ACCA Paper F1 - Accountant in Business, Course Notes, BPP 2010

Подождите немного. Документ загружается.

4: ETHICAL CONSIDERATIONS

4.5

3 Professional ethics

3.1 A profession is an occupation that requires extensive training and the study and mastery of

specialised knowledge, and usually has a professional association, ethical code and

process of certification or licensing.

3.2 Professional bodies will issue 'Codes of Conduct' or 'Codes of Ethics', which members

are expected to adhere to. The may be developed using:

(a) A rules based approach, creating specific rules for members to follow in as many

situations as possible.

(b) A framework based approach, describing fundamental values and qualities that

members should aspire to, but not laying out prescriptive rules.

Lecture example 3

Exam standard question

Required

What are the respective advantages of the rules-based and framework-based approaches to

professional ethical codes?

Solution

4: ETHICAL CONSIDERATIONS

4.6

4 A code of ethics for accountants

4.1 Accountancy is a high-profile profession and accountants are frequently in positions of trust

and responsibility. A code of ethics for accountants has been issued by the International

Federation of Accountants (IFAC), which represents all the major accountancy bodies

around the world. This has been incorporated by ACCA into its own code of ethics.

Principles of the code include:

(a) Integrity

(b) Objectivity

(c) Professional competence and due care

(d) Confidentiality

(e) Professional behaviour

4.2 To meet these principles, students and members of ACCA need to develop a mix of

personal and professional qualities.

4.3 Personal qualities include:

(a) Reliability – all work must meet professional standards

(b) Responsibility – taking ownership for your work

(c) Timeliness – delays can be costly and disruptive

(d) Courtesy – to colleagues and clients

(e) Respect – to develop constructive relationships

4.4 Professional qualities include:

(a) Independence – not only being independent, but appearing to be independent

(b) Scepticism – questioning information and data

(c) Accountability – for judgements and decisions

(d) Social responsibility – to your employer and the public

5 Chapter summary

• This chapter has reviewed ethics as an issue for organisations today.

• Specifically, it has looked at how ethics impact on accountants, and the standards

they are expected to adhere to as professionals.

4.7

Chapter 4: Questions

4: QUESTIONS

4.8

4.1 IFAC stands for

A International Financial Accounting Committee

B International Financial Accounting Commission

C International Federation of Accountants

D International Federation of Accounting Concepts

(2 marks)

4.2 Which of the following is an advantage of the rules based approach to developing a code of ethics?

A Ideal for complex or fast changing situations

B Consistency of application

C Encourage proactive members

D Hinders members trying to circumvent rules (2 marks)

4.3 Which of the following is not a source of rules that regulate behaviour of individuals and businesses?

A The law

B Ethics

C Customs and rituals

D Non-legal rules and regulations (2 marks)

4.4 Ethical behaviour is the same the world over. True or false

A True

B False (1 mark)

4.5 Which of the following is not a principle of the code of ethics issued by the International Federation of

Accountants?

A Objectivity

B Professional behaviour

C Integrity

D Courtesy (2 marks)

4.9

Chapter 4: Answers

4: ANSWERS

4.10

4.1 C IFAC is an international body representing all major bodies across the world.

4.2 B The other three possible answers are all advantages of the framework based approach rather

than the rules based approach.

4.3 C Customs and rituals are not a source of rules, although they will influence the way individuals and

organisations behave.

4.4 B Ethical behaviour can vary from country to country as a result of different cultures.

4.5 D Courtesy is a personal quality that all members of the ACCA should demonstrate.

END OF CHAPTE

R

5.1

Syllabus Guide Detailed Outcomes

Having studied this chapter you will be able to:

• Understand the essence of good corporate governance.

• Appreciate why corporate governance and social responsibility have grown in significance.

• Understand the role of directors in corporate governance.

Exam Context

Corporate governance and social responsibility is an issue for all corporate bodies, both commercial and not-for-profit.

'Best practice' in corporate governance features was in a pilot paper question.

Qualification Context

Corporate governance issues are also covered in the 'Auditing' papers, whilst social responsibility is useful background

to P3 (Business Analysis).

Business Context

In the past decade social responsibility and corporate governance have become increasingly important topics for all

organisations, especially in the wake of some corporate collapses such as Enron.

Corporate

governance and

social responsibility

5: CORPORATE GOVERNANCE AND SOCIAL RESPONSIBILITY

5.2

Overview

Corporate governance

and social responsibility

Introduction to corporate

governance

Corporate social

responsibility

The role of the board

Reporting on corporate

governance

Non-executive directors

Remuneration and audit

committees

5: CORPORATE GOVERNANCE AND SOCIAL RESPONSIBILITY

5.3

1 Introduction to corporate governance

1.1 Corporate governance is the system by which organisations are directed and controlled by

their senior officers. It is an issue not just for public companies but also not-for-profit and

public sector bodies.

1.2 Corporate governance issues generally arise from the separation between ownership and

control in organisations (for many smaller organisations, ownership and control may not be

separated and these issues are less relevant). For example, public companies are owned by

their shareholders but controlled by senior management. There is scope for senior

management to abuse the power they have.

Lecture example 1

Class exercise

Required

Why might managers act in a way that is not in the best interests of shareholders?

Solution

1.3 Corporate governance has become increasingly high profile in recent years due to a number

of factors including:

(a) High-profile corporate scandals (e.g. Maxwell, Enron, WorldCom)

(b) Increasingly active and international shareholders

(c) Increasing media scrutiny

(d) Globalisation highlighting cultural differences

(e) Developments in financial reporting

5: CORPORATE GOVERNANCE AND SOCIAL RESPONSIBILITY

5.4

Lecture example 2

Ideas generation

Required

What might the features of poor corporate governance be?

Solution

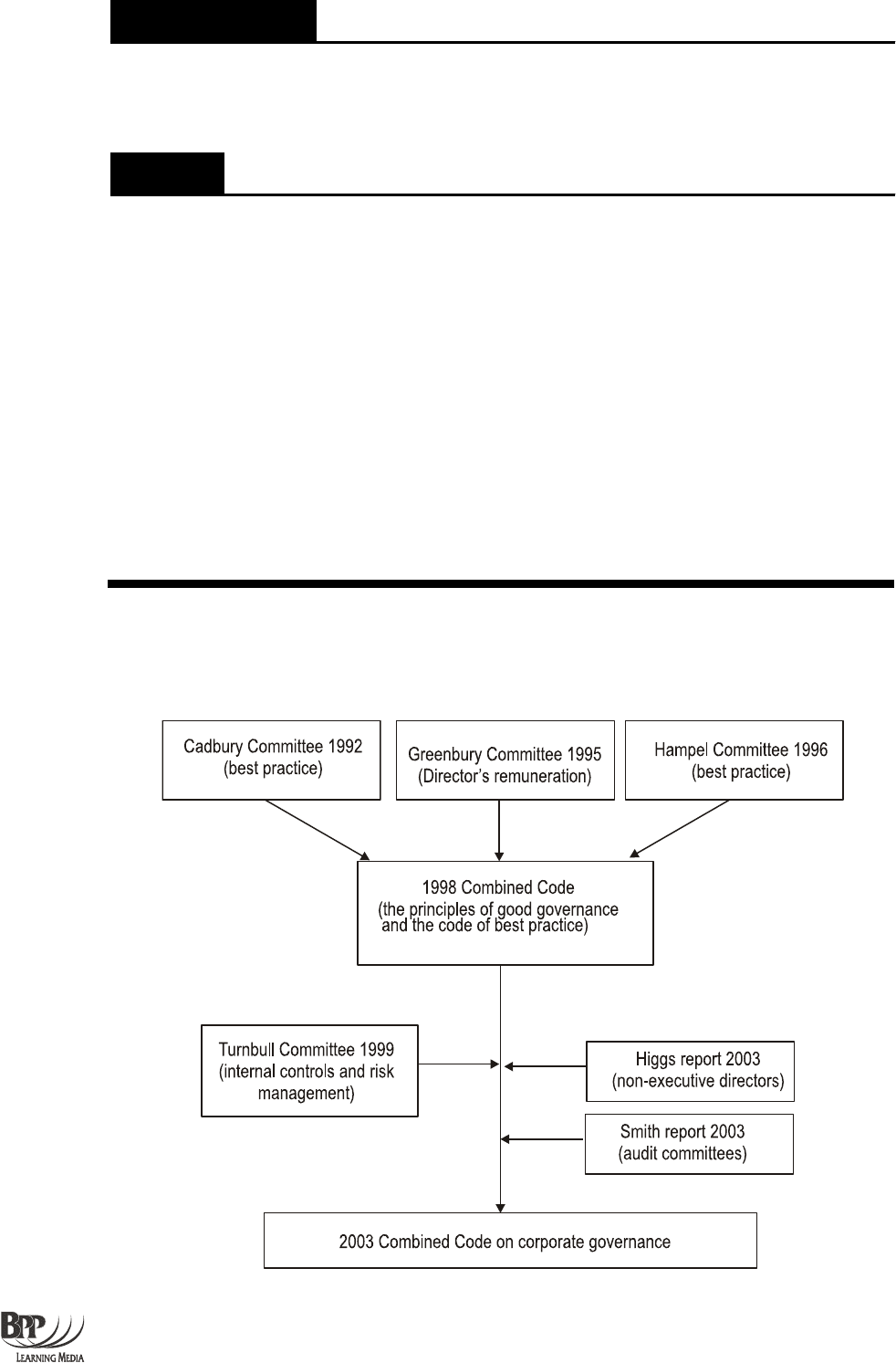

1.4 Poor corporate governance can lead to reputational damage and sometimes bankruptcy.

1.5 Corporate governance in the UK has developed through a series of committees and reports: