Jacques J., Raimondo M. Semi-markov risk models for finance, insurance and reliability

Подождите немного. Документ загружается.

228 Chapter 5

0

0

(,) ( )( )

t

Tt

tSj

jk

CS t v T t j k

φ

−

>

=

−−Δ

∑

(12.21)

which is the Janssen-Manca-Di Biase formula for the considered semi-Markov

model.

If the semi-Markov process is ergodic, then, if (T

−

t) is large enough, results

(12.19) can be well approximated by:

0

00

0

(() ( )) , ,

(() 0) , .

j

l

lK

PCT j k j k

PCT j k

π

π

≤

=− = >

== ≤

∑

(12.22)

The stationary version of the Janssen-Manca-Di Biase formula is thus given by

0

0

(,) ( ).

t

Tt

tjSj

jk

CS t v j k

πφ

−

>

=

−Δ

∑

(12.23)

Of course the vector

1

( ,..., )

m

π

π

is the asymptotic distribution of the embedded

semi-Markov process.

The evaluation of assets, formally is continuous, but substantially is given in the

discrete case; furthermore, facing the numerical solution of a continuous time

semi-Markov process gives problems of numerical and stochastic convergence.

For these reasons, we can face our problem with the discrete time homogeneous

semi-Markov process as introduced in Chapter 4.

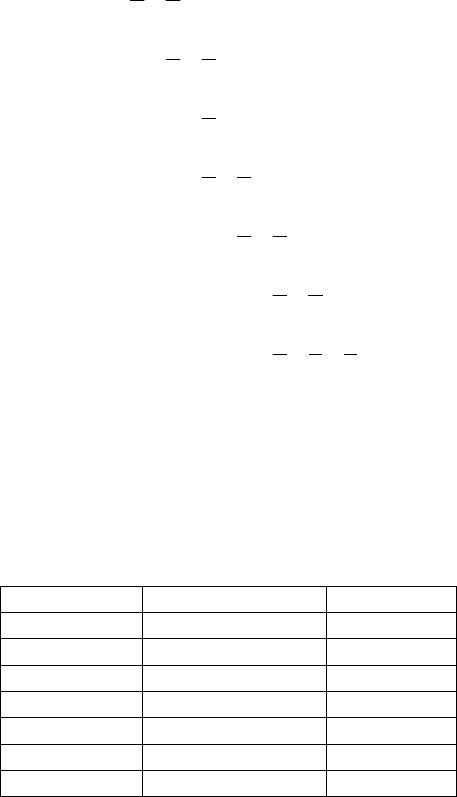

12.6 Numerical Example For The Semi-Markov JMD

Model

We will only give a numerical example for the semi-Markov model in the

asymptotic case, i.e., values of the option expectation and of the options for large

maturities.

As data, we just need as supplementary information, the conditional mean

sojourn times being computed by relations (1.15) of Chapter 4.The used values

are given by the following matrix

Σ :

Black & Scholes extensions 229

11

12111

22

11

11211

44

1

21 1221

2

11

11 111

22

11

111 21

22

11

1121 2

22

111

1111

233

⎡⎤

⎢⎥

⎢⎥

⎢⎥

⎢⎥

⎢⎥

⎢⎥

⎢⎥

⎢⎥

=⎢ ⎥

⎢⎥

⎢⎥

⎢⎥

⎢⎥

⎢⎥

⎢⎥

⎢⎥

⎢⎥

⎢⎥

⎣⎦

Σ . (12.24)

In this case, the asymptotic distribution for the semi-Markov process is:

(0.09487, 0.12650, 0.38238, 0.15352, 0.15013, 0.08358, 0.00902).

Then starting at time 0 in state 1500, the asymptotic value of the call option

expectation with 1500 as exercise price is 46 and the call value is 45.315.

The following table gives option expectations and option values with different

exercise prices:

Exercise price Option expectation Option value

1350 178.78 176.119

1400 129.234 127.308

1450 83.8638 82.614

1500 46.0002 45.315

1550 15.8126 15.577

1600 4.74378 4.673

1650 0 0

Table 12.3: semi-Markov option computation

12.7 Conclusion

The JMD models presented here give a semi-Markov approach for the pricing of

option financial products working in discrete time and with a finite number of

possible values for the imbedded asset, which is always the case from the

numerical point of view.

The main interest of these models is that they work even when there are

possibilities of arbitrage, that is to say for the most frequent cases. Of course, one

230 Chapter 5

of the main difficulties for applying this model is the fitting of the needed data

and this is only of interest in case of asymmetric information so that the

economic agent can believe in his own information, knowing that he will always

be in a risky situation expecting gain but still worried about the possibility to lose

as in the case of a real-life situation!

It is also important to point out that the numerical examples are coherent;

nevertheless, they are significant differences according to the model used:

Markov or semi-Markov, so that it is very important to select the most concrete

one.

