Principles of Finance with Excel (Основы финансов c Excel)

Подождите немного. Документ загружается.

PFE Chapter 24: Facts about option prices page 13

At time 0 (today):

• Buy one share of Microsoft stock for $63

• Buy one put with exercise price X = $60 for $3

• Write one call with X = $60, collecting (today) C

0

= $15

• Take a loan of $54.55; the loan has a one-year maturity (like the

options). At the current interest rate of 10% you will have to pay off

$60 in one year.

At time T we close out all our positions

• Sell our share of Microsoft at the prevailing market price S

T

• Exercise the put, if this is profitable

• Have the call exercised against us, if this is profitable for the call buyer

• Repay the loan

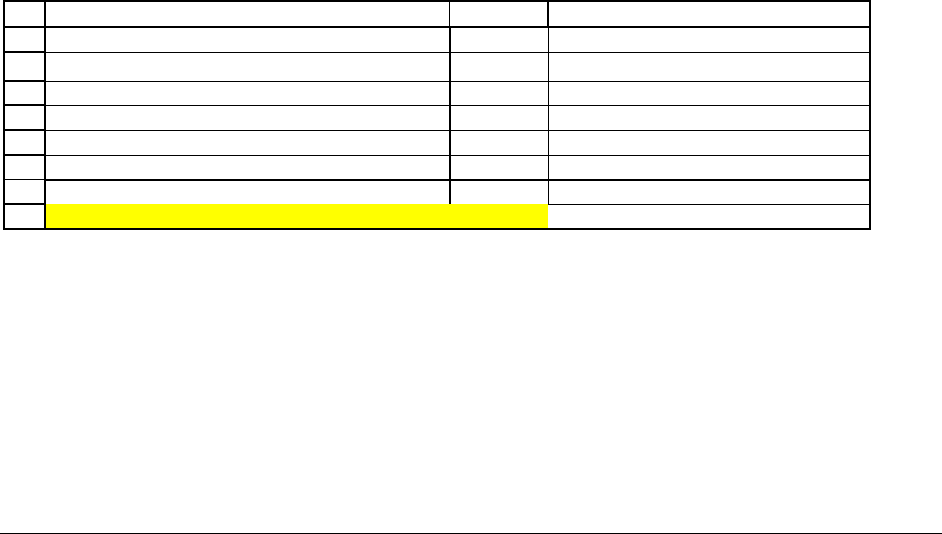

Our example above shows that the cash flow at

T=1 will be zero if S

T

= $90. The cash

flow will also be zero if

S

T

= $35:

20

21

22

23

24

25

26

27

ABC

Cash flow at time T

S

T

, stock price at time T

35

Sell stock 35 <-- =B21

Exercise the put? 25 <-- =MAX(B3-B21,0)

Cash flow from call 0 <-- =-MAX(B21-B3,0)

Repay loan -60 <-- =-B3

Total 0 <-- =SUM(B23:B26)

As you can see, no matter what the Microsoft stock price in one year, the cash flow at

T=1 from this strategy will be zero. However, the strategy has a positive initial cash flow of

$3.55. Clearly this is an arbitrage!

Symbolically, the future cash flow is given by:

PFE Chapter 24: Facts about option prices page 14

N

[

]

[

]

N

()

Loan repayment

Stock value

Put payoff Cash flow to call

writer at 1

,0 ,0

0

TTT

T

TT T

TT T

SMaxXSMaxSX X

SXSXifSX

SSXXifSX

=

+−−−−

+− − <

⎧

=

⎨

−−− ≥

⎩

=

A little thought will reveal that—given the stock price

S

0

= 60, the interest rate r=10%,

the exercise price

X = 60 of both the put and the call, and the call option price of $15—the put

option price must be $6.55 to prevent arbitrage. This follows from the put-price parity relation:

()

00 0

60

15 63 6.55

1.10

Put Call PV X S=+ −

=+ −=

24.4. Fact 4: Bound on an American put option price:

[

]

00

,0PMaxXS>−

Suppose you’re contemplating buying an American put on Microsoft stock. The stock’s

price today is S

0

= $63 and the option exercise price is X = $70. Clearly the option should sell

for at least $7. If not, you could easily devise an arbitrage, as illustrated in the spreadsheet

below:

