Brealey, Myers. Principles of Corporate Finance. 7th edition

Подождите немного. Документ загружается.

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

I. Value 4. The Value of Common

Stocks

© The McGraw−Hill

Companies, 2003

86 PART I Value

d. Suppose that competition will catch up with Growth-Tech by year 4, so that it can

earn only its cost of capital on any investments made in year 4 or subsequently.

What is Growth-Tech stock worth now under this assumption? (Make additional

assumptions if necessary.)

16. Look up Hawaiian Electric Co. (HI) on the Standard & Poor’s Market Insight website

(www

.mhhe.com/edumarketinsight

). Hawaiian Electric was one of the companies in

Table 4.2. That table was constructed in 2001.

a. What is the company’s dividend yield? How has it changed since 2001?

b. Table 4.2 projected growth of 2.6 percent. How fast have the company’s dividends

and EPS actually grown since 2001?

c. Calculate a sustainable growth rate for the company based on its five-year average

return on equity (ROE) and plowback ratio.

d. Given this updated information, would you modify the cost-of-equity estimate

given in Table 4.2? Explain.

17. Browse through the companies in the Standard & Poor’s Market Insight website

(www

.mhhe.com/edumarketinsight

). Find three or four companies for which the

earnings-price ratio reported on the website drastically understates the market capi-

talization rate r for the company. (Hint: you don’t have to estimate r to answer this

question. You know that r must be higher than current interest rates on U.S. govern-

ment notes and bonds.)

18. The Standard & Poor’s Market Insight website (www

.mhhe.com/edumarketinsight)

contains information all of the companies in Table 4.6 except for Chubb and Weyer-

haeuser. Update the calculations of PVGO as a percentage of stock price. For simplicity

use the costs of equity given in Table 4.6. You will need to track down an updated fore-

cast of EPS, for example from MSN money (www

.moneycentral.msn.com

) of Yahoo

(http://finance.yahoo.com).

19. Compost Science, Inc. (CSI), is in the business of converting Boston’s sewage sludge

into fertilizer. The business is not in itself very profitable. However, to induce CSI to re-

main in business, the Metropolitan District Commission (MDC) has agreed to pay

whatever amount is necessary to yield CSI a 10 percent book return on equity. At the

end of the year CSI is expected to pay a $4 dividend. It has been reinvesting 40 percent

of earnings and growing at 4 percent a year.

a. Suppose CSI continues on this growth trend. What is the expected long-run rate of

return from purchasing the stock at $100? What part of the $100 price is

attributable to the present value of growth opportunities?

b. Now the MDC announces a plan for CSI to treat Cambridge sewage. CSI’s plant will,

therefore, be expanded gradually over five years. This means that CSI will have to

reinvest 80 percent of its earnings for five years. Starting in year 6, however, it will

again be able to pay out 60 percent of earnings. What will be CSI’s stock price once

this announcement is made and its consequences for CSI are known?

20. List at least four different formulas for calculating PV(horizon value) in a two-stage

DCF valuation of a business. For each formula, describe a situation where that formula

would be the best choice.

21. Look again at Table 4.7.

a. How do free cash flow and present value change if asset growth rate is only 15

percent in years 1 to 5? If value declines, explain why.

b. Suppose the business is a publicly traded company with one million shares outstand-

ing. Then the company issues new stock to cover the present value of negative free cash

flow for years 1 to 6. How many shares will be issued and at what price?

c. Value the company’s one million existing shares by the two methods described in

Section 4.5.

22. Icarus Air has one million shares outstanding and expects to earn a constant $10 mil-

lion per year on its existing assets. All earnings will be paid out as dividends. Suppose

Visit us at www.mhhe.com/bm7e

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

I. Value 4. The Value of Common

Stocks

© The McGraw−Hill

Companies, 2003

CHAPTER 4 The Value of Common Stocks 87

that next year Icarus plans to double in size by issuing an additional one million shares

at $100 a share. Everything will be the same as before but twice as big. Thus from year

2 onward the company earns a constant $20 million, all of which is paid out as divi-

dends on the 20 million shares. What is the value of the company? What is the value of

each existing Icarus Air share?

23. Look one more time at Table 4.1, which applies the DCF stock valuation formula to

Fledgling Electronics. The CEO, having just learned that stock value is the present value

of future dividends, proposes that Fledgling pay a bumper dividend of $15 a share in

period 1. The extra cash would have to be raised by an issue of new shares. Recalculate

Table 4.1 assuming that profits and payout ratios in all subsequent years are un-

changed. You should find that the total present value of dividends per existing share is

unchanged at $100. Why?

MINI-CASE

1. Look again at Tables 4.3 (Growth-Tech) and 4.7 (Concatenator Manufacturing). Note

the discontinuous increases in dividends and free cash flow when asset growth slows

down. Now look at your answer to Practice Question 11: Dividends are expected to

grow smoothly, although at a lower rate after year 3. Is there an error or hidden incon-

sistency in Practice Question 11? Write down a general rule or procedure for deciding

how to forecast dividends or free cash flow.

2. The constant-growth DCF formula

is sometimes written as

where BVPS is book equity value per share, b is the plowback ratio, and ROE is the ra-

tio of earnings per share to BVPS. Use this equation to show how the price-to-book ra-

tio varies as ROE changes. What is price-to-book when ROE r?

3. Portfolio managers are frequently paid a proportion of the funds under manage-

ment. Suppose you manage a $100 million equity portfolio offering a dividend yield

(DIV

1

/P

0

) of 5 percent. Dividends and portfolio value are expected to grow at a con-

stant rate. Your annual fee for managing this portfolio is .5 percent of portfolio value

and is calculated at the end of each year. Assuming that you will continue to man-

age the portfolio from now to eternity, what is the present value of the management

contract?

P

0

ROE11 b2BVPS

r bROE

P

0

DIV

1

r g

CHALLENGE

QUESTIONS

Visit us at www.mhhe.com/bm7e

Reeby Sports

Ten years ago, in 1993, George Reeby founded a small mail-order company selling high-

quality sports equipment. Reeby Sports has grown steadily and been consistently profitable

(see Table 4.8). The company has no debt and the equity is valued in the company’s books

at nearly $41 million (Table 4.9). It is still wholly owned by George Reeby.

George is now proposing to take the company public by the sale of 90,000 of his existing

shares. The issue would not raise any additional cash for the company, but it would allow

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

I. Value 4. The Value of Common

Stocks

© The McGraw−Hill

Companies, 2003

Visit us at www.mhhe.com/bm7e

88 PART I Value

George to cash in on part of his investment. It would also make it easier to raise the sub-

stantial capital sums that the firm would later need to finance expansion.

George’s business has been mainly on the East Coast of the United States, but he plans to

expand into the Midwest in 2005. This will require a substantial investment in new ware-

house space and inventory. George is aware that it will take time to build up a new customer

base, and in the meantime there is likely to be a temporary dip in profits. However, if the

venture is successful, the company should be back to its current 12 percent return on book

equity by 2010.

George settled down to estimate what his shares are worth. First he estimated the prof-

its and investment through 2010 (Tables 4.10 and 4.11). The company’s net working capital

includes a growing proportion of cash and marketable securities which would help to meet

the cost of the expansion into the Midwest. Nevertheless, it seemed likely that the company

would need to raise about $4.3 million in 2005 by the sale of new shares. (George distrusted

banks and was not prepared to borrow to finance the expansion.)

Until the new venture reached full profitability, dividend payments would have to be

restricted to conserve cash, but from 2010 onward George expected the company to pay

out about 40 percent of its net profits. As a first stab at valuing the company, George as-

sumed that after 2010 it would earn 12 percent on book equity indefinitely and that the

cost of capital for the firm was about 10 percent. But he also computed a more conserva-

tive valuation, which recognized that the mail-order sports business was likely to get in-

tensely competitive by 2010. He also looked at the market valuation of a comparable busi-

ness on the West Coast, Molly Sports. Molly’s shares were currently priced at 50 percent

above book value and were selling at a prospective price–earnings ratio of 12 and a divi-

dend yield of 3 percent.

George realized that a second issue of shares in 2005 would dilute his holdings. He set

about calculating the price at which these shares could be issued and the number of

shares that would need to be sold. That allowed him to work out the dividends per share

and to check his earlier valuation by calculating the present value of the stream of per-

share dividends.

Assets Liabilities and Equity

2002 2003 2002 2003

Cash & securities 3.12 3.61 Current liabilities 2.90 3.20

Other current assets 15.08 16.93

Net fixed assets 20.75 23.38 Equity 36.05 40.71

Total 38.95 43.91 Total 38.95 43.91

TABLE 4.9

Summary balance sheet for

year ending December 31st

(figures in $ millions).

Note: Reeby Sports has 200,000

common shares outstanding,

wholly owned by George Reeby.

1999 2000 2001 2002 2003

Cash flow 5.84 6.40 7.41 8.74 9.39

Depreciation 1.45 1.60 1.75 1.97 2.22

Pretax profits 4.38 4.80 5.66 6.77 7.17

Tax 1.53 1.68 1.98 2.37 2.51

Aftertax profits 2.85 3.12 3.68 4.40 4.66

TABLE 4.8

Summary income data (figures in

$ millions).

Note: Reeby Sports has never paid a

dividend and all the earnings have been

retained in the business.

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

I. Value 4. The Value of Common

Stocks

© The McGraw−Hill

Companies, 2003

Visit us at www.mhhe.com/bm7e

CHAPTER 4 The Value of Common Stocks 89

Questions

1. Use Tables 4.10 and 4.11 to forecast free cash flow for Reeby Sports from 2004 to 2010.

What is the present value of these cash flows in 2003, including PV(horizon value)

in 2010?

2. Use the information given for Molly Sports to check your forecast of horizon value.

What would you recommend as a reasonable range for the present value of Reeby

Sports?

3. What is the present value of a share of stock in the company? Give a reasonable range.

4. Reeby Sports will have to raise $4.3 million in 2005. Does this prospective share issue

affect the per-share value of Reeby Sports in 2003? Explain.

2004 2005 2006 2007 2008 2009 2010

Cash flow 10.47 11.87 7.74 8.40 9.95 12.67 15.38

Depreciation 2.40 3.10 3.12 3.17 3.26 3.44 3.68

Pretax profits 8.08 8.77 4.62 5.23 6.69 9.23 11.69

Tax 2.83 3.07 1.62 1.83 2.34 3.23 4.09

Aftertax profits 5.25 5.70 3.00 3.40 4.35 6.00 7.60

Dividends 2.00 2.00 2.50 2.50 2.50 2.50 3.00

Retained profits 3.25 3.70 .50 .90 1.85 3.50 4.60

TABLE 4.10

Forecasted profits and dividends (figures in $ millions).

2004 2005 2006 2007 2008 2009 2010

Gross investment

in fixed assets 4.26 10.50 3.34 3.65 4.18 5.37 6.28

Investments in net

working capital 1.39 .60 .28 .42 .93 1.57 2.00

Total 5.65 11.10 3.62 4.07 5.11 6.94 8.28

TABLE 4.11

Forecasted investment expenditures (figures in $ millions).

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

I. Value 5. Why Net Prsnt Value

Leads to Better

Investments Decisions

than Other Criteria

© The McGraw−Hill

Companies, 2003

CHAPTER FIVE

WHY NET PRESENT

VALUE LEADS TO

BETTER INVESTMENT

DECISIONS THAN

OTHER CRITERIA

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

I. Value 5. Why Net Prsnt Value

Leads to Better

Investments Decisions

than Other Criteria

© The McGraw−Hill

Companies, 2003

IN THE FIRST four chapters we introduced, at times surreptitiously, most of the basic principles of

the investment decision. In this chapter we begin by consolidating that knowledge. We then take

a look at three other measures that companies sometimes use when making investment decisions.

These are the project’s payback period, its book rate of return, and its internal rate of return. The

first two of these measures have little to do with whether the project will increase shareholders’

wealth. The project’s internal rate of return—if used correctly—should always identify projects that

increase shareholder wealth. However, we shall see that the internal rate of return sets several traps

for the unwary.

We conclude the chapter by showing how to cope with situations when the firm has only limited

capital. This raises two problems. One is computational. In simple cases we just choose those proj-

ects that give the highest NPV per dollar of investment. But capital constraints and project interac-

tions often create problems of such complexity that linear programming is needed to sort through

the possible alternatives. The other problem is to decide whether capital rationing really exists and

whether it invalidates net present value as a criterion for capital budgeting. Guess what? NPV, prop-

erly interpreted, wins out in the end.

91

Vegetron’s chief financial officer (CFO) is wondering how to analyze a proposed $1

million investment in a new venture called project X. He asks what you think.

Your response should be as follows: “First, forecast the cash flows generated by

project X over its economic life. Second, determine the appropriate opportunity

cost of capital. This should reflect both the time value of money and the risk in-

volved in project X. Third, use this opportunity cost of capital to discount the fu-

ture cash flows of project X. The sum of the discounted cash flows is called present

value (PV). Fourth, calculate net present value (NPV) by subtracting the $1 million

investment from PV. Invest in project X if its NPV is greater than zero.”

However, Vegetron’s CFO is unmoved by your sagacity. He asks why NPV is so

important.

Your reply: “Let us look at what is best for Vegetron stockholders. They want

you to make their Vegetron shares as valuable as possible.”

“Right now Vegetron’s total market value (price per share times the number of

shares outstanding) is $10 million. That includes $1 million cash we can invest in

project X. The value of Vegetron’s other assets and opportunities must therefore be

$9 million. We have to decide whether it is better to keep the $1 million cash and

reject project X or to spend the cash and accept project X. Let us call the value of the

new project PV. Then the choice is as follows:

5.1 A REVIEW OF THE BASICS

Market Value ($ millions)

Asset Reject Project X Accept Project X

Cash 1 0

Other assets 9 9

Project X 0 PV

10 9 ⫹ PV

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

I. Value 5. Why Net Prsnt Value

Leads to Better

Investments Decisions

than Other Criteria

© The McGraw−Hill

Companies, 2003

“Clearly project X is worthwhile if its present value, PV, is greater than $1 million,

that is, if net present value is positive.”

CFO: “How do I know that the PV of project X will actually show up in Veg-

etron’s market value?”

Your reply: “Suppose we set up a new, independent firm X, whose only asset is

project X. What would be the market value of firm X?

“Investors would forecast the dividends firm X would pay and discount

those dividends by the expected rate of return of securities having risks compa-

rable to firm X. We know that stock prices are equal to the present value of fore-

casted dividends.

“Since project X is firm X’s only asset, the dividend payments we would expect

firm X to pay are exactly the cash flows we have forecasted for project X. Moreover,

the rate investors would use to discount firm X’s dividends is exactly the rate we

should use to discount project X’s cash flows.

“I agree that firm X is entirely hypothetical. But if project X is accepted, investors

holding Vegetron stock will really hold a portfolio of project X and the firm’s other

assets. We know the other assets are worth $9 million considered as a separate ven-

ture. Since asset values add up, we can easily figure out the portfolio value once

we calculate the value of project X as a separate venture.

“By calculating the present value of project X, we are replicating the process by

which the common stock of firm X would be valued in capital markets.”

CFO: “The one thing I don’t understand is where the discount rate comes from.”

Your reply: “I agree that the discount rate is difficult to measure precisely. But it

is easy to see what we are trying to measure. The discount rate is the opportunity

cost of investing in the project rather than in the capital market. In other words, in-

stead of accepting a project, the firm can always give the cash to the shareholders

and let them invest it in financial assets.

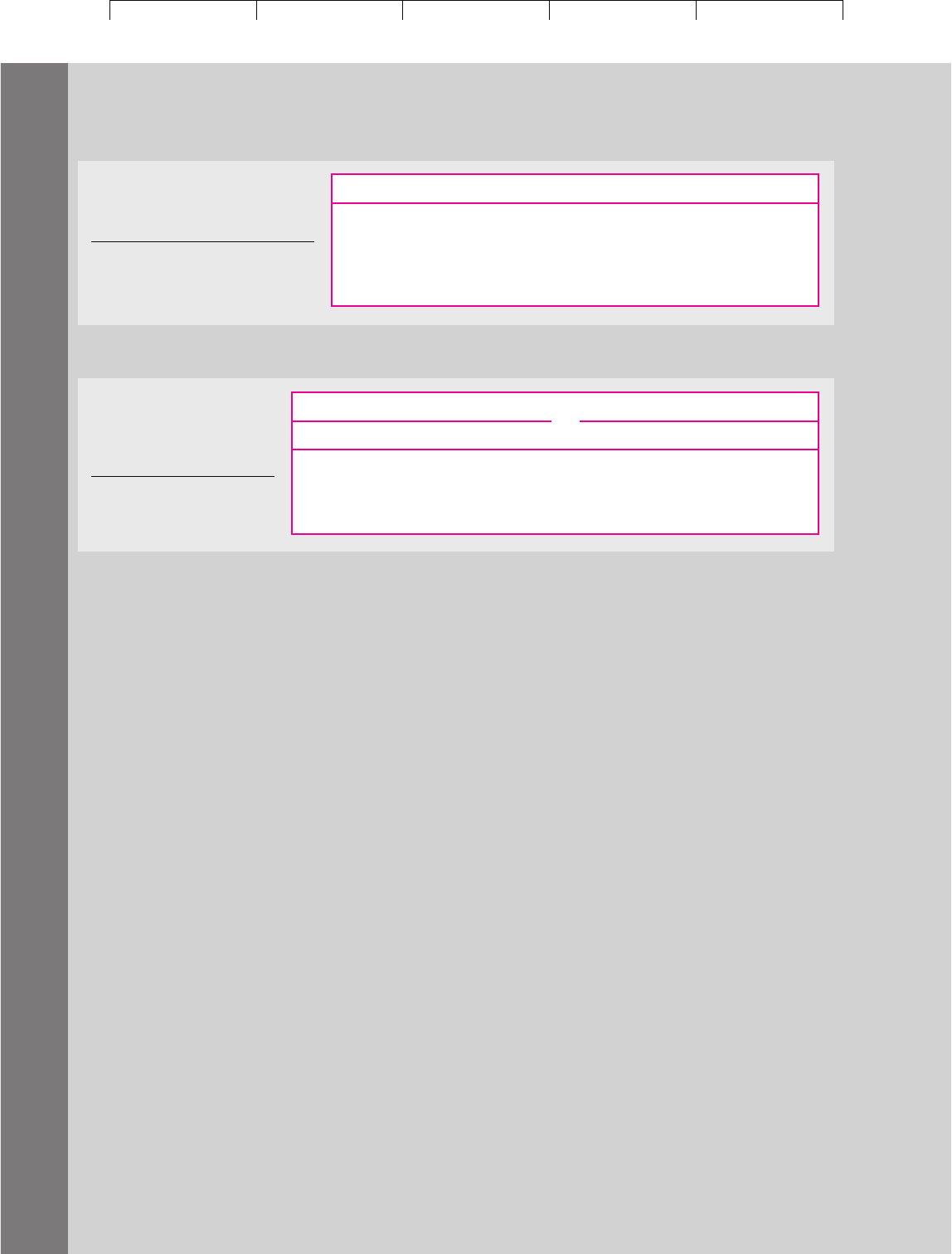

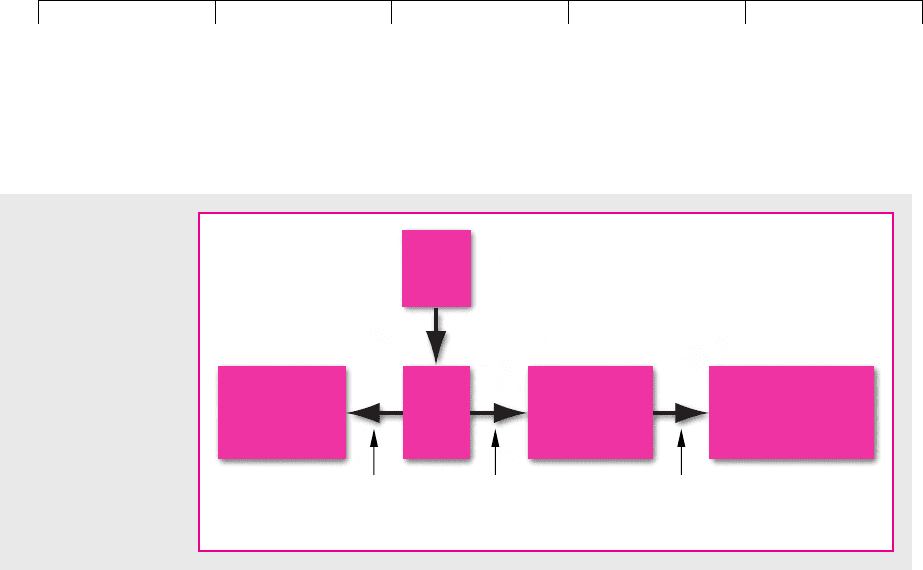

“You can see the trade-off (Figure 5.1). The opportunity cost of taking the proj-

ect is the return shareholders could have earned had they invested the funds on

their own. When we discount the project’s cash flows by the expected rate of re-

turn on comparable financial assets, we are measuring how much investors would

be prepared to pay for your project.”

92 PART I

Value

Firm

Invest

Shareholders

Cash

Investment

opportunity

(real asset)

Investment

opportunities

(financial assets)

Alternative:

pay dividend

to shareholders

Shareholders

invest for themselves

FIGURE 5.1

The firm can either

keep and reinvest

cash or return it to

investors. (Arrows

represent possible

cash flows or

transfers.) If cash is

reinvested, the

opportunity cost is

the expected rate of

return that share-

holders could have

obtained by investing

in financial assets.

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

I. Value 5. Why Net Prsnt Value

Leads to Better

Investments Decisions

than Other Criteria

© The McGraw−Hill

Companies, 2003

“But which financial assets?” Vegetron’s CFO queries. “The fact that investors

expect only 12 percent on IBM stock does not mean that we should purchase Fly-

by-Night Electronics if it offers 13 percent.”

Your reply: “The opportunity-cost concept makes sense only if assets of equiv-

alent risk are compared. In general, you should identify financial assets with risks

equivalent to the project under consideration, estimate the expected rate of return

on these assets, and use this rate as the opportunity cost.”

Net Present Value’s Competitors

Let us hope that the CFO is by now convinced of the correctness of the net pres-

ent value rule. But it is possible that the CFO has also heard of some alternative

investment criteria and would like to know why you do not recommend any of

them. Just so that you are prepared, we will now look at three of the alternatives.

They are:

1. The book rate of return.

2. The payback period.

3. The internal rate of return.

Later in the chapter we shall come across one further investment criterion, the

profitability index. There are circumstances in which this measure has some spe-

cial advantages.

Three Points to Remember about NPV

As we look at these alternative criteria, it is worth keeping in mind the following

key features of the net present value rule. First, the NPV rule recognizes that a

dollar today is worth more than a dollar tomorrow, because the dollar today can be in-

vested to start earning interest immediately. Any investment rule which does not

recognize the time value of money cannot be sensible. Second, net present value de-

pends solely on the forecasted cash flows from the project and the opportunity cost

of capital. Any investment rule which is affected by the manager’s tastes, the com-

pany’s choice of accounting method, the profitability of the company’s existing

business, or the profitability of other independent projects will lead to inferior

decisions. Third, because present values are all measured in today’s dollars, you can add

them up. Therefore, if you have two projects A and B, the net present value of the

combined investment is

NPV(A ⫹ B) ⫽ NPV(A) ⫹ NPV(B)

This additivity property has important implications. Suppose project B has a

negative NPV. If you tack it onto project A, the joint project (A ⫹ B) will have a

lower NPV than A on its own. Therefore, you are unlikely to be misled into ac-

cepting a poor project (B) just because it is packaged with a good one (A). As we

shall see, the alternative measures do not have this additivity property. If you are

not careful, you may be tricked into deciding that a package of a good and a bad

project is better than the good project on its own.

NPV Depends on Cash Flow, Not Accounting Income

Net present value depends only on the project’s cash flows and the opportunity

cost of capital. But when companies report to shareholders, they do not simply

CHAPTER 5

Why Net Present Value Leads to Better Investment Decisions Than Other Criteria 93

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

I. Value 5. Why Net Prsnt Value

Leads to Better

Investments Decisions

than Other Criteria

© The McGraw−Hill

Companies, 2003

show the cash flows. They also report book—that is, accounting—income and book

assets; book income gets most of the immediate attention.

Financial managers sometimes use these numbers to calculate a book rate of

return on a proposed investment. In other words, they look at the prospective

book income as a proportion of the book value of the assets that the firm is pro-

posing to acquire:

Cash flows and book income are often very different. For example, the accountant

labels some cash outflows as capital investments and others as operating expenses.

The operating expenses are, of course, deducted immediately from each year’s in-

come. The capital expenditures are put on the firm’s balance sheet and then de-

preciated according to an arbitrary schedule chosen by the accountant. The annual

depreciation charge is deducted from each year’s income. Thus the book rate of re-

turn depends on which items the accountant chooses to treat as capital investments

and how rapidly they are depreciated.

1

Now the merits of an investment project do not depend on how accountants

classify the cash flows

2

and few companies these days make investment decisions

just on the basis of the book rate of return. But managers know that the company’s

shareholders pay considerable attention to book measures of profitability and nat-

urally, therefore, they think (and worry) about how major projects would affect the

company’s book return. Those projects that will reduce the company’s book return

may be scrutinized more carefully by senior management.

You can see the dangers here. The book rate of return may not be a good mea-

sure of true profitability. It is also an average across all of the firm’s activities. The

average profitability of past investments is not usually the right hurdle for new in-

vestments. Think of a firm that has been exceptionally lucky and successful. Say its

average book return is 24 percent, double shareholders’ 12 percent opportunity

cost of capital. Should it demand that all new investments offer 24 percent or bet-

ter? Clearly not: That would mean passing up many positive-NPV opportunities

with rates of return between 12 and 24 percent.

We will come back to the book rate of return in Chapter 12, when we look more

closely at accounting measures of financial performance.

Book rate of return ⫽

book income

book assets

94 PART I Value

1

This chapter’s mini-case contains simple illustrations of how book rates of return are calculated and of

the difference between accounting income and project cash flow. Read the case if you wish to refresh

your understanding of these topics. Better still, do the case calculations.

2

Of course, the depreciation method used for tax purposes does have cash consequences which should

be taken into account in calculating NPV. We cover depreciation and taxes in the next chapter.

5.2 PAYBACK

Some companies require that the initial outlay on any project should be recover-

able within a specified period. The payback period of a project is found by count-

ing the number of years it takes before the cumulative forecasted cash flow equals

the initial investment.

Brealey−Meyers:

Principles of Corporate

Finance, Seventh Edition

I. Value 5. Why Net Prsnt Value

Leads to Better

Investments Decisions

than Other Criteria

© The McGraw−Hill

Companies, 2003

Consider the following three projects:

CHAPTER 5

Why Net Present Value Leads to Better Investment Decisions Than Other Criteria 95

Cash Flows ($)

Payback

Project C

0

C

1

C

2

C

3

Period (years) NPV at 10%

A –2,000 500 500 5,000 3 ⫹2,624

B –2,000 500 1,800 0 2 –58

C –2,000 1,800 500 0 2 ⫹50

Project A involves an initial investment of $2,000 (C

0

⫽ –2,000) followed by cash in-

flows during the next three years. Suppose the opportunity cost of capital is 10 per-

cent. Then project A has an NPV of ⫹$2,624:

Project B also requires an initial investment of $2,000 but produces a cash inflow

of $500 in year 1 and $1,800 in year 2. At a 10 percent opportunity cost of capital

project B has an NPV of –$58:

The third project, C, involves the same initial outlay as the other two projects but

its first-period cash flow is larger. It has an NPV of +$50.

The net present value rule tells us to accept projects A and C but to reject project B.

The Payback Rule

Now look at how rapidly each project pays back its initial investment. With proj-

ect A you take three years to recover the $2,000 investment; with projects B and C

you take only two years. If the firm used the payback rule with a cutoff period of

two years, it would accept only projects B and C; if it used the payback rule with a

cutoff period of three or more years, it would accept all three projects. Therefore,

regardless of the choice of cutoff period, the payback rule gives answers different

from the net present value rule.

You can see why payback can give misleading answers:

1. The payback rule ignores all cash flows after the cutoff date. If the cutoff date is

two years, the payback rule rejects project A regardless of the size of the

cash inflow in year 3.

2. The payback rule gives equal weight to all cash flows before the cutoff date. The

payback rule says that projects B and C are equally attractive, but, because

C’s cash inflows occur earlier, C has the higher net present value at any

discount rate.

In order to use the payback rule, a firm has to decide on an appropriate cutoff

date. If it uses the same cutoff regardless of project life, it will tend to accept many

poor short-lived projects and reject many good long-lived ones.

NPV1C2⫽⫺2,000 ⫹

1,800

1.10

⫹

500

1.10

2

⫽⫹$50

NPV1B2⫽⫺2,000 ⫹

500

1.10

⫹

1,800

1.10

2

⫽⫺$58

NPV1A2⫽⫺2,000 ⫹

500

1.10

⫹

500

1.10

2

⫹

5,000

1.10

3

⫽⫹$2,624