Another possibility is to use the more classical and less risky way of building

likely scenarios for these data and to study their possible consequences.

Chapter 6

OTHER SEMI-MARKOV MODELS IN FINANCE

AND INSURANCE

1 EXCHANGE OF DATED SUMS IN A STOCHASTIC

HOMOGENEOUS ENVIRONMENT

1.1 Introduction

According to several authors, the theory of financial operations evaluation can be

introduced from an axiomatic point of view (for a more complete treatment see

Volpe di Prignano (1985)) and any financial problem can be dealt with from the

axiomatic approach. The challenge is to find the mathematical relations that must

be solved in order to find quantitative answers to financial questions.

Of course, the choice of the interest evolution law is crucial.

For example if we call:

12

(, )tt

ν

(1.1)

an exchange factor, where:

12

12 1 2

12

1,

(, ) 1 ,

1,

if t t

tt if t t

if t t

ν

><

⎧

⎪

==

⎨

⎪

<>

⎩

(1.2)

it is not always true that:

12 23 13

(, )(, ) (, )tt t t tt

ν

νν

=

(1.3)

and then it is not possible to use the compound interest law to describe the

phenomenon which is the object of our study; we have to select another interest

law.

Furthermore the problem of the construction of exchange factors is more useful

in a stochastic environment, in the sense that the exchange factors can be

considered as random variables and, to follow time evolution, we need a

stochastic process approach.

In this chapter our aim is to show how, by means of SMP, it is possible to

introduce a stochastic environment in the axiomatic approach to describe a lot of

financial operations.

Furthermore we would like to show that the semi-Markov approach could be an

alternative to the approach under the hypothesis of the absence of opportunity of

arbitrage (AOA, see Chapter 5) which implies the use of the risk free measure for

a asset evaluation.

The semi-Markov approach enables us to get financial evaluations by means of

the physical measure. This fact is really important in the sphere of actuarial

232 Chapter 6

science because, if it is possible to know or to make good estimates of claims by

means of statistics, an insurance company can evaluate its premiums and limit its

risk of ruin.

As we have already shown in section 12 of Chapter 5, in finance, these models

can be seen as an alternative approach to the methods presented by Black and

Scholes (1973) for option evaluation and for Vasicek (1977) for bond evaluation

in continuous time evolution of a general financial problem.

In insurance there are other approaches that are really useful, see Bühlmann

(1992), (1994), Norberg (1995), but these approaches do not really consider

financial choice problems that will be developed in this chapter.

1.2 Deterministic Axiomatic Approach To Financial Choices

Fundamentally, mathematics of finance is based on the study of investor

preferences between

dated sums, given by a pair of real numbers i.e:

(,),, ,St St

∈

(1.4)

S representing a sum and t a time.

Definition 1.1 The investor prefers the pair

22

(,)St

to the pair

11

(,)St

means

that he prefers to get the sum

2

S at time

2

t instead of the sum

1

S at time

1

t.

In this case, the preference relation defined on the set of dated sums is

represented by the following notation:

11 2 2

(,) ( ,).St St≺

(1.5)

Definition 1.2 If

11 2 2

(,) ( ,)St St≺ and

22 11

(,) (,),St St≺ (1.6)

then the preference is called strict and is thus represented as:

11 2 2

(,) ( ,).St St≺ (1.7)

Definition 1.3 If

11 2 2

(,) ( ,)St St≺ and

22 11

(,) (,),St St≺ (1.8)

the two dated sums are called indifferent and we write:

11 2 2

(,) ( ,).St S t

≈

(1.9)

As given in Duffie (1988) the ideal should be that this indifference relation is an

equivalence relation (reflexive, symmetric and transitive).

Furthermore, for economic and financial reasons, it is natural to assume that:

12

12

12

if 0,

(,) (, )

if 0,

tt S

St St

tt S

>>

⎧

⎨

<

<

⎩

≺

(1.10)

12

(,) (,)St St≺ iff

12

.SS

<

(1.11)

Finance and Insurance models 233

For the very particular case of a flat interest rate curve with a yearly interest rate

r, Volpe di Prignano (1985), the strict preference relation defined by:

12

12

11 2 2

( , ) ( , ) iff

(1 ) (1 )

tt

SS

St S t

rr

<

++

≺ (1.12)

evaluated at time 0 is at the basis of all classical finance as it represents

comparisons of present values computed at time 0.

For any yield curve in which

t

r represents the interest rate for an investment

made at time 0 and of maturity t, the preceding relation becomes:

12

12

12

11 2 2

( , ) ( , ) iff .

(1 ) (1 )

tt

tt

SS

St St

rr

<

++

≺

(1.13)

Let us remark that if the considered yield curve presents some local inversion

phenomena so that the curve is no longer globally increasing, then relation (1.7)

is no longer a total order relation and moreover properties (1.12) and (1.13) are

not always verified.

In the case in which a total relation order is defined and relations (1.10) and

(1.11) are satisfied, given an investor and a certain instant, we can define a so-

called indifference relation

ℜ on dated sums as follows:

11 22 11 22

(,)(,) (,) ( ,)St St St St

ℜ

⇔≈

. (1.14)

It is clear that this indifference relation can change with time depending on the

evolution of the money utility function of the investor and the economic, political

and financial environment under consideration and in the same way, under the

same assumptions, two different investors usually have different indifference

relations.

The presented static approach to the theory of the preference between dated sums

can and must be extended from a dynamic point of view as follows: under our

assumptions, given

tt

12

,

and

S

1

, there exists one and only one amount

2

S such

that (1.14) holds and so we can define the following three-variable functions

giving this value:

2121

(, , ).SttS

ϕ

=

(1.15)

It is clear that this is a continuous approach to the problem, all three variables

being continuous. But for practical applications, it is possible to discretize the

sums to obtain the set

{

}

12 1 2

, ,..., ,

nm

ISSSSS S=<<<

(1.16)

as all possible amount values.

All remains unchanged but now relation (1.15) represents a three-variable

function in which one of the variables and the function can only assume a finite

number of values.

Though relation (1.15) represents a non-homogeneous time environment, we

begin with the time homogeneous case.

In a deterministic static homogeneous case, the indifference relation (1.14)

becomes:

234 Chapter 6

11 22 11 22

(,) (,) (, ) (, )St S t St h S t h h≈⇔+≈+∀∈ , (1.17)

so that a time translation is indifferent for the choice; only the length of the

financial operation,

)(

12

tt −

, assumes relevance.

In the dynamic approach, equation (1.15) becomes:

21

(,)SSt

ϕ

=

. (1.18)

In this case we have a two-variable function: the time variable represents the

length of the operation and

1

S the initial sum.

1.3 The Homogeneous Stochastic Approach

Though usually an investor who wants to invest a given amount at a given time

and for a given period cannot predict the final result of his investment, it seems

reasonable to assume that he can know an interval

[

]

', "SS ,

[',"]SSS

∈

, (1.19)

within which his final return S must be situated and thus with a minimal value

'S ,eventually 0, and a maximum one "S .

In this way, the final result

S of his financial operation clearly can be seen as a

random variable.

In the static approach, the maximal information of the investor will be the

distribution function of this r.v.

If p represents the density of the r.v., then he can compute the mean and variance

of his investment:

"

'

() ,

S

S

SSpSdS=⋅

∫

(1.20)

"

_

22

'

() ( ) ()

S

S

SSSpSdS

σ

=−

∫

(1.21)

and with this information (expected value and risk measure) at the basis of the

Markovitz theory, the investor can decide to make the investment or not.

If the function p represents all the information to solve the static approach, it is

much more complicated for the stochastic dynamic approach.

The stochastic model needs the introduction of a probability space

(

)

,,PΩℑ

where P is the probability measure describing the stochastic dynamics of the

process

1

( ( ), ,..., )

n

SSttt t

=

= . (1.22)

In particular for each time t, it is also possible to get the mean and the variance of

()St but of course, we can do more with the construction of a realistic stochastic

model.

The next dynamic stochastic model will be characterized by the following

transition probability function:

Finance and Insurance models 235

(

)

[]

12 2 1

12

(, ,) () (0) ,

,[',"],0,.

p

SSt PSt S S S

SS SS t T

=

==

∈∈

(1.23)

The assumption of homogeneity implies that:

(

)

[]

2112

() () (,,),

,',".

PSs t S Ss S pSS t

ss t S S

+Δ = = = Δ

+Δ ∈

(1.24)

It is clear that the knowledge of the function p(.,.,.) defined by (1.23) gives the

possibility to compute the expected values and risks of financial operations.

In fact this model can be improved with the introduction of a two-dimensional

process with time as a second component.

1.4 Continuous Time Models With Finite State Space

When we deal with the dynamic stochastic approach to a general financial

problem we are defining a stochastic process describing the evolution of the

investment during some period of time.

This evolution can be studied by means of an HSMP of kernel

Q; in fact as

already explained, one follows the evolution of the system states with a

stochastic time length.

We denote the state space I by:

{

}

12

1min2 max

,,, ,

.

m

m

ISS S

SS S S S

=

=<<<=

…

(1.25)

We will try to give a financial meaning to all the variables that are involved in an

SMP.

If

n

J

represents the value of the sum at transition n, it is usual to assume that the

stochastic process

(, 0)

n

Jn≥ (1.26)

is a homogeneous SMP where the transition matrix of the embedded MC is:

[

]

ij

p

=P . (1.27)

Here,

ij

p

represents the probability of going from the state i to the state j, where

in general the state k represents the sum value

k

SI

∈

.

