Jacques J., Raimondo M. Semi-markov risk models for finance, insurance and reliability

Подождите немного. Документ загружается.

208 Chapter 5

Numerical data are the following:

(0.05,0.90,0.05),

0.6 0.3 0.1 1.05 1.03 1.02

0.02 0.96 0.02 , 1.05 1.03 1.02 ,

0.6 0.35 0.05 1.06 1.04 1.03

1.07 1.10 1.20 0.5 0.7 0.8

1.07 1.10 1.20 , 0.6 0.7 0.8

1.07 1.09 1.15 0.65 0.7 0.8

=

⎡⎤⎡⎤

⎢⎥⎢⎥

==

⎢⎥⎢⎥

⎢⎥⎢⎥

⎣⎦⎣⎦

⎡⎤⎡⎤

⎢⎥⎢⎥

==

⎢⎥⎢

⎢⎥⎢

⎣⎦⎣⎦

a

Pr

UD.

⎥

⎥

(10.35)

For both examples, we will consider a European call option with

0

100 95.SandK==

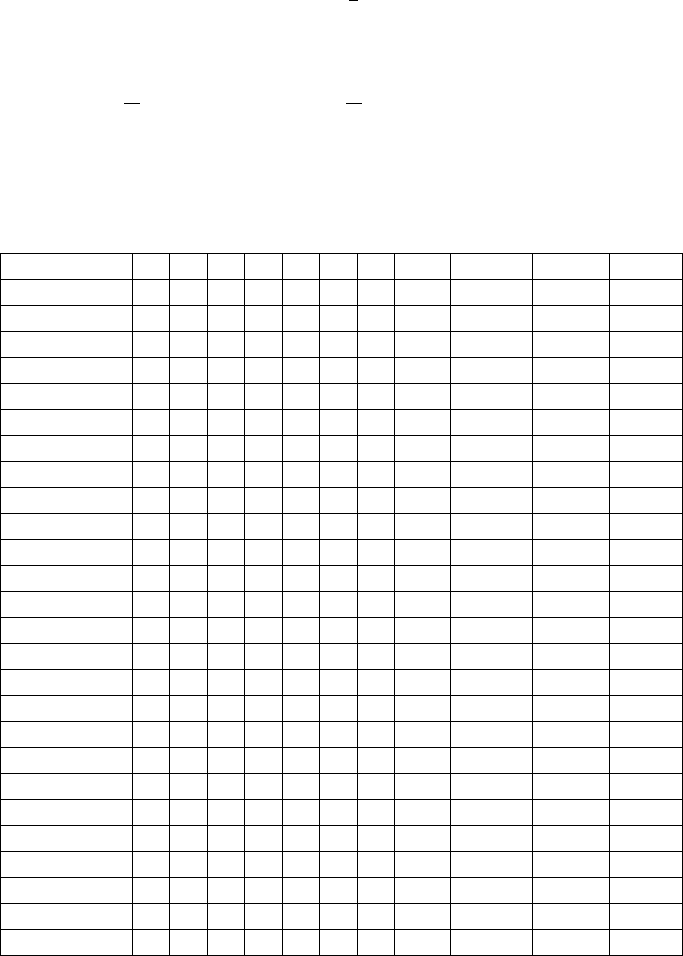

Results are given in Table 10.1.

S 100

K 95

Example 10.1

transition a1 a2 a3 p(ij) r(ij) u(ij) d(ij) q(ij)

Cij(100,1) Ci(100,1) C(100,1)

