Principles of Finance with Excel (Основы финансов c Excel)

Подождите немного. Документ загружается.

PFE Chapter 22, Dividend policy and firm valuation Page 2

Overview

The purpose of this chapter is to study the effect of dividend policy on the value of the

firm:

• What’s a dividend?

• Why might it have an effect on firm value?

• MM dividend irrelevance proposition

• Taxation and dividends: capital gains versus ordinary income

• Empirical evidence?

Finance concepts discussed

• Dividends

• Retained earnings

• Capital gains versus ordinary income

Excel functions used

We use a lot of Excel spreadsheets to put order in things, but truth to tell, this chapter

uses hardly any sophisticated Excel concepts. The one function used is Sum.

PFE Chapter 22, Dividend policy and firm valuation Page 3

22.1. Dividends

John and Mary both own taxi companies. Operationally the taxi companies are exactly

alike: Each company owns the same number of taxis, and has the same income and expenses.

Here are the balance sheets for the two companies:

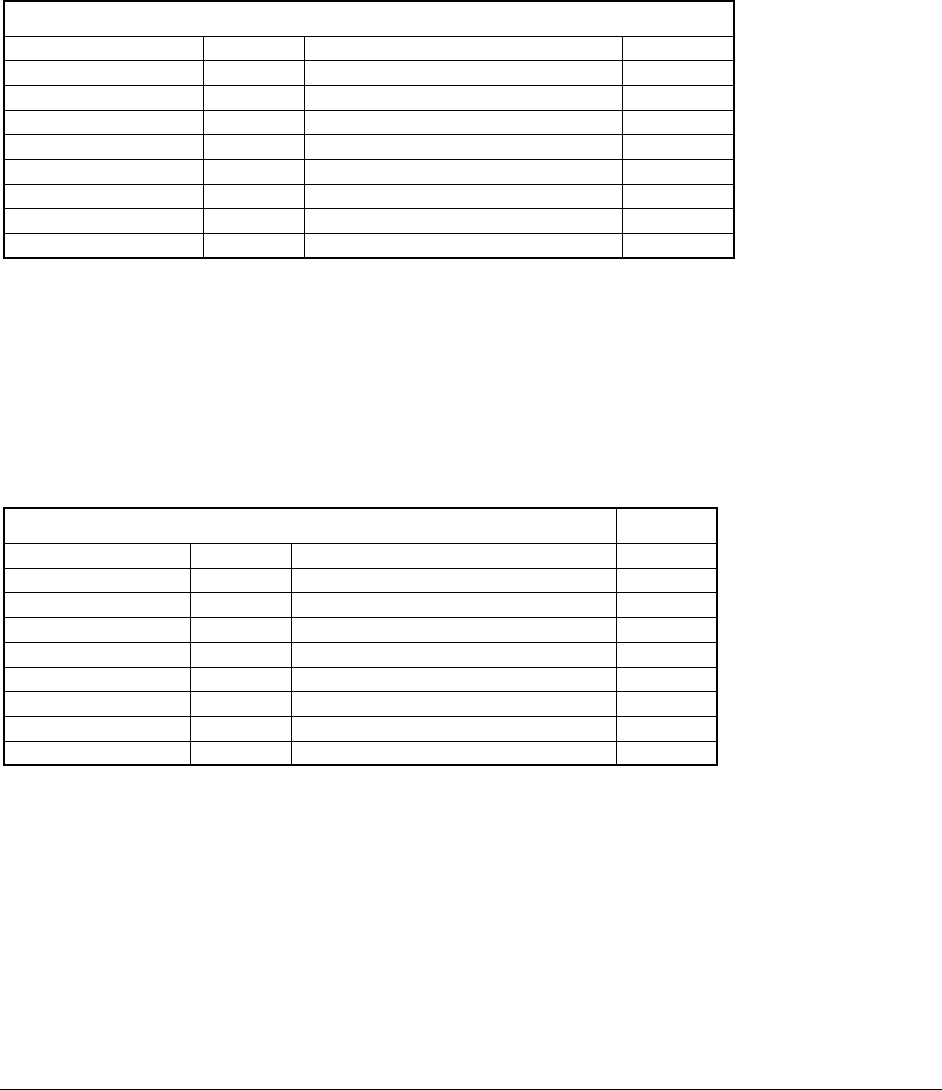

JOHN'S TAXI COMPANY, MARY'S TAXI COMPANY

Assets Liabilities and equity

Cash 5,000 Debt 10,000

Taxis 20,000 Equity

Stock 5,000

Accumulated retained earnings 10,000

Total assets

25,000

Total liabilities and equity

25,000

John pays himself a dividend

Suppose that John wants some cash and decides to declare a dividend of $3,000. Here’s

the way his balance sheet looks (Mary’s balance sheet is unchanged):

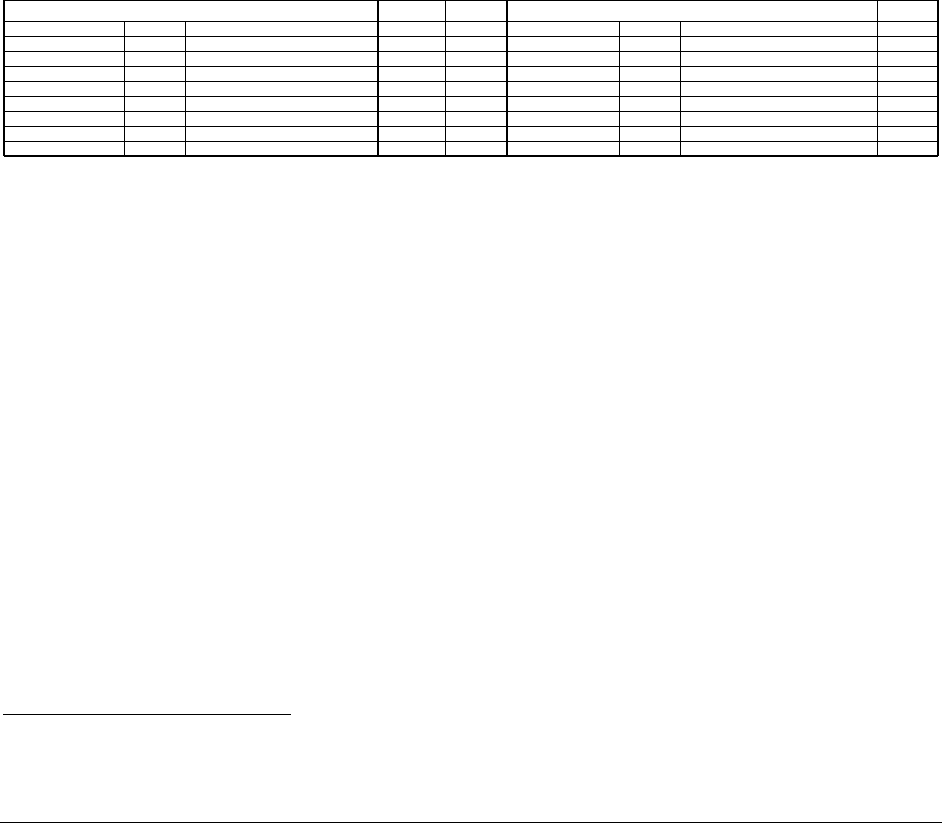

JOHN'S TAXI COMPANY--after dividend

Assets Liabilities and equity

Cash 2,000 Debt 10,000

Taxis 20,000 Equity

Stock 5,000

Accumulated retained earnings 7,000

Total assets

22,000

Total liabilities and equity

22,000

Notice that there are two changes in John’s balance sheet:

• The cash balances decrease from $5,000 to $2,000, reflecting the dividend paid.

• The accumulated retained earnings decrease from $10,000 to $7,000. This is what is

meant by the expression that “dividends are paid out of retained earnings.” We don’t

PFE Chapter 22, Dividend policy and firm valuation Page 4

like this expression, since dividends are paid out of cash; the decrease in retentions

simply reflects the matching change made in the balance sheet.

Here are some finance-type questions you could ask about this situation:

The valuation effects of the dividend

Did the dividend paid by John change the value of his taxi business vis-à-vis Mary’s

business? Obviously not—they both still have the same number of taxis, and Mary has just kept

her cash in the business instead of, as John did, pulling it out. A good way to see this is to to

write the balance sheets in terms of net debt—subtracting the cash from the debt:

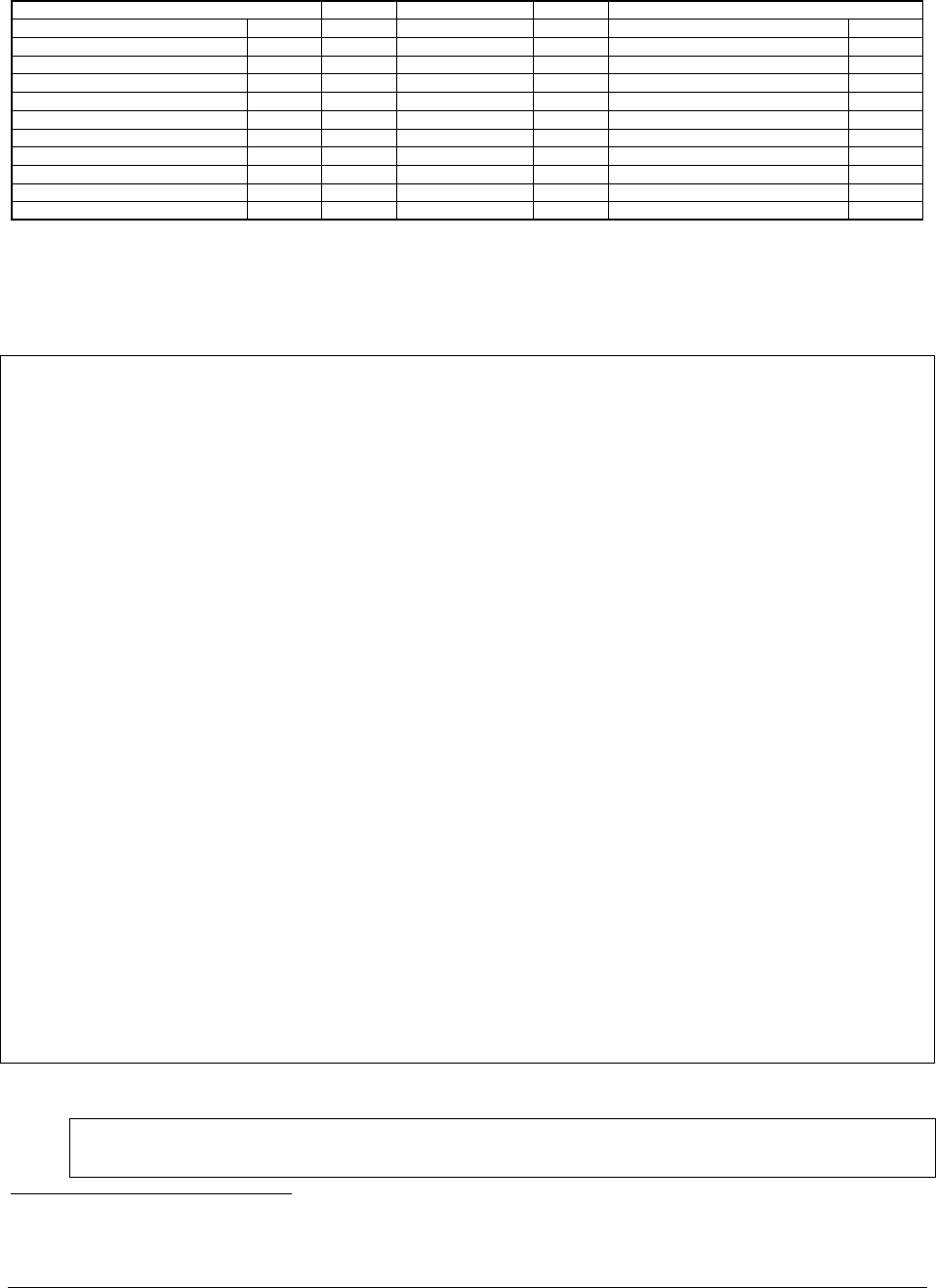

JOHN'S or MARY'S TAXI COMPANY--net debt JOHN'S TAXI COMPANY--after dividend

Assets Liabilities and equity

A

ssets Liabilities and equity

Net debt = Debt - cash 5,000 Net debt = Debt - cash 8,000

Taxis 20,000 Equity Taxis 20,000 Equity

Stock 5,000 Stock 5,000

Accumulated retained earnings 10,000 Accumulated retained earnings 7,000

Total assets 20,000 Total liabilities and equity 20,000 Total assets 20,000 Total liabilities and equity 20,000

The asset side of the balance sheet is still worth the same, whether or not the dividend has been

paid.

1

On the other hand, the liabilities and equity side of the balance sheet is different—John

has more debt and less equity than Mary.

Perhaps it’s just a capital structure question?

The above balance sheets for the two companies show that—while they are both the same

on the asset side, the dividend has changed the capital structure of the companies. So perhaps

the dividend question is related to the capital structure problem discussed in Chapters 20 and 21.

If so, this suggests

1

In a more general context we can ***************

PFE Chapter 22, Dividend policy and firm valuation Page 5

