Alfred DeMaris - Regression with Social Data, Modeling Continuous and Limited Response Variables

Подождите немного. Документ загружается.

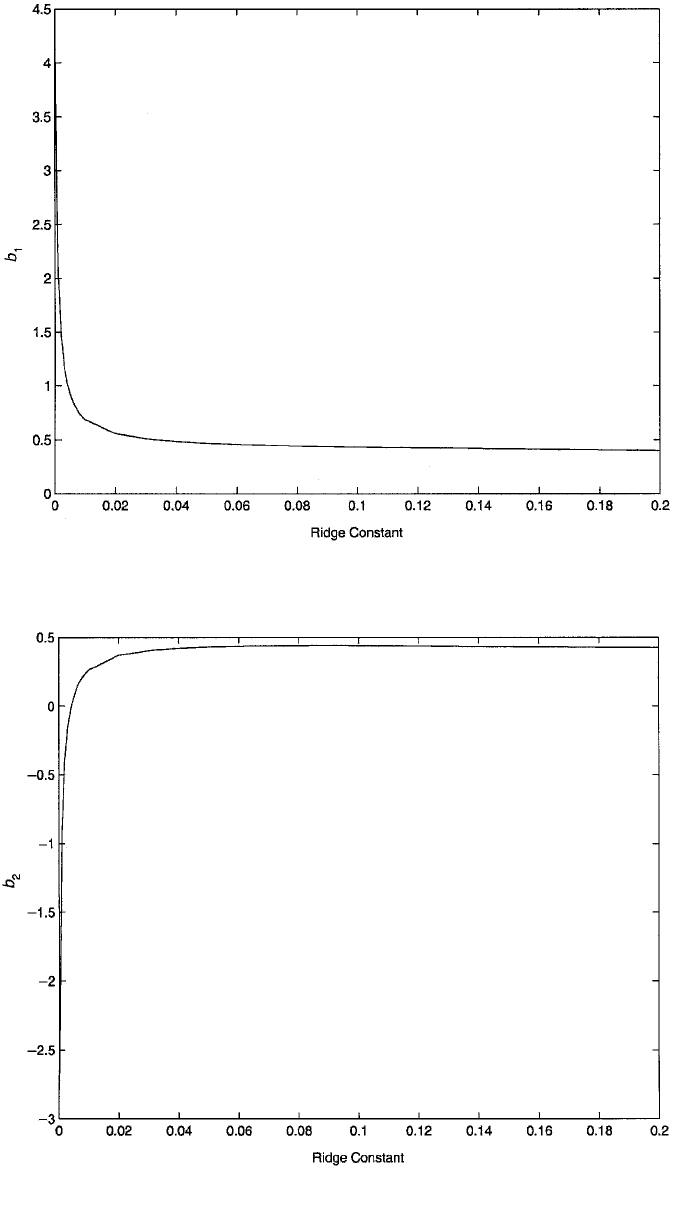

Figure 6.5 Ridge trace for the coefficient of triceps skinfold thickness (b

1

) in the regression model for

body fat.

Figure 6.6 Ridge trace for the coefficient of thigh circumference (b

2

) in the regression model for

body fat.

c06.qxd 8/27/2004 2:53 PM Page 235

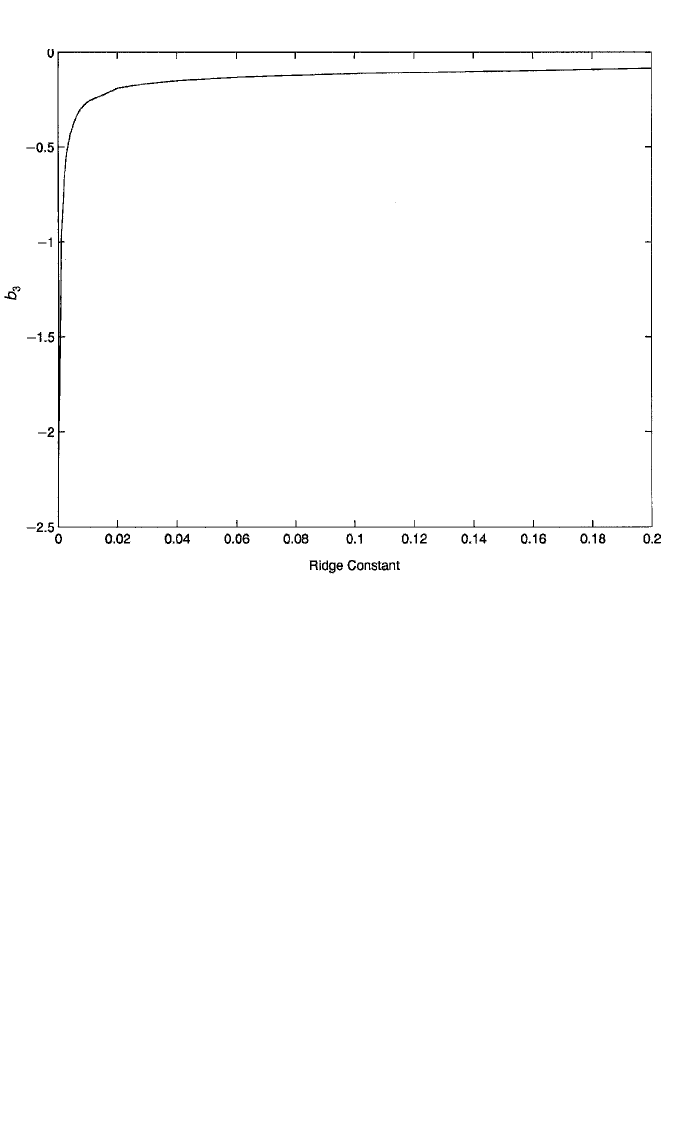

Each of the plots suggests that the coefficients stabilize right around δ .02, and

hence, this is the value chosen for the ridge constant. Notice in Figure 6.6, in partic-

ular, that the coefficient for thigh circumference changes sign from negative to pos-

itive very quickly as δ increases away from zero, and then remains positive. As

expected, this suggests that a greater thigh circumference is associated with more,

rather than less, body fat. The ridge regression estimates are shown in the “ridge

estimator” column of panel A of Table 6.7. These are the unstandardized estimates

and so can be compared to the OLS estimates in the first column. All have been

reduced markedly in magnitude, consistent with the expected reduction in the

coefficients once the multicollinearity problem has been addressed.

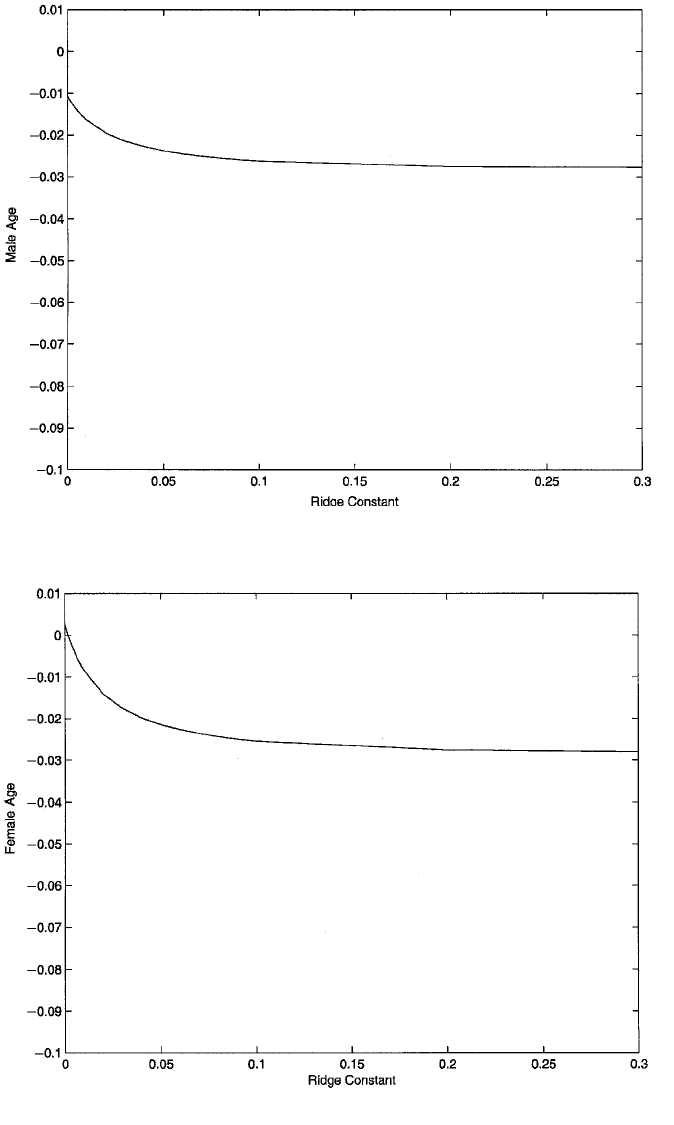

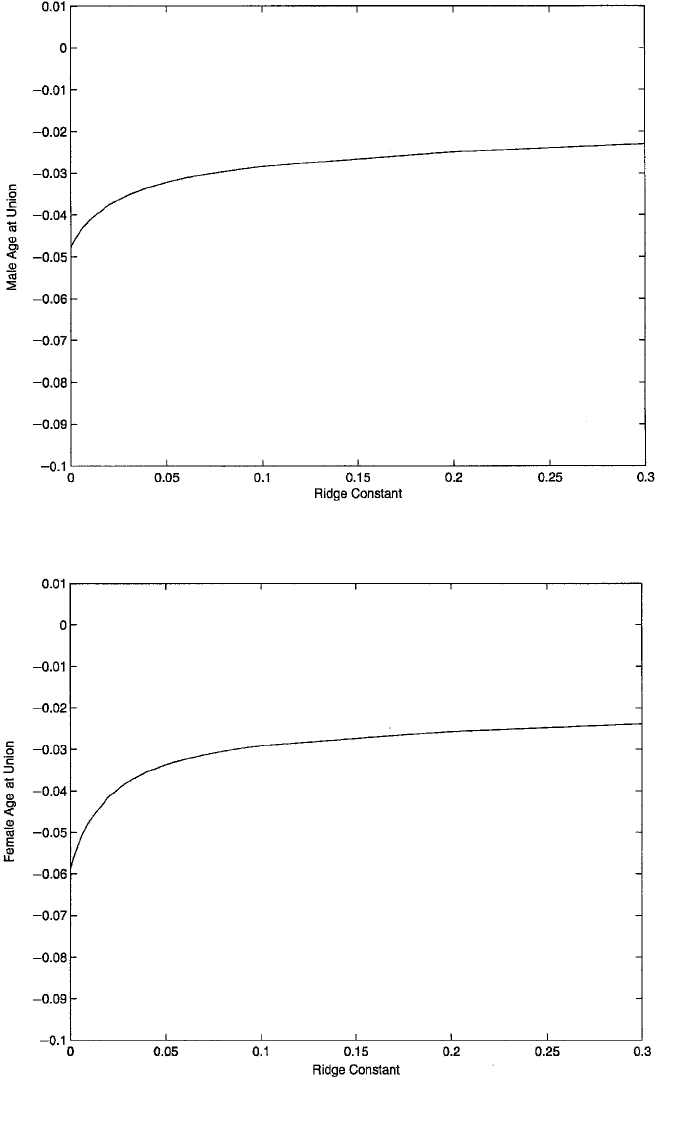

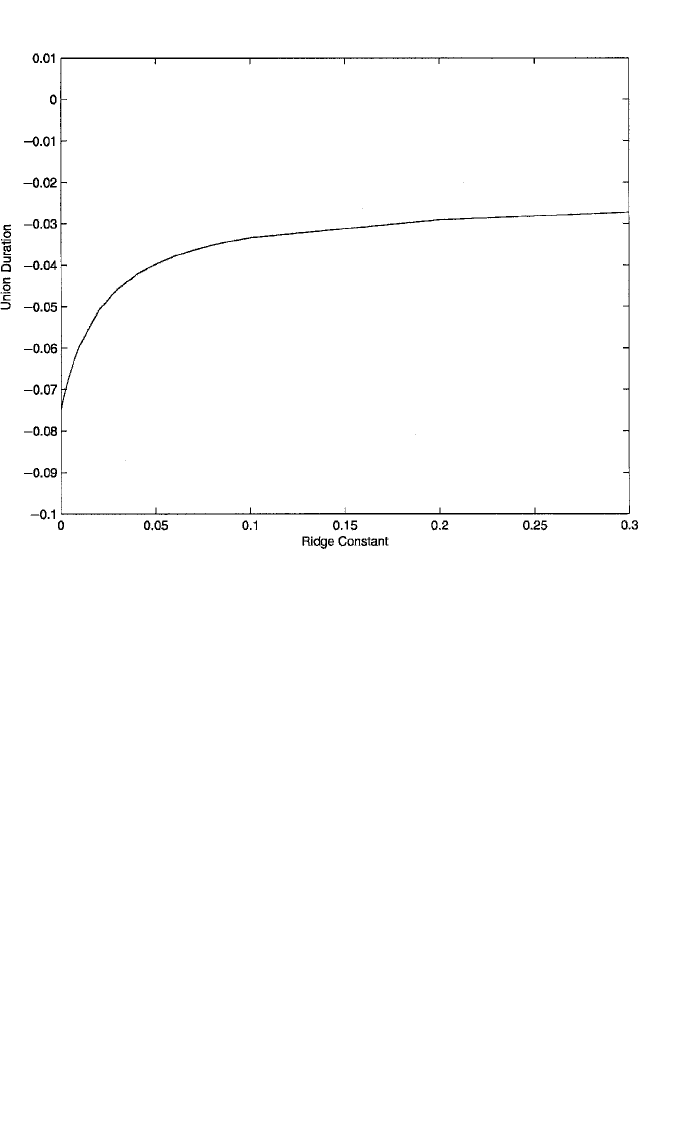

The ridge traces for male- and female age, male- and female age at the beginning

of the union, and union duration for the NSFH data are shown in Figures 6.8 to 6.12.

As these are the most problematic variables in the analysis, I choose a value of δ

based on an attempt to stabilize their effects. In this case, all of the graphs point

toward the value of .05 for δ, so this is the ridge constant that was chosen. Notice that

the coefficient for female age changes from positive to negative as δ moves away from

zero. Again, a negative effect was expected theoretically. Of the five plots, Figure

6.12, showing the trend in the coefficient for union duration, appears to evince the

most dramatic change. The ridge estimates are shown in the “ridge estimator” column

236 ADVANCED ISSUES IN MULTIPLE REGRESSION

Figure 6.7 Ridge trace for the coefficient of midarm circumference (b

3

) in the regression model for

body fat.

c06.qxd 8/27/2004 2:53 PM Page 236

Figure 6.8 Ridge trace for the coefficient of male age in the regression model for couple disagreement.

Figure 6.9 Ridge trace for the coefficient of female age in the regression model for couple disagreement.

c06.qxd 8/27/2004 2:53 PM Page 237

Figure 6.10 Ridge trace for the coefficient of male age at union in the regression model for couple dis-

agreement.

Figure 6.11 Ridge trace for the coefficient of female age at union in the regression model for couple

disagreement.

c06.qxd 8/27/2004 2:53 PM Page 238

of panel A of Table 6.8. Again, these are the unstandardized coefficients. In this case,

there is some shrinkage in all of the coefficients, compared to the OLS estimates, but

the changes are nowhere near as pronounced as in Table 6.7. The most notable change

is the aforesaid reversal of sign for the effect of female age.

Principal Components Regression. Principal components regression, also called

regression on principal components, gets its name from the fact that the n scores on

