Sioshansi F.P. Smart Grid: Integrating Renewable, Distributed & Efficient Energy

Подождите немного. Документ загружается.

Projected global greenhouse gas emissions under 550 ppm, 450 ppm, and IEA

“BLUE Map” scenarios. The 550 ppm and 450 ppm scenarios include emission

reductions from forestry and agriculture, whereas the IEA “BLUE Map” only

includes energy-related emission reductions.

Source: Commonwealth of Australia [21]; IEA [19]

Results and Discussion

Modeling Results

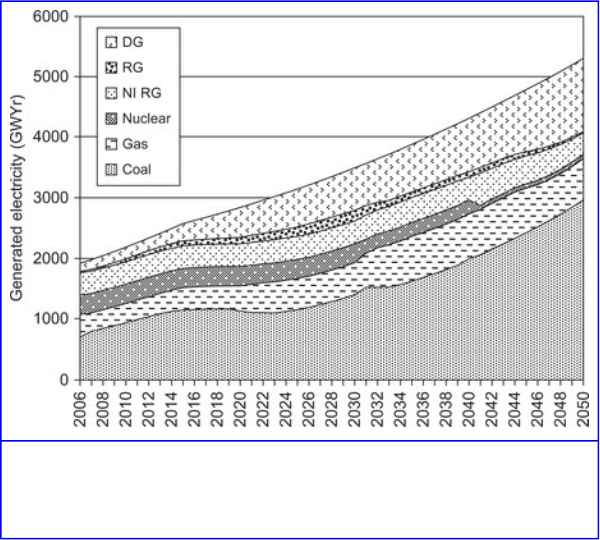

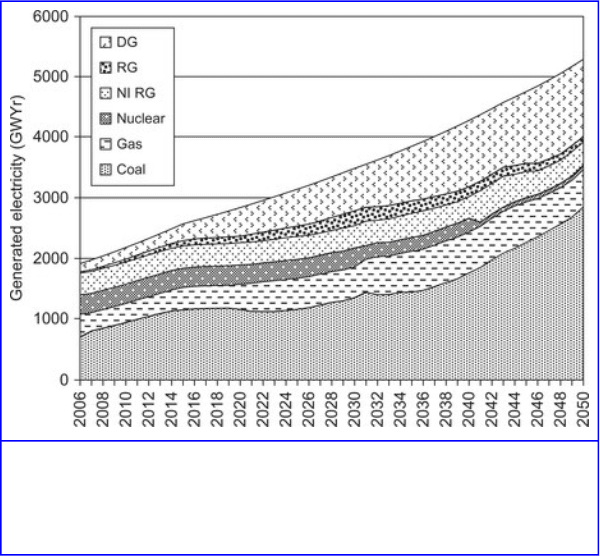

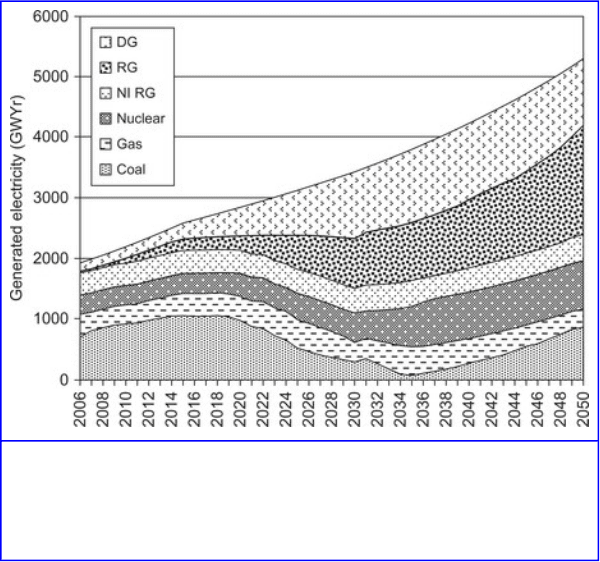

In Figure 7.7A a plot is provided for the BAU case with a

20% cap under the Case A scenario previously described. In

Figure 7.7B the BAU case for a 50% cap under the Case D

scenario is displayed for comparison. Both figures clearly

show that global electricity demand is expected to grow

significantly, increasing two-and-a-half times by 2050. In

these figures coal represents all brown and black coal sources

with and without carbon capture and sequestration (CCS).

Gas represents both open cycle and combined cycle turbines

with and without CCS. Non-intermittent renewable

generation, NI RG, includes biomass, hot fractured rocks,

conventional geothermal, and hydroelectric. RG represents

intermittent renewable generation sources including

large-scale PV and solar thermal, wind, wave, and ocean/tidal

current. Small-scale rooftop PV is not included here as it is

captured within DG, which represents small-scale

technologies such as PV, CHP, and fuel cells.

391

Figure 7.7A

Case A: Global technology mix assuming business as usual.

392

Figure 7.7B

Case D: Global technology mix assuming business as usual.

Source: CSIRO

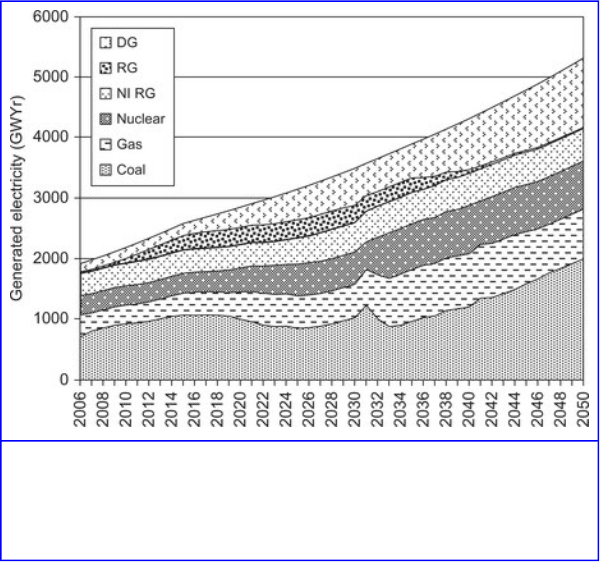

Figure 7.7A and Figure 7.7B show that the absence of a

carbon price has not prevented the uptake of solar-based

renewable technologies and CHP. All of these technologies

receive some form of government support in the model, such

as feed-in tariffs or heat credit. Solar thermal has the

additional advantage of providing some peaking power. These

technologies, with the exception of CHP, have high learning

rates as described in Table 7.1; therefore by increasing their

cumulative capacity their capital costs fall over time. Black

coal pulverized fuel plant continues generating beyond 2050,

and black coal combined cycle, with its higher efficiency,

absorbs the growing demand for electricity. Under this

393

scenario very little CCS technology is developed. This is also

the case for ocean energies, biomass, and geothermal plant.

The modeling results indicate that the total amount of

intermittent generation does not necessarily reach the cap in

all three regions in the model, but it does reach the cap in at

least one. This level of detail is not captured in these figures,

which simply present the total worldwide generation.

However, this means that even under a BAU case there are

financial benefits to be gained by using smart grids, assuming

they increase the amount of intermittent generation that can

integrated into the grid.

For comparative purposes, results from the IEA [19]

projections for the year 2050 for uptake of various electricity

generation technologies under their baseline scenario are also

presented. The results are shown in Table 7.3. It is not

apparent if any intermittent constraints have been made by the

IEA in their modeling, and therefore they are compared with

the range of outputs in the modeling presented here.

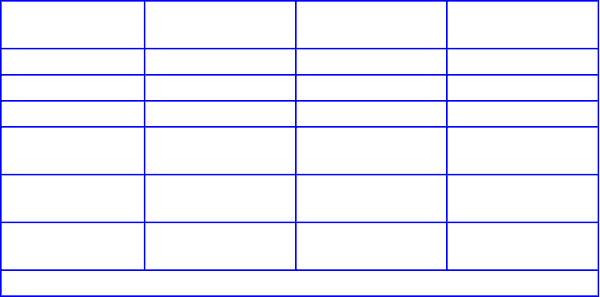

Table 7.3

BAU Cases A, Assuming a 20% Maximum Intermittency and D, Assuming a 50%

Maximum Intermittency, and IEA Baseline Scenario Projected Share of Electricity

Generation Technologies in the Year 2050

BAU Case A (%

Share)

BAU Case D (%

Share)

IEA Baseline (%

Share)

Coal 55 54 41

Gas 13 12 14

Nuclear 1 1 10

Non-intermittent

renewable

7 7 15

Intermittent

renewable

1 2 6

Source: CSIRO.

394

Distributed

generation

23 24 14

Source: CSIRO.

Major differences between the modeling presented here and

the IEA results lie in the share of coal to nuclear and the share

of renewable generation, both intermittent and

non-intermittent, and DG. The differences between coal and

nuclear arise because of two issues:

• The first is that this modeling uses a flat price for coal and

a cost curve for uranium, so that the more uranium is used

the more expensive it becomes.

• Second, this modeling has a higher capital cost for

nuclear than the IEA [19], which makes nuclear a less

attractive option in GALLM. The IEA nuclear costs are

primarily U.S. based while the figures in this analysis are

global, including European costs informed by recent data

from manufacturers. Furthermore, these baseline cases

place no cost on greenhouse gas emissions; therefore there

is no need to build zero-emission technologies unless they

are economic.