• Dividends might matter if capital structure matters: An after-dividend company (like

John’s) will have a higher debt/equity ratio than a before-dividend company (like

Mary’s).

• If companies with a higher debt/equity ratio have a higher valuation, then companies

should pay dividends.

Now this book takes a definite stand on this question: In the previous chapters we’ve suggested

that the capital structure question is ultimately a question of balancing personal against corporate

taxation. We’ve also suggested that the economic evidence suggests that on balance the taxes

are pretty much of a wash, so that capital structure doesn’t matter.

Though this argument suggests that dividends do not affect the valuation of a company,

there’s another tax aspect to this question—the tradeoff between ordinary income taxes and

capital gains taxes. We discuss this in the next section.

In the meantime: As long as Mary and John’s taxi companies aren’t taxed and as long as

Mary and John aren’t taxed on a personal level, the debt/equity aspects of the dividend decision

shouldn’t affect the valuation of their companies.

The dividend doesn’t affect the enterprise value

Here’s another way of thinking about this question: Suppose that both John and Mary are

thinking about selling their taxi companies. The “taxi part” of the business is worth $40,000

(this doesn’t include the cash balances on the books). John and Mary have slightly different

strategies about how to sell the business: John intends to first pay himself a dividend and then

sell the business, whereas Mary intends to sell the business first without taking a dividend. Here

are the calculations:

