Principles of Finance with Excel (Основы финансов c Excel)

Подождите немного. Документ загружается.

PFE Chapter 22, Dividend policy and firm valuation Page 12

very unlikely—read the note which follows the spreadsheet). In this case, John would still be

better off than if he had paid himself a dividend:

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

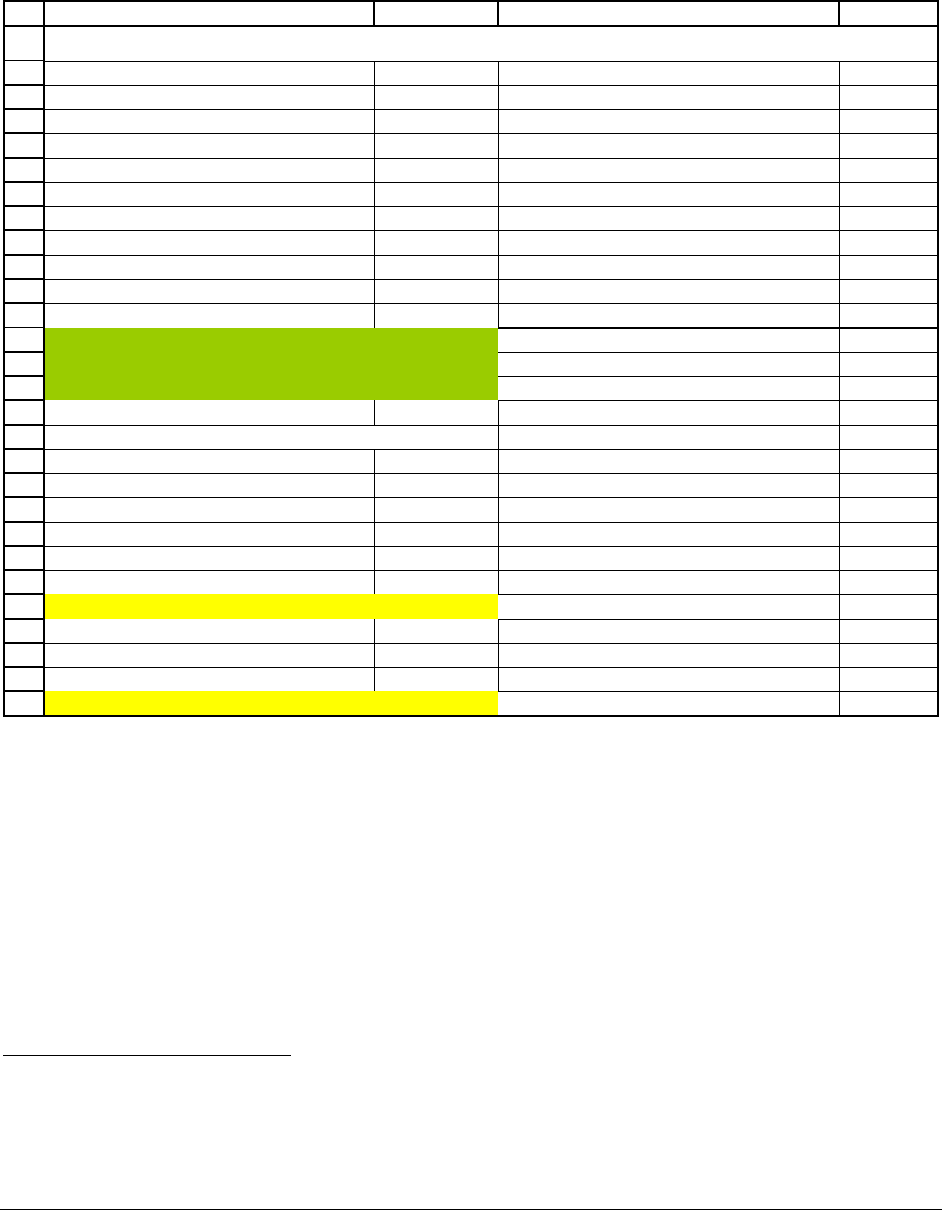

FG HI

Assets Liabilities and equit

y

Cash after repurchase 2,000 Debt 10,000

Taxis 20,000 Equity

Stock 5,000

Accumulated retained earnings 10,000

Subtract repurchase of stock -3,000

Total assets

22,000

Total liabilities and equit

y

22,000

Corporate tax rate 30%

Capital gains tax 15%

Ordinary income tax rate 40%

John sells his taxi compan

y

for $40,000

Sale price 40,000

Pay back net debt 8,000 <-- =I4-G4

Net to equity 32,000 <-- =G18-G19

Book value of equity 15,000 <-- =SUM(I7:I8)

