Blank L., Tarquin A. Engineering Economy (McGraw-Hill Series in Industrial Engineering and Management)

Подождите немного. Документ загружается.

LEARNING OBJECTIVES

Purpose: Learn

to

incorporate decision making under risk into an engineering economy analysis

using

the

basics

of

probability distributions. sampling. and simulation.

Certainty and risk

Va

ri

ables and distributions

Random

sample

Average and dispersion

Monte

Carlo and simulation

This ch

ap

ter will help you:

1.

Understand

the

different approaches

to

decision making

under

certainty and

und

er

ri

sk.

2.

Construct

the

probab

ili

ty

distri

bution

and cumulative

distribution

for

a variable.

3.

Develop

a

random

samp

le

from

th

e

cu

mulative distri

bution

of

a

va

riabl

e.

4.

Es

tim

ate the

ex

pected value a

nd

standard deviation of a

popu

lation from a r

ando

m sampl

e.

5.

Use

Monte

Ca

rl

o sampling and the simulation approach

to

select an alternative.

656

EXAMPLE 19.1

CHAPTER

19

More

on

Variation and Decision Making Under Risk

19.1 INTERPRETATION

OF

CERTAINTY,

RISK,

AND

UNCERTAINTY

All things in the world vary---one from another, over time, and with different

environments. We are guaranteed that variation will occur in engineering econ-

omy due to its emphasis on decision

making for the future. Except for the use

of

breakeven analysis, sensitivity analysis, and a very brief introduction to expected

values, virtually all our estimates have been

certain; that is, no variation in the

amount has entered into the computations

of

PW, A

W,

ROR,

or

any relations

used. For example, the estimate that cash flow next year will be

$+4500

is one

of

certainty. Certainty is,

of

course, not present

in

the real world now and surely

not in the future.

We

can observe outcomes with a high degree

of

certainty,

but even this depends upon the accuracy and precision

of

the scale or measuring

instrument.

To allow a parameter

of

an engineering economy study

to

vary implies that

risk, and possibly uncertainty, is introduced.

Risk. When there may be two or more observable values for a parameter

and it

is

possible to estimate the chance that each value may occur, risk is

present. As an illustration, decision

making under risk is introduced when

an annual cash flow estimate has a

50-50 chance

of

being either

$-1000

or

$ +

500. Accordingly, virtually all decision making is performed under risk.

Uncertainty. Decision making under uncertainty means there are two or

more values observable, but the chances

of

their occurring cannot be esti-

mated or no one is willing to assign the chances. The observable values in

uncertainty analysis are often referred to as

states

of

nature. For example,

consider the states

of

nature to be the rate

of

national inflation in a particu-

lar country during the next 2 to 4 years: remain low, increase 5% to

10% an-

nually,

or

increase 20% to 50% annually.

If

there is absolutely no indication

that the three values are equally likely, or that one

is

more likely than the

others, this is a statement that indicates decision

making under uncertainty.

Example

19.1

explains how a parameter can be described and graphed to prepare

for decision making under risk.

Sue and Charles are both seniors in college and plan

to

be married next year. Based upon

conversations with friends who have recently married, the couple has decided

to

make

separate estimates

of

what each expects the ceremony to cost, with the chance that each

estimate

is

actually observed expressed

as

a percentage. (a) Their separate estimates are

tabulated at the top

of

Figure 19-1. Construct two graphs: one

of

Charles's estimated costs

versus his chance estimates, and one for Sue. Comment on the shape

of

the plots relative

to

each other. (b) After some discussion, they decided the ceremony should cost somewhere

between

$7500 and $10,000.

