Jones D.S.J., Pujado P.R. Handbook of Petroleum Processing

Подождите немного. Документ загружается.

ECONOMICS 785

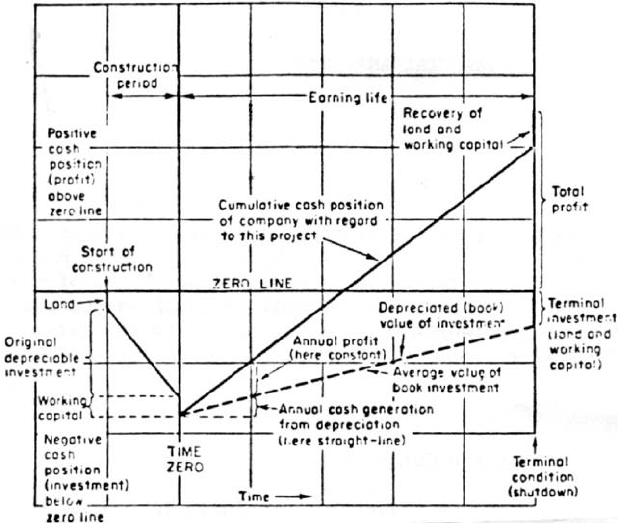

Figure 17.1.9. A diagram of cumulative cash flow.

Initially there is a financial loss when the company has to purchase land, equipment,

pay contractors to erect equipment, and the like. To do this not unlike most private

individuals, companies borrow money, on which of coarse they have to pay interest.

In addition to the cost of construction the company must keep in hand some capital

by which it can buy feedstock, chemicals, and pay the salary of its staff during the

commissioning of the plant. This working capital must also be considered as debt at

the project initiation.

At the end of construction and commissioning the cash flow into the system moves

upward toward a positive value and after a prescribed number of years moves into a

positive value. During this period of positive cash flow the money recovered from the

operation must be sufficient to:

r

Repay the loan and its interest

r

Pay all associated taxes

r

Pay all the operating costs of the project

r

Make an acceptable profit

786 CHAPTER 17

When these conditions have been met over the prescribed period of time called the

“Earning Life”or “Economic Life”, there still remains the plant hardware, the land,

and the working capital. These are considered as the projects terminal investment and

are added to the final project’s net cost recovery.

The cash flow calculation recognizes the financial milestones shown in Figure 17.1.9

and the contents of a typical cash flow calculation are discussed below:

Economic life of the project

This is the number of years over which the project is expected to yield the projected

profit and pay for its installation. These are the number of years starting at year 0

which indicates the end of construction and the commissioning of the facilities. The

last year (usually year 10) is the year in which all loans and other project costs are

repaid and the “Terminal Investment”released.

Construction period

This is the period before year 0 during which the plant is constructed and commis-

sioned. Assume this period is three years then this is designated as end of year −2,−1,

0. During this period the construction company will receive incremental payments

of the total capital cost of the plant with final payment at the end of year 0. The

construction cost may be paid from the company’s equity alone or from equity and

an agreed loan or entirely from a loan. In the case of a loan to satisfy this debt the

payment of the loan interest commences in this period. The interest payment over this

period however is usually capitalized and paid over the economic life of the project.

Net investment

The net investment for the project includes the capital cost of the plant, which is subject

to depreciation, and the associated costs, which are not subject to depreciation. The

capital cost of the plant is the contractor’s selling price for the engineering, equipment,

materials and the construction of the facilities. In a process study using a DCF return

on investment calculation the capital cost should be an estimate with an accuracy at

least that based on an equipment factored type.

The associated costs include the following elements:

r

Any licensor’s paid up royalties

r

Cost of land

r

First inventory of chemicals and catalyst

r

Cost of any additional utilities or offsite facilities incurred by the project

r

Change in feed and product inventory

r

Working capital

r

Capitalized construction period loan interest

ECONOMICS 787

Revenue

This is the single source of income into the project. In most cases it is the income

received for the sale of the product(s). This is calculated from projected process

yields of products multiplied by the marketed price of the products. A market survey

should already have been completed to ensure that the additional products generated

by the project are in demand and the price is in an acceptable range. Later a sensitivity

analysis of the DCF return on investment may be conducted changing the revenue

recovered by price escalation or other means.