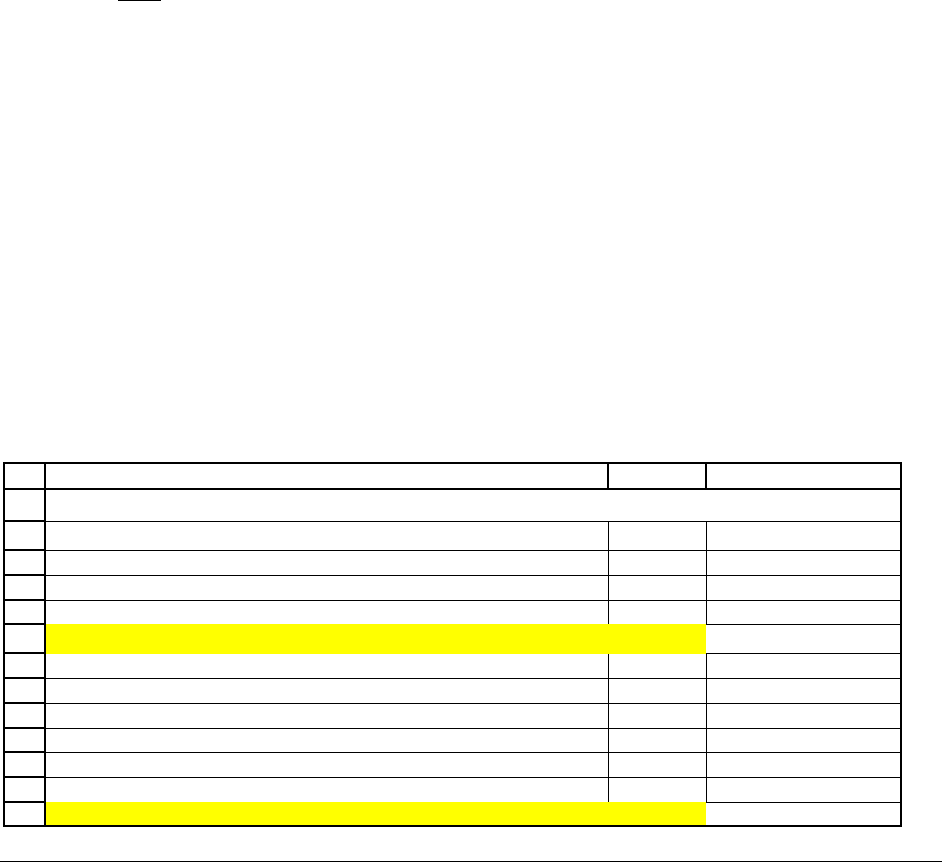

1

2

3

4

5

6

7

8

9

10

11

12

13

ABC

Microsoft stock price, 15 August 2001, S

0

63

Option exercise price, X 70

Option exercise time, T (in years) 1

Fact 4: Lower bound of American put: P

0

> Max[X - S

0

, 0]

7 <-- =MAX(B3-B2,0)

Arbitrage strategy

American put option price 3

Buy option -3

Buy stock now -63

Exercise put option immediately: deliver stock and get

X

70

Immediate profit 4 <-- =SUM(B10:B12)

FACT 4: Lower bound on

American

put price

PFE Chapter 24: Facts about option prices page 15

If the American put option is mispriced (that is, its price is less than $7), you can make

money by; buying the option, buying the stock, and exercising the option immediately. This

arbitrage profit will not exist if the option’s price is greater than $7.

24.5. Fact 5: Bounds on European put option prices

()

00

,0PMaxPVX S>−⎡⎤

⎣⎦

Fact 5 is the “put parallel” for Fact 1 about calls.

5

1

2

3

4

5

6

7

8

9

ABC

Microsoft stock price, 15 August 2001, S

0

63

Option exercise price, X 70

Option exercise time, T (in years) 1

Interest rate, r 10%

Lower bound on call price

Lower bound of American put: P

0

> Max[X - S

0

, 0]

7 <-- =MAX(B3-B2,0)

Fact 5: P

0

> Max[PV(X) - S

0

,0]

0.6364 <-- =MAX(B3/(1+B5)^B4-B2,0)

FACT 5: Lower bound on

European

put price

5

There’s a crucial difference in the parallel between Facts 1 and 5: Fact 1 applies to all calls, whether European or

American. Fact 5 applies only to European puts. Of course in both cases, the assumption is that the stock pays no

dividends before option maturity.

PFE Chapter 24: Facts about option prices page 16

American versus European Puts

Fact 5 says that the price of a European put can actually be much lower than the price of

an American put. Consider the example above, in which we look at the price of a put option on

Microsoft stock with T = 1 and X = 70. If our put was an American put, then it couldn’t sell for

less than $7. On the other hand, a European put, which cannot be exercised until date T, can sell

for anything more than $0.6364.

24.6. Fact 6: You might find it optimal to early-exercise an American put on

a non-dividend paying stock

Recall that you’ll never find it optimal to early-exercise an American call on a non-

dividend paying stock. But this is not necessarily true for a put option. Here’s an example:

Suppose that you’re currently holding an option on PFE stock. You bought the option

some time ago, when PFE stock’s price was still healthy. However, at the current date, the stock

has taken a plunge and is selling for $1 per share. Your American put option has an exercise

price of X = $100 and expires in one year. The interest rate is 10%. If you exercise the option

now, you’ll have a net payoff of $99 ($100 minus the current value of the stock of $1), which—if

you invest it in bonds with an interest rate of 10%--will be $99*1.10=$108.90 in one year. This

is more than anyone would have if they waited for a year until exercise.

Therefore any rational holder of an American put option will choose to early exercise the

option if the current stock price is very low.

PFE Chapter 24: Facts about option prices page 17

24.7. Fact 7: Option prices are convex (somewhat advanced)

Suppose we have three calls, each with a different exercise price but with the same time

to exercise T, written on the same stock. Suppose that the exercise price of the first call is X =

$15, the exercise price of the second call is X = $20, and the exercise price of the third call is X

= $25. Call price convexity says that for 3 such “equally spaced” calls, the middle call price

must be less than the average of the two extreme call prices. In an equation:

()

()

(

)

15 25

20

2

Call price X Call price X

Call price X

=+ =

=<

To see the meaning of convexity, we return to the Cisco example from Chapter 23.

Consider the three call options in rows 18, 20, and 22 of the next spreadsheet. The convexity

relation says that:

()

()

(

)

15 25

4.50 0.20

20 2.35

22

Call price X Call price X

Call price X

=+ =

+

=< = =

Since the Cisco call with X = $20 is selling for $1.35 (cell C20), it fulfills the convexity relation.

PFE Chapter 24: Facts about option prices page 18

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

ABCDEF

August 7, 2001, CSCO closing price 19.26

Stated expiration date

Exercise

price, X

Call price Put price

Actual

expiration

date

Days to

maturity

Aug01 7.50 11.90 0.05 17 Aug01 10

Aug01 10.00 9.60 0.20 17 Aug01 10

Aug01 12.50 6.50 0.10 17 Aug01 10

Aug01 15.00 4.20 0.10 17 Aug01 10

Aug01 17.50 2.10 0.40 17 Aug01 10

Aug01 20.00 0.65 1.45 17 Aug01 10

Aug01 22.50 0.15 3.40 17 Aug01 10

Aug01 25.00 0.05 5.00 17 Aug01 10

Aug01 27.50 0.10 7.50 17 Aug01 10

Aug01 30.00 0.10 11.90 17 Aug01 10

Aug01 32.50 0.05 17 Aug01 10

Aug01 35.00 0.05 16.20 17 Sep01 41

Sep01 10.00 9.50 21 Sep01 45

Sep01 12.50 6.30 0.15 21 Sep01 45

Sep01 15.00 4.50 0.40 21 Sep01 45

Sep01 17.50 2.75 0.90 21 Sep01 45

Sep01 20.00 1.35 2.00 21 Sep01 45

Sep01 22.50 0.55 3.80 21 Sep01 45

Sep01 25.00 0.20 5.50 21 Sep01 45

CISCO OPTIONS, August 7, 2001

CLOSING PRICE ON CHICAGO

BOARD OF OPTIONS EXCHANGE

Why do call prices have to be convex?

In this subsection we use a butterfly strategy (Chapter 23, page000) to show you why call

prices always have to be convex. Recall that a butterfly strategy consists of buying one low-

priced and one high-priced call and selling two medium-priced calls.

Suppose that the call option prices for Cisco were different from those actually seen in

the market. In the example below, we show how our butterfly would have looked had the X =

$20 call been priced at $2.50 instead of $1.35:

PFE Chapter 24: Facts about option prices page 19

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

37

38

39

40

41

42

43

44

45

46

ABCDEFGH

Call prices

XPrice

15 4.50

20 2.50 <-- The actual price is $1.35. To illustrate arbitrage, we assume $2.50

25 0.20

September

Cisco

stock price

Payo

ff

on

September

X=15

call

Payo

ff

on

September

X=20

call

Payo

ff

on

September

X=25

call

Total

profit

0 -4.5 5 -0.2 0.3 <-- =D10+C10+B10

5 -4.5 5 -0.2 0.3

10 -4.5 5 -0.2 0.3

15 -4.5 5 -0.2 0.3

16 -3.5 5 -0.2 1.3

17 -2.5 5 -0.2 2.3

18 -1.5 5 -0.2 3.3

19 -0.5 5 -0.2 4.3

20 0.5 5 -0.2 5.3

21 1.5 3 -0.2 4.3

22 2.5 1 -0.2 3.3

23 3.5 -1 -0.2 2.3

24 4.5 -3 -0.2 1.3

25 5.5 -5 -0.2 0.3

