Pike Robert, Neal Bill. Corporate finance and investment: decisions and strategy

Подождите немного. Документ загружается.

.

Questions with a coloured numbers have solutions in Appendix B on page 697.

1 The returns on investment in two projects, X and Y, have standard deviations of 30 per cent and 45 per cent

respectively. The correlation coefficient between the returns on the two investments is 0.2. What is the stan-

dard deviation of a portfolio containing equal proportions of the two investments?

2 Determine the risk-minimising portfolios for the following two asset portfolios.

(i)

(ii)

(iii)

(iv)

3 Tomb-zapper plc manufactures computer video games. It is considering whether to expand production at its

existing site in ‘Silicon Glen’ in Scotland, or to start production in a ‘greenfield site’ in China, where labour

costs are considerably lower than in Europe. The IRRs for each project depend on average rates of growth in

the world economy over the ten-year life span of the project. These are expected to be:

World growth Probability IRR China IRR Scotland

Rapid 0.3 50% 10%

Stable 0.4 25% 15%

Slow 0.3 0% 16%

Tomb-zapper wants to exploit the less than perfect correlation between the returns from the two projects,

without over-committing itself to the China investment.

Required

(a) What is the expected return and standard deviation of return for each separate project?

(b) Determine the expected return and standard deviation of an expansion programme that involves 25 per

cent of available funds in China and 75 per cent in the Scottish location.

4 Nissota, a Japanese-based car manufacturer, is evaluating two overseas locations for a proposed expansion of

production facilities at a site in Ireland and another on Humberside. The likely future return from investment

in each site depends to a great extent on future economic conditions. Three scenarios are postulated, and the

internal rate of return from each investment is computed under each scenario. The returns with their esti-

mated probabilities are shown below:

Internal rate of return (%)

Probability Ireland Humberside

0.3 20 10

0.3 10 30

0.4 15 20

There is zero correlation between the returns from the two sites.

Required

(a) Calculate the expected value of the IRR and the standard deviation of the return from investment in each

location.

(b) What would be the expected return and the standard deviation of the following split investment strate-

gies:

(i) committing 50 per cent of available funds to the site in Ireland and 50 per cent to Humberside?

(ii) committing 75 per cent of funds to the site in Ireland and 25 per cent to the Humberside site?

ER

A

11%; ER

B

5%; s

A

15%; s

B

1%; r

AB

0

ER

A

11%; ER

B

5%; s

A

15%; s

B

1%; r

AB

1

2

ER

A

20%; ER

B

12%; s

A

12%; s

B

6%; r

AB

1

2

ER

A

8%; ER

B

10%; s

A

3%; s

B

7%; r

AB

1

Chapter 9 Relationships between investments: portfolio theory 235

QUESTIONS

CFAI_C09.QXD 10/28/05 4:28 PM Page 235

.

5 The management of Gawain plc is evaluating two projects whose returns depend on the future state of the

economy as shown below:

Probability (%) (%)

0.3 27 35

0.4 18 15

0.3 5 20

The project (or projects) accepted would double the size of Gawain.

Required

(a) Explain how a portfolio should be constructed to produce an expected return of 20 per cent.

(b) Calculate the correlation between projects A and B, and assess the degree of risk of the portfolio in (a).

(c) Gawain’s existing activities have a standard deviation of 10 per cent. How does the addition of the port-

folio analysed in (a) and (b) affect risk?

IRR

B

IRR

A

236 Part III Investment risk and return

Select a company with a reasonably wide portfolio of activities. Such companies do not always give segmental

earnings figures, but they usually divulge sales figures for their component activities. By looking at the annual

reports for three or four years, you can obtain a series of annual sales figures for each activity.

Assess the degree of past volatility of the sales of each sub-unit and their degree of inter-correlation. Also, see

whether you can assess the extent of the correlation between each segment and the overall enterprise. How well

diversified does your selected company appear to be? What qualifications should you make in your analysis?

Practical assignment

CFAI_C09.QXD 10/28/05 4:28 PM Page 236

.

Setting the risk premium: the Capital Asset

Pricing Model

10

Learning objectives

This chapter deals with the rate of return required by shareholders of an all-equity financed compa-

ny, building on portfolio theory. Its specific aims are:

■ To explain what type of risk is relevant for valuing capital assets.

■ To explain what a ‘Beta coefficient’ is.

■ To determine the appropriate risk premium to incorporate into a discount rate, whether for

investment in securities or in capital projects.

■ To examine the case for corporate diversification.

■ To examine some criticisms of the CAPM.

An understanding of the significance of Beta coefficients is particularly important in appreciating

how financial managers should view risk.

Target practice does not make perfect

Efficient capital markets should generate an upward-

sloping risk-return frontier on which all securities

locate – the higher the risk, the higher the required

return. The Capital Asset Pricing Model (CAPM) explains

how great a premium is required for specified risks.

Although companies acknowledge the need to discount

returns expected from risky activities at higher rates,

surveys conducted by the Confederation of British

Industry (CBI) reveal some alarming information about

how firms approach capital investment decisions.

In 1998, the CBI surveyed 326 firms with turnovers

above and with capital expenditures rang-

ing from rather less than to well over

Two points stood out:

1 Firms tended to apply much higher rates than

appear warranted by theoretical best practice, with

those using IRR setting higher hurdle rates than

users of the NPV method.

2 Firms tend not to adjust their hurdle rates when

inflation rates change. Only 60 per cent of respon-

dents conducted a regular review of hurdle rates, and

there was little evidence that targets had fallen since

the previous study in 1994, despite lower inflation.

Setting too high a cut-off rate for investment proj-

ects carries two dangers. First, it may curtail the volume

of capital expenditure to the detriment of business

growth. Second, setting too high a target may lead to

over-investment in high risk, speculative projects

(albeit potentially lucrative ones) at the expense of

more secure ‘bread and butter’ capital projects.

Source: Target Practice, Confederation of British Industry, 1998.

£25 million.

£1 million

£20 million

CFAI_C10.QXD 3/15/07 7:27 AM Page 237

.

238 Part III Investment risk and return

10.1 INTRODUCTION

In Chapters 8 and 9, we examined various methods of handling risk and uncertainty in

project appraisal, ranging from sensitivity analysis to diversification to exploit the less

than perfect correlation between the returns from risky investments. Most of these

approaches aim to identify the sources and extent of project risk and to assess whether

the expected returns sufficiently compensate investors for bearing the risk. Utility the-

ory suggests that, as risk increases, rational risk-averse people require higher returns,

justifying the common practice of adjusting discount rates for risk. However, none of

these approaches offers an explicit guide to measuring the precise reward investors

should seek for incurring a particular level of risk.

The CAPM is a theory originally devised by Sharpe (1964) to explain how the cap-

ital market sets share prices. It now provides the infrastructure of much of modern

financial theory and research and offers important insights into measuring risk and

setting risk premiums. In particular, it shows how the study of security prices can help

in assessing required rates of return on investment projects. However, as we shall see,

the CAPM has not gone unchallenged.

10.2 SECURITY VALUATION AND DISCOUNT RATES

Asset value is governed by two factors – the stream of expected benefits from holding

the asset and their ‘quality’, or likely variability. For example, the value of a single-

project company is assessed by discounting future project cash flows at a discount rate

reflecting their risk. The value, of a company newly formed by issuing one million

shares to exploit a one-year project offering a single net cash flow of at a

25 per cent discount rate, is:

This suggests a market price per share of This would be the

value established by an efficient capital market taking account of all known informa-

tion about the company’s future prospects.

Sometimes, the ‘correct’ discount rate is unclear to the firm. A major contribution of

the CAPM is to explain how discount rates are established and hence how securities

are valued. However, from the capital market value of a company, we can ‘work back-

wards’ to infer what discount rate underlies the market price. In the example, if we

observe a market price of this suggests a required return of 25 per cent.

By implication, if the market sets a value on a security that implies a particular dis-

count rate, it is reasonable to conclude that any further activity of similar risk to current

operations should offer at least the same rate. This argument depends critically on

market prices being unbiased indicators of the intrinsic worth of companies, i.e. that

the Efficient Markets Hypothesis applies.

Any discount rate is an amalgam of three components:

1 Allowance for the time value of money – the compensation required by investors

for having to wait for their payments.

2 Allowance for price level changes – the additional return required to compensate

for the impact of inflation on the real value of capital.

3 Allowance for risk – the promised reward that provides the incentive for investors

to expose their capital to risk.

Ignoring expected inflation (or assuming that it is ‘correctly’ built into the structure

of interest rates), discount rates have two components – the rate of return required on

totally risk-free assets, such as government securities, and a risk premium.

£8

1£8 m>1 m shares2 £8.

V

o

£10 m

11.252

£8 m

£10 million,

V

o

,

CFAI_C10.QXD 3/15/07 7:27 AM Page 238

.

Chapter 10 Setting the risk premium: the Capital Asset Pricing Model 239

Table 10.1

The annual TSRs on

Pilkington shares

Year Return (%) Year Return (%)

1994–5 1999–00

1995–6 2000–1

1996–7 2001–2

1997–8 2002–3

1998–9 2003–4

Arithmetic mean* 4.8%

Standard deviation 42.7%

*Note: Strictly, the geometric mean should be used here as we are

dealing with proportions.

91.828.3

61.06.7

10.440.2

52.130.5

5.58.1

10.3 CONCEPTS OF RISK AND RETURN

In this section, we examine risk and return concepts relevant for security valuation.

■ The returns from holding shares

Investors hold securities because they hope for positive returns. Purchasers of ordinary

shares are attracted by two elements: first, the anticipated dividend(s) payable during

the holding period; and second, the expected capital gain. Taken together, these ele-

ments make up the Total Shareholder Return (TSR).

Total Shareholder Return (TSR)

In general, for any holding period, t, and company, j, the TSR is the percentage return,

from holding its shares:

where is the dividend per share paid by company j in period t, is the share price

for company j at the end of period t and is the share price for company j at the start

of period t.

To illustrate this calculation (and to show that returns are not always positive!), con-

sider the following figures for the UK-based glass-making firm Pilkington plc for

2003–4:

The percentage return over this year was:

Table 10.1 shows the annual returns and how they varied for the decade 1994–2004.

If we regard past returns on Pilkington shares as a good guide to likely future

returns and also believe that future annual returns will be randomly distributed about

the mean, we might assess the expected value of holding Pilkington shares for a given

year as 4.8 per cent. However, the actual return in any one year may diverge consid-

erably from this average, as indicated by the substantial standard deviation. The vari-

ability in return would suggest that investors should seek a high return to compensate

for this risk. However, not all risk is relevant in setting the required return. We will see

why in the next section.

5p 189p 49p2

49p

100

45p

49p

100 91.8%

Net dividend paid during 2003–4 5p per share

Share price at end of March 2004 89p

Share price at end of March 2003 49p

P

jt 1

P

jt

D

jt

R

jt

D

jt

1P

jt

P

jt 1

2

P

jt 1

100

R

jt

,

CFAI_C10.QXD 3/15/07 7:27 AM Page 239

.

240 Part III Investment risk and return

However, before this it is useful to examine an alternative and, arguably, more

meaningful measure of shareholder return. Instead of looking at annual rates of

return, we might look at the overall return over a particular period, and then convert

this into an annual equivalent rate of return. Indeed, this is the measure of TSR most

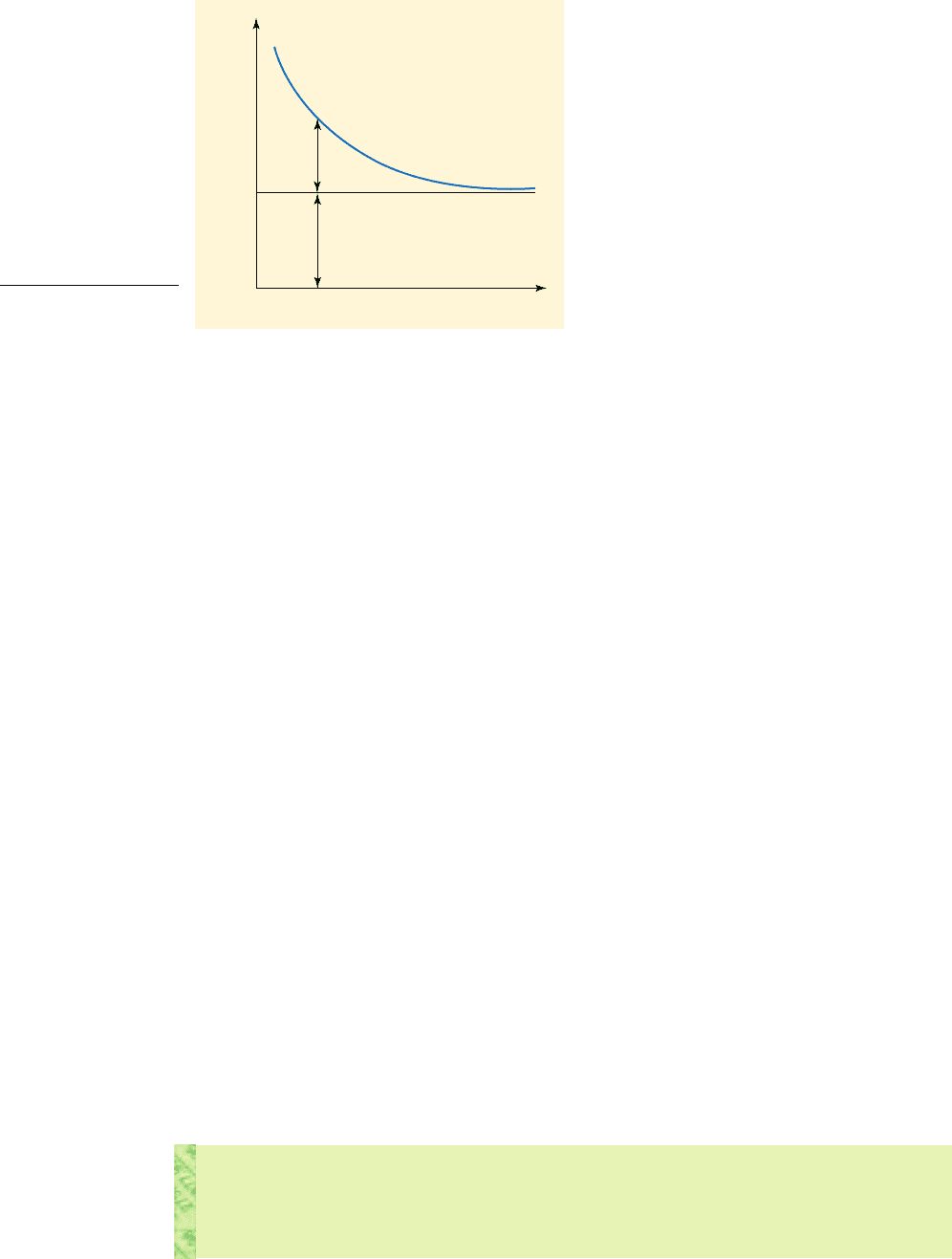

commonly used in practice. The Pilkington plc 2004 Annual Report showed its TSR

over the period March 1999–March 2004, reflecting share price movements, and

assuming re-investment of dividends. This is shown in Figure 10.1. Starting from a

base of 100, the value of the shareholders’ investment rose to 211.5, equivalent to an

annual average rate of return of about 16 per cent.

■ The risks of holding ordinary shares

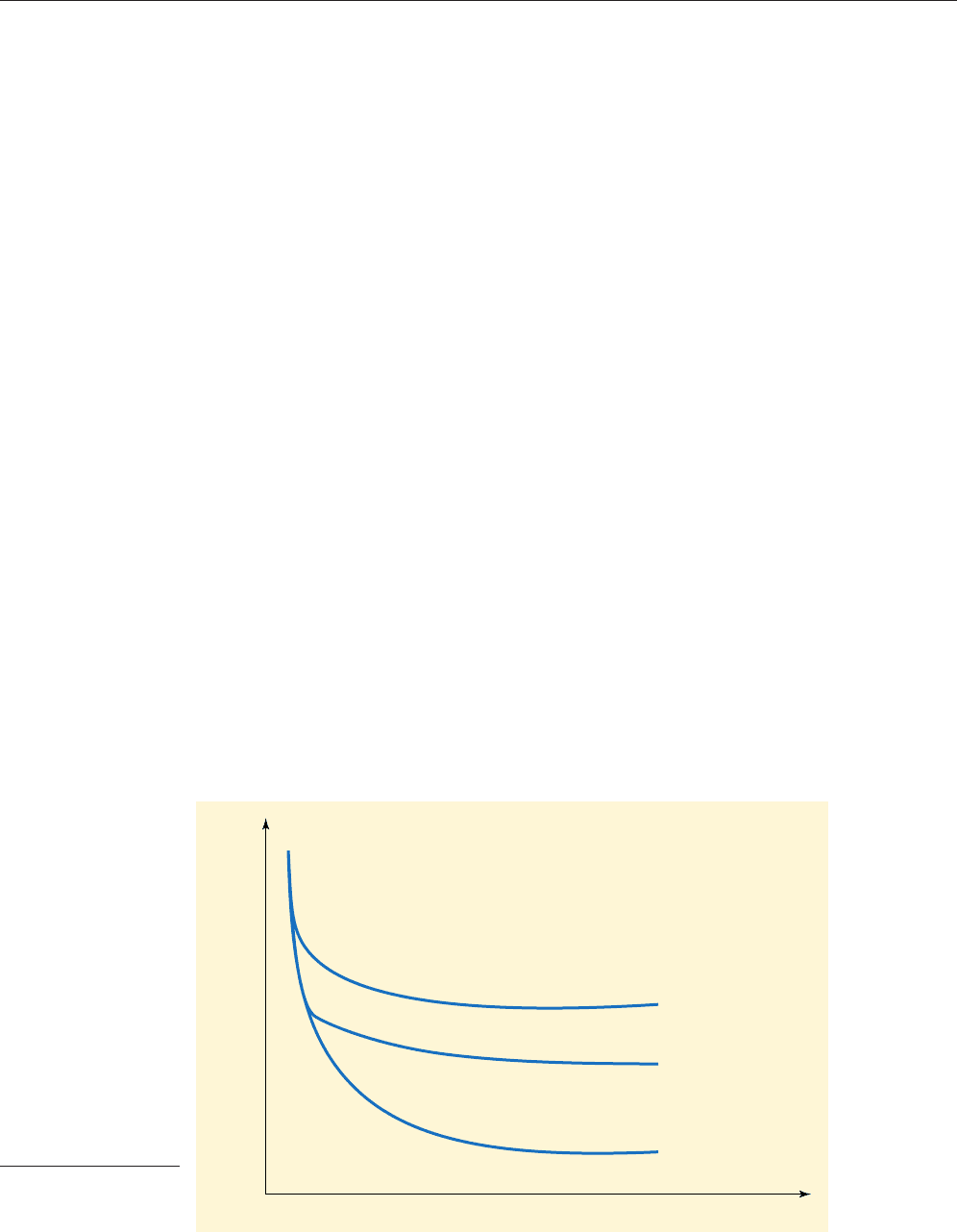

In Chapter 9, we saw the power of portfolio combination in reducing the risk of a col-

lection of investments. Risk was measured by the variance or standard deviation of the

return on the combination. This measure can also be applied to portfolios of securities,

with some remarkable results, as shown in Figure 10.2.

As the number of securities held in the portfolio increases, the overall variability of

the portfolio’s return, measured by its standard deviation, diminishes very sharply for

small portfolios, but falls more gradually for larger combinations. This reduction is

achieved because exposure to the risk of volatile securities can be offset by the inclu-

sion of low-risk securities or even ones of higher risk, so long as their returns are not

closely correlated.

March 1999

100

200

50

150

250

March 2000 March 2001 March 2002

Financial years ended

Pilkington

FTSE 250 Index

3-month moving average

TSR (re-based to 1st April 1999)

March 2003 March 2004

Figure 10.1 Total Shareholder Return (TSR) 5-year graph 1999–2004 (Covering the period from 1st April 1999

to 31st March 2004)

Self-assessment activity 10.1

Determine the TSR for the year 200X in the following case:

■ Share price January 1st:

■ Share price December 31st:

■ Interim dividend paid: per share

■ Final dividend paid: per share

(Answer in Appendix A at the back of the book)

£0.065

£0.035

£2.37

£2.20

Source

: Pilkington plc, Annual Report and Accounts 2004.

CFAI_C10.QXD 3/15/07 7:28 AM Page 240

.

Chapter 10 Setting the risk premium: the Capital Asset Pricing Model 241

■

Specific and systematic risk

Not all the risk of individual securities is relevant for assessing the risk of a portfolio of

risky shares. The total risk of securities (and also of portfolios) has two components:

1 Specific risk: the variability in return due to factors unique to the individual firm.

2 Systematic risk: the variability in return due to dependence on factors that influence

the return on all securities traded in the market.

Specific risk refers to the expected impact on sales and earnings of random events –

industrial relations problems, equipment failure, R&D achievements etc. In a portfolio

of shares, such factors tend to cancel out as the number of securities included increases.

Systematic risk refers to the impact of movements in the macroeconomy, such as

fiscal changes, swings in exchange rates and interest rate movements, all of which

cause reactions in security markets. These are captured in the movement of an index

reflecting security prices in general, such as the FTSE in the UK or the DAX index in

Germany. No firm is entirely insulated from these factors, and even portfolio diversi-

fication cannot provide total protection. Because these factors affect all firms in the

market, such risk is often called ‘market-related’ (or just ‘market’) risk.

Returning to Figure 10.2, we see that the reduction in the total risk of a portfolio is

achieved by gradual elimination of the risks unique to individual companies, leaving

an irreducible, undiversifiable, risk floor. The extent to which specific risk declines for

a portfolio comprising N equally-weighted and randomly-selected securities is also

shown in Table 10.2.

Substantial reductions in specific risk can be achieved with quite small portfolios,

and the main scope for risk reduction is achieved with a portfolio of around 30 securi-

ties. To eliminate unique risk totally would involve holding a vast portfolio comprising

all the securities traded in the market. This construct, called the ‘market portfolio’, has

a pivotal role in the CAPM, but for the individual investor, it is neither practicable nor

cost-effective, in view of the dealing fees required to construct and manage it. However,

since relatively small portfolios can capture the lion’s share of diversification benefits,

it is only a minor simplification to use a well-diversified portfolio as a proxy for the

overall market, such as the FTSE-100, which covers approximately 80 per cent of the

market capitalisation of all UK quoted companies (www.ftse.com).

Total risk

Specific

risk

Market

risk

Risk of portfolio

(Standard deviation of return)

Number of securities in portfolio

0

Figure 10.2

Specific vs. market risk

of a portfolio

Self-assessment activity 10.2

How many shares would an investor have to hold in order to

totally

eliminate specific risk?

(Answer in Appendix A at the back of the book)

CFAI_C10.QXD 3/15/07 7:28 AM Page 241

.

242 Part III Investment risk and return

Table 10.2

How to remove

portfolio risk

Number of Reduction in

securities (N) specific risk (%)

10

246

472

881

16 93

32 96

64 98

500 99

Source: Fosback (1985).

■ Implications

Three major implications now follow:

1 It is clear that risk-averse investors should diversify. Yet in reality, over half of UK

investors hold just one security (usually, shares in a privatised company or a former

building society). However, the major players in capital markets, holding well over

60 per cent of all quoted UK ordinary shares, are financial institutions such as pen-

sion funds and insurance companies, which do hold highly diversified portfolios.

2 Investors should not expect rewards for bearing specific risk. Since risk unique to partic-

ular companies can be diversified away, the only relevant consideration in assess-

ing risk premiums is the risk that cannot be dispersed by portfolio formation. If

bearing unique risk was rewarded, astute investors prepared to build portfolios

would snap up securities with high levels of unique risk to diversify it away, while

still hoping to enjoy disproportionate returns. The value of such securities would

rise and the returns on them would fall until only systematic risks were rewarded.

3 Securities have varying degrees of systematic risk. Few securities exhibit patterns of

returns rising or falling exactly in line with the overall market. This is partly because

in the short term, unique random factors affect particular companies in different

ways. Yet even in the long term, when such factors tend to even out, very few secu-

rities track the market. Some appear to outperform the market by offering superior

returns and some appear to underperform it. However, performance relative to the

market should not be too hastily judged, because the returns on different securities

do not always depend on general economic factors in the same way.

For example, in an expanding economy, retail sales tend to increase sharply, but

sales in less responsive sectors like water and defence are barely altered. Share

prices of retailers usually increase quite sharply in an expanding economy, but the

share prices of water companies and armaments suppliers respond far less dramat-

ically. Retail sales are said to be ‘more highly geared to the economy’. Systematic or

market risk varies between companies, so we find different companies valued by

the market at different discount rates. Already, we begin to see that the CAPM,

based on the premise that rational investors can and do hold efficiently diversified

portfolios, may show us how these discount rates might be assessed. Clearly, we

need to measure systematic risk. This is covered in Section 10.5.

Self-assessment activity 10.3

Give three examples of systematic and unique factors that cause the returns on holding

ordinary shares to vary over time.

(Answer in Appendix A at the back of the book)

CFAI_C10.QXD 3/15/07 7:28 AM Page 242

.

Chapter 10 Setting the risk premium: the Capital Asset Pricing Model 243

10.4 THE RELATIONSHIP BETWEEN DIFFERENT EQUITY MARKETS

Investors have tended to prefer to invest in their own national stock markets, although

this is changing. Reasons for this past parochialism include:

■ relative lack of research into overseas markets and firms

■ transactions costs, especially connected with foreign exchange

■ fear of foreign exchange risk

■ legal barriers, e.g. custody regulations

■ political risk.

Several studies have shown that international diversification can generate even greater

portfolio benefits than investing in purely domestic shares. Recall that the reason that

portfolio risk reduces as the number of component shares increases was low correlation

between investments, enabling investors to reduce specific risks. However, if foreign

stock markets are less than perfectly correlated, it may be possible to lower risk below

the level of market risk that defines the floor of the risk profile relating to purely domes-

tic investment.

Indeed, studies pioneered by Solnik (1974) have shown that international markets

are not all closely correlated. Kaplanis (1997) showed that between 1990 and 1994,

London had the following cross-national correlation coefficients: USA (0.7), Germany

(0.4), Italy (0.2), Japan (0.3) and Australia (0.5). However, European markets tended to

have higher correlations, e.g. Germany/France (0.7), Netherlands/Germany (0.7),

due, presumably, to closer European integration.

Astute investors could exploit these less than perfect correlations by combining

investments in two or more markets, thus achieving a bodily shift downwards in the

risk profile. The effect is shown in Figure 10.3.

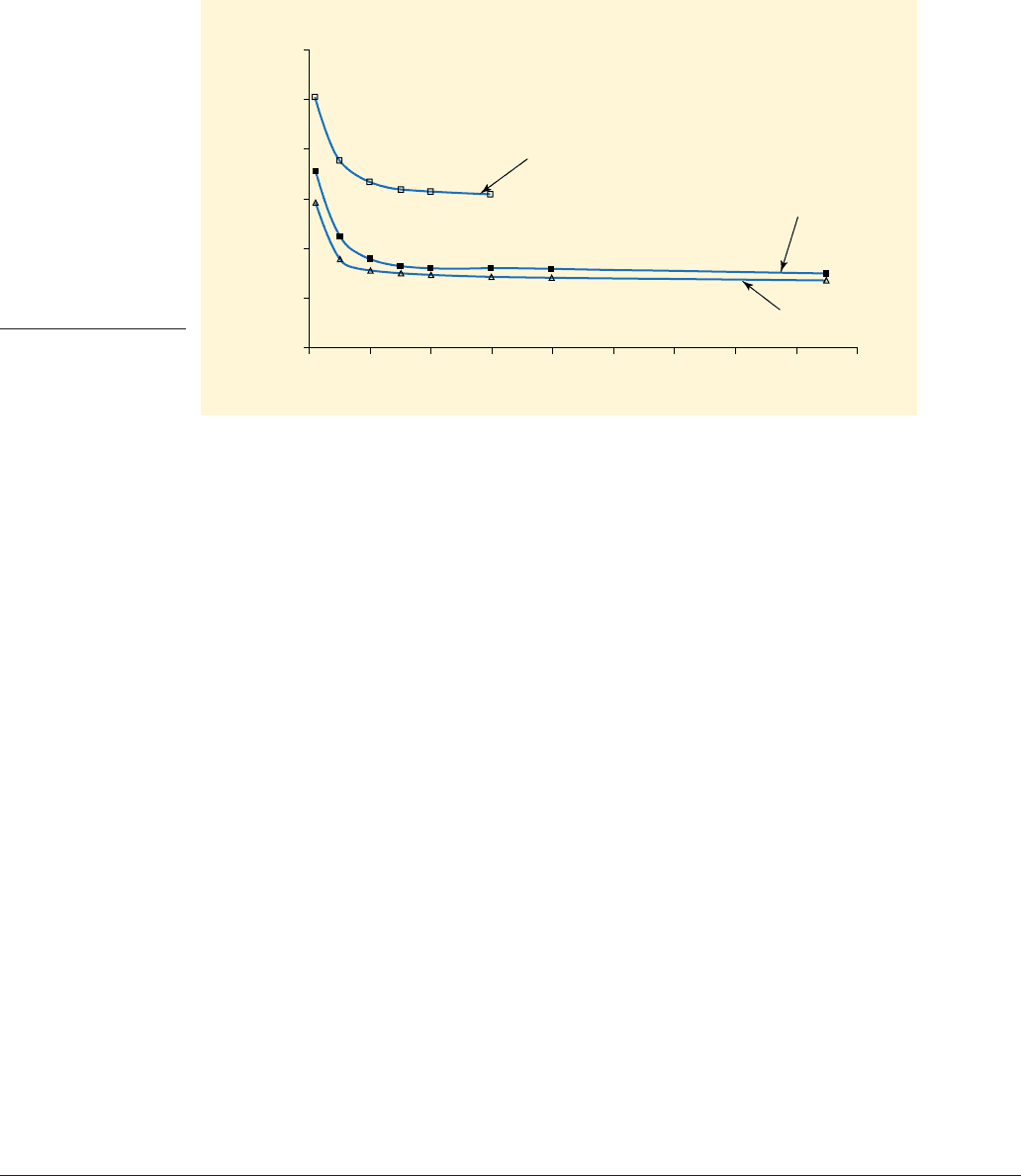

An illustration of this effect is shown in Figure 10.4. The author examined portfolio

formation on both the Polish and the London stock exchanges, and found that it

would have benefited Polish investors (but not British ones) to combine Warsaw- and

London-quoted stocks. Clearly, Warsaw stocks were more risky, possibly due to a

lower level of market efficiency, although it is interesting to observe the risk profile

flattening out at virtually the same size of portfolio for each market.

However, such opportunities may be disappearing. By the mid-1990s, the correla-

tion between changes in US and European share price movements was estimated at

Domestic portfolio

Two-country portfolio

Well-diversified

international portfolio

Total risk of portfolio

(Standard deviation of return)

Number of securities in portfolio

Figure 10.3

The effect of interna-

tional diversification

on portfolio risk

CFAI_C10.QXD 3/15/07 7:28 AM Page 243

.

244 Part III Investment risk and return

around 0.4 – Wall Street movements would ‘explain’ 40 per cent of movement in the

main European indices. But Brooks and Catao (2000) showed that rapid technical and

institutional change had raised the correlation to 0.8 by 2000.

They suggested several reasons for this convergence:

■ removal of controls on capital movements.

■ more efficient trading systems.

■ greater cross-border trading volumes.

■ more large companies obtaining listings on several markets.

■ more cross-border mergers and acquisitions with foreign activities accounting for

higher proportions of company profits.

■ easier access to information on foreign firms via the internet.

Due to these changes, equity markets have become more integrated, so that changes in

prices in one market are more easily and quickly transmitted to others, e.g. good news

for US banking shares is increasingly likely to lead to higher share prices for banking

shares across the world. This means that industry membership rather than location has

become a more important determinant of market value. In other words, investors should

diversify more by industry than by country to achieve optimal diversification benefits.

Brooks and Catao also showed that the most important factor explaining increased

correlation was developments in information technology. They found an overall cor-

relation between European IT stocks and US IT stocks at May 2000 of 0.85, but for non-

IT stocks, it was only 0.54. This implies that high-tech stocks now constitute a channel

whereby shocks in one market are spread throughout the world, e.g. in 2001, the infor-

mation announced in the US about the reduced prospects and the stock write-downs

by internet technology suppliers Cisco, had a rapid impact not just on US technology

shares, but throughout the world stock markets.

0

0

0.1

0.2

0.3

0.4

0.5

0.6

10 20 30 40

Number of shares

Risk and portfolio size

Polish

Mixed

English

Risk

50 60 70 80 90

Figure 10.4

Combining the Warsaw

and the London

markets.

10.5 SYSTEMATIC RISK

As specific risk can be diversified away by portfolio formation, rational investors expect

to be rewarded only for bearing systematic risk. Since systematic risk indicates the

extent to which the expected return on individual shares varies with that expected on

the overall market, we have to assess the extent of this co-movement. This is given by

the slope of a line relating the expected return on a particular share, to the returnER

j

,

Source: Short, T. (2000) ‘Should foreign investors buy Polish shares?’ in T. Kowalski and S. Letza (eds) Financial Reform and

Institutions (Poznan University of Economics).

CFAI_C10.QXD 3/15/07 7:28 AM Page 244