Taxable gain 17,000 <-- =G20-G21

Taxes on capital gain (15%) 2,550 <-- =$B$14*G22

Net to John from sale 29,450 <-- =G20-G23

Add back repurchase of stock 3,000

John's taxes on repurchase (15%) 450 <-- =$G$14*G26

Total 32,000 <-- =G24+G26-G27

JOHN'S TAXI COMPANY--after repurchase

Some bad tax advice from the author: In order to minimize taxes, John should consult his

accountant before repurchasing the stock.

4

It is highly unlikely that the whole repurchase would

be taxed as a dividend. It could be structured as a payout of capital (in which case there would

be no taxes). The accountant might also be able to value John’s basis in the stock (what he

originally paid for it, plus the accumulated capital gains). Here’s an example:

4

The author of this book barely understands finance and is certainly not a tax accountant. Therefore everything in

the next few paragraphs is impressionistic and probably wrong in details (although hopefully right in spirit).

PFE Chapter 22, Dividend policy and firm valuation Page 13

31

32

33

34

35

36

37

38

39

40

41

42

43

44

45

46

47

48

49

50

51

52

53

54

55

56

57

58

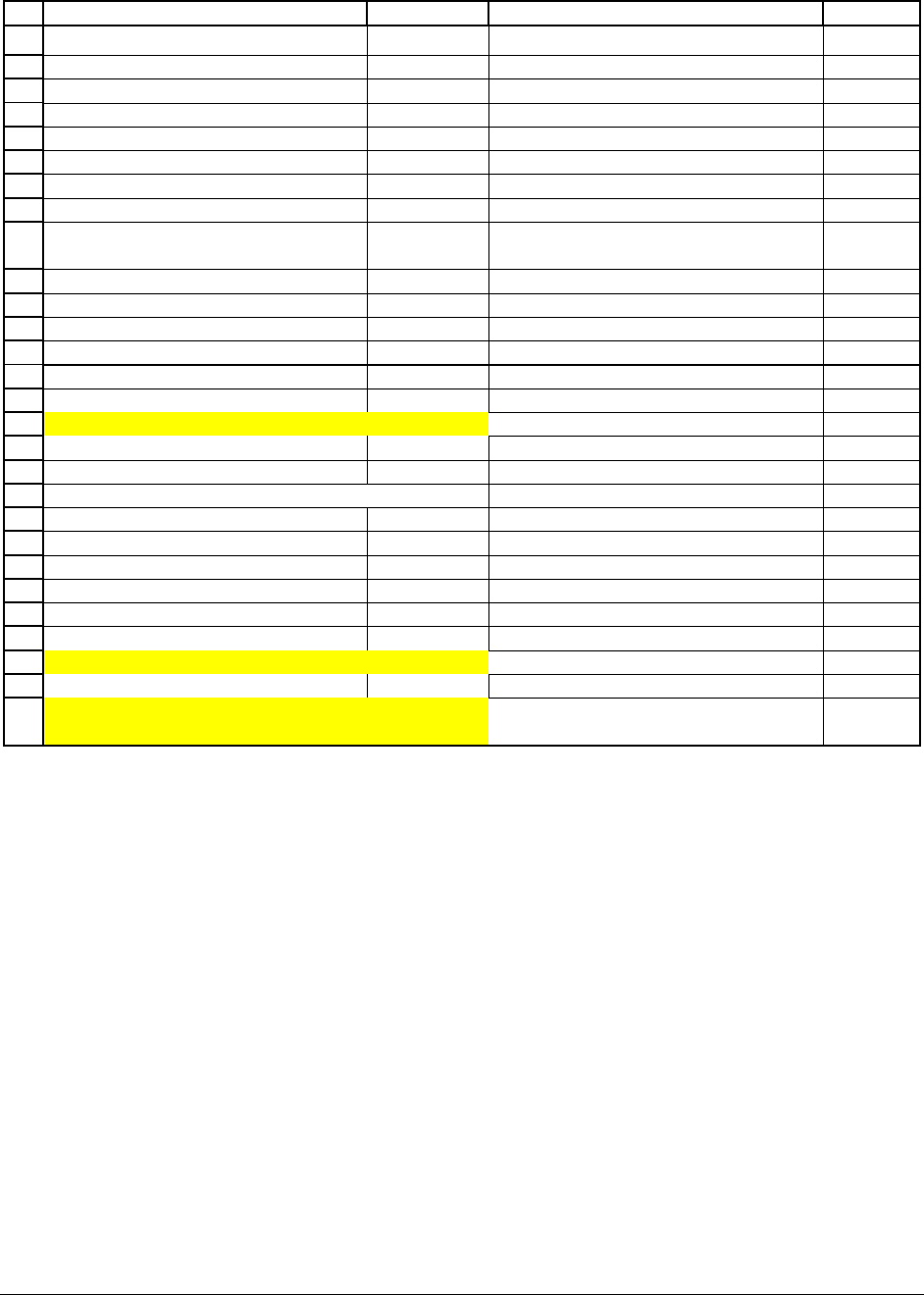

FG HI

Accountant reasoning?

Assets Liabilities and equit

y

Net debt 5,000

Enterprise value 40,000 Equity, market value 35,000

Total assets

40,000

Total liabilities and equit

y

40,000

Amount spent on repurchase 3,000

As a percent of market value

of equity

8.57% <-- =G38/I35

Book value of equity 15,000

basis = 8.57% of book equity 1,286 <-- =G39*G41

Taxable gain on repurchase 1,714 <-- =G38-G42

Taxes on gain at capital gains tax 257 <-- =G14*G44

Net from repurchase 2,743 <-- =G38-G45

John sells his taxi compan

y

for $40,000

Sale price 40,000

Pay back net debt 8,000 <-- =I34+G38

Net to equity 32,000 <-- =G50-G51

Book value of equity 13,714 <-- =G41-G42

Taxable gain 18,286 <-- =G52-G53

Taxes on capital gain (274286%) 2,743 <-- =$B$14*G54

Net to John from sale 29,257 <-- =G52-G55

Total: net from sale + net from

repurchase

32,000 <-- =G56+G46

Note: The accountant reckons as follows:

• Before the payout of cash, the company is worth $40,000, which makes the market value

of the equity $35,000.

• By paying out $3,000 in cash for stock in the company, John has effectively repurchases

8.57% of the company’s equity. Since the book value of the company’s equity is

$15,000, John has a capital gain of $1,714 (=3,000 - 8.57%*15,000) on the repurchase.

This capital gain will be taxed at 15% (=$257), so that John will net $2,743 from the

repurchase.

PFE Chapter 22, Dividend policy and firm valuation Page 14

• Now when John sells the company for $40,000, he will first have to pay off its net debt of

$8,000 (the repurchase used $3,000 of cash and raised the net debt from $5,000 to

$8,000). This leaves him with a market value of equity of $32,000 which has book value

of $13,714 (=$15,000 – 8.57%*15,000). This gain also gets taxed at the capital gains tax

rate of 15%.

• This leaves John with $32,000.

22.3. Messages

So what are we saying about dividends?

1. In a pure

22.4. Dividends (satisfaction now) versus capital gains (enjoy later)

Up to this point we’ve established that if you’re going to sell your company, dividend

taxes make it unwise to first pay yourself a dividend. But what if you’re not going to sell the

company right away? Should you leave the money in the company, for that golden day when

you’re going to sell it and benefit from the lowered capital gains taxes? Or should you pay

yourself a dividend?

It all depends, of course, on the level of trust you have in the managers of your company.

In the case of John and Mary, this is easy—they manage their own companies, and they wouldn’t

do anything to harm themselves. In this case they should leave the money in the company,

where it can earn the same amount (????) as if they paid it out.

PFE Chapter 22, Dividend policy and firm valuation Page 15

Share Repurchases Substitute for Dividends

Forbes Growth Investor, Vahan Janjigian Editor, Vol. 3, No. 9, Page 1, September 2002.

The total return on equities is composed of two components:

dividends and capital gains. Since the 1980s, however, the

proportion coming from dividends has been shrinking.

Furthermore, dividend yields (i.e., dividend per share divided by

stock price) and payout ratios (i.e., dividend per share divided by

earnings per share) have been falling steadily. Many experienced

investors take this as prima facie evidence that stocks remain

overvalued despite a tremendous two-year sell-off.

