation window that you select is supposedly a period

that was free of any problems—that is, a period that refl ects the stock’s

normal price movements.

The postevent window allows us to measure the longer term impact

of the event. The postevent window can be as short as one month and

as long as several years depending on the event.

14.2.1 Measuring the Stock’s Behavior in the Estimation Window

and the Event Window

As its name implies, the estimation window is used to estimate a model

of the stock’s returns under “normal” circumstances. The most common

model used for this purpose is the market model, which is essentially a

regression of the stock returns and the returns of the market index.

4

The

market model for a stock i can be expressed as

rr

it i i Mt

=+

αβ

Here r

it

and r

Mt

represent the stock and the market return on day t. The

coeffi cients a

i

and b

i

are estimated by running an ordinary least-square

regression over the estimation window.

The most common criteria for selecting market and industry indexes

are whether the company is listed on NYSE/AMEX or Nasdaq and

whether any restrictions are imposed by data availability. In general, the

market index should be a broad-based value-weighted index or a fl oat-

3. The regression model is similar to the fi rst-pass regression discussed in Chapter 11. See

further discussion that follows.

4. Financial economists most often use the market model to estimate the expected return

of a security, although they sometimes use the market-adjusted model or the two-factor

market model. An example of the two-factor model will be presented in section 14.5.

374 Chapter 14

weighted index. The industry index should be specifi c to the company

being analyzed. For litigation purposes, it is common to construct the

industry index instead of using alternative S&P 500 or MSCI indexes

(most industry indexes are available from Yahoo).

5

Given the equation r

it

= a

i

+ b

i

r

Mt

in the estimation window, we can

now measure the impact of an event on the stock’s return in the event

window. For a particular day t in the event window, we defi ne the stock’s

abnormal return (AR) as the difference between its actual return and the

return that would be predicted by the equation

AR r r

it it

t

iiMt

=−+

↑

↑

Actual stock

return in event

window day

Re

()

αβ

tturn predicted

by the stock’s ,

, and market return

α

β

We interpret the abnormal return during the event window as a measure

of the impact the event had on the market value of the security. This

interpretation assumes that the event is exogenous with respect to the

change in the security’s market value.

The cumulative abnormal return (CAR) is a measure of the total

abnormal returns during the event window. The variable CAR

t

is the sum

of all the abnormal returns from the beginning of the event window T

1

until a particular day t in the window:

CAR AR

tTj

j

t

=

+

=

∑

1

1

14.2.2 Market-Adjusted and Two-Factor Models

As mentioned previously, you can use several alternative models to cal-

culate a security’s expected return. The market-adjusted model is sim-

plest in design and is often used to get a fi rst impression of stock price

movements. When using the market-adjusted model, you calculate the

abnormal return by taking the difference between the actual return of

5. Yahoo is probably not the best source for index data (though it is free!). A widely used

source for industry data is Bloomberg. A wonderful free source of industry portfolio

data is available from Fama-French at http://mba.tuck.dartmouth.edu/pages/faculty/

ken.french/data_library.html.

375 Event Studies

the security and the actual return of the market index. Thus there is no

need to run OLS regressions to estimate parameters. In fact, all you need

is the returns at the time of the event. However, when testing the abnor-

mal returns for statistical signifi cance, you still need to gather returns for

the estimation period.

The two-factor model compares the returns from the market and the

industry. You calculate a stock’s expected return using parameters from

a regression of the actual returns against the market and industry returns

during the estimation period. The industry returns are included primarily

to account for industry-specifi c information in addition to the market-

specifi c information. To calculate the abnormal return you subtract from

the actual return the portion that can be explained by the market and

the portion that can be explained by the industry. The two-factor model

is illustrated in detail in section 14.5.

As Brown and Warner (1985) showed, the results in a large sample of

events are not especially sensitive to your choice of estimation model.

However, if you are dealing with a small sample, you should explore

alternative models.

