Brealey, Myers. Principles of Corporate Finance. 7th edition

Подождите немного. Документ загружается.

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

I. Value 4. The Value of Common

Stocks

© The McGraw−Hill

Companies, 2003

annual growth of 6.6 percent.

5

This, together with the dividend yield, gave an esti-

mate of the cost of equity capital:

An alternative approach to estimating long-run growth starts with the payout

ratio, the ratio of dividends to earnings per share (EPS). For Pinnacle, this was fore-

casted at 43 percent. In other words, each year the company was plowing back into

the business about 57 percent of earnings per share:

Also, Pinnacle’s ratio of earnings per share to book equity per share was about

11 percent. This is its return on equity, or ROE:

If Pinnacle earns 11 percent of book equity and reinvests 57 percent of that, then

book equity will increase by .57 .11 .063, or 6.3 percent. Earnings and divi-

dends per share will also increase by 6.3 percent:

Dividend growth rate g plowback ratio ROE .57 .11 .063

That gives a second estimate of the market capitalization rate:

Although this estimate of the market capitalization rate for Pinnacle stock seems

reasonable enough, there are obvious dangers in analyzing any single firm’s stock

with the constant-growth DCF formula. First, the underlying assumption of regu-

lar future growth is at best an approximation. Second, even if it is an acceptable ap-

proximation, errors inevitably creep into the estimate of g. Thus our two methods

for calculating the cost of equity give similar answers. That was a lucky chance; dif-

ferent methods can sometimes give very different answers.

Remember, Pinnacle’s cost of equity is not its personal property. In well-

functioning capital markets investors capitalize the dividends of all securities in

Pinnacle’s risk class at exactly the same rate. But any estimate of r for a single

common stock is “noisy” and subject to error. Good practice does not put too

much weight on single-company cost-of-equity estimates. It collects samples of

similar companies, estimates r for each, and takes an average. The average gives

a more reliable benchmark for decision making.

Table 4.2 shows DCF cost-of-equity estimates for Pinnacle West and 10 other

electric utilities in May 2001. These utilities are all stable, mature companies for

which the constant-growth DCF formula ought to work. Notice the variation in the

cost-of-equity estimates. Some of the variation may reflect differences in the risk,

but some is just noise. The average estimate is 10.7 percent.

r

DIV

1

P

0

g .033 .063 .096, or 9.6%

Return on equity ROE

EPS

book equity per share

.11

Plowback ratio 1 payout ratio 1

DIV

EPS

1 .43 .57

r

DIV

1

P

0

g .033 .066 .099, or 9.9%

66 PART I Value

5

In this calculation we’re assuming that earnings and dividends are forecasted to grow forever at the

same rate g. We’ll show how to relax this assumption later in this chapter. The growth rate was based

on the average earnings growth forecasted by Value Line and IBES. IBES compiles and averages fore-

casts made by security analysts. Value Line publishes its own analysts’ forecasts

