Principles of Finance with Excel (Основы финансов c Excel)

Подождите немного. Документ загружается.

PFE Chapter 24, Black-Scholes and binomial page 14

other parameters. The spreadsheet also includes a function called PutVolatility which computes

the implied volatility for a put option.

4

Both functions are illustrated below:

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

AB C

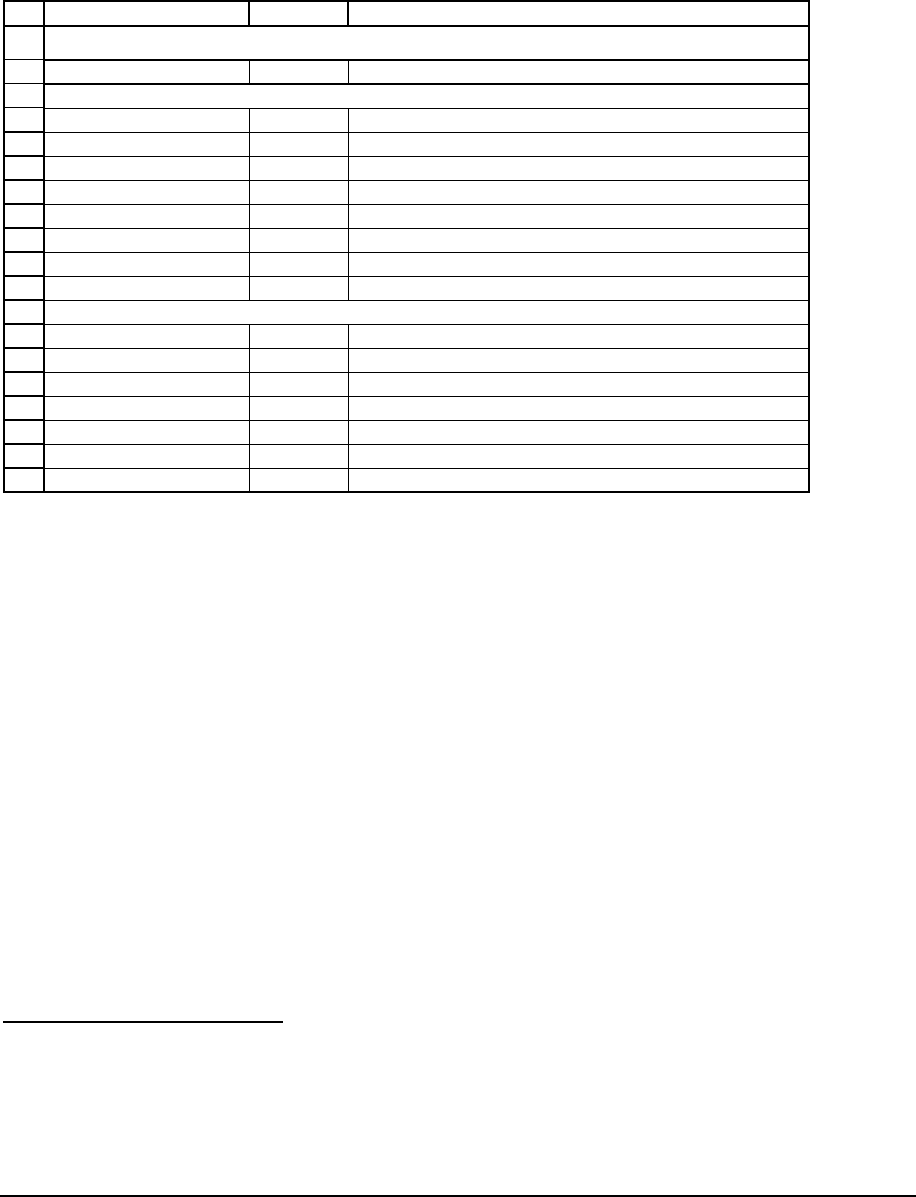

TWO IMPLIED VOLATILITY FUNCTIONS

Using CallVolatility to compute the implied volatility for a call

S 35 Current stock price

X 35 Exercise price

T 0.50000 Time to maturity of option (in years)

r 6.00% Risk-free rate of interest

Target 5.25 <-- This is the current call price we want to match

Implied volatility 48.71% <-- =CallVolatility(B4,B5,B6,B7,B8)

Using PutVolatility to compute the implied volatility for a call

S 35 Current stock price

X 35 Exercise price

T 1.00000 Time to maturity of option (in years)

r 6.00% Risk-free rate of interest

Target 3.44 <-- This is the current put price we want to match

Implied volatility 32.49% <-- =putVolatility(B13,B14,B15,B16,B17)

24.6. Doing sensitivity analysis

We can use Excel to do a lot of Black-Scholes sensitivity analysis. In this section we

give two examples, leaving other examples for the chapter exercises.