0 to 0 0.95 0.05 0.98 1.03 1.3 0.7 0.55 18.68932

18.57744

0 to 1 0.02 1.05 1.1 0.5 0.9167

13.09524

1 to 0 0.6 1.05 1.06 0.4 0.9848

10.31746 13.1484

1 to 1 0.4 1.03 1.2 0.6 0.7167

17.39482

18.27158

Example 10.2

0.05 0.9 0.05

bad to bad 0.6 1.05 1.07 0.5 0.9649

11.02757 11.56895

bad to normal 0.3 1.03 1.1 0.7 0.825

12.01456

bad to good 0.1 1.02 1.2 0.8 0.55

13.48039

normal to bad 0.02 1.05 1.07 0.6 0.9574

10.94225 12.02243

normal to normal 0.96 1.03 1.07 0.7 0.8919

12.01456

normal to good 0.02 1.02 1.07 0.8 0.8148

13.48039

good to bad 0.6 1.02 1.2 0.65 0.6727

11.05121 7.67948

good to normal 0.35 1.02 1.2 0.7 0.64

11.7357

good to good 0.05 1.03 1.15 0.8 0.6571

12.76006

11.82274

Table 10.1: European call option examples

Black & Scholes extensions 209

10.2 The Multi-Period Discrete Markov Chain Model

Let us now consider a multi-period model over the time interval

[

]

0, n , n being an

integer larger than 1 representing the maturity time of the option, always under

the assumption of absence of arbitrage as in section 1.

To obtain useful results, we will still follow the fundamental presentation of the

CRR model (Cox, Rubinstein (1985)) but adapted for our Markov environment in

such a way that tractable results may be found.

1)

result with knowledge of

0

,...,

n

J

J

Let us begin with a discrete time model with n periods and suppose that given

00

,..., , (0)

n

J

JS S

=

with

0

,,

n

J

iJ j

=

=

the up and down parameters, the non-

risky interest rate and the probabilities of an up movement for each period are the

same for all periods and given respectively by , , ,

ij ij ij ij

udrq.

Then, the asset value

S(n) at time n is given by:

01 1

0

()

nn

jj j j

Sn V V S

−

=

⋅⋅ (10.36)

where the conditional distributions of the random variables

V are defined as:

1

with probability ,

,.

with probability 1- ,

nn

ij ij

JJ

ij ij

uq

VijI

dq

−

⎧

⎪

=∈

⎨

⎪

⎩

(10.37)

Moreover, we suppose that, for each

n, the random variables

01 1

,...,

nn

J

JJJ

VV

−

are

conditionally independent given

0

,..., .

n

J

J

Now if the random variable

n

M

represents the total number of up movements on

[]

0, n , the asset value at time n is given by:

0

() ( ) ( )

nn

MnM

ij ij

Sn u d S

−

= (10.38)

and consequently:

0

()

ln ln ( )ln .

nij n ij

Sn

M

unM d

S

=+− (10.39)

Given

00 0

,..., , (0)

nn

J

jJjS S===, the conditional distribution of

n

M

is a

binomial distribution with parameters ( , )

ij

nq . It follows that:

00 0

0

()

ln ,..., , (0) ( ln (1 )ln )

n n ij ij ij ij

Sn

E

Jj JjS S nqu q d

S

⎛⎞

==== +−

⎜⎟

⎝⎠

.(10.40)

Concerning the conditional variance, we get:

2

00 0

0

()

var ln ,..., , (0) (1 ) ln .

ij

n n ij ij

ij

u

Sn

Jj JjS S nq q

Sd

⎡

⎤

⎛⎞

⎛⎞

⎢

⎥

====−

⎜⎟

⎜⎟

⎜⎟

⎢

⎥

⎝⎠

⎝⎠

⎣

⎦

(10.41)

210 Chapter 5

Choosing now for the up probability on the n periods, the risk neutral probability

given by relation (10.10):

11

1

11

ij ij

ij

ij ij

rd

q

ud

−

=

−

, (10.42)

it is now clear that, under our assumptions, for each n, given

00

,..., , (0)

n

J

JS S=

with

0

,,

n

J

iJ j== we have a CRR model, so that their results recalled in the

beginning of this chapter concerning the European call are valid. Consequently,

we get the value of the European call with exercise price and maturity n as the

present value of the expectation of the “gain” at time n under the risk neutral

measure, that is:

{}

0001

0

0

( , ) ( , , ,..., )

1

(1 ) max .

ij n

n

knkknk

ij ij ij ij

n

k

ij

CSn CSnJ iJ J j

n

qq udSK

k

ν

−−

=

===

⎛⎞

=− −

⎜⎟

⎝⎠

∑

(10.43)

After some computation, we can obtain the following expression (see Cox and

Rubinstein (1985)):

0

00 1

(;,') (;,), if ,

( , , ,..., )

0 if ,

ij ij ij ij ij

n

ij

n

ij

K

SBa nq Ba nq a n

CS nJ iJ J j

an

ν

⎧

−

<

⎪

===

⎨

⎪

>

⎩

(10.44)

where ( ; , )Bxm

α

is the value of the complementary binomial distribution

function complementary with parameters ,m

α

at point

x

and

0

ln( / )

1,

ln( / )

'.

n

ij

ij

ij ij

ij

ij ij

ij

KdS

a

ud

u

qq

r

⎡

⎤

=+

⎢

⎥

⎢

⎥

⎣

⎦

=

(10.45)

The result (10.44) can be seen as the discrete time extension of the Black and

Scholes formula given the environment:

00

,..., , (0)

n

J

iJ jS S

=

==. (10.46)

2) result with knowledge of

0

J

i

=

If we only know the initial state of the environment

0

J

i

=

, it is clear that the

value of the call is given by

()

00

1

(,) (,)

m

n

iijij

j

CSn p C Sn

=

=

∑

(10.47)

where, of course:

()

.

nn

ij

p

⎡⎤

=

⎣⎦

P (10.48)

3) result with knowledge of

n

J

j

=

Black & Scholes extensions 211

Proceeding as in the preceding section, the use of Bayes formula gives the

following result now on n periods instead of one:

()

(

)

()

0

0

()

()

0

,

n

n

n

n

iij

m

n

kkj

k

PJ iJ j

PJ iJ j

PJ j

ap

ap

=

=

=

===

=

=

∑

(10.49)

and so the value of the call given

n

J

=j, represented by

0

(,)

j

CSn, is given by:

()

00

()

1

0

(,) (,).

n

m

iij

j

ij

m

n

i

kkj

k

ap

CSn CSn

ap

=

=

=

∑

∑

(10.50)

4) result with no environment knowledge

Finally if we have no knowledge of the initial environment state but just its

probability distribution given by (10.1), the value of the call denoted

0

(,)CS nis

given by

00

1

(,) (,)

m

ii

i

CS n aC S n

=

=

∑

(10.51)

or by

()

00

11

(,) (,).

mm

nj

kkj

jk

CS n ap C S n

==

=

∑∑

(10.52)

10.3 The Multi-Period Discrete Markov Chain Limit Model

To construct our continuous time model on the time interval [0,t], t being the

maturity time of the considered option, let us begin to consider a multi-period

discrete Markov chain model with n periods where each period has length h so

that we have equidistant observations at time 0,h,2h,...,nh with /nth=

⎢

⎥

⎣

⎦

.

We also suppose that in the approximated discrete time model, the environment

process is now a homogeneous ergodic Markov chain defined by relations (10.1)

and (10.2) and that (see Cox and Rubinstein (1985),p. 200) or relations (3.8),

section 3.1 of this chapter), for each n, given

00

,..., , (0)

n

J

JS S= with

0

,,

n

J

iJ j== we select, in each subinterval

[

]

,( 1)kh k h+ , the following up and

down parameters:

212 Chapter 5

11

1

,,

11

,

22

ij ij

kk kk

kk

tt

nn

jj jj

ij

jj

ij

uede

t

q

n

σσ

μ

σ

++

+

−

==

=+

(10.53)

depending thus on the two

mm

×

non-negative matrices:

,

ij ij

μ

σ

⎡

⎤⎡ ⎤

⎣

⎦⎣ ⎦

. (10.54)

From relations (10.40) and (10.41), it follows that, for all n:

00 0

0

()

ln ,..., , (0) ,

nn ij

Sn

E

Jj JjS S t

S

μ

⎛⎞

====

⎜⎟

⎝⎠

(10.55)

2

00 0

0

()

var ln ,..., , (0) .

nn ij

Sn

J

jJjS S t

S

σ

⎛⎞

====

⎜⎟

⎝⎠

(10.56)

As our conditioning implies that we can follow the reasoning of Cox and

Rubinstein (1985), we know that, for n →+∞:

2

0

()

ln ( , ),

ij ij

St

N

tt

S

μσ

≺ (10.57)

where j

0

=i as the initial environment state observed at t=0 and j the environment

state at time t.

Concerning the non-risky interest rates, we also suppose that, for all i and j, there

exists 1

ij

ν

> such that the new return rate for all the periods

(

)

,( 1) )kh k h+ ,

denoted

ˆ

ij

r , for n →+∞, satisfies the following condition:

ˆ

(1 ) (1 )

nt

ij ij

rr+→+. (10.58)

Now let

0

(,)

ij

CSnrepresent the value at time 0 of a European call option with

maturity n and exercise price K.

Using the proof of the Black and Scholes formula given by Cox and Rubinstein

((1985), pp. 205-208) but here with our parameters depending on all of the

environment states i and j, we get under the conditions (10.53) and (10.58), for

fixed t:

00

(,) (,)

ij ij

CSn CSt→ (10.59)

where:

001 ,2

0

1

,1

,2 ,1

(,) ( ) ( ),

ln

1

,

2

.

tt

t

t

t

ij ij ij ij

ij

ij ij

ij

ij ij ij

CSt S d Kr d

S

Kr

dt

t

dd t

σ

σ

σ

−

−

=Φ − Φ

=+

=−

(10.60)

Black & Scholes extensions 213

This result gives the value of the call at time 0 with i as initial environment state

and j as environment state observed at time t, represented from now on by

.

t

J

If we want to use the classical notation in the Black and Scholes (1973)

framework, we can define the instantaneous interest rate intensity

ij

ρ

such that:

ij

ij

re

ρ

= (10.61)

so that the preceding formula (10.60) becomes now:

001 ,2

2

,1

,2 ,1

(,) ( ) ( ),

1

ln ,

2

.

ij

ttt

t

t

t

ij ij ij

ij

ij ij

ij

ij ij ij

CSt S d Ke d

S

dt

K

t

dd t

ρ

σ

ρ

σ

σ

−

=Φ − Φ

⎛⎞

⎛⎞

⎜⎟

=+−

⎜⎟

⎜⎟

⎜⎟

⎝⎠

⎝⎠

=−

(10.62)

10.4 The Extension Of The Black-Scholes Pricing Formula

With Markov Environnment: The Janssen-Manca Formula

The last result (10.62) gives a first extension of the Black and Scholes formula in

continuous time from the knowledge of the initial and final environment states,

respectively

0

,

t

J

J where

t

J

represents, as said above, the state of the

environment at time t.

Now, always with the assumption that the Markov chain with matrix

P is

ergodic, we can extend results (10.43), (10.47) (10.50) and (10.52) valid for our

discrete multi-period model to our continuous time model thus giving the

following main result.