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

I. Value 4. The Value of Common

Stocks

© The McGraw−Hill

Companies, 2003

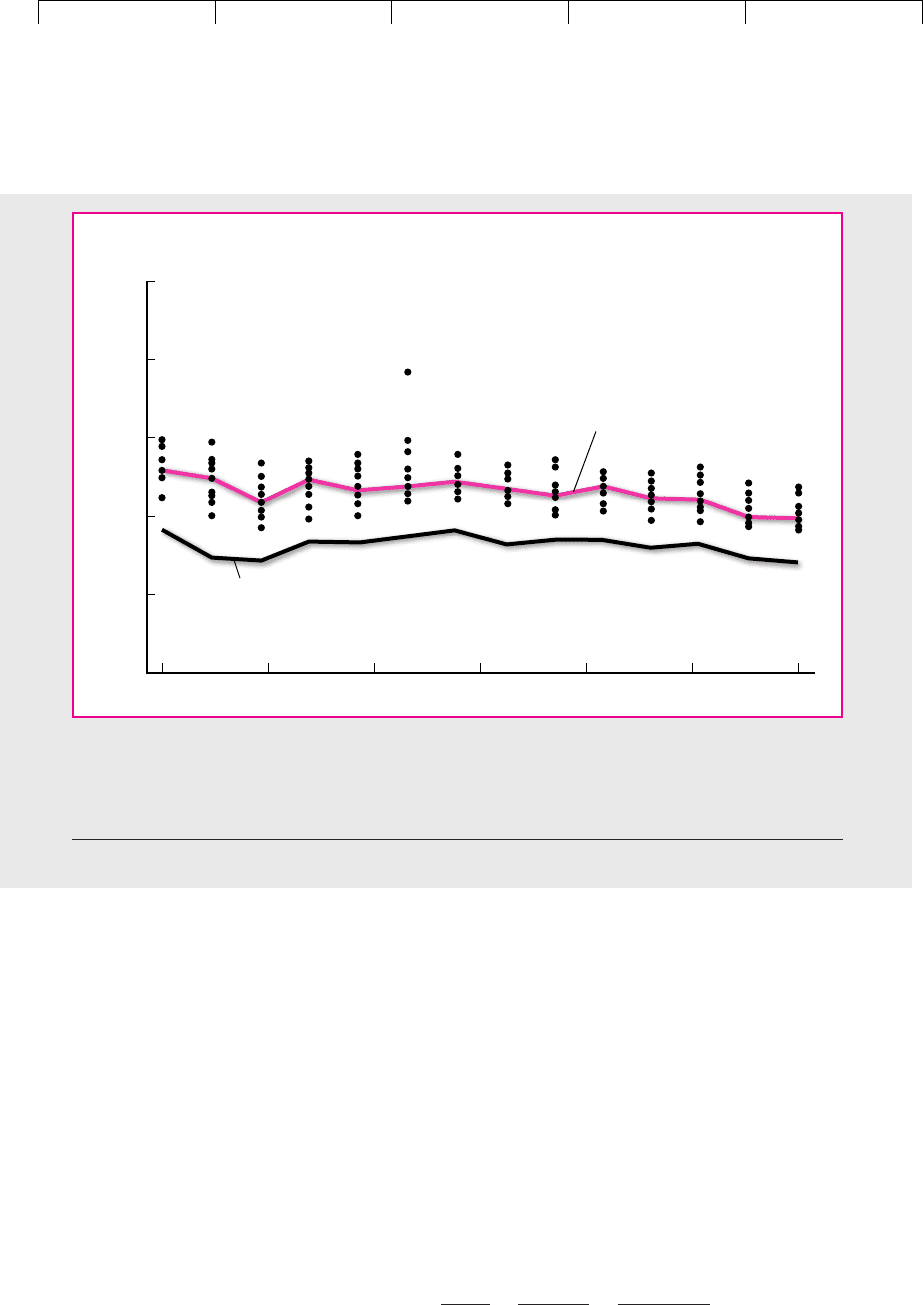

Figure 4.2 shows DCF costs of equity estimated at six-month intervals for a sam-

ple of electric utilities over a seven-year period. The burgundy line indicates the

median cost-of-equity estimates, which seem to lie about 3 percentage points

above the 10-year Treasury bond yield. The dots show the scatter of individual es-

timates. Again, most of this scatter is probably noise.

Some Warnings about Constant-Growth Formulas

The simple constant-growth DCF formula is an extremely useful rule of thumb, but

no more than that. Naive trust in the formula has led many financial analysts to

silly conclusions.

We have stressed the difficulty of estimating r by analysis of one stock only. Try

to use a large sample of equivalent-risk securities. Even that may not work, but at

least it gives the analyst a fighting chance, because the inevitable errors in estimat-

ing r for a single security tend to balance out across a broad sample.

In addition, resist the temptation to apply the formula to firms having high cur-

rent rates of growth. Such growth can rarely be sustained indefinitely, but the

constant-growth DCF formula assumes it can. This erroneous assumption leads to

an overestimate of r.

Consider Growth-Tech, Inc., a firm with DIV

1

$.50 and P

0

$50. The firm has

plowed back 80 percent of earnings and has had a return on equity (ROE) of 25 per-

cent. This means that in the past

Dividend growth rate plowback ratio ROE .80 .25 .20

The temptation is to assume that the future long-term growth rate g also equals

.20. This would imply

r

.50

50.00

.20 .21

CHAPTER 4 The Value of Common Stocks 67

Stock Price, Dividend, Dividend Yield, Growth Cost of Equity,

P

0

DIV

1

DIV

1

/P

0

Rate, grⴝ DIV

1

/P

0

ⴙ g

American Corp. $41.71 $2.64 6.3% 3.8% 10.1%

CH Energy Corp. 43.85 2.20 5.0 2.0 7.0

CLECO Corp. 46.00 .92 2.0 8.8 10.8

DPL, Inc. 30.27 1.03 3.4 9.6 13.0

Hawaiian Electric 36.69 2.54 6.9 2.6 9.5

Idacorp 39.42 1.97 5.0 5.7 10.7

Pinnacle West 49.16 1.60 3.3 6.6 9.9

Potomac Electric 22.00 1.75 8.0 5.7 13.7

Puget Energy 23.49 1.93 8.2 4.8 13.0

TECO Energy 31.38 1.44 4.6 7.7 12.3

UIL Holdings 48.21 2.93 6.1 1.9 8.0

Average 10.7%

TABLE 4.2

DCF cost-of-equity estimates for electric utilities in 2001.

Source: The Brattle Group, Inc.

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

I. Value 4. The Value of Common

Stocks

© The McGraw−Hill

Companies, 2003

But this is silly. No firm can continue growing at 20 percent per year forever, except

possibly under extreme inflationary conditions. Eventually, profitability will fall

and the firm will respond by investing less.

In real life the return on equity will decline gradually over time, but for sim-

plicity let’s assume it suddenly drops to 16 percent at year 3 and the firm responds

by plowing back only 50 percent of earnings. Then g drops to .50(.16) .08.

Table 4.3 shows what’s going on. Growth-Tech starts year 1 with assets of $10.00.

It earns $2.50, pays out 50 cents as dividends, and plows back $2. Thus it starts year

2 with assets of $10 2 $12. After another year at the same ROE and payout, it

starts year 3 with assets of $14.40. However, ROE drops to .16, and the firm earns

only $2.30. Dividends go up to $1.15, because the payout ratio increases, but the

firm has only $1.15 to plow back. Therefore subsequent growth in earnings and

dividends drops to 8 percent.

Now we can use our general DCF formula to find the capitalization rate r:

Investors in year 3 will view Growth-Tech as offering 8 percent per year dividend

growth. We will apply the constant-growth formula:

P

0

DIV

1

1 r

DIV

2

11 r2

2

DIV

3

P

3

11 r2

3

68 PART I Value

25

Cost of equity,

percent

20

15

10

5

0

Jan. 86

Jan. 87 Jan. 88 Jan. 89 Jan. 90 Jan. 91 Jan. 92

10-year Treasury

bond yield

Median

estimate

FIGURE 4.2

DCF cost-of-equity estimates for a sample of 17 utilities. The median estimates (burgundy line) track long-

term interest rates fairly well. (The blue line is the 10-year Treasury yield.) The dots show the scatter of

the cost-of-equity estimates for individual companies.

Source: S. C. Myers and L. S. Borucki, “Discounted Cash Flow Estimates of the Cost of Equity Capital—A Case Study,”

Financial Markets, Institutions and Instruments 3 (August 1994), pp. 9–45.

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

I. Value 4. The Value of Common

Stocks

© The McGraw−Hill

Companies, 2003

We have to use trial and error to find the value of r that makes P

0

equal $50. It turns

out that the r implicit in these more realistic forecasts is approximately .099, quite

a difference from our “constant-growth” estimate of .21.

DCF Valuation with Varying Growth Rates

Our present value calculations for Growth-Tech used a two-stage DCF valuation

model. In the first stage (years 1 and 2), Growth-Tech is highly profitable (ROE

25 percent), and it plows back 80 percent of earnings. Book equity, earnings, and

dividends increase by 20 percent per year. In the second stage, starting in year 3,

profitability and plowback decline, and earnings settle into long-term growth at 8

percent. Dividends jump up to $1.15 in year 3, and then also grow at 8 percent.

Growth rates can vary for many reasons. Sometimes growth is high in the short

run not because the firm is unusually profitable, but because it is recovering from

an episode of low profitability. Table 4.4 displays projected earnings and dividends

for Phoenix.com, which is gradually regaining financial health after a near melt-

down. The company’s equity is growing at a moderate 4 percent. ROE in year 1 is

only 4 percent, however, so Phoenix has to reinvest all its earnings, leaving no cash

for dividends. As profitability increases in years 2 and 3, an increasing dividend

can be paid. Finally, starting in year 4, Phoenix settles into steady-state growth,

with equity, earnings, and dividends all increasing at 4 percent per year.

Assume the cost of equity is 10 percent. Then Phoenix shares should be worth

$9.13 per share:

PV (first-stage dividends) PV (second-stage dividends)

We could go on to three- or even four-stage valuation models—but you get the

idea. Two warnings, however. First, it’s almost always worthwhile to lay out a simple

P

0

0

1.1

.31

11.12

2

.65

11.12

3

1

11.12

3

.67

1.10 .042

$9.13

.50

1 r

.60

11 r2

2

1.15

11 r2

3

1

11 r2

3

1.24

r .08

P

0

DIV

1

1 r

DIV

2

11 r2

2

DIV

3

11 r2

3

1

11 r2

3

DIV

4

r .08

P

3

DIV

4

r .08

CHAPTER 4

The Value of Common Stocks 69

Year

1234

Book equity 10.00 12.00 14.40 15.55

Earnings per share, EPS 2.50 3.00 2.30 2.49

Return on equity, ROE .25 .25 .16 .16

Payout ratio .20 .20 .50 .50

Dividends per share, DIV .50 .60 1.15 1.24

Growth rate of dividends (%) — 20 92 8

TABLE 4.3

Forecasted earnings and dividends for

Growth-Tech. Note the changes in year

3: ROE and earnings drop, but payout

ratio increases, causing a big jump in

dividends. However, subsequent

growth in earnings and dividends falls

to 8 percent per year. Note that the

increase in equity equals the earnings

not paid out as dividends.

再

再

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

I. Value 4. The Value of Common

Stocks

© The McGraw−Hill

Companies, 2003

spreadsheet, like Table 4.3 or 4.4, to assure that your dividend projections are consis-

tent with the company’s earnings and the investments required to grow. Second, do

not use DCF valuation formulas to test whether the market is correct in its assessment

of a stock’s value. If your estimate of the value is different from that of the market, it

is probably because you have used poor dividend forecasts. Remember what we said

at the beginning of this chapter about simple ways of making money on the stock

market: There aren’t any.

70 PART I

Value

Year

123 4

Book equity 10.00 10.40 10.82 11.25

Earnings per share, EPS .40 .73 1.08 1.12

Return on equity, ROE .04 .07 .10 .10

Dividends per share, DIV 0 .31 .65 .67

Growth rate of dividends (%) — — 110 4

TABLE 4.4

Forecasted earnings and

dividends for Phoenix.com. The

company can initiate and increase

dividends as profitability (ROE)

recovers. Note that the increase in

book equity equals the earnings

not paid out as dividends.

4.4 THE LINK BETWEEN STOCK PRICE AND EARNINGS

PER SHARE

Investors often use the terms growth stocks and income stocks. They buy growth

stocks primarily for the expectation of capital gains, and they are interested in the

future growth of earnings rather than in next year’s dividends. On the other hand,

they buy income stocks primarily for the cash dividends. Let us see whether these

distinctions make sense.

Imagine first the case of a company that does not grow at all. It does not plow

back any earnings and simply produces a constant stream of dividends. Its stock

would resemble the perpetual bond described in the last chapter. Remember that

the return on a perpetuity is equal to the yearly cash flow divided by the present

value. The expected return on our share would thus be equal to the yearly dividend

divided by the share price (i.e., the dividend yield). Since all the earnings are paid

out as dividends, the expected return is also equal to the earnings per share di-

vided by the share price (i.e., the earnings–price ratio). For example, if the dividend

is $10 a share and the stock price is $100, we have

Expected return dividend yield earnings–price ratio

The price equals

P

0

DIV

1

r

EPS

1

r

10.00

.10

100

.10

10.00

100

EPS

1

P

0

DIV

1

P

0

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

I. Value 4. The Value of Common

Stocks

© The McGraw−Hill

Companies, 2003

The expected return for growing firms can also equal the earnings–price ratio.

The key is whether earnings are reinvested to provide a return equal to the market

capitalization rate. For example, suppose our monotonous company suddenly

hears of an opportunity to invest $10 a share next year. This would mean no divi-

dend at t 1. However, the company expects that in each subsequent year the proj-

ect would earn $1 per share, so that the dividend could be increased to $11 a share.

Let us assume that this investment opportunity has about the same risk as the

existing business. Then we can discount its cash flow at the 10 percent rate to find

its net present value at year 1:

Thus the investment opportunity will make no contribution to the company’s

value. Its prospective return is equal to the opportunity cost of capital.

What effect will the decision to undertake the project have on the company’s share

price? Clearly none. The reduction in value caused by the nil dividend in year 1 is

exactly offset by the increase in value caused by the extra dividends in later years.

Therefore, once again the market capitalization rate equals the earnings–price ratio:

Table 4.5 repeats our example for different assumptions about the cash flow gen-

erated by the new project. Note that the earnings–price ratio, measured in terms of

EPS

1

, next year’s expected earnings, equals the market capitalization rate (r) only

when the new project’s NPV 0. This is an extremely important point—managers

frequently make poor financial decisions because they confuse earnings–price ra-

tios with the market capitalization rate.

In general, we can think of stock price as the capitalized value of average earnings

under a no-growth policy, plus PVGO, the present value of growth opportunities:

P

0

EPS

1

r

PVGO

r

EPS

1

P

0

10

100

.10

Net present value per share at year 1 10

1

.10

0

CHAPTER 4 The Value of Common Stocks 71

Project’s Impact

Project Rate Incremental Project NPV on Share Price Share Price EPS

1

of Return Cash Flow, C in Year 1* in Year 0

†

in Year 0, P

0

P

0

r

.05 $ .50 $ 5.00 $ 4.55 $ 95.45 .105 .10

.10 1.00 0 0 100.00 .10 .10

.15 1.50 5.00 4.55 104.55 .096 .10

.20 2.00 10.00 9.09 109.09 .092 .10

.25 2.50 15.00 13.64 113.64 .088 .10

TABLE 4.5

Effect on stock price of investing an additional $10 in year 1 at different rates of return. Notice that the earnings–price

ratio overestimates r when the project has negative NPV and underestimates it when the project has positive NPV.

*Project costs $10.00 (EPS

1

). NPV 10 C/r, where r .10.

†

NPV is calculated at year 1. To find the impact on P

0

, discount for one year at r .10.

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

I. Value 4. The Value of Common

Stocks

© The McGraw−Hill

Companies, 2003

The earnings–price ratio, therefore, equals

It will underestimate r if PVGO is positive and overestimate it if PVGO is negative.

The latter case is less likely, since firms are rarely forced to take projects with nega-

tive net present values.

Calculating the Present Value of Growth Opportunities

for Fledgling Electronics

In our last example both dividends and earnings were expected to grow, but

this growth made no net contribution to the stock price. The stock was in this

sense an “income stock.” Be careful not to equate firm performance with the

growth in earnings per share. A company that reinvests earnings at below

the market capitalization rate may increase earnings but will certainly reduce

the share value.

Now let us turn to that well-known growth stock, Fledgling Electronics. You may

remember that Fledgling’s market capitalization rate, r, is 15 percent. The company

is expected to pay a dividend of $5 in the first year, and thereafter the dividend is

predicted to increase indefinitely by 10 percent a year. We can, therefore, use the

simplified constant-growth formula to work out Fledgling’s price:

Suppose that Fledgling has earnings per share of $8.33. Its payout ratio is then

In other words, the company is plowing back 1 .6, or 40 percent of earnings. Sup-

pose also that Fledgling’s ratio of earnings to book equity is ROE .25. This ex-

plains the growth rate of 10 percent:

Growth rate g plowback ratio ROE .4 .25 .10

The capitalized value of Fledgling’s earnings per share if it had a no-growth pol-

icy would be

But we know that the value of Fledgling stock is $100. The difference of $44.44 must

be the amount that investors are paying for growth opportunities. Let’s see if we

can explain that figure.