26 6.5 -7 0.8 0.3

30 10.5 -15 4.8 0.3

35 15.5 -25 9.8 0.3

40 20.5 -35 14.8 0.3

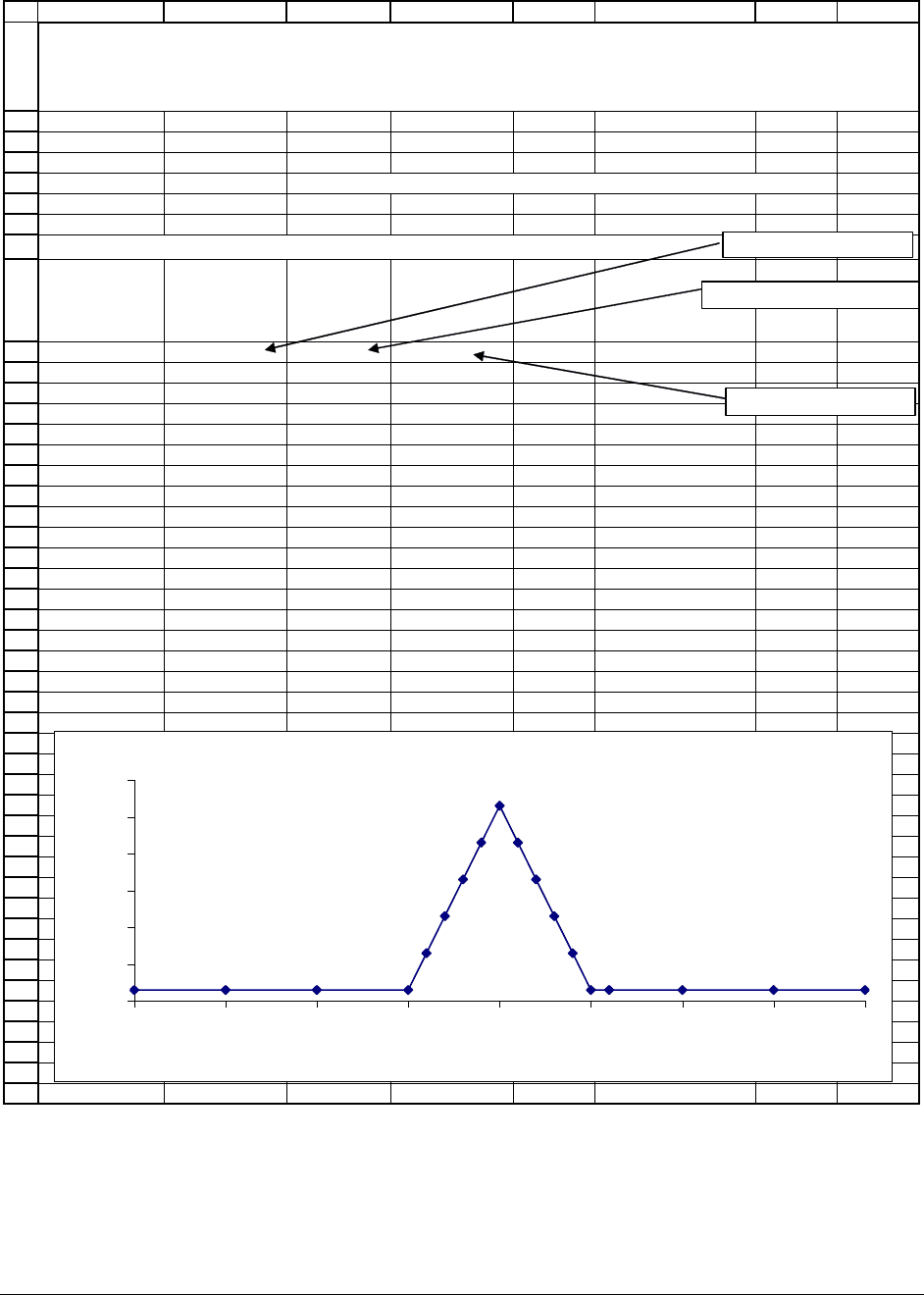

WHEN DOES A BUTTERFLY INDICATE AN ARBITRAGE OPPORTUNITY?

Strategy: Buy 1 September X=15 Call, Write 2 September X=20 Calls,

Buy 1 September X=25 Call

Butterfly payoff and profits

Butterfly: Profit Pattern

When the total profit line is > x-axis, there's an arbitrage opportunity!

0

1

2

3

4

5

6

0 5 10 15 20 25 30 35 40

Cisco stock price, September

Total profit

=MAX(A10-15,0)-$B$4

=-2*(MAX(A10-20,0)-$B$5)

=MAX(A10-25,0)-$B$6

Notice that the total profit graph is completely above the x-axis. This means that—no

matter what the stock price in September, you will make a profit. This is clearly not logical—

something is wrong with these prices!

PFE Chapter 24: Facts about option prices page 20

You get the same thing if you assume that the X = $15 call option is priced at $2.25

instead of $4.50:

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

37

38

39

40

41

42

43

44

45

46

ABCDEFGH

Call prices

XPrice

15 2.25 <-- The actual price is $4.50. To illustrate arbitrage, we assume $2.25

20 1.35

25 0.20

September

Cisco

stock price

Payo

ff

on

September

X=15

call

Payo

ff

on

September

X=20

call

Payo

ff

on

September

X=25

call

Total

profit

0 -2.25 2.7 -0.2 0.25 <-- =D10+C10+B10

5 -2.25 2.7 -0.2 0.25

10 -2.25 2.7 -0.2 0.25

15 -2.25 2.7 -0.2 0.25

16 -1.25 2.7 -0.2 1.25

17 -0.25 2.7 -0.2 2.25

18 0.75 2.7 -0.2 3.25

19 1.75 2.7 -0.2 4.25

20 2.75 2.7 -0.2 5.25

21 3.75 0.7 -0.2 4.25

22 4.75 -1.3 -0.2 3.25

23 5.75 -3.3 -0.2 2.25

24 6.75 -5.3 -0.2 1.25

25 7.75 -7.3 -0.2 0.25

26 8.75 -9.3 0.8 0.25

30 12.75 -17.3 4.8 0.25

35 17.75 -27.3 9.8 0.25

40 22.75 -37.3 14.8 0.25

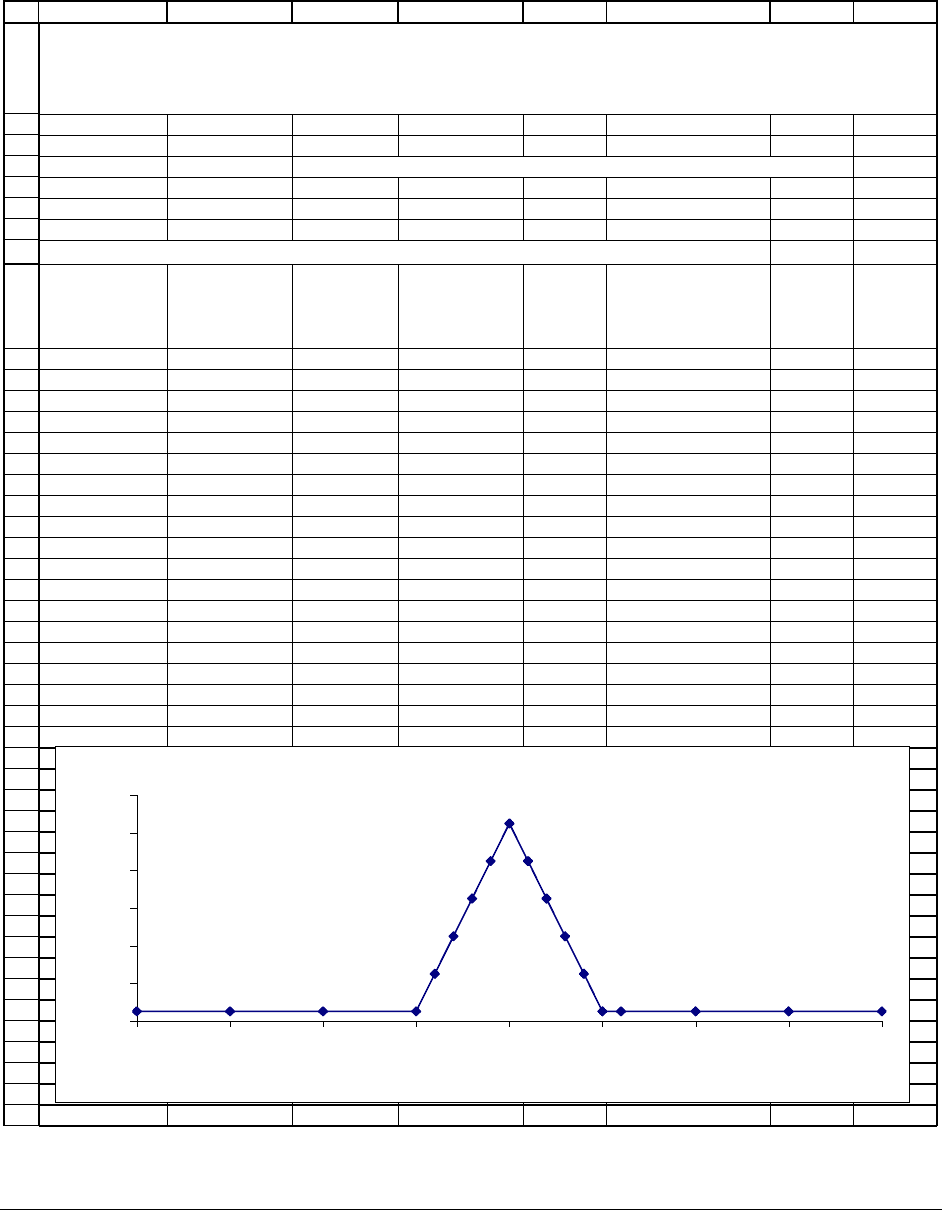

WHEN DOES A BUTTERFLY INDICATE AN ARBITRAGE OPPORTUNITY?

Strategy: Buy 1 September X=15 Call, Write 2 September X=20 Calls,

Buy 1 September X=25 Call

Butterfly payoff and profits

Butterfly: Profit Pattern

When the total profit line is > x-axis, there's an arbitrage opportunity!

0

1

2

3

4

5

6

0 5 10 15 20 25 30 35 40

Cisco stock price, September

Total profit

PFE Chapter 24: Facts about option prices page 21

What’s wrong?

Playing around a bit with the numbers will convince you that a condition necessary for

the butterfly graph to straddle the x-axis is:

()

()

(

)

2

Low High

Middle

Call price X Call price X

Call price X

+

< ,

where

,,

Low Middle High

XX X are three equally-spaced exercise prices.