PFE Chapter 22, Dividend policy and firm valuation Page 6

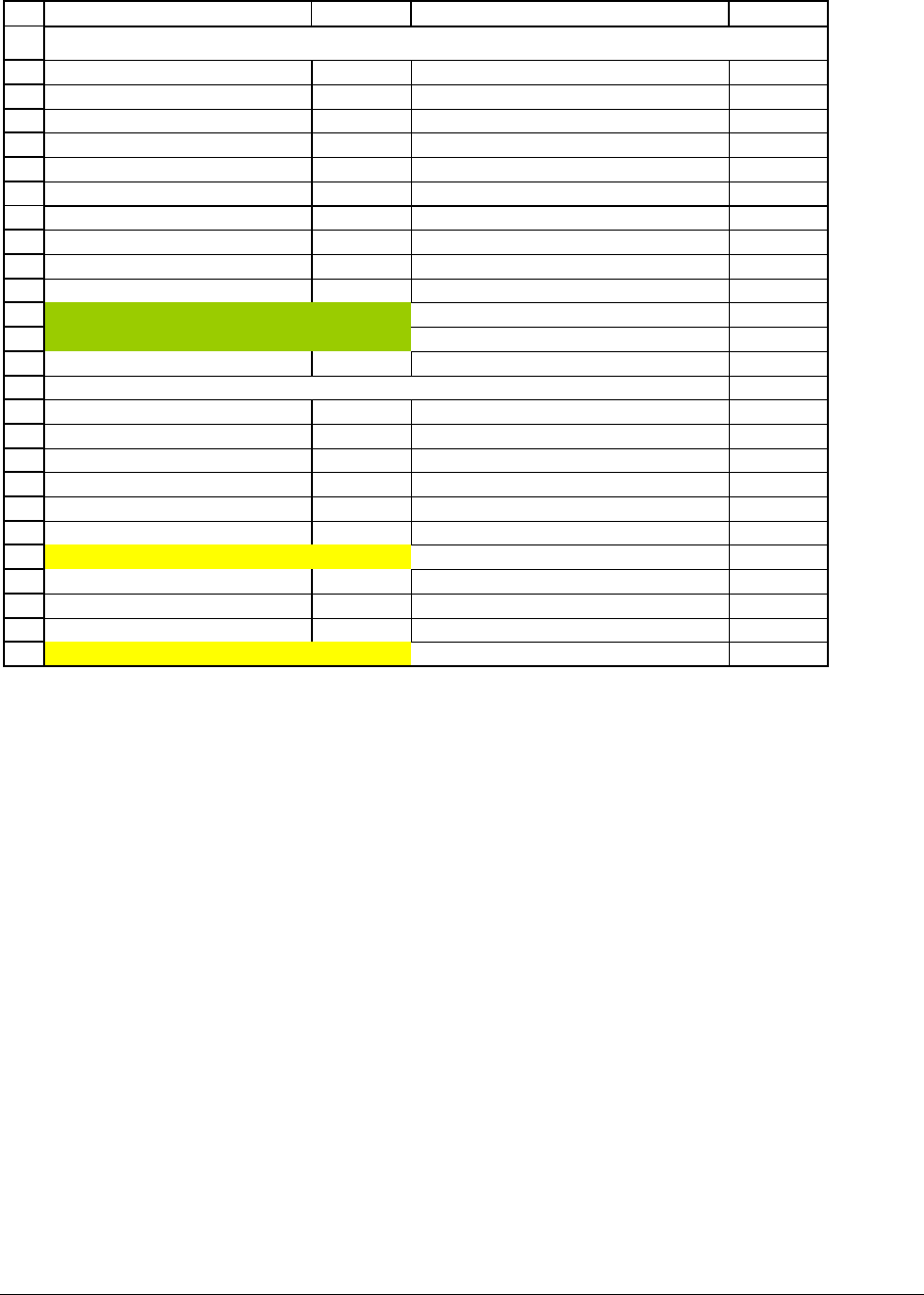

Mary sells her taxi company for $40,000 John sells his taxi company for $40,000

Sale price 40,000 Sale price 40,000

Pay back net debt 5,000 Pay back net debt 8,000

Net to equity 35,000 Net to equity 32,000

Book value of equity 12,000 Book value of equity 12,000

Taxable gain 23,000 Taxable gain 20,000

Taxes on gain (0%) 0 Taxes on gain (0%) 0

Net to Mary from sale 35,000 Net to John from sale 32,000

Add back dividend 0 Add back dividend 3,000

Taxes on dividend (0%) 0 Taxes on dividend (0%) 0

Total 35,000 Total 35,000

Clearly it doesn’t matter.

2

Who cares where the money is as long as it’s there?

This is really what it’s all about—who cares whether the money is in the taxi company or

in the individual bank account of the owner? Of course you can think of many answers to this

question which make it appear that it does matter:

• Taxes: If the company and its owners pay different tax rates, perhaps dividends are

worthwhile (or not—read on).

• Trust: If there are multiple owners of the company, maybe you want the money in your

hands as opposed to leaving it in the company. Economists call this “agency costs”—an

agent being someone you’ve hired to do your work for you (that is, the manager). The

agency cost argument for paying dividends suggests that you and your manager may have

different goals; if the manager’s goal includes wasting your money, then maybe you

should get the money out of his hands by paying a dividend.

•

Miller and Modigliani’s “dividend irrelevance” proposition (1961)

2

Although—to anticipate the next section, the assumption that there are no taxes is critical to this argument.

PFE Chapter 22, Dividend policy and firm valuation Page 7

The enterprise value of the firm—the sum of the values of the operating current assets

and fixed assets—is not affected by dividend policy. On the other hand, an increased

dividend implies a corresponding decrease in the market value of the firm’s equity.

22.2. Taxes!

In the above section we’ve made two points:

• The value of the “taxi part” of the business—the enterprise value—is not affected by the

dividend policy of John and Mary’s taxi business

• The proceeds—dividends plus gains from selling the business—to John and Mary are

exactly the same, independent of their dividend policy.

Now look at the second point again, and suppose that we introduce taxes. We’ll assume that

dividends are taxed as “ordinary income” at a rate of 30% and that the gains from selling the

business are taxed at a capital gains tax rate of 15%.

We’ll start with John, who sells his taxi company for $40,000 right after he’s paid

himself a $3,000 dividend. As the calculation below shows, John’s net from the sale of the

company is $31,1000:

PFE Chapter 22, Dividend policy and firm valuation Page 8

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

FG H I

Assets Liabilities and equity

Net debt = Debt - cash 8,000

Taxis 20,000 Equity

Stock 5,000

Accumulated retained earnings 7,000

Total assets 20,000 20,000

Capital gains tax 15%

Dividend tax 30%

John sells his taxi company for $40,000

Sale price 40,000

Pay back net debt 8,000

Net to equity 32,000 <-- =G16-G17

Book value of equity 12,000 <-- =SUM(I7:I8)

Taxable gain 20,000 <-- =G18-G19

Taxes on capital gain (15%) 3,000 <-- =$G$12*G20

Net to John from sale 29,000 <-- =G18-G21

Add back dividend 3,000

Taxes on dividend (30%) 900 <-- =$G$13*G24

Total 31,100 <-- =G22+G24-G25

JOHN'S TAXI COMPANY--after dividend

Now Mary: She also sells her company, but she hasn’t paid herself a dividend. Her net

is higher:

PFE Chapter 22, Dividend policy and firm valuation Page 9

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

AB C D

Assets Liabilities and equity

Net debt = Debt - cash 5,000

Taxis 20,000 Equity

Stock 5,000

Accumulated retained earnings 10,000

Total assets 20,000 Total liabilities and equity 20,000

Capital gains tax 15%

Dividend tax 30%

Mary sells her taxi company for $40,000

Sale price 40,000

Pay back net debt 5,000

Net to shareholders (Mary) 35,000 <-- =B16-B17

Book value of equity 15,000 <-- =SUM(D7:D8)

Taxable gain 20,000 <-- =B18-B19

Taxes on capital gain (15%) 3,000 <-- =$B$12*B20

Net to Mary from sale 32,000 <-- =B18-B21

Add back dividend 0

Taxes on dividend (30%) 0 <-- =$B$13*B24

Total 32,000 <-- =B22+B24-B25

MARY'S TAXI COMPANY

The reason for the difference between John’s net of $31,100 and Mary’s net of $32,000 is

that dividends are taxed. By not paying herself a dividend, Mary has saved herself $900 =

30%*3,000 of taxes on her dividends.

3

This analysis suggests that dividends might matter if there is both a dividend tax and a

capital gains tax: In this case you shouldn’t pay dividends.

3

In any case both John and Mary are going to pay the same capital gains taxes. This is because a dividend, paid out

of cash, reduces the firm’s equity and increases the firm’s net debt. The result, as you can confirm from the

examples, is that the capital gain to the firm’s shareholders is independent of the dividend.

PFE Chapter 22, Dividend policy and firm valuation Page 10

What if John really needs the money? Solution 1: pay a bonus

Suppose for some reason John really needs the money now. Then he should pay himself

a bonus, which is a tax-deductible expense for the company:

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

AB C DEF G H I

Assets Liabilities and equity

A

ssets Liabilities and equity

Cash 2,000 Debt 10,000 Cash 3,200 Debt 10,000

Taxis 20,000 Equity Taxis 20,000 Equity

Stock 5,000 Stock 5,000

Accumulated retained earnings 7,000 Accumulated retained earnings 8,200

Total assets 22,000 Total liabilities and equity 22,000 Total assets 23,200 Total liabilities and equity 23,200

Corporate tax rate 40% Corporate tax rate 40%

Capital gains tax 15% Capital gains tax 15%

Dividend tax 30% Dividend tax 30%

John sells his taxi company for $40,000 John sells his taxi company for $40,000

Sale price 40,000 Sale price 40,000

Pay back net debt 8,000 <-- =D4-B4 Pay back net debt 6,800 <-- =I4-G4

Net to equity 32,000 <-- =B17-B18 Net to equity 33,200 <-- =G17-G18

Book value of equity 12,000 <-- =SUM(D7:D8) Book value of equity 13,200 <-- =SUM(I7:I8)

Taxable gain 20,000 <-- =B19-B20 Taxable gain 20,000 <-- =G19-G20

Taxes on capital gain (15%) 3,000 <-- =$B$13*B21 Taxes on capital gain (15%) 3,000 <-- =$B$13*G21

Net to John from sale 29,000 <-- =B19-B22 Net to John from sale 30,200 <-- =G19-G22

Add back dividend 3,000 Add back dividend 3,000

Taxes on dividend (30%) 900 <-- =$B$14*B25 Taxes on dividend (30%) 900 <-- =$B$14*G25

Total 31,100 <-- =B23+B25-B26 Total 32,300 <-- =G23+G25-G26

JOHN'S TAXI COMPANY--after dividend JOHN'S TAXI COMPANY--after bonus

When John pays himself a bonus, it comes out of cash but gets tax deductibility. Here’s

what happens to the cash balances:

Initial cash balances $5,000

After-tax cost of bonus to

company

$1,800 The company pays John a $3,000 bonus, which is

an expense for tax purposes. At the company’s

40% corporate tax rate, the after-tax cost of the

bonus is

(

)

1 40% *3,000− .

Cash on hand after bonus $3,200

This little trick (the tax deductibility of the bonus) is actually more profitable than Mary’s

not paying a dividend at all (compare John’s net of $32,300 to Mary’s net of $32,000).

However, whether a bonus is better than no bonus depends on the corporate versus the ordinary

income tax rate. In the example below the corporate rate is 30%, which is less than John’s

PFE Chapter 22, Dividend policy and firm valuation Page 11

ordinary income tax rate; he’d be better off by not paying himself a bonus (or a dividend) and

selling the company.

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

FG H I

Assets Liabilities and equity

Cash 2,900 Debt 10,000

Taxis 20,000 Equity

Stock 5,000

Accumulated retained earnings 7,900

Total assets

22,900

Total liabilities and equity

22,900

Corporate tax rate 30%

Capital gains tax 15%

Ordinary income tax rate 40%

John sells his taxi company for $40,000

Sale price 40,000

Pay back net debt 7,100 <-- =I4-G4

Net to equity 32,900 <-- =G17-G18

Book value of equity 12,900 <-- =SUM(I7:I8)

Taxable gain 20,000 <-- =G19-G20

Taxes on capital gain (15%) 3,000 <-- =$B$13*G21

Net to John from sale 29,900 <-- =G19-G22

Add back bonus 3,000

John's taxes on bonus (40%) 1,200 <-- =$G$14*G25

Total 31,700 <-- =G23+G25-G26

JOHN'S TAXI COMPANY--after bonus

What if John really needs the money? Solution 2: repurchase stock

Maybe John needs the money but can’t, for some reason pay himself a bonus. In this

case, he should—instead of paying himself a dividend—get the company to repurchase some

stock from him. Suppose that John convinces the management of the company (himself!) to buy

back $3,000 of stock. Suppose that after this repurchase of equity, John sells the company.

Finally, suppose that all of the $3,000 repurchase of stock is taxed to John a capital gain (this is