Each year Fledgling plows back 40 percent of its earnings into new assets. In the

first year Fledgling invests $3.33 at a permanent 25 percent return on equity. Thus

the cash generated by this investment is .25 3.33 $.83 per year starting at t

2. The net present value of the investment as of t 1 is

NPV

1

3.33

.83

.15

$2.22

EPS

1

r

8.33

.15

$55.56

Payout ratio

DIV

1

EPS

1

5.00

8.33

.6

P

0

DIV

1

r g

5

.15 .10

$100

EPS

P

0

r a1

PVGO

P

0

b

72 PART I Value

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

I. Value 4. The Value of Common

Stocks

© The McGraw−Hill

Companies, 2003

Everything is the same in year 2 except that Fledgling will invest $3.67, 10 percent

more than in year 1 (remember g .10). Therefore at t 2 an investment is made

with a net present value of

Thus the payoff to the owners of Fledgling Electronics stock can be represented

as the sum of (1) a level stream of earnings, which could be paid out as cash divi-

dends if the firm did not grow, and (2) a set of tickets, one for each future year, rep-

resenting the opportunity to make investments having positive NPVs. We know

that the first component of the value of the share is

The first ticket is worth $2.22 in t 1, the second is worth $2.22 1.10 $2.44 in t

2, the third is worth $2.44 1.10 $2.69 in t 3. These are the forecasted cash val-

ues of the tickets. We know how to value a stream of future cash values that grows

at 10 percent per year: Use the constant-growth DCF formula, replacing the fore-

casted dividends with forecasted ticket values:

Now everything checks:

Share price present value of level stream of earnings

present value of growth opportunities

$55.56 $44.44

$100

Why is Fledgling Electronics a growth stock? Not because it is expanding at

10 percent per year. It is a growth stock because the net present value of its fu-

ture investments accounts for a significant fraction (about 44 percent) of the

stock’s price.

Stock prices today reflect investors’ expectations of future operating and invest-

ment performance. Growth stocks sell at high price–earnings ratios because in-

vestors are willing to pay now for expected superior returns on investments that

have not yet been made.

6

Some Examples of Growth Opportunities?

Stocks like Microsoft, Dell Computer, and Wal-Mart are often described as growth

stocks, while those of mature firms like Kellogg, Weyerhaeuser, and Exxon Mobil

are regarded as income stocks. Let us check it out. The first column of Table 4.6

EPS

1

r

PVGO

Present value of growth opportunities PVGO

NPV

1

r g

2.22

.15 .10

$44.44

Present value of level stream of earnings

EPS

1

r

8.33

.15

$55.56

NPV

2

3.33 1.10

.83 1.10

.15

$2.44

CHAPTER 4 The Value of Common Stocks 73

6

Michael Eisner, the chairman of Walt Disney Productions, made the point this way: “In school you had

to take the test and then be graded. Now we’re getting graded, and we haven’t taken the test.” This was

in late 1985, when Disney stock was selling at nearly 20 times earnings. See Kathleen K. Wiegner, “The

Tinker Bell Principle,” Forbes (December 2, 1985), p. 102.

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

I. Value 4. The Value of Common

Stocks

© The McGraw−Hill

Companies, 2003

shows the stock price for each of these companies in October 2001. The remaining

columns estimate PVGO as a proportion of the stock price.

Remember, if there are no growth opportunities, present value equals the av-

erage future earnings from existing assets discounted at the market capitaliza-

tion rate. We used analysts’ forecasts for 2002 as a measure of the earning

power of existing assets. You can see that most of the value of the growth stocks

comes from PVGO, that is, from investors’ expectations that the companies will

be able to earn more than the cost of capital on their future investments. How-

ever, Weyerhaeuser, though usually regarded as an income stock, does pretty

well on the PVGO scale. But the most striking growth stock is Amazon.com. Its

earnings have been consistently negative, so its PVGO accounts for more than

100 percent of its stock price. None of the company’s value can be based on its

current earnings. The value comes entirely from future earnings and the NPV

of its future investments.

7

Some companies have such extensive growth opportunities that they prefer to

pay no dividends for long periods of time. For example, up to the time that we

wrote this chapter, “glamour stocks” such as Microsoft and Dell Computer had

never paid a dividend, because any cash paid out to investors would have meant

either slower growth or raising capital by some other means. Investors were happy

to forgo immediate cash dividends in exchange for increasing earnings and the ex-

pectation of high dividends some time in the future.

74 PART I

Value

Stock Price, P

0

Cost of PVGO PVGO, percent

Stock (October 2001) EPS* Equity, r

†

ⴝ P

0

ⴚ EPS/r of Stock Price

Income stocks:

Chubb $77.35 $4.90 .088 $21.67 28

Exxon Mobil 42.29 2.13 .072 12.71 30

Kellogg 29.00 1.42 .056 3.64 13

Weyerhaeuser 50.45 3.21 .128 25.37 50

Growth stocks:

Amazon.com 8.88 .30 .24 10.13 114

Dell Computer 23.66 .76 .22 20.20 85

Microsoft 56.38 1.88 .184 46.16 82

Wal-Mart 52.90 1.70 .112 37.72 71

TABLE 4.6

Estimated PVGOs.

*EPS is defined as the average earnings under a no-growth policy. As an estimate of EPS, we used the forecasted earnings per share for

2002. Source: MSN Money (moneycentral.msn.com).

†

The market capitalization rate was estimated using the capital asset pricing model. We describe this model and how to use it in Sections

8.2 and 9.2. For this example, we used a market risk premium of 8 percent and a risk-free interest rate of 4 percent.

7

However, Amazon’s reported earnings probably understate its earnings potential. Amazon is growing

very rapidly, and some of the investments necessary to finance that growth are written off as expenses,

thus reducing current income. Absent these “investment expenses,” Amazon’s current income would

probably be positive. We discuss the problems encountered in measuring earnings and profitability in

Chapter 12.

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

I. Value 4. The Value of Common

Stocks

© The McGraw−Hill

Companies, 2003

What Do Price–Earnings Ratios Mean?

The price–earnings ratio is part of the everyday vocabulary of investors in the

stock market. People casually refer to a stock as “selling at a high P/E.” You can

look up P/Es in stock quotations given in the newspaper. (However, the newspa-

per gives the ratio of current price to the most recent earnings. Investors are more

concerned with price relative to future earnings.) Unfortunately, some financial an-

alysts are confused about what price–earnings ratios really signify and often use

the ratios in odd ways.

Should the financial manager celebrate if the firm’s stock sells at a high P/E?

The answer is usually yes. The high P/E shows that investors think that the firm

has good growth opportunities (high PVGO), that its earnings are relatively safe

and deserve a low capitalization rate (low r), or both. However, firms can have high

price–earnings ratios not because price is high but because earnings are low. Afirm

which earns nothing (EPS 0) in a particular period will have an infinite P/E as

long as its shares retain any value at all.

Are relative P/Es helpful in evaluating stocks? Sometimes. Suppose you own

stock in a family corporation whose shares are not actively traded. What are those

shares worth? A decent estimate is possible if you can find traded firms that have

roughly the same profitability, risks, and growth opportunities as your firm. Mul-

tiply your firm’s earnings per share by the P/E of the counterpart firms.

Does a high P/E indicate a low market capitalization rate? No. There is no reli-

able association between a stock’s price–earnings ratio and the capitalization rate

r. The ratio of EPS to P

0

measures r only if PVGO 0 and only if reported EPS is

the average future earnings the firm could generate under a no-growth policy. An-

other reason P/Es are hard to interpret is that the figure for earnings depends on

the accounting procedures for calculating revenues and costs. We will discuss the

potential biases in accounting earnings in Chapter 12.

CHAPTER 4

The Value of Common Stocks 75

4.5 VALUING A BUSINESS BY DISCOUNTED CASH FLOW

Investors routinely buy and sell shares of common stock. Companies frequently

buy and sell entire businesses. In 2001, for example, when Diageo sold its Pillsbury

operation to General Mills for $10.4 billion, you can be sure that both companies

burned a lot of midnight oil to make sure that the deal was fairly priced.

Do the discounted-cash-flow formulas we presented in this chapter work for

entire businesses as well as for shares of common stock? Sure: It doesn’t matter

whether you forecast dividends per share or the total free cash flow of a business.

Value today always equals future cash flow discounted at the opportunity cost of

capital.

Valuing the Concatenator Business

Rumor has it that Establishment Industries is interested in buying your company’s

concatenator manufacturing operation. Your company is willing to sell if it can get

the full value of this rapidly growing business. The problem is to figure out what

its true present value is.

Table 4.7 gives a forecast of free cash flow (FCF) for the concatenator business. Free

cash flow is the amount of cash that a firm can pay out to investors after paying for