Expenses

This is the major cost of carrying out the project. It consists of the following items:

r

Plant operating cost. This includes the cost of utilities used in the process, such as

power, steam, and fuel. It also includes the cost of plant person in salaries, burdens,

and indirects and the cost of chemicals and catalyst used.

r

Maintenance. There are two kinds of maintenance cost included in this item. These

are the preventive maintenance carried out on a routine basis, and those costs

associated with incidental breakdowns and repair.

r

Loan repayment. The loan principle is paid back in equal increments over the

economic life of the plant. This item includes the payback increments and the

associated interest on a declining basis.

These are incurred running costs and as such are considered tax free.

Depreciation

The second cost to the project which is considered as a deductible from the gross

profit for tax purposes is the depreciation of the plant value. This is calculated over

the PLANT LIFE as the plant capital cost divided by the plant life. The term Plant Life

is the predicted life of the facility before it has to be dismantled and sold for scrap.

Usually this is set at 20 years and indeed all specifications relating to Engineering and

Design of the facilities will carry this requirement. So that all material and design

criteria such as corrosion allowances associated with the plant will meet this plant

life parameter.

Ad valorem tax

This is the fixed tax levied in most countries payable to local municipal authorities,

provincial, or state authorities to cover property tax, municipal service costs etc.

Taxable income

Taxable income is revenue less operating cost, depreciation, and Ad Valorem Tax.

This of course is simply put as in most countries, States, or Provinces there will

probably be certain local tax relief principles and tax credits that will affect the final

788 CHAPTER 17

taxable income figure. The company’s financial specialist will be in the position to

apply these where necessary.

Tax

This is quite simply the tax rate applied to the “Taxable Income”figure. This will vary

from location to location but will be taken as one rate over the economic life of the

project for the purpose of a process study, unless there are legislative changes already

in place.

Profit after tax

This is the gross profit less the tax calculated in the previous item.

Net cash flow

This item is calculated for each year of the project’s economic life. It commences

with year 0 with the net investment shown as a negative net cash flow item. Then for

each successive year until the end of the last year of the economic life, the net cash

flow is calculated as the sum of profit after tax PLUS the depreciation.

The depreciation is added here because it is not really a cost to the project. It is a

“Book”cost only and is used specifically for tax calculation. The cash flow item for

the last year of the economic life must now include the “Terminal Investment Item”.

This item is the sum of the salvage or net scrap value of the plant (scrap value less

cost of dismantling), the estimated value of the land and the Working Capital initially

used as part of the “Associated Costs”.

Thus the final cash flow item will be the sum of profit after tax, plus depreciation,

plus terminal investment.

With the net cash flow in place the second part of the calculation which is the de-

termination of the return on investment based on the present worth concept for the

project can be carried out.

Calculating the cumulative present worth

This is an iterative calculation using three or more values as the discounting per-

centage. The result of the cumulative values of the present worth at the end of the

economic life from these calculations are plotted against the discount percentages

used for each case. The discount value when the cumulative present worth is zero is

the return on investment for the project.

For each value of the discount percentages selected first calculate the discount factor

for each year of the economic life starting at year 0 where the discount factor is

always 1.0. Then divide the discount factor for year 0 which is 1.0 by (1.0 + d) where

ECONOMICS 789

d = discount percent divided by 100. Do the same for each successive year. Thus, if

the discount percent selected is 10% then the discount factor for year 0 =1.0, for year

1 = 1/1.1 = 0.909, and for year 2 = 0.909/1.1 = 0.826, and for year 3 = 0.826/1.1 =

0.751, and so on until the last year.

The present worth value for each year is then calculated as the net cash flow value

for that year multiplied by the discount factor for that year. Remember the cash flow

value for year 0 is always negative. Next determine the cumulative present worth

value by adding the value for each successive year to the value of the year before.

Starting with that value for year 0 which is negative add that value for year 1 which

is positive to give a positive or negative cumulative value for year 1. Continue by

adding the present worth value for year 2 to the cumulative value for year 1 to give

the cumulative value for year 2, and so on through the last year. The cumulative value

of the present worth for the last year in each of the discount percentages selected

is plotted linearly against the discount percentage. This cumulative value can either

be positive or negative. Indeed to be meaningful the discount percentages selected

must be such that the calculated present worth values for the last economic years be a

mixture of negative and positive values. In this way the resulting curve plotted must

pass through zero.

The following example calculation is based on Scheme 1 in Item 8.2. Similar cal-

culations may also be carried out on one or more of the other schemes that were

screened to confirm their comparative profitability. In this case, it is important to

remember that the economic parameters used for each case are identical to enable a

proper comparison and analysis to be made.