Value investors in particular believe that steadily rising cash

dividends are an indication of financial health. These investors

often shun stocks that lack a long history of dividend payments.

But others, such as growth investors, believe dividends are not

very meaningful.

A recent article in the Journal of Finance, a leading scholarly

publication, provides evidence that the demise of the cash

dividend is just an illusion. The authors, Gustavo Grullon and

Roni Michaely, argue that focusing only on dividends ignores an

increasingly important form of cash payout to stockholders: share

repurchases. Cash dividends have been increasing at an

annually compounded rate of only 6.3% since 1980. Yet cash

spent on share repurchases has been rising at a much more

rapid clip of 18.4% compounded annually. Furthermore, cash

spent on share repurchases now exceeds that spent on

dividends. And total cash paid out (i.e., dividends plus

repurchases) as a percentage of earnings has actually been

rising during the period studied.

Our tax code explains much of this behavior. When corporations

pay dividends, investors are forced to pay taxes. In fact,

dividends are taxed at the ordinary rate. But when corporations

initiate share repurchases, investors can avoid taxes altogether

by choosing not to sell. Yet if they do sell, they are taxed at the

capital gains tax rate, which is much lower than the ordinary tax

rate.

This was the case thirty years ago as well. So why weren’t share

repurchases as popular then? Grullon and Michaely argue that

share repurchases didn’t really start growing in popularity until a

1982 regulatory reform, which made it less likely that

repurchasing firms would be accused by the SEC of trying to

manipulate their stock prices.

PFE Chapter 22, Dividend policy and firm valuation Page 16

There are a number of lessons to be drawn from this study. First,

those who argue that stocks remain overvalued simply because

dividend yields or dividend payout ratios are historically low are

being shortsighted. They should instead focus on total cash

payouts. Second, there should be no doubt that, good or bad,

regulatory reforms affect firm behavior. Well-managed firms will

do what is best for shareholders. As long as cash dividends are

unfavorably taxed, investors will prefer capital gains. And as long

as regulators allow it, good corporate boards will deliver what

shareholders want.

Which brings us to a very important point. Dividends are paid from

after-tax dollars. Taxing investors again for receiving those

dividends imposes a very heavy burden. Regulators should

eliminate this double taxation. Dividends should either be treated

as a tax-deductible expense for corporations, or tax-exempt

income for individuals.

Source:

https://www.forbesnewsletters.com/fagin/index.jhtml?page=sample

PFE Chapter 22, Dividend policy and firm valuation Page 17

Open Book

Why Dividends? There Doesn't Seem to Be a Good Answer

By Don Luskin

Special to TheStreet.com

6/4/01 4:26 PM ET

URL: http://www.thestreet.com/comment/openbook/1449809.html

Remember Bill Cosby's act in the 1960s? As a child he used to ask a profound question that

adults were too grown up to ask: "Why is there air?"

With a child's innocence, let us ask, "Why are there dividends?"

Is this a question we should be too grown up to ask? An awful lot of investment gurus think that

dividends are awfully important. For example, I noticed over the weekend that Jim Jubak,

senior editor at MSN Money Central, is saying, "What this stock market needs is a really juicy

5% yield. Instead, the dividend yield on stocks that make up the Standard & Poor's 500 is

down to a paltry 1.23%. Thunderation!"