Proposition 10.1 (Janssen and Manca (1999))

Under the assumption that the Markov chain of matrix

P of the environment

process is ergodic and that given the initial environment state

iI∈ and the

environment state at time t is j I

∈

, the non-risky rate is given by

ij

ρ

and the

annual volatility by

ij

σ

, then we have the following results concerning the

European call price at time 0 with exercise price K and maturity t:

(1) with knowledge of state

0

,

t

J

iJ j

=

= , the call value is given by result (10.62),

(2) with knowledge of state

0

J

i

=

, the call value represented by

0

(,)

i

CSt is

given by:

00

1

(,) (,),

m

ijij

j

CSt C St

π

=

=

∑

(10.63)

(3) with knowledge of state

t

J

j

=

, the call value represented by

0

(,)

j

CSt is

given by:

214 Chapter 5

00

1

(,) (,),

m

j

iij

i

CSt aCSt

=

=

∑

(10.64)

(4) without any environment knowledge, the call value represented by

0

(,)CS t is

given by:

00

1

(,) (,)

m

ii

i

CS t aC S t

=

=

∑

(10.65)

or

00

1

(,) (,)

m

j

j

j

CS t C S t

π

=

=

∑

. (10.66)

Proof

Result (1) is proved above.

Result (2) follows from relation (10.47) letting n go to

∞

+

and then using result

(1) and the assumption of ergodicity on the environment matrix chain

P .

Result (3) can easily be deduced from result (2) and relation (10.50).

Finally, result (4) follows immediately from relations (10.51) or (10.52) and

results (2) and (3).

Example

The Example 10.1 is now treated in Table 10.2 with the following annual

volatility matrix

0.20 0.30

0.25 0.35

⎡

⎤

=

⎢

⎥

⎣

⎦

σ

Using for the matrix

P being given by relation (10.33), using relation 2(9.77), the

asymptotic distribution is given by:

[]

[

]

12

, 0.977742,0.032258

ππ

==π

Example 10.1

K 80 K 95

S 100 S 100

0 to 0 0 to 0

1-t Cij(100,t) 1-t Cij(100,t)

0.25 20.45 0.25 7.23

0.5 21.10 0.5 8.98

0.75 21.84 0.75 10.42

1 22.61 1 11.67

1 to 0 0.25 20.57 0.25 8.08

Black & Scholes extensions 215

0.5 21.52 0.5 10.24

0.75 22.56 0.75 11.98

1 23.59 1 13.49

0 to 1 0.25 20.79 0.25 8.97

0.5 22.13 0.5 11.54

0.75 23.48 0.75 13.57

1 24.76 1 15.33

1 to 1 0.25 21.12 0.25 9.88

0.5 22.87 0.5 12.85

0.75 24.53 0.75 15.18

1 26.07 1 17.18

? To 1 0.25

20.8065

0.25

9.0155

0.5

22.167

0.5

11.6055

0.75

23.5325

0.75

13.6505

1

24.8255

1

15.4225

? To 0 0.25

20.456

0.25

7.2725

0.5

21.121

0.5

9.043

0.75

21.876

0.75

10.498

1

22.659

1

11.761

? To ? 0.25

20.46731

0.25

7.328726

0.5

21.15474

0.5

9.125661

0.75

21.92944

0.75

10.59969

1

22.72889

1

11.87911

Table 10.2

In conclusion, the Janssen-Manca approach gives for the first time a new family

of Black and Scholes formulae taking into account the economic and social

environment showing that:

- a “good” extension of the classical Cox-Rubinstein model is possible,

-the model also extends the Black and Scholes model

-numerical results are possible.

Moreover, as the JM formulas are linear combinations of the classical BS results,

the Greek parameters can also be computed and will be linear combinations of

the Greek parameters given in section 6 and similarly for hedging coefficients.

We also add that, in our point of view, one of the main potential applications of

our new model concerns the possibility to get a new way of acting with the Black

216 Chapter 5

and Scholes formula with information related to the economic, financial and even

political environment provided it can be modelled by an ergodic homogeneous

Markov chain.

This model also gives the possibility of taking into account anticipations made

by the investors in such a way as to incorporate them in their own option pricing

and can also be used for models with financial crashes as well as to construct

scenarios and particularly in the case of stress in a VaR type approach.

11 THE EXTENSION OF THE BLACK-SCHOLES

PRICING FORMULA WITH A MARKOV

ENVIRONMENT: THE SEMI-MARKOVIAN JANSSEN-

MANCA-VOLPE FORMULA

11.1 Introduction

In this section, we present another semi-Markov extension of the Black and

Scholes formula to the so-called Janssen-Manca-Volpe model to eliminate one of

the restrictions of the Black and Scholes model that is the assumption of constant

volatility upon time.

If there have been a lot of attempts to slacken this condition, as for example in

the model of Hull and White (1985) where the concept of stochastic volatility is

introduced, nevertheless, to our knowledge, in practice, no generalised model

really supplants the classical Black and Scholes model.

Whilst comparing with the Markovian Janssen-Manca model of the preceding

section, we develop another type of model. More precisely we present new semi-

Markov models for the evolution of the volatility of the underlying asset.

In fact, the SM model presented here supposes a type of SM evolution for the

volatility of an initial Black-Scholes model presented for the first time in an oral

communication in the ETH Zurich (1995) by J. Janssen and in a different

approach by E. Çinlar in an oral communication at the First Euro-Japanese

meeting on Insurance, Finance and Reliability, held in Brussels in 1998, and

leading to a generalization of the classical Black and Scholes formula for the

pricing of European calls with easy numerical applications.

11.2 The Janssen-Manca-Çinlar Model

Hereby, we present our initial model of 1995 close to the oral presentation of

Çinlar but he gives the formula for the pricing of a call option using the Markov

renewal theory.

Black & Scholes extensions 217

11.2.1 The JMC (Janssen-Manca-Çinlar) Semi-Markov Model (1995, 1998)

Let us consider a two-dimensional positive (J-X) process of kernel Q with as

state space:

{

}

1,..., .Im= (11.1)

This means that on the probability space

(

)

Ω

,,

ℑ

P , we define the three-

dimensional process

(

)

(

)

,( , ) , 0

nnn

JX n

σ

≥ (11.2)

with:

,( , ) ,

nnn

JIX

σ

+

+

∈∈× (11.3)

such that:

()

()

1

, , ,( , ) , 0.1..... 1

(, ), ..

n

nn n kkk

Jj

PX x J j J X k n

Qxps

σσ σ

σ

−

≤≤= = −

=

(11.4)

We know that the , ,

ij

Qij I∈ can be written in the following form:

(, ) (, )

ij ij ij

Qx pFx

σ

σ

=

(11.5)

where:

(

)

1

,1,

ij n k n

p

PJ jJ k n J i

−

== ≤−=, (11.6)

()

1

( , ) , ( ,( , )), 1, .

ij n n k k k n

F

xPXx JX knJi

σσσσ

−

=≤≤ ≤−= (11.7)

We also introduce the following r.v.:

{}

1

()

,0,

() sup : , 0,

() , 0.

nn

n

Nt

TX Xn

Nt nT t t

Zt J t

=++ ≥

=

≤≥

=≥

(11.8)

As usual, the transition probability for the process

(

)

(), 0ZZtT

=

≥ is designed

by:

(

)

() () ()

ij

tPZt jZti

φ

=

==

(11.9)

and the stochastic processes ( ( ), ),( ( ), )Nt t Zt t

+

+

∈∈are respectively the

Markov renewal counting and the semi-Markov processes.

To give the financial interpretation of our model, let us define on the probability

space

()

,,PΩℑ , the following filtration ( , )

t

t

+

ℑ= ℑ ∈ ,

(( ,( , )), ( )).

tnnn

J

XnNt

σ

σ

ℑ= ≤ (11.10)

Given

ℑ

t

, let us consider the random time interval

() ()1

,

Nt Nt

TT

+

⎡

⎤

⎣

⎦

on which we

define the new stochastic process

((), )St t

+

∈ , representing the value of the

considered financial asset, as the solution of the stochastic differential equation: