Principles of Finance with Excel (Основы финансов c Excel)

Подождите немного. Документ загружается.

PFE Chapter 23: Facts about option prices page 2

Overview

In this chapter we discuss some facts about option pricing. Our emphasis is on a set of

propositions knows as

arbitrage restrictions on option prices. These restrictions specify

relations between the prices of puts and calls and the prices of either the stock underlying the

options or a risk-free asset.

Notation: Throughout the chapter we use the following notation

0

price of stock at time 0 (today)

price of stock on option exercise date

option exercise price

interest rate

call option price at time 0 (today); sometimes we also write this as

put option pric

T

0

S

ST

X

r

CC

P

=

=

=

=

=

=

0

e at time 0 (today); sometimes we write this as

call option price at time

put option price at time

t

t

P

Ct

Pt

=

=

Dividends: We assume that the stock on which the options are written does not pay

dividends before the option maturity date. This is not an overly-restrictive assumption: Stocks

which pay dividends tend to do so at regular intervals (quarterly, semi-annually, or annually).

Holders of options on these stocks are thus reasonably sure when the stocks will pay a dividends.

There are thus long periods of time when market participants can be assured that a stock will not

pay a dividend.

For example: General Motors pays a regular quarterly dividend in February, May,

August, and November. An investor who purchases an option on GM in March with an April

maturity knows that in the intervening period no dividends will be paid on the stock.

Many other stocks have never paid a dividend and investors in these stocks’ options can

be reasonably assured that the dividend pricing restriction imposed in this chapter is not

PFE Chapter 23: Facts about option prices page 3

restrictive. Stocks which fall into this category include many of the high-tech stocks whose

options tend to attract the most investor interest.

Finance concepts discussed in this chapter

•

Option pricing restrictions

• No early exercise of calls

• Put-call parity

• Early exercise of American puts

• Option price convexity

Excel functions used

•

Max

• Sum

23.1. Fact 1: Call price of an option >

(

)

0

,0Max S PV X

−

It’s 15 August 2001, and you’re considering buying a call option on Microsoft. Currently

the MSFT share itself is selling for S

0

= $63; you want to buy a call on MSFT with an exercise

price X = 60 and with time to maturity T = 1 year. Furthermore, we’ll suppose that the option is

an American call option, and can be exercised at any time on or before T.

We will examine Fact 1 in two stages. We start with a “dumb fact,” something that is

obvious once we say it, and then proceed to demonstrate Fact 1 for you.

Dumb fact:

[

]

0

,0Call price Max S X≥−

.

PFE Chapter 23: Facts about option prices page 4

Now it’s probably clear to you that the Microsoft option should be selling for at least $3.

To see this, suppose that the option is selling for $2. We’ll devise an arbitrage strategy—a

strategy which will make us money risklessly:

Action taken today Cash flow (negative

numbers indicate

costs)

Buy the option -$2

Immediately exercise the option, buying the

stock

-$60

Immediately sell the stock on the open market +$63

Arbitrage profit +$1

So the “dumb fact”—that an American call option should sell for more than the

difference between the stock price and the exercise price—is pretty obvious.

Smart fact:

(

)

0

,0Call price Max S PV X

>−

.

1

This is a lot less obvious than the previous fact. It’s also a lot more powerful. The

“dumb fact” above says that the option should sell for at least $3. As the spreadsheet below

shows, the “smart fact” says much more; if, for example, the interest rate is 10%, then the smart

fact says that the option should sell for at least $8.45.

1

How smart? Robert Merton, who first established this and lots of other facts about options, subsequently won the

Nobel Prize for economics, in part for his work on option pricing.

PFE Chapter 23: Facts about option prices page 5

1

2

3

4

5

6

7

8

9

10

ABC

FACT 1: Lower bound on call price

Microsoft stock price, 15 August 2001, S

0

63

Option exercise price, X 60

Option exercise time, T (in years) 1

Interest rate, r 10%

Lower bound on call price

Dumb fact, call price > Max[S

0

- X,0]

3 <-- =MAX(B3-B4,0)

Fact 1: call price > Max[S

0

- PV(X),0]

8.45 <-- =MAX(B3-B4/(1+B6)^B5)

To prove the “smart fact,” let’s assume that you can buy the call for $5. We’ll show that

there exists an arbitrage strategy, and we will therefore conclude that the option price is too low.

Definition: An arbitrage strategy is a combination of assets—usually short or long positions in

the stock, calls and puts on the stock, and a risk-free security—which produces positive cash

flows at all points in time. If you can design an arbitrage strategy for a given set of asset prices

(as we do below), it shows that at least one of the prices is wrong.

Here’s the strategy. At time 0 (today), we will:

At time 0 (today):

•

Short one share of the stock

• Invest in a riskless security paying off the call’s exercise price at time

T.

• Buy a call on the option.

At time T:

•

Purchase the stock on the open market at the time-T price, in order to

close the short position

PFE Chapter 23: Facts about option prices page 6

• Collect from our investment in the riskless security

• Exercise the option if this is profitable

Here’s an example, which assumes that the stock price at time 0 is 63 and that the interest

rate is 10%:

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

ABC

Arbitrage proof

Call price at time 0 (today) 5

Actions at time 0 (today)

Short the stock 63 <-- =B3

Buy a bond which pays of X at time T -54.55 <-- =-B4/(1+B6)^B5

Buy a call -5 <-- =-B16

Total cash flow at time 0

3.45 <-- =SUM(B19:B21)

Cash flow at time T

S

T

, stock price at time T

33

Repay the shorted stock -33 <-- =-B25

Collect money from the bond 60 <-- =B4

Exercise the call? 0 <-- =MAX(B25-B4,0)

Total 27 <-- =SUM(B27:B29)

In cells B25:B30 we calculate the cash flow at time T=1 from the strategy. In the

example above, Microsoft stock at T is selling for $33. In this case, we would have a positive

time T cash flow of $27.

In the example below, we assume that Microsoft stock at T is 90. In this case you

exercise the call (giving you a positive cash flow of $30), but the total payoff from the strategy is

now $0:

24

25

26

27

28

29

30

ABC

Cash flow at time T

S

T

, stock price at time T

90

Repay the shorted stock -90 <-- =-B25

Collect money from the bond 60 <-- =B4

Exercise the call? 30 <-- =MAX(B25-B4,0)

Total 0 <-- =SUM(B27:B29)

PFE Chapter 23: Facts about option prices page 7

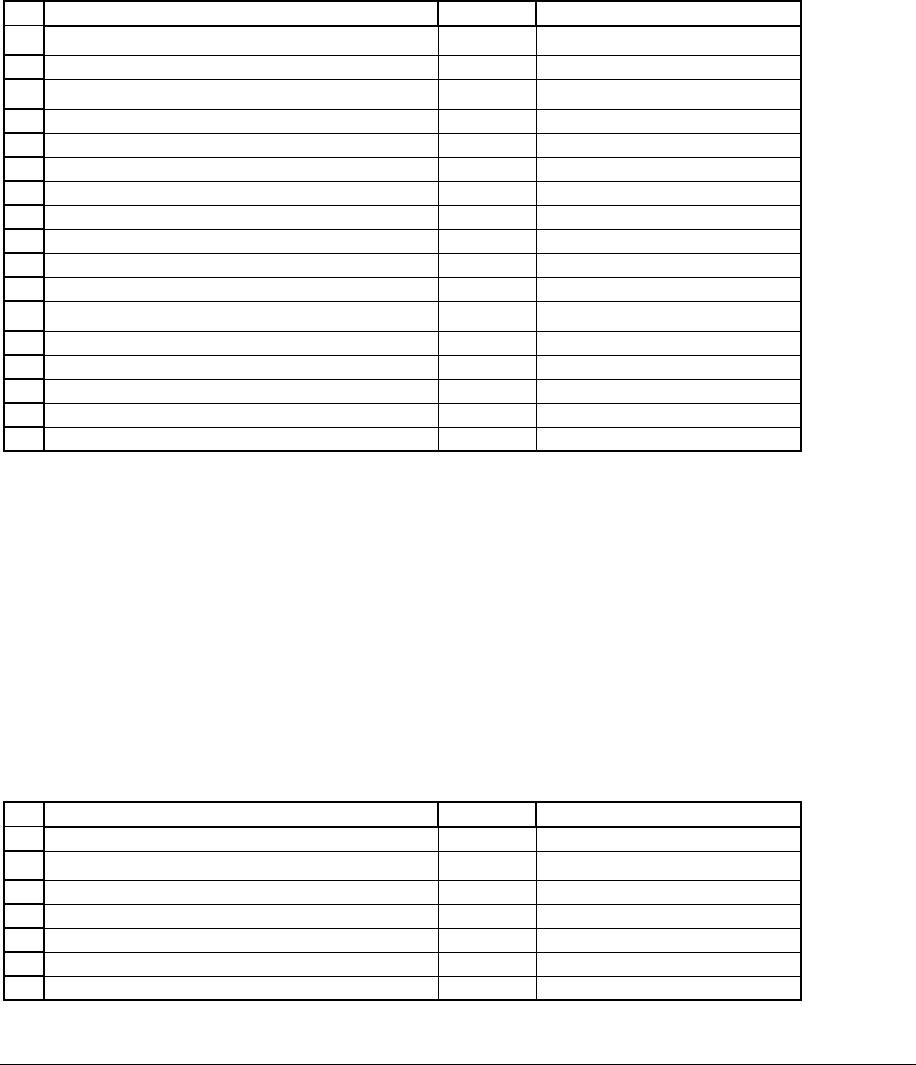

If we build a data table (see Chapter ???) for the time-T cash flow from the strategy, we

see that the strategy always has a positive cash flow:

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

ABCDEFGHIJKLM

Data table: Cash

Arbitrage proof

Flow from strategy

Call price at time 0 (today) 10

S

T

<-- Data table header is hidden

060

Actions at time 0 (today) 555

Short the stock 63 <-- =B3 10 50

Buy a bond which pays of X at time T -54.55 <-- =-B4/(1+B6)^B5 15 45

Buy a call -10 <-- =-B16 20 40

Total cash flow at time 0 -1.55 <-- =SUM(B19:B21) 25 35

30 30

Cash flow at time T 35 25

S

T

, stock price at time T

33 40 20

45 15

Repay the shorted stock -33 <-- =-B25 50 10

Collect money from the bond 60 <-- =B4 55 5

Exercise the call? 0 <-- =MAX(B25-B4,0) 60 0

Total 27 <-- =SUM(B27:B29) 65 0

70 0

75 0

80 0

85 0

Cash Flow at time T from Fact 1 Arbitrage

Strategy

-10

0

10

20

30

40

50

60

70

0 5 10 15 20 25 30 35 40 45 50 55 60 65 70 75 80 85 90

S

T

Time T cash flow

So: We’ve designed an arbitrage:

• At time 0, the cash flow is $3.45 > 0

• At time T, the cash flow is either positive (if the stock price S

T

< 60) or zero.

You can’t lose from this strategy!! In a rational world this means that something is wrong with

the asset prices. In this case, it’s clear what’s wrong—the call price is too low.

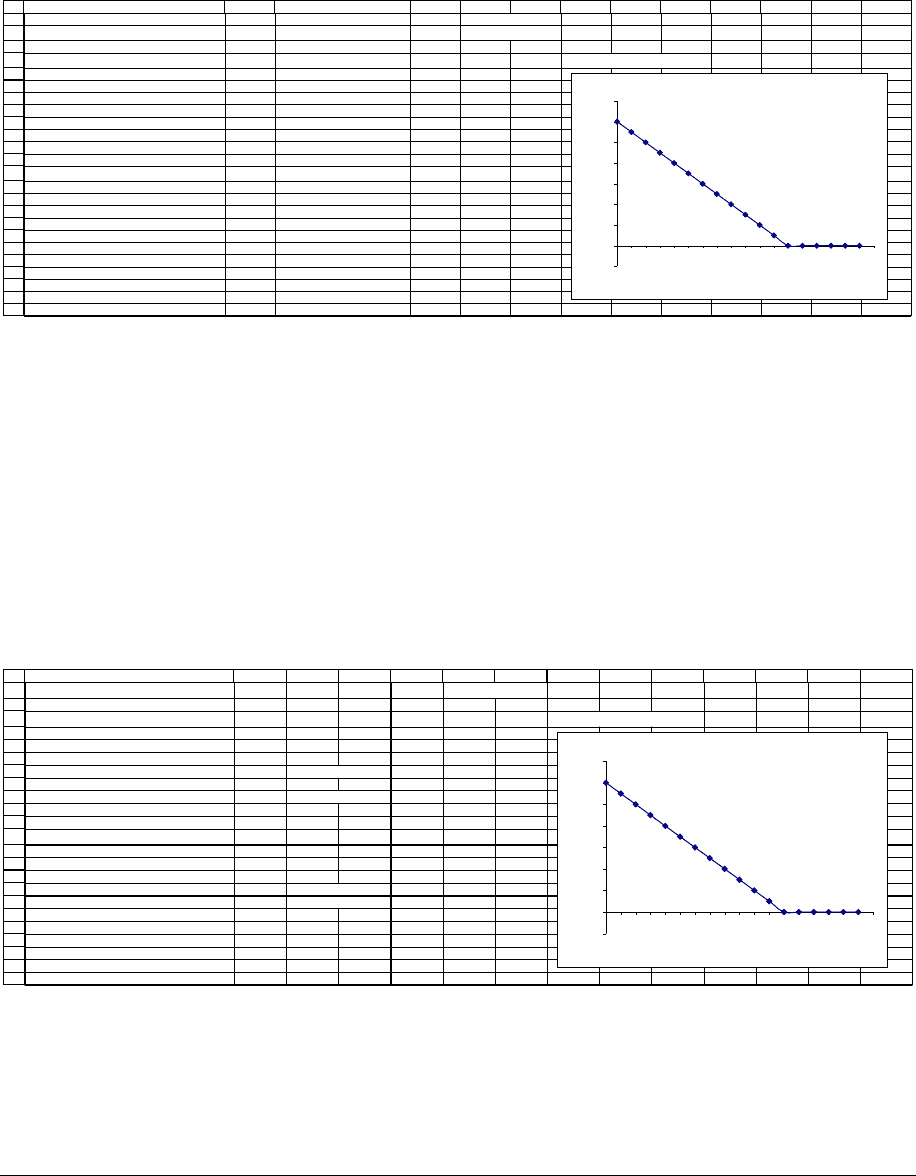

To see this, consider the case where the call price is $10:

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

ABCDEFGHIJKLMN

Arbitrage proof

Flow from strategy

Call price at time 0 (today) 10

S

T

<-- Data table header is hidden

060

Actions at time 0 (today) 555

Short the stock 63 <-- =B3 10 50

Buy a bond which pays of X at time T -54.54545 <-- =-B4/(1+B6)^B5 15 45

Buy a call -10 <-- =-B16 20 40

Total cash flow at time 0

-1.545455 <-- =SUM(B19:B21) 25 35

30 30

Cash flow at time T 35 25

S

T

, stock price at time T

90 40 20

45 15

Repay the shorted stock -90 <-- =-B25 50 10

Collect money from the bond 60 <-- =B4 55 5

Exercise the call? 30 <-- =MAX(B25-B4,0) 60 0

Total 0 <-- =SUM(B27:B29) 65 0

70 0

75 0

80 0

85 0

Cash Flow at time T from Fact 1 Arbitrage

Strategy

-10

0

10

20

30

40

50

60

70

0 5 10 15 20 25 30 35 40 45 50 55 60 65 70 75 80 85 90

S

T

Time T cash flow

The cash flows at T (shown in the graph) don’t change, but the initial cash flow (cell B22) is now

negative. This makes more sense: If the call price is > 8.45, then you have to invest money

today in order to have a non-negative cash flow in the future.

PFE Chapter 23: Facts about option prices page 8

We’ve proved our first option pricing fact:

()

0

,0Call price Max S PV X

>−

.

23.2. Fact 2: It’s never worthwhile to exercise a call early.

2

Suppose that on 15 August 2001 you bought a Microsoft call option for $12 (note that

this price does not violate Fact 1’s price restriction). Furthermore, suppose that the option

expires one year from today, on 15 August 2002.

Now suppose that after 8 months (approximately 2/3 of a year), you want to get rid of the

option. To make the problem interesting, we’ll assume that the price of Microsoft has risen to

$80. You have two possibilities:

• You could exercise the option. In this case you would collect $20 =

[

]

[

]

,0 80 60,0

t

Max S X Max−= −

.

• You could also sell the option on the open market. Of course, we don’t know what

the option’s price would be, but Fact 1 tells us that in no case will the price be less

than

()

()

()

1

12/3

,0 ,0

1

60

80 ,0 21.876

110%

tt

t

X

Max S PV X Max S

r

Max

−

−

−=−

+

=− =

+

What should you do? Clearly you should sell rather than exercise the call.

2

When the call is written on a non-dividend-paying stock.

PFE Chapter 23: Facts about option prices page 9

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

ABCDEFGHI

FACT 2: No early exercise of calls

Assumption: Stock pays no dividends between t = 0 and T

Microsoft stock price, 15 August 2001, S

0

63

Option exercise price, X 60

Option exercise time, T (in years) 1

Interest rate, r 10%

Call price at time 0 12

t=0 t=0.6 1

Buy option for $12.00 Consider selling the option

or exercising it.

Stock price, S

t

80

Payoff from option exercise 20 <-- =MAX(E15-B5,0)

Minimum value of option

according to Fact 1 22.24439 <-- =MAX(E15-B5/(1+$B$7)^(1-0.6),0)

Exercise option or sell it? sell <-- =IF(E19>E17,"sell","exercise")

23.3. Fact 3: Put-call parity

(

)

00 0

Put Call PV X S

=

+−

Put-call parity states that the put price is determined by the call price, the stock price, and

the risk-free rate of interest.

3

Here’s an example: Suppose that we’re considering a one-year put

option on the Microsoft stock we’ve been discussing throughout this chapter. What should be

the put price on Microsoft—where we assume that the put has the same exercise price X=60 and

the same time to maturity T=1?

1

2

3

4

5

6

7

8

9

ABC

FACT 3: Put-Call Parity

Microsoft stock price, 15 August 2001, S

0

63

Option exercise price, X 60

Option exercise time, T (in years) 1

Interest rate, r 10%

Call price 15

Put price by put-call parity 6.55 <-- =B8+B4/(1+B6)^B5-B3

Here’s a proof of the important fact about option pricing. We assume that t

3

Again: Recall that the assumption is that the stock pays no dividends before the option maturity date T.

PFE Chapter 23: Facts about option prices page 10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

ABC

Arbitrage proof of put-call parity

Put price today (t=0) 3

Actions at time 0 (today)

Buy stock -63 <-- =-B3

Buy put -3 <-- =-B13

Write call 15

Take a loan of PV(X) at risk-free interest 54.55 <-- =B4/(1+B6)^B5

Total cash flow at time 0 3.55 <-- =SUM(B16:B19)

Cash flow at time T

S

T

, stock price at time T

90

Sell stock 90 <-- =B23

Exercise the put? 0 <-- =MAX(B4-B23,0)

Cash flow from call -30 <-- =-MAX(B23-B4,0)

Repay loan -60 <-- =-B4

Total 0 <-- =SUM(B25:B28)

In the example above we assumed that at time 0 the put was priced at $3. We then

designed an arbitrage strategy:

At time 0 (today):

• Buy one share of Microsoft stock for $63

•

Buy one put with exercise price X = $60 for $3

•

Write one call with X = $60, collecting (today) $15

•

Take a loan of $54.55; the loan has a one-year maturity (like the

options). At the current interest rate of 10% you will have to pay off

$60 in one year.

At time T we close out all our positions

• Sell our share of Microsoft at the prevailing market price S

T

•

Exercise the put, if this is profitable

•

Have the call exercised against us, if this is profitable for the call buyer

•

Repay the loan

PFE Chapter 23: Facts about option prices page 11

Our example above shows that the cash flow at T=1 will be zero if S

T

= $90. The cash

flow will also be zero if S

T

= $35:

22

23

24

25

26

27

28

29

ABC

Cash flow at time T

S

T

, stock price at time T

35

Sell stock 35 <-- =B23

Exercise the put? 25 <-- =MAX(B4-B23,0)

Cash flow from call 0 <-- =-MAX(B23-B4,0)

Repay loan -60 <-- =-B4

Total 0 <-- =SUM(B25:B28)

As you can see, no matter what the Microsoft stock price in one year, the cash flow at

T=1 from this strategy will be zero. However, the strategy has a positive initial cash flow of

$3.55. Clearly this is an arbitrage!

Symbolically, the future cash flow is given by:

N

[

]

[

]

N

()

Loan repayment

Stock value

Put payoff Cash flow to call

writer at 1

,0 ,0

0

TTT

T

TT T

TT T

SMaxXS MaxSX X

SXSXifSX

SSXXifSX

=

+−−−−

+−− <

=

−−− ≥

=

A little thought will reveal that—given the stock price S

0

= 60, the interest rate r=10%,

the exercise price X = 60 of both the put and the call, and the call option price of $15—the put

option price must be $6.55 to prevent arbitrage.