Pike Robert, Neal Bill. Corporate finance and investment: decisions and strategy

Подождите немного. Документ загружается.

.

Appendix A Solutions to self-assessment activities 675

CHAPTER 3

3.1 Most likely, the banker would wish to reflect on the rate of interest required:

(a) the rate of interest available from a risk-free investment,

(b) the expected changes in purchasing power over the five years, and

(c) the risk that you may not be able to repay.

We consider other factors a banker will consider in a later chapter.

3.2

3.3

Discounting at 15 per cent, a pound halves in value every five years. The present value of the purchase cost

is therefore £750,000 (£500,000 today and £250,000 in year 5).

3.4

3.5

Using the tables:

3.6 The main elements in the capital budgeting decision are found in the formula

where X is the net cash flow arising at the end of year, k is the minimum required rate of return (or dis-

count rate), I is the initial cost of the investment and n is the project’s life.

3.7 The net present value rule states that a project is acceptable if the present value of anticipated cash flows

exceeds the present value of anticipated cash flows. Wealth is maximised by accepting all projects offering

positive net present values when discounted at the required rate of return.

NPV

X

1

1 k

X

2

11 k2

2

p

X

n

11 k2

n

I

PV 1£250 8.07512 1£1,200 0.100672 £2,140

PV

£1,000

11.122

12

£257

PV

£623

11.072

8

£1,092

11.072

16

£732

CHAPTER 4

4.1 The value of a whole company, or enterprise value, is the value of all its assets, whether measured at book

value or market value (£5 billion in the case of Innogy plc). The value of the equity is the value of the own-

ers’ investment in the firm, or shareholders’ funds (£3 billion in the case of Innogy). These are equal only

when the firm is financed entirely by equity.

4.2 (i) DS Smith’s enterprise value is the total value of its assets, i.e. £1,363.1 million.

(ii) Total liabilities are creditors falling due within one year plus those payable after one year, valued at

£401.2 million and £394.1 million respectively, total £795.3 million. Minority interests represent remain-

ing shares in firms previously taken over by Smiths. These are neither Smiths’ liabilities nor Smiths’

owners’ equity. They represent ‘outsiders’ share of the total assets. Strictly, the figure given for total

assets in (i) should be adjusted for this small item.

(iii) The value of owners’ These four

terms are synonymous.

4.3 Profit after

Implied share value EPS surrogate P:E ratio 156p 152 £8.40.

EPS 1£56 m>100 m2 56p

tax 31 30% 4 £80 m £56 m

equity shareholders' funds net assets NAV £562.0 million.

CFAI_Z01.QXD 10/26/05 5:42 PM Page 675

.

676 Appendix A Solutions to self-assessment activities

4.4 Break-even value is £1 million, of which £0.361 represents the PV of the rental income. To break even, the

resale value must have a PV of Reversing the discounting process, this is a

value of Hence, the property must rise in value by about 13% to prevent

investors from losing out.

4.5

4.6

With shareholders seeking a 20% return, share price reduces to:

Because the return on reinvestment now is less than the cost of equity the firm should stop reinvesting, at

least in the short term.

4.7 The effects are:

(i) lower SV by the investment outlay, i.e. £0.3 million.

(ii) higher SV by a five year annuity delayed by five years, viz.

(iii) effect of the postponed terminal value, i.e.

The net effect is thus a marginal increase of:

1£0.51 m £0.30 m £0.13 m2 £0.08 m.

£1.42 m £1.29 m £0.13 m.

1£2.5 m 0.56742 1£4 m 0.32202

1£2.5 m 5-year PV factor2 1£4.0 m 10-year PV factor2

1£0.25 m 3.6048 0.56742 £0.51 m.

1£0.25 m 5-year annuity factor 5-year present value factor2

4.54p

10.20 0.13502

£0.70

Share price

4.54

10.15 0.1352

£3.03

growth 10.75 0.182 0.135,

i.e.

13.5% and D

1

4p 11.1352 4.54p

D

o

125% 16p2 4p

Price per share

D

1

k

e

g

D

o

11 g2

k

e

g

1£25 m £2 m £1 m £7.2 m £3 m2 £15.8 m.

Free cash flow Operating Profit depreciation interest tax investment expenditure

Taxation 30% 1£25 m £1 m2 £7.2 m

£0.639 11.122

5

£1.126 m.

1£1 m £0.361 m2 £0.639 m.

CHAPTER 5

5.1 Your answer could include the costs of developing a new product; a marketing campaign designed to

increase long-term brand awareness; investment in training and management development; acquisition of

other businesses; reorganisation and rationalisation costs (frequently in the form of redundancy payments),

or research costs incurred in developing a strategic advantage.

5.2 Accept when

Net Present Value

Internal Rate of Return

Profitability Index (or if based on NPV)

5.3 For Against

Payback period

Simple to calculate Ignores time-value of money

Easily understood Ignores cash flows beyond payback period

Crude measure of profitability Problems in setting payback requirement

Emphasises liquidity

Net present value

Theoretically sound Not well understood by non-financial managers

PI 7 0PI 7 1

IRR 7 k

NPV 7 0

CFAI_Z01.QXD 10/26/05 5:42 PM Page 676

.

Appendix A Solutions to self-assessment activities 677

Based on cash flows

Incorporates the time-value of money Estimating the appropriate discount rate is

difficult in practice

Internal rate of return

Based on cash flows Can incorrectly rank projects

Incorporates the time-value of money Difficult to calculate without a computer

Accounting rate of return

Can be related to accounts Ignores time-value of money

Based on profits not cash flows Problems in setting the required return

5.4 Evaluation of mutually exclusive projects using IRR and NPV approaches can produce different recommen-

dations. This is particularly the case where projects are very different in scale or where the cash flow profiles

of the various alternatives differ significantly. In such circumstances, the NPV approach is the better method.

5.5 Project Y offers the highest NPV for all discount rates up to 17 per cent. At the 12 per cent cost of capital,

it offers a better cash return than Project X.

5.6 Soft capital rationing is internally imposed by the firm. This may be because management is unwilling to

borrow or wishes to pursue a policy of stable growth. Hard rationing is externally imposed by the capital

market. No additional external finance is available to the firm. Capital for a single period may be resolved

by applying the profitability index to investment cash flows. Multi-period rationing requires a form of

mathematical programming.

5.7 The modified IRR is that rate of return which, when the initial outlay is compared with the terminal value

of the project’s cash flows reinvested at the cost of capital, gives an NPV of zero. Whereas the IRR method

implicitly assumes that cash flows generated by the project are reinvested at the project’s internal rate of

return, the modified IRR assumes reinvestment at the cost of capital. This means that it gives the same

investment advice as the NPV approach.

CHAPTER 6

6.1 Incremental cash flows, applied to capital budgeting, are the additional cash flows created as a direct result

of making an investment decision. Frequently, identifying these is not as straightforward as one might

think, particularly where replacement decisions are involved or where decisions in one part of the business

have ramifications for other parts.

6.2 The original cost of developing the drug is a sunk cost and should not form part of the analysis. Any adverse

effects on other parts of the business resulting from the decision to manufacture the product are an associat-

ed cash flow and should be included in the analysis. The external sale value of the patent is an opportunity

cost of proceeding with production. The million cost should be deducted from the project’s cash flows.

6.3 To: Sid Torrance

From: Rick Faldo

Clubs for Beginners Proposal

I have re-examined the points raised in your e-mail and discussed them with our accountant.

In analysing capital projects, only future investment cash flows incremental to the business are relevant to

the decision.

1 Depreciation is not a cash flow – it is a charge against profits. By comparing operating cash flows

against initial outlay, the need for depreciation becomes unnecessary.

2 Only additional fixed costs resulting from the introduction of the new project should be charged. I have

checked that no extra overheads are incurred.

3 The market research is a past cost. Its existence is not dependent upon the outcome of the decision, so

it should not be included.

£10

CFAI_Z01.QXD 10/26/05 5:42 PM Page 677

.

678 Appendix A Solutions to self-assessment activities

4 I agree that finance costs are important, but the cost of finance has already been accounted for within

the discount rate.

My ‘Clubs for Beginners’ proposal is, I suggest, an attractive one, from which the business should benefit

considerably.

6.4 Many companies have failed to take account of the relatively low inflation and interest rates when calculat-

ing the required return on investment projects. For example, a nominal rate of 20 per cent, which many firms

use, may not be unreasonable during times of relatively high inflation, but is probably excessive during

periods of low inflation. This makes it more difficult for economically attractive projects to be accepted.

6.5 Tax is a cash flow and shareholders want firms to maximise their after-tax cash flows. It affects companies

in different ways, depending on their tax situations and the capital allowances available to them. Some

types of business attract more generous allowances than others. However, for the majority of capital proj-

ects, the tax effect will have a relatively minor impact on the project outcome. Good projects are usually

viable both before and after tax.

CHAPTER 7

7.1 The attractiveness of any project depends, in large measure, on how well it helps the business implement

agreed strategies to achieve agreed goals. Investment is one of the main vehicles for implementing strategy.

It is quite possible for capital projects to be rejected because they are not compatible with long-term cor-

porate intentions. An important element of the investment decision process is to ensure that there is a good

‘fit’ between projects proposed and corporate strategy.

7.2 Stages in the investment process:

Search for opportunities

Screening (is it worth evaluating further?)

Defining the project

Evaluation

Transmission through the organisation

Authorisation

Monitoring

Post-audit

7.4 Post-auditing may confer substantial benefits on the firm. Among these are the following:

1 The enhanced quality of decision-making and planning, which may stem from more carefully and rig-

orously researched project proposals.

2 Tightening of internal control systems.

3 The ability to modify or even abandon projects on the basis of fuller information.

4 The identification of key variables on whose outcome the viability of the current and similar future proj-

ects may depend.

CHAPTER 8

8.1 While a capital project may have a high expected return, the risks involved may mean that there is the pos-

sibility that it will be unsuccessful – even to the extent of putting the whole business in jeopardy.

8.2 (1) Financial risk; (2) Business risk; (3) Project risk; (4) Portfolio or market risk.

8.3 X has the lower degree of risk relative to the expected returns.

Coefficient of variation:

Y 400>1,000 0.4

X 400>2,000 0.2

CFAI_Z01.QXD 10/26/05 5:42 PM Page 678

.

Appendix A Solutions to self-assessment activities 679

8.4

(a) Risk – a set of outcomes for which probabilities can be assigned.

(b) Uncertainty – a set of outcomes for which accurate probabilities cannot be assigned.

(c) Risk-aversion – a preference for less risk rather than more.

(d) Expected value – the sum of the possible outcomes from a project each multiplied by their respective

probability.

(e) Standard deviation – a statistical measure of the dispersion of possible outcomes around the expected

value.

(f) Semi-variance – a special case of the variance which considers only outcomes less than the expected value.

(g) Mean-variance rule – Project A will be preferred to Project B if either the expected return of A exceeds

that of B and the variance is equal to or less than that of B, or the expected return of A exceeds or is

equal to the expected return of B and the variance is less than that of B.

8.5 Monte Carlo simulation involves constructing a mathematical model which captures the essential charac-

teristics of the proposal throughout its life as it encounters random events. It is useful for major projects

where probabilities can be assigned to key factors (e.g. selling price or project life) which are essentially

independent.

CHAPTER 9

9.1 To eliminate the risk of, say, a two-asset portfolio, there would have to be perfect negative correlation

between the returns from the two assets, and also the portfolio would have to be ‘correctly’ weighted.

9.2 Expected values:

Standard deviations

9.3 The expected as explained. The standard deviation is:

9.4 To minimise portfolio risk, let invested in asset Z. Using the risk-minimising for-

mula 10.4:

1800>2400 0.75, i.e. 75%

1600 200

400 1600 400

40

2

12002

200

2

40

2

12 2002

a

*

s

y

2

cov

zy

s

z

2

s

y

2

2 cov

zy

a

*

the proportion

24

2576

21368.642 1207.362

2310.642

2

1302

2

10.362

2

1402

2

04

value 20%

21600

40, i.e. 40%

2310.5 16002 10.5 160024

B: s

B

2310.52160% 20% 2

2

10.52 120% 20% 2

2

4

2900 30, i.e. 30%

2310.5 9002 10.5 90024

A: s

A

2310.52110% 20% 2

2

10.52 150% 20% 2

2

4

B: EV 10.5 20% 2 10.5 60%2 20%

A: EV 10.5 10% 2 10.5 50%2 20%

CFAI_Z01.QXD 10/26/05 5:42 PM Page 679

.

680 Appendix A Solutions to self-assessment activities

9.5 An efficient frontier is a schedule tracing out all the available portfolio combinations that either minimise

risk for a given expected return or maximise expected return for a given risk.

9.6

9.7

The outright risk-minimiser locates at point B, the portfolio with minimum possible risk. However, risk-

averters are willing to accept higher levels of risk if offered sufficient additional rewards, i.e. higher returns.

Hence, any portfolio along AB is consistent with risk aversion. The lower the investor’s concern with risk,

the nearer to point A he/she will locate.

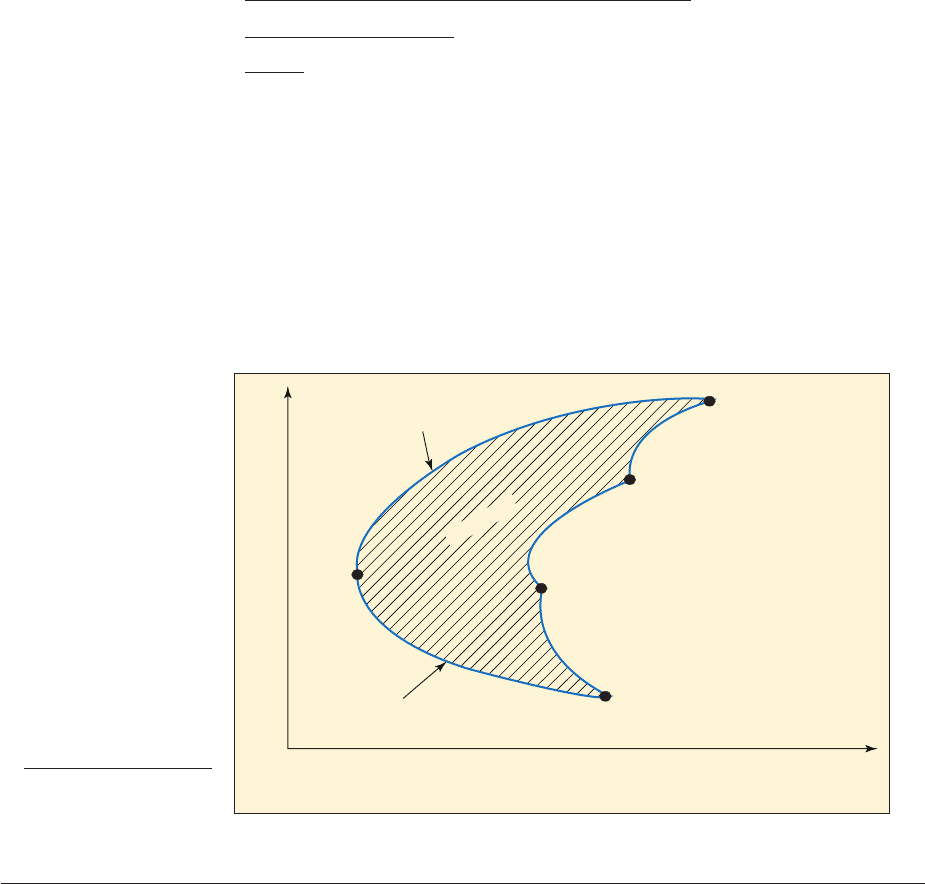

9.8 With four separate assets to choose from, the investor faces a wider array of available portfolios. The enve-

lope that summarises his/her opportunities has the same basic shape as in the text, but with an extra ‘cor-

ner’ representing the fourth asset, denoted by point D in Figure A.1. Notice that all sorts of configurations

of the envelope are possible, depending on the location of the four assets.

£349

2121,288

272,900 127,428 78,840

Standard deviation 230.272

2

11,0002

2

10.732

2

14892

2

210.27210.7321200,00024

£2,562

Expected NPV 10.27 £3,0002 10.73 £2,4002

A

D

B

C

E

AE efficient

EC inefficient

Combinations of

A and B, A and C

and of C and D

lie within the

envelope

inefficient

Expected return on

portfolio (ER

P)

Risk of portfolio

(Standard deviation, s

p

)

Figure A.1

Portfolio combinations

with four assests

CHAPTER 10

10.1

10.2

To eliminate the specific risk, the investor would have to hold every share quoted on the market i.e. the

market portfolio.

10.3 Systematic risk: political turmoil

exchange rate fluctuation

interest rate changes.

Unique risk: labour relations problems

announcement of a major new contract

discovery of a defect in a key product.

3£0.01 £0.174>£2.20 £0.27>£2.20 0.123 i.e. 12.3%

TSR 3Dividend Capital Gain4>Opening share price, expressed as a percentage.

CFAI_Z01.QXD 10/26/05 5:42 PM Page 680

.

Appendix A Solutions to self-assessment activities 681

10.4

According to the CAPM, the Beta of Walkley Wagons is 1.2. Hence, the predicted return on its shares

would be the predicted market return of 25%, i.e. 30%. (If you believe the experts!)

10.5 Variations around the characteristics line reflect the impact of factors unique to the firm. For BA, this

could be due to a pilots’ strike, pressure to relinquish landing slots at Heathrow, sale of its stake in

Qantas, competition authorities blocking a proposed strategic alliance, etc.

10.6 The Beta values cluster in a relatively narrow range because these are large firms that are, themselves,

mostly well diversified, and also because they constitute a major part of the overall market portfolio,

which has a Beta of 1.0.

10.7 The market portfolio has a Beta of 1.0 simply because it varies in perfect unison with itself!

10.8 Over to you!

10.9 Here, we need surrogate Betas. Two very similar retailing Betas are given: Boots with 0.64, and Marks &

Spencer with 0.67. Taking their average of 0.655, and using a risk-free rate of 5 per cent and the market

risk premium of 6 per cent, the required return is:

This investment would lower the overall Beta of British Airways, depending on the relative size of the

two areas of activity.

10.10 An investor might outperform the market with this policy, assuming it did actually rise. However, with

such a narrowly-diversified portfolio, he/she would be unduly exposed to risk factors unique to these

five firms.

10.11 Long-term performance. Some of a firm’s businesses may be cyclical and during the downswings,

the other businesses with more stable characteristics can protect overall performance. St Gobain’s

glass manufacturing activity is cyclical whereas its building materials business is more stable over

the long term.

Cash flow for expansion. A diversified company can generate strong cash flow that can enable it to

expand further (only half of St Gobain’s cash flow is allocated to capital spending).

Shared expertise. St Gobain operates the nine ‘delegate offices’ that act as collection points for ideas

across the company.

Candidate for state support. The strongest companies – the ‘national champions’ – often receive sup-

port from central governments. St Gobain hopes for support to allow it to develop new glass structures

for flat-screen TVs, in particular.

5% 0.65516%2 5% 3.9% 8.9%.

1.2

CHAPTER 11

11.1 With and the dividend covered three times, the dividend per share must be

Hence, the cost of equity is:

11.2 The DVM breaks down totally:

(i) when the firm pays no dividend

(ii) when the growth rate of dividends exceeds the cost of equity.

11.3

For activity B, it is

5% 0.836% 4 9.8%

For activity A, it is

5% 2.036% 4 17%

Overall, the required return 5% 1.236% 4 12.2%

k

e

12p 11 3% 2

£1.80

3% 16.9% 3%2 9.9%

12p 136p>12p 32.EPS 36p,

CFAI_Z01.QXD 10/26/05 5:42 PM Page 681

.

682 Appendix A Solutions to self-assessment activities

CHAPTER 12

12.1 (1) A call option gives the owner the right to buy shares (or whatever) at a fixed price within a set period.

A put option is the right to sell at a fixed price.

(2) A European option can only be exercised on the expiry date, while an American option can be exer-

cised any time over the life of the option. Most traded options in Europe are actually the American

variety.

(3) A wide range including shares, bonds, currency, interest rates, gold, silver, wool, soya beans, etc.

Options are also available on interest rates.

(4) (a) The lower the exercise price, the more likely it is that it will be profitable to exercise the call, and

therefore the more investors are prepared to pay for the call.

(b) The longer the time that a call has to run to maturity, the greater the scope for the price to drift

above the exercise price. Of course there is also more time for prices to fall below the exercise price.

However, the potential gains and losses are not symmetrically distributed. There are limits to the

losses but not to the gains.

(c) The price exceeds the profit that can be made immediately by exercising the call as over its remain-

ing life there will be the opportunity to capitalise on further price movements. These may be

upwards or downwards but we have already noted a bias in the consequence of price changes –

this offers a higher expected value of potential gains than losses.

12.2 Applying the equation on page 304, we find that the put–call parity relationship holds:

12.3 Option value increases with the volatility of the underlying share price because the greater the variability

in share price, the greater the probability that the share price will exceed the exercise price. Because option

values cannot be negative, only the probability of exceeding the exercise price is considered.

12.4 Option values are determined by five main factors:

■ share price

■ exercise price of the option

■ time to expiry of the option

■ the risk-free rate of interest

■ volatility of the underlying share price

In addition, the payment of dividends and underlying stock market trends have some influence on option

values.

PV exercise price 50p

44

7

1 55>1.10

Share price value of put value of call E>11 R

f

2

11.4

11.5

Hence, the required return 5% 0.4836% 4 5% 2.9% 7.9%.

10.5 0.8 1.22 0.48

The project Beta RSF OGF divisional Beta

10.65 2.02 10.35 0.82 1.58.

Company Beta 10.65 Beta of A2 10.35 Beta of B2

CHAPTER 13

13.1 Treasury management involves the efficient management of liquidity and risk in the business. The treas-

urer usually has primary responsibilities for funding, risk management, working capital management and

liquidity, and managing banking relationships.

CFAI_Z01.QXD 10/26/05 5:42 PM Page 682

.

Appendix A Solutions to self-assessment activities 683

13.2

The matching approach to funding is where the maturity structure of the company’s financing matches the

cash flows generated by the assets employed. In simple terms, this means that long-term finance is used to

fund both fixed assets and permanent current assets, while fluctuating current assets are funded by short-

term borrowings.

13.3 Over to you!

13.4 It should let it lapse as the spot price is cheaper than the exercise price.

13.5 Forward – commits the user to buying or selling an asset at a specific price on a specific future date.

Future – a forward contract traded on an exchange.

Swap – a contract by which two parties exchange cash flows linked to an asset or liability.

Option – the right to buy or sell at an agreed price.

13.6 Smaller firms will rarely have a separate treasury function, the accountant or managing director having to

perform much of this role. There is a real danger that key areas will be neglected. For example, liquidity

management or banking relationships may be largely neglected. Funding may be through short-term over-

draft facilities when a larger, more secure form of funding may prove beneficial. Other dangers are that

small businesses involved in exporting or importing may neglect the need to manage or hedge currency

risks, or corporate borrowers may neglect exposure to interest rate fluctuations.

13.7 A company with a simple production process, that makes to order, enjoys generous supplier credit terms and

offers cash discounts for early payment could have a much shorter operating cycle than the industry average.