Example 1: The sensitivity of the Black-Scholes call price to the stock price

4

In the spirit of this chapter, we do not explain how these functions work. For details see my book Financial

Modeling.

PFE Chapter 24, Black-Scholes and binomial page 15

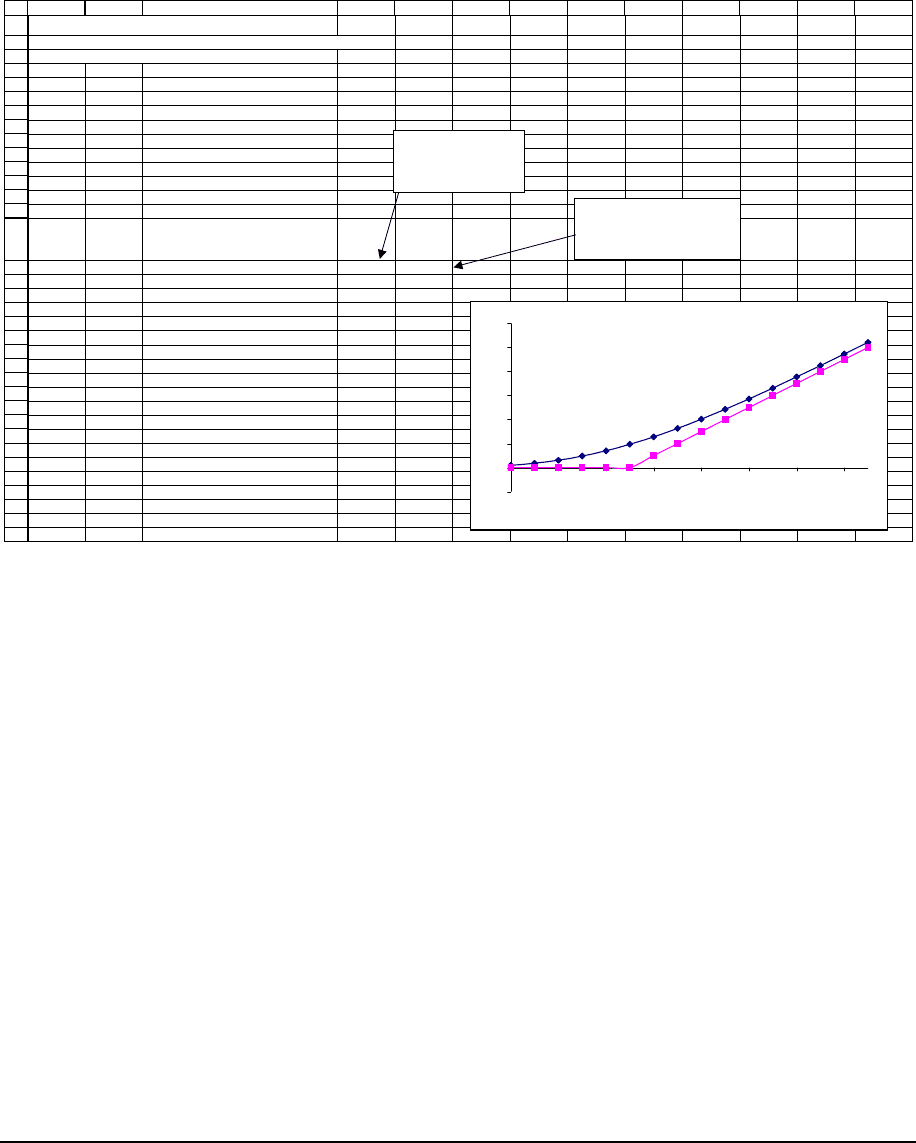

For example, the following Data|Table (see Chapter ???) gives—as the stock price S

varies—the Black-Scholes value of the call compared to its intrinsic value (i.e., max(S-X,0) ) .

Note that we have not shown the header of the data table.

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

AB C DEFGH I JKLM

BLACK-SCHOLES OPTION FUNCTIONS

The functions in this spreadsheet--

Calloption

and

Putoption

--were

defined by the author; they are part of this spreadsheet.