The IEA results show a bigger share of generation from

non-intermittent renewable generation, most likely due to

constraints in GALLM, particularly for hydroelectric

generation. The IEA's biomass component includes waste,

which is modeled here as DG since this can encompass

bagasse and other locally produced biomass waste that is used

as fuel close to where it has been harvested. GALLM predicts

more DG mainly because of rooftop PV, which has a high

learning rate compared to other technologies, and its capital

cost becomes quite low in time, reaching 1400 $AU/kW by

2050. In this modeling there are no limits on the amount of

395

rooftop PV that can be constructed, aside from the cap on

intermittent sources. It is worth noting, however, that an

earlier study [22] in Australia showed that PV installation was

economically constrained rather than physically constrained

by available roof space, assuming slightly less than one

quarter of available rooftop space was used.

In Figure 7.8A a plot is provided for the 450 ppm case with a

20% cap (Case A). In Figure 7.8B the 450 ppm case for a

50% cap (Case D) is displayed for contrast. These results

show that for a grid constrained by 20% intermittent

resources, large centralized low-emission plant such as coal

with CCS, shown as Coal, and nuclear play a strong role,

while gas turbines provide a large amount of the generation

mix because of its cheap price and its use in peaking

operation. When the constraints on intermittency are relaxed,

the strong price of carbon results in large amounts of rooftop

PV, in the DG set, and solar thermal and wind, in the RG set,

being economically deployed over the period to 2050. In this

case nuclear also plays a strong role, while gas and coal with

CCS, shown as Coal, are deployed at much lower rates than

in the more constrained intermittency case.

396

Figure 7.8A

Global technology mix under a 450 ppm case with a 20% cap on intermittent

sources.

397

Figure 7.8B

Global technology mix under a 450 ppm case with a 50% cap on intermittent

sources.

For comparison, Table 7.4 shows the projected share of

electricity generation technologies in the year 2050 under the

450 ppm case compared with the IEA [19]“Blue Map”

scenario, which has also been designed to achieve 450 ppm.

In Case A where intermittent sources are limited to a cap of

20%, the modeling shows a 21% share in DG. In this case

little large-scale intermittent renewable generation is

predicted. When the intermittency constraint is relaxed in

Case D, the DG and large-scale intermittent renewable

technologies increase to a 54% share. In contrast, the IEA in

their predictions shows a 34% total for intermittent

renewables. The technologies that have increased the most

due to the relaxing of the intermittent constraint are solar PV,

398

solar thermal, and wind. In the IEA's case, the renewable

technologies that have increased their share the most

compared to the BAU case are wind and solar. Geothermal

triples its share but it is starting from a lower BAU generation

capacity.

Table 7.4

450 ppm Cases A and D and IEA BLUE Map Scenario Projected Share of

Electricity Generation Technologies in the Year 2050

450 ppm Case A

(% Share)

450 ppm Case D

(% Share)

IEA BLUE Map

(% Share)

Coal 37 16 12

Gas 16 6 7

Nuclear 15 15 24

Non-intermittent

renewable

10 8 23

Intermittent

renewable

1 34 19

Distributed

generation

21 20 15

Source: CSIRO.

The differences between Case A and the IEA BLUE Map are

again in the shares of nuclear vs. coal and of renewable

generation, both intermittent and non-intermittent, vs. DG.

However, there are fewer differences between Case D and the

BLUE Map scenario. Case D has more intermittent renewable

generation than non-intermittent, whereas the IEA has more

non-intermittent generation. The GALLM model also predicts

more than double the amount of intermittent renewable

generation compared to nuclear, whereas the IEA has more

nuclear than intermittent renewable generation.

These differences reflect the generous 50% intermittent

constraint, which is allowing more large-scale intermittent

399

renewable technologies with high learning rates, such as solar

thermal, wave, and wind, into the market. The more these

technologies are deployed, the lower their capital costs

become due to assumptions on learning rates. The IEA does

not state the limits used in their modeling but the results

suggest they may use a cap lower than 50% on intermittent

technologies, yet not as low as 20% since both intermittent

renewable generation and DG contain intermittent

technologies and the total of these is 34%.

It is worth reiterating that the modeling simply examines the

savings that might be achieved by allowing an increase in

intermittent generation—mostly attributed to the presence of

smart-grid-enabling infrastructure. It does not specify how

this may be achieved, only the savings that might be realized

through their use. There are many possible ways in which

intermittent generation may be better integrated into

electricity networks including the use of storage, better

management of demand through increased consumer

awareness and appliance automation, and better forecasting of

demand and supply for instance as discussed below and

covered in more detail in other chapters of this book.

The modeling displayed above shows that in later years,

traditional peaking plant such as gas turbines become less

prevalent and slower reacting plant such as nuclear begin to

dominate large centralized facilities. In simple terms in

current electrical networks the balance between supply and

demand is provided by these large plant, which receive

appropriate signals from a central control to ramp their supply

up or down as required. Ongoing developments in

transmission and centralized dispatch fit within the wider

smart grid paradigm, and it will need to continue to evolve to

400