This condition—in the jargon of the options markets referred to as the convexity property

of call prices—says that for 3 “equally spaced” calls, the middle call price must be less than the

average of the two extreme call prices. Another way of saying this is that the line connecting

two call prices always lies above the graph of the call prices:

PFE Chapter 24: Facts about option prices page 22

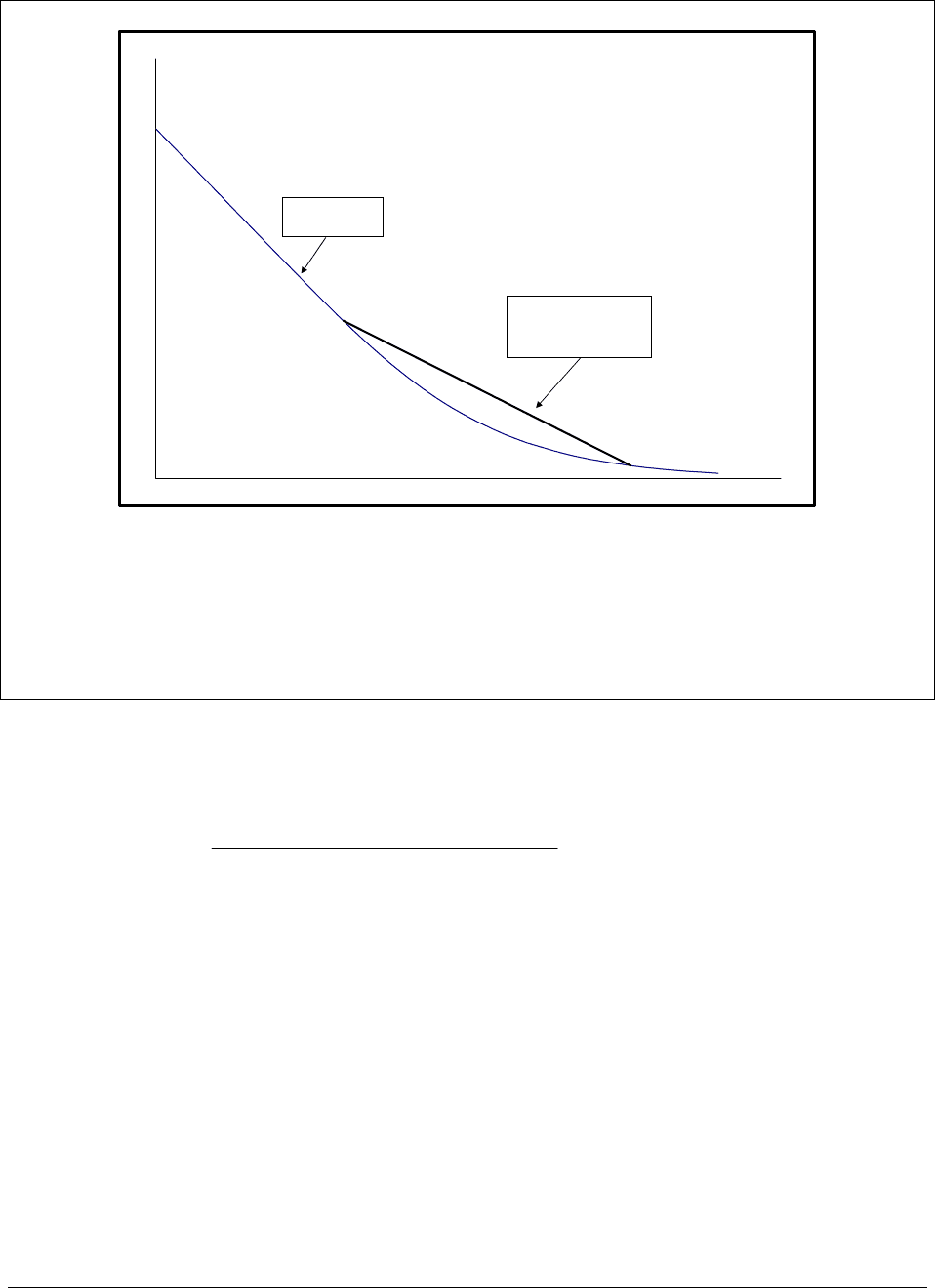

The Convexity of Call Prices

Call exercise price, X

Call price

Call price: Declines

as exercise price

increases

Straight line connecting 2 call

prices: always above

the call pricing line (this is the

convexity)

Figure 24.1: The curved line illustrates the actual call prices for various exercise prices. Call

price convexity means that the line connecting two call prices is always above the actual call

pricing curve.

Put prices are also convex.

()

()

(

)

2

Low High

Middle

Put price X Put price X

Put price X

+

<

We leave put butterflies as an exercise and let you prove this on your own. Here’s the way put

prices look: