Principles of Finance with Excel (Основы финансов c Excel)

Подождите немного. Документ загружается.

PFE Chapter 21, Capital structure, empirical evidence page 18

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

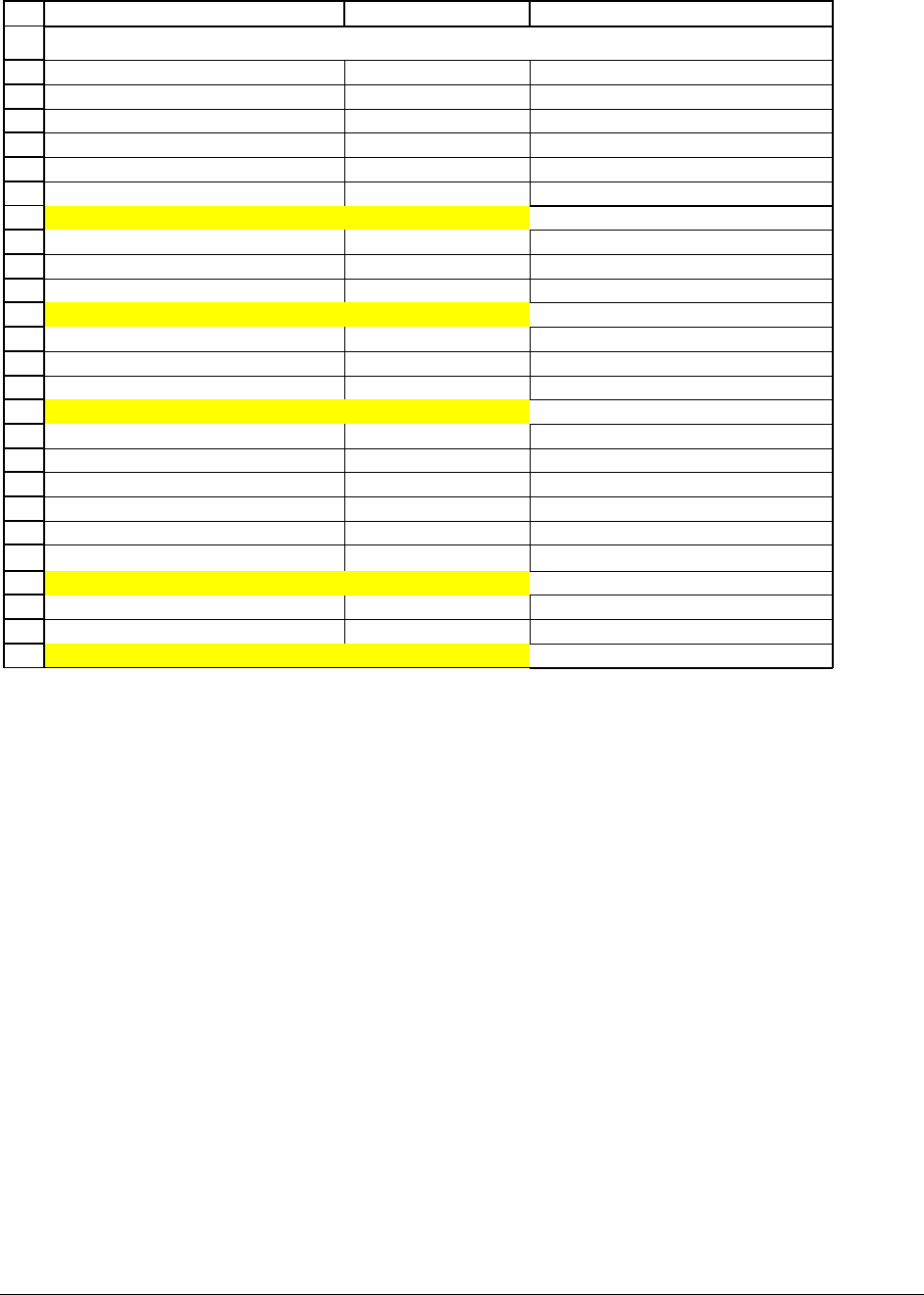

ABC

2000 1999

Short-term debt 277,000,000 1,602,000,000

Long-term debt 169,503,000,000 158,150,000,000

Total debt 169,780,000,000 159,752,000,000

Interest expense 10,902,000,000

Implied interest rate 6.62% <-- =B7/AVERAGE(B5:C5)

Risk-free rate 4.80%

Market risk premium 5%

Debt beta 0.3633 <-- =(B8-B10)/B11

Debt/Equity, book values 12.45

Price/Book 2.45

Debt/Equity, market values 5.08 <-- =B14/B15

Debt/Assets, market values 0.8356 <-- =B16/(B16+1)

Equity/Assets, market values 0.1644 <-- =1-B18

Income Before Tax 8,234,000,000

Income Tax Expense 2,705,000,000

Tax rate 32.85% <-- =B22/B21

Equity beta 1.07

Asset beta 0.3798 <-- =B25*B19+B12*B18*(1-B23)

FORD MOTOR COMPANY

PFE Chapter 21, Capital structure, empirical evidence page 19

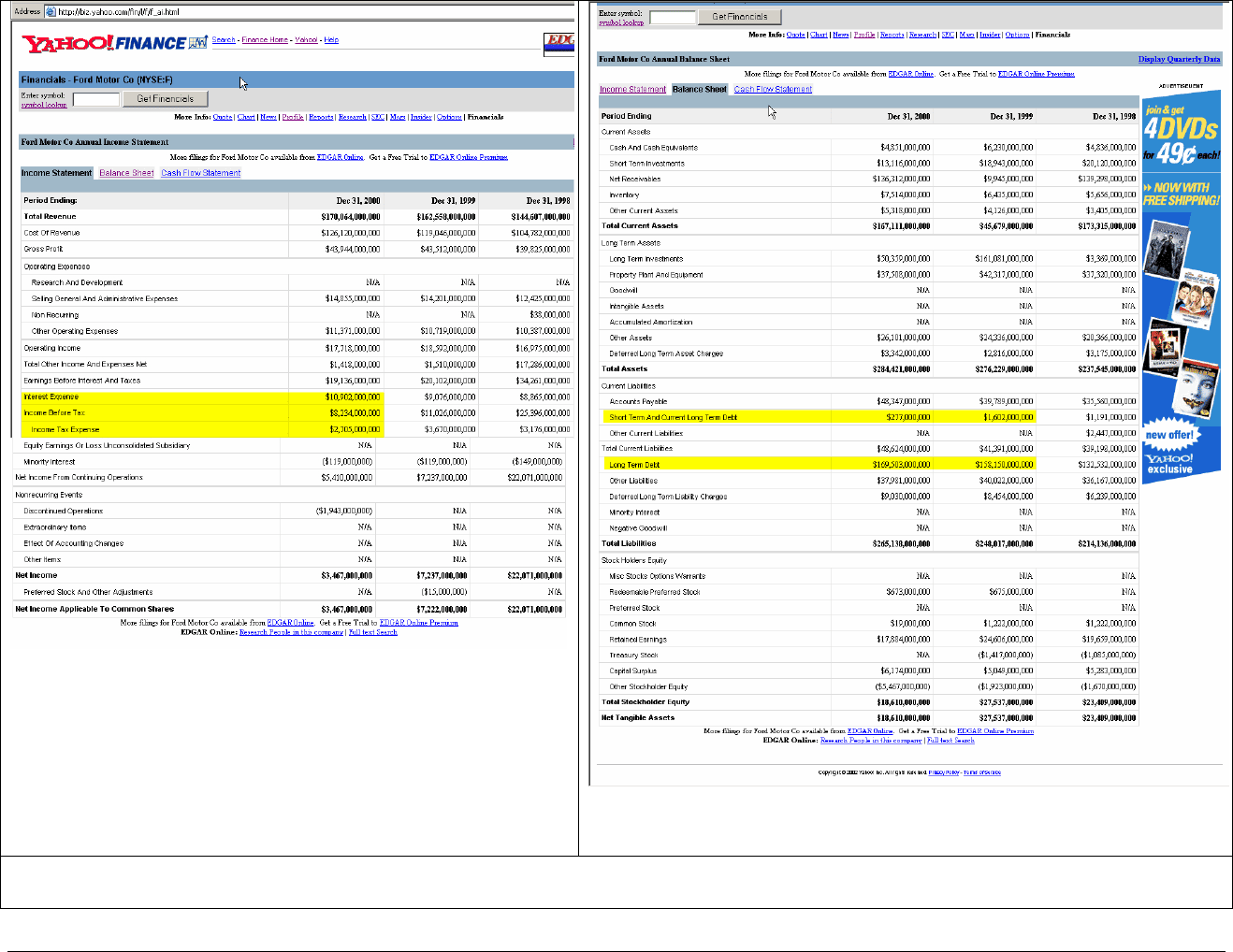

Ford’s income statements, as displayed on Yahoo

Ford’s balance sheets, as displayed on Yahoo

Figure 21.1: The Ford computations in section 21.?? are based on the Yahoo exhibits above for Ford’s balance sheets and income

statements.

PFE Chapter 21, Capital structure, empirical evidence page 20

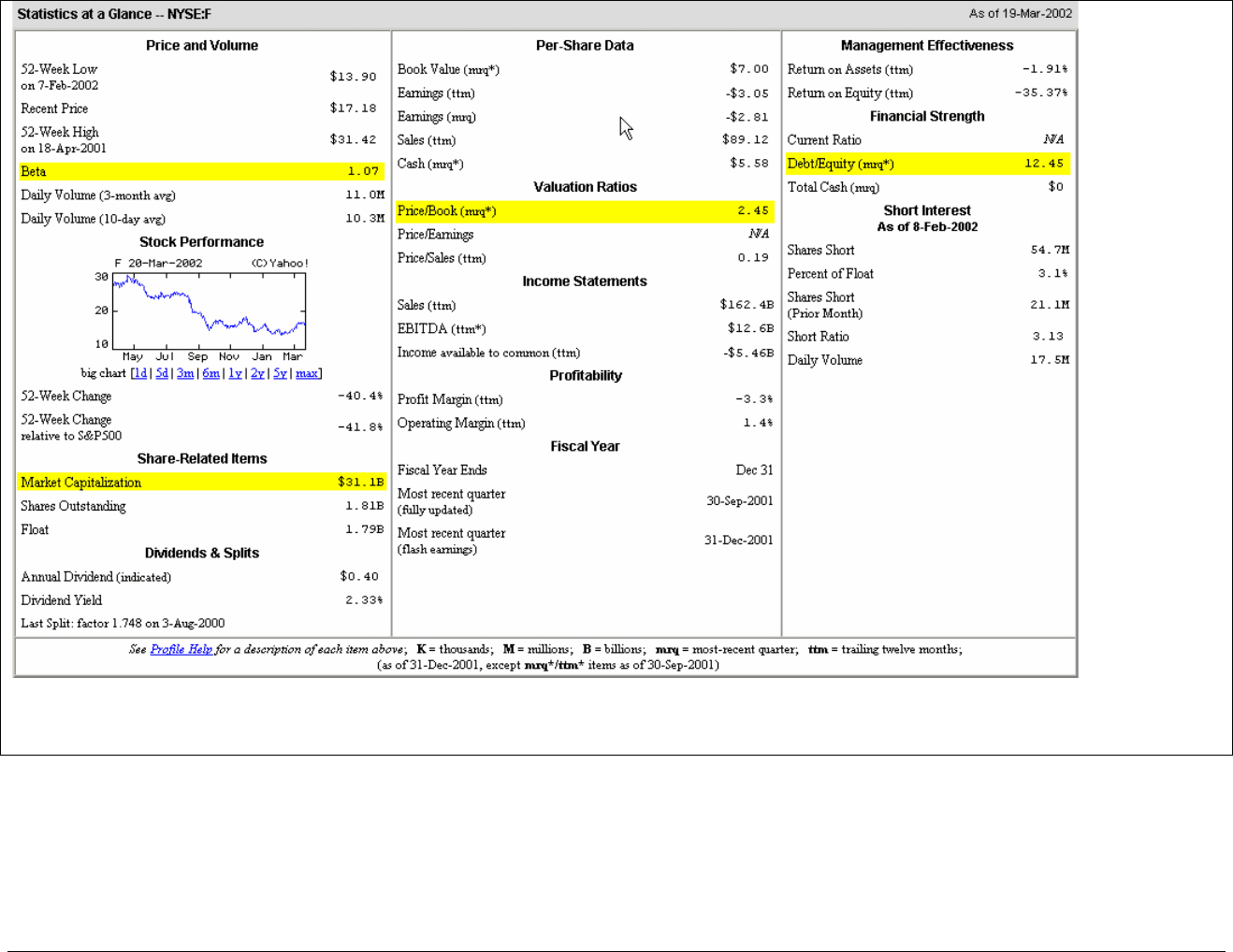

Figure 21.2: Financial profile of Ford, from Yahoo

PFE Chapter 21, Capital structure, empirical evidence page 21

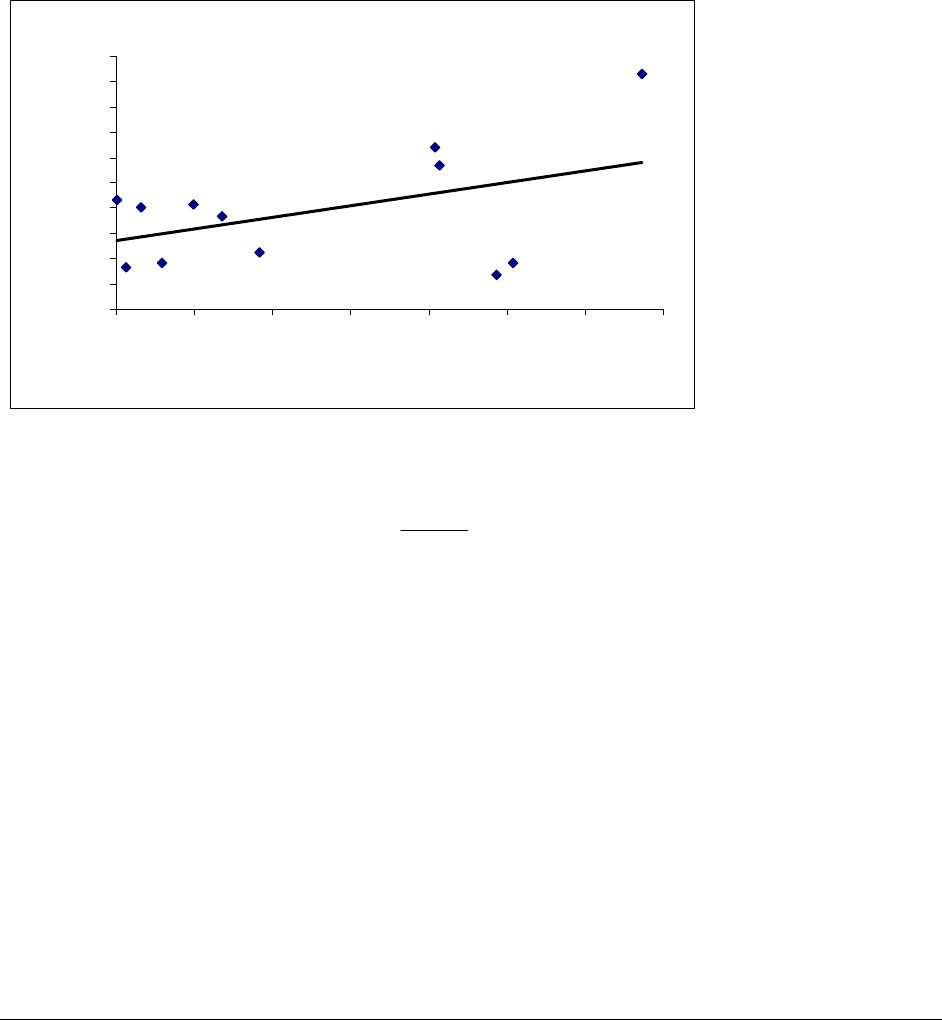

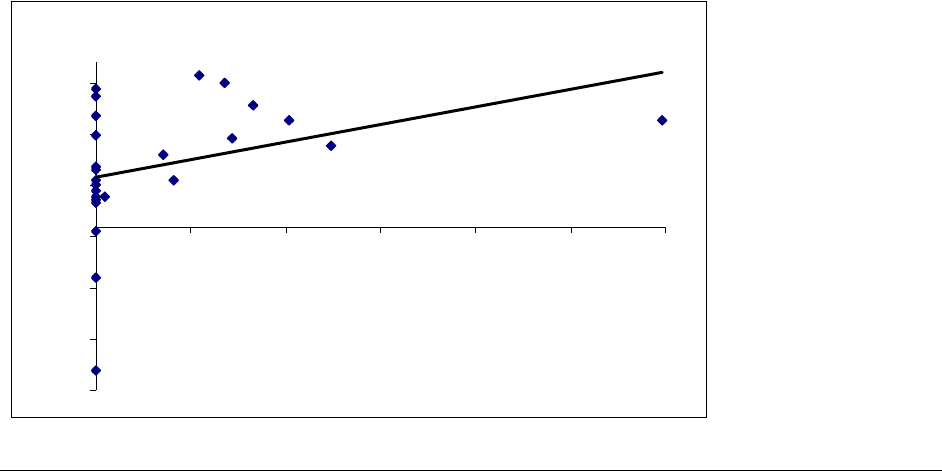

21.4. Repeating the asset

β

calculation for an industry

In the previous section we showed how to calculate the asset

β

Asset

for Ford. Suppose we

repeat this calculation for all American manufacturers of autos and trucks. The results are

displayed on a separate page. Here’s the graph which relates the firms’ debt/equity ratio and

their asset betas:

U.S. Auto-Truck Industry:

Asset Beta versus Debt/Equity

y = 0.0912x + 0.5444

R

2

= 0.2013

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

1.80

2.00

0.0 1.0 2.0 3.0 4.0 5.0 6.0 7.0

Debt/equity

Asset beta

The graph shows a slight upwards trend:

2

0.5444 0.0912* , 20.13%

Debt

Assetbeta for autos R

Equity

=+ =

Using this equation, we would conclude that the

β

for an unlevered auto firm is 0.54, and that

increased leverage adds to this

β

. A more careful analysis (not repeated here, but on the disk

with the book) reveals that the positive slope is not statistically significant. Meaning: At least

for this small sample, we can conclude that the asset

β

is not affected by the capital structure.

This is Miller’s position:

PFE Chapter 21, Capital structure, empirical evidence page 22

• If the Modigliani-Miller results are representative, then the WACC of will decrease when

the amount of debt increases. The effect on the

β

Assets

will be that

β

Assets

should decrease

as leverage increases.

•

If the Miller results are representative, then the WACC will be unaffected by the amount

of debt. The effect on the

β

Assets

will be that

β

Assets

should stay constant as leverage

increases.

In the event,

β

Assets

seems to increase slightly with leverage for auto firms. The effect is

not large and is statistically insignificant; if it were significant, it would be consistent with a tax

disadvantage to debt. So—at least for the auto industry, Miller’s theory seems to do better at

explaining things that the MM theory.

One more industry

The experiment we’ve performed on the auto industry in the first part of this section is

just that—a small experiment to see if we can find any effects of leverage on asset betas. To

show that this experiment is not a fluke, we repeat it for the grocery industry:

Grocery Industry:

Asset Beta versus Debt/Equity

y = 0.1714x + 0.4728

R

2

= 0.128

-1.6

-1.1

-0.6

-0.1

0.4

0.9

1.4

0.0 1.0 2.0 3.0 4.0 5.0 6.0

Debt/equity

Asset beta

PFE Chapter 21, Capital structure, empirical evidence page 23

As for the auto industry, there seems to be a slight upward trend in the asset beta as a

function of the debt/equity ratio of grocery firms. And, as for the auto industry, this upward

slope is not, when we subject it to more statistical scrutiny, significant. We conclude (again) that

there is little evidence that leverage affects the asset beta and the WACC.

Several further notes about the grocery industry:

•

The average equity

β

for grocery firms was 0.366 (with a standard deviation of 0.568—

meaning that the equity beta was very widely dispersed).

•

The average asset

β

for these firms was 0.594 (with a

σ

= 0.638).

•

In a period (1999-2000) where the risk-free rate of interest was around 5%, these firms

paid average interest rates of 16.75% (with

σ

= 4.39%). Thus, while shareholders

perceived these firms as having fairly low risk, lenders perceived them as having very

high risks—the average debt

β

D

= 2.39 (with

σ

= 0.88 ).

PFE Chapter 21, Capital structure, empirical evidence page 24

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

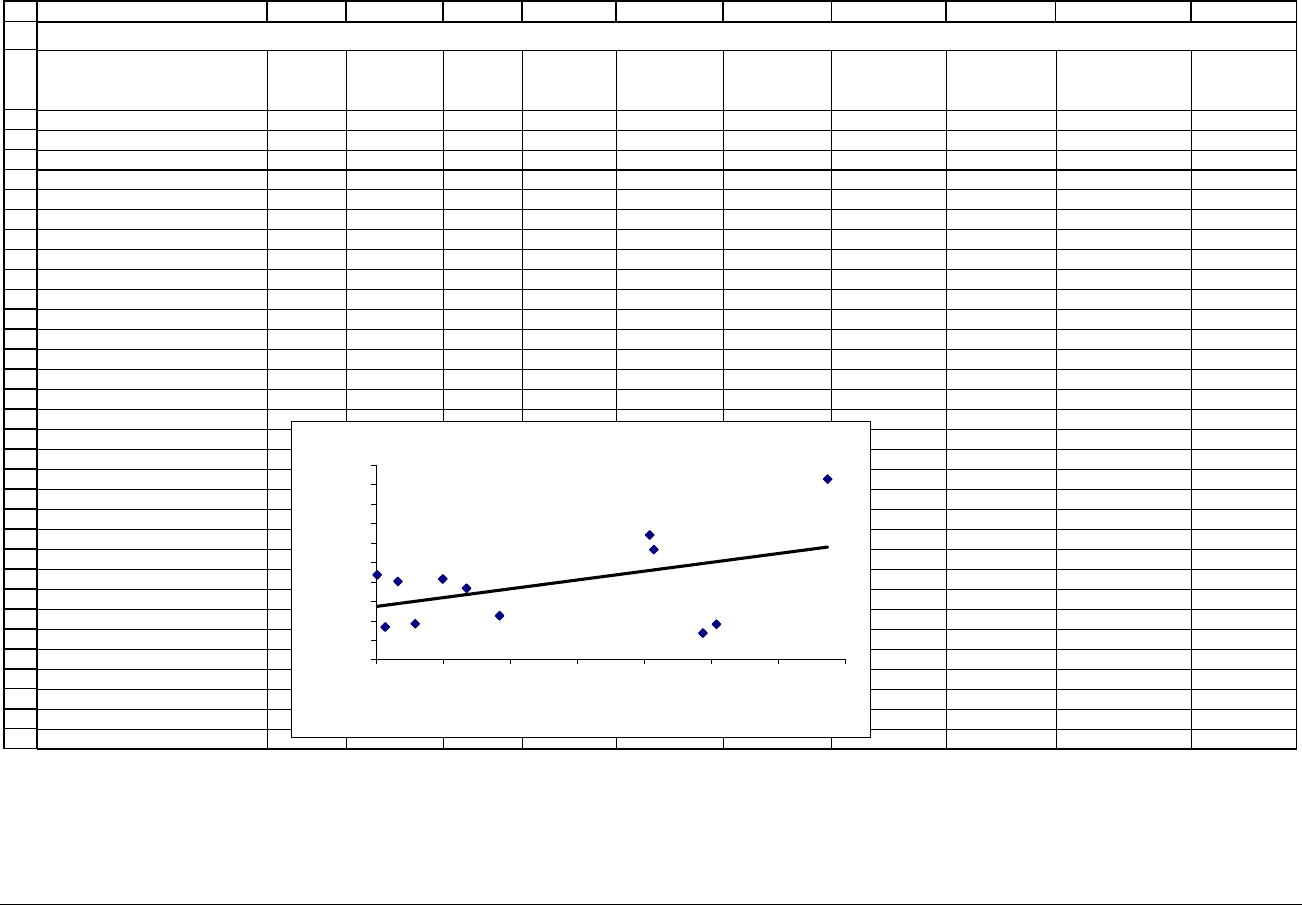

ABCDEFGHIJK

Equity

beta

Debt

beta

Tax rate

Market

value

of equity

Debt/Equity

book values

Price/Book

Debt/Equity

market values

Debt/Assets

market

values

Equity/Assets

market values

Asset beta

Collins Industries (COLL) 0.150 1.134 35.31% 28.1 0.62 1.05 0.59 0.3713 0.6287 0.3667

Featherlite (FTHR) 0.800 2.162 6.87% 7.51 2.56 0.38 6.74 0.8707 0.1293 1.8569

Ford (F) 1.070 0.363 37.98% 31.1 12.45 2.45 5.08 0.8356 0.1644 0.3642

General Motors (GM) 1.120 0.147 33.40% 34 8.44 1.73 4.88 0.8299 0.1701 0.2715

Miller Industries (MLR) 1.560 1.811 33.03% 24.9 0.98 0.24 4.08 0.8033 0.1967 1.2809

Navistar International (NAV) 1.490 0.233 29.02% 2.65 2.47 2.47 1.00 0.5000 0.5000 0.8275

Oshkosh Truck (OTRKB) 0.930 0.674 37.25% 987.6 0.94 2.82 0.33 0.2500 0.7500 0.8032

PACCAR (PCAR) 0.880 0.627 33.57% 5.82 0.06 2.58 0.02 0.0227 0.9773 0.8695

Rush Enterprises (RUSH) 0.520 2.133 39.99% 49.4 2.53 0.61 4.15 0.8057 0.1943 1.1325

Spartan Motors (SPAR) 0.360 0.199 30.37% 86.6 0.36 2.53 0.14 0.1246 0.8754 0.3324

Supreme Industries (STS) 0.390 0.793 39.00% 65.9 2.27 1.23 1.85 0.6486 0.3514 0.4509

Wabash National (WNC) 0.910 0.984 39.04% 240.5 1.22 0.9 1.36 0.5755 0.4245 0.7316

Average 0.848 0.938 32.90% 0.774

Standard deviation 0.437 0.733 0.089 0.473

ASSET BETAS FOR AMERICAN TRUCK AND AUTO COMPANIES

U.S. Auto-Truck Industry:

Asset Beta versus Debt/Equity

y = 0.0912x + 0.5444

R

2

= 0.2013

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

1.80

2.00

0.0 1.0 2.0 3.0 4.0 5.0 6.0 7.0

Debt/equity

Asset beta

PFE Chapter 21, Capital structure, empirical evidence page 25

21.5. Academic evidence

In the previous section we’ve looked at a specific example—the U.S. auto-truck

industry—to try to gauge whether capital structure affects the asset

β

Asset

of these firms. Our

conclusion is that, for this industry, they don’t: The asset

β

Asset

, and hence the WACC, is not

affected by the capital structure.

Recent academic research seems to come to the same conclusion.

3

•

When Eugene Fama and Kenneth French regress firm value on leverage, they conclude

that leverage doesn’t matter.

4

[graph?]

•

John Graham, in a survey published in 2001, concludes that “at the margin the tax costs

and tax benefits [of leverage] might be of similar magnitude.”

5

To show you how

confusing this is, Graham concludes that—using another method—the tax benefit of debt

is approximately 9% for the years 1995-1999.

6

This probably represents the costs of

bankruptcy.

•

Ivo Welch, in a paper written in 2002, finds no evidence whatsoever that firms look for

an optimal structure.

7

He finds that firms tend to make few changes in their debt, so that

the actual capital structure (i.e., the ratio of debt to the market value of equity) is largely

3

Be warned that this is still controversial. Every finance professor seems to have an opinion on this matter! If you

want a good grade in the course, disagree with the book and not with your professor.

4

“Taxes, Financing Decisions, and Firm Value,” Journal of Finance 1998, pp. 819-843.

5

“Taxes and Corporate Finance: A Review,” working paper. The quote is from page 25.

6

Ibid, page 26-27.

7

Ivo Welch, “Columbus’ Egg: The Real Determinants of Capital Structure,” Yale School of Management working

paper, 2002.

PFE Chapter 21, Capital structure, empirical evidence page 26

driven by the market prices of the firm’s shares. There is little evidence, according to

Welch, of any optimizing in the debt decision.

Summing up

The theory of capital structure suggests that the capital structure decision is largely driven

by the differential taxation of debt and equity. The empirics of capital structure suggest that it

doesn’t matter very much in determining the value of the firm.

For practical purposes:

•

You can assume that the weighted average cost of capital (WACC) of a firm is invariant

to the firm’s capital structure.

•

This means that the WACC of a firm can be measured by taking the average WACC of

the firm’s industry. It also means that the asset

β

of a firm’s industry is representative of

the industry’s overall risks and is not a function of the capital structure of the industry.

•

The best way to value a firm is to use the WACC to discount the firm’s anticipated future

free cash flows (recall that these are operating cash flows and do not include interest and

other financing). We have illustrated this approach in a number of chapters of this book:

Chapter 5, 7, 15.

PFE Chapter 22, Dividend policy and firm valuation Page 1

CHAPTER 22: DIVIDEND POLICY

*

This version: February 8, 2004

This chapter is incomplete!

Chapter contents

Overview..............................................................................................................................2

22.1. Dividends ...................................................................................................................3

22.2. Taxes!.........................................................................................................................7

22.3. Messages..................................................................................................................14

22.4. Dividends (satisfaction now) versus capital gains (enjoy later) ..............................14

*

This is a preliminary draft of a chapter of Principles of Finance with Excel. © 2001 – 2004 Simon Benninga

(benninga@wharton.upenn.edu

).