S 100 Current stock price

X 90 Exercise price

T 0.50000 Time to maturity of option (in years)

r 4.00% Risk-free rate of interest

Sigma 35% Stock volatility

Call price 16.32 <-- =calloption(B5,B6,B7,B8,B9)

Put price 4.53 <-- =putoption(B5,B6,B7,B8,B9)

Stock price

BS call

price

Option

intrinsic

value

16.32 10

65 0.974881 0

70 1.823552 0

75 3.084287 0

80 4.808631 0

85 7.015908 0

90 9.695162 0

95 12.81164 5

100 16.31546 10

105 20.14963 15

110 24.25671 20

115 28.58313 25

120 33.08179 30

125 37.713 35

130 42.4445 40

135 47.25076 45

140 52.11206 50

This cell is part of the

data table header; it

contains the formula

=B11.

This cell is part of the data table

header. It contains a formula

=MAX(B5-B6,0)

which the

option's intrinsic value.

Comparing the BS Option Price (the curved line)

to the Option Intrinsic Value

when the stock price S is varied

-10

0

10

20

30

40

50

60

65 75 85 95 105 115 125 135

Stock price

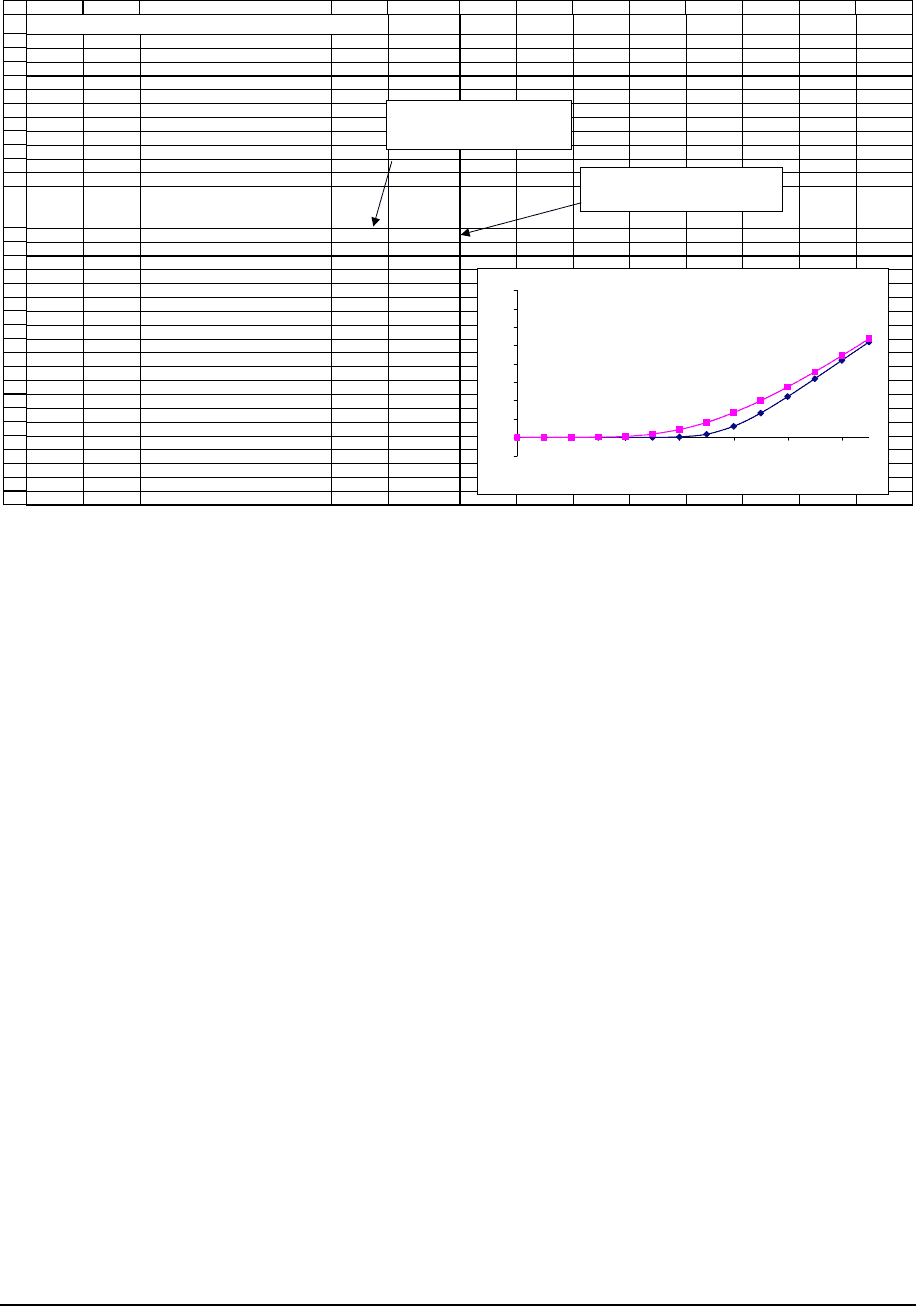

Example 2: The sensitivity of the Black-Scholes price to different estimates of

σ

Here’s the sensitivity analysis of the Black-Scholes price to the

σ

:

PFE Chapter 24, Black-Scholes and binomial page 16

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

AB C D E FGH I J KLM

BLACK-SCHOLES SENSITIVITY ON SIGMA

S 100 Current stock price

X90Exercise price

T 0.50000 Time to maturity of option (in years)

r 4.00% Risk-free rate of interest

Stock price

BS call

price

Option

intrinsic

value

13.15 19.90771512

10 0.00 0.00

20 0.00 0.00

30 0.00 0.01

40 0.00 0.09

50 0.00 0.53

60 0.01 1.78

70 0.24 4.25

80 1.72 8.14

90 5.96 13.41

100 13.15 19.91

110 22.14 27.38

120 31.86 35.60

130 41.80 44.37

140 51.78 53.53

150 61.78 62.96

160 71.78 72.57

This cell is part of the data table

header; it contains the formula

=calloption(B5,B6,B7,B8,20%).

This cell is part of the data table header.

It contains a formula

=calloption(B5,B6,B7,B8,50%).

Comparing the BS Option Price (the curved line)

for 2 values of Sigma

The top line is the higher sigma

-10

0

10

20

30

40

50

60

70

80

10 30 50 70 90 110 130

Stock price

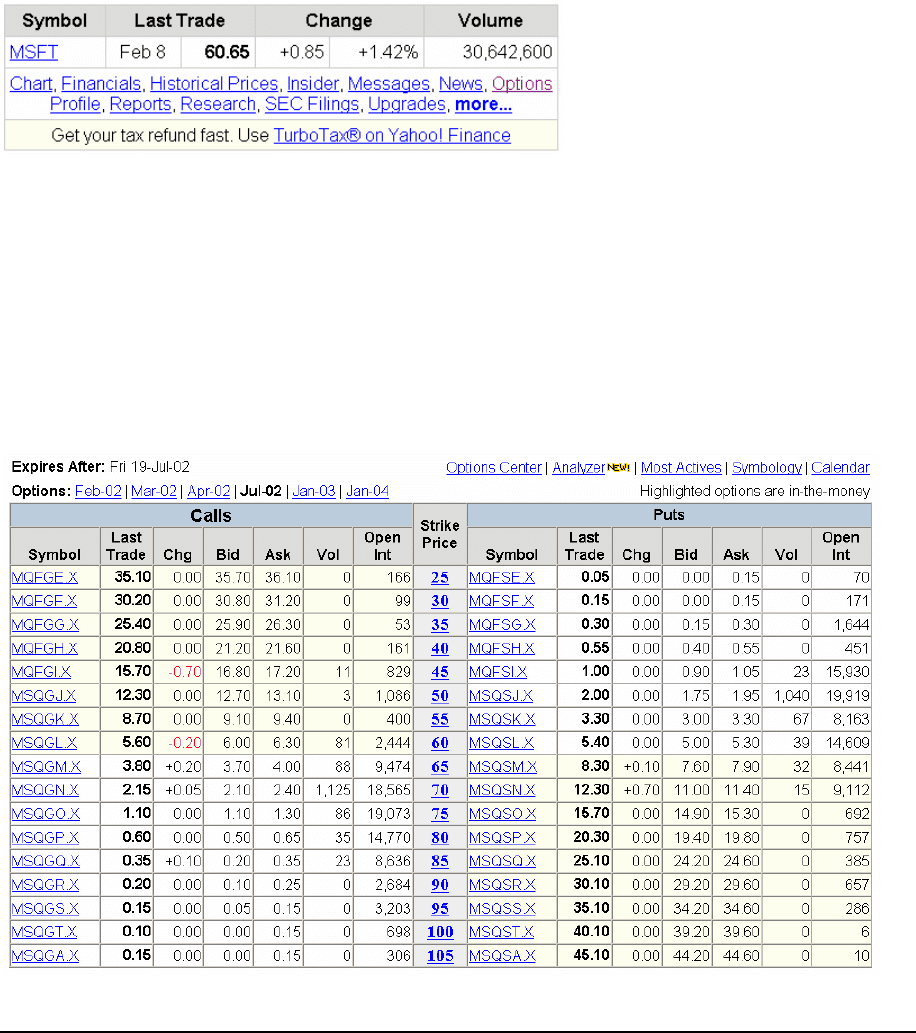

24.7. Does the Black-Scholes model work? Applying it to Microsoft options

To examine whether and how well the Black-Scholes model works, we do two

experiments in this section. First we compare the Black-Scholes option prices for a set of put

and call options on Microsoft stock to the actual market prices. Then we compare the implied

volatilities for the same options.

Our conclusion: Black and Scholes works “pretty well.” That’s a big complement for a

financial model!

Comparing actual market prices to Black-Scholes prices

The experiment we run here looks at options on Microsoft stock.

•

On 8 February 2002 we look at the call and put options on Microsoft stock which expire

in July 2002.

PFE Chapter 24, Black-Scholes and binomial page 17

• We calculate the Black-Scholes price of these options and compare it to the actual market

price.

As you will see, our conclusion is that the Black-Scholes model works pretty well.

We get our data from Yahoo, which allows us to look up the stock price of Microsoft on

8 February 2002 and also look up the prices of Microsoft options.

The closing stock price of Microsoft stock on 8 February 2002 was $60.65. The stock

was up 1.42% from the previous day’s close, and the total volume of stock traded was

30,642,600 shares.

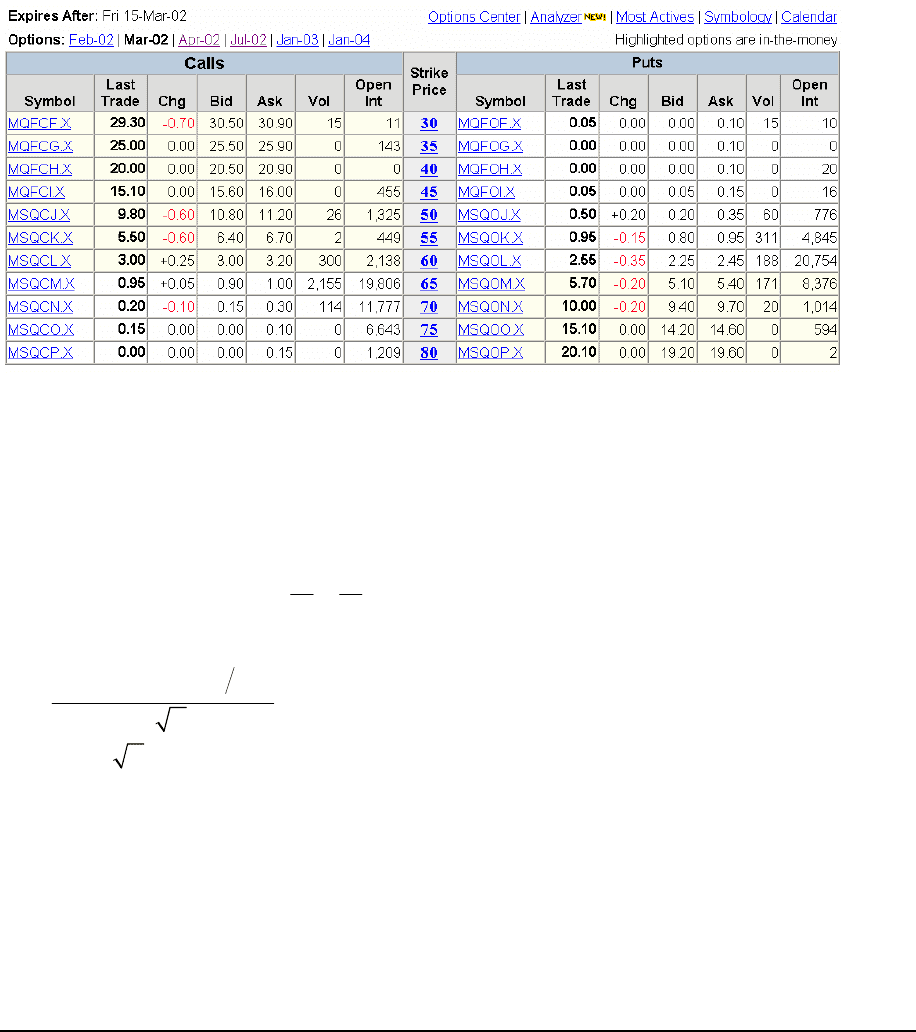

We now look at the closing prices of options on Microsoft stock which expire in July

2002. Clicking on

options in the above box leads us to the option prices:

PFE Chapter 24, Black-Scholes and binomial page 18

Look carefully at the above box:

•

Not all the options were traded on 8 February. For example—there was no “volume”

(and hence no trading) of either calls or puts with exercise price (“strike price”) of 25.

•

Significant amounts of call options traded on 8 February were only for exercise prices

X=60, 65, 70, 75, 80, 85. Significant amounts of put options traded were only for

exercise prices X = 45, 50, 55, 60, 65, 70.

•

The price of the “last trade” is in bold face black. But where there is no volume for this

day, the price refers to a previous day’s trading.

In the spreadsheet below we look at the Microsoft July options which actually traded on

8 February and compare the Black-Scholes price to the actual market price. We use the 6-month

Treasury bill rate of 1.7% as our risk-free rate.

5

5

We computed MSFT’s volatility by using Goal Seek to find

σ

such that the difference between the market price

and the Black-Scholes price of the at-the-money call is zero.

PFE Chapter 24, Black-Scholes and binomial page 19

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

37

38

39

40

41

42

43

44

45

46

47

48

49

ABC D E F GH I JK

MICROSOFT OPTIONS: Comparing BS to actual prices

This spreadsheet computes the Black-Scholes value of the Microsoft

July 02 options on 8 February 2002 and compares

the prices to the actual market prices. As you can

see, the Black-Scholes formula works pretty well!

Computing the time to maturity

S 60.65 Microsoft stock, closing price 8 Feb 02 Current date 8-Feb-02

T 0.35890 Time to maturity of option (in years) Expiration date 19-Jun-02

r 1.70% Risk-free rate of interest Time (days) 131 <-- =G8-G7

Sigma 35.38% Stock volatility Time (% of year) 0.3589 <-- =G9/365

Exercise

price

BS call

price

Actual call

market price

Market minus BS

in dollars

Market minus BS

in percentage

50 12.04 12.30 0.26 2.14% <-- =(D14-C14)/D14

55 8.43 8.70 0.27 3.11% <-- =(D15-C15)/D15

60 5.60 5.60 0.00 0.00%

65 3.54 3.80 0.26 6.82%

70 2.14 2.15 0.01 0.40%

75 1.25 1.10 -0.15 -13.20%

80 0.70 0.60 -0.10 -16.69%

85 0.38 0.35 -0.03 -9.30%

Exercise

price

BS put

price

Actual put

market price

Market minus BS

in dollars

Market minus BS

in percentage

45 0.37 1.00 0.63 62.83% <-- =(D26-C26)/D26

50 1.08 2.00 0.92 45.88%

55 2.44 3.30 0.86 25.92%

60 4.59 5.40 0.81 15.09%

65 7.50 8.30 0.80 9.69%

70 11.07 12.30 1.23 10.04%

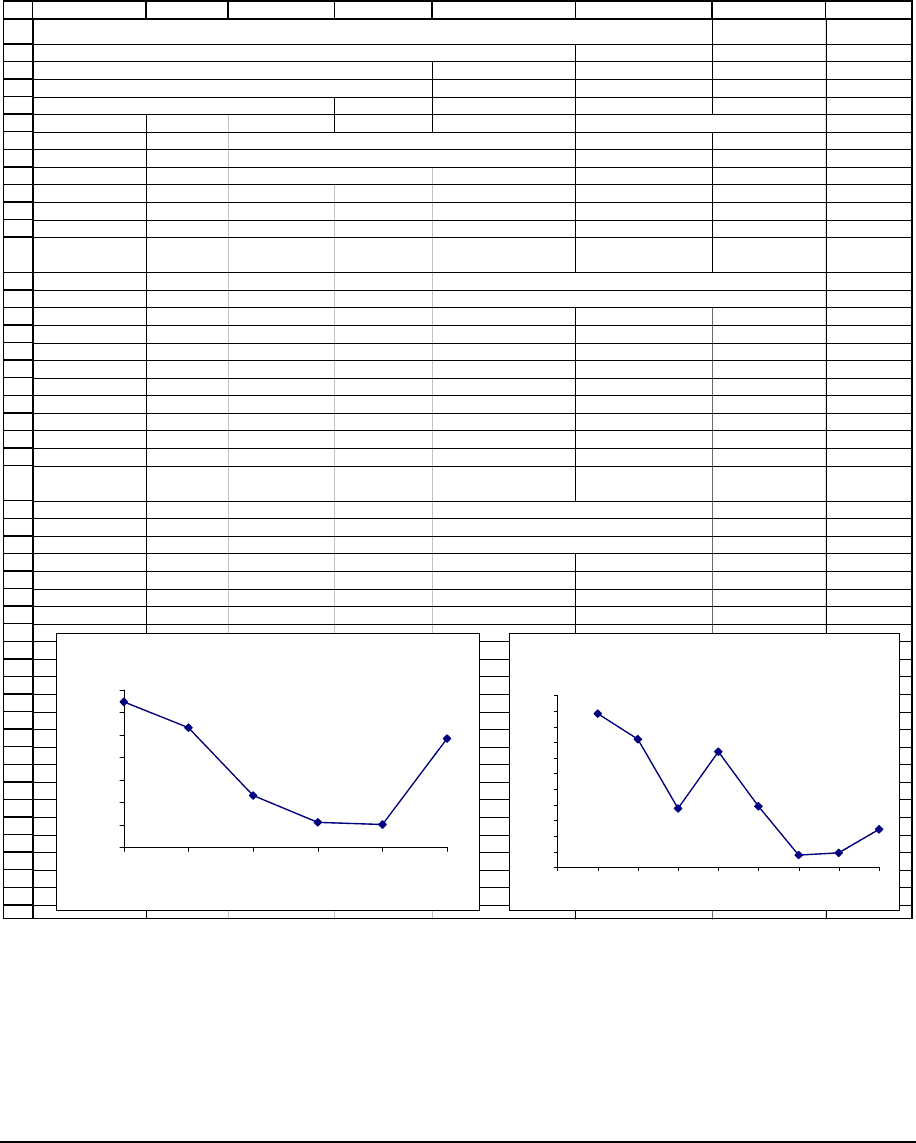

BS Call Option Pricing--

Microsoft July 02 Options

-20%

-15%

-10%

-5%

0%

5%

10%

50 55 60 65 70 75 80 85

Market minus BS

in percentage

BS Put Option Pricing--

Microsoft July 02 Options

0%

10%

20%

30%

40%

50%

60%

70%

45 50 55 60 65 70

Market minus BS

in percentage

The pattern of the prices is interesting:

•

In fact the BS model does a remarkably good job of pricing the calls.

•

There appears to be a much bigger bias in the put prices. Investors appear to price low

exercise puts at more than the Black-Scholes price. This phenomenon is often seen in

markets—it apparently stems from investor demand for puts as insurance. Having said

this, however, the market prices and the Black-Scholes prices show a remarkable

convergence.

Does the Black-Scholes model work? Looking at implied volatilities

PFE Chapter 24, Black-Scholes and binomial page 20

This is our second experiment. We take the Microsoft data above calculate the implied

volatility for each option (using the functions

CallVolatility and PutVolatility discussed in

Section ????). Here’s our spreadsheet:

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

37

38

39

40

41

42

43

44

45

46

47

48

49

ABC D E F GH

MICROSOFT OPTIONS: Computing the implied volatilities

This spreadsheet computes the implied volatility of the Microsoft

July 02 options on 8 February 2002 and compares

The average volatility of the calls appears to be lower

than the average implied volatility of the puts

Computing the time to maturity

S 60.65 Microsoft stock, closing price 8 Feb 02 Current date 8-Feb-02

T 0.35890 Time to maturity of option (in years) Expiration date 19-Jun-02

r 1.70% Risk-free rate of interest Time (days) 131 <-- =G8-G7

Time (% of year) 0.3589 <-- =G9/365

Exercise

price

Actual call

market price

Implied

volatility

50 12.30 38.42% <-- =CallVolatility($B$7,B14,$B$8,$B$9,C14)

55 8.70 37.60% <-- =CallVolatility($B$7,B15,$B$8,$B$9,C15)

