Pike Robert, Neal Bill. Corporate finance and investment: decisions and strategy

Подождите немного. Документ загружается.

.

Chapter 22 Foreign investment decisions 655

Investing in Indonesia: at a crossroads

Indonesia’s judiciary unnerves foreign investors – again

Once more Indonesia’s notoriously corrupt courts have struck a blow to the government’s efforts

to woo foreign investors. In a reprise of its 2002 verdict against Manulife, a Canadian insurer,

Jakarta’s commercial court has declared bankrupt Prudential Life Assurance (PLA), the local unit

of Prudential, Manulife’s British rival, even though no one denies that the firm is solvent.

The judges ignored PLA’s rude health and invoked a bizarre article in the bankruptcy law

that allows a company to be declared bankrupt regardless of its financial condition if it refuses

to settle its debts. The company is alleged to owe 365.8 billion rupiah ($42.4 m) to a

Malaysian agent, Lee Boon Siong, mainly for claimed loss of future earnings. Mr Lee says that

his contract was ended nine years prematurely without good reason.

PLA has suspended its operations and is hurriedly filing an appeal with the supreme court.

The company describes the suit as baseless, but refuses to discuss it in detail. Whatever the

merits of Mr Lee’s claim and of allegations of judicial graft, the wider considerations bode ill

both for Prudential and for Indonesia’s stuttering economic recovery.

If the court-appointed administrator is able to secure access to the company’s assets, many

millions of dollars of policyholders’ money could be at risk. PLA claims that last year alone its

premiums from new policies topped 1 trillion rupiah ($11.6 m).

On the national level, the continuing legal uncertainty and accompanying endemic corrup-

tion are driving investors away in droves: Indonesia is the only country in the region recording

negative foreign direct investment. The speed with which Indonesian government ministers

and legislators rallied to support Prudential demonstrates their desperation to resolve what is

unquestionably a deep embarrassment for them. But they have only themselves to blame.

In the wake of the Manulife saga an amendment was proposed to the existing laws to

transfer the power to declare companies bankrupt from the courts to the financial regulators.

This legislation is, however, still buried in the ministry responsible for drafting legislation and

Continued

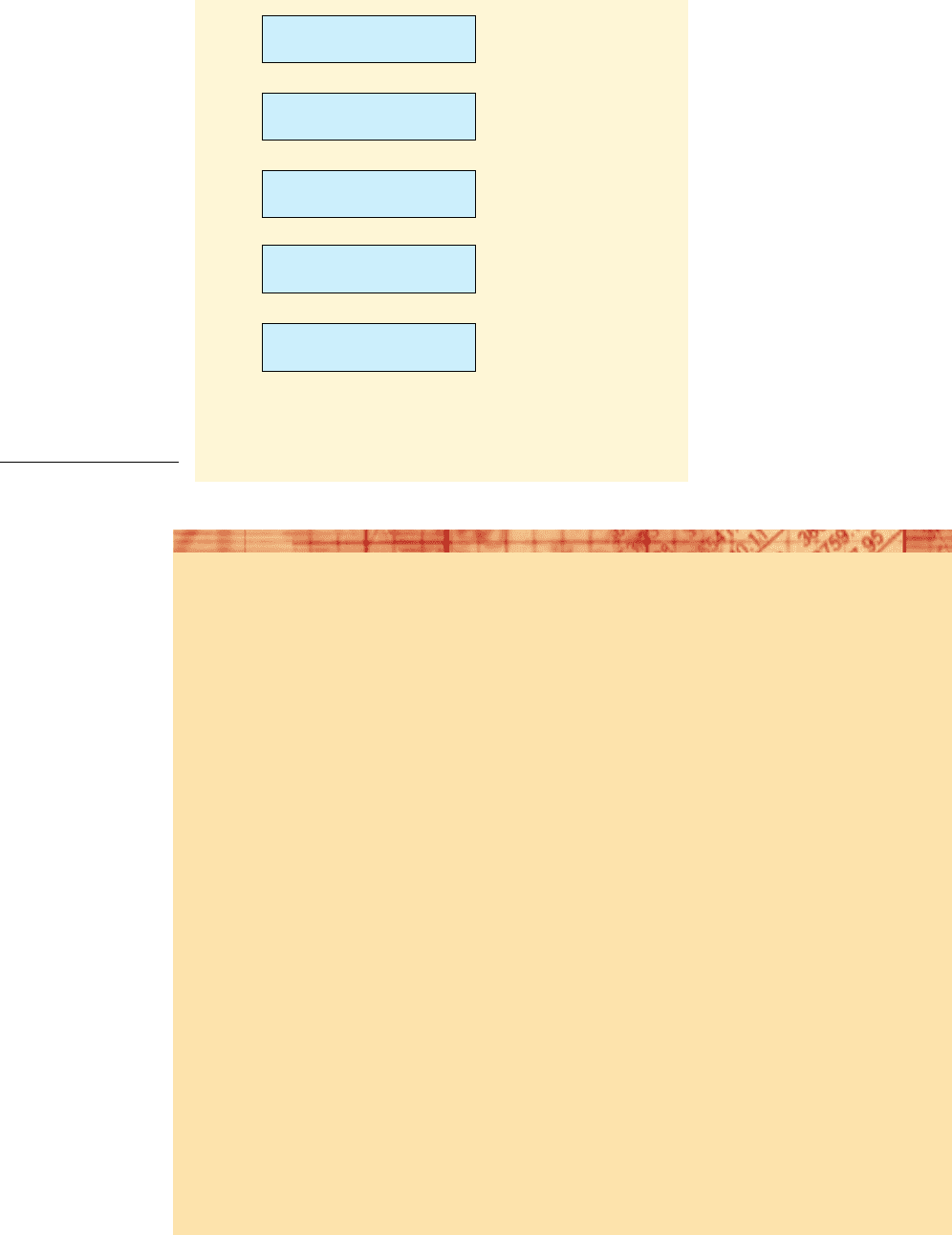

NPV of remittable after-

tax cash flows

PV of tax savings from

capital allowances

PV of tax savings from

interest deductibility

PV of subsidies

and grants

PV of spillover effects

on other activities

APV = NPV of basic project Plus/Minus PV of financing benefits, etc.

ACCEPT IF APV IS POSITIVE

APV =

+

+

+

+

Figure 22.5

A simple APV model

CFAI_C22.QXD 3/15/07 7:07 AM Page 655

.

656 Part VI International finance

This chapter has examined the strategic motivations that drive firms to enter foreign

markets, and methods of effecting entry, in particular, direct investment. Evaluating

FDI is a complex process that differs in several important respects from evaluation of

home country investment, not least the exposure to FX rate variations. As a result, FDI

evaluation is more art than science, especially as it involves so many unquantifiable

aspects such as the prevailing political mood of the host country, assessing political

and other country risks and devising appropriate safeguards. Clearly, this topic tran-

scends purely financial strategy.

Key points

■ Foreign direct investment (FDI) may be undertaken for a variety of strategic rea-

sons: for example, globalisation of component sources or meeting the threat of a

competitor already based overseas.

■ FDI is generally undertaken when exporting (with relatively high variable costs,

but low fixed costs) becomes more expensive than overseas production (with rela-

tively high fixed costs but low variable costs).

■ In principle, the evaluation of FDI is similar to the evaluation of ‘domestic’ investment.

■ In practice, FDI may be complicated by factors such as concessionary access to local

finance, difficulties in repatriating profits and differential inflation rates.

SUMMARY

Further reading

Interesting and comprehensive texts on international business strategy and operations are

Daniels and Radebaugh (2004) and Rugman et al. (1985). The texts by Eiteman et al. (2003),

Shapiro (2004) and Madura (2005) all focus more closely on multinational business finance, each

devoting several chapters to foreign investment. Special issues of Managerial Finance (Wilson,

1990; Shao, 1996) were devoted to the evaluation of overseas investment, while Holland’s con-

tribution to Firth and Keane (1986) is clear and concise. Prasad (1987) reports on a survey of

there are few signs of its being unearthed soon. Even if it were, parliament’s sloth has resulted

in such a backlog of work that legislators are unlikely to find time for the amendment in the

next six months.

Ironically, the Prudential affair has erupted just as Jakarta’s stock exchange is hitting new

highs almost daily and when government bonds are several times oversubscribed. Interest in

making money in Indonesia thus clearly exists, but mainly in ways that avoid the courts and

come with a simple exit strategy.

Source: The Economist, 8 May 2004.

Self-assessment activity 22.8

List eight ways in which MNCs can lower political risk.

(Answer in Appendix A at the back of the book)

CFAI_C22.QXD 3/15/07 7:07 AM Page 656

.

Chapter 22 Foreign investment decisions 657

MNC motivations to invest in Ireland, while Madura and Whyte (1990) discuss the diversifica-

tion benefits of foreign direct investment.

Buckley (1996) is probably the most comprehensive text on overseas capital budgeting.

The World Investment Report, published each September by UNCTAD (www.unctad.org) is a

mine of information of patterns and trends in FDI.

Excellent analyses of operating exposure can be found in Lessard and Lightstone (1998) and in

Grant and Suenen (2004).

CFAI_C22.QXD 3/15/07 7:07 AM Page 657

.

658 Part VI International finance

QUESTIONS

Questions with a coloured number have solution in Appendix B on page 720.

1 The USD vs. GBP exchange rate is $1.50 vs. A UK MNC operating in the US plans to sell goods worth $100

million at today’s prices to US customers. Show that its GBP revenue in real terms will not be affected if PPP

applies under each of the following conditions:

(i) UK and US inflation at 5% p.a.

(ii) UK inflation 5%, US inflation 2%.

(iii) UK inflation 2%, US inflation 5%.

2 OJ Limited is a supplier of leather goods to retailers in the UK and other Western European countries. The

company is considering entering into a joint venture with a manufacturer in South America. The two compa-

nies will each own 50 per cent of the limited liability company JV (SA) and will share profits equally. £450,000

of the initial capital is being provided by OJ Limited, and the equivalent in South American dollars (SA$) is

being provided by the foreign partner. The managers of the joint venture expect the following net operating

cash flows which are in nominal terms:

Predicted future rates

SA$ 000 of exchange to £ sterling

Year 1 4,250 10

Year 2 6,500 15

Year 3 8,350 21

For tax reasons, JV (SA), the company to be formed specifically for the joint venture, will be registered in

South America.

Ignore taxation in your calculations.

Assume you are a financial adviser retained by OJ Limited to advise on the proposed joint venture.

Required

(a) Calculate the NPV of the project under the two assumptions explained below. Use a discount rate of 16

per cent for both assumptions, and express your answer in sterling.

Assumption 1: The South American country has exchange controls which prohibit the payment of divi-

dends above 50 per cent of the annual cash flows for the first three years of the project. The

accumulated balance can be repatriated at the end of the third year.

Assumption 2: The government of the South American country is considering removing exchange controls

and restrictions on repatriation of profits. If this happens, all cash flows will be distributed

as dividends to the partner companies at the end of each year.

(b) Comment briefly on whether or not the joint venture should proceed based solely on these calculations.

(CIMA)

3 PG plc is considering investing in a new project in Canada that will have a life of four years. Initial investment

is C$150,000, including working capital. The net cash flows that the project will generate are C$60,000 per

annum for years 1, 2 and 3 and C$45,000 in year 4. The terminal value of the project is estimated at C$50,000,

net of tax.

The current spot rate for C$ against the pound sterling is 1.70. Economic forecasters expect the pound to

strengthen against the Canadian dollar by 5 per cent per annum over the next four years. The company eval-

uates UK projects of similar risk at 14 per cent per annum.

Required

Calculate the NPV of the Canadian project using the following two methods:

(i) Convert the foreign currency cash flows into sterling and discount at a sterling discount rate.

(ii) Discount the cash flows in C$ using an adjusted discount rate that incorporates the 12-month forecast spot rate.

(CIMA)

£1.

CFAI_C22.QXD 3/15/07 7:07 AM Page 658

.