We also introduce the r.v.

n

T representing the time at transition n, i.e., the time of

the nth sum transition, where clearly:

01

0

n

TT T

≤

≤≤≤≤

, (1.28)

0

T representing the time of the initial investment.

The basic assumption of the model considered here is that the (J-T) process is a

continuous time homogeneous semi-Markov process of kernel

Q.

Here, the general element

()

ij

Qt of the semi-Markov matrix kernel Q represents

the probability that after a time t from the n-th transition, the value of the

236 Chapter 6

financial operation is ,

j

S given that the value of the operation was

i

S at time

n

T

and that the ( 1)n

+ th transition happened in a time less than or equal to t.

()

i

H

t gives the probability that the financial operation value will change, given

that the value at the moment of the

n

T was

i

S and that the value change will take

place in a time less than or equal to t.

Another interesting r.v. is the sojourn time in one of the states after a transition in

this state. For example, if at time

n

T the r.v. sum gets the value

i

S , the

probability of this sum becoming

j

S in a time length t will be represented, as we

already know, by the increasing distribution function

()

ij

F

t .

The associated homogeneous semi-Markov process Z represents the value at time

t of the dated sum.

()

ij

t

φ

represents the transition probabilities of the Z-process.

The evolution equations of the Z-process are reported to give their financial

meaning:

()

0

() 1 () ( ) ( )

t

ij ij i ik kj

kE

tHtQstsds

φδ φ

∈

=− + −

∑

∫

. (1.29)

()

ij

t

φ

represents the probability that the sum

i

S

at time 0 will be

j

S

after a time t.

(

)

1()

ij i

St

δ

− represents the probability that the value of the investment will

remain

i

S after a time t; this element has sense iff i=j.

0

() ( )

t

ik kj

kE

Qs t sds

φ

∈

−

∑

∫

represents the probability that the value of the financial

operation will be

j

S after a time t, taking into account that at initial time the

value was

i

S

and that the financial operation changed value at least once.

Instead of working with continuous time, we can also consider discrete time; this

generally implies a simplification for the numerical treatment as we have already

explained before.

1.5 Discrete Time Model With Finite State Space

We will now look at an application of the model defined in the previous

paragraph in real problems.

As we noted previously, in the real world, we are not usually interested in the

continuous state approach. For example, we can decide to use as a monetary unit

the amount of $1000 and so automatically, the underlying state space is discrete;

moreover if we are sure that the maximum amount will be no more than one

billion dollars, we also have a finite state space. Bühlmann (1994) also gives

some advantages of working with discrete state space.

Finance and Insurance models 237

Furthermore, from an applied point of view, discrete time is in general enough to

get results; for example, depending on our kind of investment, we are interested

to know the results after an hour or a day or, maybe a year, and not necessarily

instant after instant.

Of course, we know continuous time models can generally give more elegant

mathematical developments as is shown in examples in Chapters 3 and 4, but we

also know that the numerical results obtained in Chapter 4 needed discrete time

and finite state space.

Also, as before, relation (1.25) represents the finite state space and furthermore:

t

∈

, (1.30)

and the semi-Markov model used here still has (1.27) as embedded MC.

We also need the conditional probabilities

11

() [ , ],, ,

ij n n n n

bt PX jT T tX iij I

++

==−==∈ (1.31)

representing the probability that, after a time t from the nth transition, the value

of the financial operation is ,

j

S given that the value of the operation is

i

S at

time

n

T and that the (

1n +

)th transition happens after

n

T in a time just equal to t.

Relations (1.19) of Chapter 4 give the evolution equation of the DTHSMP.

1.6 An Example Of Asset Evaluation

Now we seek to examine stochastic process problems that can explain the

dynamic stochastic development of financial operations.

We would like to apply our model to a general stochastic financial operation, the

purchase of goods or shares by an investor who would like to sell them for a

profit.

First of all, we have to observe that we are in the hypothesis that the time is

discrete if the quotations are fixed at the end of every stock exchange day, for

example.

We also suppose that the investor is interested in a medium term investment, in

the sense that he doesn’t want to buy for a short period of speculation.

For this reason, the time unit will represent a month and "t" will give the number

of months from a starting date. Furthermore, as we said previously, we suppose

that the state space is finite, i.e.,

12

{ , ,..., }

m

ISS S

=

. (1.32)

From the general results of Chapter 3, the model is characterized by the semi-

Markov kernel

Q equivalently by

, , , 1,...,

ij ij

p

Fij m

=

, (1.33)

()

ij

F

t representing the increasing distribution function of waiting time

ij

τ

, in the

sense that the asset value becomes

j

S starting from

i

S .