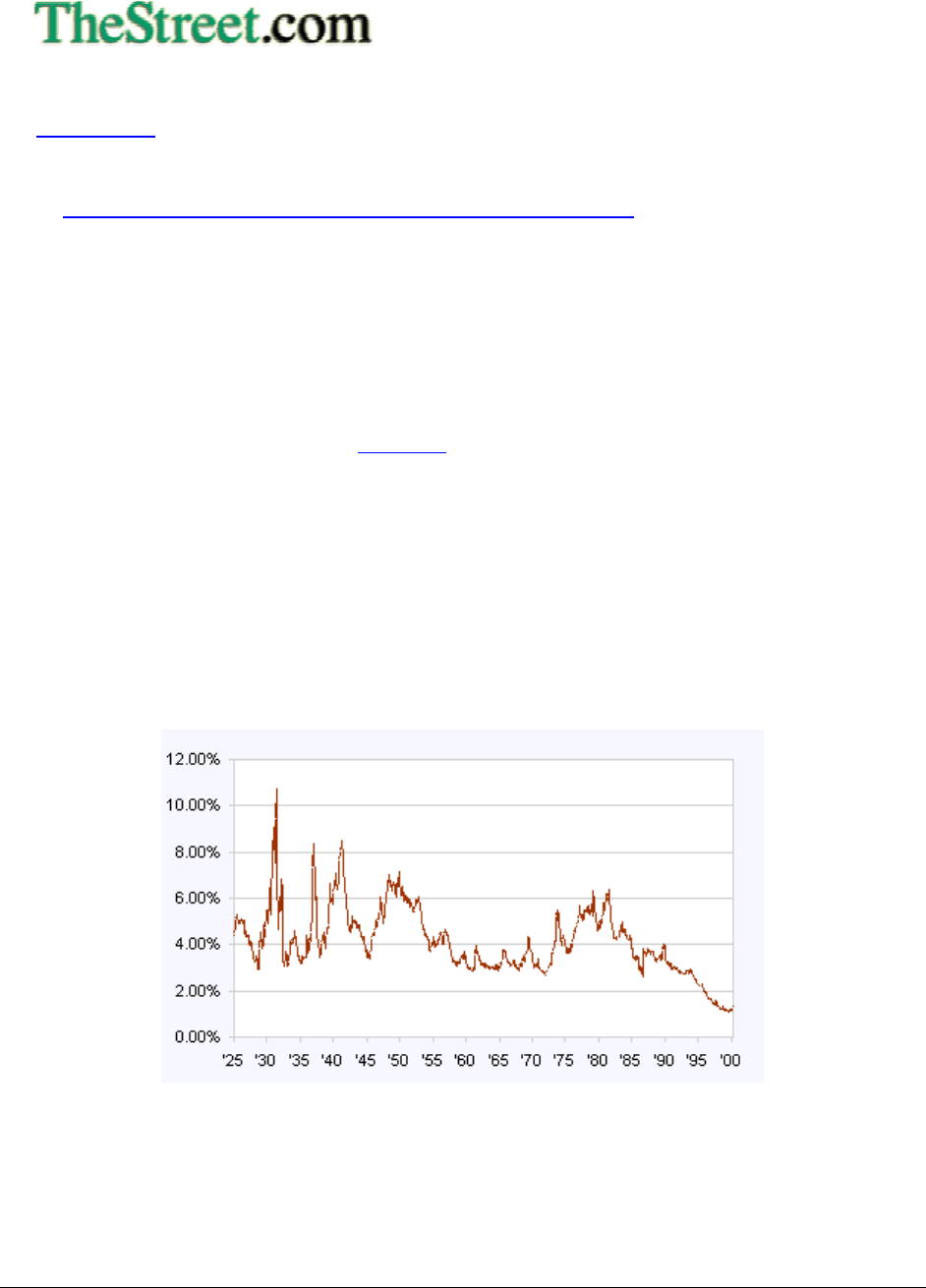

Jubak is right, in the sense that dividend yields are near historic lows -- even after this year's stiff

correction. Take a look at the chart below. Dividend yields today are less than half of what they

were at the top of the market in 1929.

Annual Dividend Yield: S&P 500

Source: Global Financial Data

Jubak, and many other observers, would argue that today's low dividend yields are symptomatic

of our overvalued markets. Well, maybe markets are overvalued. But I believe dividend yields

are so low for another reason: Investors are beginning to ask our childish question: "Why are

there dividends?" And they're not finding good answers. So dividends are becoming less and less

important.

PFE Chapter 22, Dividend policy and firm valuation Page 18

Just think about how silly it all really is. Why would a shareholder want a company to send him

his own money back? That's a confession by the investor that he would really rather not invest in

that company to begin with. And it's a confession by the company that its investors can invest

their money more profitably than the company can.

More and more investors and companies are seeing it this way. But there was a time when

everyone felt like Jubak. In those days, dividend yields on stocks had to be high because

investors saw high dividends as compensating for the risk of equity ownership. When dividend

yields were low, investors reasoned they'd be better off investing in the same company's bonds.

After all, why not earn a higher return with less risk?

In fact, for most of the last century, the conventional wisdom was that whenever the dividend

yield on the stock market fell below the coupon yield of the bond market, it was time to sell

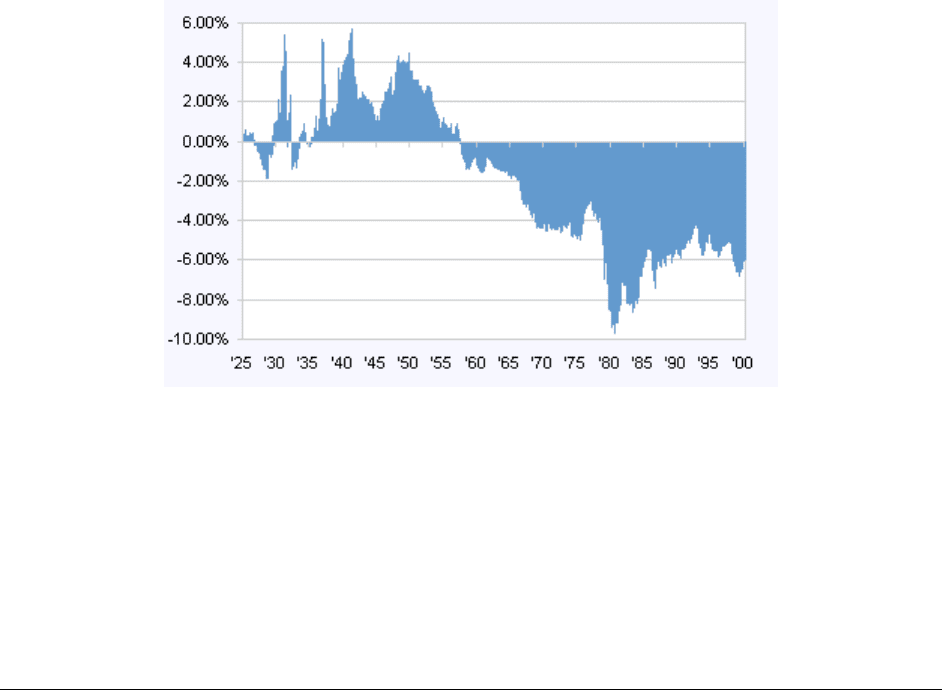

stocks. Take a look at the chart below, which shows the difference between the dividend yield on

the S&P 500 and the coupon yield on Moody's Aaa Corporate Bonds Index. When stocks

yielded less than bonds briefly in 1929, that was one of the greatest stock market sell signals in

history.

Yields: Moody's Aaa Corporate Bonds Minus S&P

500

Source: Economagic and Global Financial Data

But then in August 1958, something very strange happened. The dividend yield on the S&P 500

fell below the coupon yield on Moody's Aaa bonds -- and it never came back. For some reason,

at that moment, the world decided that dividends weren't so important after all. And dividends

have declined in importance ever since.

What happened in 1958 to change investors' preferences so profoundly? Perhaps it happened

then because the late 1950s saw the dawn of the age of inflation in America. Bond yields had to

PFE Chapter 22, Dividend policy and firm valuation Page 19

rise in relation to equity yields because bonds are completely unprotected against the ravages of

inflation.

Or perhaps it was because the 1950s was the dawn of the age of the individual investor, in which

pioneers like Merrill Lynch brought Wall Street to Main Street. When individuals had poor

access to markets, they needed dividends as a low-cost way of getting their money back. As their

access improved, they needed dividends less because they could simply pick up the phone and

sell shares if they needed cash.

Or perhaps it was because the 1950s was the dawn of the age of financial economics. Academics

like Harry Markowitz -- who eventually won the Nobel Prize for this work -- were beginning to

codify the realities of investment risk and return. And one of the first lessons was that there was

nothing special about dividends as a component of total equity returns.

Twenty-five years later, in the 1980s, another nail was driven into the coffin of dividends. That's

when companies started to learn that paying dividends wasn't the most efficient way to return

money to shareholders -- buying back their own stock in the open market was smarter.

Repurchases allow investors to decide when and how much to cash in. And investors get to

decide whether to bear a taxable event -- and if they do, to pay the favorable capital gains tax

rate, not the higher ordinary rate they would have paid on dividend income. And investors who

don't sell their shares back to the company benefit from reduced earnings dilution.

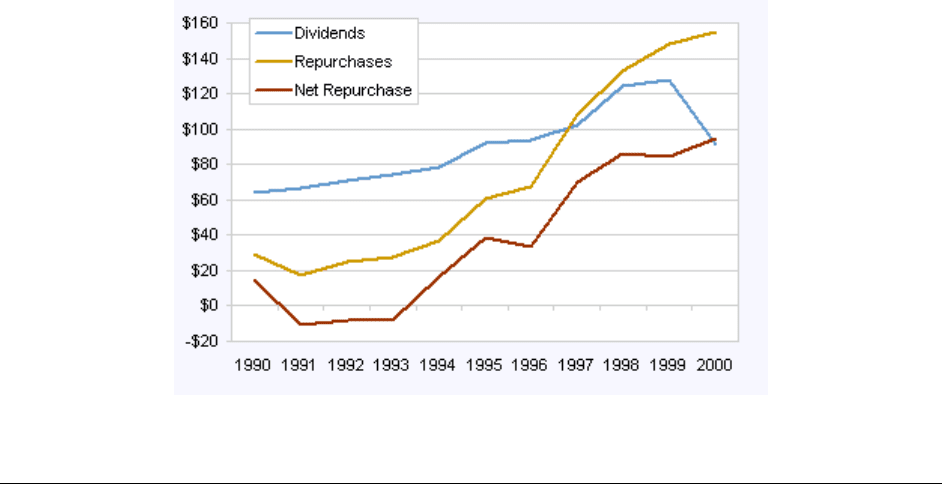

This logic has been so powerful that, starting in 1997, the total value of share repurchases by

S&P 500 companies exceeded the total value of dividends paid. Take a look at the chart below:

The spread between repurchases and dividends has gotten wider every year since 1997. And last

year, even the value of net repurchases (repurchases minus the value of new stock issued)

exceeded dividend payouts for the first time.

Dividends and Repurchases (in Billions): S&P 500

Source: Morgan Stanley

PFE Chapter 22, Dividend policy and firm valuation Page 20

This means that to understand the true yield of the equity market -- which has to include both

dividends and repurchases -- you would have to at least double the dividend yield quoted by

commentators like Jubak.

But while this perhaps blunts Jubak's point about overvaluation, it tends to confirm his broader

point that payouts to stock investors are important. Indeed, the mystique of dividend yields is far

from dead. Many companies that feel they have lots of good things to do with their money other

than pay it out to their investors still pay dividends or engage in buybacks. How do they do it?

Well, it's simple -- and utterly crazy.

There are many companies that pay dividends that have to borrow money in the debt market in

order to do it. If the purpose of a dividend is to return surplus cash to shareholders, then why

would any company that had debt pay a dividend? A company in debt has no surplus cash -- by

definition. But hundreds and hundreds of companies both borrow and pay dividends at the same

time.

For example, in the first quarter Dow Chemical (DOW:NYSE) spent $158 million in net interest

expenses (accrued interest expense less capitalized interest and debt income) servicing its $10.5

billion in debt. The same company spent $260 million paying dividends of 29 cents a share.

And it gets even nuttier when we start looking at buybacks.

Morgan Stanley Dean Witter's U.S. Equity Strategist Steve Galbraith told me, "Want to know

something almost as screwy as borrowing in the bond market to pay dividends? Our wonderful

tax and options accounting system has created the following situation -- of the top one-dozen

issuers and the top one-dozen buyers back of stock in the S&P, five companies are on both lists!

How inefficient and stupid is that?"

So what is there about dividends -- directly, or in the form of repurchases -- that is still so

attractive to investors? "Why are there dividends?"

Dividends can't exist simply so that investors can earn income from their investments. Anyone

who needs cash from his investment portfolio can have it with a mouse click, just by selling

some of his shares. And doing it that way, the investor controls the amount and the timing -- and

from which of his stocks he wants the income.

And dividends can't exist as a discipline on company management, forcing them to turn a

consistent profit. If they want to pay a dividend, they can simply borrow to do it. And if they

want to repurchase shares, they can just issue more later.

Dividends remain one of the great mysteries, like "Why is there air?"

By the way, if you're too young to remember Cos in the 1960s, the answer to the question is: "To

blow up basketballs."

Don Luskin is president and CEO of MetaMarkets.com and a portfolio manager of OpenFund, an aggressive growth

fund investing in the New Economy. OpenFund strives to be fully invested, expecting to be at least 90% invested

under most market conditions. At time of publication, OpenFund was long futures contracts on the S&P 500 and

PFE Chapter 22, Dividend policy and firm valuation Page 21

Microsoft, although holdings can change at any time. Luskin appreciates your feedback and invites you to send it to

Don Luskin.