Example calculation

This scheme includes the addition of the following units into an existing oil re-

finery.

r

New naphtha hydrotreater (13,500 BPSD)

r

New naphtha splitter (1,350 BPSD)

r

Revamped debutanizer and new light end units (3,830 BPSD)

r

New thermal cracker (34,320 BPSD)

r

New diesel hydrotreater (9,000 BPSD)

r

New catalytic reformer (9,000 BPSD)

The capacity factored capital cost estimate used in the screening studies for this

scheme was 125.490 mm $. A subsequent estimate based on a more definitive design

and equipment definition (equipment factored estimate) gave a capital cost figure of

119.216 mm $ for this configuration. This latter figure will be used as the capital cost

in this example calculation.

790 CHAPTER 17

Net investment cost

This will consist of:

r

The capital cost

r

Associated costs

r

Capitalized construction loan interest

Associated costs

1.0 Paid up royalties. This is a once off licensing fee paid to the licensors of the

hydrotreater processes, and the catalytic reformer process. There may also be

a running licensing fee for these processes, but this will be included into the

operating cost.

Paid up royalties = 2.026 mm $.

2.0 First catalyst inventory = 4.052 mm $.

3.0 Cost of land = 1.0 mm $.

4.0 Cost of incremental utility / offsite facilities = 2.501 mm $.

5.0 Cost of increased product / feed inventory (only product inventory is considered

here as there is no change in crude oil throughput). Statutory requirements for

this refinery location is a mandatory inventory of 14 days feed and product.

Additional inventory cost = 14 × ((564,845 + 162,798) − (452,756))

= 3.848 mm $. (see this chapter Item 2)

6.0 Working capital. This is taken as 5.0% of the capital cost = 5.835 mm $.

Total associated costs = 19.262 mm $.

Construction cost and payment

End of year −2 −10

Construction schedule of payments mm $. 11.922 47.686 59.608

The construction costs will be paid out of equity up to the limit of the equity. The

remainder will be paid by a loan at 8.0% interest. Initial equity is 60% of Capital +

associated costs = 0.6 (119.216 + 19.262) = 83.087 mm $.

The loan to complete the construction schedule of payments is raised during year 0

and interest on this is 2.89 mm $. This is capitalized but will be paid out of an increased

equity.

Net Investment:

mm $.

Capital cost of plant 119.216

Associated costs 19.262

Construction loan interest 2.89

Net investment 141.368

ECONOMICS 791

Table 17.1.18. Schedule of operating and

maintenance costs

Operating costs Maintenance

End of year mm $ mm $

1 11.01 4.76

2 11.34 4.81

3 11.681 4.86

4 12.031 4.904

5 12.392 4.953

6 12.764 5.003

7 13.147 5.053

8 13.541 5.103

9 13.947 5.154

10 14.366 5.206

Operating and maintenance costs

Operating cost for year 1 is made up as follows:

mm $

Operating labor = 1.49

Utilities = 8.32

Chemicals, catalyst, running royalties = 1.20

Total = 11.01

Operating costs escalate at a rate of 3.0% per year. The yearly operating cost schedule

is given in Table 17.1.18.

The maintenance cost for year 1 is taken as 4% of capital cost which is 0.04 ×

119.216 = 4.76 mm $. Maintenance costs are escalated at a rate of 1.0% per year.

The annual schedule for this item is also given in Table 17.1.18.

Loan repayments and interest

The total loan for the project is 55.390 mm $ and is repaid over 10 years at an interest

rate of 8.0% per annum discounted annually.

The schedule of repayments and interest is given in Table 17.1.19 assuming uniform

returns in principal.

Revenue

There is a single source of revenue which is from the sale of all products at the refinery

price given in Item 2 of this section of the chapter. For the base case given in this

example there is no escalation of this figure which remains at 77.7 mm $ per year.

Sensitivity analysis performed later gives the change in ROI for escalated product

pricing of 3% and 4% per year, respectively.

792 CHAPTER 17

Table 17.1.19. Schedule of debt repayments and interest

Principal Total, repayments

End of year Principal, mm $ repayments, mm $ Interest, mm $ Total, repayments mm $

0 55.390

1 49.851 5.539 4.431 9.970

2 44.312 5.539 3.988 9.527

3 38.773 5.539 3.545 9.084

4 33.234 5.539 3.102 8.641

5 27.695 5.539 2.659 8.198

6 22.156 5.539 2.216 7.755

7 16.617 5.539 1.772 7.311

8 11.078 5.539 1.329 6.868

9 5.539 5.539 0.886 6.425

10 0 5.539 0.443 5.982

Schedules of increased pricing are given in Table 17.1.20.

Depreciation

Depreciation is normally the capital cost of the plant divided by the plant life. The

plant life in this example is 20 years but the capital cost in this case has been taken as

the original capacity factored estimate of 125.490 mm $. This allows for such items in

the associated costs such as the precious metal content of catalysts which are subject to

depreciation. For this example therefore depreciation is taken as 7.7 mm $ per year

throughout.

Ad Valorem Tax

This item includes plant insurance and is set at 2.0% of capital cost per year.

Tax

This is 40% of taxable income. For the purpose of this study it is assumed there are

no tax credits.

Table 17.1.20. Schedule of escalated revenue (for sensitivity analysis)

End of year Escalated @ 3.0%, mm $/year Escalated @ 4.0%, mm $/year

1 77.709 77.709

2 80.040 80.817

3 82.441 84.050

4 84.915 87.412

5 87.462 90.901

6 90.086 94.545

7 92.789 98.327

8 95.572 102.260

9 298.439 106.351

10 101.392 110.601

ECONOMICS 793

Table 17.1.21. Consolidation of net cash flow

mm $

Endofyear 0 12345678910

Investment

Cap cost 119.2

Assoc cost 22.2

Net investment 141.4 18.7

(1) (2)

Revenue @ 0% Esc 77.7 77.7 77.7 77.7 77.7 77.7 77.7 77.7 77.7 77.7

Expenses (1)

Operating 11.0 11.3 11.7 12.0 12.4 12.7 13.1 13.5 13.9 14.4

Maintenance 4.8 4.8 4.8 4.9 4.9 5.0 5.1 5.1 5.2 5.2

Loan repayment

(Table 8.17) 10.0 9.5 9.1 8.6 8.2 7.8 7.3 6.9 6.4 6.0

Total expense (1) 25.8 25.6 25.6 25.5 25.5 25.5 25.5 25.5 25.5 25.6

Depreciation (1) 7.5 7.5 7.5 7.5 7.5 7.5 7.5 7.5 7.5 7.5

Ad Valorem Tax (1) 2.4 2.4 2.4 2.4 2.4 2.4 2.4 2.4 2.4 2.4

Taxable income 42.0 42.2 42.2 42.3 42.3 42.3 42.3 42.3 42.3 42.2

Tax @ 40% 16.8 16.9 16.9 16.9 16.9 16.9 16.9 16.9 16.9 16.9

Profit after Tax 25.2 25.3 25.3 25.4 25.4 25.4 25.4 25.4 25.4 25.3

Net cash flow 141.4 32.7 32.8 32.8 32.9 32.9 32.9 32.9 32.9 32.9 51.5

(1)

Note: (1) These are costs and therefore negative values in cash flow. (Shown here in Italics.)

(2) These are cash recoveries and therefore have positive values in cash flows.

Results

Consolidation of the net cash flow is given in Table 17.1.21.

Figure 17.1.10 gives a plot of the cumulative net present worth versus percent discount

from the results of the calculations given in Table 17.1.22.

From Figure 17.1.9 the DCF return on investment for this scheme is 20.5% per

year. Based on the plant location and the current investment environment Return

on Investment above 18% DCF makes the venture economically attractive. Similar

calculations for scheme 3 will also be conducted to verify its ROI on a DCF basis for

comparison with scheme 1.

The sensitivity of scheme 1 to escalation of refinery fence product costs are as follows:

r

At an escalation rate of 3.0% per year the ROI becomes 23.5%

r

At an escalation rate of 4.0% per year the ROI becomes 24.8%

794 CHAPTER 17

Percentage Discount

Net Present Worth

ROI=20.5

10 15 20 25 30 35

120

100

80

60

40

20

0

−20

−40

Figure 17.1.10. A plot of net present worth versus percent discount.

Using linear programs to optimize process configurations

Linear programming is a technique to solve complex problems having multi variable

conditions by the use of linear equations. The equations are developed to define

the inter relationship of the variables. Computers are used to solve these equations

and to select from a matrix of these equations the solution or solutions to the pro-

blem.

This is not a new technique. It has been used for many years in industry and particularly

the oil industry to plan and optimize its operation. Indeed in oil refining today there

is considerable development in process control using linear programming “on line”

to optimize the units operation. In its use as a management tool it can refine the

calculations described in item 8.2 to a very fine degree. It is possible also by using

this technique to examine many more options than could be examined in a manual

operation.