A firm with a longer cycle demands more capital and is more exposed to bad debt and stock losses.

13.8 Overtrading arises when businesses operate with inadequate long-term capital. It occurs when firms:

(a) are set up with insufficient capital;

(b) expand too rapidly without a commensurate increase in long-term finance;

(c) utilise net current assets in an inefficient manner. The consequences can be extremely serious and pos-

sibly fatal unless the problem is addressed.

14.1 Rough approximation

APR method

per period

In both cases, the cost of granting the cash discount terms looks prohibitive, unless it is thought likely that

the customer would take much longer to pay than most other customers.

14.2 (a) Credit terms, including credit period.

(b) Credit standards for offering credit to existing and new customers, including credit risk screening.

(c) Credit collection policy, including use of cash discounts and collection agents.

(d) Credit reporting.

14.3 Carrying costs include the cost of storing, insuring and maintaining stocks as well as the lost interest tied

up in holding such assets.

Ordering costs include not only the obvious administrative cost of making regular orders, but also the

costs associated with running out of stock (lost orders, goodwill, etc.). These two types of cost are traded

APR 1.0256

365>16

1 78%

Interest 2.5>1100 2.52 2.56%

2.5

100 2.5

365

46 30

58.5%

Cost of discount

Discount %

100 discount %

365

Final date discount date

CHAPTER 14

CFAI_Z01.QXD 10/26/05 5:42 PM Page 683

.

684 Appendix A Solutions to self-assessment activities

off to find the optimum order quantity, given by the formula:

where C is the cost of placing an order, A is the annual stock usage and H is the cost of holding a unit of stock.

14.4 The main motives for holding cash are:

(a) to act as a buffer to ensure that transactions can be paid for (transactions motive);

(b) to cater for unanticipated cash outflows (precautionary motive);

(c) to permit companies to take advantage of profitable opportunities (speculative motive);

(d) to take advantage of ‘free’ banking services for firms with positive cash balances (compensation bal-

ances motive).

14.5 With interest at 12% p.a., the EOQ formula becomes:

EOQ

B

2 £2,400,000 £25

0.12

£10,000

EOQ

B

2AC

H

CHAPTER 15

15.1 Trade credit results from the time lag between receiving goods and having to pay for them. For as long as

it takes the recipient of the goods to settle the account, the supplier is effectively financing the client. Hence,

each order and delivery triggers a ‘spontaneous’ supply of finance.

15.2 Effective annual interest:

15.3 The mnemonic PARTS is sometimes used to help remember this:

Purpose: Is the purpose of the loan acceptable to the bank?

Amount: Has the financial requirement been correctly specified (e.g. will additional working capital be

required later)?

Repayment: How will the loan be repaid? Will the funds generate sufficient income to enable repayment?

Term: What is the duration of the loan?

Security: What, if any, is the proposed security?

15.4 Overdrafts are normally cheaper than term loans because:

■ They can be recalled at short, or no, notice; term loans are for agreed durations.

■ Arrangement fees are higher for a term loan.

■ With an overdraft, interest is only paid on the credit used, not the credit available.

15.5 It receives cash to pay suppliers promptly and take advantage of any early payment discounts available.

■ Growth can be financed through revenue from sales rather than through additional capital.

■ Management need not devote so much time to chasing debtors and running the sales ledger.

■ Finance is directly linked to sales. (Overdrafts are linked to the balance sheet and the security offered

by assets.)

■ If factoring is ‘without recourse’, any bad debts are no longer the firm’s problem.

15.6

Monthly payment £39,200>14 122 £816.67

Total to be repaid 1£28,000 £11,2002 £39,200

Total interest 14 10% £28,0002 £11,200

Loan 170% £40,0002 £28,000

Effective interest rate 11 0.015232

14.6

1 0.247, i.e. 24.7%.

Number of 25 day periods in a year 1365>252 14.6

Discount lost>Extra finance 11.5%>98.5%2 1.523%

CFAI_Z01.QXD 10/26/05 5:42 PM Page 684