the K independent variables can be linearly transformed into a comparable set of

scores on K principal components. However, the principal components have the

property that they are orthogonal to each other. Each principal component is a

weighted sum of all K of the original variables. Moreover, the principal components

contain all of the variance of the original variables, but the first J K principal com-

ponents typically account for the bulk of that variance. The variance of the jth com-

ponent is equal to the jth eigenvalue of R

xx

. So components associated with small

eigenvalues contribute very little to the data and as a result, can be omitted from the

analysis. As the small eigenvalues are associated with linear dependencies, this

omission also greatly reduces the impact of those linear dependencies on the design

matrix. Standard treatments of principal components regression (e.g., Jolliffe, 1986;

Myers, 1986) usually develop the technique by writing the regression model in terms

of the principal components.

REGRESSION DIAGNOSTICS II: MULTICOLLINEARITY 239

Figure 6.12 Ridge trace for the coefficient of union duration in the regression model for couple dis-

agreement.

c06.qxd 8/27/2004 2:53 PM Page 239

Instead, I employ an alternative, but equivalent development that is more consistent

with the notion of altering the correlation matrix, as discussed above with respect to

ridge regression. Once again, we rely on the spectral decomposition of the design

matrix to understand the procedure. Recall that the design matrix can be decomposed

as R

xx

冱λ

j

u

j

u

j

, which is the sum of K rank 1 matrices, each of the form λ

j

u

j

u

j

(that

these matrices only have rank 1 is left as a proof for the reader). However, if λ

j

is small,

the contribution of λ

j

u

j

u

j

to R

xx

is relatively insignificant. But it is at the same time the

contribution that is associated with a linear dependency, so it is also troublesome to

include (as we see below). In principal components regression we simply leave this

contribution out of R

xx

(and its inverse, R

xx

1

) when calculating the regression estimates.

To see the benefits of this, let’s return to our simple two-regressor example used ear-

lier. For the design matrix in which X

1

and X

2

are correlated .995, the eigenvalues are

1.995 and .005, with corresponding eigenvectors u

1

[.7071 .7071] and u

2

[.7071

.7071]. The spectral decomposition of R

xx

shows that it is the sum of two parts:

λ

1

u

1

u

1

1.995

冤冥

[.7071 .7071]

冤冥

(6.17)

and

λ

2

u

2

u

2

.005

冤冥

[.7071 .7071]

冤冥

. (6.18)

The reader can easily verify that the sum of the rightmost matrices in (6.17) and

(6.18) is R

xx

. But notice that the matrix in (6.17), which I refer to as the reduced cor-

relation matrix and denote as R

red

, almost perfectly reproduces R

xx

, while the con-

tribution of the matrix in (6.18) is almost negligible. However, the decomposition of

R

xx

1

, following equation (6.13), shows that its two parts are

λ

1

1

u

1

u

1

′ .5013

冤冥

[.7071 .7071]

冤冥

(6.19)

and

λ

1

2

u

2

u

2

′ 200

冤冥

[.7071 .7071]

冤冥

. (6.20)

Adding the rightmost expressions in (6.19) and (6.20) gives us R

xx

1

, as shown above.

Here it is clear that the contribution of the second eigenvalue, in the form of its

inverse, and associated eigenvector are what “blow up” R

xx

1

. Therefore, in con-

structing “R

xx

1

,” we simply omit the matrix in (6.20). I’m using quotation marks here

since the reduced form of R

xx

1

, which I now denote R

red

, is not actually the inverse

of R

red

(which can easily be verified by noting that R

red

R

red

I). In fact, R

red

is not

invertible, since it is a 2 2 matrix with rank 1, as is immediately evident—there is

only one independent vector present. In general, R

red

is not invertible because it is

K K but is the sum of fewer than K rank 1 matrices. As the rank of a summed

matrix is no greater than the sum of the ranks of its component matrices (Searle,

1982), the rank of R

red

is always less than K, and therefore R

red

cannot have an

100 100

100 100

.7071

.7071

.2506 .2506

.2506 .2506

.7071

.7071

.0025 .0025

.0025 .0025

.7071

.7071

.9975 .9975

.9975 .9975

.7071

.7071

240 ADVANCED ISSUES IN MULTIPLE REGRESSION

c06.qxd 8/27/2004 2:53 PM Page 240

inverse. Consequently, I refer to R

red

in (6.19) as the pseudoinverse of R

red

. The stan-

dardized principal components coefficients are therefore

b

s

pc

R

red

r

xy

冤冥冤冥

冤冥

.

Although these are not quite as close to the true values of .25 and .15 as are the ridge

estimates, they represent a vast improvement over the OLS estimates.

In general, then, the principal components estimator of

ββ

s

is of the form b

s

pc

R

red

r

xy

, where

R

red

冱

J

i1

λ

1

i

u

i

u

i

and J K. Some authors recommend using the percentage of variance accounted for

by the J retained components as a guide to how many components to omit (e.g., Hadi

and Ling, 1998). However, typically, dropping the last component, which is associ-

ated with the smallest eigenvalue, will be sufficient. As with ridge regression, the

bias of the principal components estimator is easy to see, since

E(b

s

pc

) E(R

_

red

r

xy

) R

_

red

1

n

Z E(y

z

) R

_

red

1

n

ZZ

ββ

s

R

_

red

R

xx

ββ

s

ββ

s

.

Body Fat and NSFH Data, Revisited. The last column in panel A of Tables 6.7 and

6.8 presents the unstandardized principal components estimates for the body fat and

NSFH data, respectively. Notice that the principal components estimates are quite

close to the ridge regression estimates, and both are substantially different from the

OLS estimates for the body fat data. For the NSFH data, all of the estimates, whether

OLS, ridge, or principal components, are fairly similar. Perhaps the key substantive

difference between OLS and the other estimators are that the latter have more intu-

itive signs for the effect of thigh circumference in the body fat data and for the effect

of female age in the NSFH data. Again, the primary limitation with the latter esti-

mators is that inferences to the population parameters cannot be made. On the other

hand, the ridge and principal components estimators are probably closer than the

OLS coefficients to the true values of the parameters. It should be mentioned that not

all software makes these two techniques available to the analyst. SAS offers both

estimators as options to the OLS regression procedure, invoked using the keywords

RIDGE (for ridge regression) and PCOMIT (for principal components regression).

Concluding Comments. Although I confine my discussion of influential observa-

tions as well as collinearity problems and remedies to this chapter, these issues apply

to all generalized linear models. Influence diagnostics have been devised for tech-

niques such as logistic regression (Pregibon, 1981) and are included in such software

packages as SAS. Collinearity problems can plague any model that employs multiple

regressors; however, not all procedures offer collinearity diagnostics. On the other

hand, multicollinearity is strictly a problem in the design matrix and does not depend

on the nature of the link to the response. Therefore, it can always be diagnosed with

.2

.2

.40925

.38875

.2506 .2506

.2506 .2506

REGRESSION DIAGNOSTICS II: MULTICOLLINEARITY 241

c06.qxd 8/27/2004 2:53 PM Page 241

an OLS procedure that provides collinearity diagnostics, which most of them do. One

simply needs to code the dependent variable in some manner that is consistent with

the use of OLS. Versions of ridge and principal components regression have been

developed for logistic regression (see, e.g., Barker and Brown, 2001; Schaefer, 1986),

suggesting that such techniques should become more widely available for other gen-

eralized linear models in the future.

EXERCISES

6.1 Suppose that we have a population of N 4 cases. Let X be a matrix with

columns x

1

[1 2 4 8] and x

2

[2 1 3 4]. Suppose further that

σ

x

1

2.681 and σ

x

2

1.118. Also, let C be the centering matrix with dimen-

sions C

44

I

44

1

4

J

44

.

(a) Show that Z CXD

1/2

is the matrix of standardized variable scores for

these four cases, where D

1/2

is a diagonal matrix with elements 1/σ

x

i

.

(b) Calculate the correlation matrix using R

xx

(1/n)ZZ.

6.2 Prove that the inverse of D

c

i

is D

1/c

i

for i 1,2,...,n.

6.3 Show that A 冱λ

j

u

j

u

j

UD

λ

U.

6.4 Prove that if λ

j

are the eigenvalues of A, 1/λ

j

are the eigenvalues of A

1

.

(Hint: Start with the spectral decomposition of A and then take the inverse of

both sides of the equation.)

6.5 Let r

x

1

x

2

.675 and show that VIF

1

and VIF

2

are the diagonal elements of R

1

xx

.

6.6 Prove that MSQE(θ

ˆ

) V(θ

ˆ

) [B(θ

ˆ

)]

2

. (Hint: Start with the definition of MSQE;

let Eθ

ˆ

E(θ

ˆ

) for economy of notation, then subtract and add this term from

the expression inside parentheses and expand the expression.)

6.7 Prove that the matrix λuu has only rank 1, for any scalar λ and any vector u.

6.8 Verify that, in general, for any square matrix A, tr(cA) c tr(A), for any

scalar c.

6.9 For the following data:

Case XY Case XY

1 22 6 612

2 3 3 7 9 5.5

336 8 98

4 6 4.5 9 15 2

567

242 ADVANCED ISSUES IN MULTIPLE REGRESSION

c06.qxd 8/27/2004 2:53 PM Page 242

Do the following using a calculator:

(a) Calculate h

ii

for all nine cases.

(b) For case 9, calculate t

i

, dffits

i

, dfbetas

ji

for the slope of the SLR and

Cook’s D

i

. Note that another formula for Cook’s D is (Neter et al.,

1985)

D

i

pM

e

2

S

i

E

(1

h

i

h

i

ii

)

2

.

Also, for dfbetas

ji

, use σ

ˆ

b

1

from the regression that omits case 9.

6.10 Let Z

1

z

11

z

2

11

and let Z

2

[z

21

z

22

] represent matrices of standardized

variable scores (i.e., assume that Z

2

11

is standardized after being created from

the square of Z

11

) and suppose that the following model (in standardized

coefficients) characterizes the data:

Y

z

.25Z

11

.01Z

2

11

.3Z

21

.25Z

22

ε

y

,

Z

21

.2Z

2

11

ε

21

,

Z

22

.15Z

2

11

ε

22

,

Cov(Z

11

,Z

2

11

) .8,

Cov(Z

11

,ε

y

) Cov(Z

11

,ε

21

) Cov(Z

11

,ε

22

)

Cov(Z

2

11

,ε

y

) Cov(Z

2

11

,ε

21

) Cov(Z

2

11

,ε

22

) 0.

(a) If the analyst, instead, estimates y

z

Z

1

ββ

s

1

υ, where υ Z

2

ββ

s

2

εε

y

,give

the value of E(b

s

1

). [Hint: First, note that E(b

s

1

)

ββ

s

1

r

1

11

r

12

ββ

s

2

, where

r

1

11

r

12

β

s

2

is the bias in b

s

1

and

r

11

冤冥

and

r

12

冤冥

.

Then use covariance algebra to derive all unknown correlations (recall that the

covariance between standardized variables is their correlation), and do the

appropriate matrix operations.]

(b) Interpret the nature of the bias in the sample quadratic term.

6.11 Let Z

1

[z

11

z

12

cp], where CP Z

11

Z

12

, and let Z

2

[z

21

z

22

]. Suppose

further that all variables, including CP, are standardized. (Note: Normally, we

don’t standardize quadratic or cross-product terms; rather, they are formed as

products of standardized variables; see Aiken and West, 1991. However, we

Cov(Z

11

,Z

22

)

Cov(Z

2

11

,Z

22

)

Cov(Z

11

,Z

21

)

Cov(Z

2

11

,Z

21

)

Cov(Z

11

,Z

2

11

)

1

1

Cov(Z

11

,Z

2

11

)

EXERCISES 243

c06.qxd 8/27/2004 2:53 PM Page 243

do so here to simplify the covariance algebra.) Suppose that the following

model (in standardized coefficients) characterizes the data:

Y

z

.25Z

11

.15Z

12

.10CP .35Z

21

.3Z

22

ε

y

,

Z

21

.2CP ε

21

,

Z

22

.1CP ε

22,

Cov(Z

11

,Z

12

) .45,

Cov(Z

11

,CP) .85,

Cov(Z

12

,CP) .90,

and the covariances of Z

11

, Z

12

, and CP, with all equation errors equal zero.

(a) If the analyst, instead, estimates Y

z

Z

1

ββ

s

1

υυ

, where υ Z

2

ββ

s

2

εε

y

,give

the value of E(b

s

1

). (Hint: Follow the hint for Exercise 6.10.)

(b) Interpret the nature of the bias in the sample estimate of the coefficient of

the cross-product term (i.e., CP).

The following information is for Exercises 6.12 and 6.13: Suppose that the true

model for Y is β

1

Z

1

β

2

Z

2

ε, where all observed variables are standardized.

Suppose, further, that the sample correlation matrix is R

xx

冤冥

and

the sample vector of correlations of the regressors with Y is r

xy

冤冥

. Note also that the eigenvalues of R

xx

are λ

1

1.997 and λ

2

.003, while

the eigenvectors are u

1

冤冥

and u

2

冤冥

.

6.12 Estimate

ββ

s

冤冥

using OLS. Then perform a ridge regression using the

following values for the ridge constant: .05, .10, .15, .20, and .25. You will

have five different pairs of coefficient estimates. What appears to be the best

ridge constant based on the changes in the coefficients?

6.13 Conduct a principal components regression for the data in Exercise 6.12.

The following information is for Exercises 6.14 and 6.15: In the model

y* X*

ββ

s

εε

*

, the spectral decomposition of the 4 4 correlation matrix, R

xx

,

results in the following:

D

λ

冤冥

,

0

.

0

.00091806

.

.

.0689

0

0

.9996

2.9305

0

.

0

β

s

1

β

s

2

.7071

.7071

.7071

.7071

.7192

.6786

.997

1

1

.997

244 ADVANCED ISSUES IN MULTIPLE REGRESSION

c06.qxd 8/27/2004 2:53 PM Page 244