All

values between the two limits are equaUy likely with a

chance

of

I

in

25. Plot these values versus chance.

SECTION 19.1

Interpretation

of

Certa

in

ty, Risk, and U

nc

erta

in

ty

657

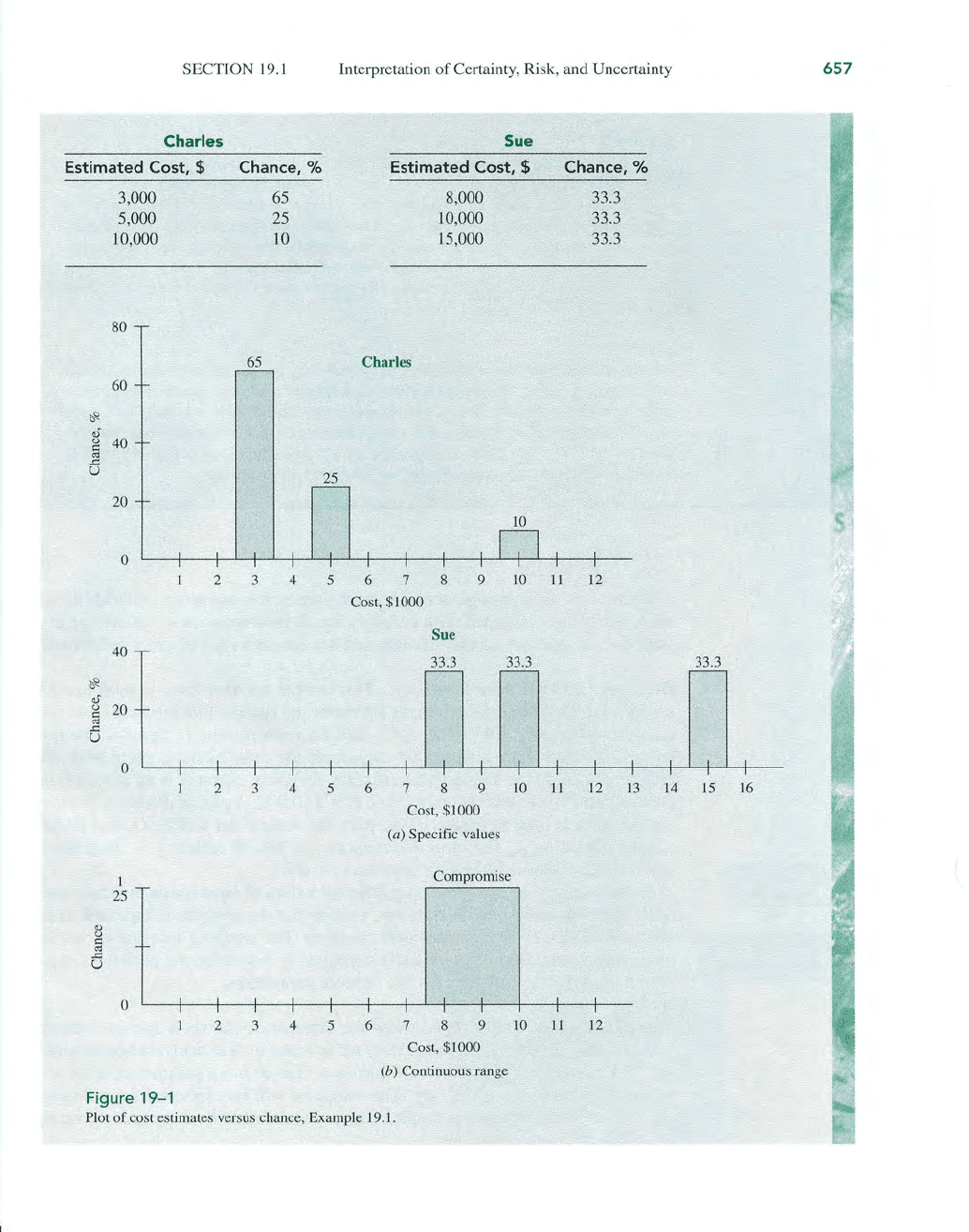

Charles

Sue

Estimated Cost,

$ Chance, % Estimated Cost, $ Chance, %

3,000

65

8,000 33.3

5,000

25

10,000 33.3

10,000 10

15,000

33.3

658

CHAPTER

19

More

on

Variation and Decision Making Under

Ri

sk

Solution

(a) Figure

19-1a

presents the plot for Charles's and Sue's estimates, with the cost

scales aligned. Sue expects the cost to be considerably higher than Charles. Addi-

tionally, Sue places equal (or unjform) chances

on

each value. Charles places a

much higher chance

on

lower cost values; 65% of his chances are devoted to $3000,

and only 10% to $10,000, whjch

is

Sue's mjddle cost estimate. The plots clearly

show the different perceptions about their estimated wedding costs.

(b) Figure 19-1b

is

the plot at a chance

of

1 in

25

for the continuum

of

costs from $7500

thl'ough $10,000.

Comment

One significant difference between the cost estimates in parts (a) and (b)

is

that

of

discrete

and continuous values. Charles and Sue first made specific, discrete estimates with chances

associated w

ith

each value. The compromise estimate they reached is a continuous range

of

values from $7500 to $10,000 with some chance associated with every value between

these limits. In the next Section, we introduce the term

variable and define two types

of

variables-discrete and continuous

-w

hich have been illustrated here.

Before initiating

an

engineering economy study, it

is

important

to

decide if the

analysis will be conducted with certainty for all parameters or if risk will be in-

troduced. A summary

of

the meaning and use for each type

of

analysis follows.

Decision Making Under Certainty This is what we have done in most analy-

ses thus

far.

Deterministic estimates are made and entered into measure

of

worth

relations-PW

,

AW

, FW, ROR,

B/C-and

decision making is based on the re-

sults. The values estimated can be considered the most likely to occur with all

chance placed on the single-value estimate. A typical example

is

an

asset's

fir

st

cost estimate made with certainty, say,

P = $50,000. A plot

of

P versus chance

has the general form

of

Figure

19-1a

with one vertical bar at $50,000 and 100%

chance placed on

it.

The term deterministic,

in

lieu

of

certainty, is often used

when single-value estimates are used exclusively.

In fact, sensitivity analysis using different values

of

an estimate is simply an-

other form

of

analysis with certainty, except that the analysis is repeated with

different values,

each estimated with certainty. The resulting measure

of

worth

values are calculated and graphically portrayed

to

determine the decision's sen-

sitivity

to

different estimates for one or more parameters.

Decision Making Under

Risk

Now the element

of

chance

is

formally taken

into account. However, it is more difficult

to

make a clear decision because the

analysis attempts

to

accommodate variation. One or more parameters

in

an

al-

ternative will be allowed to vary. The estimates will be expressed

as

in

Exam-

ple

19

.1 or

in

shghtly more complex forms. Fundamentally, there are two ways

to consider risk

in

an

analysis:

SECTION

19.1

Interpretation

of

Certainty, Risk, and Uncertainty

Expected value analysis. Use the chance and parameter estimates

to

calcu-

late expected values, E(parameter) via formulas such

as

Equation [18.2].

Analysis results

in

E(cash flow), E(AOC), and the like; and the final result

is the expected value for a measure

of

worth, such

as

E(PW), E(AW),

E(ROR), E(B/C).

To

select the alternative, choose the most favorable

expected value

of

the measure

of

worth. In an elementary form, this is what

we learned about expected values in Chapter

18

. The computations may

become more elaborate, but the principle is fundamentally the same.

Simulation analysis.

Use the chance and parameter estimates

to

generate re-

peated computations

of

the measure

of

worth relation by randomly sam-

pling from a plot for each varying parameter similar

to

those in Figure 19-1.

When a representative and random sample is complete, an alternative

is

se-

lected utilizing a table or plot

of

the results. Usually, graphics are an impor-

tant part of decision making via simulation analysis. Basically, this is the

approach discussed

in

the rest

of

this chapter.

Decision Making Under Uncertainty When chances are not known for the

identified states

of

nature (or values)

of

the uncertain parameters, the use

of

ex-

pected value- based decision making under risk

as

outlined above is not an option.

In fact, it is difficult

to

determine what criterion

to

use to even make the decision.

If

it

is possible to

agree

that

each

state

is equally likely,

then

all states

have

the

same

chance,

and

the

situation reduces to one

of

decision

making

under

risk, because expected values

can

be

determined.

Because

of

th

e relatively inconclusive approaches necessary to incorporate

decision making under uncertainty into an engineering economy study, the tech-

niques can be quite useful but are beyond the intended scope

of

this text.

In

an

engineering economy study,

as

well

as

all other forms

of

analysis and

decision making, observed parameter values in the future will vary from the

value estimated at the time

of

the study. However, when performing the anal ysis,

not

all

parameters should be considered

as

probabilistic (or at risk). Those that

are estimable with a relatively high degree

of

certainty should be fixed for the

study. Accordingly, the methods

of

sampling, simulation, and statistical data

analysis are selectively used on parameters deemed important to the decision-

making process.

As

mentioned in Chapter

18

, interest rate-based parameters

(MARR, other interest rates, and inflation) are usually not treated

as

random

variables in the discussions that follow.

Parameters such

as

P, AOC, n,

S,

mate-

rial and unit costs, revenues, etc., are the targets

of

decision making under risk

and simulation. Anticipated and predictable variation in interest rates is more

commonly addressed

by

the approaches of sensitivity analysis covered in the

first two sections

of

Chapter

18

.

The remainder of this chapter concentrates upon decision making under risk

as

applied in

an

engineering economy study. The next three sections provide

foundation material necessary to design and correctly conduct a simulation

analysis (Section

19

.

5)

.

659

660

Figure

19-

2

Ca) Discrete and

continuous variable

scale

s,

and

Cb)

scales

for a varia

bl

e versus its

probabili

ty.

CHAPTER

19

More on Variation and Decision Making Under Risk

19.2 ELEMENTS IMPORTANT

TO

DECISION

MAKING

UNDER

RISK

Some basics

of

probability and statistics are essential to correctly perform deci-

sion making under risk via expected value or simulation analysis. These basics

are explained here.

(If

you are already familiar with them, this section will pro-

vide a review.)

Random Variable

(or

Variable) This is a characteristic or parameter that can

take

on

anyone

of

several values. Variables are classified

as

discrete or continu-

ous.

Discrete variables have several specific, isolated values, while continuous

variables can assume any value between two stated limits, called the

range of

the variable.

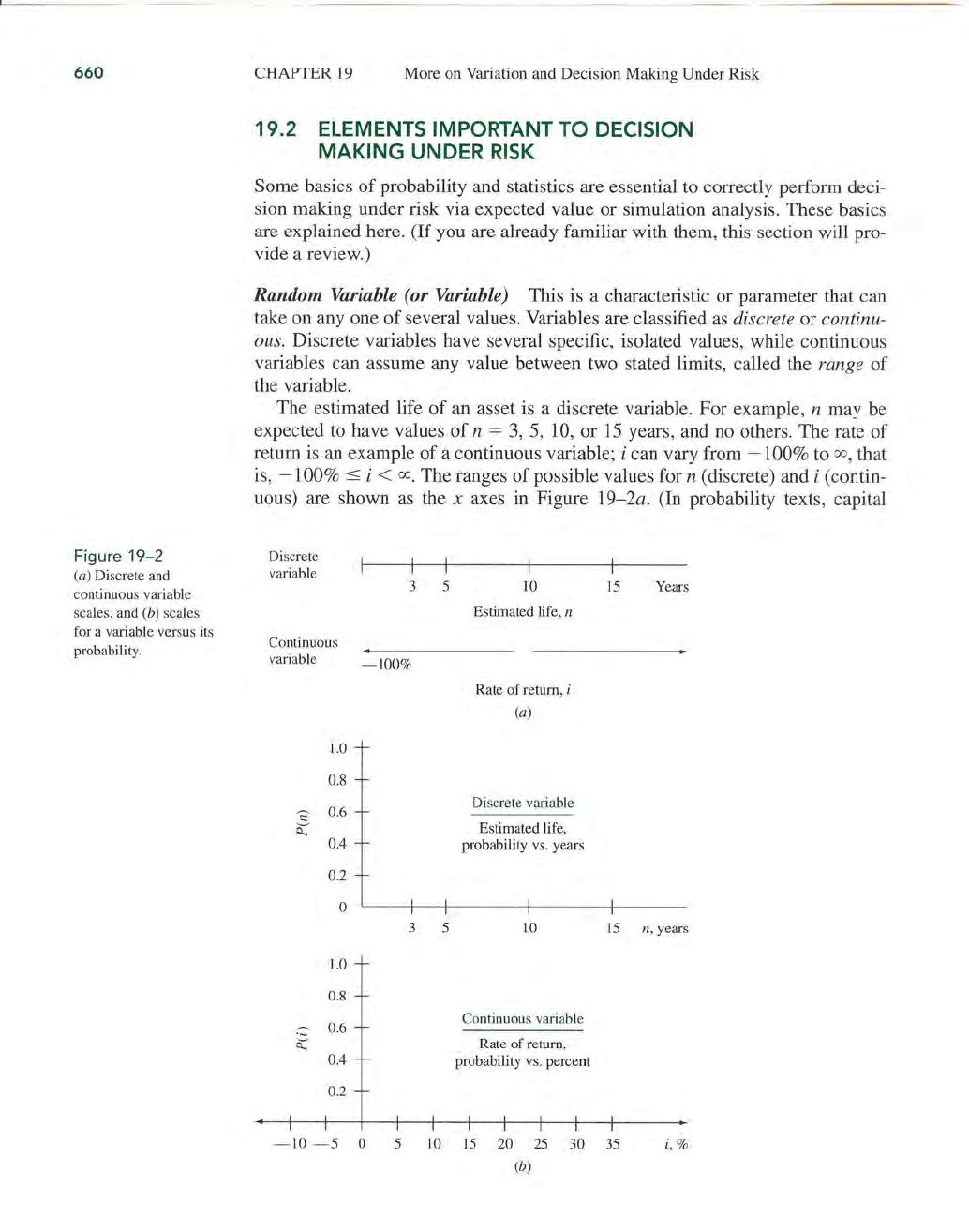

The estimated life

of

an

asset

is

a discrete variable. For example, n may be

expected

to

have values

of

n = 3, 5,

10,

or

15

years, and no others. The rate

of

return is an example

of

a continuous variable; i can vary from - 100%

to

00

, that

is,

- 100%

::;

i <

00

. The ranges

of

possible values for n (discrete) and i (contin-

uous) are shown

as

the x axes

in

Figure 19-2a. (In probability texts, capital

Discrete

variable

3 5

10

15 Years

Estimated life, n

Continuous

variable

- 100%

Rate

of

return, i

Ca)

1.0

0.8

0.6

Discrete variable

?

i(

Estimated life,

0.4

probability

vs.

years

0.2

0

3 5

10

15

n, years

1.0

0.8

0.6

Continuous

variable

~

Rate

of

return,

0.4

probability

vs.

percent

0.2

-

10

- 5

0 5

10

15

20

25

30

35

i, %

(b)

SECTION 19.2 Elements Important to Decision Making Under Risk

letters symbolize a variable, say

X,

and small letters, x, identify a specific value

of

the variable. Though correct, this level

of

rigor in terminology is not included

in this chapter.)

Probability This

is

a number between 0 and 1.0 which expresses the chance in

decimal form that a random variable (discrete or continuous) will take on any

value from those identified for

it.

Probability is simply the amount

of

chance, di-

vided by 100.

Probabilities are commonly identified by P(X

i

)

or P(X =

X),

which is read

as

the probability that the variable X takes on the value Xi' (Actu-

ally, for a continuous variable, the probability at a single value is zero,

as

shown

in a later example.) The sum

of

all

P(X)

for a variable must be 1.0, a requirement

P(Xi)

already discussed. The probability scale, like the percentage scale for chance in

Figure

19-1, is indicated on the ordinate

(y

axis)

of

a graph. Figure 19-2b shows

the

0

to

1.0 range of probability for the variables

nand

i.

661

Discrete

Probability Distribution This describes how probability is distributed over the I I I

different values

of

a variable. Discrete variable distributions look significantly

L..'--'--.L...'-----'----'-----'

-Xi

different from continuous variable distributions,

as

indicated by the inset at the

P(Xi)

right. The individual probability values are stated

as

P(X)

= probability

that

X equals

Xi

[19.1]

The distribution may be developed

in

one

of

two ways: by listing each probabil-

ity value for each possible variable value (see Example

19.2) or by a mathemat-

ical description or expression that states probability in terms

of

the possible vari-

able values (Example

19

.3).

Cumulative Distribution Also called the cumulative probability distribution,

F(Xi)

this is the accumulation

of

probability over all values

of

a variable up

to

and

including a specified value. Identified

by

F(X), each cumulative value is calcu-

lated

as

F(X)

= sum

of

all probabilities

through

the value

Xi

=

PCX-

::;

X)

[19.2]

As

with a probability distribution, cumulative distributions appear differently for

discrete (stair-stepped) and continuous variables (smooth curve). The next two

examples illustrate cumulative distributions that correspond to specific probabil-

ity distributions. These fundamentals about

F(X) are applied in the next section

to

develop a random sample.

EXAMPLE

19.2

'.

Alvin

is

a medical doctor and biomedical engineering graduate who practices at Med-

ical Center Hospital. He

is

planning to start prescribing an antibiotic that may reduce

infection

in

patients with flesh wounds. Tests indicate the drug has been applied up to

6 times per day without harmfuJ1side effects.

If

no drug is used, there is always a posi-

tive probability that the infection will be reduced by a person's own immune system.

Continuous

Discrete

X

I

662

CHAPTER

19

More on Variation and Decision Making Under Risk

Published drug test results provide good probability estimates

of

positive reaction

(i.e., reduction in the infection count) within 48 hours for different numbers

of

treat-

ments per day.

Use the probabilities listed below to construct a probability distribution

and a cumulative distribution for the number

of

treatments per day.

Solution

Number

of

Treatments

per

Day

o

1

2

3

4

5

6

Probability

of

Infection Reduction

0.07

0.08

0.10

0.12

0.13

0.25

0.25

Define the random variable T as the number

of

treatments per day. Since T can take on

only seven different values,

it

is a discrete variable.

The

probability

of

infection reduc-

tion is listed for each value in column 2

of

Table 19-1.

The

cumulative probability

F(T)

is determined using Equation [19.2] by adding all peT) values through T

i

,

as indicated

in

column 3.

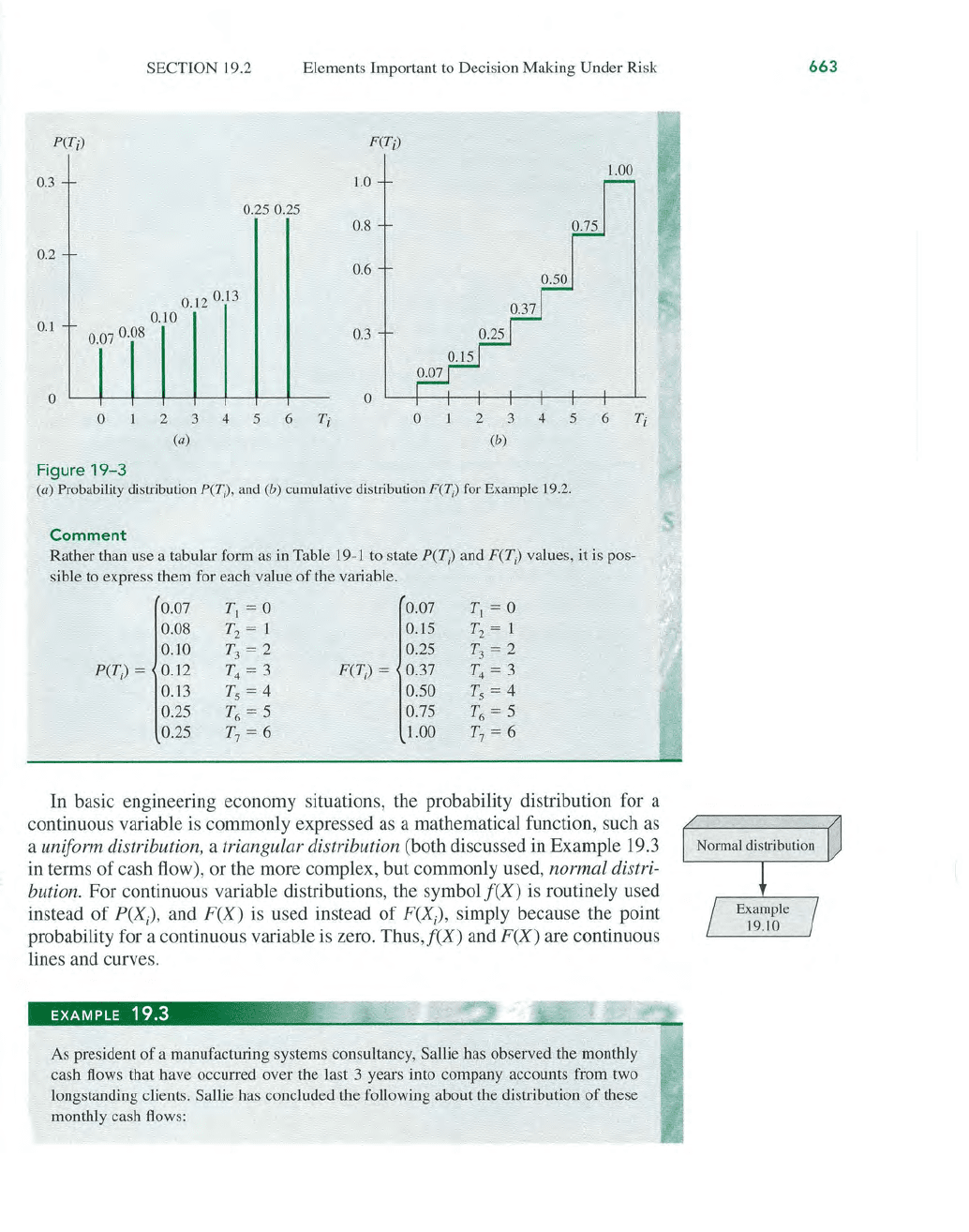

Figure

19-3a and b shows plots

of

the probability distribution and cumulative dis-

tribution, respectively. The summing

of

probabilities to obtain

F(T)

gives the cumula-

t

iv

e distribution the stair-stepped appearance, and

in

al

l cases the final

F(T)

= 1.0,

since the total

of

a

ll

peT)

values must equal l.0.

TABLE

19-1

Probability Distribution

and

Cumulative

Distribution for

Example

19

.2

(1

)

(2) (3)

Cumulative

Number

per

Day Probability Probability

T

j

P(T

j

)

F(T

j

)

0

0.07 0.07

0.08

0.

15

2 0.10 0.25

3

0.12 0.37

4 0.13 0.50

5

0.25 0.75

6

0.25 1.00

SECTION

19

.2

Elements Important

to

Decision Making Under Risk

P(Ti)

F(Ti)

1.00

0.3

1.0

0.250

.

25

0.8

0.2

0.6

0.12

0

.13

0.1

0.10

0.07 0.08

0.3

0

0

0

2 3 4

5

6

T-

/.

O

2 3

456

T'

I

(a)

(b)

Figure

19-3

(a) Probability distribution P(T;), and (b) cumulative distribution F(T,) for Example \9.2.

Comment

Rather than use a tabular form as in Table 19-1 to state peT) and F(T) values, it is pos-

sible

to

express them for each value

of

the variable.

0.07

T, = 0

0.07

T, = 0

0.08

T2

= 1

0.15

T2

= 1

0.10

T3

= 2

0.

25

T3

= 2

peT) = 0.12

T4

= 3

F(T) =

0.37

T4

= 3

0.13

Ts

= 4

0.50

Ts

= 4

0.25

T6

= 5

0.75

T6

= 5

0.25

T7

= 6

1.00

T7

= 6

In basic engineering economy situations, the probability distribution for a

continuous variable is commonly expressed

as

a mathematical function, such

as

a uniform distribution, a triangular distribution (both discussed in Example

19

.3

in terms of cash flow), or the more complex, but commonly used,

normal distri-

bution. For continuous variable distributions, the symbolf(X) is routinely used

instead

of

P(X), and F(X) is used instead

of

F(X), simply because the point

probability for a continuous variable is zero. Thus,f(X) and

F(X) are continuous

lines and curves.

EXAMPLE

19.3

S

As

president

of

a manufacturing systems consultancy, Sallie has observed the monthly

cash flows that have occurred over the last 3 years into company accounts from two

longstanding clients. Sallie has concluded the following about the distribution

of

these

monthly cash flows:

663

664

CHAPTER

19

More on Variation and Decision Making Under

Ri

sk

Client 1

Estimated low cash

flow:

$10,000

Estimated high cash

flow:

$15,000

Most likely cash flow: same for

all

values

Distribution

of

probability: uniform

Client

2

Estimated low cash flow: $20,000

Estimated high cash

flow:

$30,000

Most likely cash

flow:

$28,000

Distribution

of

probability: mode at $28,000

The mode is the most frequently observed value for a variable. Sallie assumes cash flow

to be a continuous variable referred to

as

C.

(a) Write and graph the two probability dis-

tributions and cumulative distributions for monthly cash

flow,

and (b) determine the

probability that monthly cash flow

is

no more than $12,000 for client I and no more

than

$25,000 for client

2.

Solution

All cash

flow

values are expressed

in

$1000 units.

Client

i:

monthly c

ashjlow

distribution

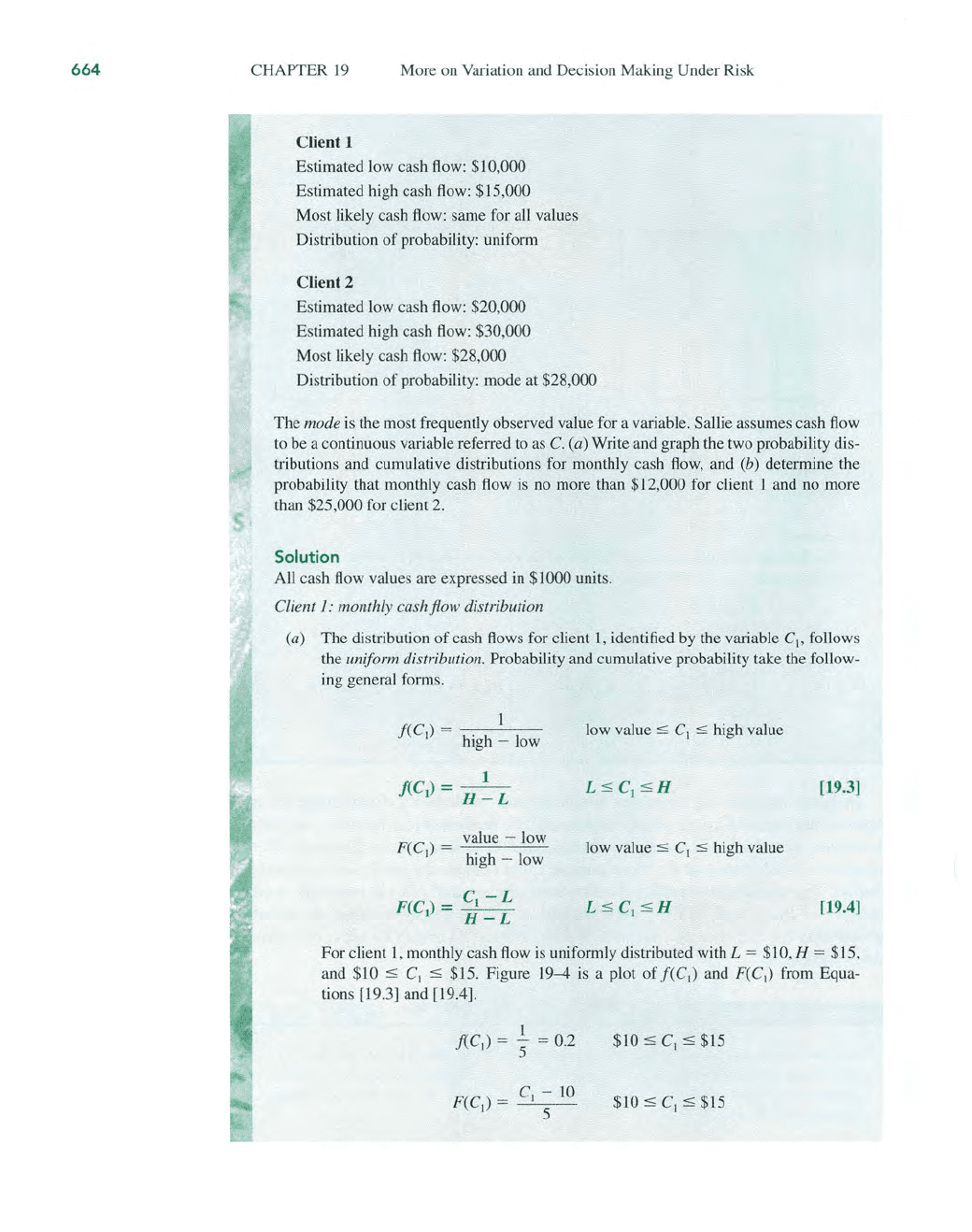

(a) The distribution

of

cash flows for client 1, identified by the variable C

I

,

follows

the uniform distribution. Probability and cumulative probability take the follow-

ing general forms.

fCCI)

=

---'-

--

high - low

value - low

FCC

I

)

=

----

high - low

low value

$ c

l

$ high value

[19.3]

low value $ c

l

$ high value

[19.4]

For client 1, monthly cash

flow

is

uniformly distributed with L = $10, H = $15,

and $10

$ C

I

$ $15. Figure 19-4

is

a plot

of

fCC

I)

and

FCC

I

)

from Equa-

tions [19.3] and [19.4].