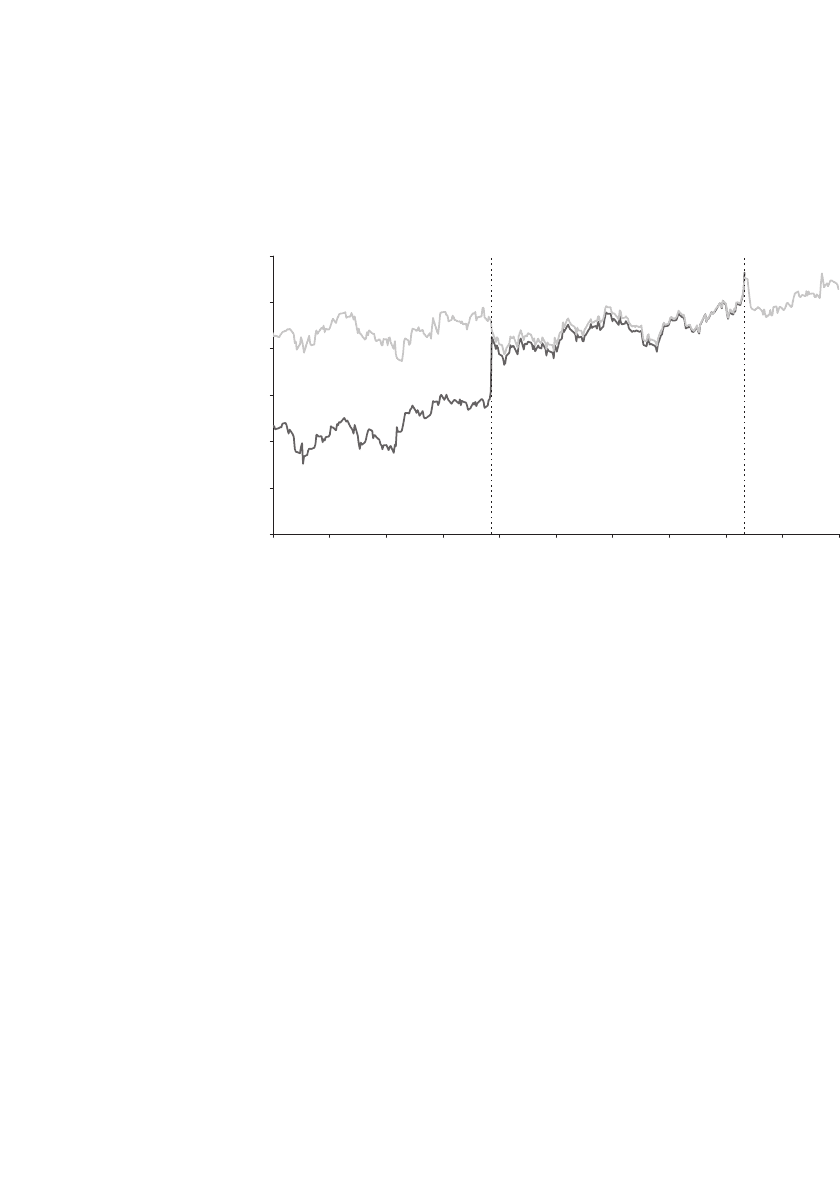

14.3 An Initial Event Study: Procter & Gamble Buys Gillette

On 28 January 2005, Procter & Gamble announced a bid for Gillette

Company. As can be seen from the press release on page 379, the bid

valued Gillette at a premium of 18 percent over its market price. As might

be expected, the bid had a dramatic effect on Gillette’s stock price:

376 Chapter 14

From the graph it appears that there might have also been a decrease in

the price of Procter & Gamble.

14.3.1 The Estimation Window

We will attempt an event study to judge the impact of the takeover

announcement on the returns of Gillette and Procter & Gamble. We fi rst

determine the event window as the 252 trading days preceding the two

days before the announcement on 28 January 2005:

$30

$35

$40

$45

$50

$55

$60

6/30/2004 8/23/2004 10/17/2004 12/11/2004 2/4/2005 3/31/2005 5/25/2005 7/19/2005 9/12/2005 11/6/2005 12/31/2005

Stock

Price

Gillette Company and Procter & Gamble

Closing Stock Price

6/30/04 – 12/31/05

Procter & Gamble

Gillette Company

1/28/05

Announcement Date

10/3/05

Completion Date

377 Event Studies

1.68%

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

258

259

260

261

262

263

264

265

266

267

268

269

270

271

272

273

274

275

276

277

278

279

280

281

282

283

284

285

286

287

288

289

290

291

292

293

294

ABCDEFG

Intercept 0.0007 <

--

=INTERCEPT($C$11:$C$262,$B$11:$B$262)

Slope 0.6364 <

--

=SLOPE($C$11:$C$262,$B$11:$B$262)

R-squared 0.1315 <

--

=RSQ($C$11:$C$262,$B$11:$B$262)

Steyx 0.0113 <

--

=STEYX($C$11:$C$262,$B$11:$B$262)

Days in estimation

window

252 <

--

=COUNT(A11:A262)