Chapter 22 Foreign investment decisions 659

4

Kay plc, a UK-based chemical firm but with plants in Germany and the Netherlands, manufactures man-made

fibres. It would like to expand its exports to Latin America and the country of Copacabana, in particular.

However, Copacabana is unable to pay in Western currency and its own currency, the poncho, is subject to

rapid depreciation, due to high local inflation. One solution to this problem is an arrangement whereby Kay

manages and pays for the construction of a fibres plant and accepts payment in the form of the finished prod-

uct of fibres (a so-called buyback).

Construction will take two years and expenditures can be treated as four equal half-yearly payments of

10 million ponchos at today’s prices, beginning in six months’ time. The plant will have a 15-year life, but will

attract no local investment incentives. The inflation rate in Copacabana is expected to average 20 per cent p.a.

over the construction period. The current exchange rate of the poncho vs. sterling is 1:4 and inflation in the

UK has recently averaged 5 per cent.

The fibres produced and taken as payment can be traded on world markets, probably in Europe, where the

present price is ;500 per tonne. Kay is not prepared to accept payment in this way for more than five years. The

expected production rate of the plant is 20,000 tonnes per annum, and Kay would take 40 per cent of this in

payment.

The current euro vs. sterling rate is per £1, and sterling is expected to depreciate by 5 per cent per

annum prior to joining the euro bloc.

Further information

■ The project will be financed by equity only.

■ Kay is at present debt-free. Its shareholders seek a return of 20 per cent p.a. for projects of this degree of risk.

■ Profits from the operation will be taxed at 30 per cent when repatriated to the UK. Assume no delay in tax

payment. All development costs will qualify for UK tax relief.

■ Any losses will be carried forward to qualify for tax relief.

■ There will be no tax liability in Copacabana.

Required

Determine whether Kay should undertake this project.

5 Brighteyes plc manufactures medical and optical equipment for both domestic and export sale. It is investigat-

ing the construction of a manufacturing plant in Lastonia, a country in the former Soviet bloc. Initial discussions

with the Ministry of Economic Development in Lastonia have met with favourable response, providing the proj-

ect can generate a 10 per cent pre-tax return. Shareholders look for a return of 15 per cent in real terms.

The investment will be partly import-substituting and partly export-based, selling to neighbouring coun-

tries. The project has been offered a local tax holiday, exempting it from all taxes for the first ten years, except

for cash remittances, for which a 20 per cent withholding tax will apply. Modern factory premises on an indus-

trial estate with convenient road and rail links have been offered at a reasonable rent.

The initial investment will be £10 million in plant, machinery and set-up costs, all payable in sterling by

the parent company. Additional funds will come from a bank loan of 20 million latts, the local currency

negotiated with a local bank, at a concessionary rate of interest of 10 per cent p.a. This will be

used to finance working capital. Operating cash flows, the basis for calculating tax, are estimated at L10 mil-

lion in Year 1 and L22 million thereafter until year 5.

The whole of the parent’s earnings after payment of local interest and taxation will be repatriated to the

UK. The Lastonia withholding tax is to be allowed as a deduction before calculating the UK Corporation Tax,

currently at the rate of 30 per cent. All transfers can be treated as occurring on the final day of each account-

ing period, when all taxes become due.

The new venture is expected to ‘cannibalise’ exports that Brighteyes would otherwise have made to neigh-

bouring countries, resulting in post-tax cash flow losses of million in each of years 2 to 5. For planning

purposes, year 5 is the cut-off year, when the realisable value of the plant and equipment is estimated at

L24 million. The working capital will be realised, subject to losses of L2 million on stocks and L2 million on

debtors. Funds realised will be used to repay the local borrowing, and the balance transferred to the UK with-

out further tax penalty or restriction.

The exchange rate is forecast to remain at L4 vs. until year 2, when the Latt is expected to fall to L5 vs.

Required

(i) Is the project acceptable from the Lastonian Ministry’s point of view?

(ii) Is it worthwhile from the viewpoint of the foreign subsidiary?

(iii) Does it create wealth for Brighteyes’ shareholders?

£1.£1

£0.5

14 latts £12,

;1.60

CFAI_C22.QXD 3/15/07 7:07 AM Page 659

.

660 Part VI International finance

6 Palmerston Plc operates in both the UK and Germany. In attempting to assess its economic exposure, it

compiles the following data:

■ UK sales are influenced by the euro’s value as it faces competition from German suppliers. It forecasts

annual UK sales based on three possible scenarios:

Euro:sterling exchange rate Revenue from UK business

1.65:1

1.60:1

1.55:1

■ Revenues from sales made in Germany are expected to be

■ Expected cost of goods sold is from UK materials purchases, and ;200 m from purchases in

Germany.

■ Estimated cash fixed operating expenses are

■ Variable operating expenses are estimated at 20 per cent of total sales value including German sales trans-

lated into sterling).

■ Palmerston is financed entirely by equity and shareholders require a return of 15 per cent p.a.

Required

(i) Construct a forecast cash flow statement for Palmerston under each scenario.

(ii) Value Palmerston’s equity under each scenario, assuming a ten-year operating time horizon. Ignore

terminal values.

(iii) Suggest how Palmerston might restructure its operations to lower its sensitivity to exchange rate

movements.

Ignore taxation.

7 A professional accountancy institute in the UK is evaluating an investment project overseas in Eastasia, a

politically stable country. The project involves the establishment of a training school to offer courses on inter-

national accounting and management topics. It will cost an initial 2.5 million Eastasian dollars (EA$) and it

is expected to earn post-tax cash flows as follows:

Year 1 2 3 4

Cashflow (EA$000) 750 950 1,250 1,350

The following information is available:

■ The expected inflation rate in Eastasia is 3 per cent a year.

■ Real interest rates in the two countries are the same. They are expected to remain the same for the period

of the project.

■ The current spot rate is EA$2 per sterling.

■ The risk-free rate of interest in Eastasia is 7 per cent and in the UK 9 per cent.

■ The company requires a sterling return from this project of 16 per cent. (CIMA)

Required

Calculate the sterling net present value of the project using both the following methods:

(a) by discounting annual cash flows in sterling,

(b) by discounting annual cash flows in Eastasian $.

£1

£50 m p.a.

£120 m p.a.

£120 m p.a.

£220 m

£215 m

£200 m

Inspect the Report and Accounts for a company of your choice, to examine how its international profile of activities

has changed over the years. You may find difficulty in obtaining a full set of accounts reaching very far back in time,

but examination of a sample should give you a flavour of the company’s policy regarding internationalisation.

Look also at the chairman’s statements to glean an indication of the importance attached to overseas operations

in the company’s strategy.

Practical assignment

CFAI_C22.QXD 3/15/07 7:07 AM Page 660

.

Review and behavioural finance

23

Market inefficiencies prove we’re only human

Investors have an insatiable appetite for information.

Company announcements, macro economic variables

and the latest political news are just some of what

they digest on a daily basis. It is almost impossible for

investors to assimilate and process the information

tidal wave of data that faces them every day. But this

does not have to be a problem for market efficiency.

Classical economics tells us that market efficiency is

not driven by the activities of one participant but

rather the overall effect of many self-serving individuals

– Adam Smith’s invisible hand.

More information should increase transparency and

promote efficiency. However, evidence suggests this is

not happening in the stock market. Factors such as

cheap valuations or earnings upgrades turn out to have

predictive power for future share price movements.

This runs counter to the concept of efficient markets

where all information should already be reflected in

the price.

An increasingly persuasive explanation for market

inefficiency comes from the field of behavioural

finance. Not only do individuals make mistakes

when analysing masses of data but, more funda-

mentally, they all seem to make the same mistakes.

Errors are therefore magnified rather than negated

by the combined efforts of many market partici-

pants. Faced with complex financial decisions,

investors often employ heuristics, or rules-of-thumb,

when making decisions. Heuristics can be useful in

everyday life, but these inbuilt tendencies are too

blunt a tool for the complex environment of finan-

cial decision-making.

Source: Based on article by James Hand and Greg Davies, Financial Times,

25 October 2004, p. 6.

CFAI_C23.QXD 10/28/05 10:26 AM Page 661

.

Most readers will be familiar with the popular board game Monopoly. There is more

than a passing resemblance between this game and corporate finance. Both are about

maximising investors’ wealth in risky environments, making investment decisions

with uncertain payoffs, raising finance and managing cash flow. Players and managers

must stick to the rules of governance and seek to devise appropriate investment, financ-

ing and trading strategies to gain competitive advantage. While rational analysis and

sound judgement are essential, there remains room for sentiment, psychology, fun, and,

to make the game interesting, a generous portion of luck!

Some aspects of finance, particularly routine finance decisions, can be opera-

tionalised through clear rules and procedures. But good managers look for something

more than rules and procedures. They seek to understand:

1 Why managers behave as they do.

2 Why firms behave as they do.

3 Why markets, in particular financial markets, behave as they do.

Theories of finance provide explanations for the behaviour of individuals, firms

and markets. The better the theory, the better we understand how finance operates.

Throughout the book we have sought to combine the ‘why’ with the ‘how’ in the the-

ory and practice of finance. By way of revision, we will introduce readers to the main

financial principles covered.

■ Understanding individual behaviour

To understand how organisations function we must first understand individual

behaviour. There are many models of human behaviour (e.g. sociological, psycholog-

ical and political); we shall restrict our examination to two models of most relevance

to finance.

The first is the traditional economic model of human behaviour. Here the manager

is seen as a short-run wealth maximiser. The model is a useful starting point in study-

ing finance because it offers a simple approach to model building, using only the pur-

suit of wealth as a goal. Much of the argument underlying the theories discussed in

this book is based on this model. But we all know that this is a poor explanation of

many aspects of human behaviour. For many people, and in many situations, money

may not come before morality, honesty, love, altruism or having fun. As the song said

‘Money can’t buy me love’.

This leads us to develop a more realistic model of human behaviour which Jensen

and Meckling (1994) term the resourceful, evaluative, maximising model (or REMM).

This model assumes that people are resourceful, self-interested maximisers, but rejects

the notion that they are only interested in making money. They also care about respect,

power, quality of life, love and the welfare of others. Individuals respond creatively to

opportunities presented, seeking out opportunities, evaluating their likely outcomes,

and working to loosen constraints on their actions.

662 Chapter 23 Review and behavioural finance

23.1 INTRODUCTION

This book has presented the theory and practice of modern financial management. This

final chapter summarises the main principles of finance underpinning the book and

develops several key areas, specifically those relating to behavioural finance.

23.2 REVIEW OF MAIN PRINCIPLES IN FINANCE

CFAI_C23.QXD 10/28/05 10:26 AM Page 662

.

Neither of the above models place much emphasis on psychological factors in

human information processing and decision-making. This growing area of finance,

termed behavioural finance, is discussed in a later section.

To sum up the foregoing discussion, money is not the only, or even the most impor-

tant, thing in life. But when all else is equal, we act in a rational economic manner,

choosing the course of action that most benefits us financially. Two fundamental con-

cepts naturally follow.

Managers should only consider present and future costs and benefits

in making decisions

This is the principle of incrementalism – only the additional costs or benefits resulting

from a choice of action should be considered. For example, expenditures already incurred

are not relevant to the decision in hand; they are sunk costs.

Choices often involve trade-offs, denying the possibility of other alternatives. The

opportunity cost of making one decision is the difference between that choice and the

next best alternative.

Most managers are risk averse

Most managers are risk averse; given two investments offering the same return, they

would choose the one with least risk. Unlike the risk-seeker or gambler, most managers

try to avoid unnecessary risks. Risk aversion is a measure of a manager’s willingness

to pay to reduce exposure to risk. This could be in the form of insurance or other ‘hedg-

ing’ devices. Alternatively, it could be by preferring a lower-return investment because

it also has a lower risk.

In business, risk and the expected return are usually related. Rational managers do

not look for more risk unless the likely benefits are commensurately greater. This is the

principle of risk aversion. One way in which investors can reduce risk is by spreading

their capital across a range (portfolio) of investments. This is the principle of

diversification, or not putting all your eggs in one basket. However, the key to risk

management should not simply be to reduce it, but to take decisions in a risky business

environment that create value.

■ Understanding corporate behaviour

A firm may be viewed as a collection of individuals and resources. More precisely, it is

a set of contracts that bind individuals together, each with his or her own interests and

goals. As we have seen, agency theory explores the relationship between the principal

(e.g. owner) and the agents responsible for taking actions on his or her behalf (e.g.

board of directors). It follows that, to understand how firms behave, we must under-

stand the nature of the contracts and monitoring procedures.

Information is not usually available to all parties in business in equal measure. For

example, the board of directors will know more about the future prospects of the busi-

ness than the shareholders, who have to rely on published information. This

information asymmetry means that the investors not only listen to the board’s rheto-

ric and confident projections, but also examine the information content in its corpo-

rate actions. This signalling effect is most commonly seen in the reaction to dividend

declaration and share dealings by the board. An increase in dividends signals that the

company is expected to be able to sustain that level of cash distribution in the future,

because it is regarded as the height of corporate financial incompetence to be forced to

cut a dividend. Similarly, when directors increase their shareholdings, the odds are

that this is favourable information (although the asymmetry factor appears here also,

insofar as share sales are not necessarily dire warnings. For example, directors could

Chapter 23 Review and behavioural finance 663

CFAI_C23.QXD 10/28/05 10:26 AM Page 663

.

664 Chapter 23 Review and behavioural finance

be selling to fund personal expenditures such as refurbishments to a country home, or

to finance a messy divorce. Both rationalisations were used by prominent directors in

2004–5.)

Value is created by investing in wealth-creating opportunities. The firm should

invest in those areas in which it has some competitive advantage, giving rise to superi-

or returns or positive net present value when cash flows are discounted at the rate of

return commensurate with the perceived level of risk. Options have value. An option

is the right, but not the obligation, to do something – usually to buy or sell assets. A firm

will only exercise its right if it adds value to the business. This time, the more risky the

option, the more valuable it is, because only the ‘good news’ is taken up. The convert-

ible loan stock instrument is one example of options in business. ‘Convertibles’ begin

as a loan, but at some point may be converted into ordinary shares of equity. The

investor can decide at that point whether to take up the option to convert, and this

option has a value.

Financing decisions that change the capital structure do not affect the value of the

firm – at least in perfect markets. Value is independent of capital structure just as long

as the total cash flows of the firm’s assets are unaffected. In practice this is unlikely to

be the case because borrowing creates a valuable tax shield for the firm.

■ Understanding how markets behave

To make sound financial decisions consistently, we need to understand how financial

markets operate.

Money has a time-value

Fundamental to the study of financial management is the principle of the time-value of

money. Put simply, we cannot add current and future money together in a meaningful

way without first converting into a common currency. This currency can be either pres-

ent (i.e. today’s) value or future value. The value of money changes with time because

it has an alternative use (opportunity cost): it can be invested somewhere in financial

markets to earn a rate of interest.

Non-diversifiable risk matters

The only risk that really matters is that which cannot be diversified away. The Capital

Asset Pricing Model argues that the required return on an asset is commensurate to the

amount of non-diversifiable risk. While some may question the validity of this model,

it is still probably the best we have and this distinction between diversifiable and non-

diversifiable risk is important.

Capital markets are efficient

In an efficient market, the prices of financial assets, such as those of stocks and shares,

reflect all available information and adjust quickly to new information. There are degrees

of market efficiency and, in Chapter 2, we considered the efficiency of the London

Stock Exchange together with its implications. Many of the theories discussed in the

book assume that capital markets are reasonably efficient in reflecting all available

information.

The exact form of market efficiency in financial markets in developed and develop-

ing countries has been the subject of much debate and research. For major European

stock markets, however, the consensus is that they exhibit efficiency in both weak form

(i.e. share prices contain all past data and superior returns cannot be consistently

achieved from trading rules based on past stock market data) and semi-strong form

(i.e. share prices contain all publicly available information, and superior returns can-

not consistently be achieved from trading rules based on such information).

CFAI_C23.QXD 10/28/05 10:26 AM Page 664