60 5.60 35.38%

65 3.80 37.20%

70 2.15 35.45%

75 1.10 33.89%

80 0.60 33.96%

85 0.35 34.72%

Exercise

price

Actual put

market price

Implied

volatility

45 1.00 46.46% <-- =putVolatility($B$7,B26,$B$8,$B$9,C26)

50 2.00 45.32% <-- =putVolatility($B$7,B27,$B$8,$B$9,C27)

55 3.30 42.30% <-- =putVolatility($B$7,B28,$B$8,$B$9,C28)

60 5.40 41.10%

65 8.30 41.01%

70 12.30 44.83%

Microsoft Jul 2002 Calls--Calcuting the

Implied Volatility

34%

34%

35%

35%

36%

36%

37%

37%

38%

38%

39%

39%

45 50 55 60 65 70 75 80 85

Exercise price

Implied volatility

Microsoft July 2002 Puts--Calculating the

Implied Volatility

40%

41%

42%

43%

44%

45%

46%

47%

45 50 55 60 65 70

Exercise price

Implied volatility

The results are both encouraging and discouraging:

•

The implied volatilities for the calls are pretty close together, as are the implied

volatilities for the puts. This is good news.

PFE Chapter 24, Black-Scholes and binomial page 21

• On the other hand the implied volatilities for the puts are uniformly larger than the

implied volatilities for the calls. This is strange, since in the Black-Scholes formulation,

the implied volatility refers to the volatility of the stock’s return and hence has nothing to

do with whether we’re discussing a put or a call option.

•

On the third hand,

6

the actual difference between the implied volatilities for the calls and

the puts is not that great (only about 6%).

This is not the place to summarize the vast finance literature on implied volatilities. For

our purposes, the Black-Scholes model works pretty well. That’s enough!

Summary

This chapter has given you a quick and hopefully practical insight into how to use the

Black-Scholes model. Of all the financial models developed in the past 50 years, this model

works best. It is remarkably good at pricing options and is widely used. It is also easy to use,

provided you don’t get too hung up on the details of where the formula comes from (in this

chapter we’ve left these hang-ups behind us, and concentrated exclusively on implementational

details).

6

Harry Truman is reported to have gotten so sick of hearing economists say “On the hand, ... . But on the other

hand, ... ” that he asked his chief of staff to get him a “one-handed economist.” History does not record if he

succeeded. The economist in this section’s bullets has at least 3 hands. Harry Truman would not have liked him.

PFE Chapter 24, Black-Scholes and binomial page 22

Exercises

1. Use the Black-Scholes model to price the following:

•

A call option on a stock whose current price is 50, with exercise price X = 50, T =

0.5, r = 10%,

σ

= 25%.

•

A put option with the same parameters.

2. Use the data from exercise 1 and

Data|Table to produce graphs that show:

•

The sensitivity of the Black-Scholes call price to changes in the initial stock price S.

•

The sensitivity of the Black-Scholes put price to changes in

σ

.

•

The sensitivity of the Black-Scholes call price to changes in the time to maturity T.

•

The sensitivity of the Black-Scholes call price to changes in the interest rate r.

•

The sensitivity of the put price to changes in the exercise price X.

3. Produce a graph comparing a call’s intrinsic value (defined as Max(S-X,0) ) and its Black-

Scholes price. From this graph you should be able to deduce that it is never optimal to exercise

early a call priced by the Black-Scholes.

4. Produce a graph comparing a put’s intrinsic value (= Max(X-S,0) ) and its Black-Scholes

price. From this graph you should be able to deduce that it is may be optimal to exercise early a

put priced by the Black-Scholes formula.

PFE Chapter 24, Black-Scholes and binomial page 23

6. Use the Excel Solver to find the stock price for which there is the maximum difference

between the Black-Scholes call option price and the option’s intrinsic value. Use the following

values: S = 45, X = 45, T = 1,

σ

= 40%, r = 8%.

Repeat the MSFT exercise in the text for the March 2002 options:

9. Note that you can use the Black-Scholes formula to calculate the call option premium as a

percentage of the exercise price in terms of S/X:

() () () ()

()

12 12

2

1

21

ln( / ) 2

rT rT

CS

C SNd Xe Nd Nd e Nd

XX

where

SX r T

d

T

dd T

σ

σ

σ

−−

=− ⇒= −

++

=

=−

Implement this in a spreadsheet.