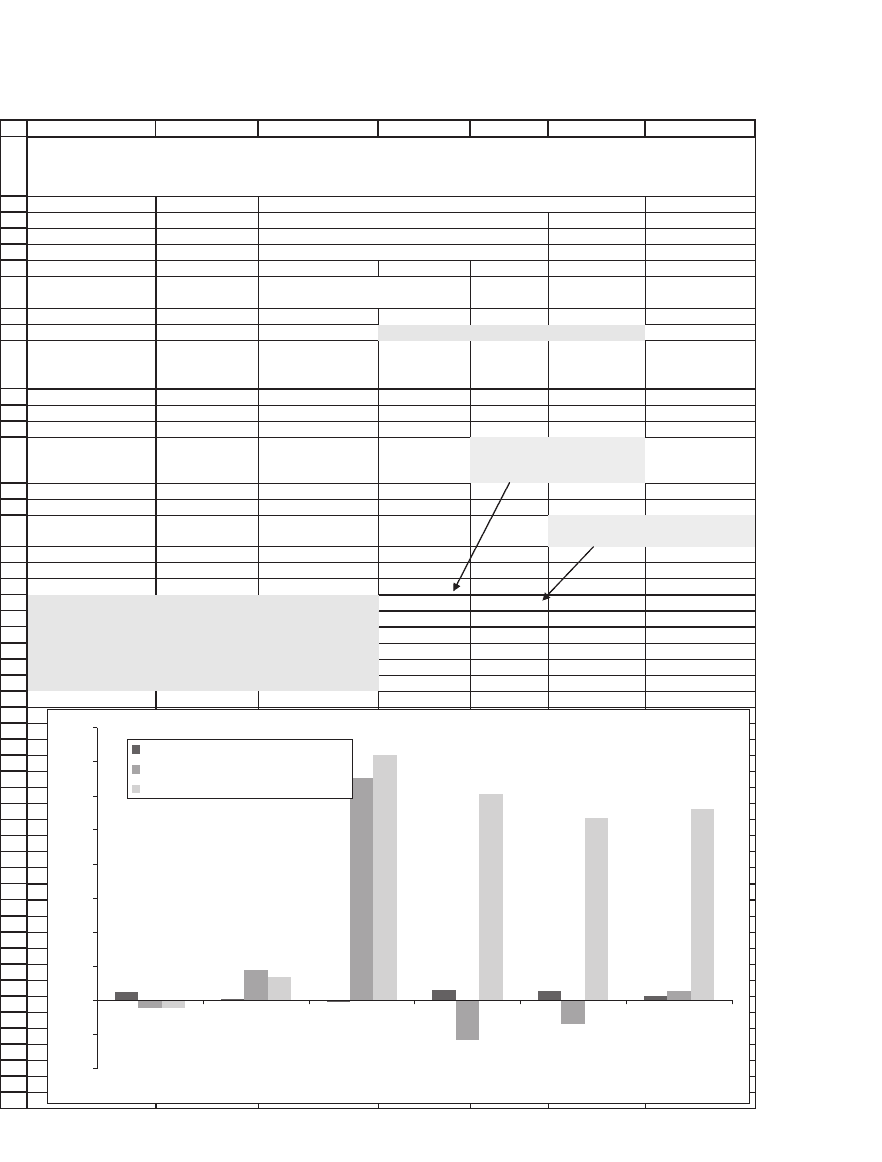

Date NYSE Gillette

Expected

return

Abnormal

return (AR)

Cumulative

abnormal

return (CAR)

27-Jan-04 -0.48% -0.42%

28-Jan-04 -1.26% -1.27%

29-Jan-04 0.00% -0.94%

30-Jan-04 -0.06% -1.39%

2-Feb-04 0.26% -0.74%

19-Jan-05 -0.78% -0.09%

20-Jan-05 -0.69% -0.56%

21-Jan-05 -0.20% -1.50%

24-Jan-05 -0.18% 0.57%

25-Jan-05 0.21% 1.44%

26-Jan-05 0.68% 0.07% 0.50% -0.44% -0.44% <

--

=E263

27-Jan-05 0.04% 1.89% 0.09% 1.80% 1.36% <

--

=F263+E264

28-Jan-05 -0.24% 12.94% -0.09% 13.03% 14.39% <

--

=F264+E265

31-Jan-05 0.82% -1.71% 0.59% -2.30% 12.09%

1-Feb-05 0.80% -0.83% 0.57% -1.40% 10.69%

2-Feb-05 0.32% 0.80% 0.27% 0.52% 11.21%

3-Feb-05 -0.29% -0.59%

4-Feb-05 0.97% -1.29%

7-Feb-05 -0.23% -0.38%

8-Feb-05 0.09% -0.75%

9-Feb-05 -0.63% -1.20%

10-Feb-05 0.68% 0.37%

11-Feb-05 0.71% 1.58%

14-Feb-05 0.26% 0.67%

15-Feb-05 0.32% 1.68%

16-Feb-05 0.04% -0.41%

17-Feb-05 -0.47% 0.18%

18-Feb-05 0.21% 0.10%

22-Feb-05 -1.05% -1.82%

23-Feb-05 0.45% 2.05%

24-Feb-05 0.55% 0.81%

25-Feb-05 1.08% 0.57%

28-Feb-05 -0.55% -2.33%

1-Mar-05 0.41% 1.19%

EVENT WINDOW

Cell D263 contains formula

=$B$2+$B$3*B263

Cell E263 contains formula =C263-

D263

GILLETTE RETURNS: ESTIMATION WINDOW

AND EVENT WINDOW

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

14%

16%

26jan05

27jan05

28jan05

31jan05

1feb05

2feb05

Expected return

Abnormal return (AR)

Cumulative abnormal return (CAR)